These Canadians are in a “highly vulnerable” position.

By Daniel Wong, Better Dwelling:

Canadian real estate debt hit a new high, and the news gets worse as they explain it further. The Bank of Canada (BoC) updated household debt numbers for March. In a speech this week, BoC’s Governor Stephen Poloz also gave further insights on the numbers. The record debt levels are concentrated in a smaller segment of Canadians. These Canadians are now in a “highly vulnerable” position, and they’re f**ked if they don’t start preparing for higher rates now.

8% of Canadians Have Mortgage Debt Over 3.5x What They Make

In a speech this week, the BoC gave us further insights on the Canadian debt problem, and it’s worse than we thought. It turns out 8% of households have mortgage debt that’s more than 350% of their gross income.

This segment of borrower represents “a bit more than 20 percent of total household debt.” BoC Governor Poloz stressed that these households need to understand how “personally vulnerable” they are, as rates rise.

Rising rates are already putting the pinch on households, and it should get worse. The BoC reiterated the “neutral rate,” which is the rate where policy is no longer expansionary, is between 2.5% and 3.5%. Assuming no “shock” to the economy, rates will get there. Currently we’re at 1.25%, so that would mean rates will double over the next few years. You know, if we don’t face a major recession. Then you’re in the clear on rates, but a whole other bag of issues will crop up. On that note, onto those climbing debt numbers.

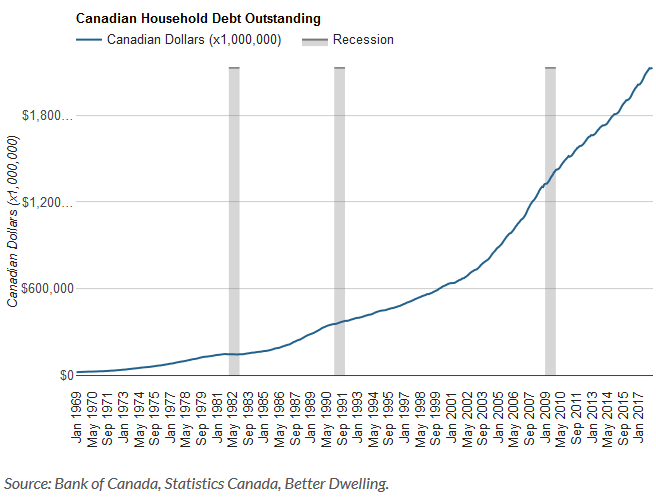

Canadian Households Owe More Than $2.1 Trillion Dollars

Total household debt hit a new record, but the annual pace of growth continued to decline. The total balance at the end of March stood at a whopping $2.129 trillion, up $3.4 billion from the month before. The annual rate of growth is now 5.25%. While it’s a new all-time high, it’s also the slowest pace of growth since November 2015. Let’s break this down into the two major components – mortgages, and consumer credit.

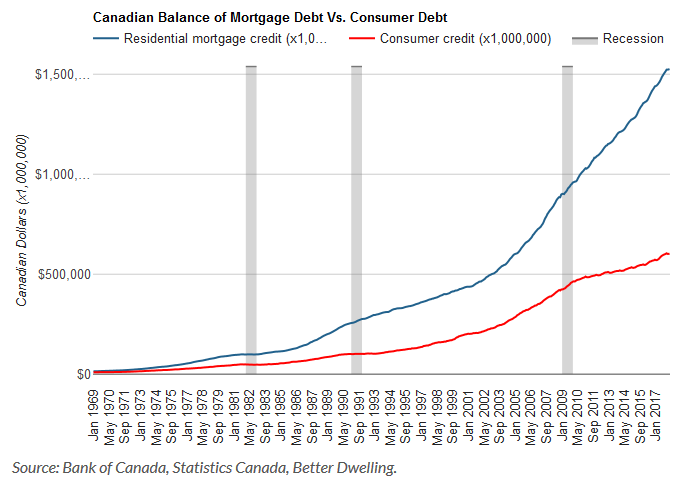

Canadians Owe Over $1.52 trillion Worth of Mortgage Debt

Outstanding residential mortgage credit is also at a new high. The total outstanding balance of residential mortgages hit $1.52 trillion, up $1.88 billion from the month before. That brings the annual rate of growth to 5.27%, the lowest since March 2015. The slowing rate of growth is being attributed to B-20 stress tests, and isn’t the good news people think it is.

Canadian Owe More Than $603 Billion In Consumer Credit

It’s not just mortgage debt those crazy Canucks are diving into, consumer credit is also at an all-time high. The total balance of outstanding consumer credit stood at $603 billion, up $1.54 billion from the month before. The annual rate of growth is now 5.2%, the lowest its been since July 2017. Consumer debt growth is the closest to beating mortgage growth, since 2010. That’s… a special moment for all of us.

