Variable-rate mortgages, the HELOC phenomenon, and new stress tests meet higher rates.

By Steve Saretsky, Vancouver, Canada, Vancity Condo Guide:

The Bank of Canada raised interest rates another 25 basis points last week. It was the third time in the past six months. Rates have more than doubled in that time, going from 0.50% to 1.25%. This hike was baked into the economic data, and now it’s getting baked into the debt loads of Canadian households.

Following the announcement, Canadian banks hiked their prime lending rate by an equivalent 25 basis points. The prime lending rate is the annual interest rate Canada’s major banks use to set interest rates on variable-rate loans, lines of credit, variable-rate mortgages, and HELOCs (Home Equity Lines of credit).

This means nearly instantly higher interest payments for borrowers carrying variable-rate mortgages, HELOCs, and lines of credit.

This is critically important, considering the context of the current situation. Interest rates have been at historically low emergency levels since the Financial Crisis. This has allowed households to absorb elevated house prices and a record amount of debt. Each rate hike reduces the ability to service that debt.

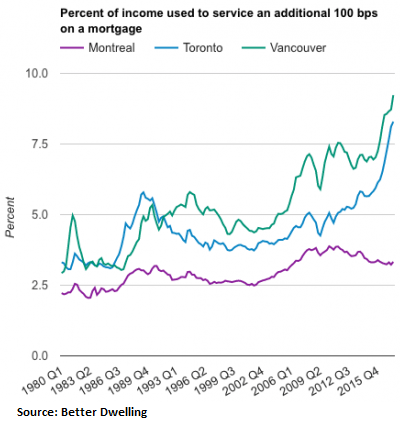

Given the current size of the mortgages, for Vancouver households, a 1% rate increase in their variable mortgage rate would require an additional 9.2% of their income to make the payment, according to Better Dwelling, and for households in Toronto, it would require an additional 8.3% of their household income. In Montreal, it would require an additional 3.2% of their household income:

Further, the newly required stress tests for variable-rate mortgages require that applicants qualify at the minimum specified rate of the stress test, which just jumped from 4.99% to 5.14%, or at the actual rate they’re borrowing at PLUS 2%, whichever is greater.

A five-year fixed rate (rate adjusts in five years from when the mortgage was taken out) at most banks is now 3.54%. So most borrowers will be stress tested closer to 5.54%. Ouch.

The BOC’s rate hike will immediately impact the roughly 30% of existing Canadian mortgages with variable rates that adjust nearly instantly. And it will also put pressure on the C$211-billion HELOC phenomenon, whose outstanding balances have surged 500% since the year 2000.

The Bank of Canada is well aware of the current situation, and while they have assured Finance Minister Bill Morneau further rate hikes won’t cripple the economy, they have warned him of a potential household deleveraging.

It remains to be seen how the resilient housing market will digest the changes. It’s early. By Steve Saretsky, Vancouver, Canada, Vancity Condo Guide

The Canadian Housing & Debt Bubble ascends to the next level of risk. Read… Canadian Homeowners Take Out HELOCs to Fund Subprime Buyers Unable to get a Mortgage

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Won’t affect the Chinese – they use all cash. It will affect the Canadians who want to compete with the Chinese. It could be a losers game. If prices fall, the Chinese will just buy more. Then they get an EB-5 Visa and come here and play Monopoly. Between the Hedge Funds and the Chinese, our kids will all be renters. The owner-occupancy ratio will eventually be the lowest since the 1950’s. Thanks Federal Reserve!

If there are actual[y three rate hikes baked in for 2018 it spells big trouble ahead.Man the torpedoes and batten down the hatches and dive, dive dive!!

From what I understand, the banks will not increase your monthly mortgage payments as rates increase.

What they are doing is tacking on the additional interest to the end of your mortgage loan.

So in the end it will just take you longer to pay off the mortgage at the same monthly payments regardless of how many interest rate increases occur.

People forget Banks don’t want to foreclose on people and would rather get the guaranteed interest.

Banks may not want to foreclose, but mortgage servicers in the US make good money by foreclosing, and charging fees to the banks.

