Fed’s monetary policy shift is finally taking hold. It just took a while.

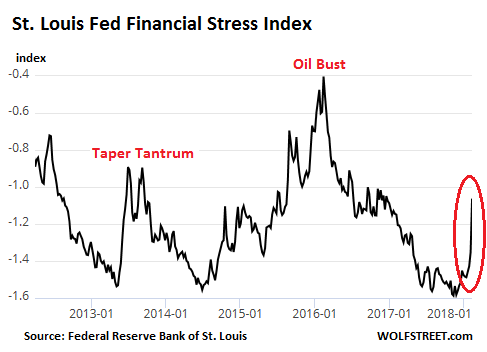

The weekly St. Louis Fed Financial Stress index, released today, just spiked beautifully. It had been at historic lows back in November, an expression of ultra-loose financial conditions in the US economy, dominated by risk-blind investors chasing any kind of yield with a passion, which resulted in minuscule risk premiums for investors and ultra-low borrowing costs even for even junk-rated borrows. The index ticked since then, but in the latest week, ended February 9, something happened:

The index, which is made up of 18 components (seven interest rate measures, six yield spreads, and five other indices) had hit a historic low of -1.6 on November 3, 2017, even as the Fed had been raising its target range for the federal funds rate and had started the QE Unwind. It began ticking up late last year, hit -1.35 a week ago, and now spiked to -1.06.

The chart above shows the spike of the latest week in relationship to the two-year Oil Bust that saw credit freeze up for junk-rated energy companies, with the average yield of CCC-or-below-rated junk bonds soaring to over 20%. Given the size of oil-and-gas sector debt, energy credits had a large impact on the overall average.

The chart also compares today’s spike to the “Taper Tantrum” in the bond market in 2014 after the Fed suggested that it might actually taper “QE Infinity,” as it had come to be called, out of existence. This caused yields and risk premiums to spike, as shown by the Financial Stress index.

This time, it’s the other way around: The Fed has been raising rates like clockwork, and its QE Unwind is accelerating, but for months markets blithely ignored it. Until suddenly they didn’t.

This reaction is visible in the 10-year Treasury yield, which had been declining for much of last year, despite the Fed’s rate hikes, only to surge late in the year and so far this year.

It’s also visible in the stock market, which suddenly experienced a dramatic bout of volatility and a breathless drop from record highs. And it is now visible in other measures, including junk-bond yields that suddenly began surging from historic low levels.

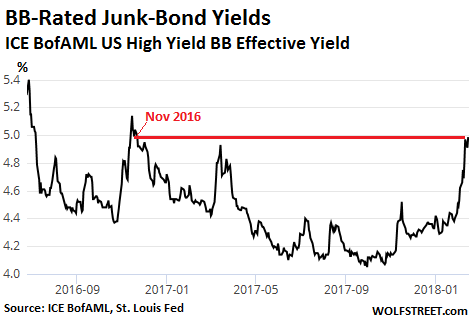

The chart of the ICE BofAML US High Yield BB Effective Yield Index, via the St. Louis Fed, shows how the average yield of BB-rated junk bonds surged from around 4.05% last September to 4.98% now, the highest since November 20, 2016:

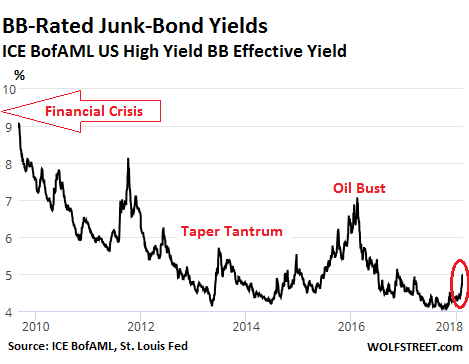

But a longer-term chart shows just how low the BB-yield still is compared to where it had been in the years after the Financial Crisis, and how much more of a trajectory it might have ahead:

When yields rise, it means that bond prices are dropping. And so the selloff that has been hitting the Treasury market is finally creeping into the riskier parts of the corporate bond market, which had been in denial of the Fed’s efforts to tighten financial conditions via rate hikes and the QE Unwind.

