Shares Soar. Bond market on cloud 9.

Wall Street gushed over Netflix’s “earnings” Monday after-hours, sending its shares up 8.5% to $246, from around $10 five years ago, giving it a market capitalization of over $100 billion for the first time. Actually, what everyone gushed over were the metrics that Netflix wants everyone to gush over, namely the number of subscribers that pay monthly fees and subscriber additions, and they’re growing. Revenues jumped 32% to $11.7 billion for the year 2017. And there were some gems in its earnings report today:

Its voracious cash-burn requires massive borrowing

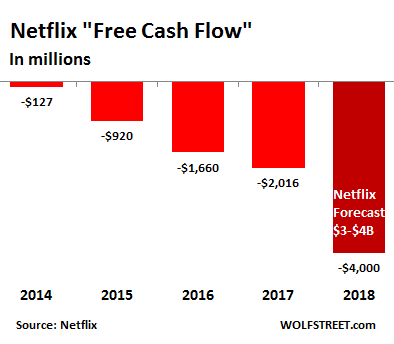

Netflix had a “free cash flow” (FCF) of negative $524 million in Q4, which brought the total for 2017 to negative $2 billion. FCF is a measure of the amount of cash it earns or burns. For 2018, Netflix expects to burn $3 billion to $4 billion in cash, it said. This is not exactly a propitious trend:

A company that has been publicly traded for 15 years should have figured out by now how to be cash-flow positive. But no way. That’s not the goal. The goal is to create new content no matter what the costs, and borrow the money to do it, and hope that revenues will eventually catch up. That’s what it said:

When we develop a title like Bright, the cash spend is 1-3 years before the viewing, associated membership growth, and P&L expense. Thus, the faster we grow our originals budget (particularly for self-produced content), the more cash we consume. We are increasing operating margins and expect that in the future, a combination of rising operating profits and slowing growth in original content spend will turn our business FCF positive.

Meanwhile, back at the balance sheet, to make ends meet under these conditions, Netflix has to sell a running ton of debt, including about $3 billion of bonds in 2017:

- $1.6 billion in 10.5-year notes rated B+ (four notches into junk) at yield of 4.875%, in October 2017;

- €1.3 billion (currently $1.6 billion) of 10-year unsecured junk bonds at a yield of 3.625% to take advantage of the ludicrously low borrowing costs for junk-rated companies in the Eurozone.

The $3 billion in borrowing in 2017 was up from $1 billion in 2016, and up from much smaller amounts in prior years. And 2018 issuance will be a doozie – “We anticipate continuing to raise capital in the high yield market,” it said – given its cash burn of $3-$4 billion.

So the pile of debt has ballooned in the year 2017 at a disconcerting speed:

- Non-current liabilities rose 15% to $3.33 billion.

- Long-term debt soared 93% to $6.5 billion.

- Total liabilities jumped by 41%, or by nearly $5 billion, to $15.4 billion.

The “net income” mirage

The company reported “net income” of $185 million for Q4 and $559 million for the year 2017. It said it burned $2 billion in cash. And then it said something else:

The new limitation on deductibility of interest costs is not expected to affect us.

The new tax law limits the extent to which companies can deduct interest expense from income. Under the old tax law, 100% was deductible. But in order to be able to deduct it, and thus save on taxes, a company must have taxable income to deduct it from. A company that loses money doesn’t pay income taxes, neither under the old tax law nor under the new tax law.

For 2018, there are limitations on the deductibility of interest expense, but these limitations don’t “affect” Netflix. Why? Because Netflix does not expect to pay any income taxes. In other words, on its tax return to the IRS, Netflix expects to report a loss.

Is the bond market on cloud 9?

So why would the bond market continue to fund a junk-rated operation with a voracious cash-burn rate, and with nearly $10 billion in long-term debt and “non-current liabilities” that will likely grow to $13 billion or $14 billion in 2018? Why would the “high-yield” end of the bond market fund that $3 to $4 billion Netflix will burn in 2018? Netflix provided part of the answer: “High yield has rarely seen an equity cushion so thick,” it said.