Steve Saretsky, the author of the article, says this:

“Most mortgages will see higher interest payments and higher total monthly payments. Yes there are some lenders who provide an option to keep payments the same and pay higher interest than principal and extend amortization. This is less common. Also, 100% of insured mortgages will see higher monthly payments. There is no such option for insured mortgages (less than 20% down payment).”

Since most people keep extending their mortgage end date with endless refinancing what’s a few more months? Higher mortgage rates may induce sellers to carry the paper at a lower rate and get the full asking price so a mortgage rate crash is a long ways off.

Almost half of Canadian mortgages are up for renewal this year, banks will increase mortgage rates and payments.

Also, you can’t easily leave them for another bank or private lender with the new rules (B-20) in place, which means they don’t have to give competitive lower rates anymore to encourage you to stay.

Also worth mentioning is, in Canada, mortgages are typically “full-recourse”.

https://www.cmhc-schl.gc.ca/en/corp/nero/jufa/jufa_018.cfm

I’ve been hearing that same gloom and doom for over eight years but the judgement day never arrives. There is just too much easy money washing over the planet to have to worry about mortgage finance. If Canadian banks raise rates on adjustable rate mortgages money will flood in from other sources to fill the vacuum.

Global investors must be salivating over 3% for five year debt. Here’s an idea – finance Canadian mortgages, pool them into bonds and sell them to eager buyers around the world. There is no shortage of money looking for yield – I’m guessing Canadian home owners will have no problem rolling their debt for more cheap money.

Stan, how does the US Federal Reserve affect our Cdn immigration policies and housing market? The Bank of Canada raises or lowers interest rates in Canada, not the US Fed. And the EB-5 Visa is a US Visa, nothing to do with Canada.

You don’t think the price of the dollar affects your real estate and how your central bank acts?

lol.

If canada did not raise rates in lockstep with the fed the loonie would have a meltdown.

The value of the loonie is tied to oil and other commodities including electricity (which they export to the U.S. from their vast hydro resources).

Canada is an commodity export machine and their vast commodity wealth is spread among just 35 million people – they have no worries regarding the loonie. The loonie will get stronger as the world depletes vital commodities. Of course this assumes the U.S. won’t just take what they would otherwise have to pay for.

>>Won’t affect the Chinese

So many errors in that comment. The China ill-gotten money outflow is waay down. The mainlanders are now turning to bitcoin to get their money out, and that will end badly, too. Chinese buyers are not predominantly cash buyers anyway, their cash outflow is now severely restricted, and interest rates are up. Conclusion: Vancouver is going down.

Not only that. If home prices were to plunge, some Chinese might just sell as well and try to pick the bottom. After all they are partly buying this for speculation.

Speculation is like leverage, it increases volatility on the way up and down.

Correct about global competitive interest rate repression which emanated from Federal Reserve and Wall Street. It is debatable who is the bigger culprit.

On immigration, it’s your dear government’s criminal negligence. The Chinese are only exploiting scams they are allowed to.

Not true, the Chinese are borrowing the money.

I’m not sure what % is borrowed through western banks though.

I was born in a communist country, spend my early childhood in that socialist “hell”, underlined by lack of upward opportunity, poverty, and no private property.

Stop thinking in terms of western culture, there’s an innate HATE of authority in Chinese society because of how long they’ve been suppressed by their oppressive government. Add to that cultural difference, decades of no real estate market making it hard to price.

Like a little boy who just discovered masturbation.

Imagine, being a young Chinese men in your early 30s, wanting to be married and start a family, and the pressures from your family.

You need the trifecta to even be considered by a young woman.

1. a car.

2. good job

3. house, or down-payment for house.

Without these, you don’t even get to play, an adult.

And this is how you get most of the Chinese middle class savings funnelled into property. The exodus to the west is justified.

What would you do, if you knew that your currency would eventually inflate. An apartment in Bejin to compare to a relative one in California?

How? Must be that amazing China sea beach front view, clean air and perfectly blue skys, clearly.

