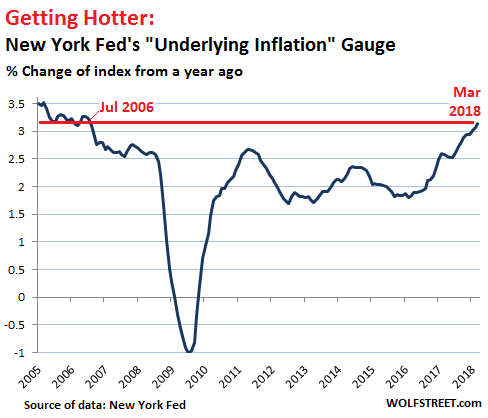

Inflation day didn’t disappoint. “Underlying Inflation” hottest since July 2006.

After the Bureau of Labor Statistics released its Consumer Price Index for March this morning, including a hotter-than-expected (or feared) reading for the core Consumer Price Index – more on that in a moment – several other inflation gauges were released, all based on various ways of analyzing the data pile of the BLS. This includes the New York Fed’s “Underlying Inflation Gauge,” which hit the highest level since July 2006.

Consumer price inflation is in the eye of the beholder. Every household has its own inflation rate, which varies with what their lives look like: medical expenses, kids in college, renting in a city where rents are soaring, etc. No inflation gauge does justice to that particular reality. But they all show nationwide if watered-down trends.

The New York Fed’s Underlying Inflation Gauge (UIG), an index that was first released in September 2017 based on data going back to 1995, comes in two forms that take a broader look at inflation than any of the other indices (detailed list):

The “prices-only” UIG is based on 242 disaggregated price series of the CPI and the Producer Price Index (PPI), import and export prices, and the Dallas Fed’s “Trimmed-Mean 12-month PCE” inflation. This is comparable to a “core” inflation measure.

The “full data set” UIG incorporates all the data of the “prices-only” UIG plus 103 macroeconomic and financial variables.

In March, the “prices-only” UIG rose 2.23% from a year ago, and the “full data set” UIG rose 3.14%. This chart shows the “full-data set” UIG:

The report by the NY Fed summarizes: “The UIG measures currently estimate trend CPI inflation to be approximately in the 2.2% to 3.2% range.”

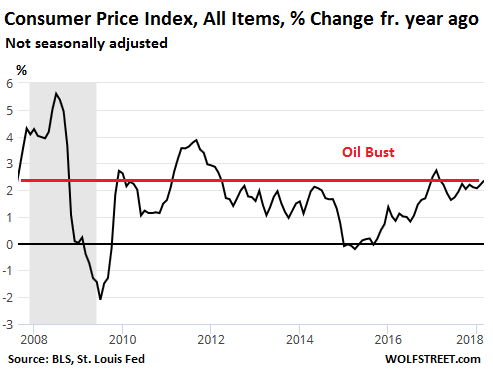

By comparison, the Consumer Price Index for “all items,” released today by the Bureau of Labor Statistics, rose 2.4% in March compared to March last year (not seasonally adjusted). This was the sharpest increase in prices since March 2017:

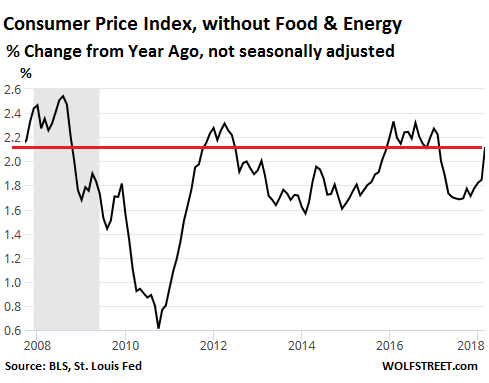

Energy was up 7% from a year ago, with gasoline up 11%, which people have started to notice at the pump. When the all-items CPI surges, it’s usually blamed on food and energy prices, which are volatile. So these prices are eliminated to get a view of “core” inflation. But even core CPI in March rose 2.1% from a year ago, the sharpest increase since February 2017:

The sub-index for “services less energy” – the biggie, with a relative importance of 59% of CPI – rose 2.9% over the past 12 months. It is comprised mostly of various housing costs, including rent and owners’ equivalent of rent, both of which rose 3.3% year-over-year. Transportation services jumped 4.1%. Medical care services rose 2.1%, with hospital services jumping 5.2%!