In other words, the junk-bond market has rarely seen this kind of share price and market capitalization, and the sky-high share price itself – or the “value of the firm,” as Netflix put it – “is what also ultimately secures our debt.”

This shows that the corporate bond market, and particularly the high-yield end of it, is still on cloud 9, even as the Treasury market is starting to keel over. Investors buy anything with a slightly higher yield, for now. And as long as they do, Netflix can get funding at a very low cost despite its junk rating. And given the supply of easy funding, its share price can stay sky-high, and the sky-high share price guarantees this funding. If this sounds circuitous, it’s because it is. But hey, that’s what a bond market and a stock market on cloud 9 will do.

The US government bond market has soured, even the 10-year yield is surging, and mortgage rates have jumped. Read… What Will Rising Mortgage Rates Do to Housing Bubble 2?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Here is why I am going all in on Netflix. A minus $2 billion negative cash flow for 2017 = a stock price of $246. If Netflix’s negative cash flow doubles in 2018 to a minus $4 billion, I expect the stock price to double to an easy $500 per share. I don’t see anything wrong with the math here.

You’re really onto something there, @Joan. I think you should be a professional financial analyst. As I don’t see anything wrong with your maths either, I’m thinking of going IPO on my mortgage. Debt plus upcoming necessary maintenance plus recurring costs against possible job redundancy should equal a very solid financial foundation on which to base…oh, I’m not greedy…a $50+ initial share price. You in?

I like your plan :but you would need a mortgage in excess of 1bil. to to justify such a lofty ipo value.

Your math is impeccable. I would simply add that an additional 2 million subscribers vs street expectations has provided the stock something of a lift.

But to Wolf’s broader point, this is not the first company to finance itself liberally with lots of stock sales and junk debt. (Amazon, Tesla)

What an article. My wife is watching netflix tonight, I think. I seldom bother. It is my son’s account so we have yet to pay for a show. My sister-in-law has a bunch of folks on her account. No wonder they don’t make any money. No one pays, because no one has to pay. Pretty weird business model.

Well, they could put a stop to that almost immediately. What I’m wondering is why don’t they? The time is long overdue to restrict concurrent access to one per paying account.

I think a huge problem for the Netfix, etc. business model is that the cost of access is peanuts compared to the mostly monopolistic business model monthly pricing of getting the electrical pulses representing ones and zeroes of the content to one’s home.

I am not worried about Netflix; once they cornered the market, they will start raising prices like Amazon. Amazon prices on many items are now double what I pay at a local store or online elsewhere, but the peeple keep coming back for more.

Got some significant samples of your claim?

Amazon generally does a pretty good competitive job.

Amazon definitely has algos driving price. Anything on the Wirecutter recommended site experiences a significant price jump. I was shopping humidifiers recently and found that Walmart often was far cheaper for online shopping with pick up at my local store when compared to Amazon. It’s key to cross shop any purchase as Amazon tends to have a great price, but there is no guarantee they are the low price.

Amazon just increased Prime subscription by a few dollars. They’re sneaky like that.

Larry

Maximus Minimus made the claim that “…Amazon prices on many items are now double what I pay at a local store or online elsewhere…” – all I’m asking for is a few examples to support his charge.

Unsubstantiated claims are a dime a dozen (ie: cheap).

“High yield has rarely seen an equity cushion so thick,”

Because Amazon hasn’t entered the crypto space yet. Eventually Bezos or one of his minions will happen upon the idea of a coin tied to a share of Amazon stock. It will be appropriately named for some flora or fauna in the Amazon Rainforest and quickly renamed “Ammo” spendable in the Amazon ecosystem for goods and services.

Every citizen of planet earth will convert his currency for “Ammo” and have that currency on account in the Bank of Amazon. The value of “Ammo” will increase as the purchasing power of the worlds paper is diminished and to not own “Ammo” will be the new wealth gap.

“Ammo” will eventually become the worlds reserve currency. You won’t be able to shop without it.

Psych DVD set for one.

I regularly go to Costco.com and Walmart.com in addition to AMZN

I also go to stores like Bed Bath for toiletries.

