Market still blows off Fed, Treasury selloff, and volatility in stocks.

“Leveraged loans,” extended to junk-rated and highly leveraged companies, are too risky for banks to keep on their books. Banks sell them to loan mutual funds, or they slice-and-dice them into structured Collateralized Loan Obligations (CLOs) and sell them to institutional investors. This way, the banks get the rich fees but slough off the risk to investors, such as asset managers and pension funds.

This has turned into a booming market. Issuance has soared. And given the pandemic chase for yield, the risk premium that investors are demanding to buy the highest rated “tranches” of these CLOs has dropped to the lowest since the Financial Crisis.

Mass Mutual’s investment subsidiary, Barings, has packaged leveraged loans into a $517-million CLO that is sold in “tranches” of different risk levels. The least risky tranche is rated AAA. Barings is now selling the AAA-rated tranche to investors priced at a premium of just 99 basis points (0.99 percentage points) over Libor, according to S&P Capital, cited by the Financial Times.

Also this week, New York Life is selling the top-rated tranche of a CLO at a spread of less than 100 basis over Libor. And Palmer Square Asset Management sold a $510-million CLO at a similar premium over Libor.

In the secondary markets, where the CLOs are trading, red-hot demand has already pushed spreads below 100 basis points. These are the lowest risk premiums over Libor since the Financial Crisis.

These floating-rate CLOs are attractive to asset managers in an environment of rising interest rates. If rates rise further, Libor rises in tandem, and investors would be protected against rising rates by the Libor-plus feature of the yields.

And it’s big business: In 2017, about $117 billion in new CLOs were issued in the US, which brought the total US CLOs outstanding to nearly $1 trillion.

Libor has surged in near-parallel with the US three-month Treasury yield and on Monday reached 1.83%. So the yield of Barings CLO was 2.82%. While the Libor-plus structure compensates investors for the risk of rising yields and inflation, it does not compensate investors for credit risk!

These low risk premiums over Libor are part of what constitutes the “financial conditions” that the Fed has been trying to tighten by raising its target range for the federal funds rate and by unwinding QE. It’s supposed to make borrowing a little harder and a little more costly in order to cool off the credit party.

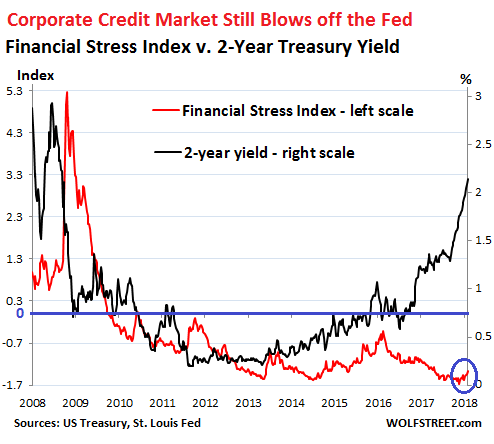

One of the measures that track whether “financial conditions” are getting “easier” or tighter is the weekly St. Louis Fed Financial Stress Index. In this index, zero represents “normal.” A negative number indicates that financial conditions are easier than “normal”; a positive number indicates that they’re tighter than “normal.”

The index, which is made up of 18 components – including six yield spreads, including one based on the 3-month Libor – had dropped to a historic low of -1.6 on November 3, 2017. Despite the Fed’s rate hikes and the accelerating QE Unwind, it has since ticked up only a smidgen and remains firmly in negative territory, at -1.35.

The Financial Stress Index and the two-year Treasury yield usually move roughly in parallel. But since July 2016, about the time the Fed stopped flip-flopping on rate hikes, the two-year yield began rising and more recently spiking, while the Financial Stress Index initially fell.

The chart below shows this disconnect between the St. Louis Fed’s Financial Stress Index (red, left scale) and the two-year Treasury yield (black, right scale). Note the tiny rise of the red line over the past few weeks (circled in blue):

The horizontal blue line marks zero of the Financial Stress Index (left scale). At or above zero is where I — after reading the tea leaves — think the Fed would like to see the index at this point. But the index is far from it. And the CLOs mentioned above are examples of just how ebullient corporate credit markets still are at every level. A similar ebullience is still visible in junk bonds as well.

