Corporate America fears that a Trade War would hit supply chains in China.

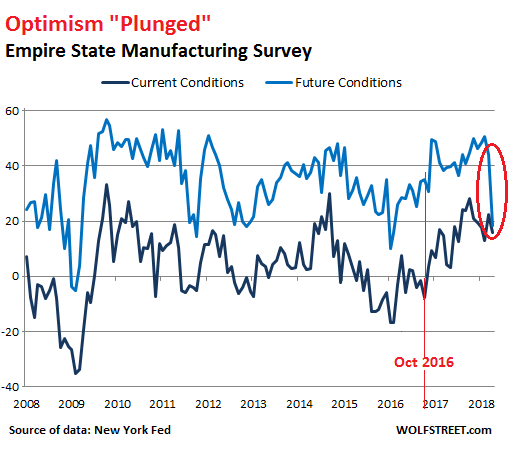

Something strange happened in the Empire State Manufacturing Survey released by the New York Fed this morning. The survey has two headline components: The index for current conditions and the index for future conditions six months down the road. The first index behaved reasonably well; the second index plunged the most ever.

Executives are notoriously optimistic. In the survey, which goes back to 2001, expectations for future conditions are always higher than current conditions, and often by a big margin, even early on in the Financial Crisis before all heck was breaking loose.

The index of future conditions reacts to events. For example, it spiked after Trump’s election. So today’s biggest plunge in survey history is a reaction to an event.

“Optimism tumbles,” the New York Fed’s report called it. And more emphatically: “Optimism about the six-month outlook plunged among manufacturing firms.”

The headline index is based on a question about “general business conditions.” The sub-indices are based on questions about specific aspects of the manufacturing business, such as new orders, shipments, unfilled orders, employment, etc.

In this “diffusion index,” respondents rate their business on each question, with conditions either rising or falling. The number of respondents who said the level was falling is subtracted from the number who said it was rising. Respondents who say there has been no change don’t count. If half say the level is falling and half say the level is rising, the index is at zero.

The index for current “general business conditions” in April dropped slightly: 37.9% of the executives reported better general business conditions; 22.1% reported worse conditions. The difference between the two, 15.8 points — the index value for April — was down 6.7 points from March, and as the report said, “firmly in positive territory.”

But the index for future conditions – which is usually highly optimistic – got crushed, with only 40.3% of the respondents saying “general business conditions” are getting better and 21.9% saying they’re getting worse. This pushed the index down to 18.3, the lowest level since February 2016. The 25.8-point plunge from March to April was the steepest monthly plunge in the history of the survey.

This chart shows the General Business Condition indices for current conditions (black line) and forward-looking conditions (blue line) with the plunge circled. The thin vertical red line indicates the last survey period before the November 2016 election:

The 25.8-point April plunge took the index from 44.1 points in March to 18.3 points in April, the largest monthly plunge ever.

The second largest plunge (25.1 points) occurred in January 2016 as credit in the energy sector was freezing up and as the S&P 500 index was on its way to drop 19%.

The third steepest plunge (24.3 points) occurred in January 2009, during the Financial Crisis.

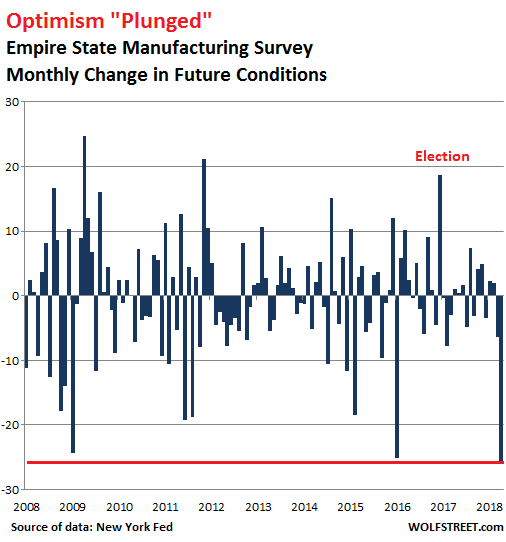

The chart below shows the month-to-month changes in the forward-looking general business conditions index:

Among the forward-looking sub-indices were some standouts, in terms of by how many points they plunged from March to April:

- New Orders: -24.5

- Shipments: -24.8

- Number of Employees: -10.2

- Average Employee Workweek: -11.0

Over the history of the survey, the index for future conditions has been on average 31 points higher than the index for current conditions, attesting to the rampant and enduring optimism of the executive mindset about the future. But in April, the difference plunged to just 2.5 points, the smallest difference since 9-11, when it had plunged to 0.6 points.