The prices are all over the place. and yes sometimes double if the consumer does not mind being taken advantage of.

recently I bought a package of 12 pens for 13 bucks at amazon and I received 1 pen. The going price was 14.

Then I have bought headphones and have received knock offs

I had tried to buy packaged food but what I received was at stale dated product.

Now-I just do not trust Amazon

I am currently looking for a sound bar so I figured I would compare. In Canada the LG SJ4Y @ Bestbuy website it cost $230, Amazon is $640 for the matching speaker but lists older models for $400.

Don’t simply trust Amazon to be the cheapest, they still have to make money at the end of the day. As people get wise to the prices we will see Amazon come back down to reality.

M&M

Amazon sells 536,641,219 unique products (https://www.scrapehero.com/number-of-products-on-sale-at-amazon-com-august-2017/)…

…and you found a set of kitchen containers that you could buy cheaper in the discount store.

Wow. Good job.

Sure.

Last week I was shopping for kitchen containers. Found them at a local discount store for $8. Checked at Amazon, they went for between 14 and 25!

Now, this is a great discount store which wouldn’t be an option in a rural area. As an aside, they carry household cleaning items “Made in Germany” for Chinese prices, debunking the myth about the high cost economy.

I also buy clothing by a Swedish company at a online discount site. On Amazon, these are super expensive.

Let’s not mention that on Amazon prices jump up-and-down between two visits, kind of like auction, but sometimes both ways.

Just wanted to add, that I hate shopping malls with a vengeance. That’s why I like online shopping, but go to Amazon as a last resort.

Spot on. The investment thesis is “monopoly” even if no one will say it on the earnings call.

By the way, I think Amazon remains a good deal, a least on the down-the-middle items like books, toys, and dog food that we buy.

I have a Netflix account. The Netflix originals do appear to be growing in number like wildfire. However, 90% of the Netflix originals are pure garbage, not worth watching even if you have time to kill. These are low budget flicks with extremely poor acting. They should pay you to watch it.

+1. I can’t even get into the Stranger Things. Someone told me it takes a while to get into it. The problem with Netflix as my friend pointed out is that you can binge watch a series. Why is that a problem? Well on cable, there’s a time gap between episodes, so content is produced with the intention of increasing the chance of the audience coming back the following week i.e. cliffhangers are almost a necessity. By definition Netflix does not do that very often, and I think that makes less compelling shows.

Stranger Things was great!

Refreshing to see something other than another laugh track comedy aimed towards the common denominator.

Netflix also has runs documentaries and movies about the housing bubble / economic bubble and what not.

They crushed the cable TV market, and probably have done some shakeup with regards to the movie industry.

$20 mil x 3 for Chappell 1 hour specials is dumb though.

I’m with you. Netflix is basically just another TV channel or, at best, a home movie theater. There is a finite limit to the amount of creative talent capable of making ‘watchable’ entertainment and a finite amount of time people ( with disposable incomes ) have to watch entertainment.

Maybe AI and CGI can overcome the constraints of the former but unless robots are prepared to pay for entertainment there is hard limit to the latter.

Hmm.

Robots already write the news, serve the adds while other robots consume those news and those adds.

The robots even do A/B split tests to improve the spaminess of their work

As a side effect, the news gets ever weirder when chains of robots consume a bunch of robot news and regurgitate their understanding of it.

It is only logical that the same will happen with movies- it is happening now with robots doing mashups of popular children’s characters on YouTube to suck in add traffic from kids left in front of an iPad.

When bitcoin mining blows up all that hot hardware will hit the market for nothing -/ and then this will really go exponential!

I’m more shocked that Netflix doesn’t seem to have any price controls in the bid for original content. Who was competing with Netflix for Dave Chappelle’s new original stand up?

http://www.businessinsider.com/dave-chappelle-salary-netflix-comedy-specials-deal-2016-11

This is not expensive content to produce, and yet Netflix is handing out gargantuan sums of cash to popular comedians.

I enjoy Netflix and like some of the originals, but I really have to ask if Netflix is entering into bidding wars with itself and thus creating a content bubble.

Netflix has separated investors from their money without having to submit to market discipline. There’s no natural limit to the price.

