It’s just a question of how disruptive the adjustment will be, whether it will be just a painful sell-off or junk-bond mayhem.

Treasury securities have been selling off and Treasury yields have been rising, with the two-year yield at 2.15% on Friday, the highest since September 2008, and the 10-year yield at 2.84%, the highest since April 2014. Rising yields mean that bond prices are falling, and this selloff has been an uncomfortable experience for holders of Treasury securities.

But corporate bonds have been in their own la-la-land, and even Tesla, despite its cash-burn rate that should scare the bejesus out of investors, was able to sell $546 million in bonds last week – bonds collateralized by lease payments it receives from customers that have leased its cars.

S&P rates Tesla “B-minus,” a highly speculative rating just one notch above the deep-junk rating of triple-C. But no problem. Yield-desperate, risk-blind bond investors had the hots for these auto-lease-backed securities, according to Bloomberg:

The sought-after debt deal allowed Tesla to slash the risk premiums it would pay on the notes. They were sold to yield between 2.3 percent and 5 percent. At initial offered prices, investors had put in orders for as much as 14 times what the electric-car maker intended to sell on some slices of an asset-backed security, according to people familiar with the matter.

Junk-rated and cash-burning Netflix, or oil-and-gas companies drilling billions into their fracking endeavors, and many other junk-rated companies such as Fiat-Chrysler are in hog-heaven, with high demand for their debt, which pushes down the yield for investors and the costs of borrowing for the companies.

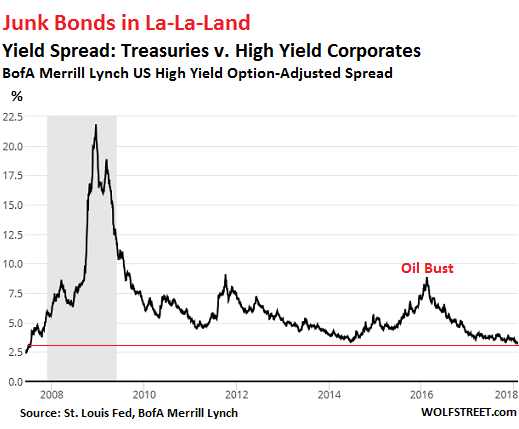

And the spread between average junk-bond yields and equivalent Treasury yields has now fallen to just 3.29 percentage points. That’s the premium investors demand to be paid for taking on the additional risk of junk bonds versus Treasury securities.

This is the narrowest spread since July 2007, just before credit froze as the Financial Crisis began to unfold, and numerous of these junk-rated companies, cut off from further funding and losing money as they went, ended up in bankruptcy court, an experience during which stiffed bondholders and other creditors re-learned to appreciate the notion of risk.

This chart of the BofA Merrill Lynch US High Yield Option-Adjusted Spread, retrieved from the St. Louis Fed, shows the minuscule premium investors are currently demanding for holding high-risk junk bonds versus nearly risk-free Treasuries, and just how far in denial the corporate junk-bond market is:

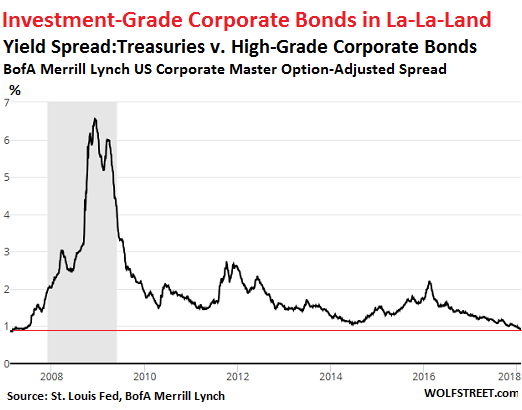

Investment-grade bonds, issued by the corporations that are deemed to be financially among the most stable, are showing a similar pattern.

The premium investors demand to be paid for taking on the additional risk of corporate bonds versus Treasury securities has now dropped to just 90 basis points (0.9 percentage points), according to the BofA Merrill Lynch US Corporate Master Option-Adjusted Spread index. This is the lowest since March 2007. During the subsequent Financial Crisis, major investment-grade rated corporations – including GE – suddenly couldn’t borrow anymore even to meet payroll, and the Fed, in its function as lender of last resort, began bailing them out with special loan programs.

The chart below of the BofA Merrill Lynch US Corporate Master Option-Adjusted Spread index, retrieved from the St. Louis Fed, shows the la-la-land that the corporate bond market thinks it’s in:

Here’s how this is going to work out:

- The Fed will continue to raise its target range for the federal funds rate.

- The 10-year yield will follow.

- As the Treasury yield curve, which is still relatively flat, steepens back to some sort of normal-ish slope, the 10-year yield will make up for lost time over the past year and will rise faster than the Fed’s target range for the federal funds rate.

- Corporate bonds will follow, but they have even more catching up to do, and so they will rise even faster than the 10-year yield, as yield spreads between the 10-year Treasury and corporate bonds widen back to some sort of normal-ish range.

In other words, corporate yields will rise further and faster than Treasury yields, just to catch up, thus pushing down prices with gusto. Junk bonds are more volatile and will react more strongly. Junk-rated companies will find it more difficult to raise new money to service their existing debts and fund their money-losing operations, and there will be more defaults, which will push yields even higher as the risks of junk bonds suddenly become apparent for all to see. This will make it even tougher for companies to raise funds needed to service their existing debts and fund their operations.

This is not a secret. It’s just how it works. The initial moves are what the Fed wants to accomplish. It wants to tighten the current extraordinarily loose financial conditions. Yield spreads and corporate bond yields are a big part of those financial conditions. This will happen, it always does. It’s just a question of how fast and how disruptive the adjustment will be, how many junk-rated companies find themselves unable to raise funds to service their debts and keep going, and whether it will be just a painful sell-off or junk-bond mayhem.

The QE Unwind is now in full swing, with a sense of urgency. No more dilly-dallying around. Read… Fed’s QE Unwind Accelerates Sharply

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

There is no mention here of the HUGE increase in the amount of treasuries and MBS that the market is expected to start absorbing soon, and what the ramifications will be.

$ Trillion plus deficits as far as the eye can see, tapering of the FED balance sheet, and then there is expected QT from the ECB and BOJ.

