The Housing & Debt Bubble ascends to the next level of risk.

By Steve Saretsky, Vancouver, Canada, Vancity Condo Guide:

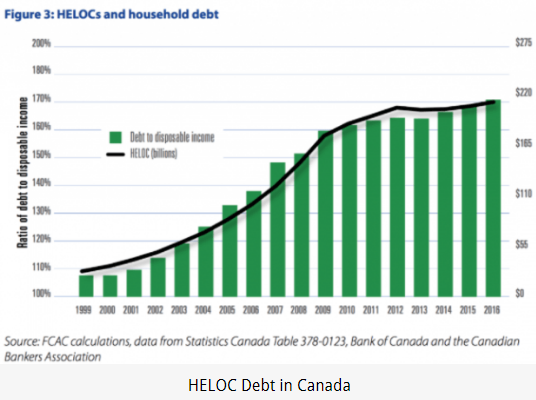

The HELOC (Home Equity Line of Credit) has been a blessing and a curse for Canadian households. While it has helped spur house prices and simultaneously provided consumers the ability to tap into their new found equity, it has also crippled many Canadian households into a debt trap that seems insurmountable.

Between 2000 and 2010, HELOC balances soared from $35 billion to $186 billion, according to the Financial Consumer Agency of Canada, an average annual growth rate of 20%. As of 2016, HELOC balances sit at $211 billion, a 500% increase since the year 2000. While also pushing Canadian household debt to incomes to record highs of 168%.

Scott Terrio, a debt consultant, says the situation is a full blown “extend and pretend,” meaning borrowers are just continuously refinancing or taking on more and more debt in order to sustain their lifestyle. Canadians can extend their debt repayment terms and pretend to live a lifestyle they can’t otherwise obtain.

What the HELOC has also been able to do is help spur the private lending space which has ultimately supported rising house prices. Seth Daniels of JKD Capital, one of the most astute Canada-Watchers, says there’s a growing trend where “a homeowner acts as a sub-prime lender by drawing a HELOC at 3% interest only, and lends it to a subprime borrower at 8-12% for one year (interest only).”

This is something I’ve been hearing on an ongoing basis from mortgage brokers and lawyers who help facilitate these deals. Especially since mortgage lending conditions tightened, starting with OSFI’s first mortgage stress test back in November, 2016. The financial regulator required “high-ratio” borrowers (those with less than 20% down payment) to qualify for a mortgage at the borrowing rate plus 2%. So basically you’re getting qualified on what you can borrow at 5% even though you’re borrowing at 3%.

Rising interest rates pose special risks in Canada because most mortgages come with adjustable rates. Many of them adjust very quickly to rate increases. Others have a five-year fixed portion and then adjust. Meaning a rising interest rate environment is much more impactful. Hence the new stress tests, and new ways to get around them, including using private lenders that source their funds from taking out HELOCs.

This strategy has been bulletproof, because, well, prices can only go up. The lender makes a juicy return, and the borrower gets his house. The borrower then transitions into a traditional mortgage once his home equity rises after the one year expires.

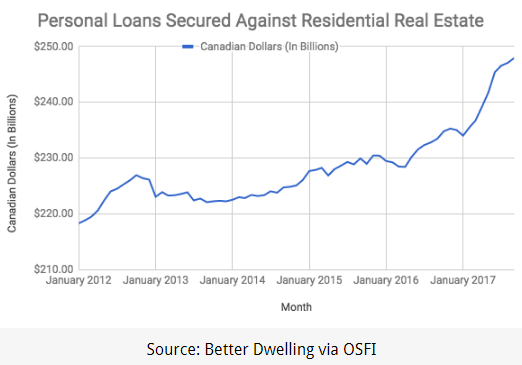

This has created a situation where, as of September 2017, personal loans secured against residential real estate hit a record high $247 Billion.

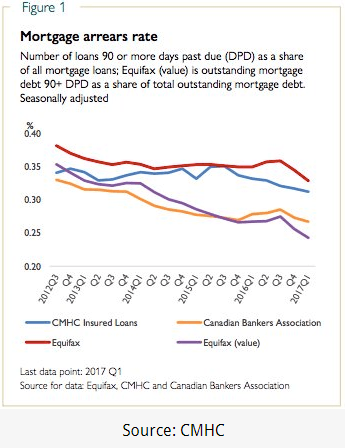

Thanks to an endless supply of new loans (credit) and rising house prices, mortgage arrears rates continue to fall to rock bottom lows.