The Fed looks at a broad range of inflation data. But its target of 2% is based on the core PCE inflation index, which runs roughly in parallel but usually lower than CPI. So with this CPI release, the Fed is getting more data to support faster rate increases.

In the minutes of the Fed’s meeting on March 20-21, released this afternoon, the Fed already warns of a higher 12-month PCE inflation in the March data, as if to prepare the markets not to get spooked. The 12-month comparison will go back to the “low” inflation period a year ago, which had caused so much hand-wringing at the time. That year-over-year comparison could look ugly, and the Fed doesn’t want the markets to overreact. The minutes:

Several participants noted that the 12-month PCE price inflation rate would likely shift upward when the March data are released because the effects of the outsized decline in the prices of cell phone service plans in March of last year will drop out of that calculation.

So 12-month core PCE inflation for March could spike near or above the Fed’s target? Is that what the Fed is warning about? Either way, the Fed is getting “gradually,” as it always says these days, more serious.

The bullishness of retail investors, measured by how they’re actually positioning their investments in their brokerage accounts, has plunged 39% in three months, more than wiping out the spectacular year-long spike that preceded it. Read… Retail Investor Bullishness Bites Dust after Huge Trump Spike

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“Energy was up 7% from a year ago, with gasoline up 11%, which people have started to notice at the pump.”

That may be true, but it isn’t showing up in the vehicles purchased in my area. I suspect that if folks are noticing the increased cost to fill up their Yukon Grandes and top of the line F150s, there is no pain quite yet. At least in that isolated budget item.

In the ongoing conflict in Yemen the Houthis have been attempting to take out tankers with mines and boats. Should they succeed that Yukon is going get real expensive to fill up.

Why? Murica is now producing quite a bit of oil.

US still imports 30-40% of daily needs and World increases in production are flat to declining. Total World petroleum consumption is between 8-10X the rate of new discoveries.

Add to that a shooting war and watch prices skyrocket and economies collapse. There is a reason the US has been making war in the ME for the last 20 years. This is it.

Oil is fungible, in 2015 the law preventing the export of crude from the US was repealed. So oil will find its highest price wherever it is.

I think the pain will be felt at the restaurant level first. Easiest area to cut back on. And if you don’t go out, that’s saves gas too.

We have been here before.

The current Treasury yield spreads (2&10’s, 5&30’s) are the lowest they have been since the Summer of 2007, just before the great recession began. The inflation trend then was about to peak, just as the bubble peaked.

Then the bottom fell out. The Treasury yield spread has mostly telegraphed the coming economic sea changes, throughout the cycles.

Why should this time be different? Its not.

This time the inflation rate has the potential to rise out of control. Something like high inflation with mass defaults at the same time, worse than stagflation. Not possible? We’ll see…

Not sure where I heard it, but someone recently commented that debt has so outrun the money supply that galloping inflation is just not in the cards as cash will be sucked into a black hole of margin and debt payments if the economy tanks. With so much wealth in so few hands, and the velocity of money still sluggish, 1970’s style inflation is very hard to generate. Trillions in liquidity pumped out by the big central banks has barely kept the system afloat and blown a few big bubbles, but the Weimar-level inflation that so many people were screaming about in 2008 simply hasn’t happened. So much for the Friedmanite “inflation is always a monetary phenomenon” dogma. If inflation hits big-time, it will be by deliberate policy, not as an unintended consequence of elite policy.

You have to distinguish between economic inflation, and fed induced inflation. Real interest rates are still abysmally low, and it could be that the Fed will continue to hike rates beyond a corresponding rise in inflation, for purposes which are obvious.

There is inflation, and then there is overall increasing price levels. IMO, three decades worth of industrial, retail, and small business consolidation has bestowed huge pricing power due to the simple fact of vanishing competition. Prices are rising because new business formation is collapsing, competition has vanished, and existing businesses simply can’t or won’t expand due to (a) the inability to find quality employees, and (b) a lack of interest in investing in their core business because speculation pays better than capital assets do.

I fail to understand how creating trillions of FedBux out of thin air and gifting them to the Fed’s Wall Street cohorts to buy up the distressed assets of the proles could ever be inflationary. I mean, the same “print our problems away” monetary policy was implemented by the Weimar Republic, with results that would warm the heart of any Keynesian economist.

