Update on the 100 most expensive cities. A story of deep-red and big surges.

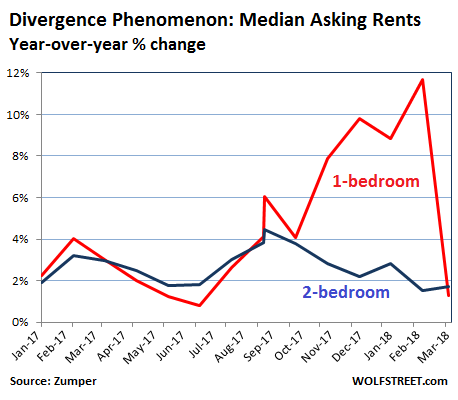

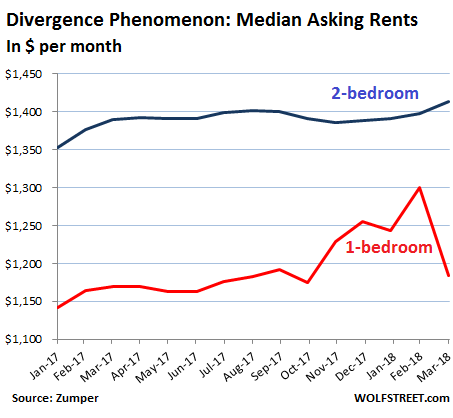

The peculiar phenomenon that started last November was this: One-bedroom median asking rents in the US were skyrocketing in the double-digits, even as two-bedroom rents were barely ticking up and remained below the rate of inflation – nearly unheard of in recent years. But it seems the final paroxysm was in February, when one-bedroom rents had shot up 11.7% year-over-year to $1,300.

In March, the median 1-BR asking rent plunged 9% on a monthly basis to $1,184 to where it was up only 1.3% year-over-year. The median 2-BR asking rent rose only 1.7% from a year ago to $1,414. Whatever the reasons had been for this divergence between the red-hot growth of 1-BR rents and the tepid growth of 2-BR rents – there were several contenders – it’s over:

The data, provided by Zumper, is based on asking rents in multifamily apartment buildings, including new construction, as it appeared in active listings in cities across the US. Single-family houses and condos for rent are not included. Zumper releases the data in its National Rent Report.

The most expensive markets cool off.

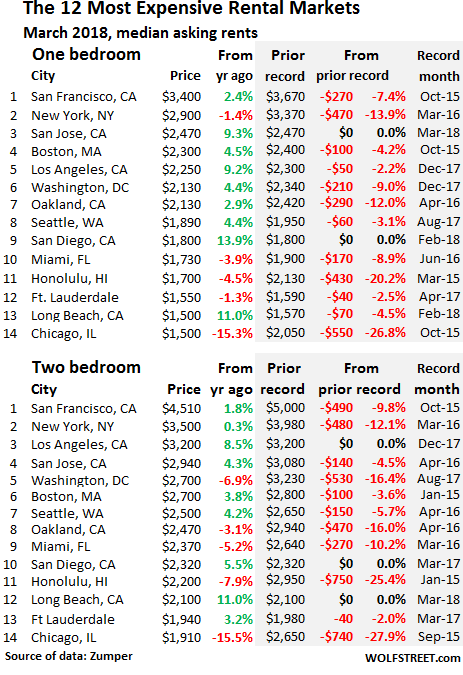

In the most ludicrously expensive major rental market in the US, San Francisco, the median asking rent for 1-BR apartments rose 2.4% year-over-year to $3,400 in March, but was down 7.4% from the peak in October 2015. For 2-BR apartments, the median asking rent rose 1.8% year-over-year to $4,510 but was down 9.8% from the peak in October 2015.

There is no housing shortage in San Francisco. For example, Zillow lists 1,581 apartments for rent, a 38% jump from the 1,149 apartments Zillow had listed in August 2016. This is a result of the construction boom. Note that there are only 386,755 total housing units in San Francisco (it’s not a big city). But almost all the new construction is high-end, most of the units on the market are too expensive, and people cannot afford them. Hence the local term, “Housing Crisis” – a crisis not of availability but of price.

