Use of home equity to fund personal consumption spikes.

By Daniel Wong, Better Dwelling:

Canadian real estate related debt tapering? That would be ridiculous! Filings obtained from the Office of the Superintendent of Financial Institutions (OSFI) show, after a brief decline in January, the balance of loans secured by residential real estate hit a new high in February. More interesting is the segment of loans being used for personal consumption, is growing at the fastest pace in years.

Securing A Loan With Home Equity

Loans secured by residential real estate are exactly what they sound like. They’re loans that you pledge your home equity in order to secure. The most common example would be a Home Equity Line of Credit (HELOC). You know, the same type of loan the Canadian government is discretely paying to teach you how to borrow. There’s also more productive uses, like when you start a new business and need to use your home as security – just in case you aren’t able to pay your loan shark bank back.

Either way, debt is debt. The big difference to note is a loan secured for personal reasons, is considered non-productive. The borrower isn’t expected to take a calculated risk, in order to earn more money. A business loan is considered productive, since it might generate more money. This isn’t just our opinion, banks actually classify these loans separately in their filings. Today we’ll go through the aggregate of these numbers, then break them down segment by segment.

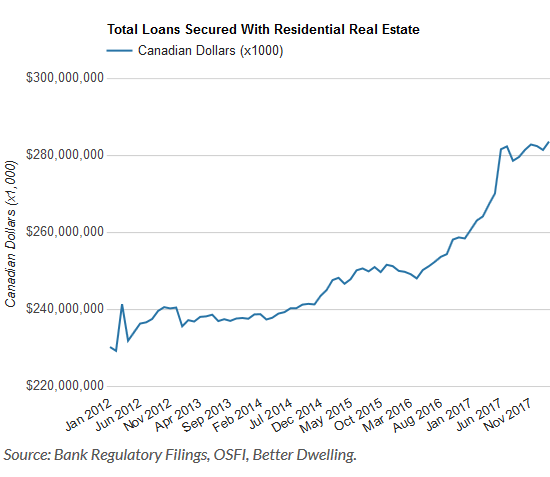

People Used Over $283 Billion In Home Equity To Secure Loans

Loans secured by real estate hit a new all-time high in February. The total balance of loans secured with real estate racked up to C$283.65 billion, up 0.77% from the month before. This represents a 7.79% increase compared to the same month last year. It almost looked like Canadians were reeling that debt in January, with a tiny decline. Instead it made a monster move, more than making up the ground lost the month before. Now, let’s break this down.

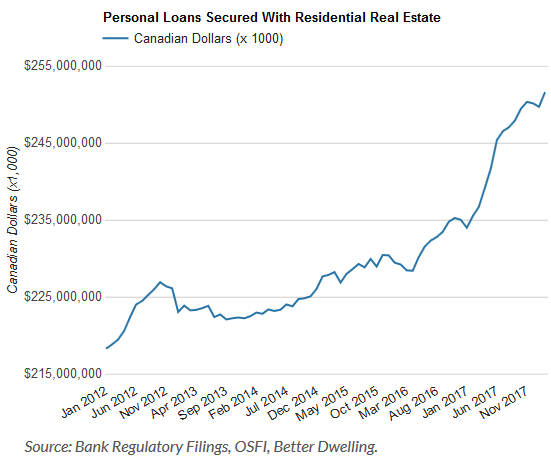

Over $251 Billion In Homes Are Being Used To Secure Personal Debt

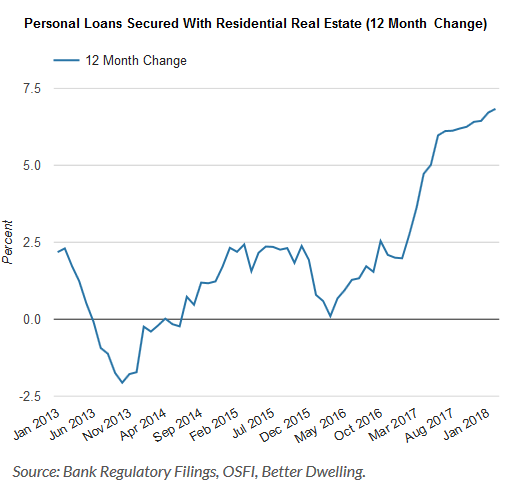

The total of loans secured with residential real estate for non-business purposes spiked in February. The outstanding balance reached C$251.64 billion, a 0.77% increase from the month before. This represented a 6.83% climb compared to the same month last year. This brings the total to an all-time high.

The rate of growth is definitely something people should be taking note of. The monthly rate of 0.77% is the fastest rate pace since June 2017. The annual rate of 6.83% is the fastest rate of growth since… well, since banks started reporting these numbers on their balance sheets. Apparently higher rates aren’t slowing borrowers down.