The Fed target rate may well be a very minor player in determining what 10 year bonds yield.

I stay as far away from all this stuff as I can.

I have little opinion as to what the spread should be between the debt of zombie governments and zombie companies.

In part, that is because there are other options, in other currencies, where one doesn’t need to ponder such issues.

“There is no mention here of the HUGE increase in the amount of treasuries and MBS that the market is expected to start absorbing soon, and what the ramifications will be.”

Note the link at the bottom to my article on that very topic posted a couple of days ago.

Yes, obviously I can see what it IS.

My comment was that I have no idea what it SHOULD BE.

In my mind, it is trying to determine the differential in risk between two zombie entities, a mugs game.

That is separate from the fact that both numbers should probably have at least another 10 percentage points on them.

Again, I stay away from this stuff.

Oh, and here’s the one about the Federal debt:

https://wolfstreet.com/2018/01/30/us-national-debt-will-jump-by-617-billion-in-5-months/

Question: Who will buy Tesla and Netflix bonds when people quit buying the products put out by these two companies?

Answer: Central banks will.

Conclusion: Central banks, like Atlas, are needed to hold the global financial system up. Unlike Atlas, they don’t need muscles, they just need computer keystrokes, the ones labeled QE.

Well, assuming all people will quite buying Netflix & Telsa products might not work out that way.

What may be more likely to happen is these companies go bankrupt when investors refuse to buy the bonds they need to issue to keep running…or will only buy the bonds at coupons so high these companies can’t afford to pay.

Then, what might happen is another company buys, say, Netflix. Netflix products continue, new company makes changes, and might raises prices and cut back Netflix spending on crapy…err…”original” content.

Next, project that same process onto fracking and we might be talking about events that can feed into the Fed’s much vaunted method of measuring “inflation.”

And presto magico…we got ourselves some “inflation”!

Which central banks? The ECB is not going to buy bonds of a US company. Nor will the Japanese. They each have their own problems and the ECB is trying its own unwind.

That leaves the Fed and I’ll bet you a drink (if you are in town) that the Fed won’t buy the bonds of either.

The Fed is not immune to the pounding it has taken from all sides re: asset bubbles. It has an institutional memory of hard- ass guys like Volcker and it knows there is going to be some wailing on the road to normality.

Makes you wonder why the Fed would do this? If this was the ECB then Draghi would be buying Tesla and Netflix bonds right now. If it was Japan a large portion of the stock market would be in the Treasury account. But we aren’t. Answer: The Fed is not a Central Bank. It’s not a private bank and the authorization for QE is not a given.

Also, not even the ECB is allowed to buy junk-rated bonds, though it has ended up with them following a downgrade.

The FED needs congresses authority to do that, and by the time. Congress possibly agrees something it will be to late for many of the Junk supported unicorn’s.

Lehmans Went before Congress even got interested. By then it was a, how much of the system and Economy can we save, which could have been a how can we prevent this occurring.

Congress “Day late, Dollar short” as usual.

20/20 Hindsight, it would have been much cheaper to bail out Lehmans and at the same time put the brakes on the credit. 20/20 Hindsight is free, like dreams. Unlike dreams, you can learn from the past..

Instead Lehmans was sacrificed, we had the 2008 event, which for many, ten years later, has not even started to turn into a recovery, and the Credit system has been allowed to run wild.

So the Question is. Can the FED successfully put the brakes on the out of control Credit system, and not Crash what is left of the real Economy.

d:

I believe that Lehman Brothers was not sacrificed, but it was allowed to have free market forces give it what it deserved, which was death.

From Wikipedia: “Lehman had morphed into a real estate hedge fund disguised as an investment bank. By 2008, Lehman had assets of $680 billion supported by only $22.5 billion of firm capital. From an equity position, its risky commercial real estate holdings were three times greater than capital. In such a highly leveraged structure, a 3% to 5% decline in real estate values would wipe out all capital.”

In my 20/20 Hindsight, all of Wall Street’s ‘real estate hedge fund investment banks’ that were highly leveraged should have been left to their free market fates.

We shall see how the corporate bond market plays out ???

Less well known is that Lehman was HUGELY short silver, and silver was a screaming upwards at the time.

I believe they filed bankruptcy within days of the peak silver price, facing huge margin calls.

That huge silver short was then taken over by JPM, at the behest of the government, and there starts a very long story.

I suspect that part of the negotiations involved JPM being given immunity from SEC regulations in order to deal with that huge silver short, and thus began the SERIOUS manipulations of PMs.

It will soon be 10 years since that happened.

Maybe JPM was given immunity for 10 years?

Wife and I will be long to the hilt around the next intermediate term price low, as it might be the last one.

Kindly note that we just closed some shorts on the drop Friday and might open some more today if the bounce (in THB) is adequate.

I believe it is a bit early to go long, but not much.

“and thus began the SERIOUS manipulations of PMs.”

PM Manipulation began long before that and the biggest players are russia and china as they can not operate their 3 and 4 gram per ton mines, with a true gold price.

Which is around 27% (APP) of what is currently quoted to buy physical Gold.

Blaming the FED and US Bank’s for PM manipulation, is a Gold Bug Fairy story.

I also did well Friday, Monday, and currently this AM Asian (as it refereed to) session is open, and we open first in the world every day.

For me its already 10.40 Tuesday.

Kindly give more detail?

3-4 grams is more than adequate for cyanide processing.

I am aware that the Opium Wars were really fought over a British shortage of silver, not opium.

How far back are you going?

What does the 27% refer to???

“From Wikipedia: “Lehman had morphed into a real estate hedge fund disguised as an investment bank. By 2008, Lehman had assets of $680 billion supported by only $22.5 billion of firm capital. From an equity position, its risky commercial real estate holdings were three times greater than capital. In such a highly leveraged structure, a 3% to 5% decline in real estate values would wipe out all capital.””

All undisputed facts.

“In my 20/20 Hindsight, all of Wall Street’s ‘real estate hedge fund investment banks’ that were highly leveraged should have been left to their free market fates. ”

That would have created a situation that would have made the 2008 and 1929 Events, with their following depressions, seem like minor corrections.

