But savers are still getting shafted.

Outstanding “revolving credit” owed by consumers – such as bank-issued and private-label credit cards – jumped 6.1% year-over-year to $977 billion in the third quarter, according to the Fed’s Board of Governors. When the holiday shopping season is over, it will exceed $1 trillion. At the same time, the Fed has set out to make this type of debt a lot more expensive.

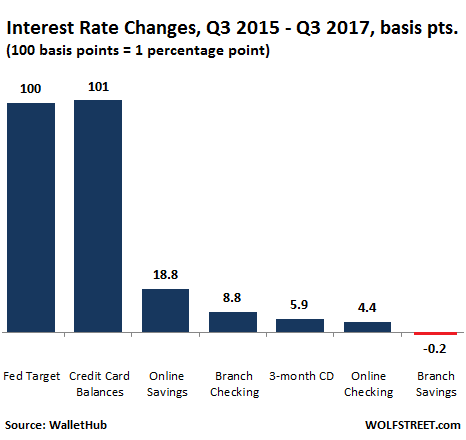

The Fed’s four hikes of its target range for the federal funds rate in this cycle cost consumers with credit card balances an additional $6 billion in interest in 2017, according to WalletHub. The Fed’s widely expected quarter-percentage-point hike on December 13 will cost consumers with credit card balances an additional $1.5 billion in 2018. This would bring the incremental costs of five rates hikes so far to $7.5 billion next year.

Short-term yields have shot up since the rate-hike cycle started. For example, the three-month US Treasury yield rose from near 0% in October 2015 to 1.33% today. Credit card rates move with short-term rates.

Mortgage rates move in near-parallel with the 10-year Treasury yield, which, at 2.39%, has declined from about 2.6% a year ago. Hence, 30-year fixed-rate mortgages are still quoted with rates below 4%, and for now, homebuyers have been spared the impact of the rate hikes.

Auto loans, in line with mid-range Treasury yields, have wavered a lot and moved up only a little. The average APR on a 48-month new-car loan rose only 40 basis points over the past two years to 4.4% in August 2017, according to WalletHub, citing the most recent data available. Note that the offers of “0% financing” are usually in lieu of rebates or other incentives and are therefore rarely free.

The chart below shows the increase in the Fed’s target for the federal funds rate, from 0-0.25% to 1-1.25% (not including a hike on December 13), so an increase of 100-basis points. Credit card rates have increased in lockstep by 101 basis points. But bank deposits rates have lagged woefully behind, on the logic that credit-card borrowers and savers, both, are going to get shafted:

So how do these rate hikes translate for households with credit card balances?

Revolving credit outstanding of $1 trillion, spread over 117.72 million households, would amount to $8,300 per household. But many households do not carry interest-bearing credit card debt; they pay their cards off in full every month. Finance charges are concentrated on households that use this form of debt to finance their spending and that cannot pay off their balances every month. Many of these households are already strung out and are among the least able to afford higher interest payments.

Consumer credit bureau TransUnion shed some light on this in its Q3 2017 Industry Insights Report, according to which 195.9 million consumers had a revolving credit balance at the end of Q3, with total account balances of $1.35 trillion. This equals $6,892 per person with revolving credit balances. If there are two people with balances in a household, this would amount to nearly $14,000 of this high-cost debt. If the average interest rate on this debt is 20%, credit-cart interest payments alone add $233 a month to their household expenditures.

What is next for these folks?

For now, the Fed has penciled in, and economists expect, three hikes next year. But recent developments – particularly the expected tax cuts and what the Fed calls “elevated asset prices” – suggest that the Fed might “surprise” the markets with its hawkishness in 2018.

The Fed is currently pegging the “neutral” rate – the rate at which the federal funds rate is neither stimulating nor slowing the economy – at somewhere near 2.5% to 2.75%, so about five or six more rates hikes from today’s target range.

Interest rates on credit cards would follow in lockstep. These rate hikes to “neutral” would extract another $8 billion or so a year, on top of the additional $7.5 billion from the prior rate hikes.