I agree it’s not sane, but how nice of investors to subsidize our movies and cab rides! The money men think they’ll skin us in the end but that’s no sure thing.

I think once people get used to cheap stuff, then as soon as you raise the prices, many stop using your services. I think the likes of NetFlix, Uber, etc. are dreaming that later on, they can raise the prices and thus become profitable.

The Netflix comedy shows are awful, I never watch them. Most of their “original” content is awful. I watch mostly foreign shows and love the shows from places considered obscure, like northern Europe, ME, and even Russia. The cultural differences are fascinating.

+1! LOL

When did the Film Actor’s Guild grow another “A”?

The main thing going in Netfix favor is that all replacements are too fragmented. Either you get Netfix or pay at least two of the other alternatives to get similar content. Until most companies start to realize Netfix replacements need to be like at least basic cable not like buying extra channels for TV, the fragmentacion of content on netfix wannabes won’t stop.

An alternative would be to watch little or no TV. My life is certainly richer for it, and not only in the pecuniary sense.

Hear, hear; I can’t even stand TV anymore. What a waste of your limited time to sit on a couch and watch the idiot box.

American corporate tv is basically dead.

Very true, and idiot box is an accurate name. I do enjoy watching sporting events on TV, and the technology with the cameras is truly amazing.

For the best picture and sound, the old rabbit ears are the way to go. My Panasonic plasma looks great with the Dish Network HDTV satellite playing on it, but the same program showing on the antenna input, which is broadcast for free, is even better. The Dish subscription with sports package isn’t cheap, but the programming is fantastic.

Netflix? No thanks. $100 billion market cap with total liabilities of – $15.4 billion and a 2017 net income of $559 million??? No thanks to being a subscriber or a shareholder, but they and Tesla have made a lot of investors rich, eh?

Depends what you watch. If you rate the production output of the last decade, that’s probably true, but I can’t judge not having watched any of it. However, when you go back to the past century, you can find some valuable series, movies, and documentaries. Some nature documentaries by BBC are once-in-the-history.

have you tried Hulu? I find it has more recent shows, has new shows weekly on series like TV and they do their own content also. Very similar price. I just closed my Netflix as I find Hulu much better.

The best part of this joke is that it is in fact reflective of what would happen. The thought police types intent upon ruining absolutely everything would jump on the idea in an absolute snap.

I can see the article title now:

“We need to talk about the financial media and its problematic acronyms.”

Wonder what Netflix’s share price will do if they announce they’re doing something involving the block-chain.

“Netblox?”

Questions/thoughts on Netflix:

1. Revenue per paid member seems to be about $115 for total memberships at the current run rate. That means the average shareholder gets about 1/4 of a subscriber’s revenue per share. So by buying one share at $250 I get theoretical access to about $30 of revenue and $1.25 of profit. Great deal! By comparison, for each share, Netflix will burn $6-8 of cash next year.

2. But but but … the growth … US member growth for the last year was only about 10%. Not “stellar”. Also the number of unpaid memberships seems to be up more than the paid ones (percentage wise).

3. Growth seems to come from international … at lower prices and lower margins.

4. Streaming revenue growth was 35.3% while subscriber growth was 24.2%. So what we see is a slowdown in subscriber growth made up for by raising prices. In a low inflation world there are only so many quarters that you can pull this off in without running into trouble.

Summary. Interesting company, but way way way over valued… unless the world population goes to 20 billion and Netflix sells all of them a netflix account.

Here in Europe the basic Netflix subscription is about (a few cents more or less across the spectrum due to different taxation) €7/month, all taxes and extra fees included, a true pittance compared to the competitors, but double that will allow up to 4 different devices to watch Netflix at the same time, meaning they are effectively giving away two subscriptions for free every two paid ones.

I honestly have no idea how Netflix can go close to breaking even, let alone turn a profit at those prices, even pricing in they do away with sports (the most expensive part of TV package deals). I mean… I have a subscription to NJPW World and I pay about €7.5/month for that.

Somebody must be subsidising the whole endeavor.