The most important thing that should have been done no matter how Lehmans was resolved, is to reduce the leverage in lenders.

What the FED did was recapitalise the Major banks at the expense of savers, and continue to allow the third tier finance industry to run wild. Hence today. America is even more over-leveraged than it was in 2008.

The Majority of that leverage risk is however. Not at the Major bank’s.

Are the FED and the Major bank’s out to crash the system, then swoop in and scoop up the assets for pennies on the Dollar. As many claim?? That is so F)(&(%G juvenile. It is not worth addressing..

Would the majors and the FED be concerned if a large number of the third tier financial risk takers failed, and they ended up with the assets cheap. No.

The FED has done what it can since 2008, whilst working with an uncooperative congress and both an uncooperative and now an insane POTUS.

Most Americans blame the FED, every time there is a Financial/Economic problem, when the blame lies in Congress, and the Stupid constitution that protects the corporate owned Duopoly in Congress.

Dood Fank simply made a bigger mess, when reenacting Glass Stegal, and increasing regulations over leverage in every tier of the lending industries. Would have made the system safer and better.

Every time Congress allows this financial mayhem boom bust cycle based in excessive leverage to continue happening, the world pays for it. Which is why when a better option arrives via Global Consensus, the US is a fish in a barrel. That’s a when.

However it wont be CCP china, or 1 Party State/Ogliarchy china, as that would be a frying-pan fire move.

For the last 43 (App) years, china has milked the west, it still has not had to weather an internal 1929/2008 type event. Lets see whats left after it does, and then how long it takes them to truly return to where they were, before that event.

If you guys manage to get an insider seat at the good ‘ol boys club table, let me know!

The best way to rob a bank is from the inside.

The central banks have (I know it’s a tired cliché) kicked the metaphorical can down the road and into a dark forest.

Now, central banks have taken a few baby steps toward popping their frightening and massive asset bubble but they have reached a scary fork in the can kick road. As the bubble implodes the central banks can either 1) watch from the sidelines as the collapse in assets crushes the world economy or 2) open the currency floodgates, lose credibility, and watch as confidence in the currencies is destroyed and we suffer a worldwide currency crisis.

Ben Bernanke and his colluding cohorts led us down this dangerous path and there is no direction we can turn to avert disaster, we are stuck between a rock and a hard place, there is no good outcome from here.

Where is Robespierre when and his guillotines when you need him. Arrogance has run amuck – Courage to Act.. Indeed (courage to destroy the currency and bail out world elites).

Yep, thankfully it doesn’t escape you that their plan hasn’t helped anyone but themselves.

I guess you know what happened to Robespierre? He too had his date with the ‘hot hand’ aka the ‘Republican Window’ along with about 70,000 victims of the Great Terror.

BTW: you can make the case, and I do, that France never really recovered from the Revolution. If anything it fueled an understandable horror of revolution but also an aversion to change and a preoccupation with preserving the establishment.

It is today by miles the least egalitarian Western democracy. The country is run by a thousand people, all of whom attended one of two institutions. No one of modest origins has ever risen to power.

The British class system, which has seen one PM, Thatcher, raised above a grocery store and one ( Major) fathered by a circus acrobat in his 50’s is not in the same league.

There is something wrong with the y axis of the first chart.

Yes. The decimals got cut off. Fixed. Thanks.

Hi wolf, great article. Who are the best known companies known as being junk rated?

Tesla and Netflix :-]

And Uber!

An interesting question is, if you could short for 2 years without getting slaughtered (not true, I know), which company would you short?

I guess I’d pick Tesla because they are faced with giant capital costs and well-capitalized competition.

:)

Tesla is a good choice. I would bet GE is facing collapse if they don’t get a Fed bailout. No doubt there has been a lot of financial engineering going on the last decade but GE got a two decade head start.

The sharks are circling and it’s starting to look like the whole decrepit structure is finally going to topple. The Fed seemed only to be waiting for retail investors to get back into the market – strange how these things always seem perfectly timed to shear the sheep.

I am soooo looking forward to higher rates that I can almost feel them. Kind of a pleasant tingle. It will be heaven on earth when they return.

I plan to mix it up. Some in a MM fund for cash needs, some in a govt treasury fund, some corporate, and some in a higher risk fund, most of which do not appear to be really risky. All I need is 4% to meet my anticipated needs to live a nice life, but I expect to earn much higher. Once that pile is secure, I have a Roth IRA I want to range trade for pin money. I used to be good at that and plan to give it a go, again. My hobby.

Note: yes, I know over 4% is available today. I have no desire to see the share price drop when rates rise while I am in said fund. I will not jump in until I see a big dip from the terror I expect to see as rates normalize and people catch on. Hopefully, I will make some capital gains on the aftermath and then move into shorter duration funds to minimize volatility.

One thing I don’t know is … what’s a historically decent range for high yield in relation to US debt? What’s the premium for risk in that class? What about decent corporate debt over US debt?

If, for example, the 30 day US rate was 3% and this were an average Tuesday in a country where rates were mostly normal from a historical perspective (and I imagine the Eurozone will be a collapsing mess), what would the rest of the market probably look like?

Back in the day I didn’t care much about debt investment. Now that I’m old, I have a much higher interest in earning interest. Yield differentials are fairly new to me. Any ideas about the spread to come?

You can research the spreads off of the prime rate, historically. I haven’t kept track in a long time but 2% over prime was considered very good and not more than 4 or 5% over prime was considered good high yield. Higher spreads than 5 or 6% were considered ill advised.

Thanks. Looks like a good rule of thumb.

What if you get 4% yield but nominal GDP is growing 7%?

I spend the cash I get. 4% is better than 1/2%, which is what was common a year ago. I expect to earn more than 4% as rates normalize, as I hope they eventually do soon.

I prefer to think in terms of how the world actually affects me, as opposed to some theoretical situation. Also, you would be amazed at how I can avoid a lot of the inflation the stats say exists. Hint, try to avoid retail prices and shop around. Think changing consumer preferences and substitutes, too.

Besides, as rates rise, real income rises. When the Fed dragged rates to zip, they also removed a big part of the real income people earned. Then they fretted about the lack of inflation, unaware that they created deflation by eviscerating savings rates and lowering real income as a result. People can’t spend what they don’t have, unless they want to live on credit …. which makes little sense if your income is declining. Prices fell to match available income. Hence, the Fed created the deflation they said they wanted to overcome and made it worse with successive QE and rate management efforts.