In the second most expensive major rental market, New York City, the median asking rent for 1-BR apartments edged down 1.4% year-over-year to $2,900 and is down 13.9% from the peak in March 2016. 2-BR apartment rents edged up 0.3% to $3,500 but are down 12.1% from the peak in March 2016.

These median asking rents do not include incentives or “concessions,” such as “1 month free” or “2 months free,” which reduce the effective rent for the first year by 8% or 17%. Concessions have appeared in San Francisco and have reached record levels In New York City.

The table below shows the 14 most expensive major rental markets. The shaded area shows peak rents and the movements since then. There are now a number of double-digit declines from their respective peaks:

Formerly red-hot Seattle is perhaps a prime example of a phenomenal housing construction boom that went all high-end with no place to go. Rents seem to have hit a ceiling in 2016 or 2017.

Chicago is worrisome. Its place on this list above has plunged from eighth in September 2016 to 14th now, in line with the free-fall in rents that now approaches 30% from the peak in late 2015.

Rents in Honolulu might be groping for a bottom. The declines seem to have slowed down, though this could just be another blip, with sharper declines to follow.

There are three Bay Area cities on the above list. Rents in two of them (San Francisco and Oakland) are significantly down from the respective peaks. Oakland serves as escape for SF housing refugees, and rents had surged over the past few years, but now 1-BR and 2-BR rents have dropped 12% and 16% from their peak. In San Jose, however, 1-BR rents set a new record in March, but barely, and are down only 4.5% from the peak.

There are three Southland cities on the above list – Los Angeles, San Diego, and Long Beach. And rents in all three of them have been setting new records.

Across the country, every market is different, and the national average glosses over the surges and plunges – often in the double digits. And there is some real drama going on in the less expensive markets. The percentages are based on year-over-year (Y/Y). Use the search function in your browser to look for a specific city in Zumper’s list of the 100 most expensive rental markets:

| City | 1 BR Rent | Y/Y % | 2 BR Rent | Y/Y % | |

| 1 | San Francisco, CA | $3,400 | 2.40% | $4,510 | 1.80% |

| 2 | New York, NY | $2,900 | -1.40% | $3,500 | 0.30% |

| 3 | San Jose, CA | $2,470 | 9.30% | $2,940 | 4.30% |

| 4 | Boston, MA | $2,300 | 4.50% | $2,700 | 3.80% |

| 5 | Los Angeles, CA | $2,250 | 9.20% | $3,200 | 8.50% |

| 6 | Oakland, CA | $2,130 | 2.90% | $2,470 | -3.10% |

| 6 | Washington, DC | $2,130 | 4.40% | $2,700 | -6.90% |

| 8 | Seattle, WA | $1,890 | 4.40% | $2,500 | 4.20% |

| 9 | San Diego, CA | $1,800 | 13.90% | $2,320 | 5.50% |

| 10 | Miami, FL | $1,730 | -3.90% | $2,370 | -5.20% |

| 11 | Honolulu, HI | $1,700 | -4.50% | $2,200 | -7.90% |

| 12 | Fort Lauderdale, FL | $1,550 | -1.30% | $1,940 | -2.00% |

| 13 | Chicago, IL | $1,500 | -15.30% | $1,910 | -15.50% |

| 13 | Long Beach, CA | $1,500 | 11.10% | $2,100 | 11.10% |

| 15 | Philadelphia, PA | $1,470 | 6.50% | $1,640 | 3.10% |

| 16 | Atlanta, GA | $1,430 | 7.50% | $1,840 | 9.50% |

| 17 | Denver, CO | $1,400 | 15.70% | $1,910 | 13.70% |

| 18 | Minneapolis, MN | $1,390 | 3.00% | $1,850 | 12.80% |

| 19 | Providence, RI | $1,380 | -0.70% | $1,440 | -2.70% |

| 20 | Portland, OR | $1,370 | 2.20% | $1,590 | -0.60% |

| 21 | New Orleans, LA | $1,360 | 0.00% | $1,410 | -6.60% |

| 22 | Baltimore, MD | $1,320 | 14.80% | $1,520 | 15.20% |

| 23 | Nashville, TN | $1,310 | 7.40% | $1,440 | 9.10% |

| 24 | Dallas, TX | $1,300 | -1.50% | $1,760 | -1.70% |

| 25 | Houston, TX | $1,290 | 12.20% | $1,630 | 14.00% |

| 25 | Scottsdale, AZ | $1,290 | 2.40% | $2,010 | -8.20% |

| 27 | Madison, WI | $1,200 | 4.30% | $1,360 | 7.90% |

| 28 | Orlando, FL | $1,180 | 15.70% | $1,390 | 15.80% |

| 29 | Sacramento, CA | $1,170 | 9.30% | $1,400 | 11.10% |

| 30 | Austin, TX | $1,160 | 10.50% | $1,450 | 9.00% |

| 31 | Charlotte, NC | $1,150 | 0.00% | $1,290 | 1.60% |

| 32 | Irving, TX | $1,140 | 6.50% | $1,540 | 12.40% |

| 32 | Tampa, FL | $1,140 | 14.00% | $1,340 | 9.80% |

| 34 | Aurora, CO | $1,120 | 9.80% | $1,410 | 3.70% |

| 34 | Plano, TX | $1,120 | 5.70% | $1,500 | 4.90% |

| 36 | Virginia Beach, VA | $1,090 | 16.00% | $1,200 | 4.30% |

| 37 | Gilbert, AZ | $1,070 | 5.90% | $1,330 | 3.10% |

| 38 | Fort Worth, TX | $1,060 | 11.60% | $1,260 | 14.50% |

| 39 | Chandler, AZ | $1,050 | 10.50% | $1,250 | 8.70% |

| 39 | Newark, NJ | $1,050 | 14.10% | $1,250 | 6.80% |

| 39 | Pittsburgh, PA | $1,050 | 1.00% | $1,280 | -1.50% |

| 39 | Richmond, VA | $1,050 | 7.10% | $1,210 | 10.00% |

| 43 | Chesapeake, VA | $1,040 | 14.30% | $1,200 | 4.30% |

| 44 | Durham, NC | $1,030 | 10.80% | $1,170 | 13.60% |

| 44 | Henderson, NV | $1,030 | 6.20% | $1,200 | 7.10% |

| 46 | Salt Lake City, UT | $1,020 | 15.90% | $1,260 | 9.60% |

| 47 | Raleigh, NC | $1,010 | 0.00% | $1,170 | 1.70% |

| 48 | Buffalo, NY | $990 | 10.00% | $1,150 | -8.70% |

| 49 | St Petersburg, FL | $980 | 14.00% | $1,620 | 14.10% |

| 50 | Kansas City, MO | $960 | 4.30% | $1,040 | 11.80% |

| 51 | Phoenix, AZ | $950 | 9.20% | $1,140 | 8.60% |

| 52 | Jacksonville, FL | $930 | 9.40% | $1,050 | -2.80% |

| 53 | Las Vegas, NV | $910 | 15.20% | $1,050 | 11.70% |

| 54 | Baton Rouge, LA | $900 | -1.10% | $940 | -1.10% |

| 54 | Fresno, CA | $900 | 5.90% | $1,050 | 10.50% |

| 56 | Mesa, AZ | $880 | 11.40% | $1,010 | 3.10% |

| 56 | Milwaukee, WI | $880 | 10.00% | $990 | 15.10% |

| 56 | San Antonio, TX | $880 | 6.00% | $1,140 | 5.60% |

| 59 | Boise, ID | $870 | 7.40% | $950 | 2.20% |

| 59 | Colorado Springs, CO | $870 | 10.10% | $1,050 | 0.00% |

| 59 | Louisville, KY | $870 | 8.70% | $950 | 13.10% |