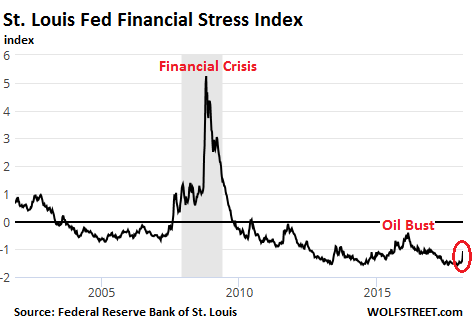

The Financial Stress Index is designed to show a level of zero for “normal” financial conditions. When these conditions are easy and when there is less financial stress than normal, the index is negative. The index turns positive when financial conditions are tighter than normal.

But at -1.06, it remains below zero. In other words, financial conditions remain extraordinarily easy. This is clear in a long-term chart of the index that barely shows the recent spike, given the magnitude of prior moves:

This is precisely what the Fed wants to accomplish. The market is just slow in reacting to a shift in monetary policies. But when it begins to react, the adjustment can be sudden and large. Given that the Fed wants to “normalize” financial conditions – where these kinds of measures return to normal levels – there will have to be quite a bit more tightening in the markets before the market catches up with the Fed’s intentions. And the Fed itself is likely behind the curve – in which case it too will have to do some catching up. So these adjustments in yields and prices are coming. And yesterday’s reports didn’t help at all. Read… Retail Sales, Inflation Add Fuel to Fed’s Rate-Hike Trajectory, Treasuries Dive as Yields Surge

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

As economic nervousness at home and international political uncertainties grow, so should higher bond risk premiums. Historically, risk premiums rise in sync with heightened economic/political turbulence.

As bond yields rise and bond values decrease, currencies fall into deeper crisis mode. Global capital flows are seeking a safe financial shelter, as banking sector fragility increases along with disfunctional markets and withering global trade.

Pretending that debts are assets rather than liabilities, has led many to believe this false construct and to lull them into a perception of perceived wealth. This perception is now changing and with it an enormous amount of presumed notional wealth is going to vanish.

What financial stress? I don’t see any.

We are back to all time highs almost in the stock market .

Buy the dip.

In a manipulated market indicators are irrelevant just like value.

Why worry about indicators or value when you are part of the gang that manipulates the prices and you have a seat at the table to predetermine which prices will be pushed up and which will be pushed down because price movement depends not on earnings or other news but rather on how the gang decides it should be interpreted.

So far the gang is more influential than the Fed, That is the reason there needs to be an overshoot.

The chart of interbank lending fell off a cliff as well so they discontinued it.

Wait – I’ve seen two articles now showing a plunge but yes the series is discontinued as of Q417. Was there some artifact in the display with a discontinued series or is there really not a plunge?

Interbank lending died when the fed started paying interest on excess reserves. The banks with a surplus no longer needed to lend it out overnight to earn more revenue. The fed paid them more to keep money on reserve, than they would have earned lending it overnight.

I did not know that. A lot of folks here are quite seasoned in banking and finance. Some of us much less. So if a comment informs a few, it is worth the commenter’s time to provide it.

Thanks

https://www.federalreserve.gov/econres/notes/feds-notes/overnight-reverse-repurchase-operations-and-uncertainty-in-the-repo-market-20171019.htm

the Fed was pushing long rates down using QE and now they use direct subsidy to raise them at the short end, and the yield curve shows that, now the hope is that raising at the short end (by levitation) will transfer to the long end, even while the fiscal demons bring more bond supply to market, which led 45 to suggest maybe we should have a gas tax?

Greenspan used the discount window while he raised rates to provide liquidity, thus avoiding the blip in the financial stress index. his program of incremental rate hikes was key to easing the concerns of the market. The current market rally is based on a huge dose of foreign hot money, and what the fed says or does is of small importance. the real question does the Fed have one hand tied behind its back due to congressional restraints?

Think this should have started last year, not now, Wolf; but that said…a good & finally smart step the right direction. Markets naturally are now confused and thus ‘VIX-eated’. Best…PJS

being 60, I have a few junk bond crashed under my belt. This one has three unique features.

1) The bonds were issued as junk, (Some were under Milken) but usually they become junk after issue.

2) There are far less people to buy a falling market since there are (or will be) far more supply.

3) The interest rate is too low for anyone to want to buy yield unless they fall 75%.

This one is going to be awesome. When Milken fell, I was buying bongs with 25% yields haha..

Happy days are here again

Sorry, not seeing it. Maybe later. By ‘maybe later’, I mean maybe enough to link cause and effect. Too many players out there with the ability to print unlimited money for the purpose of pumping the measurements in their favor. The ECB, the Swiss, the Chinese, the BOJ, several others. Eventually, yes. Until then, I expect a weird concentration of flunky obedience … and by that I mean bureaucrats sticking to the plan without regard to reality. Then some more. Then even more. Then, eventually, reality and consequences. It’s going to take a while, overall. OK to go out for coffee.