Why the plunge in optimism?

The report did not explain why optimism among manufacturers, after the 16-month Trump surge, plunged to this extent, so suddenly, and to such a low level even as the economy was clicking along, as long-term interest rates remained low, and as current conditions didn’t signal any major deterioration.

The future conditions index reacts to events. And there was only one major economic event that cropped up in the US during the survey period: Fear of a trade war with China.

It’s not that US manufactures export that much to China – they don’t, and that’s part of the problem. As a group, they worry less about China cracking down on manufactured goods exported from the US to China. But they worry about their supply chains. They’re going all over China and through China, importing into the US essential components and materials, thus contributing to the horrendous trade imbalances between the US and China. And these components and materials are now being specifically targeted by US tariffs.

The proposed tariffs would not stop those imports but would raise their costs, and the rising costs of those imports – or the costs of switching to another supplier outside of China – would eat into the profit margins of the US manufacturers. This would be the opposite of what happened when these executives decided to cut costs by offshoring their supply chains to China.

For now, no actual tariffs have been imposed. And it’s possible that Trump will cave under the pressure of Corporate America and that nothing will change — in which case we could expect this optimism gauge to spike once again.

Leverage – the risk it poses to banks – is why the Fed has been worried about the price bubble in commercial real estate. Read… As Malls Get Crushed, Commercial Real Estate Prices Fall to Lowest in Nearly Two Years

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Or Pessimism Surged? Recently I have bought things online which are drop-shipped from China. I wonder how that will all work out?

new rumor to start: those things you bought from China will generate an excise tax bill that you will pay under penalty of law. They know who you are and they know where you live and you bought something from China, cheap. Or the bios was infected with spyware that will steal your bank account. Foreign devils. You’re lucky to be alive.

Things are good but we suspect they are going to get bad: Can’t tell exactly why but we’re pessimistic for free floating reasons and don’t suspect media culpability because we’re too busy working to see the media’s games –> business as usual and a good sign for tomorrow being great and growing.

as opposed to

Things are good today but the recent actual, real crater that everyone sees and can’t be ignored will affect us next month: If the media shows up with photos and no spin then there’s a real problem afoot. Assume Yellowstone or aliens landing. Not vague threats of possible unpopular ideas flourishing.

Not to be confused with bond and equity markets that are massively overvalued and should experience a correction sooner than later. Neither has a lot to do with the real economy.

Suffice it to say anyone with a modicum of discernment , knowledge , intelligence , education along with ” Eyes Wide Open ” are skeptical at best but more likely pessimistic because of the simple fact that the entire global economy at present is the very epitome of a Smoke & Mirrors based Potemkin Village completely devoid of substance : exacerbated by political instability across the globe , incompetent at best leadership worldwide and a collective stupidity among a general public addled by entertainment and addicted to celebrity .. all of which has everything to do with the all too REAL economy

If all the fraud in all the markets, and all the fraud in creating currency out of thin air comes due, along with the inherent fraud in fractional reserve lending by our compassionate bankers….. do we get to not only audit and eliminate the Federal Reserve, but see some major jail time for the perpetrators as well ?

Of course.

As one commentator observed in another thread, the US is a country of law.

HAHAHAHAHAHA.

It says a lot that 2 black people in a Starbucks have a far higher chance of being arrested than bankers.

As I said, the internal contradictions will eventually blow this country apart, just like any Banana Republic really.

Everything is relative. Yes the rich and powerful have better access to law than the rest of us.

But thinking this makes the US the same as Russia or China just illustrates a lack of knowledge.

If you can’t go there READ about it. Actually you will find more about Russia by reading than going there, because the main drag in Petersburg with Gucci etc. shops could be in New York.