| 62 | Anchorage, AK | $860 | -5.50% | $1,100 | -4.30% |

| 62 | Corpus Christi, TX | $860 | 8.90% | $1,070 | 11.50% |

| 64 | Syracuse, NY | $850 | 13.30% | $930 | -2.10% |

| 65 | Cincinnati, OH | $830 | 12.20% | $1,070 | 11.50% |

| 65 | Omaha, NE | $830 | 13.70% | $970 | 7.80% |

| 67 | Rochester, NY | $820 | 15.50% | $1,000 | 13.60% |

| 68 | Reno, NV | $800 | 14.30% | $1,170 | 15.80% |

| 69 | Laredo, TX | $790 | 8.20% | $940 | 9.30% |

| 70 | Arlington, TX | $770 | 10.00% | $1,020 | 10.90% |

| 70 | Chattanooga, TN | $770 | 10.00% | $810 | 12.50% |

| 70 | Knoxville, TN | $770 | 14.90% | $870 | 13.00% |

| 73 | Bakersfield, CA | $760 | 10.10% | $890 | 6.00% |

| 73 | Des Moines, IA | $760 | 1.30% | $800 | -1.20% |

| 75 | Glendale, AZ | $750 | 7.10% | $900 | 2.30% |

| 75 | Lexington, KY | $750 | -6.30% | $940 | 1.10% |

| 75 | St Louis, MO | $750 | 10.30% | $1,060 | 11.60% |

| 78 | Cleveland, OH | $730 | 15.90% | $800 | 14.30% |

| 78 | Norfolk, VA | $730 | 10.60% | $930 | 3.30% |

| 80 | Augusta, GA | $710 | 14.50% | $790 | -1.30% |

| 80 | Spokane, WA | $710 | 7.60% | $900 | 8.40% |

| 82 | Tallahassee, FL | $700 | 11.10% | $830 | 6.40% |

| 82 | Winston Salem, NC | $700 | 1.40% | $760 | 8.60% |

| 84 | Greensboro, NC | $680 | 13.30% | $810 | 5.20% |

| 84 | Indianapolis, IN | $680 | 15.30% | $760 | 11.80% |

| 84 | Oklahoma City, OK | $680 | 11.50% | $820 | 5.10% |

| 87 | Columbus, OH | $670 | 3.10% | $1,000 | 5.30% |

| 87 | Tucson, AZ | $670 | 11.70% | $820 | 2.50% |

| 89 | Memphis, TN | $660 | 13.80% | $720 | 14.30% |

| 90 | Albuquerque, NM | $630 | 5.00% | $800 | 5.30% |

| 90 | El Paso, TX | $630 | -1.60% | $770 | 0.00% |

| 92 | Lincoln, NE | $610 | -9.00% | $810 | 0.00% |

| 92 | Shreveport, LA | $610 | 5.20% | $650 | 1.60% |

| 94 | Tulsa, OK | $600 | 5.30% | $750 | 2.70% |

| 94 | Wichita, KS | $600 | 15.40% | $690 | 4.50% |

| 96 | Akron, OH | $590 | 11.30% | $700 | 4.50% |

| 96 | Lubbock, TX | $590 | 1.70% | $750 | 7.10% |

| 98 | Detroit, MI | $560 | 3.70% | $630 | -3.10% |

| 99 | Fort Wayne, IN | $540 | 12.50% | $610 | 10.90% |

| 100 | Toledo, OH | $530 | 15.20% | $640 | 14.30% |

Where are the Most Splendid House Price Bubbles in the US? City by city, with some flat spots disappearing, new ones forming. Read… Update on the Most Splendid Housing Bubbles in the US

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Million-dollar rehab is listed down the block from me in Seattle, across the street from a halfway house. Dick’s Drive-In and a very good Value Village are also nearby. Value Village has a copy of the excellent “Margin Call” in the DVD section tonight, if you can snag it in time.

https://www.seattlegroupre.com/

This is Crown Hill, not Ballard.

There is a ton of supply coming online in downtown Denver over the course of the next year or two. Several massive projects. In addition, i am aware of several recently completed projects in Lodo and Uptown offering incentives including free month(s) rent and $500 gift cards. For rent signs all over the place. But to confirm your research most would be considered luxury projects in the Denver market.

I think legally you can have two people per bedroom. What you do is, you put in two bunk beds. The people sleep on the top bunk and the bottom bunk is made into a “cubicle” with small desk, chair, etc. so they have some personal space. It’s amazing how much of a difference it makes.

Extra-legally, you can probably put 3 setups like this in each room and have it work out OK. It helps if the people come from large families, have gone to boarding schools, been in the military etc.