But that’s not all. Credit card balances continue to rise as our brave consumers are trying to prop up US consumer spending and thus the global economy by borrowing more and more. Thus, rising credit card balances combined with rising interest rates on those balances conspire to produce sharply higher interest costs.

Since consumers with high-interest credit-card balances already don’t have enough money to pay off their costly debt, these additional interest payments will further curtail their efforts at making principal payments and thus inflate their credit card balances further.

For many consumers whose credit is already challenged, this scheme eventually ends in default. Credit card delinquencies have started to tick up, from 2.16% in Q1 2016 to 2.53% in Q3. While still soothingly low overall, the damage is always concentrated in the subprime segment – and on lenders that specialize in subprime lending. And there, delinquency rates are jumping. Yet these are still the best of times, with the lowest unemployment rate since the year 2000.

This parallels the delinquencies in auto loans. The 90+ day delinquency rate for loans originated by auto finance companies has hit 9.7% in Q3 2017, the highest since Q1 of 2010, when it was on the way down from the Financial Crisis. Delinquencies first hit that rate on the way up in Q3 2008, during the Lehman moment. But now, there is no Financial Crisis. These are the boom times. Read… Auto-Loan Subprime Blows Up Lehman-Moment-Like

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

My pity to the poor. They will always be among us. I came from such a background as a child. We were bad off.

That being said, debt is often a choice. Poor people don’t deserve the right to expect me to earn less interest just so they can afford to live above their means.

I want the Fed to raise rates. I can earn interest income on my savings without capital gains risk if they keep going. I deserve it because I lived a frugal life, saved a lot, and got past my under privileged early life on my own without public support.

Behold our intrepid hero, succeeding through all of life’s adversities without any federal assistance whatsoever, if you can believe it.

At least the story is truthy, even if it is recycled by libertarians anxious for bigger tax cuts on their inherited assets.

Thanks. I worked hard at it. I didn’t pi** my pay away on expensive vacations, large car loans, credit card balances, or the latest fashions. No Starbucks for me ever. The Sunday ad supplements were only curiosities to me when I was younger before my life matured. People couldn’t understand why I didn’t like to travel far away to expensive destinations. We tried to live on one check and saved the other. This is called being frugal. Hence, I see no interest to see why the Fed should support the less forward thinking with low rates at my expense.

Mr. Map,

My life story is identical to out “intrepid hero”-s story. No expensive vacations or cars or $50,000 kitchens in a tony urban condo.

To your point, I got these Federal benefits in the 1970 time frame, plus or minus two years:

BEOG grant, small sum, but it helped a lot

PELL grant, again, under $1000, but a lot in that day

Some kind of student loan or loans at 8% — stiff rate, the loan(s) were from my bank, I got a good job and paid them off really fast.

I know I live better and smarter than the ones I see in debt today. I never smoked, just to name one better and smarter choice. A lifetime of one pack a day cigarettes would finance a pretty good retirement, were the money to be properly invested in something that is not burnt up.

I just convinced my daughter to stop smoking after fifteen years of smoking. I don’t know why my entreaties to her suddenly worked last summer. She drives a new Subaru now, and I finally convinced her that the pack a day habit was a new car payment. She vapes now, a much cheaper habit.

And she tells her friends that their cigarette habit costs them the like of her rather nice, well-outfitted Subaru. I don’t know if her comments to her friends will ever bear fruit.

I worked hard, lived a frugal life and made better choices than most people stuck on the debt slave treadmill.

I had some meaningful Federal help given or lent to me in my late teens, too.

Married very young and 2 daughters with no formal education. Worked retail as a manager and would often face choices between keeping the lights on, paying the rent or eating from week to week.

Tried to get assistance, but lived in FL and was denied. Spent many years struggling.

Lots of rice/beans, cheap meats, no vacations, no toys, and always wrenching on my cars as I could not afford a mechanic and I drove old cars that needed work.

Put my spouse through school, then I went to school.

Now I work as an ICU nurse and make a decent living. Still no fancy cars ( 2006 xterra which I do all the work on to this day). No granite counters, no credit card debt……

So yeah, people do pull lift themselves up without help (though I did take out a small loan for community college for my associate nursing degree ($6000)). So I did get a small bit of help, but most was hard work, self discipline and a bit of desperation.