Don’t hate on the Chinese, its actually a sad predicament their in.

The “One child policy” being your clue. You would want to get your family out of there as well. Inflation, communist oppression, pollution, corruption. The west is accepting their wealth, at a cost, but they’re overpaying to escape and you would do the same.

In the 19th century they were junkies to the Brits.

During WW2 they were japans geisha.

Now they’re Americas “B#$#ch”

Get it.. if anything its sad. And we are witnessing the biggest heist of our lifetime. And we are all complacent, and as pessimistic as this sounds, it will be glorious if this financial manipulations remove that communist crust off of the Chinese backs.

The only Canadians/Americans who will get screwed are the greedy ones, or that part of the lower middle class who thinks they can live beyond their means. You ever listen to bloomberg? you must have heard the saying. Bears make money, Bulls make money, Pigs, they get slaughtered. Now stop complaining, as corrupt as our gov can be, its still the best thing we have managed. Cherish your freedom, and play it safe.

Correct me if I’m wrong Wolf, and sorry for getting off topic.

ps. love your site and sorry for mixing ideology into it.

Awesome comment, Lenz. Most appreciated. My Mom used to have a saying about Russians when people were slagging them during the cold war, (and now).

“You can say what you like, but 100 years ago they were bought and sold with the land. They’re doing much better now, despite what you think”.

The U.S. is not so free as you imagine it in your post – we are really just coasting on a reputation of freedom.

I have fond memories of a USA that was glorious and free, those memories make the current state of intrusion and corruption all the more chafing. We let corporate lobbyist lawyers write our laws so I suppose we deserve our fate.

Tenny mucho mucho dinero in su trucky trailer? If you’re not familiar with that meme google it. I lived in Brasil for a while – I had much more freedom there – not unlike the U.S. thirty years ago.

Honest words with the ring of truth will always be welcomed here.

This is a common fallacy with RE in Canada. Look outside the top bubbly markets and prices aren’t really that bad. Canada is a HUGE country! No shortage of housing or land.

Except the majority of the Canadian population lives in the bubble areas. Remember because of Poloz even the cities that are considered low in price really aren’t because of Stephen Poloz. Had someone else been at the helm prices nationwide would be lower.

China has already closed the tab; no more billion dollar loans for wealthy Chinese to go and pay stupid prices for commercial or residential real estate. All Chinese companies have been bared from doing that. So, adios Chinese money :).

If that’s true there’s big hurt and big pain in store for Canadians (real Canadians) as virtually the only driving force for home prices in Canada are the Chinese. Yup, it all started with one small city called Agincourt in the suburb of Scarborough and now the nightmare has enveloped the entire country of Canada. Sad the politicians would let it get this far in such a short period of time.

Meanwhile, the comatose SEC has to occasionally stir itself and pretend to be a responsible enforcement arm, while the same fraudulent practices that led to the 2007 housing bubble implosion continue with impunity.

http://www.businessinsider.com/broker-price-opinions-popular-on-wall-street-drawing-sec-inquiry-2018-1

Variable-rate mortgages are a pain in the rear end. But then people usually don’t think long term about money.

Heck I know people who had to move in with relatives or live in their cars for a few months because of how much their rent was raised. And that was just paying rent.

And again big companies no longer want you working from home.

Good comments you guys. I have noticed a few things on Vancouver Island where I live. The high prices in Vancouver and Victoria are really bleeding out into other markets. I know instances where people commute from lake Cowichan to Victoria over the Malahat (for God’s sake). Prices are exploding, everywhere. The house I used to own in Campbell River (bought it for $63,000 in ’87), is over $400,000 now. I sold it in 2006 for $300,000. Where I currently live (rural) we are getting all kinds of new people moving here from Victoria. Why? Lots of space, quiet, and affordable. People could not believe it when we sold our house in town and bought here. Now they are saying, “How did you find this place, anyway”?

The article really emphasized a big concern for me. If people are just barely squeezing into the Market at 4% mortgage rates, they are screwed when rates normalize. I know this is the point of the article, but the ugly reckoning will be unbelieveable.

regards

There will be no ugly reckoning in real estate – just more and more money flooding in seeking any yield that’s positive.