Oh, wait….

Um, Weimar policy caused massive inflation within months. We are ten years into massive central bank interventions. Prices are not 10,000% higher and you can still by a hell of a lot with a wheelbarrow full of greenbacks. Obviously, conditions are different and the dogmas of monetarism need revising.

Velocity has fallen — perhaps, by some measures — velocity has collapsed.

From Newton, F = ma

If you’ll allow me to pose an analogy, the force (or maybe the “power” ) of the money in circulation is equal to its mass ( its “quantity” ) times its acceleration ( its velocity ) .

I know I am stretching the analogy just a bit, but the premise seems valid to me .

If you have the mass of money increasing, just as its velocity is dropping at about the same rate, then the “force” ( or effect ) of that money on the economy is rather static.

Velocity has been dropping because the vast masses of people with little money, have been spending less, better put, “spending less frequently” — which is seen in the drop in money velocity.

Watch out when velocity increases, or perhaps reverts to its mean, and the “force” of that money on the economy begins to behave as the monetarists predicted.

Perhaps they had something to say on the effect of money velocity on inflation — I am working now and that inquiry will have to wait.

Exactly. And if one clicks on the Fred M2 Velocity chart, one will see a definite up trend when clicking on the 1 Yr box.

Financialization has funnelled inflation directly into asset markets. Not to mention the fact that some inflation in the consumer markets isn’t being picked up by the common indices. The inflation is there if you look for it. Hiding in plain sight.

In fact it took almost a decade of money printing on an ever escalating scale before hyperinflation conditions began to emerge in Weimar Germany. The uptrend in prices began in 1914, the first year of the war, gradually accelerated between 1918 and 1922 and then went out of control in 1923. This final period during which the paper mark ceased to be a viable medium of exchange definitely did not just drop out of the sky suddenly or without warning.

Since the Markets have been contrary to the FED, won’t they get spooked upon hearing this?

As of this moments, all rates are going up today by a respectable amount. This means savers incomes are going up.

Just think how much income, and spending, savers would be generating today if the Fed had not eviscerated their savings accounts over the past decade. Today would be boom time. But Fed incompetence and support of the Globalist movement created the stagnation we have today, instead. To the good, the Globalists are on the run. Daylight is on the horizon.

The arrival of inflation means rates will keep rising. Hooray! My MM fund is now earning 1.7%, seven day average. Not fantastic from a historical perspective, but a major improvement from as recent as 12 months ago. No capital gains risk. The cash coming off of it is spendable, and I’m spending it. Expect others to do the same and watch the economy expand, mysteriously, while interest rates rise. Just the opposite of what the economics pros predicted.

With rates rising, more income and spending in higher amounts can be expected as time passes. My lifestyle has improved, all due to real inflation and how it affects the cost of funds from the market place, as opposed to the recent past, where money was printed and distributed at deflationary interest rates to favored interests and patrons.

Even better, Goldman has created an online bank with FDIC insured accounts that are paying 1.6% today on essentially passbook savings. Their ad compares what they pay to the pittances the other major banks pay. A competition for funds is on the horizon, I think. Another step towards rate normalization occurs when banks start paying decent interest rates for deposits. I never thought I would say this, but Go Goldman!

And another kick in the pants for the fading Globalists and the crooked economists who covered for them. Bigger Hooray!

1.6 percent is below the rate of inflation.

Look into banks that provide kasasa checking.

Their are banks that are paying 3.5 percent

for checking accounts.

https://kasasa.com

You amaze me. Sneering at a currently superior rate of interest that provides actual spending money just because it isn’t up to some theoretical ideal that only matters to people who are gobsmacked by goofy theories.

3.5% today on passbook savings is high risk, to say the least and to say it politely.

It’s not high risk. The checking accounts are FDIC insured .

If your bank already offers it then you should go for it. However, if not, for most folks it is probably not worth the hassle of changing their checking account.

Here’s the math…

The going FDIC insured online savings accounts rate is about 1.8%.

The highest kasasa rate is 3.5% for the first 10K and that’s for some bank in North Dakota. For most other banks it’s considerably less.

So the difference is about $170 a year. Not sure it’s worth changing checking accounts for that.