Same as CDR here. Married young, with nearly zero assets, went back to school (BS, MS) after Army tour…used my paltry ‘federal benefit’, which I considered delayed payment for services rendered in advance. Put wife through school to doctorate level at our expense…no grants or loans.

Built our own homes (first and current). Small mortgages for materials, paid off quickly. Always tried to live on one income (both school teachers initially, I went back to self employed construction work after a few years, she stayed for 32yrs in school system).

Worked our backsides off for many years, built rental properties, (for cash as we went) invested wisely in real estate, saved money, bought fair amount of precious metals…now we’re that millionaire-next-door. Last vacation was 18 years ago, took a 7 cruise (my first and last) for 25th anniversary. Buy new mid-priced vehicles for cash, and get 12-15 years out of them, do all my own maintenance.

In short, we’ve done everything right…..and none of it came from inherited money, because neither of our widowed mothers had any.

Nice to see others think the same as me. The stories above make me think of people I would like to meet.

If rates rise and, as a result, my retirement income goes up, my big goals are to take my wife of the vacations we missed along the way. Perhaps a boat ride to Alaska, top deck, to pet the bears. A visit to Sandals in the Caribbean in one of those open water cabins to scandalize everyone. See lots of sites in DC while staying in an upscale room. Assorted visits to Las Vegas to see some shows and people watch, no gambling.

Then we’ll be comfortable without worries and leave some for the nieces and nephews.

All we need is for the Fed to stay out of the way and raise rates.

While I agree that some people live above their means, there are so many that a single catastrophic event destroys years, and in some cases decades of living within their means.

Debt is often not a choice. A catastrophic medical debt, the death of the primary breadwinner, or loss of employment with no new job to be found for an extended period of time can destroy a lifetime of saving in a few months to a few years. I have seen medical debt for a sick child wipe out a family in a matter of months, and that was with good health insurance.

Since the crash of 2007, a great many people have be unable to find employment that is enough to support a family. And they have taken multiple jobs to try to make ends meet. Or any job that they can find. You may know this as the gig or sharing economy.

The more site comments I read on a daily basis, the more convinced I become that almost everyone is living with the illusion that they are somehow more deserving than some “other” person/group/sect that isn’t just like them.

This may be a little preachy, but it really is apt in the times we live in now. We are all in this together. It’s easy to look at the patrons in a Starbucks and come to your conclusion, it’s harder to look at the guy/gal down the block, on the bus, or in the market who’s trying their hardest to keep food on the table and a roof overhead.

The car numbers vs the trucks and SUV numbers that Wolf posts on here on a regular basis should be telling. How many of these people NEED a truck or SUV? Lifestyle choices are not problems of the few, but the many.

Yep that’s how our system works. One bobble and woops, months, sometimes weeks, later, and you’re living in your car or in a homeless shelter or shantytown. Our cult of extreme individualism means generally any family or friends you have will turn their backs on you, declaring that you’ve “chosen” to be poor/homeless.

It’s easy to look at the patron in Starbucks and not see that they’re in there living on a small drip coffee to stay in out of the cold for a few hours. Maybe they’re waiting to meet someone about a job; interviews happen at Buck’s’ a lot. Maybe they’re having a “flat white” which admittedly is kinda expensive at about $4 for a small, but maybe that’s their treat for that month. Maybe they like socializing, which is hard to do in our work-work-work society. Maybe they were me, too poor to buy any s’bux coffee but if you ask nicely for a “taster” they’ll give you a nice little cup, to sip and savor and it’s wonderful indeed when your budget doesn’t allow you coffee at all.

When I was at my down-and-outest, I could still use the bathroom, get a free cup of water or “taster” coffee, hang out and talk, just relax at that “third place”that’s not the couch I was sleeping on or what work I could find, and I’ll never forget that. These days the ‘bux is even a decent place to work, and pays for peoples college degrees, assuming those are worth anything any more.

That is a poignant story and I thank you for sharing it. It reminded me of a scary time in my life when I was hanging out at the library because I had nowhere else to spend the day. When my fortunes improved, I bought a home cash so that I would never again have no place to go. It’s hard to pull yourself up out of poverty, and it’s disquietingly easy to be cast back down into poverty.