The corporate credit markets are starting to take into account the risk of slightly higher inflation – hence the appetite for these floating-rate CLOs. But the risk premium over Libor and other risk premiums show that credit markets are still totally in denial about the bigger risk for junk-rated credits: the risk of default. And this risk of default surges when rates rise and financial conditions tighten as these companies have trouble refinancing their debts when they come due. But for now, investors are blithely ignoring that they’re in for a big reset.

The chorus for more rate hikes is getting louder. But no one will be ready for those mortgage rates. Read… Four Rate Hikes in 2018 as US National Debt Will Spike

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The corporate credit market is betting that the Fed will chicken out as soon as a few chickens come home to roost.

The fed will chicken out sooner or later but since they rely on statistics to prove things are bad out there it’ll be a long time before they react by lowering rates again which is why their policy so heavily lags reality assuming it’s even a sensible strategy in the first place. In the meantime who wants to bet how many companies will go bankrupt when credit markets finally start to react and these businesses can’t afford to rollover their debt anymore? I think this crisis is going to hit fast and furiously in different ways than last time more than the banks we’ll see it hitting businesses closer to main street and it won’t be pretty. I can only assume when the fed notices the carnage they will go to much more extreme measures next time around.

And yet….does Main Street even exist anymore?

All the downtown main street areas, even those in areas that can’t be called poor, are hollowed out with something like 50% vacant commercial store fronts.

Quincy, Ma. Brockton, Ma. Tuanton, Ma….just to name a few I see frequently. How many trendy bars/restaurants can the prosperous areas like downtown Providence or Boston support? And the upscale niche retail stores don’t seem to last too long in the prosperous downtown areas (Boston, downtown Providence). For example Copley Mall in Boston last time I visited had about a 30% vacancy on the first level although they did a very good job of completely walling off all the empty store spaces with well done signs announcing the awesome new store that was soon to occupy each and every empty space, and they were all stores I’ve never heard of and sounded niche and upscale.

Not disagreeing with your point, Just saying….

A lot of commercial landlords have become very greedy in recent years.

“I can only assume when the fed notices the carnage they will go to much more extreme measures next time around.”

That last voice from the wilderness, Bernanke, and the new ideas he brought where income from savings could be replaced with monetary policy and asset bubbles, aka the wealth effect, was the inspiration for the central bank credit bubbles that exist today. Granted, the Japanese were trailblazers, too, but Bernanke made it a scientific process. (Some cynics think Bernanke turned the Fed into the corner bank for the Globalist movement – providing low rates and promoting low wages, while politicians promoted open boarders and flexible labor sources. Me – I think he built an all purpose theory and turned the economy into a cage match between the upper and lower classes. Negative rates were just around the corner with some new made up fictional theories to justify them.)

His little mistake involved the propensity of people to spend their bubble wealth … there was little to none … so removing income from savings from the economy created the deflation he and his peers so strongly disapproved of. Prices fell to meet available income. More and more QE was piled on to fix this. This was a bad idea as that just dug the hole deeper.

Somehow, after nearly a decade, inflation that couldn’t be ignored by the CPI any more finally appeared and the Fed was backed into the corner. Plus, the Washington DC political climate changed abruptly in a way that didn’t support the Globalist plan. Now the big questions ….

Will they continue to raise rates? If so, will they normalize relatively quickly or go up at an infinitesimal rate?

Will they continue to reduce the balance sheet?

Will they repudiate the old Globalist plans and the concept of negative rates or will they still remain as 16 ton weights waiting to fall on our heads down the road?

Will anyone admit removing income from savings reduces overall income and creates the deflation they claim to hate so much?

Will anyone admit asset bubbles do not increase the propensity to spend?

Will the Fed members start talking QE forever again as a stall until a more agreeable political climate supports a return to the old Globalist plan?

To answer the original question … another decade like the last one is still on the table unless the Fed publicly admits its past plan and how it failed so miserably, using both words and actions.

Many people do NOT get this. The fundamental motive for FED’s action is to protect CAPITAL. You may think printing money and shower the credit market will benefit capital, but there is a limitation to this. And that is this encourages “BAD” business to compete out “good business”. Imagine you can operate at loss and cut prices for 10years, that will kill the profitable businesses. In other words, CAPITAL starts to kill themselves.