Recommend reading: ‘Russians’ by Gregory Feifer. 2014

Feifer has a Russian mother. She met his American father when he was working as young presenter at the 1959 American Exhibition in Moscow. This was the occasion of the famous Khrushchev-Nixon debate/ argument, the gist being that Nikita thought the exhibit was phony and that there was no way ordinary Americans could have dishwashers etc,

Moving on, Feifer notes that as early as the 1800’s Western visitors to Russia noted the general lack of interest in law, including the concept. For their part, Russians were, and are, bemused by what they see as a Western preoccupation with the idea of rules applying to everyone.

In the US, business has lots of influence on government. In Russia big business IS the government.

Maybe an example is worth a lot of words. There is a large office building in the US( I forget which city maybe NY) with its frontage built AROUND a shack.

The developer assembling the site could not get that last holdout to sell and so built around it.

That would NEVER happen in Russia. Even if property rights existed as they do in the US, the owners wouldn’t dream of opposing the project. Their fate would be too predictable.

“In the US, the banks ARE the government. In Russia big business IS the government”

FIXT!

I didn’t say that the US is the same as China and Russia. In some ways it’s a lot better and in a lot of other ways it’s worse. Property rights, etc, they are all good, but a lot of the prosperity in the US are built on top of violence and brutality US forces, diplomats, etc commit in other countries, the benefits of which (cheap oil), the consumers partake on. The Middle East, the drug wars, Ukraine, etc, etc. And violent people eventually bring the act home. Opioids, insane level of homelessness in what’s supposed the most prosperous country in the world, school shootings, etc, etc. No doubt those children are acceptable offerings to the gods of property rights, eh? And let’s be real eh, if we REALLY believe in property rights, we’ll be returning this country to the Indians ;)

“In the US, business has lots of influence on government. In Russia big business IS the government.”. English is so ambiguous, I am not sure what you meant by that. Are you saying Russia is run by a cartel of companies? Then the answer is no. Russia is run by Putin, full stop. And China soon will be run by Xi. They are not businessmen, they are just like any other dictators. Nothing special. In fact if that’s you meant, then that’s a more apt description of the US. This country is indeed run by big businesses. Big banks, uncle Warren, big Techs, big Weapon companies. There’s a reason why Eisenhower spoke of the “military industrial complex”.

If I lack knowledge, then you lack the capacity to reflect on this country’s history. This is not the first time this country has been ruled by big businesses. Corruption, etc was rife during the railroad eras. It was also rife during the years leading up to the Great Depression. And speaking of not believing in the law, you should dig up the history of New York in the 19th and early 20th century. Not being ruled by big businesses is actually more the exception.

> That would NEVER happen in Russia. Even if property rights existed as they do in the US, the owners wouldn’t dream of opposing the project. Their fate would be too predictable.

My friends Indian dad mentioned a year or two ago a friend in India didn’t want to sell his high end condo. He did after a couple of guys walked in and said ‘don’t mind us, we’re here to help move your piano’ And then heaved it out the six story window. They said they’d be back next week to help move more stuff.

More recent comment about Putin is before Putin ordinary business owners had no protection from being shaken down. Or having thugs take over your apartment. Now they do mostly. If you’re running a flower shop say.

The policing of racial minorities is not relevant to this discussion, which is about business and property laws.

As for Russia, a Russian friend from a successful business family (not mafia, not Putin-connected) put it like this:

‘If someone connected wants to buy your business/property, you will in fact usually get a good price from them, but you must sell: if you refuse, something nasty will probably happen and you will get screwed financially at the very least’.

In other words: comply, or get robbed. Perhaps the difference is that between the highwayman who leaves you something to wear, your horse, etc, and the house raiders who murder you……

His other maxim is:

‘Never ever go against the connected. They always screw you, and will chase you down wherever you are.’

If the US banks are the government, why is Wells Fargo looking at a billion dollar fine?

That’s not my point. We have a lot of homeless people here hanging around the Starbucks at 9th and Irving (San Francisco). They would occupy the tables outside without buying anything. And when I mean outside, those tables are still owned by Starbucks. Did the people in the cafe call the police to arrest them? Nah, why don’t you guess the skin color eh?

Should a business be allowed to refuse service to anyone? Absolutely, but not because of skin color.

Well said. Laws and the constitution are meaningless. All that matters are societal norms. It is not a societal norm for black men to hang out at a Starbucks (or other fast food dive) in a white neighborhood so that is de facto against the law. It is not a societal norm to enforce speed limits so you may drive as fast as you please. It is not a societal norm to prosecute those who have wealth and power so they may commit fraud without fear of being punished.