A balanced economy requires people to spend what they earn over their lifetime. People who incur debts above their means hurt the system. People who save beyond their needs also hurt the system. In both cases, the system is unsustainable if everybody does it that way.

People who spend what they earn, and leave a reasonable amount for their offspring are what is needed in a sustainable economy.

Right now we have too many savers and too many debtors, and not enough people in the middle.

I am not going to choose to debate this point, with you, now – but this is as ridiculous and unsupported a statement as I am likely to read that is not in a Trump Tweet (from your post):

“People who save beyond their needs also hurt the system.” Save beyond their needs. What a load of rubbish.

Followed by “Right now we have too many savers”, further down in your post.

Hardly. Unsupportable rubbish.

Look at Japan and re evaluate. It is well supported, your echo chamber notwithstanding.

“Look at Japan and re evaluate.”

You should

Japan is possibly finally starting to recover from the damage done to it by the “Plaza Accord” and The Mistakes of QE then.

Look at the time frame it will give you some idea how long QE can take to unwind if Japan is finally recovering from the damage inflicted on it by the US with the “Plaza Accord”.

The US incidentally is now trying to inflict similar damage on Canada and Mexico, again to its advantage by ripping up NAFTA.

Blaming the US as a nation is really unfair, but the US is doing, what its Globalised Vampire Corporate Masters tell it to.

@T.T.T.

Nevertheless, the comment was directed at the USA – and not qualified as being a characteristic of the Japanese in any way.

Too much saving IN THE USA ? Hardly.

Americans are told they need to save more for retirement and at the same time also told they need to spend more to grow the economy (must always keep growing). Ben Bernanke referred to savers as “hoarders” and, in testimony before congress, he explained there is no reason retirees should expect their savings to earn a return above inflation.

If you save money you are a minority among the masses and the minority gets trampled. After 2008 Ben lowered mortgage payments of the typical homeowner by over $250 (with his low, low rates) but the minority of renters received nothing but rent increases. Why care about renters, they are a minority and everyone else is happy with their extra $250/month.

Why care about savers getting wiped out by inflation when the vast majority don’t save and will have their debts forgiven by inflation. Even though people lose purchasing power they are still, overall, happy to have their debts inflated away. It’s best to be part of the crowd – borrow and spend as much currency as you can. Use the money to buy assets and let the debt get wiped away by central bankers, that’s what wealthy people do (just ask Trump).

From about 1981 to 1994, bond investors probably earned more than the rate of inflation and since about 2009 they have earned less. Be glad the government did not allow the FDIC to go under, as it probably would have if the major troubled banks had been allowed to go bust. Then you would have complained a lot more. It is not a surprise to me that many Americans are having a tough time these days. Since I got my first credit card almost 50 years ago, I have received a lot more credit card rebates and bonuses than I have paid in interest charges.

It wasn’t your fault or my fault that the US went to war in Viet Nam and later in Afghanistan and Iraq. But as Americans, we are responsible for the costs incurred. We will be paying for costs related to the Middle East wars for decades to come.

Oh b.s. Get off The Bernank Hero bus. Assets would have been repriced at lower levels and life would have gone on. Common stock would have been wiped out and creditors converted to equity, if there was any left.

BTW, the crisis isn’t over.

Well said.

The crisis has past. The bill (so far) to paper over the crisis was an additional $10 trillion added to the debt. Thankfully the debt is just a number stored in an electronic account and such numbers are easy to create and destroy. But the question remains: now that we have decided to start monkeying with the electronic numbers (creating more of them at will) what will we use as money and a measure of account for people’s work going forward? And what will become of people who thought they were saving wealth but are left with only worthless electronic numbers?

the crisis is past (or has passed) I must be more careful or get caught by the grammar police

You don’t deserve some arbitrary level of real return on your savings.

The period of 1980 – 2007, with regards to real risk-free returns (roughly 2% real return in 3-mo T-bills), is a historical anomaly.

From 1930 – 1980, the real return of risk-free capital was negative, just as it is today.