Count me also skeptical. Let us see ALL the central banksters do it and then I will switch sides. But it does appear that things are going to get interesting for a change with the biggest central bankster on one side and the other central banksters on the other!

If they keep Printing/Debasing.

Whilst the US Continues to Unwind/Normalise, eventually this must seriously filter into currency rates.

Then those oil, priced in a Euro/and other basket deals, start to look very ugly.

EU in particular would NOT ease when the FED did. The FED is MAD Etc Etc, Was the response from the EU.

Now the EU is the second biggest QE Junkie on the planet, and it dosent want to get clean.

So again the EU will not cooperate and Normalise with the FED.

So the Stagnation/Depression of 2008 in the real Economy, Outside paper assets, will be dragged out even further.

https://www.lyrics.com/lyric/1589159/James+Reyne/Some+People

“Sit and watch while the candle’s burning

Some peopel they never learn

Sit and watch while the city’s burning

Some peopel they never learn”

The EU, even worse than Americans, are defiantly “People who never F(*&^%G learn”

You won’t keep printing if the money is disappearing down a rat hole. I predict negative money velocity, money will leave the economy faster than the Fed can print it, complete lack of confidence in markets will cause them to stop printing and that will be IT

“You won’t keep printing if the money is disappearing down a rat hole. I predict negative money velocity, money will leave the economy faster than the Fed can print it,”

Helps when you read the comment properly before you reply to it.

“If they keep Printing/Debasing. Whilst the US Continues to Unwind/Normalise, eventually this must seriously filter into currency rates.”

How can the FED print and “Normalise” at the same time??????

“EU in particular would NOT ease when the FED did. The FED is MAD Etc Etc, Was the response from the EU.

Now the EU is the second biggest QE Junkie on the planet, and it dosent want to get clean.

So again the EU will not cooperate and Normalise with the FED. ”

FED Normalises, EU keeps on Debasing/Printing. Eventually This alone must cause an FX shift.

Glad you posted these charts Wolf, now lets keep a sharp eye on the labor market trends, this will be the next tell. Expect hiring to slow, and unemployment claims to tick up in coming months. I am selling into strength here. Playing the long game you don’t have to nail the top. Getting to 70% cash within 10% of the top is very rewarding. Hard to do in practice, as is buying through the trough at the bottom. This time around it will be excruciating. Stock prices, real estate prices, bond prices, margin debt, public debt, private debt, it is all at extreme record high on the back of an economic recovery that was tepid at best. The bottom will be awful. Right now, the shorts are feeling their oats, it has been a long painful time since they have.

A nice thing to have would be a dated list for some of the really nasty junk.

That’s when this “Normalisation” game may start to get “Interesting”

If there is a sudden financial crisis, it won’t necessarily be the Fed’s fault. As much as people don’t like it, the Fed has seemed strangely irrelevant over the years. And After ten years of failure, normalization is the only financial experiment the Fed hasn’t tried.

If there is a sudden financial crisis, there will be a lot of blame to go around. I just assume there will be one and try to manage my finances to lessen the damage. At my age, I am very risk averse and have tried to keep my portfolio as diverse as possible. But, with all the insane bubbles I see, I expect some juicy buying opportunities not too far out. I have found myself lately trying to determine how much “mad” money I can free up if I feel the need and see the opportunity.

1) On ICE BofAML, US Corp BBB Effective Yield, the tilting up trading range from June 2004 to Feb 2008, point at where we might go (slightly different chart and earlier period).

We are not there yet, but it will be a new higher high, one day.

2) So far, a sub par retracement in the German DAX, the French CAC,

the Chinese SSEC and the Japanese NIKK.

VXX ETF & Bitcoin are not impressed.

The fact that this index, nor the chicago fed financial conditions index, showed any sign of trouble between 2004 and about August 2007 when the cat was already out of the bag illustrates the uselessness of their predictive value. Although I would agree with your conculsions. Perhaps more interesting will be the upcoming debate on whether or not estimates of r* have declined too much, and the subsequent impact on the dots and expectations for the extent of how much the fed can tighten without blowing up the system.

The index isn’t a predictor of anything. It’s a summary of current conditions in the credit markets. So its moves combine and document a variety of moves in the credit markets, such as yields and risk premiums. If credit gets tight, this index shows it as it happens.