Much has changed for the better in the last forty years but without question corruption has become a societal norm in the U.S. We have gone down a dangerous path when the police force is used only to oppress anyone who might inconvenience or make uncomfortable people of privilege . Imagine Jamie Dimon being removed from Starbucks because he was making two black patrons uncomfortable – wouldn’t happen, no matter what Jamie was doing.

“It is not a societal norm”

Translation: Stay in your lane. There are invisible lines that you should not cross. If you do, then the consequences are on you.

How in the world did someone decide fractional reserve banking is a conspiracy or even a problem. This defines …. (list of suitable words omitted).

You borrow money. You spend it. The person you spent it with deposits it. The bank lends out some of the deposit. BANKS CREATED DEPOSITS AND MONEY OUT OF THIN AIR! This is fractional reserve banking. It’a a litmus test for certain types of thinkers, and not a good one.

Fractional reserve banking means the bank does not have to keep sufficient funds on hand to pay out all depositors should they all request their funds at the same time. Fair enough – as long as the depositors know this is the case. I think we agree on this one.

The fact that banks create *new money* when they issue loans (home loan, for example) is a separate issue. I am not clear on whether you understand/believe the second one, but it’s true. A bank with 1M on hand in the form of deposits can lend out 10M that was not already on deposit (the exact ratio is determined by the fractional reserve limit).

Simple, you borrow $500k. You spend it. The person you spent it with deposits the money, The bank holding it lends $450k. It gets spent and deposited again. $400k is loaned again. You have $1300k in loans from a $1million deposit. This is creating money in the form of loans out of thin air, not deposits out of thin air.

However, if bank one loans the $500k and gives the borrower a deposit slip, you have deposits of $1500k, cash of $1000k, and loans of $500k, temporarily, until the cash is withdrawn.

Deposits are never created, Loans are created to the extent of the reserve requirement. a 10% reserve requirement can support x/.1 in deposits, or $10million in this example.

The key to the puzzle

————————————-

The ‘funny math’ is just loan proceeds being deposited over and over again by the people who are the sellers to the loan recipients. Spooky!

Risk management keeps the system under control. Panicky faux economists,who often sell gold on the side to those who get suckered into the panic, are the others who propagate this ‘conspiracy’.

” x/.1 in deposits”

meant to say “loans”, not deposits. No conspiracy here so don’t pounce at the inconsistency. Only a typing error.

Look, lots of fake pundits believe as you do. It’s a good way to identify them as fakes. True believers in gold as the only sound money are another great way to spot the economist fakes.

No bank anywhere ‘creates deposits’ by loaning the same $1million over and over again just at the snap of the fingers. That’s the image the fake economists want to you ‘see’. The only way money gets ‘created’ is by it flowing through the banking system.

With the exception of the loan being disbursed as a deposit slip as opposed to a check, making the borrower use their own checks to spend it, $1million in deposits is always only $1million in deposits, but could be as much as $10million, with a 10% reserve requirement, in loans after is propagates throughout the banking system.

I know, you don’t believe me. There must be a conspiracy out there making the system so fragile a sneeze could knock it over. Can’t fool you.

@ZeroBrain said: “The fact that banks create *new money* when they issue loans (home loan, for example) is a separate issue. ”

reply

———–

THAT IS FRACTIONAL RESERVE BANKING. THAT’S ALL IT IS. THE REST IS YOU AND OTHERS NOT TAKING THE TIME TO LOOK IT UP AT NON-CONSPIRACY OR NON-GOLD SALES SITES!

This ongoing rant against fractional reserve banking is one of the odder hobby horses on this circuit, maybe tied with the ‘you can’t go bankrupt if you have your own currency.’

If the bank had to have one hundred percent of deposits on hand then how could it POSSIBLY make any loan?

It just would be a glorified vault where you would obviously have to pay to store your money because it would have no profits

Good, sound banking existed for centuries before banks became gambling in derivatives, and had stock trading desks etc.

In it’s simplest form banking forms a bridge between older persons who have accumulated resources but lack energy and younger persons who have energy but lack capital.