One could argue that in a strong, highly productive economy that real risk-free returns are justified… but that’s definitely not the economy of today.

Not to worry. Increasing wages, per the guberment, will more than offset any interest rate increases. Don’t be a Scrooge this Christmas. Load up all of those credit cards and take any more offered.

Used to be government put a cap on interest rates. The Supreme Court broke that by allowing the highest rate, most laxly regulated state provide credit across state borders.

Money talks. Big banks have been organizing the law in their favor very efficiently the last 40 years or more.

Does it really make sense that savers will sit still while being raped by central banks and their “tools” on Wall Street and in Government ?

How long ’till negative real yields will be recognized for what the are ?

The puns “open carry” and “open carried interest” come to mind :-), given the analogy with the current congress push to let the laxest states control the rules for open carry and concealed carry of weapons, nationwide.

Perhaps criminals will set up mailboxes in South Dakota so as to be able to enable their criminal actions. Oh wait, they already did. For example,

Citi – Citibank, National Association (Main Office)

701 East 60th Street NorthSioux Falls, SD 57104

I have read your post several times and am still unable to understand how “poor people can afford to live above their means” people factors into your seeming complaints about substandard interest rates on your savings accounts. According to Trans Union 195.9 MILLION people had a credit card balance in Q3. I’d reckon that only a small portion of these individuals would be considered “poor”. I think most folks instead have only succumbed to what I call “the immediate gratification syndrome” or worse are charging ever more on the credit card simply to maintain their lifestyles.

What bears considering at this point is how can these rentier/pirate banks get away with charging such a usurious (20% and up) interest rate to lend funds in the first place- funds the Fed conjured up out of thin air and lend to them for practically nothing! Sadly, I fear, this type of greedy rent seeking has become such a drag on the economy that the system is rapidly slowing down- just like as if someone was pressing the brake. Or, put another way, the parasites of society (nope, they ain’t the poor people) are beginning to suck the very life out of the host economy.

What also bears considering is that, minus increasing amounts of debt-spending and inflation of CPI, what exactly is the true growth (??) rate of our economy’s GDP?

Me, I’m wonderin’ if getting into the manufacture and sale of guillotines n pitchforks might be a good idea- there could be quite a demand in a few short years.

rx

The Federal Reserve and the complicit government bailed out banks and big businesses by giving out free money (QE) and ultra low interest rates like candy at the expense of savers and pensioners. Who made them high priest/priestess at the Eccles Temple? Who made them rules of free markets? IF so, how can the markets be free if they stick their noses in the markets? What a shame. We want our money back.

Yellen, keep raising them rates higher faster.

Congress made the Fed with the Federal Reserve Act which President Wilson signed into law on 23 December 1913. Originally, this Act gave the Fed a 20-year charter, just as Congress did in 1791 with the First Bank of the United States and in 1816 with the Second Bank of the United States.

But on 25 February 1927, Congress pulled the 20-year expiration. “To have succession after the approval of this Act until dissolved by Act of Congress or until forfeiture of franchise for a violation of law.”

The United States does not have a ‘free market’. We are controlled primarily by the Federal Reserve Bank of New York. Citigroup got TRILLIONS of dollars of secret and nearly zero percent interest money from the Fed ten years ago. From their website: “Working within the Federal Reserve System, the New York Fed implements monetary policy, supervises and regulates financial institutions and helps maintain the nation’s payment systems.”

Supervises and regulates … ???

Points well made.

As you said, “Supervises and regulates . . “. In each of the most recent three bubbles, in the case of the extreme rise in the various stock indexes, the so’n’so Fed could pinch off the speculative mania by increasing margin requirements. But it never does, in part because the Fed cannot see the bubbles that are visible to all. Cooling speculative fever by increasing margin requirements is an excellent example of supervising or regulating, both.

In the case of the mortgage-lending frenzies, they could cool that by increasing down-payment requirements — instead those requirements get ever lower, blowing the bubble bigger. I recognize that this is only operative in the sphere of Federally chartered, or regulated banks and agencies, but they could stretch it to cover mortgage lending behemoths that operate across state lines.