My son is with 4 others in a 3br, works on a day to day basis if you have agreed upon rules, thick skin, and somewhere to get the hell out of town to on the weekends. Also nice if it provides the opportunity to save some $$$ for that pretty much fairy tale dream of being able to afford to buy. Nothing lasts forever – when this shit goes down, it’s going down hard.

Wolf, is there no data available for Orange County, CA – population 3.1 million? I ask because it is a very different market than LA, yet you have data for Long Beach (population 460k) and many smaller cities.

Yes, I can see how that happens. That data is pulled by city, not by county. So the county seat of Orange is Santa Ana, which is pretty small. And Anaheim is pretty small too. Etc.

I’ll ask them to see if they can pull up the Orange County data for my next report.

The larger OC cities have a higher population than many on your list. According to Google, the 2016 population for:

1. Anaheim – 351,000

2. Santa Ana – 334,000

3. Irvine – 266,000

4. Huntington Beach – 201,000

That said, there are significant differences in the coastal and inland OC rental markets, but Irvine is generally used as a proxy OC as a whole. My point of reference is Jonathan Lansner in the OC Register, who writes daily on OC’s real estate markets.

I’ve now asked. Thanks for bringing it up. This is really a pretty big void.

BTW, my comment above notwithstanding, yours is one of the BEST financial sites on the unbiased and informed analysis.

“most of the units on the market are too expensive, and people cannot afford them.”

This is what happens when sellers want the moon and do not budge since they have been conditioned to expect it. “House prices never go down” Bernanke was under the same illusion pre-2007.

And why not when the housing bust of 2008 has been fully reversed and then some. After all the Fed has their back covered! Let us see how this movie ends.

I hope this time people get the fact it is the Fed that is responsible for this by playing hanky panky with interest rates, bailing out banks with free money and buying up bonds at will.

“I hope this time people get the fact it is the Fed that is responsible for this by playing hanky panky with interest rates, bailing out banks with free money and buying up bonds at will.”

You have to wonder if it ever will happen, as the MSM is resolutely dedicated to keep people in the dark: whenever you see “The Fed”, think “The banks that own the Fed,” and then perpetual zero% interest rates (or better yet, negative interest rates- for them, not you, who still get to pay 20+% on the bank cards they issue) makes perfect sense, as will the fact that when they talk about “tightening” they mean as little change as humanly possible

Totally agree. The 20% plus rates on bankcards is an outrage

and so is the reluctance to report it by mainstream TV news.

“the trend of media conglomeration has been steady. In 1983, 50 corporations controlled most of the American media, including magazines, books, music, news feeds, newspapers, movies, radio and television. By 1992 that number had dropped by half. By 2000, six corporations had ownership of most media, and today five dominate the industry: Time Warner, Disney, Murdoch’s News Corporation, Bertelsmann of Germany and Viacom.”

Quoted from PBS source, or just do a google search about the billionaires who own the media.

There was also an article in the NYT about the increasing control billionaires have over media as they buy them up.

Dave P, or here…

https://wolfstreet.com/2018/02/20/why-do-billionaires-keep-buying-us-newspapers-despite-their-terrible-future-as-buffett-said/

Low interest rates resulted in a boost to Real Estate values while keeping the average loan payment ‘affordable.’

Municipalities get the majority of their revenue from property taxes mil rated to those values.

http://www.taxpolicycenter.org/statistics/local-property-taxes-percentage-local-tax-revenue So this has been a boon for local revenues.

What will be the impact of higher interest rates and inflated property values be on this dynamic?

It’s my personal view of course; but I think the big boys have unloaded most of the assets that they wanted unloaded to Joe plumbers. Now, it is time to crash the market, and buy back the same assets at pennies on the dollar. So, I think you’ll get your wish within the next 2 years.

Toledo is NICE this time of year

Frederick,

Spain or Ohio?

Hummm……………. For one bedroom units there is zero change shown for two communities, San Diego and San Jose. We see many of these units now being occupied by multi generational families or multiple non related groups in order to cover the costs. Homes in my area (SD) are too expensive for most folks so a ‘single family’ rental becomes a overnight haven for two, or even three generations, uncles, cousins, etc. Same with apartment rentals. Lots of multi family units are being built in the San Diego area but I doubt it will help much as a result of land and development costs. I’m still on the side of a complete re-set of all this starting soon.