Left to themselves to make private one- on- one arrangements,

the person with capital will sometimes meet the right entrepreneur, but as with all barter, this is very inefficient.

Enter: banking.

A not bad defense of why a bank does not all or even most deposits on hand happens in ‘A Wonderful Life’ where Jimmie Stewart makes a speech defending against a run on his bank.

Nick, I’m getting that people understand loans come from deposits. The ‘mystery’ and ‘conspiracy’ comes from gold sales people, bad pundits, and economic illiteracy.

Creation of money somehow became banks as mini feds who print money somehow but no critic will cogently explain the problem or how the ‘created money’ propagates. One fake pundit and gold salesman I read cryptically said ‘the Fed creates reserves’ as the entire explanation. That was enough to shut down the sheep. I’m still waiting for anyone to explain the issue so that anyone could grasp the problem. Bonus: use accounting 101 T-accounts to show the flows.

Wolf, can you please set one of us straight? Can a bank with 1M in customer deposits and no other obligations proceed to loan ~900k, or can it loan ~10M?

My understanding is that 10M can be created and loaned out.

ZeroBrain,

I cannot set anyone straight. But I will ask everyone to quit arguing about it.

Here is my reply:

How much a bank can lend is highly regulated and depends largely on how much “regulatory capital” it has (not deposits), and what the capital ratio required by regulators in that jurisdiction is.

To simplify it to my level (banking regulations are really arcane and give me headache just to think about), if the capital ratio is 10%, and if the bank has $1 million in regulatory capital, the bank can lend out $10 million.

Banks have a banking license, which allows them to lend out more money than they have (but this is limited by the regulatory capital ratio). The sources of this money to be lent out run the spectrum: banks have lots of deposits, and the cost of deposits is currently near zero. So that’s a primary source for many banks. But banks also issue bonds, and they borrow short-term from other banks (less and less these days) and in the markets, and they can borrow from central banks if they have to.

Banks don’t run out of money to lend out. But they can run out of capital. And when push comes to shove, they cannot pay back all their deposits at once (run on the bank). That’s why there has to be a lender-of-last-resort behind every bank (the central bank). This prevents runs on banks even taking place.

Wolf, just one nit:

You say the bank can loan out at 10 to 1 with a 10% reserve ration.

Correctly, the ‘banking system’ can do this, not 1 bank unless there is only 1 bank in the banking system.

Also, another nit, while correctly you stated banks can raise capital, it was not especially clear to some readers that the bank does not magically create the cash it lends. It must either take deposits or borrow it from another bank or from the Fed. The conspiracy nuts all think the deposits appears as if by dark magic.

My explanation above came from a basic ‘money and banking’ class, with poetic license. So many people around the internet, perhaps millions and millions, it seems, fret and bombast about ‘fractional reserve banking’ and none – even those who are considered pros – have any clue what it is or do and use it to sell fear and gold. Thus my ‘I just can’t take it anymore’ attitude and my nits to point out … these people need a dick and jane level explanation to get it. And even then it’s doubtful.

@zerobrain “My understanding is that 10M can be created and loaned out.”

No, only $900k with a $1 million deposit and a 10% reserve ratio. And then prudent risk management needs to be applied. Preferably this cash is in long term deposits, not demand deposits. Otherwise, the bank run scene from It’s a Wonderful Life might happen. The rest of the magic money is just the loan proceeds being spent, deposited,and re-lent over and over again and propagating until it can’t ‘creating money out of thin air’ as the saying goes.

And, yes, the cash in does not have to be from deposits, but those are the most common and lowest cost funds available to a bank. No bank creates money to loan out of thin air unless it prints it in the basement, and only one bank in the US, the Fed, can legally do that.

Big surprise. With tens of thousands of stores closing(not just publicly announced, but many others)orders for goods has to be cratering.

Orders for goods are falls. I own a few online businesses and have seen a slow drop in orders over the past 12 months. Not sure where or when the fix will come but I know for sure consumers are tapped out.

Talking to retailers in our city they are all squeezed with high rents and lower sales volume. This all goes down the chain from restocking to ordering more inventory from the manufactures and wholesalers.

ZH had a data point a week ago or so – which was basically US exports to china are 150 billion. Trump’s first round of tariffs/etc were 50 billion and he instructed the Treasury to put together a plan for bumping that to 100 billion.