No supervision or regulation is done or can be done. To do so would crimp the profit line that enriches the elite banksters, preventing them from building ever larger Hampton cottages.

Let’s not get carried away here. There has been no tightening and there never will be. The Fed’s QE program stopped several times in the last eight years but it was always started up again – why expect anything different this time? Don’t expect the flood of cheap currency to ever stop. QE3 stopped (for the moment) but Draghi and Kuroda and the rest of the gang stepped up their efforts with a massive gusher of even more currency. There is more currency flooding around the globe than ever before – talk of tightening is nonsense.

The Fed says they are going to tighten yet somehow the dollar has not strengthened against the Euro. Draghi is still relentlessly printing Euros but somehow it holds up against the dollar. Could it be the market knows the U.S. (a country with a huge debt, unsustainable deficits and now cutting it’s tax revenues) needs to print dollars to fund government spending? The Fed has hit the QE pause button to try to slow the loss of confidence in the dollar but we know QE will soon start up again (as it has in the past).

The U.S. cannot pay it’s bills. The Fed needs to print money to monetize the debts but the more money they print the more the government spends. We are on the path toward a currency crisis (worthless currency) and there is no incentive to change course so we never will. The dollar (and the Euro and Yen…) will be destroyed and the suffering and starvation will be horrifying. Money is what motivates workers to grow your food – if money becomes worthless what will motivate people to harvest your food. It is dangerous what the central banks are doing but society just sleep walks toward the cliff. Kicking the can down the road? Not hardly, they are burning up the supply of confidence in the currency and the supply is running low.

Fed tightening? Not a chance. A momentary pause is not the same as a course correction. The captain may have cut the engines but the ship is still floating downstream toward a waterfall.

Stay tuned on the Fed’s QE unwind. A lot of people in the markets think like you do, and so the markets are not reacting to it. This encourages the Fed like nothing else to move forward.

If the markets totally blew up tomorrow, maybe the Fed would stop. But for now, stocks are at all-time highs, real estate is booming, bond yields are low, asset bubbles reign everywhere. These are the greatest encouragements for the Fed.

IMO van_down is correct.

Because the “tightening” you keep referencing, and the QE “unwind”, is teeny weeny itsy bitsy as to be in fact more easing not tightening, and is massively overwhelmed, canceled out, and rendered useless by huge QE’s going on in Japan and Europe and with looney tooney policy like the Swiss bank buying U.S. stock.

The Fed rate is far below the rate of asset appreciation (maybe a TRUE measure of “inflation” and therefore IMO it is still in MASSIVE stimulate and easing mode.

IMO the fed needs to raise rate TODAY by 3-4% just to move towards neutral monetary policy, and consider additional similar increase the following week if bloated asset prices do not fall.

Wolf,

I think you inadvertantly gave the answer. Think about this:

Stock markets are up because of realization of high and increasing inflation. People in the know are moving money into “productive” assets. A lot of speculation too.

Housing continues to try and climb. Again, getting cash into something tangible.

The bond market is the big conundrum. If the smart money knows inflation is continuing, why would they stay in bonds?

The primary answer is they are pretty sure the Central Banks will bail again and target bonds. Thus bonds will be protected.

All of this makes total sense from a standpoint of serious inflation occurring and accelerating.

I too am in the camp that the Fed’s moves are mostly theatre to convince the masses that everything will be ok again.

The CB’s have to get signficant inflation to reduce the enormous debt overhang around the world.

So more QE is in the offing. It may be called something else or there will be outright printing hidden by the governments.

But rest assured, things are NOT going back to past normal.

Finally, I am seeing signficant price increases for food over the past 6 months. Oil is on the way up again and that will pressure prices upward. Of course many wages will not increase with prices and thus more and more people will continue to loose. Expect social unrest to skyrocket.

” Draghi is still relentlessly printing Euros but somehow it holds up against the dollar Could it be the market knows the U.S. (a country with a huge debt, unsustainable deficits and now cutting it’s tax revenues) needs to print dollars to fund government spending? ”

1) Not yet. The financial markets are too manipulated … world wide … by relentless central bank money printing and HFT so that no price is accurate.