When printing helps capital by preventing bad business to go under, they will print. When printing hurts capital by encouraging bad business to compete out good capital,l as well as causing labor to benefit, they will stop.

Hi Cdr

Your comment about the Fed “removing income from savings” hits the nail on it’s head!

Most people are not aware that by taking this step the Fed permanently destroyed a lot of main street’s real capital (savings). However as a consequence this destroyed real capital also created a permanent deflationary force!

The Fed now seems to believe that they can create new capital to replace the destroyed real capital by just creating more debt money out of thin air!

To answer your question, the Fed will never admit it doesn’t know what it is doing! The Fed only knows how to do one thing. Create more debt money!

JZ, WES,

Thank you. It’s always a good day when someone else notices the monetary games played by the central banks and how they create fake theories to support their intentions.

To me, the falsehood and ludicrousness of these ideas are as obvious as white on rice. I can not understand why so few others mention them, not only here but everywhere and often. It’s like people go massively stupid and are taken to new levels of gullible if someone official says the sky is really orange plaid with green polka dots … nobody disagrees and lots of science test books are changed to support the new proclamation. TV weather personalities lose their jobs if they disagree.

To me, this is the state of modern day economics.

The Fed has admitted this. Yellen remarked multiple times that she was surprised inflation hadn’t taken hold, as planned. That’s the admission.

Now, the Fed obviously believes inflation has taken hold, or that systematic risks are too great. Hence, the automatic balance sheet reduction plan. There would have to be a huge amount of market turmoil to reverse the automatic plan and restart QE. If the Fed abandoned the automatic plan prematurely, people would surely see the Fed has no clue and is therefore providing absolutely no benefit to the economy.

Gteat article, learned a lot. What is the total value of CLO’S and vs 2007 or is their a place to look it up?

Issuance in the US for Collateralized Loan Obligations (CLO’s) peaked in 2006 at $98 billion before sliding in 2007 and collapsing in 2008.

I am yet to find reliable data for 2017, but in early November US issuances for the year were already standing at $120 billion.

Worldwide CLO issuances for 2017 are estimated (note the word) to have been over $450 billion, with Asia issuing the most.

The scariest thing about CLO’s is not their size (inflation being much underreported, especially in financial assets) but how aggressively they are pitched as “high yield” or even “juicy” while in reality CLO yield spreads have been steadily falling off against US treasuries, one of the most boring yet safest assets around.

Asian investors, especially in Japan, South Korea and Hong Kong, are the most exposed to CLO’s following an extremely aggressive sales pitch by local mega-banks in close co-operation with Wall Street and Mainland China firms specializing in these risky assets.

MC01, I just added data below on CLO issuance and total outstanding in the US. I also updated the article with the data.

Tks.

In 2017, about $117 billion in new CLOs were issued in the US. This brought the total US CLOs to nearly $1 trillion.

http://www.leveragedloan.com/category/clo/

Wolf,

Would you say this is because the market does not believe the Fed can raise rates due to the following:

1. Given the way the Fed had dithered in the past whenever the market sneezed, it may not be a wrong assumption. One would not know as the Fed is data dependent, sorry market dependent and it depends on how the market reacts.

2. Also, given what BoJ said recently (unlimited bond buying) and that ECB may not have the stomach to end QE or raise rates when push comes to shove, would that not hamper the Fed in its march to higher rates. After all in an interconnected unless all the central banksters move in tandem (as they did while lowering rates and doing QE-the easier part), one or the other central bankster is going to howl when it gets hurt. So if the other central banksters cannot move for various reasons, the Fed also may not be able to raise rates.

Markets are often in denial for an amazingly long period of time until suddenly they aren’t. But they’ll come around. Give it some time :-]

Will EU and Japan be handle rate increase as they will have to follow suit

Watching the Federal reserve for future rate directions is going to be fruitless? The Fed is way behind the curve and will stay that way? Paying interest on excess reserves and admitting they are clueless to why dollar falls when short rates rise? This pass thru is the reason inflation and its effects are explored but have no chance of causing the current carnage? The Fed is floating longer term paper as a substitute for soaking up the excess paper? Sell useless paper rinse repeat? If the fed can’t buy bonds or cut short rates they should pack it in and dissolve? Before its too late!!!