People say San Diego has lack of inventory

I see lot of homes to choose from if you have a million dollar plus

I don’t see this as lack of inventory but shortage of affordable inventory

You can get a decent house in so cal for 750-800k. You don’t need 1mil.

I remember a time when $175,000 for a 20 year old home, was considered high….30 years ago in Calif.

Same for the Boston area. Lots of 1 million + houses for sale. Recently a house sold for over 2K in sleepy, formerly blue collar Arlington, MA which is the now the new Cambridge. Most people I talk to who “own” here do not believe prices will come down, will only go up. Local newspaper articles also concur with continual price increases and ongoing relentless demand, thus no end in sight. Traffic is getting worse by the day with new “luxury” construction on seemingly every street corner. Surrounding towns, once considered gritty, undesirable areas are now “hot” with uber inflated prices due to low inventory and oh yeah, new “luxury” apartments. Rents are also up from what I can tell.

For a longtime renter who has to find a new place to live and was hoping to buy, it is not a fun situation. The question is: do you wait it out and hope for a “correction”, or bite the bullet? It feels like buying now would be close to the top of the market. Yet, if you don’t buy now, will you be “priced out forever?” Sure seems that way and my neighbors all agree.

Gee whiz, is everyone making 200K+ around here? Apparently not everyone. I remember reading an article in the Boston Globe from 2016 that nearly half of Boston residents make less than $35,000 a year. My entire family is here including my elderly mother so sadly, I can’t pack up and move to an oasis like Toledo.

What about New Hampshire? Or Maine? It’s not that far away. Maine has some friggin awesome deals. Houses for under 20K.

I can’t believe you an get a one bedroom in Toledo for $530. You could probably live solely on social security and live there.

Actually you could buy a house in Toledo for about $500/ mo mortgage. Not luxury, but quite liveable and even with a yard and garage. Check out Zillow.

There are so many pleasant small cities around the country – many within an hour or so drive of larger cities, if one needs something more occasionally – where the cost of living is far, far below these major cities. I think best of all worlds would be working remotely for a big company while living in a small town like this.

Live in an area that has been in a housing boom going on 18 years. 2007 crisis had virtually no impact locally. Large apartment buildings going up all over the place. Zumper provides average rates on both 1 & 2 bedroom rentals that would put my community at 63rd on the list. Yet it is nowhere on the list. What numbers should I believe, Zumper’s or Zumper’s?

Just reading the numbers posted for most of the “popular” areas is truly scary considering the depressed wages that most young people will face in the immediate future, let alone the retirees that were raped in the 2008 market crash and have not really recovered. I know that times change but these numbers are ridiculous! I have grandchildren both in San Jose and San Francisco; I was born and raised in SF and it’s unrecognizable today. Two level “flats” are yielding upwards of $5-$6,ooo month from renters.

If this second housing bubble pops, I’m not sure if that will effect rents. People losing their homes and being forced to move to an apartment may actually cause rents to rise, even as house prices fall.

If housing prices fall, buying becomes more appealing and other people get in at those lower prices. The housing stock doesn’t change – just ownership of it. The issue you mention is self-correcting in the medium term.

Also, you can just look at the historical record. Rents decreased in the immediate aftermath of the housing crash.

In sheer dollar amounts Denver is still cheaper than San Francisco or Silicon Valley; however, when incomes are factored something doesn’t add up and hasn’t been adding up for the last 4-5 years.

Will Denver eventually experience a correction–prices rising faster than incomes is unsustainable, at least in a “normal” market–or is Denver becoming the Bay Area, just with mountains, instead of beaches and ocean?

I guess time will tell.

Denver is going to be an interesting market to watch over the next few years. To be fair, there has been strong in-migration here over the last 5 years. But good grief, so many people here are SOOO confident that their home values are on the way to the moon. The confidence scares me a little bit. Personally, I’m not so confident. I think the right (wrong?) combination of circumstances could easily cool this market off.

“But, but, there’s no inventory! Lending standards are tighter now!”