First financial out of Arkansas is offering 4 percent. You’re right on the

dollar limits but my wife and I each have an account holding the max.

These are checking accounts and most banks here are still paying less than

1 percent checking. Not going to make a huge difference but once set up

it is better than 1 percent.

Not seeing that 3.5% number, or any numbers for that matter, on yonder website you’ve linkified.

All I do see is a bunch of cute kids on skateboards who I would not trust my money with. Except maybe if they’re selling lemonade.

You sound like a person just came out of the torture room and back into prison and you felt so much better.

If you as a saver start to spend, the debtors start to bleed when they find cost rise every time they roll the loans.

I do NOT know what will happen to the economy. I have my guess.

But please remember, ZIRP hurts saver, inflation hurts saver too. ZIRP helps debtor, inflation helps debtor too. I am a saver but I am conscious about I am getting screwed no matter what. For debtor, you better be the too big to fails or you can drag somebody else big down with you. As a debtor nation, inflation is a dream.

“I am a saver but I am conscious about I am getting screwed no matter what. ”

You get most of it. However, once you see the spendable $$ come rolling in and you actually get a few things you wouldn’t have bought otherwise, the difference between theory and reality goes big.

I’m doing much better now and expect normalization to get things, well, back to normal within a couple of years. Sorry that you would rather see the glass as half full, cracked, and leaking. As long as I’m getting my share, I could not care less about who is getting away with anything else. As long as interest rates rise to livable levels for income generation, the S&P could inflate to 100,000 via central banks and algos for all I care. (Although I do pity those who have to live under ZIRP.)

I feel you man. It does feel better to see your savings grow by 1% while everything goes 3% more expensive comparing to your savings stay the same while everything goes 2% more expensive. That 1% changes all the perceptions. Maybe this is why inflation works.

Even the savers feel good about it since it gets more yield on saved principle. Debtors feels good, savers feels good, government collecting tax on those yield also feels good. Hmmmmmm.

Anyone ever wonder how the Fed is able to manage inflation within a 3 % bound? I mean, if you really understand inflation, you realize there are numerous variables that contribute/detract from an increase in the money supply as well as other economic and social factors that play a part.

Just asking becasue we all seem to believe these numbers almost regiously.

I think they are all engineered to make the Fed look like it’s in control. Not perfectly in control of course; thus the variation. But I’m not convinced they can engineer inflation at this steady of a rate.

Thoughts/opinions?

It all starts with the mainstream news media who prints what they’re told to print and goes downhill from there. Business and economics reporters are as bad as any other reporter, probably worse. They cover economics like the NY Times and Washington Post cover current events, only their readers need a lot of info to be dumbed down for popular consumption. From there, readers become cattle.

Schools that teach economics come next. Economics, as a field of study, is more theology than science. Math just makes it look legitimate.

The Fed is a product of that environment. As long as rates continue to normalize, they may receive redemption for the past decade of misery they inflicted by keeping rates too low for too long.

Maybe that’s why they use arcane methods for computing inflation. It gives them the ability to manipulate the numbers, just like corporations manipulate their EPS numbers to meet targets.

The biggest item in the basket is living costs, and the method for computing inflation on that is ridiculous. Then you have the hedonic adjustments, which allows the Fed to adjust reported inflation at will.

People at the Fed (at all the major central banks, really) have two examples of action in their heads that define the bounds of their thinking: Volker’s chocking inflation by tanking the economy in 79-81, and Bernanke turning on the fire hose of liquidity in 2008-9. From their elite perspective, both of these policies were big-time successes, as they were great for the owners of money. The fact that the first had long-term deleterious effects on the middle class and heralded both financialization and deindustrialization means nothing to them. The fact that the latter made the investor class whole why the rest of society stagnated or rotted also doesn’t show up on their radar. So the central bankers remain convinced that they can control inflation and reboot a collapsing economy at their whim.

Volcker had no choice. Inflation was not going to go away by itself.

These central bank policies have virtually ruined 80+ % of the plebs assets, leaving them to founder …

The ONLY thing the Banking Fraudsters will understand, is when the tumbrils be seen on the horizon !

If one is going for official numbers that are “Unbelievable” might as well look seriously at these, as an alternative. http://www.chapwoodindex.com/

I think the interest rate changes are fairly well bounded for a number of reasons. First, they cut out items they consider too volatile (food & energy). They also totally ignore financial assets where most of the money goes. Owner-equivalent rent is also a large fudge number giving leeway.