High levels of household debt are a concern, that gets even worse when you realize how concentrated it is. It’s also created a debt trap for the BoC. Continued economic growth will send rates higher, putting these households at further risk. Lowered growth will send debt levels higher, putting even more households at risk. By Daniel Wong, Better Dwelling

Canadians’ tapering their personal debts against their homes? That would be ridiculous! Read… Congrats! Canadians Just Set a New Record for Borrowing Against their Homes

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Warren Buffet got their back, right Warren?

He’s probably talking to Goldman right now trying to replicate what John Paulson did :) Together, they’ll take these guys to the cleaner.

The Oracle of Omaha only bailed out the largest Alternative Mortgage Lender in CANADA. Our Chartered Banks are not involved in the Alt-M-Loans whatsoever. If our largest Alt-M-Loans lender defaults on the Oracle of Omaha it will be on Berkshire H. and their dime.

If our RE implodes it will leave WB holding a very large bag of odorous excrement that cannot be sold due to debt saturation in all markets.

Personally, I think Buffett will take a loss when it folds, and it will fold eventually.

MOU

You underestimate the Omaha Man’s powers. He’ll get uncle Sam to intervene.

The other shoe to drop is that all the people who DID make money from real estate in the boom probably don’t have much of that wealth left. In line with human instinct they’ll have rewarded themselves with pricey, depreciating consumables imagining themselves on a new plane of life, free from having to work ever again. Now the 12%pa capital appreciation is over, they’re left only with the costs and repayments. Here in Australia I hear repo men for private schools is big business. It’s a pity we probably can’t see any statistics on that. It’s a big “tell”.

I’d love to know what “Here in Australia I hear repo men for private schools is big business” means.

Private schools are going bust? or is it the kids being collected by the repo man when their parents can’t pay the fees?

My Catalan cousins were sent to an up-market Church school by their rather shady father, whose finances were precarious.

When he failed too many times to pay the fees on time, the priest announced this over the school loudspeaker system, to shame the kids.

Christianity in action. :)

Cynic, more accurate to say a branch of Catholocism in action. No need to tar all Christians with the same brush, although I take your point that that priest’s actions were not Christ-like.

Curious on what the situation looks like inUS….

I’m sure there will be a bail-out for these indebted people. I doubt the govt will stay the course on rate hikes when they don’t have the QE baggage the USA has. Canada is not the US.

More likely, Chinese investors will be allowed to become citizens providing they buy real estate. It’s called ‘riding the tiger’.

The Canadian economy now runs on ‘real estate’ as their energy industry winds down.

https://thetyee.ca/News/2018/05/02/Government-Revenue-Fossil-Fuels-Sharp-Declin/

And the governor didn’t identify who is responsible for said debt for fear he might poke out his own eye. It is a no-brainer that punishing prudent behavior and rewarding speculation will end up as it did.

We will get to 3.5% on a straight line when there is no hiccup, and Santa Clause is real. Just what does he think kept the economy from diving?

Doesn’t this mean that if I have mortgage debt of a million dollars, and I am part of those 8% of Canadians, my gross income is under $285,000 (annually I presume).

So let’s say I only make $200,000. Let’s say the interest rate is 8% and I pay back over 30 years. My annual mortgage payments still come to less than $100,000.

It’s hard for me to see how this is unsustainable.

This is what matters in a best-case scenario: What is your after-tax income, how large is it compared to your mortgage payment now, and what will that relationship be when mortgage interest rises by 2 percentage points (since most mortgages in Canada are adjustable-rate or variable-rate).

Then there are more typical scenarios in a mortgage crisis where one of the earners in the household loses their job. Then the question turns into: How long can you make the mortgage payments?

That’s what it means to be “at risk.”

The rate would never go to 8% anytime soon. Let’s say it goes to 5.5% though, which is foreseeable. On a $1M mortgage, that would be $55,000 per year. The person’s after-tax income would be about $170,000 assuming a 40% tax rate (federal and provincial) against $285,000 income. The person is spending a little less than a third on housing cost. I think that is a wast of money, but not unsustainable unless the person loses his/her job, which very well could happen in the next recession.

In my mind, the mortgage defaults will occur on a large scale when the recession hits, not before. Good jobs are hard to find, especially for people who have the additional stigma of getting laid off or are over 40.

TD has already increased its 5-year rate to 5.49%. The others will soon follow.