But as Seth Daniels remarked, “Up to a point, the greater the debt growth, the lower the arrears because as they say, ‘a rolling loan gathers no loss’. In other words when debt growth is exploding people can find ways of avoiding default by rolling the loan, refinancing, selling the asset, or whatever. So, paradoxically, the default rate will seem to improve when the actual risk in the economy is exploding.”

With another mortgage stress test set to roll out January 1, 2018, this will likely push another swarm of borrowers into the private lending space. We’re already witnessing a huge end of the year push as buyers scramble to secure a home prior to further mortgage clamp-downs.

The new mortgage stress test — which previously only targeted high-ratio borrowers (less than 20% down) — will now include low-ratio borrowers (more than 20% down) as well. This could be substantial, considering 85% to 90% of all mortgages in Toronto and Vancouver are low-ratio.

It’s anticipated to eliminate some 12% of low-ratio borrowers while simultaneously reducing borrowing power by 20%. This could signal a final boom for the private lending space in Canada. By Steve Saretsky, Vancity Condo Guide

Canadians, fasten your seat-belt. Here are the charts. Read… Whose Private-Sector Debt Will Implode Next: US, Canada, China, Eurozone, Japan?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Isn’t there more than the fixed vs. variable mortgage type too? Here in Oz, 46% of new loans over the last few years have been Interest Only (IO) so I wonder if they’re allowed in Canada at all. I think IO loans are financial madness. If a decent percentage are IO in Canada then an awful lot more people are going to fold when the prices start to depreciate.

The IO mortgage represents a risk bankers take when they know they can make money on a foreclosure. Right now in the US, on average, the bankers are making money on foreclosed properties. They are capturing gains over their loans when homeowners walk away.

Having owned a few houses which on average turned out to be bad investments, I would consider taking an IO loan because I see them as long term lease deals.

…except with a standard housing lease the tenant is not responsible for costs associated with maintenance, normal repairs, upgrades, and natural disasters.

You haven’t been in the rental market lately. The mega landlords are using every trick in the book to charge back repairs to the tenants. They are also increasing rents at 5-10% a year.

If you get a good rate on an IO and buy a good house, your risk of loss is not that big. Insurance covers big risks and the “rent” protection covers the little things. Over time you would be better off with an IO over renting.

The bankers know this and this is why IOs exists.

This Interest Only loan sounds like a loan shark program. I have only watched long term rate mortgages myself and haven’t seen an IO offered, but I also refuse to look into financing through any private lender. I stick with Credit Unions or RBC/BoM type banks. The HELOC is definitely where the Canadian market is being propped up, I fell for that 10 years ago and luckily housing didn’t drop. I wouldn’t do it in the current market.

I see zero risk to IO loans. As the price of housing continues to march higher and central banks guarantee fixed rate mortgages will stay under 4% these home owners can choose a conventional 30 mortgage anytime they choose to start paying down the balance.

House purchases are subsidized by easy, cheap money from central banks and central banks realize they cannot, ever, withdraw the subsidy – to do so would cause house price deflation. Think about it, an outcome that is deemed unacceptable will not be accepted.

Borrow money to buy assets, it’s the only way to survive, central banks will help you default by inflating away the debt and you will be left with an asset that still has value. Borrow as much funny money as you can.

People who bought in Toronto in April are already looking at a median price decline of 17%.

And they will get bailed out, just like last time.

Sadly for me I can’t afford to even get in the game, with my income I couldn’t get approved for anything where I live.

Hey Wolf,

Do you believe the real estate correction will hit residential real estate before it hits the commercial realm?

Or is it possible to ‘kick the can’ a full presidential term?

btw, thanks for keeping this site current, insightful and entertaining.

Real estate is local. So it’s market by market. Residential and commercial are not per se linked either. So Houston’s office sector tanked while home prices in San Francisco soared.

However, if the BOC suddenly raised rates in half-point increments meeting after meeting — which it won’t — asset classes would likely move together. During the Financial Crisis in the US, residential and commercial moved together. And since then, they moved together. So there are things that impact residential and commercial the same way averaged out across the nation. But locally, it still works out differently.