2) I strongly suspect the overall ‘secret’ plan was to print massive amounts of money in unison world wide so that all currencies degraded at the same rate, thus holding parity. The money printing would provide free benefits for the citizenry, such as the ECB’s financing of EU socialism or the SNB and tens of billions in stock purchases. The US provided low rates so that asset bubbles would provide a replacement for the traditional return on capital from savings and benefit the top of the upper class as a result at the expense of everyone else.

The US raising rates will have no direct effect on the others, who will print until the end of time if possible.

The real fun will occur if equity prices fall and the SNB has to explain how they ‘lost’ money when their wealth came from endless printed money. Perhaps they’ll join the bitcoin rage and blow the values to seven digits using their printing press? Or when the rest of the world sees the ECB and Eurozone realistically. Or if some other major power normalizes a bit.

“I strongly suspect the overall ‘secret’ plan was to print massive amounts of money in unison world wide so that all currencies degraded at the same rate”

You only need to look back to 2008 to see how wrong you are.

The FED said PRINT. Everybody Except china, which has always been clandestinely printing, and Japan that was looking for a way to stop, said NO.

Eventually they came round to what had to be done.

Now the FED says STOP Printing. Draggi and china say NO,NO.

There is no Global Synchronised CB action, this is a BIG part of the problem.

Spot on! All fiat currencies revert back to their intrinsic value – ZERO.

Currency is a medium of exchange, while money has that property, but money is also a store of wealth; currency is not. There is a big difference between Federal Reserve Notes (FRN) fiat currency and gold and/energy. Gold/energy is money and FRNs are just a currency.

Effectively every FRN in existence has a coupon. The FRN on paper is merely the manifestation of some debt somewhere else. Most of those debts are in eDollar form. It makes no difference as they were ALL borrowed into existence by somebody at some point in the past.

Without MORE borrowing in the future the interest owed on the debt that created today’s money can never be paid. Or, it can, but then there is inadequate remaining money to repay the principal; this is very simple math.

There used to be the petro-dollar recycling with KSA (GCC at large) – US (NB, many say the USSR died and went away; I’ll argue, no, it just packed up and want to America) sends FRN clownbux to the oil (energy) based world, receives oil and trinkets that the American consumer loves (Walmart, etc.). The US has been able to sustain this because it has been exporting inflation to the world via FRNs. Due to a severe decline in cheap energy (energy that is easy to extract – think energy return on energy invested or EROEI), the petro-dollar scheme was failing in the late 1990’s/early 2000’s. Enter China via low interest rates set by the FED. Then we had the plastic/junk-dollar scheme with China and that lasted ’till the financial melt-down of 2007-2008 (China would recycle FRNs for treasuries). It’s important to note that currencies are a confidence scheme; nothing more. The rest of the world, including China basically said “enough with the treasury purchases.” Sure there was little purchases here and there, but the world had run out of the desire to hold treasuries, hence the math problem.

Now, back to the math problem. Printing money is the only way to solve this math…literally, it is. Janet (and other CB clowns) has to print the coupon because there is no credit growth that can pay it! If P is outstanding now, and P+I is owed one year from now, SOMEONE *must* borrow that extra I in order for it to EXIST in a debt-money system. So central banks have been taking up the slack since the financial crisis. How do you think their balance sheets have exploded? They literally have printed up I.

It is either that or FRNs snuff themselves out of existence and cease becoming currency. Deflationists understand this “blackhole vortex” principle of deflation but they don’t understand that a scarce FRN will lose its ability to serve as a currency due to its scarcity. Excessively scarce things aren’t currencies.

*There is NOTHING that can SOLVE the problem of exponential growth in a FINITE world*

The death of this current fiat system is a process not an event. That is just one reason the CBs are taking turns printing.

For the extremely frugal who have to live on credit, my heat goes out for those people. But I suspect most of those are few and far in between. The convenient stores, Starbucks, and casinos are filled with low income individuals. Netflix, cable, and a separate home internet provider are wants. Whenever I see those habitual Starbucks customers (We all know a few of those people) l, I wonder what is like to be rich. I mean I’m doing alright in life, but these people must have run out of places to put their money.