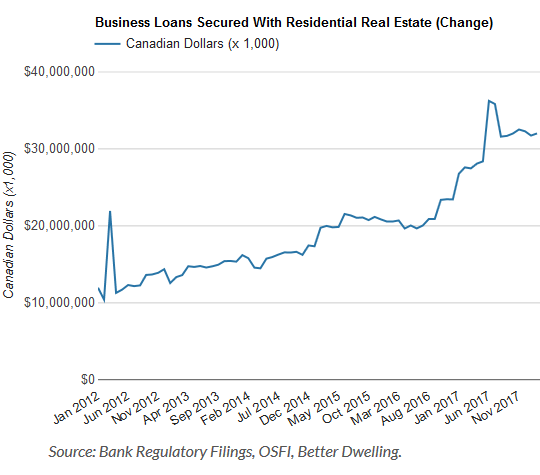

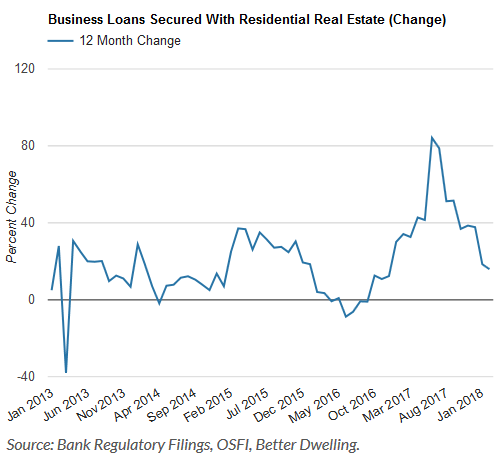

Over $32 Billion In Homes Are Being Used To Secure Business Debt

Business loans secured with residential real estate also saw a rise in February. Just over $32 billion in business loans were secured with homes, up 0.86% from the month before. This represents a 15.96% increase from last year. These more “productive” loans, are not at an all-time high. Totes disappointing, we know.

The takeaway here is the decline in growth. This is the fourth month we’ve seen the annual trend taper, bringing it to the lowest levels since December 2016. A decline in debt growth is typically seen as good, but we get mixed feelings when business borrowing slows.

If you’re going to have debt, it might as well be for productive reasons. Unfortunately, residential real estate being used for personal consumption is reaching the fastest pace of growth in years. Meanwhile the segment being used for business purposes, is seeing growth decline rapidly. That next rate hike is going to be rough. By Daniel Wong, Better Dwelling

Canada’s magnificent house price bubble wheezes. Read… Canada Home Prices Fall 6% in Q1 from Year Ago, First Decline since 2009

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I recently read an article that suggested that Canadians use of HELOC’s was 5 times that of Americans! Love to see an update of where we currently stand on that ugly statistic.

Reminds me of the USA circa 2007.

If Canada is like most countries (except the USA) then most mortgages are variable interest. In other words… the average Canadian better hope rates never normalize.

In Canada the variable is still in use, and the fixed rate is maxed out at 20 yrs. The mortgage rate is almost double at the max term length so I think the fixed 3 yr or 5 yr tends to get the most use, I read something around 75% of the current mortgages are due to rate changes in the next 3 years.

Bank of Canada already slowed down on rate hikes, they smell the smoke.

In around 2006 in Massachusetts a neighbor of mine was talking about getting a “home eq” loan to repair the roof. I had no idea that people were doing this, taking out new debt on a home instead of paying it down. But roof repair at least seemed a sensible purpose.

It turned out this couple had previous home eq loans, and on this credit line increase they bought a Harley motorcycle ? instead of replacing the roof, which was covered with a blue tarp! No doubt the bank did not inspect the collateral against this loan.

If it’s good enough for Trudeau, it ought to be good enough for the Canadians.

Problem is, they don’t need more Trudeau, they need more True Dough!

If everyone was a trust baby, and never had to have a real job, yes.

“Personal consumption”= Making their car payment or mortgage.

But of course, that’s embarassing to tell your lender, so they will say they’re using it to go on a vacation, which works because they don’t have to show anything for the money.

(Canadian here),

I have no idea what these people are doing with their borrowed money? To be honest, I don’t know anyone with debt in my age bracket…(62). My kids have mortgage debt, and my son has a truck payment with his mortgage, but he uses the truck for business and deducts it. Most of my friends have had their homes paid off for the last 20 years or so and they have been modest wage earners their entire lives. If I had to guess I would think the referenced home LOCs are used for home improvements and renos. Mind you, there are lots of Audis and Beemers on the roads these days in addition to honkin big trucks..

Anyway, this Canuck is almost finished constructing a rental, using cash. The tenant is an elderly neighbour and family friend. The finished cost per square foot comes out at a whopping $40 if I include the new hydro service and machine time for site prep, etc… This is due to my free labour and using up surplus materials I have squirreled away over the years. The cottage is a 640 sq ft gem, 1 bedroom, combo laundry/bathroom, post and beam open design, vaulted…t&g pine ceiling. It has a mountain view and sits on a 7 acre lot. I am currently drywalling the last two rooms after pressure testing the plumbing. He starts moving in the first week of May. It would cost $200,000 to replace with a similar modular, and new single family construction is now going for $300/sq ft for basic layouts. I designed the house for future bedroom additions if desired. However, limiting size and design to a cottage allows us to focus on elderly tenants or single working (non-smoking) males. In our rural location multi-bedroom houses attract dodgy tenants. It would break my heart if someone abused this house. I have a lot of hours invested.