KPL,

The ECB can’t normalize rates or end ECB QE without causing an economic catastrophe in the Eurozone. ECB QE started several years ago as a kick the can measure to avoid paying higher sovereign rates on lower quality Euro debt. Rates were rising at the time and reversed when Draghi promised “it would be enough”. Negative rates can’t exist outside of a forced environment such as ECB QE. Much of Europe is negative at this time. The rest pay abnormally low rates.

The whole world is in a central bank QE environment. Endless money printing and reinvestment of interest paid will not debase currencies if everyone does it at the same time. It’s an arithmetic problem … if you multiple both sides of the equation by the same amount, nothing changes regarding inflation via currency debasement.

The Fed ending QE and normalizing both rates and the balance sheet is a big monkey wrench in that plan. It remains to be seen how it will end – you can be sure badly if the Fed continues with real intent – and when the first cracks in the dam will appear. Big changes ahead after people notice the growing cracks – assuming they ever do.

More world QE bigger and for longer will put that day off. Too soon to say the Fed has changed sides. Looks hopeful, though.

Currently what the FED is doing really only effects Americans.

chian EU and others are still printing like there will never be an end to it.

Long Term this is good for Dollar and. Most of America.

Wrong, LIBOR has been rising ahead of Fed Rates, that’s the rub, one would imagine to slow down the exit of global capital seeking better yield. How long can you set rates higher and run QE?

“Wrong, LIBOR has been rising ahead of Fed Rates, that’s the rub, one would imagine to slow down the exit of global capital seeking better yield. How long can you set rates higher and run QE”

This needs some who, where, and whom put in it.

As you appear to be talking about more than just the FED and the US.

The FED is not Printing.

LIBOR Is rising, the ECB china Etc are still printing. And EU retail deposit rates are not rising.

Indefinitely!

Thanks to “Interest on Excess Reserves” (IOER), there’s no longer a direct relationship (constraint) between QE (size of Federal Reserve balance sheet) and Interest Rates. The two are now independent parameters for the Fed to manipulate.

In the past there was a very strong relationship between interest rates and the size of the Fed balance sheet. A few years ago John Hussman had some beautiful charts showing how many trillions the Fed would have to roll off before rates returned to even 1%. But with IOER, the Fed has “raised rates” even without shrinking the balance sheet.

I don’t see any constraint on this practice, other than the point at which people start squawking about how IOER is basically a multi-billion $$ annual handout to the banks that own the Fed, at taxpayer expense…

Im not at all worried about Corp debt. The fallout is worse here when this starts to fail as it did in 07-08 in the USA.

-Total US household debt soars to record above $13 trillion–

Total household debt rose to an all-time high of $13.15 trillion at year-end 2017, according to the Federal Reserve Bank of New York’s Center for Microeconomic Data.

The report said it was fifth consecutive year of annual household debt growth with increases in the mortgage, student, auto and credit card categories.

The consumer balance sheet is in much better shape than 08. The vast majority of the $13T is mortage debt and every new loan since 08 is pristine. Card and auto paper is solid.

Student debt is a different story – a new wedge issue for the pol’s. It is a very very big and new ball and chain …, not a bomb like the mortgage excesses associated with trying to get everyone to own a home.

Auto paper is solid?!!

Interesting take…

Solid in the sense that banks have not taken a lot of risk and that Auto paper is not going to be disruptive. …(my comment was in response).

Consumer debt situation is not comparable to last cycle at all. Student is the weak part and again, not a bomb …only a big drag.

Also, auto paper is about half auto manufacturing lending arms aka captives and half banks, etc. Only the captives have loaned into deep subprime. They are not allowed to fail anymore because we didnt take moral hazzard seriously. Alas, I digress.

Auto paper is solid? I’d read just the opposite here. Unless it’s already purged itself.

Agree about mortgages as underwriting since 2009 has gotten comparatively conservative. Student loan debt is a problem, but the rules about what constitutes a “default” have been strongly massaged in favor of the borrower. Albeit , the debt still exists.