Everyone’s talking about supply, but let’s not forget that supply doesn’t exist in a vacuum separate from demand. What would demand (and therefore supply) look like if rates had been closer to 6% over the last three years? If there aren’t enough homes/condos on the low end (where supply is tightest), could that be partly because the existing owners in those homes don’t have the means to move up into something nicer in this economy/market? Some folks are scared to sell their homes because they’re afraid they won’t be able to find something they like and successfully buy it. This in turn has also put downward pressure on supply. What if that dynamic changed somehow?

I have a half-baked theory that the right combination of factors involving the rental market could be key to causing a slump in housing prices in Denver’s market (and maybe others). The theory goes something like this:

1. A recession hits just as it does every 10 years or so. This could coincide with a “bust” in tech and higher fuel prices.

2. With job losses and general economic malaise, enough renters (who’ve been paying out the nose these last few years and saved little) consolidate their living arrangements. Some of the midwestern 20-somethings in Denver move back home to mom and dad’s basement. Friends move in together. The key point here is that rental *demand* could contract significantly.

3. Many property owners, who’ve grown to feel entitled to high and ever-increasing rents, find themselves having a difficult time renting out their homes/units at the price listed. Even a non-leveraged property isn’t great to have if it isn’t generating any cash flow.

4. With prices still [relatively] high, it becomes too tempting to cash out, and many property owners do.

5. To make things more interesting, some owners of newly-built apartment buildings may be pushed to convert their units to condos if they’re not getting the rental revenue they projected. This could put more downward pressure on prices.

6. Add in some serious drought problems and a change in the cannabis situation (marijuana becomes legal everywhere, or the feds crack down on it everywhere), and all of the sudden Denver isn’t the paradise that all the Illinois transplants thought it was.

Will all of the above happen? Probably not. And if Initiative 66 gets on the ballot and passes this fall, then Front Range prices will be artificially supported into the future. I hope that doesn’t happen.

adjusting for new construction, subsidies, etc …..don’t see it.

but yes, supply is impinging……

I really disagree with the numbers for San Jose; San Jose YoY, even for one bedroom is down and not up; there is no way in hell that rents in San Jose are increasing. Some property manager are stupid enough to increase the rent of the existing tenants reasoning that moving is difficult and the tenants will pay, but eventually they lose a lot of tenants since there are better and cheaper apartments on the market. And if the number for San Jose is totally wrong, what other numbers from Zumper are wrong?

Real Estate industry obviously has the incentive to keep the perception that rents are increasing, or at the least are not decreasing. If people have the perception that rents are increasing, then they can be blackmailed into paying higher rents and higher property prices. People should look at the reality on the ground and not the numbers that these zombies generate.

Exactly. Zillow seems to be in the same business of ‘predicting’ higher rents, which are then used by landlords to ask for the higher rents. Sometimes they get the rents. But they also get more tenants than they thought they were getting. Free parking spaces become scarce and the place is crowded. I guess this is how some cities end up getting the ghetto tag from being sought after places.

Other times, the rents come down and Zillow will not have information about how much the place rented out in the end.

Rents continue to soar in the north bay, no thanks to the fires.

A little caveat: It’s VERY misleading to comfabulate NYC with Manhattan. It’s not said I know but implied. Manhattan below 110th street and the rest of NYC are worlds apart.

And Manhattan is way more expensive than SF.

That said the building boom of the west side of the city (the city means Manhattan in NYC) has created a surplus of very expensive rentals still being built. The situation on the ground is WORSE than your stats. You can get 2 months free just for asking, and no broker fee are a given. When it’s all said and done we’re facing some greatly inflated prices.

I’ll just give you an example:

I live in Chelsea, west Manhattan, very gentrified. Next to me was developed a rental tower. When you visit they show you a plan with “a few units left” , studio 3000, 2 bed with terrace 8000. from my place I can see the back of the building, and at night it’s mostly dark….maybe 1/3 full. There’s dozens like that being built, all luxury . Nonsense.

Why would anyone want to live in San Francisco gridlock for $4500 per month when they can live in Honolulu and walk to the beach for $2200?

I would take a very hefty stock option package with a clear path to getting the hell out for me to make that choice.