Moody’s presently rates Netflix B1 meaning “speculative and high credit risk” and Standard & Poor’s rate them B+ if I remember correctly, pretty much the same thing. B+ rating means “the obligor currently has the capacity to meet financial commitments but adverse economic, financial or business conditions will likely impair the obligor’s capacity or willingness to meet its financial commitments”. I love Wall Street trying to pass financial junk for something not so terrible.

In short Netflix is firmly in junk territory, as confirmed by the yield they pay: bonds maturing in 2025 yield 5.85%, which is in line with the BofA Merril Lynch US High Yield Effective Yield (5.76% right now).

So who is paying the subsidy?

As I am far too lazy to look up what Netflix pays to banks for their ordinary loans, I point my finger in the direction of shareholders: $246 for share is a damn good collateral to bring interest rates down.

I am biased here since I own Netflix, having bought back when Reed Hastings blunder regarding DVD vs online memberships was going on. Fast forward, and now I have a 10+ bagger on my hands. I have sold enough to cover the initial purchase, so the remainder is play money, but I find myself like a deer in the headlights watching in terrified wonder as this thing just keeps going. I find it interesting that we all know Netflix stock is overpriced, so only fools would buy it, and for other reasons, fools like me are unable to sell. What a strange world we are in now.

Just keep it till it actually drops, then sell it. It won’t go straight to Zero anyway. We see pretty big misses being punished by immediate 10-15 % downs in Scandinavia at the moment, yet, the stocks tend to rebound to about half of the initial drop shorty after. So, there is time.

Usually, unless there are other reasons such as dividends or taxes to hold on to a stock, I would guesstimate what the volatility is (how much the stock normally changes from the average in % terms, averaged over the timescale one usually looks at the price movements).

If the volatility is 5% daily volatility then one could have a “closeout” point at “If this thing suddenly drops by more than 10% in 1-2 days, I shall sell”.

By having a “exit recipe”, “strategy” is too fancy, the decision is already made and mulled over. When the event happens, there is not need to think more, one just have to execute.

I think there will be another six-eight months of rising stock markets before any correction happens. Might as well get that off the table too.

PS –

I.M.O. it is risky to leave an automatic stop-loss instruction (fixed or trailing stop) with the brokers because their traders will of course game those stops. Also My Stop probably will go right to the bottom of the execution queue if anything happens, guaranteeing pretty much the worst sell price of the day.

In a crash, stop- losses won’t work. The market gaps past the order point in a second. A guy had a stop- loss on Sino-Forest on the Toronto and then the OSC halted trading after Muddy Waters accused it,correctly, of being a fraud. The guy’s order was finally executed at 6.25. At least that was more than the zero it went to.

This was big one, not a thinly traded mining stock.

That was a crash in one stock but the flash- crash was a warning of how fast this entire robo-market can drop.

Your broker is not going to lose money to execute your order. He will sell at the stop- loss point if he can.

Forgot to mention: his stop loss was at 16 and change.

Yep. Exactly. And one is showing ones cards, so to speak!

My first random excursions into the market was with DATEK, later acquired by Ameritrade. While there it happened several times in the morning, right on the open, that an order exactly matching my meagre position just “happened” to trigger my stop loss, then exactly the same meagre position was sold minutes later at +5%.

Then I Googled DATEK and found out the history of the people running it and understood much better why this could happen!

If there is a big move, either the broker’s computers will move the big blocks first (or the execution centre the orders are routed to will prioritise, following its own agenda).

The result is that my meagre position of maybe a few thousand shares will “float” on that stack of transaction, kinda like a saturated drain during a rainstorm, until traffic dies down and it eventually executes. When traffic dies down, that is usually at the low of the day, where the flow reverses because the robots “know” that there often is 1/3-1/2 retrace of the first excursion. Which is rubbing salt in the wound.

I have a bunch of Netflix shares and I do subscribe to Netflix 2 months a year as I exhaust the good content in 2 months.

Tried Netflix twice. Once when it involved very complicated procedures because their service wasn’t officially available in my country, and again when it was. Problem is that their content is pathetic.

Netflix should make content using Wolf! I’m sure Wolf could add subscribers and his cost per episode would be far below Game of Thrones’ costs.