China can only retaliate up to … how much?

Don’t get me wrong – this is bad for both sides – but China will feel 600 billion in pain versus the US feeling 150 billion in pain (assuming trade stops which is likely the outcome as soon as China retaliates to the tune of 150 billion or ALL US exports to China).

Granted, some of that trade will carry on at higher prices, but much of it will cease and get sourced elsewhere.

If I had a management position in a company with a Chinese supply chain, I would be looking at early retirement about now …

Regards,

Cooter

The worries are not about the money, its about fragility. Sure, one can source from other manufacturers, but, is it going to be the same “stuff”? Delivery times? Terms & conditions? Does the process need tuning?

Thanks to Globalisation, base materials and chemicals are often produced at the one or two surviving plants that can produce most efficiently, at the lowest margin on the planet. Nobody invest based on conquering a market that is already at the slimmest of margins. They will when markets are good, which is well after “The Crimp” in output.

Back in the naughties a Japanese epoxy manufacturer had a fire. Lost about a years production. Tiny gobs of this epoxy was used on top of silicon chips to seal out moisture and as a conformity layer for the outer epoxy encapsulation. There was an epic rise in the costs of RAM-Devices.

Chip vendors rapidly sourced an alternative epoxy and life went on. Except, it turned out that wasn’t exactly the same “stuff”, it leaked.

Millions of HDD’s failed after about 2 years of use. The pro versions had to be replaced by manufacturers under their extended warranty, while consumers were left stranded, now with an undying hatred for Seagate and Hitachi.

Huge mess. Just over one, trivial bulk-item bought in pallet-size quantities, that wasn’t “fungible” after all!

And, right out of the gate the steel and aluminum tariffs, supposedly aimed at China, hardly impact China. They are number 11 in steel exports to the US.

And the day after Trump announces them his chief economic adviser resigns.

Another thing to bear in mind, before even getting into the grit, almost half of Chinese imports to the US are to markets where US suppliers DON’T EXIST.

These are consumer electronics (27%) and budget apparel including shoes (19%)

The US was out of consumer electronics before China was in.

Last US TV Zenith 1995.

US pushed out by Japan

Now Japan is out, Toshiba exiting TV.

The supplier of the 32 inch flat- panel to the TV assembler is making less profit than a Starbucks latte. This is not a business to chase.

I forced myself to append ‘budget’ to apparel because of course there are always niche makers of cool $ 200 fleeces or duck shoes etc.

Good for them, but the idea that tariffs on Chinese apparel will create US jobs is about as likely as Americans picking their own lettuce.

Google the stories about China transshipping steel and aluminium through other countries, such as Vietnam (where some processing may take place), to the US. Don’t be fooled by how Chinese manufactures play the game.

Well it may be like Solar panels, which say made in America but which are really only assembled in America? The supply lines are dark and deep and I have miles to go before I sleep.

– Nonsense. Blame the new federal tax rules.

– A number of states here in the US have high state and local (income) taxes and these are no longer (or only to lesser extent) tax deductable from federal taxes. It simply means that taxpayers in these states (e.g. New York, New Jersey, California, …….) must pay more taxes to the federal government.

– Similar story for the deduction for interest payments on a mortgage.

– And people are now catching up to this reality. I have heard stories/rumours that California is already losing A LOT OF people who are fleeing to other states.

Do you realize the article is talking about manufacturers in the New York Fed’s district and not consumers and homeowners in California and New Jersey???

-Yes, I know. And what are the other districts reporting ?

I think a whole series of arbitrary and capricious actions by the government may be alarming business. It starts to add up. Rule of law or banana republic?

I would bet that, yes, the tariffs are the big one but it may also be disturbing that the ruling party has it in for your state when it makes law. Will the Feds really bail out failing coal plants? Rick Perry apparently wants to do it. More cronyism and socialized losses. THAT was something this administration claimed to be against, if I remember rightly. the cabinet seems unusually careless with tax dollars. Just like Congress. Our sons and daughters could be forgiven for going for the pitchforks since we are stealing them blind. And not for any public good that might help them.

My point is that I think Wolf has the main, immediate cause. But New York can look at a whole series of laws, including the tax law and the coal support and the killing of that long overdue rail fix up but not limited to those, that look deeply antagonistic.