I’d stay in equities and ride this wave a little bit longer. When the yield curve inverts, then move into Treasuries and IG corporate bonds (yields will be even higher then).

You should get significant a capital gain in the short term and income/asset protection during the next bear market, though you would miss out on the melt up at the very end of the cycle. Risk/reward still looks very favorable for equities for the next year or two.

I’m thinking, these new corporate tax cuts have put a lot

of cash into their coffers. They all need a place to put it and with equities

looking toppy, competition for bonds is heating up and

driving down yields. Govt has been wise to sell into this .

Corporations have saddled themselves with a record amount of debt. Junk-rated companies have very little cash, and what they have, they burn up (see Tesla and Netflix). Some companies, such as Apple and Microsoft have a huge amount of cash, and they won’t get in trouble. Many other companies will get in trouble. Easy credit always has this consequence.

Same with individuals.

Do now its clear Apple buying Tesla & ms buying netlfix ;)

I know your kidding, but other people are serious about this. Which always causes a good laugh to make my day.

Why Apple would buy an automaker that cannot mass-produce anything and whose global market share is almost nil, for $58 billion, when it could buy for $42 billion an automaker such as Ford that sells 6.6 million vehicles a year, into which Apple could instantly install its software and hardware?

There is nothing that Tesla has that Apple wants.

That’s not to say that some company will not buy some Tesla assets out of bankruptcy down the road, such as the name.

Thanks again Wolf.

Has anyone noticed(sarc) that Apple products have no moving parts,I think that’s smart.

“Why Apple would buy an automaker that cannot mass-produce anything and whose global market share is almost nil, for $58 billion, when it could buy for $42 billion an automaker such as Ford that sells 6.6 million vehicles a year, into which Apple could instantly install its software and hardware?”

It’s most likely due to Tesla’s huge imaginary mote.

The Fed is truly trapped are they not? They can stop printing money and buying everything that is not tied down, but interest rates will skyrocket and that will implode the system. Or they can print to oblivion and destroy the dollar. You can bet the farm they will go for door #2. The 80% paycheck to paycheck people will be crushed. Perhaps then people will not think I am crazy for saving in silver coins.

I don’t think you are crazy.

At least you understand that bad things are going to happen.

Most are sheeple, and oblivious.

Predicting exactly what will happen, when, and what is the best thing to do now to prepare for it is nearly impossible.

You are undoubtedly doing better than most.

Paul, please check out the commenting guidelines, particularly #3 – the “5%” guideline. thanks.

https://wolfstreet.com/2017/10/07/finally-my-guidelines-for-commenting/

Paul You are being reprimanded for your truth Shame on you( sarc off)

I think that is what the junk bond buyers are expecting also. That is why the risk premium from corporate bonds to treasury bonds is so low. They believe there is little risk. If anything happens that will negatively affect many of the larger companies, junk bond rated or not, the Fed will resume its QE and the increase in yields will stop. We have to remember they bailed out GM and Chrysler last time and those companies didn’t even then represent a significant portion of the economy. And at some point the increase in interest rates will affect state and local governments who are mostly as heavily indebted as the junk bond companies.

Bailouts may happen, but not before stock prices and RE fall through the floor and there is concern about high unemployment. I don’t view the likelihood of bailouts as any kind of insurance for stock prices.

I thought (still think) you are wise, not crazy.

Some event is in the offing, but what will light the fuse is hard to predict. For instance, the central bankers can inflate the housing market to oblivion, but at some point, rents will through the roof, or property taxes on overpriced houses will suck up all disposable income, and the dominoes will start to fall.

Man, you are spot on.

It’s remarkable how little this reality is discussed anywhere. Confidence in the currency is fragile and the Fed has shockingly abused that confidence. Now the Fed have painted themselves into a corner that will require money printing on a massive scale yet people are still in denial over the outcome (don’t expect the dollar to buy much in the future).

Nice work once again Wolf.

The current market swoon reminds me of yet another “taper tantrum”.

Over the last couple of years, every time there is a real threat of rate rises, the market throws a slight fit and the FED will immediately relent and scale back their QE unwind and temper down their “rate rise” rhetoric.

My bet is this time is Not going to be different, because grandma Yellen knows EVERYONE is yoked to debt; like slaves with their feet all chained together to their Roman galleys… all furiously heaving against the oars of the economic ship according to the drum-beat and the whips of the slave driver.

If the ship goes down, EVERYONE drowns together… the slaves drown first of course, the captain of the ship may jump overboard but without a ship with slave rowers, he too will become fish food or be stranded.

There is no escape for anyone if interest rates are allowed to rise beyond the pain threshold. We are all literally in this together for richer and poorer, in health and sickness until total economic collapse do we part.

The market will fall until the FED blinks first….just wait for it. I hope Grandma won’t get a heart attack from the vertiginous view from great heights such as what we have now.

If I remember correctly, and please correct me if I am wrong, the “taper tantrum” resulted in a sharp strengthening of the $ and that spread the trauma all over the world.

This time, the $ appears to be in a secular decline, which may well keep the trauma domestic, until such time as the trauma becomes a liquidity crisis, which will immediately engulf the globe.

2008, IMHO, was exactly that, just a minor liquidity glitch that brought the global economy to its knees.

It only took Paulson and team creating $20 T and loaning it out in secret, another $20 T of central bank QE, and 10 years to sort of get over it.

The next one will be “The Big One”!!!

That’s because people worldwide are fed up with the dollar and faith in it is waning FAST It’s definitely different this time around

Any data to back that up, Frederick? As far as I can tell, USD demand hasn’t gone anywhere. Sure there is recent USD weakness, but it’s within the range we’ve seen over the last 10 years.

Also, check out the IMF data showing its share of worldwide reserves hasn’t decreased:

http://data.imf.org/?sk=E6A5F467-C14B-4AA8-9F6D-5A09EC4E62A4

I expected the USD to tank ~10 years ago as we racked up war debt, but I’ve been proven wrong time and time again. Predictions are tough, especially when they’re about the future.