Forget to mention: the combined Federal and Provincial marginal tax rate in Ontario for taxable income exceeding $220k CAD is a little over 52%. Quebec is about the same, and BC is ~ 48%.

My understanding is mortgage interest on a private residence IS NOT TAX DEDUCTIBLE in Canada.

Is my understanding correct?

Correct, but the gain on sale is tax free for primary residence.

Never say Never. That is a foolish statement considering that the bond rates dictate the fixed mortgage rates. Government cannot control bond rates as they represent debt obligations and with the average Canadian holding just a 3-5 year fixed mortgage, what happens when they are up for renewal? Unlike the US we do not have 30 years mortgages.

If you have a fixed rate mortgage higher rates mean nothing, (or that you can inflate away your personal debt) That chart is deceptive because home prices in 1970 were a fraction of what they are today. Inflation seems to be finding it way into wages. The problem could be shaky finance companies selling or calling their paper. So it matters who you do your REFI with, just like the same CDs with a bank or a brokerage have different rates. I just read Doug Noland on this and he says the consumer is not the inflection point in this crisis. So we may be entering a period like the 1970s.

Ambrose Bierce,

Very few mortgages in Canada are fixed rate. Many are variable (adjust almost immediately) and many adjust in a certain number of years after origination (often 5 years). The 30-year fixed-rate mortgage that is nearly standard in the US is very hard to find in Canada. This is why rising rates are a particularly tricky problem for the Canadian housing markets.

I believe I read somewhere that a rather high percentage of Canadian variable-rate mortgages are due to readjust this year, possibly somewhere in the tune of 35-40%. I can’t remember the exact stat, though.

I remember those days.

I could buy 5 Mojo’s for a penny, now a single Mojo is 5 cents if you can find them.

Show me 1 Canadian in any average Canadian neighborhood who makes over $100K. $285,000 annual income in Canada? Are you kidding me? In Toronto median household (that’s husband and wife) is around $79K.

It’s a bit more complicated than that.

In parts of Canada with loose lending policies like Vancouver and Toronto. It is more likely that someone/family making 150k bought a house for 500k years ago that’s now worth $1.5 million and they went up the property ladder to buy a home for $2 million.

You could have bought a new home in early 2017 from a developer for $2 million hoping to sell your home for $1.5 – $1.7 million and get a mortgage of 300k – 500k at a rate of 2%, which was the rate for variable mortgages at the end of 2016.

But with rising mortgage rates and changes to the mortgage qualification rate and a housing market that just fell out of the sky because speculators never believed rates would rise ever again. You may only be able to sell your home for $1 million while still on the hook for the $2 million dollar home under construction.

If your current home is sold conditionally on financing, banks are having appraisers undervalue homes to protect themselves from the risk borrowers default in a rising interest rate environment. They may come back and say the home is only worth 900k which means buyers won’t pay more than that or risk having to go to an alternative lender who charges rates at 9% – 12% for second mortgages.

You also have to renew your mortgage every 2 – 5 years depending on the terms of your agreement with your lender. For bigger banks, they may not renew the full outstanding mortgage balance if they see you have overextended yourself and borrowed a lot of money on your credit line. You would either have to sell your home or take a second mortgage with the alternative lender at 9% – 12%. If you have a second mortgage of 300k- 500k with an alternative lender you could be paying over 30k a year in interest costs from your 150k pre-tax income.

If your mortgage is already with an alternative lender, they may have clauses in their agreement preventing you from leaving them for any reason. And the only way out of those mortgages is to sell your home (which is now falling in value). Your mortgage rate with them was probably already higher than a regular bank, at renewal, your mortgage could go from 5% to 8% or higher.

Similar problems exist in the new condo developments which take 3-5 years to build, where people purchased units based on the assumption rates would stay around 2% – 2.5% and they would qualify for the mortgage. Now not only could their bank say they don’t qualify, the only people lending them money may be private/alternative lenders who demand a rate of 8% or more.

“The borrowing and spending binge by Canadian households, businesses and governments (all levels) continues unabated.

At the end of December, 2017 the total debt outstanding in Canada (bottom line of the Statistics Canada credit market summary data table) was $7.603 trillion. At the end of December, 2016 the total debt outstanding was $7.25 trillion. In the 1 year period from the end of December, 2016 to the end of December, 2017 it increased by $353.5 billion. This is an increase of 4.8%.”

http://owecanada.blogspot.ca/2018/03/canadian-total-household-business-and.html

“The Bank of Canada held its overnight rate at 1.25 percent on April 18th 2018, in line with market expectations. Policymakers said the transitory impact of higher gasoline prices and recent minimum wage increases will likely cause inflation in 2018 to be modestly higher than expected and the economy is projected to operate slightly above its potential over the next three years. As a result, the central bank sees higher interest rates over time, although some monetary policy accommodation will still be needed to keep inflation on target. Interest Rate in Canada averaged 5.90 percent from 1990 until 2018, reaching an all time high of 16 percent in February of 1991 and a record low of 0.25 percent in April of 2009.”