– An economy is about supply and demand.

– Keep also in mind the taxcuts benefit for say 90% the crporate sector. But how is the corporate sector/the economy going to benefit from these taxcuts when the workers (=demand) hardly see any benefit of these taxcuts ?

– The new taxcode also limits the amount of interest companies can deduct from their income/revenues. Very bad for companies that have large amounts of debt.

– I assume that the corporate sector already sniffs this out in this report.

– No, the more I look at the new taxcode the more I think it will ruin the US economy. And I fear there’s an agenda behind all these tax changes. And I also have an idea what the agenda is.

Could be there be a bigger lag (two months) due to the volatility stock market and threat of the 10yr yield rise way back in February/March, as the reason for the changing the sentiment, rather than the recent trade war spat? Or could it be the last interest rate hike by the Fed? It will be interest to see if the actual number follows through, followed by company forecasts start issuing earnings warnings..

Could this explain why JP Morgan is stockpiling huge quantities of physical silver bullion? What do they know?

They know silver is at historic lows relative to gold, and that logic is flawed to the degree that Silver may outperform Gold, and by a lot, while both are losing value.

Silver is NOT losing value nor is gold They have both traded sideways for a few years now That’s about to change

Raise your hand if you saw this coming a mile away?

With Quantitative Tightening & knock-on effects of an end to stock buybacks and liquidity issues, it is not unreasonable to conclude that

the NYF Manufacturing Survey would deliver the projected slide in confidence. This survey is tantamount to a mass plea for new deals on manufacturing. It’s a major business district and manufacturing base that is stating a projected need for contracts to support their erroneous projections for growth that is absent in an environment of Secular Stagnation.

MOU

For more than a hundred years, U.S. businessmen have been talking about the potential of selling to the China market (“Open Door Policy” etc.). It is a mirage and a deception. The lowering of trade barriers (tariffs) in the trade agreements with China in the Clinton years of the ’90’s was sold to the public as intended to increase U.S. exports to China, and increase U.S. jobs. That was a deception and a Trojan Horse: the real goal was to offshore U.S. manufacturing, and import the products back here with little or no tariff penalties. Exports to China are puny, because China is not interested in buying U.S. products- they want to make their own. China wants to be self-sufficient and sell to their own market – and ours too! U.S. exports to China are only 2% of S&P earnings. Just read the China 2025 paper- China intends to be self-sufficient in aerospace, high tech, software, biomed- everything that the U.S. is currently exporting to China. China dose not want to continue buying U.S. products! But China does want to continue selling to the U.S. market. So a trade war hurts China much more than it hurts the U.S. But the U.S. manufacturers who have offshored their supply chain will then be whacked for bringing their parts back into the U.S. Oh Boo Hoo! Solution: move production back to the U.S.! Support jobs here in our own country for a change. Forget the China mirage. It was never real.

Even the China bulls can’t connect the dots between China’s GDP and a consumer society that sustains their output. The problem with surreptitious change is the rate of change and the fallacy that pulling levers (or raising rates using price control policies) works for more than a short period of time. We all live in the system which came before us, and a new system which began abruptly without any consideration of the long term results. (We make cars before we build highways). The immediate problem (pessimism) is built on a number of conflicting policies that are working against the existing. The system can adapt to new technology, we quickly figure it out, sell the horse, buy a car. (The greatest technological era, the early part of the 20th century was also accompanied by a deep Depression). The changes to policy have no direction or vision, or new technology, they are reactionary (one definition of a Republican). There is no going back

I didn’t realize there still were any manufacturers in the Empire State!

Who are they? What do they manufacture? Who buys their wares? How many are reporting here? How many people do they employ?

If I were paying more for stuff, and not raising my prices, and suddenly getting fewer new orders, I’d be losing my optimism too.

New York is a HUGE state in terms of its economy. The district also includes parts of the New Jersey and Connecticut, in addition to Puerto Rico and the U.S. Virgin Islands.

There are over 15,000 manufacturing firms in the state of NY. This will get you started:

http://www.nam.org/Data-and-Reports/State-Manufacturing-Data/State-Manufacturing-Data/January-2018/Manufacturing-Facts—New-York/

Thanks. Very interesting.