The US $ isnt going anywhere as the # 1 reserve currency for the same reason that the US is still the global super power of choice for the majority of free nations, which is the Majority that counts.

THERE IS NO BETTER OPTION ON OFFER.

It is that simple.

iran, china, india, and russia, are your next options, in decreasing order of evil.

What sort of madman, outside a national or supporter of one of those nations, would replace the US, with one of those nations???

And our continuing foreign affairs blunders hurt our cred too.

Jeremy Powell is being sworn in February 5th. Yellen’s last day was last Friday.

Oh, I forgot grandma retired 2 days ago and Jeremy is the VIP now. *headslap*. No wonder, the markets took the opportunity to test the Man while they are passing the bacon…I mean the baton.

Thanks for the reminder, Jeremy. Btw, are you actually Jeremy Powell himself? lol.

Cause if you are, do make sure you stand your ground against the Beast and allow this market to fall much further… many folks here are hoping to get into this current dip and there’s still significant cash on the sidelines.

Jeremy can make a mark in history by being the first FED chair to crash the market immediately on swearing in. Monday is coming up … so we’ll see soon if it its going to be Black in color.

“Bacon” Freudian slip there huh Kevin ? I like it

Keep in mind, Powell is only an attorney as opposed to an economist like Lawrence Lindsay and Lindsay has argued the tax bill relies on accommodating support from the FED.

Has anyone heard why last night Lindsay withdrew from being FED chair #2 guy?

This is the big wonderment.

After the change in management at the Fed will they gratuitously trot out Bullard so CNBC can proclaim more QE is inevitable if the market falls a little more?

Or, will the Fed sit silently and watch the panic because they sat silently?

Or will they include a surprise rate hike and sit silently afterward?

Or will they passively stick with Yellen’s stated plan and continue to mumble nonsense at each press conference?

To be seen.

Knowing when to time the next Fed QE announcement is the trick. I’m pretty sure Goldman will know at least one day in advance prior to the next QE announcement but I doubt you’ll receive an alert in your inbox.

By the way it’s hapless Jerry Powell in charge of steering Ben’s steamer over the waterfall now. It’s time for Yellen to get a figurehead job at a hedge fund, collect tens of millions and write an autobiography focusing on the topic of her “courage to act”. They are all so courageous – don’t ya know.

Like Lord Jim, most of the crew has abandoned ship for the lifeboats and left the pilgrims behind to die.

“By the way it’s hapless Jerry Powell in charge of steering Ben’s steamer over the waterfall now. It’s time for Yellen to get a figurehead job at a hedge fund, collect tens of millions and write an autobiography focusing on the topic of her “courage to act”. They are all so courageous – don’t ya know.”\

Pays to be up to date before you pick on old ladies.

https://mainichi.jp/english/articles/20180203/p2g/00m/0bu/045000c

Now that the markets are falling like a rock…I’d like to see how courageous the new FED chair Mr. Jeremy Powell will be. I hope his knees are not buckling under him now.

Just look at the Dow, S&P and NASDAQ on Monday & Tues !

I’ll bet if it drops another 5% over this week, Jeremy is going to wet his pants and drop hints to the market on possible QE4.

He must be thinking: To hell with that Grandma and her QE-unwind. Jeremy’s not going to be the fall-guy on his watch.

That Jeremy above did NOT dare reply to my question, so he could really be the REAL deal from the FED? lol.

If its true, his ego seems a little hurt, after we forgot he is now the new VIP in-charge now ;-)

Hey Wolf, you could potentially have the new FED chair being a regular patron of your website here.

Most of the time, I have no idea who is behind the screen names the commenters use. And there are a lot of Jeremys in this world. At any rate, no “Jeremy” as ever signed in with an email attached to any part of the Fed.

That said, I know that some people at some of the Fed’s various corners are looking at my site from time to time because I’ve had contact with them. But the Fed Chair has so far not been one of those I had contact with :-]

Wolf, wouldn’t you think that there is a pretty low ceiling to how high yields on investment grade corporate bonds could go?

We’ve already extensively established there is a glut of savings out there looking for a return on investment. Years of monetary repression have pushed a good deal of that money into equities rather than bonds, due to the low yields.

As the 10 year gets to 3% or even 3.5% in the next few months and investment grade corporate bonds get to 4.5%, maybe 5%, there’s got to be an enormous number of market participants who would love to take 5% on IG bonds. That ought to cap yields at a level not too much higher than they currently are, no?

The oil bust in 2015 and early 2016 showed that even in the era of ZIRP (now over), the “low” ceiling was around 20% for low-rated energy junk bonds. So this gives you a feel of where junk bonds can go. For investment grade, you might look at a spread of 2% as a ceiling. When the 10-year yield hits 4%, it would mean 6% for the average investment grade bond. When things get tough, the investment-grade spread can be much higher. And the 10-year yield could go above 4% too. So yes, historically speaking, 7% investment-grade yield would still be low, but from today’s world, it will be a huge move.

Thanks.

By issuing more and more debt worldwide since 2007/8 crash, even fractional moves in yield rates and bank interest rates resonate far more now that debt levels are at historic highs.

Room to manoeuvre becomes less and less, as the debt levels escalate.

There is nothing to say that yield rate cannot rise to a given threshold. The fact is under a regime of unprecedented cheap debt for the last 10 years, that regime can very abruptly come to an end, and an era of very expensive debt could be upon us.

Many of today’s Wall Street bond traders hadn’t even born yet when 30 year US Treasuries were yielding over 15% at the bottom of the last huge bear market in bonds. Back in late 1981 and early 1982, the Franklin California Tax Free Bond Fund (munis), had a net asset value of under $6 per share. It had first come to market in 1977 at $10 per share (including a sales charge). At the recent peak in bond prices in mid-2016, its net asset value had not even recovered to $8 per share and as of 2/2/18 stood at $7.30. Yahoo Finance has a price chart for the fund going back to Jan. 1980, in case you want to follow the carnage.

I have not bought any bonds for myself since the great Meridith Whitney sell off in California munis in 2010-11 and will allow my remaining bonds to mature over the coming 10 years.