Not all of us up here are profligate spenders. Plus, there is no better return than sweat equity.

regards

That does sound pretty sweet! What part of Canada?

Also, do people eat canadian geese, and if so, do they taste as good as they look?

Yes, people eat geese. If I remember right they are like the dark meat of chicken.

We tried roasting a Canada goose some years ago, it didn’t go over well.

Could be was wrong time of season or they were eating something (grass?) at the time that tainted the meet?

The cabin sounds sweet, good job! :)

That “most” Canadians are not in trouble means nothing. It’s the margins that cause crashes.

8% of American mortgage holders were in default at the very peak of their housing crisis, and it brought down the world economy. There are way too many Canadians in way too much debt for us to avoid a major reckoning now.

I have come to find that if Paulo doesn’t see it, it does not exist. Life has been so much better in Canada for that very reason. In a few weeks the positive vibes will start to diminish when B.C. starts running out of fuel at the pumps. Unless he also manufacturers his own fuel, I would expect he has a preparation for that scenario too.

Sorry to pick on ya Paulo, but we know you and your kids are stable – you point it out in every tale. The banks are reporting on people with mortgages, you are not one of those people. You own your home, you are not who they speak of.

They speak of neighbours who don’t tell you a single bit of truth about their financial situation so that they can appear to be better than the Jones’. Those home “owners” are not owners, they are debtors to the bank until the day they hand in the keys or make that last payment. The people exist or the stats wouldn’t exist to tell us they exist.

Interesting discussion. For Govinda’s question, I believe Paolo lives in the Campbell River area on Vancouver Island.

It is not unusual for Islanders to feel smug about their good fortune, but as Prairies points out, islanders are subsidised by cheap gas for hauling trucks and private vehicles, and our governments susbsidise ferry costs to the mainland. These supports could change.

I think Prairies (and the author) are right; there is a large proportion of Canadian “home owners” who, in fact, owe the bank. It’s a shame we don’t see more business loans (and not just Bed and Breakfast construction) going on.

The stories out of Canada keep getting weirder, luckily most cities in Canada do not have a housing bubble.

‘Bought the house for $655,000 with a $55,000 down payment. Monthly payments of $6,000 with a mortgage rate of 11.99 percent weren’t sustainable, but she was hoping to cut that sharply by refinancing after she moved in’

https://globalnews.ca/news/3951652/interest-rates-canaa-housing-underwater/

The globalnews article makes no mention of a co-borrower such as a husband or even a boyfriend. This whole fiasco sounds like a Canadian version of Ameriquest, which became the largest subprime lender in the US before the collapse of the US real estate market at the onset of the Great Recession.

They don’t have money to make mortgage payments and payments for other junks such as new SUVs that they have bought, so, they have to use the house as ATM. This is just the beginning. The end should scare everyone in Canada like hell. Not to worry though; the other parts of the world will follow with 1-2 years delay.

Not to worry, my friends. It’s different this time. My realtor and every financial media talking head on TeeVee said so. Surely they would not steer me wrong, with our ever-vigilant regulators and enforcers being such fierce and dedicated guardians of the public interest.

/sarc

Thanks for the chuckle, Gershon. I don’t watch the financial media talking heads on TV any more, nor do I read them in the MSM, except for a few British exceptions.

Here in Canada I find that most friends and relatives get a glazed look if I start to talk about the state of the world economy. I suppose it’s human nature not to want to face unpleasant realities. They’ll be running around like headless chickens when their brethren come home to roost.

What good is all that hard earned equity if you don’t take advantage of it?!

Real Estate “equity” is nearly invariably inflation. The banking rentiers can’t stand seeing “equity” which is not leveraged back to them.

The mule chasing the carrot.

I used my HELOC for immediate life-saving care in the US. $40,000. That’s hardly productive.

The Canadian medical system is in far graver shape than personal debt.

Most boomers are coming of age for healthcare they paid into for over 40 years only to be denied or postponed.

My doctor says I don’t have access to healthcare but access to a waiting list.

Tonight I tried to book an appointment for blood work. All locations were booking out over a week. 40% taxes and I have to wait a week for routine lab work and 2 years for hip surgery.

There will be riots over healthcare in Canada in the next 10 years.

Canadians used to be sensible. But fiat central banking eventually destroys all peoples.

A great article and totally true.

It’s amazing how many people with mortgages and little in savings buy or lease luxury vehicles to suit their ‘in crowd’ image.

No problem at all in Canada though. We can just roll that HELOC and personal LOC debt into our next mortgage when it resets next year and just like that the balance is paid!

What’s even better is that now we still have the LOC to use for vacations and designer clothes until the next mortgage a few years later.

Lather, rinse, repeat… good times.