Netflix is paying absurd amounts for content . This model requires injections of debt funded new content periodically to keep its current subscribers from cancelling . I have been a subscriber for maybe 2 years now and have exhausted my viewing preferences . If you can wait a few months most movie theater new releases will appear at a red box rental for 2 dollars. Seinfeld netted a 100 mill deal with Netflix for this:

http://www.businessinsider.com/jerry-seinfeld-move-to-netflix-comedians-in-cars-getting-coffee-deal-2017-1

Nflx has a flawed business model.Its subscriber growth is dependent on foreign countries.The largest potential market is China,which is never going to be profitable for Nflx.Its second largest potential market is India,which because of cultural issues is increasingly costly to penetrate.

The other side of the equation is acquisition content acquisition.While there are still some major movies available on Nflx,most are old tv series and home produced series.The cost for their home productions had grown exponentially and is approaching 7-8 billion.

Nflx is hoping that their subscriber growth will continue as they reduce the amount spent on home grown productions.Inherent in this argument is the hope that their home grown series will continue to attract viewers into the future.While this happen in some instance ,it is very unlikely to apply to most.SoNflx will be a position where it has to spend more and more to maintain its subscriber base

As an aside Nflx plays games with its accounting.If it amortized its content costs over a shorter period of time ,its losses would go up

It seems people only care to own stocks that go up, no worries about the debt piling up, no worries about burning cash, no worries about a price earnings of 100 or 200 with no sign of profits.. If they go up, that’s all that matters. The Shiller PE ratio is at nose bleed levels. The is no point of giving advice to anyone anymore, as we would be defined as the doom and gloom people, how we will never getting head without taking risks. But I digress.. Lol

Netflix sounds a lot like Tesla to me. The “logical” thing to do would be to short the stock, and even the bonds, but anybody who did that would end up the same as the people who short Tesla’s stock: getting carried out on stretchers as the stock keeps rocketing upward.

Right now, the market is like Iron Mike Tyson doing his bull rush toward you. He’ll knock you out 99 out of 100 times. At some point, however, an opponent will land a jab that puts a glaze in his eye’s and a little uncertainty in his step. That’s when to begin your shorts. You at least have a good chance.

Collapsar,

Your comment sounds about the same as the highly respected investors, interviewed in “Barrons” in the 1997-1999 time frame, where they admitted to having lost their shirts (and investors) shorting the clearly worthless telecoms and dotcoms during their non-stop run-up towards the 2000 collapse. Check some of the archived interviews from the mag to verify, and you’ll see that the same problem was happening back then.

Great article, Wolf.

I’m old enough to remember a time when a company share price was largely predicated upon the commercial and operational performance of that company.

A company making annual losses, while increasing it’s level of indebtedness, and “burning” cash, has no redeeming commercial features in my view.

Then again other media companies such as Rupert Murdoch’s media companies have been getting away with similar antics for decades.

When the Fed will raise rates that will rattle junk bonds investors.

They will move into the safety of the $US10y and push rates down.

A US recession, lasting over 2.5 years will be a new “rock” hit on Deca record.

This squeaky music will push the $UST10Y further down.

Wolf, I knew last night you would have a Netflix article. I looked at some data on Yahoo last night, I need to take a longer look at their intangible assets ( >9B) in the last 10-Q, should be interesting.

I need to stop being so predictable :-]

Nice P/E

I’m noticing the PCK municipal here, does this also qualify as junk?

The number of antenna offerings is growing, at the end of the day television built around the daily cycle of life has more appeal. The five o’clock news. Services like Netflix rip the context out of television viewing, something that reassures us about the cycle of life.

These ain’t your grandma’s T shares.

Another Ponzi market “success story” until the financial reckoning day can no longer be deferred.

Hedgies are going all-out to lure the last of the retail-investor marks into the Wall Street-Federal Reserve Looting Syndicate’s rigged game.

https://www.marketwatch.com/story/head-of-worlds-largest-hedge-fund-says-if-youre-holding-cash-youre-going-to-feel-pretty-stupid-2018-01-23