Netflix just increased my subscription by $2, a 15% increase. I still think it provides good value in comparison to my cable tv bill. I estimate that I watch Netflix more than cable, maybe a 2/1 ratio. This leads to an interesting question, which are really the junk bonds, Netflix or those other guys?

Netflix is also increasing their original content spending to $8B from $6B in 2017. They have been running on negative cash flow in the order of $2B a year.

Plus, competition is only going to get stronger (HBO, Disney, Amazon, etc.) and the amount of quality content is not directly proportional to amount of money invested, it never is.

Are any the Netfix alternatives any good? That type of TV streaming service is getting mote and more fragmented, I mean competition is good but I don’t want to pay three different services to watch three different TV series.

As it is I have “basic” Direct TV and just watch the stuff there.

With Telsa, what is the competition doing? Telsa must be doing something right to always be on the news, and not like Uber who is finding out that yes, there is such a thing as bad publicity.

Amazon Prime is building credible content.

My favorites though are old, more genteel TV series re-runs on CD.

Westerns, the whole “Gunsmoke” series is available for a little over a hundred dollars

Northern Exposure (get the Canadian copy with original sound track), runs for many hours.

raxadian,

Hulu no commercials and amazon prime provide a lot. Plex channels, if you know how to make a media server, add more for free with no commercials legally. I plan to add Netflix when I run out of content on Hulu and Amazon later on. Doing lots of binge watching now. Lots to watch.

I remember a time when Cable selling point, bedides more channels was “No commercials” that lasted only a few years. HBO selling point? Uncut movies and no commercials, that also didn’t last.

So really you need something better that “No commercials” to make me interested.

I found the entire “Are You Being Served?” series in a Costco DVD bin for under $30. It probably had been marked down for clearance. I suspect that just about any series that had been popular in its day is now available on DVD via the Internet.

The big boys are joining the self driving EV chase – – – but – – – AT THIS TIME there is NO competition – startup wise – for Tesla. Uber has several existing and some new competiors chewing on it’s behind.

Only time will tell the future of Tesla.

Or the others.

“Its just how it works.” No, Wolf. Its how it USED TO WORK before the Fed decided to eliminate the free market’s pricing function in favor of a managed economy. And even now as they congratulate themselves for a job well done during the past 10 years, aren’t they implying that there will be no material change in their behavior, just a gentle touch on the brakes for appearance’s sake?

It can be argued that the recent bull markets in stocks and bonds were largely gifts of the Fed. Will those worthies now step back and let nature take its course in the future? Apparently junk bond buyers don’t think so. And what evidence is there to suggest that these investors, among the most successful lately, will suddenly be wrong?

Not all bond buyers/owners see the exact same set of facts exactly the same way, and don’t act the same way to the same stimulus.

For example, junk bond owners probably tolerate more risk (or, perhaps, are greedier).

It’s just how it works.

Short bond ETF may be equivalent to having your own printing press.

To me the logic behind the long bond yields rising is the supply demand situation with the falling US dollar and the increased supply combined with the QE unwind. In my mind only the short term rates are controlled by the Fed and the events causing long rates to increase are exogenous, and helpfully deflationary. The whole risk complex whether it be equities, junk bonds, emerging market bonds etc in a repricing risk off tantrum has different ramifications depending on the sector.

Given the risks is the Fed going to be that aggressive? A good general would prefer to retreat a foot rather than advance an inch. A deflationary event out of China or a stand alone stock market repricing for example, if these events can be contained, is better than a more widespread debacle. The typical way excess debt is dealt with historically is financial repression, and this means inflation and low interest rates. As long as the Fed is perceived as being in the game participants will be found way out on the yield curve. Therefore it is a matter of sustaining credibility more than anything else, at the same time as inflation does its work. I think the Fed would much rather sit on the sidelines and let deflationary events do its work. I’m sure there is a list of things somewhere of situations waiting to implode hopefully with all the relevant contingencies established. After all with everything a bubble it’s a mine field out there.

Thanks again for providing such an excellent forum for discussion on these issues.

Given the risks is the Fed going to be that aggressive?

Of course they are going to be aggressive, it’s their job, as lender of last resort.

>> In my mind only the short term rates are controlled by the Fed

Wrong, wrong, wrong. The long term rates are most decidedly controlled by FRB, via QE and QE-unwind.

They are not the only game in town.

The deficit must be funded, and the ECB and BOJ will start taper and QT soon.

Funds may well start to seriously rotate out of US stocks.

The FRB may well become totally impotent as far as rates on anything much longer than overnight are concerned.

Not that I care much, to be honest.

There are better currencies to be in than the USD, in better markets than the US.

and regulations as to quality of assets and debt to income ratios and such.

>>and regulations as to quality of assets

Quantitative easing could just as easily be called Qualitative easing

>>and debt to income ratios and such.

For new mortgage issuance, yes.

Yes I stand corrected. There is potential for the Fed to control long rates through QE. I had assumed their QE unwind was locked in and hence was a known factor. On reflection they could ease off but this would potentially impact credibility in that they publicly underestimated the effects of their actions. It may turn out the QE unwind is a material factor in the recent increase in long bond yields even though the unwind has barely started. If this is the case the planned unwind will probably not happen. This just reinforces my belief that Fed has to do very little to have an impact and therefore would prefer to act very slowly and carefully. This being the opposite of aggressive.

I wonder, we have now a generation on traders on Wall Street that have no experience of a real bear market, all they know is to buy at the f*ing dip and neither do they have any experience of money having an actual price, having experience only with ZIRP etc. And what about people who have made their first investments during the last few, happy years, will they be able to ride out a bear market with falling stocks etc ?

Then the algos that apprently handle a ( too ? ) big chunk of trading, how will they behave when things really begin going south ?

And what if the FED loses control of rates and rates begin living a life of their own, when will the wall be reached, ie when will the cost of serving existing debt be too much for the federal state, states, local councils, corporations and ordinary people ? What then ?

Peopel like Steve Cohen and wolf are asking the same question’s.

That is a problem.

People like Cohen note entire trading floors where the only peopel who have ever worked through a bad black day, are the bosses. Thats dangerous as Algos dont work for you, on a black day.

I think algos where a factor in the 665.4 – on the Dow. They not written to handle such moves.