The ugly reckoning will eventually arrive in the currency debasement arena. Debasement has been shown to cause horrific pain and suffering but we humans still fall back on it every time – we an never pass up the allure of a free lunch.

That “currency debasement” has already arrived in a massive way: now it takes 50% more dollars to buy the exact same house in some cities than it took six or seven years ago. Those homes haven’t gotten bigger or better. What happened is that the dollar has lost its purchasing power with regards to assets. This is asset price inflation. Or as you put it, “currency debasement.”

You don’t need to wait for it. It has already happened massively since 2009.

@van and @wolf

If currency debasement has arrived and unfolded over the past 5-6 yrs, and will continue…does it make sense to buy RE now and lock in a low 30yr rate so that you can pay down the low rate debt with cheaper dollars in the future?

Unfortunately that’s the fallout from the Chinese driving home prices to the stratosphere. We see it today and young people are leaving Vancouver because even a 6 figure income can no longer support someone as rents have gone skyward.

More incentive for canadians to sell U.S. second homes and they bought a lot of homes.

http://www.cbc.ca/news/business/snowbirds-loonie-real-estate-1.3425322

Something else to consider.If people are forced to exit their

condo’s and home’s maybe this opens up many more units to rent.

If this leads to a surplus then rent prices go down , Owners have

counted on being able to rent out their units if prices go south and

things get tough. What happens if they cannot rent or sell.

One factor that will offset any such fears is the government policy to gradually increase immigration rates over the next several years, which will maintain demand in the population centres.

Oh, immigrants story again; real estate agents in Canada and Australia love that story. Immigrants are generally poor people who don’t have 2 nickles to rub together. So, in the first 10 years, immigrants are generally a burden and not an asset. They are not gonna start buying your $1M shack for $1.5M.

These are not the immigrants you’re looking for.

Unless, you’re looking for wealthy Chinese, with knowledge, purpose, a certain desperation to save their gains, and are business savvy.

Lenz: Yeah, you want to look for “wealthy Chinese, with knowledge, purpose, a certain desperation to save their gains, and are business savvy.”, but at least 99% of your immigrants will be those who will don’t have 2 nickles to rub together. No wealthy Swiss or London banker is gonna say “Oh, let’s drop everything and go to Canada or Australia.”

America’s declining geopolitical risk as well as protection is also negative for global real estate.

We will see another 5 to 6 percent rate rise with the new tax benefits for Americans.

Global companies will rush to America because of the cheap taxes and cheap power.

Capital will cost more in Canada so rates will rise the American vacuum will suck all of global capital. Don’t think that the Canadian Banks will even consider investing consider investing in Canada they never do anyways the hammer has reached the Nail Canada has had a great ride and you will see a major major change let’s face it Trudeau Harper are badly equipped to deal with any Financial issues it’s too bad this country has made a fortune from robbing the resources of the land and dumping them in the global market the canceling of the North American Free Trade Agreement and the future lift between North America and Europe does not bode well for Canada maybe a lot of the readers are correct the Chinese will not be affected by rate Rises Florida lotto numbers don’t realize the Chinese do not buy houses cash they are heavily heavily mortgaged and they’re not mortgage by the Bank of China their mortgage by Canadian Banks it will be the Canadians who bear the Brunt a possible bank that is but hey in Canada it doesn’t matter they always get bailed out so who cares that’s facing the Chinese are very very small part of the market

Canada has finalized TPP negotiations, it’s a go.

Too much doom, Canada is doing well.

Everything is awesome until it is not.

This story has been repeated many time… we are different ..this time is different… etc etc

The cost of living is far too high in Canada. That’s all you have to know how this will work out. The future looks bleak for Canada to put it mildly.

I live in socal.. where the weather is awesome and jobs are decent…

Not sure why would anyone with decent money want to live in places like vanc or Toronto.. or even canada…

Have you ever been to Canada? There’s no place on earth like parts of BC, Alberta, Y.T. etc. I was born and raised in beautiful W. Colorado and would trade it in a minute if I could. I love the Canadian people. I spend most of every summer up there.