Also, multi-family might be running into trouble and the office sector might be slowing while industrial (fulfillment centers for e-commerce) is booming and lodging is already tanking. So it’s not straightforward.

That doesn’t mean much when the asset is worth a fraction of the amount borrowed.

Low interest rates didn’t stop the US market from cratering 10 years ago. Yet Canada will be different somehow?

“I think IO loans are financial madness”

Why? If there is anything like here (USA) if you just have the balls to pull the trigger you too will get a bit of the bailout cash or get to live mortgage free for half a decade.

This next bailout of those who were reckless is going to be a dozy!!!

It is so frustrating being honest.

Would be great if you could post an update on the Canadian metro markets such as Toronto. A few months back I recall you posting on ‘the collapse’ of the Toronto markets. Did the newly imposed taxes on speculative buying have any effect?

What happened? Seems the markets are still powering forward. As your article states, if loans can be rolled over then there will be no end to real estate appreciation.

I never wrote about any “collapse of the Toronto housing market.” I wrote about a “deflating housing bubble,” most recently in October, when home sales (not prices) “plunged 35%”:

https://wolfstreet.com/2017/10/05/deflating-house-price-bubble-toronto/

That process continues in Toronto. The median price in the Toronto metro has dropped 17% from the peak of C$800K in April to C$665K in November but remains up somewhat year-over-year. So as I said, not a collapse, just a deflating housing bubble.

Vancouver has split in two, with the condo market being hot and detached homes cooling off. The BC government is subsidizing down payments up to a limit, which favors condos. And condo speculation is huge and totally crazy in the Vancouver metro.

HELOC Loans turn property into ATM’S.

Which is fine, for the Municipalities Governments and States, along with Bank’s that make money and Garner Higher taxes from the property spiral.

Not so good for the Borrower when property Stagnates or declines generally at the same time interest rates are rising.

HELOC loans came from the concept of encouraging older peopel to “Spend and Enjoy” the Equity in their homes.

Instead of leaving it to their grandchildren, ensuring that their children, and grand children, remained tax and interest slaves, for much longer.

Nowadays many People with these types of loans can frequently NEVER AFFORD to ever retire.

I couldn’t have retired without the HELOC because I used it to buy my pension back (which I had withdrawn over the years). Now, 10 yrs. later, I have refi’d to a fixed rate again. Everything worked out well.

The previous B.C. government needed to bailout their condo developer political supporters, hence, the “first time” owner subsidy.

No free market anywhere.

“the collapse of the Toronto markets”

Too hilarious, no one says these things anymore – and for good reason. Collapses have been deemed unacceptable and are easily prevented by deploying cash into any market under strain. It’s not as though there is now, or ever will be, a shortage of cash available to prevent the market in any asset from “crashing”. Appreciating at a rate of less than 10% is no longer acceptable, in what imaginary world would a crash be allowed. That is Alice Through the Looking Glass type imaginary thinking.

Guys, money is swirling all around us, grab as much of it as you can and buy stuff while the money still has any whiff of value.

So they were using their own homes to provide credit for those needing to buy a home at a higher rate for first year, which only made demand increase, and home prices rise, which only works if prices go up perpetually .. forever…. why does it sound like a ponzi scheme?

It’s not a Ponzi scheme. It’s Canadian Manifest Destiny. The Canucks are so special, the real world is going to bend backwards and somehow make it work.

Don’t worry though. Uncle Warren is going to backstop the entire thing. In fact he’s done some fishing around already. Pretty soon the worry about NAFTA will disappear. Once Uncle Warren owns Canada, then the whole country will just get annexed.

Too late for the U.S. to annex Canada. The Chinese run the table now. In fact, Trudeau Junior just had his butt handed to him by the Chinese.

Why is it too late? We share a border. The Chinese doesn’t even have a working carrier yet. Prepare to join the Greater North American Prosperity Sphere. Resistance is futile.

Also Canada’s GDP looks decent in 2017, best in the G7. They really must have Manifest Destiny.

That’s “The Greater North American Co-Prosperity Sphere.”

If this seems reasonable I have some nice sea front property here in Kansas you may be interested in.