But a loss of income (job) changes the situation pretty quickly.

Yea and about that savings rate. Alot of homeowners have zero to little savings to survive unemployment overall. Mortgages are not safe. Safer in a marginal sense…maybe.

Fitch rates a lot of auto-loan ABS. Its subprime “Auto Loan Annualized Net Loss Index” was at 10% in January 2018, up from 6.4% in January 2014. Subprime auto loans – about 23% of total auto loans – are in bad shape.

Mortgages may be better evaluated on the front end but alot of ‘good’ loans went bad when the job was lost the last time. That has not changed at all no matter what criteria was used. Home loans can and will go bad. Its econ 101.

What comes around goes around, and this is especially true of money velocity. The problem with the money markets today is that regulation is beyond the scope of governments or the fed. When banks can unload risk for a commission, the only thing standing between the loan and bankruptcy is time.

This situation reminds of the 90’s when “investors” were flooding into junk bonds. So much of this toxic waste is in 401-k’s and IRA’s, whose “investors” are, frankly, totally oblivious. When the market turned, the howling was ear piercing.

The same was (is) true of muni’s. When the market falls, as it is now, people who thought they were buying low risk securities will start screaming.

How anyone can say we have a “market” for debt when commercial paper is 2% and the 30 year treasury 3% is beyond me. You get 1% yield for 29 years of risk? This is what the glorius fed has bequeated us. The risk if uncontrollable flash crashes is off the charts.

Frankly Wolf, until investors start getting stung, these warnings are just shaking your sword at windmills.

Junk bond flood in the ’90’s ? PRICELESS! The junk bond market was collapsed because the Banks feared that high yield would destroy their model, like bitcoin today? An alternative finance model that cuts out banks?

Mike milikin was a genius manipulater until he got to big for the times?

The single reason (good or bad) we are gizillions in debt and LOVING IT MANA FROM heaven until its not?

A niche comfortably populated in an environment of very low rates sustained for a very long time starts to depopulate when the conditions causing it change. In this case low sustained short term rates are the main cause. Gradually increasing short term rates are the “cure”.

Under this model the repricing for default risk occurs as defaults occur, this widens spreads which increases defaults which further widens spreads. This process starts very slowly but accelerates.

If this is the way it actually unfolds it will be interesting to see how stoic the Fed remains through this process.

Hence my concern about aggregate consumer debt I posted.

The structural mess they’ve gotten us into is staggering.

The tax system has allowed about 3 million households to convert a huge amount of income into wealth. That wealth is rising much faster than the incomes of over 100 million Americans. As more and more money is tied up in wealth, and not sloshing around the economy in salaries and sales, tax revenue stagnates and inequality soars. ZIRP has helped to make and keep those who have wealth wealthy, by making access to cheap credit to buy even more assets easy (while the bottom 2/3 of the country pay 19% on their credit cards and get nothing from the checking and savings accounts). But it has also turned those people with massive wealth into wild, unhealthy speculators as they search out new ways to increase that wealth in a world where safe investments have returns below the modest rate of inflation. Thus, the creation of wacky “instruments” like those described above; time bombs waiting to blow up the global economy.

I think the system itself is doomed. I think we are headed for a Tainter reset. This level of complexity, of Ptolemaic epicycle on epicycle, seems unsustainable to me. And they have only added more complexity and risk since 2007-09.

“The structural mess they’ve gotten us into is staggering.”

Exactly my thought. How can one be so irresponsible as a regulator beats me. How do you extricate from it is beyond me.

“I think the system itself is doomed. I think we are headed for a Tainter reset. This level of complexity, of Ptolemaic epicycle on epicycle, seems unsustainable to me. And they have only added more complexity and risk since 2007-09.”

Again you said it. I would consider it impossible to come out of this mess without a reset. Doing QE in a synchronised manner was all too simple but how are ALL OF THEM going to do QT and raise rates is beyond me more so when some of the countries cannot handle it. The risks to my eyes are enormous. It is a wonder Phds cannot see it. Probably they look at it through tinted glasses.