IG rates at 2% above the 10 year are going to be rather disconcerting for the geniuses borrowing to buy back shares to boost their stock price.

I think it is funny that a lease payment on a depreciating asset is collateral. Sort of like a cool mist in the early morning.

The stock market has made it abundantly clear that as long as the Fed remains dovish, the market will rise quickly until it explodes like a supernova. This is why the Fed must take the stock market down a good 10-20%. The Fed will remain with its interest rate increases until the current market frenzy is extinguished.

More pain to come over the next few weeks. There is no need to revisit the thesis until stocks are down 10%-20%.

The HYG can go to zero, and Netflix and Tesla can follow, but what happens to energy? The last great surge of new drilling was done on cheap High Yield Bonds. This is where the Fed is screwed, as rates increase the price of energy will rise, and that hurts our energy exporting business and causes consumer pain and destroys lots of r-e-a-l g-o-o-d jobs.

If Prof. Steve Keens, Kingston University, London, is right and it’s unsustainable private debt that causes financial crisis’s then we could have the makings of something mainstream economists can’t seen coming because in their model private debt is just that; private debt and is not a cause of a financial crisis. If rates really do rise in a significant way how many corporations will be stressed to breaking when their debts have to be rolled over? Will home sales simply slow on rising rates and how much will home prices fall because of rising rates?. How many loans were adjustable rate taken with the assurance that rates would be low forever? How much will car sales slow with rising rates? If businesses have leveraged debts in the hopes that rising sales would bail them out and sales do slow on rising rates then how many will fail and will that snowball? I think we could be seeing something that ought to frighten the hell out of us.. Maybe not come Monday morning but it’s coming.

√

Out of most of you any way.

Me I have nothing on credit.

Private debt in US is between 3X to 4X the public debt. Of course, the capital(ism) fundamentalists believe or espouse that private debt does not matter, because private == good or some other simplistic nonsense. Steve Keen is correct, it is unsustainable private debt that has caused every bubble and crisis so far in modern US history.

“Steve Keen is correct, it is unsustainable private debt that has caused every bubble and crisis so far in modern US history.”

How about Insane unsustainable lending.

If you are willing to advance large quantities of money to NINJA people who can walk away if the speculation deal goes bad why wouldnt they take it. The NINJA has nothing to loose.

Behind every over leveraged Person/Entity is an Imprudent lender/Loan shark/Speculator who is at fault the most???

Who is the root of the credit problem, the over-leveraged Entity/Person, or the Imprudent Lender/Loan shark/Speculator, who lends to them???

Very hard for the Drug addict to get clean, when there is a legal dealer, supplying on credit, on almost every street corner.

“How about Insane unsustainable lending.”

That is the private debt that Keens is talking about..

Here is Keen lecturing in 2015 on a YouTube posting.

https://www.youtube.com/watch?v=twkH2z4gxr0

Most likely the next crisis will start in a hedge fund or insurance company.

If you are going to talk about private debt you should define it. Do you mean household debt or all non public debt. Every financial panic hasn’t been caused by household debt. LTCM was private debt, not household debt. It got bailed out, at the insistence of the fed, to avoid a financial crisis.

All private debt.. Household debt affects each household to different degrees but I have never heard of household debt bringing on a financial crisis. I suppose it could but mostly, as I understand it, it reacts to stresses caused by debt implosions by corporations and businesses and banks that have become overextended. When banks tighten then households can become insolvent which stresses more banks and so on. It all becomes a closed loop debt spiral. The vicious cycle. All leading to layoffs and more debt defaults. All of the Wall Street banks were private banks and all but Lehman got bailed and the un-bailed collapse of that one bank nearly collapsed the whole system.

Most MSM economists dismiss private debt as being in balance between those who are impatient borrowing from the patient. Keen explains that this fallacy is the key to why economists like Krugman didn’t see the coming collapse in 2008 and why Krugman has spent the last 10 years trying to explain it away..

I have enclosed Keen’s YouTube lecture posted in 2015 and take notice that only 4,000 hits were posted in 3 years..

https://www.youtube.com/watch?v=twkH2z4gxr0

You have never heard of household debt bringing on a financial crisis??

What do you think happened in 2008???????

MBS is an acronym for packaged household (mortgage) debt.

Paul Fillion

True, but what I was thinking of was personal household debts such as medical, car loans, credit cards, and mortgages which were actually pretty solid for the majority of families.. It was the banks that leveraged themselves up by as much as 33 times so when 3% or less went bad it brought down the whole house making them insolvent.. It was the banks that didn’t screen clients when making subprime loans but they didn’t care when they could just bundle them into MBS as Triple A and sold them all over the world as solid investments. The one thing economists kept saying over and over was subprime was tiny fraction of the market, which might have been true, but it was the leveraged banks who bet heavily which started the crash..

Its the way stuff is held this time–non banks and passive retail–that will make corporate debt the last (and worst) to capitulate.

We saw some of of this in 08, when securitized debt becomes so bespoke that continuous MTM is ignored until you try to actually sell it.

Then it goes par, par, par, par…80.

Then the REPO market for AAA securitized seniors bonds goes BOOM, and the “structured finance markets” close.

What many do not understand is that this time the FED is actually ready for it.

They may not be able to avoid it, but at least it is not the Primary Dealer banks that have the exposure this time around.

The “non-banks” have waded into to fill the Dodd Frank void with investor money and a stunning disregard for risk in any traditional sense.

For 10 years those who took the most leverage and risk did the best, so it shouldn’t be a surprise that this is all that is left now.

But DF held the banks back, at least in many cases, and that left the non-banks free to go nuts.

Look at BB mezz at under 6%.

NO ONE IN THEIR RIGHT MIND WOULD PAY THESE PRICES WITHOUT NON RECOURSE LEVERAGE.

The FED HATES these non bank companies anyway–the STWDs and LADRs and NLYs of the world–they sit outside the regulatory envelope and force feed the banks risk at operating costs they cannot afford.

That is why no big banks make money, they can’t compete with wholesale financial engineers.

The good news is that when this bubble bursts the non-banks will be gone forever, or 25 years, whichever happens first.

Then the traditional banks can start to make loans again that make economic sense for lenders, borrowers AND society at large.

Good Riddance.