==============================

These people really are clowns. They suppress interest rates to the bone and leave them there for about 9 years, maintain massive liquidity and ease of credit and then wonder why they got the result they did.

What did these buffoons think would happen? People are going to borrow more in this Goldilocks interest rate environment (where abnormal rates no longer reflect risk) and are forced to for RE when the effects of both Government policies and Central Bank monetary policies combine to cause real estate to “demand inflate”.

Why? Credit expansion creates present tax revenues from future money. Everybody wants to get paid now from the debt bubble….mostly governments but of course the RE and knock on industries.

We are in deep do-do whether anyone believes it or understands it. Oh….and the marks/victims/patsies in the debt Ponzi will suffer greatly as well.

interesting, so just to save 8% speculators, bank of canada keep screwing the rest of the populatins by keeping interest rates so low so those guys can keep making their payments? Government of the people for the people indeed!

Remember: this is just household debt, debt owed by private individuals.

I am pretty sure debt owed by Canadian companies, whether public or private, has grown at a similar if not faster pace.

I am almost ready to bet a sixpence debt at the lower end of the scale (where junk rated companies dwell and where in the US lower FICO scores are) has grown at a much faster pace than at the top over the past four-five years.

And it’s not just the speculators. I’ve been actually told, with a straight face, 6.75% financing for a fifty grands BMW is “insanely high”.

Perhaps I am the only one to remember when double digit auto loans were the norm and not the exception. I am old but not that old: Oliver Cromwell had already cut off the King’s head when I was a boy.

In fairness to Canada this is happening in most countries. The issue is that people have been warned long enough that interest rates will go up, if they’re just burying their head in the sand then unfortunately no sympathy.

Canadian here,

As individuals we only have ‘eclipse viewing’ pin-hole cameras to understand our country, and have to rely on the same stats as everyone else. I assume they are fairly reliable, but most likely reflect only a few of the larger cities like Toronto and Vancouver. Anecdotally, I know of no one who fits these statistics other than the sons and daughters of some friends; ‘kids’ in their thirties. Their parents have no debts and have been mortgage free for a long time, decades in some cases. Their kids, on the other hand, build ‘end of career’ high-end homes for their starter, and God help them if a divorce or job loss is in the works because they owe big time on both vehicles and these newly minted mortgages.

I preached to my kids ad nauseum about the evils of debt during their lifetimes with mixed results. They don’t seem to be as afraid of debt as I am, but their mortgages are affordable, much less than rent. My son’s mortgage for a stunning riverfront home on 3 acres is 2X his income. I helped him ‘convert’ a motel into a sprawling rancher about 6 years ago. Lots and lots of sweat equity involved. It is now worth 2X what he paid for it and has a caretakers ‘shack’ to rent out if need be. My daughter has a modest bungalow just south of Nanaimo in the town of Ladysmith. It is a lovely little place with a very large yard. It should be paid off by the time she is 50. Both, she and her husband, have very stable employment and they have just one child and plan to keep it at that.

The son of a long time friend just split up with his new wife and promptly returned home to the basement. The wife continues to live in the unaffordable waterfront fixer-upper with the two kids. I assume it will be sold very soon. Another friend’s son is building a first home…new, with a $600k plus price tag. I have no idea how these young folks sleep nights.

My old friend Art, (who worked running cranes loading log barges….which is an extremely high paying job), was fond of saying, “It’s not what you can afford when you are working that’s important, it’s what you can afford when you are not working”.

I think these 8%…or 20% folks, whatever the number, are going to learn and earn Art’s wisdom the hard way.

Whether you can reasonably keep to small mortgage is partly down to luck and the pain of holding that home isn’t simply a factor of the purchase price as we all know. So 2x income or 3x income mortgage isn’t the same state to state or even county to county.

In theory you can always move where it cost less to live. In practice if your roots and whole family are in a single city it makes it highly undesirable to leave that area.

I will say in the top 10 bubble cities we list 3.5x income mortgage is not uncommon and may even be on the low side of things… Some justify overpaying and say it’s okay to be house poor.

I am still not sure what house poor means. I am right at or under 3.5x depending on bonuses and stock and we are still roughly able to save 20% of our income. Not great, but I wouldn’t use the term house poor…. So I would guess people are living pay check to pay check to pay far more than that on similar incomes.