The desire to race to buy a home before regulations clamp down baffels me. The reason to be in that situation would be to sell a property at a peak price and trade up or down. Otherwise your better off waiting for regulations to deflate the bubble.

They are probably thinking the new regulations will bar them from buying and have bought into the prices will go up forever mentality and thus must buy now.

The regulation is just there to prevent peopel from buying somethign they couldn’t afford. Just beucase someone would lend the money, especially when the loan has to be insured with CMHC (beucase under20% the bank doesn’t want to touch it as it is too risky), does not mean one SHOULD and can afford the loan. What about losing a job what about one parent on leave after having a kid? Now in recent history those who over extended lucked out by the price increases but lucking out does not mean it was the right thing to do.

Compared historically prices have never been so high however interesting to consider maybe historical measures no longer represent reality? Maybe this generation will not buy houses and will raise teh next generations with less space? it is amusing that those having kids now may likely have grown up in large hosues over 3000 sq/ft however their parents raised more kids in the little 1950s and earlier hosues 1200 sq ft. It really just seems tehre was a blip in the system where we went big and space wasnt so expensive then now we are just going abck to what things used to be and 1000-1400 of efficient useable space is perfectly fine.

My dad grew up in a house of around 900 sq ft…5 kids, one washroom downstairs, two small bedrooms up with parents downstairs in the ‘big’ bedroom. They were happy and all kids did well. Go figure. :-)

As for the article, this does not reference all Canadians by any means. I have been pretty much mortgage free from age 30, and that was on a lower mid-class workingman’s wage. My friends have also been mortgage free for most of their working lives. My kids in their 30’s have modest mortgages and should have them paid off in their 40’s. This is on Vancouver Island, a very sought after place to live. My daughter is in Ladysmith and my son is in Campbell River if anyone cares to Google?

That is the Canada I know and what I have been exposed to my entire life. Because mortgage interest has never been deductible in Canada, Canadian wisdom has always been to pay the damn house off as soon as possible in order to get ahead and prepare for retirement. This is what I have drummed into my kids. I retired at age 57 because my housing costs are almost non-existent. My kids understand that if they do not own their house outright, they cannot retire, ever.

This recent phenomenon of debt and instant housing gratification is not universal, nor is it something to accept as normal. It will be a very valuable object lesson in the next downturn. My only question for those who will lose their unaffordable homes will be, “Still watching those Toronto-based home improvement shows with the granite counter tops”?

what happens when the subprime borrower defaults?

Ambrose,

I’ll tell you exactly what happens. They just stop making payments and because there are so many they will live mortgage free for up to 5 years. I’ve seen this happen here in the states.

In one instance I read about the person didn’t make a payment for 4 years and saved the payments. Once prices hit bottom this person went and bought the house down the street for a 60% discount. AND the banks were all to willing to let this dead beat buy again…….they even had a name for these people “boomerang buyers”.

lets face it, if you play by the rules and live within your means you are a sucker and a fool………..and I am and always will be.

But if the bank forgave his debt, would they not have to report it to the IRS, it then being deemed income to him, on which taxes would be due? (Nor do I believe that a reliable way to establish credit is to establish a history of defaulting on loans)

Yes, the bank is supposed to send the lenders a 1099. However, prior to ex President Bush’s exit, he signed a law to have the banks waive this, and the banks can write it off in their own P&L. But that has expired. Not sure whether they will sign another one similar to that on the next crisis.

Good article – I am sure that here in the states the same scenario exists where personal heloc money is lent out (maybe peer to peer lending) to capture the yield spread . Homeowners are becoming levered mini banks. In the case of canada what financial products are available that helocs are funding ? thanks

It’s no longer possible to pay too much for a house on the west or northeast of North America. Currencies are being intentionally and relentlessly devalued by the central banks so in nominal terms the value of homes will continue to rocket higher. These buyers are taking the logical course by doing whatever they can to get on the property (hard asset) ladder so they aren’t left with nothing in the confetti currency world.

Draghi is running out of debt to purchase yet he keeps the accelerator pedal mashed to the floor and likewise money is printed and flooding the globe from Japan, China… Money crowded out of other assets by central bank funny money floods into any debt it can find and Canadian houses seem like a safe bet compared to Italian bonds.