I have lived very close to Toronto for couple of years and weather was shitty.

Nothing against Canadian, just stating a fact that weather is shitty..

Come to San Diego: A Land of all year sunny days but with shitty real estate price and people with snobbish attitude :-). IN San Diego, you can surf and ski in a single day!!

Jon, are you asking why the Chinese move to Vancouver?

1. Weather is healthier then most industrialised Chinese cities

2. spending 500k allows entry to their socialised health care + Canadian education for their children.

3. Canadian citizenship (shield against Chinese gov & repatriation of their wealth).

4. When the Brits handed over Hong Kong, many immigrated to Vancouver, forming an Asian community to lean on. Familiarity.

When you think of the city geography, it is perfectly situated for a real estate bubble. Beautiful scenery, easy to sell to investors, a nice water front bay, and surrounded by mountains on all other sides. No horizontal expansion, just a limited vertical option. A perfect bubble, if there’s such a thing.

I work in entertainment, and the BC gov provides subsidies to my industry. Up to 60% of pay is covered by Canadian taxpayers, in form of tax subsidies + medical coverage.

In many respects, turning my profession not too far off from a college professor working for a state university accept the pay differnece. I’ve always wandered why Vancouver? 10-15 years to shift the production/ post-production from California up there.

Even strip-clubs put their cuter girls at the front door to lure costumers. Maybe that’s what we’ve become. =)

I love Canada too but we’re not special, as much as we like to tell ourselves we are. Asset bubbles will cause the same dislocations here as they do anywhere else on earth.

There is a fundamental difference between “Canada is awesome” and “Canada is immune”. I heartily concur with the first sentiment and absolutely reject the second.

The rise in rates had to happen sooner or later. The central bank have little left in their bag of tricks. Even if they had inclination for more QE, the systematic risks prevent them from doing it.

The Fed knows the reversal of its balance sheet is going to end the bubble. It’s just a matter of months. They were hoping the market would heed its warning and react gradually, but it didn’t. Stocks continue to rise, and LT rates haven’t responded. However, all it takes is one scared minnow to change the direction of the whole group in a second.

A good summary of the current situation.

A few other notes. The number of units under construction in Vancouver is off the (historical chart) – that won’t help in a slowdown (even though long term it is a good thing).

Related, a huge percentage of the economy is built around building, marketing, selling, re-selling, furnishing, etc. real estate. Even if the market just goes flat, this sector will take a big hit.

People here generally fall into three camps.

1) By far the largest is people who are simply oblivious, the market always goes up, so they buy as much real estate as they can, and if they have all they need, they buy it for their kids or they buy rental properties. Most of our immigration comes from countries with no bubble meltdown in living memory – if ever! – so immigrants are mostly in this camp.

2) There is a group like van down by the river who have heard these stories for so many years they’ve stopped paying attention. Many of these folks missed much of the initial run-up and have vowed to make up for lost time. The one thing that is different in this case (vs the warnings of the past decade) is that we currently have central bank tightening around the world. This happened in 2004-2007 as well, but that time the U.S. blew up first, so Canada pulled back in time (it is interesting to see the historical double wave of defaults in Canada – a first wave came as rates rose but this wave subsided after the 2008 meltdown brought rates crashing down, then there was a 2nd wave due to unemployment rising in the mild (in Canada) recession).

This time around, there is every indication that Canada will be (one of) the first to blow up as rates rise and conditions tighten. Still, it’s worth remembering that last time around the fed started raising rates in mid-2004 and it took 4 years and 400bp of increases for the wolf to blow the house down. As the author rightly says, it’s early.

3) The third, very small, group is people who don’t really think this bubble can last forever, but it feels like it already has and they’ve been wrong for a long time (Robert Shiller, bubble guru declared Vancouver the bubbliest city in the world – in 2006) – they can’t change their mind, and they can’t convince anyone, and they’re really not sure of anything themselves any more, so now they just (mostly) keep their mouth shut, and wait and see.