From the article: “It turns out 8% of households have mortgage debt that’s more than 350% of their gross income.”

That’s probably true just about everywhere in the world.

Maybe the author means 80%, not 8%? Or maybe the author means 1350%, not 350%?

Look at the chart in this article: http://www.businessinsider.com/house-prices-income-wages-2017-3

The title of the chart is “Median Home Price Divided by Median Income”.

Vancouver has a multiple of around 11 and in Toronto the multiple is around 8.

Traditionally a multiple of 3 is supposed to be affordable and that recommendation comes from the days of high interest rates.

I noticed the same thing…

I’ve traced the statistics cited in the article to the actual report by the Bank of Canada. However, are the statistics provided by the Bank of Canada accurate or misleading in some way? I assume they have an incentive to say everything is OK.

When you think about it though, if 8% of “homeowners” have risky mortgages, that may be a high percentage considering many homeowners don’t have a mortgage at all, or at least no mortgage with a Canadian bank. If you took them out of the equation, that 8% would be a higher percentage.

Further, if 8% of all homeowners become delinquent, that’s obviously enough to put all Canadian banks in a crisis mode, even before consideration of any commercial RE that is also at risk. Even a 4% default rate may put the banks under. I assume bank capital is only around 10%.

Future Historian: Now you got it. Most Canadians dream of $100K annual income. Bank of Canada is lying like hell. The thing is how coolly these bastards lie despite the fact that they know any intelligent guy can easily find the necessary statistics. They are trying to prevent their population from freaking out. Imagine if this BoC’s Governor Stephen Poloz comes out and says those 8% owe 10-12 times what they earn.

I don’t think the Bank of Canada studies considers that if prices drop more than 10%, people who CAN repay their mortgages will simply choose not to. It is emotionally difficult for someone to continue making mortgage payments on an underwater house. There is a risk of jingle mail that goes unaccounted for.

So Wolf ,what happens if someone in Canada can’t pay their mortgage? Is giving up the house enough or even after that they are still in debt?

Unlike IOUSA, most Canadian mortgages are full recourse, meaning the Banksters can come after you personally for any unpaid balance. This is far less common in the US.

Actually no, as far as the US is concerned. Most mortgages in the US are full recourse.

See my comment below. And click on the link. The article explains this in detail and lists the lucky 12 states where mortgages are non-recourse.

In all but two provinces, banks can get deficiency judgments if the house sells for less than the mortgage.

Same as in the US. In the US, only 12 states have non-recourse mortgages; in the remaining states and DC, mortgages are full recourse, just like in Canada, and banks can get a deficiency judgment. So what played out in the US during the mortgage crisis can also play out in Canada.

https://wolfstreet.com/2017/04/25/mortgages-u-s-canada-recourse-states-non-recourse-states/

I venture to say that if enough people don’t pay their mortgages, it will not matter whether the loans are recourse or not. Safety in numbers. The banks don’t have the resources to go after these people, and the politicians lack the will power. They’ll be a taxpayer bailout of underwater homeowners before there is any kind of recovery from them.

Sounds like the America in 2005-2007 using ARM’s.

When sorrows come, they come not single spies, but in battalions”

Heckova job, central bankers.

Root cause is the greed of private financiers, not government central bankers.

We’ve made the mistake of allowing the financial sector to become far too large and now it can call the shots and that means ‘keep the cheap money coming or we’ll crash the markets again’.

Yeah those evil bankers forced people to take that 1 million dollar mortgage

Poor things.

Evil bankers indeed.

People who were stupid, arrogant, and greedy took on massive debt this way to play hte market.

They speculated and they will lose if they haven’t sold by now.

Smart money left the buyilding long ago. I’ve owned real estate for 40 years and sold 3 years ago. Massive returns.

I rent you see becuase I went through the crisis in Alberta 40 years ago when Trudeau Senior wipe dout Alberta with NEP. I learned then that buying high and selling low was a mugs game.

Unfortunately any person holding real estate will face massive decline in values.

Thus the greed of the few affects the many like it did in the US.

Blaming bankers for your hubris is not the way to see this.

This is why renting is the only way out until teh markets flushes.

Use the US as your guide.

“8% of Canadians Have Mortgage Debt Over 3.5x What They Make”

Are the Canadian bankers trying to be funny? The median household income is $78,280 in Toronto and Vancouver. Many have bought houses at over one million dollars. More likely, those 8% owe 10 times their income and not 3.5 times their income. Lies, lies, lies, even when they pretend to be telling the truth.

That’s a scary amount of debt but thanks for putting this together.