Money has become untethered from it’s anchor and floats high up in the sky, its value has become arbitrary – how is it possible to determine the value of a given asset when central banks hit the bid with no consideration of the price. Some people still need to work for a living but their pay is crushed by the flood of easy money made by speculators and printed up relentlessly by central banks. What’s a person to do, the music is playing you’re a fool not to get up and dance.

It is different this time because the central banks are not pulling back from the brink – they learned their lesson from Greenspan and Bernanke in 2006 – 2008 (never tighten the money supply, always keep money loose).

Wake me if the money supply ever tightens and I will admit I was wrong – I won’t hold my breath. The tidal wave of confetti cash will not be turned back.

Every credit bubble implodes sooner or later, no matter how hard central banks might try to keep them going. If non-stop printing could guarantee housing would go up forever, then a house in Zimbabwe would have been the best investment in the world over the past 20 years.

It has been a great ‘investment’–for the highest echelon of the Zanu PF crony-klepto state!

Interest rates dropped below 1% in Weimar Germany but in the end borrowers easily paid back their loans in German marks. There was no credit crisis – just a little monetary problem.

Just one more hit on the credit bong, and then I’ll quit…

Still this seems less risky than the rapidly increasing U. S. fad for mortgaging your home to “invest” in bitcoin futures.

Do these people have a financial “death wish?”

That’s heresay created by media to get eyeballs.

Each and every one of these leveraged-to-the-hilt debt donkeys who used their houses as ATMs is going to wail what victims they are when the central bankers’ asset bubbles implode, which they most assuredly will. They will demand to know why no one, least of all banks or their captured regulators and enforcers, tried to protect them from their own greed and irresponsibility.

Canada doesn’t come close to matching the coming sub-prime saga here in the US.

It doesn’t matter……nothing does. I don’t have the testicular fortitude to do it but if you don’t care just borrow borrow borrow and you too will be rewarded. Prices never seem to correct only those willing to go into hock win.

i’m sick and tired of the same articles over and over about how insane this all is and while I agree and keep living within my means i keep looking like the fool year after year.

I don’t know if the Canadian banks have the guts to cut the HELOC of their customers. Regulators might have to write a new law to force them to take action on over-leveraged homeowners as interest rates go up and house prices fall.

Canada oil is under blockade. There are problems with pipelines

and rail, preventing shipment, while production is growing & growing.

WCS , Canadian oil future for Jan 2018 = $21 USD.

We will see what that will do to the Canadian debt bubble.

We will see what that piling up inventory will do to the shell shock oil co.

in the USA, with 1/2 Trillion USD junk debt.

WCS is at $39.00 US right now.

With the proposed and under construction new pipeline to Burnaby, thus opening up a Chinese export market, it should rise much closer to WTI.

It’s absolutely crazy here in Canada! The credit expansion that keeps the entire Ponzi scheme that is our financialised economic system afloat is in full display almost everywhere you look.

For example, I noted the other day in one of my infrequent drives to do some errands that the Sports-talk radio station I most often listen to had numerous commercials for 1) the shadow banking industry to push home equity loans and sub-prime mortgages; 2) debt consolidation services; 3) consumer products at sub-prime interest rates and/or deferred payment plans. And this was just in the 30 minutes I listened. (sports is a great distraction from the insanity that is so prevalent in the sociopolitical realm–I just had to stop listening to CBC as it was more and more focusing on US politics and the mainstream neoliberal narratives)

On a local news front regarding the housing market, I have noticed that homes in our area (fringe of Greater Toronto Area) are not selling. Where just a few months ago home were popping up on the market and selling within a week or two, the houses listed in the last couple of months are still on the market with little to no sales to speak of. Far fewer homes seem to be going on the market as well–probably because they are not selling.

Homes are not selling near me, either, but this is because they have mostly been bought by Chinese, and Chinese don’t usually sell their property. The Italians were also known for this trait, but I’m not sure it still holds true for them.

Anecdotally speaking, I can attest that the vast majority of homes purchased in our local area have been purchased by foreign nationals of ‘Asian’ descent as well (I can only assume due to ‘Chinese’ money flowing in, even though our government/real estate agencies are downplaying this. It would appear the present global trend of central banks tightening credit (via interest rate raises and balance sheet ‘normalization’) is beginning to have an impact on the housing market everywhere.