Also, it’s interesting how they use a chained CPI to reduce the inflation when people switch to lower quality goods in response to higher prices (more chicken, less steak is a common example though food is excluded) , while creating hedonic adjustments to technology items in order to create deflation that doesn’t necessarily exist (new iPhone costs $800, but it has better specs than last version so the price is adjusted down even though functionality is little improved and cheaper alternates don’t suddenly appear).

I need to review spelling before posting .

“Markets panic?”

I think the markets are still in the middle of a roaring bull market, with no end in sight. Remember North korea? Not even a wince of concern from the market!

And now we stand on the brink of WWIII with Syria and Russia (over nothing) and again the market only yawns.

They fail to realized ‘The Donald’ may launch WWIII to derail that Meuller investigation.

Computers must account for 90% of all trading today as sane people would have sold long ago.

https://davidstockmanscontracorner.com/the-deep-state-closes-in-on-the-donald-part-1/

(Interesting that I had to go through a proxy to gain access to the above link)

Fed raises rates: Inflation rises

Fed says, Look inflation is rising, we better raise rates

Rinse and repeat

Back in the real world, the tax cuts hit paychecks in February as did tax refunds. The parking lots in most malls I go to were packed from late February thru March. The spike in inflation in Feb/Mar is probably from increased spending, which had been suppressed, until money started hitting the wallets of deplorables.

A significant part of my increased income was quickly siphoned off by increased car insurance, and other recurring cost increases. Even so, I still had some left over money to spend. I expect to have a few more dollars until the fed comes up with a reason to siphon off the rest. Considering how manipulated most markets are now, how could the inflation rate not be as well.

That tax refund money is already spent. In a service economy the word of new money spreads and everyone down the line is waiting for you. I have noticed the hispanic service workers always seem to know when to raise their rates, and they are doing pretty well.

So with that in mind, even increasing the minimum wage 2X is pointless if prices also double down the line. Not to mention putting a few more small businesses out of business in the short run. What good is getting your pay doubled only to pay all the extra $ for the exact same expenditures? Or worse, you lose your job? Big companies speed up increased investment in lobbyists and robotics, etc. And even more people begin to want that “living wage” that Zuckerburg and others among today’s intelligentsia want so desperately.

Being dead economically aint much of a living.

No actually raising the minimum wage has the effect of putting wage pressure on at the lower end. Service workers who have pricing power are often in the cash economy, which means their wages go up, while traditional employees (who often belong to labor unions) do not. The service industry is somewhat immune to robotic job replacement, this part of the economy is allowed to function normally, outside the reach of corporate robber barons and financial repression, there is inflation.

Ambrose, so service workers get our new/extra money we received from the tax cut, but would not get it from lower wage workers who had their wages increased? Hmmm, i am missing something.

Inflation is welcomed by those who plan for it. I have four mortgages. Let’s stoke the inflation fires!!

Inflation in an economy where employment is expanding might save you, assuming your income is expanding faster than inflation, a rare occurrence. Otherwise you are at the mercy of an even more impoverished consumer who can’t afford to buy your homes or rent them, a more likely scenario.

About a year before the meltdown in Florida, I read a profile of a worker earning $32K who had flipped his way to a $500K house. Two years later, the economy in the area would have wiped him out and then some.

You will only benefit from this inflation if it drives up RENTS in your city. If it just drives up the costs of healthcare, energy, tuition, apparel, telecommunications, municipal services (water, garbage), etc. etc., but not rents in YOUR city because the market is oversupplied, you will not benefit. Instead you might get hurt.

Thinking about how to win with inflation is a complex matter.

The amount of cash in circulation is so extreme that it is inconceivable that the cost of money should be rising . Trillions of dollars have been created under the QE theory, globally supplied, and that implies that, central banks are at-risk, essentially of failing credits issued to the well-heeled, and diminished money values, which will be the shock absorber that soaks up the losses of this speculative binge. The safest place in this status quo is in commodities, provided that one can places trust in the markets. When the readjustment of accounts comes, no investment will be safe. Especially not the money market in your 401k. Best bet is to pay off your mortgage so when the big chill comes, you will at least have a roof over your head, if not a job.