Interesting write-up but I find the much of the jargon very obtuse. Let me see if I can clarify, please correct any errors found. I added some terms that I will use below.

MTM= mark-to-market

MBS = mortgage-backed security

REIT = real-estate investment trust

USG = US government, the federal government

GA = Government Agencies (GNMA Ginnie Mae, guaranteed by USG)

GSE = Goverment Sponsored Enterprises (Fannie MAe and Freddie MAC)

FRB = Federal Reserve Bank System

NLY = Annaly Capital Managment ( a speculator in MBS spreads?)

LADR = Ladder Capital Corporation (a REIT?)

STWD = Starwood Property Trust ( a REIT?)

After digging around a bit I learned there are Equity REITs and Mortgage REITs. The above list may contain a mix of both.

Taking a step back, I get the sense that author RD’s thesis is that in the 2009-2018 bubble, unlike the previous 2001-2009 bubble, the risk has been loaded upon REIT investors, stock investors, bond investors, GA (taxpayer backed), GSE (not supposed to be taxpayer backed), but NOT on the banks. It follows that the banks, which control the FRB, this time would like to crash the markets and scoop up a lot of assets at the resulting firesale prices. This ensures that the FRB this time around WILL stay the course with interest rate increases. It is a war between different factions of Wall St (banks versus non-bank brokers and shadow-banks, roughly), and they do not give a hoot what happens to the peons, even if the peons end up as collateral damage.

I have been thinking along these lines myself, that is, what would it take for banks and some of Wall St to WANT to crash the market valuations? And I think the above explains it. Don’t fight the Fed (FRB).

pretty close, yes

After reading justme’s comments on RD’s I went to look at a list of Primary Dealers. There are a lot of US branches of foreign banks and institutions.

The next thing that caught my eye was the number of them that are listed as LLCs? I guess I don’t understand LLCs because I thought they were mostly for small entities that weren’t yet big enough to be a S or C corp… Is this OK or is it shady?

Then the number of those that have had fiduciary issues or big trading losses in the past are also listed including Wells Fargo. Societe Generale, Deutsche Bank?

That makes me wonder if the premise that the Primary Dealers are all as sound as implied. And according to Steve Keen, they don’t even have a clue as to how private debt can affect the entire system. He is pretty disgusted with main stream economics and their very incomplete models. At some point we are going to see if he is correct. Maybe soon.

Investment banks were traditionally partnerships, now LLCs. They take the partnership route to avoid regulation. A bunch of guys doing business as a partnership can do anything they want with their money.

Maybe much sooner.. Keen took his inspiration from Minsky. The same as in the “Minsky Moment” when what can’t happen, shouldn’t happen, just did..

Nothing goes to heck as Wolf puts it in a straight line but if the Fed is reacting to rising wages, which are inadequate as they are, with some serious tightening then I feel we’ll see something the Fed and all of their neoliberal governors can’t see coming.. They never do..

They will feel the pain, sure.

But Dodd Frank has ensured they are so overcapitalized that there will be no running—that will allow them to re-intermediate and tale over credit price discovery in lending once again.

Pension plans have actually had it quite good the last few years (though they may not agree), what with bonds and stocks moving higher. Yet many are still well underfunded. If we go to stocks and bonds both moving lower, watch out for the crisis in funding. With a little inflation thrown in, requirements will go up, but returns will never match the projections. This will be the extra big crisis.

The only argument contradicting Wolf’s point is that not long ago European junk yields were about equal to 10 year yields,so why can’t US junk yields do the same?Admittedly that argument sounds ridiculous,but the fact that TSLA has a huge market cap along with huge cash burn is also ridiculous

I guess the Fed is less scared because they already bailed out the GSE’s and the banking system?

Tesla… I think they would be smarter to sell (a lot) more stock at this elevated level and borrow less (0), debt is dangerous in a recession.

Their products are great, definitely having major problems ramping up to meet demand for product. Buyers have patience now, maybe not in recession. Battery factory will have value no matter what.

Equities and euphoria are holding up the economy, economy is growing just enough to hold up the market. If either goes the other follows… back in Oct 2007 equities fell, economy went into recession two months later.

Low rates and surging bank loans have kept economy growing a real 1.5%.

Commercial bank loan growth already down 2/3, higher rates will reduce it further.

IMO growth will not continue as rates climb.

Recession will bring low rates to the long bond and high, nose-bleed rates to junk. Spread jumps not just because junk goes so high but also because treasury rates fall.

I expect 1 handle on long bond and 0 on 10-year. And these will be high vs. Japan and EU.

Products are great? Says who? Electric cars are not green or efficient. It takes a lot of rare earth metals to build them and they end up being “plugged” into the petroleum/coal/nuclear power grid anyways. Plus they are so overpriced and out of reach for 99% of the world’s population. This Elon Musk worship is so misguided and disgusting. I’m not saying you but in general. What does Musk REALLY do to help mankind except suck off the government tit and enrich himself? Flamethrowers? LOL………Bezos, Musk, Zuckerberg are not great visionaries they are pompous, self righteous, arrogant quacks who profit off the backs of the American tax payer. I don’t know if it was someone on here or on another site that said at least the robber barons of the Gilded age built great monuments, libraries, civic centers, museums etc . back in the day. What doe these build for society? What do they really give back? NOTHING!

‘Tesla… I think they would be smarter to sell (a lot) more stock…’

They WOULD have been smarter. Good advice three days ago but now those days are probably over.

When the alternative to selling stock is bankruptcy, and the market knows that, it will have to be one heck of a deal.

The Fed has been looking for an excuse to raise for awhile. There’s a difference between needing to raise (legitimate inflation fears) and a tactical move to allow for future rate cuts if the economy sours.

I’m not sure how state mandated minimum wage increases are sending the fear of the inflation god into the Fed. Just don’t see it since the Fed has willfully ignored healthcare and housing costs.

Minimal incremental raises this year according to plan. They are well aware of the importance of Junk rated debt and stock buybacks to the new US economy.

what’s to stop new Fed Chair Powell from just firing up the monetary engines and having overseas funds (Fed front companies) just keep up the buying and stocks rising? I think Wolf and most commentators underestimate the utter corruption, amorality and yes psychopathology of the people in charge of the printing press….