One thing for sure, if ALL THE CENTRAL BANKSTERS can come out of it whole I am willing to acknowledge they are the supermen they think they are.

Oh but the mortgage paper is safe LOL> you read it here.!!!

As a former investment manager at Prudential, it’s so interesting to note how financial repression has resulted in these formerly conservative, yield-harvesting financial institutions up to their necks in sketchy underwriting writing and issuance in an effort to stay solvent.

The Fed will continue their rate hikes this year, next year? With the current US president I have no clue.

Back in 1980, a small Los Angeles based bank holding company came to market with 20 year floating rate notes. As interest rates started to soar and the bank was perceived to be a greater credit risk, the yield spread on the notes vs Treasury bills widened out by several hundred basis points and the notes were trading at about 60 (vs 100 at the time of issue). I don’t know whether the notes were ever repaid in full or whether the bank is still in business. But the lead underwriter, which had survived the Great Depression, lost its independence a few years later.

Interesting FLRN was rolled out by Treasury last year to give investors a hedge on rising rates. Most of the preferred devices are linked to LIBOR.

I worked as a financial officer (since retired) in a medical device company that was listed on the NYSE. We were bought out in an M&A transaction and Chase financed the $5 billion in bonds at 9% to purchase the company. Chase then sold the bonds to pensions and asset managers with yield of 8% and pocketing a cool $50 million. The company is staggering under its debt load and the M&A is unable to sell the company 7 years later as its revenues decline.

That is the classic description of asset stripping and it’s sickening that it’s legal in any way, shape or form.

Having read that Fed boffins are war gaming a univariate Markov-switching model to decide just when to deploy their countercyclical capital buffers I am much comforted. These wizards aren’t just playing video games; they are depressing their GDP deflators to find out exactly when to turn on their money hose. There is no alternative.

A reference would be good.

And here you are: https://www.frbatlanta.org/-/media/documents/news/conferences/2017/1102-financial-regulation-fit-for-the-future/brave-lopez.pdf

I need to bone up on my math.

Thanks. Havjng glanced at the model, I must say that I doubt that a Markov model (next state probability depends only on current state) is a good predictor of “financial stability”. Especially when the remedy (called CCyB) is to demand an increase in bank capital AFTER instability occurs. But then again, I am no expert on economic modelling.

My gut feel, though, is that you can make a model that justifies whatever action you have already decided to take for other and less palatable reasons. And that is probably how the FRB operates, generally speaking.

Does corporate debt take a downgrade with the Feds unwind? The Feds rate hike fallacy is that they PAY for those rate hikes with RRPO. Mish reported that interbank lending has fallen off a cliff. That certainly can’t bode well. We just lived through a mini stagflation event, higher asset inflation, stagnant wages (other than service who enjoy legislative support), and the followup to stagflation is often deflation. Markets are waiting to see CPI, and if it’s low end (since it doesn’t follow RE, stocks) they might not react well. Jim Rickards says its the deficit, but all that means is that they’ll be trying to sell ten pounds of bonds in a five pound bag.

Yield Shock

It will not be a liquidity crisis that will be the cause of the looming big reset, but a reset of valuations. What is coming is a drastic downward reset of financial asset prices, compliments of a yield shock.

In the coming months, the Fed and the US Treasury will be dumping massive amounts of public debt on the bond market. Upwards of $1.8 trillion in fiscal year 2019 alone! This in turn will generate the said “yield shock”.

As debt becomes ever more unmanageable, it begins to collapse under its own weight and asset values begin to fall.

Why?

Quite simple really, because debts are the other side of assets.

I agree only rates are going to collapse, the forex market wants you to believe that its a zero sum game, but when currencies lose value in concert how can you tell? Global liquidity is contracting. If rates do rise much from here it will only be symbolic, or temporary before the final race to the bottom.

PCG is certainly getting a big reset. For icing on top, energy industry haters groove on the rubble with big smiles.

win-win-win!

Look at what happened today

Treasuries got killed,investment grade bonds had a bad day, but Hyg and Jnk rallied slightly.

This deviation can get to a silly point-just look at last year when European junk yields equaled the yield on the 10 year

But with the Fed determined to force credit spreads into line,it will eventually be financial to go contrary to the Fed