In most cases, the only reason a person needs to buy new clothes is maybe a first time job interview or a change in size. Americans buy new clothes because they say they have gone out of style and wonder why they are in the debt situation they are in.

I used to have a separate internet package for the house. Cox has a monopoly here. Kicked them to the curb. That will be a yearly savings of just over $900. Changed garbage services and saved $230 annually. Some people buy those bags of chips for four dollars a bag. You can get some celery and peanut butter for half the cost, and it is much better for you.

Poverty in America could be eliminated if only the impoverished would listen to your sage advice, Ray, particularly about overpaying for their internet packages and refuse pickup.

I’m just wondering how those homeless people manage to slip into those glamorous casinos with their ragged clothes and shopping carts, and what they would do there. Perhaps they favor the baccarat table.

Right on, Walter, an sarcasm noted. Ray Rogers, you seriously think that poverty is caused by not bundling their intenet connection with other monopolistic services? Get real.

I’ve read both of your snide remarks. Both are without merit. Before this job I did bankruptcy work for a large company. When a company is a creditor you get to see the nature of the debt accumulated.

Like I said earlier there are some people with credit card debts that do so as the last result, but sorry that isnt the picture for most. When I did that bankruptcy work I could see those who filed for medical reasons and those that just loved to shop. Very few fillings that I saw had less than 5 digit credit card bills, most of which on multiple cards or store accounts? How does one end up owing thousands on Kohls, JCPenny’s, and Best Buy without being irresponsible?

And what about Wolf’s ongoing reports on the sale of cars vs Subs and Trucks? I’m sure Americans NEEDS these vehicles. The consumer debt numbers speak for themselves. If this was skyrocketing due to frugal people no longer able to afford the essentials, youd have an instant pitch-fork revolution.

Maybe we should go to studies that show people don’t save. Oh it’s true. And is it because people are impoverished. It’s amazing how I was still able to save and have at least $1500 in the bank many years ago, allthewhile making about $10 an hour. And yes I was considered in the poverty range then (then being classified as below the poverty line really meant you didn’t make much, not like what it is today). How did I do that Walter? I’ll tell you how. I had roommates and didn’t splurge.

When my better half is home (she works abroad, and we don’t get to see much of one another- the word is “sacrifice”) we go out to play bingo once in awhile. We meet and talk to these people at the casinos. They have jobs that pay 20k, 30k, 50k, 70k. They are usually very polite and open. I hear what what they spend on the slot machines. We would never do what they choose to do despite making more than this. And no Walter, we are not trust fund babies like you may attribute to people who are not impoverished. We do this thing called- wait for it- work many hours.

I’m sure others can attest to this. If you work with people who you are close enough with to talk about basic home life and finances, the debt problems are very apparent. Heck, all I have to do at work is look at the parking lot. The 2016 and 2017 models say enough.

What about home sizes Walter? How has the increase in home sizes across the board not speak about rampant consumerism? And cars. How many cars do people need? I’ve been hearing problems of rampant consumerism for decades from people like you, and now you want to say the excess doesn’t exist? How about we take a walk down University Ave shall we? The one near us is lined with coffee shops and restaurants and is filled with college students. It’s funny, I don’t remember being able to afford to do that. I’m not talking your cheap takeout food. I’m talking about Indian, Lebaneese, Turkish cuisine. And even the takeout is not the dollar menu. Here we are talking about an $8 Dinner.

I’ve already addressed you before on assuming that successful people were given their money, so I’m going to save my time with the one. But anyone who is honest, and has been around enough people, has an idea of how the culture of rampant consumerism destroys finances. This is not to say that some people have not done all they can. I’m just addressing the 8000lb gorilla.

One should keep in mind that the US is incredibly rich by any standard. The US poverty line is about where the average yearly global income is. Of course, there are cost of living issues and purchasing power parity issues, but as a rule of thumb a lot of US poor are not bad off in a global sense.

There will always be a percentage that are “justifiably needy” due to medical or other reasons. I don’t know what percentage that is.

I would guess that probably half the poor people in the US could live a much better, more “decent” life if they were more frugal and responsible with the resources they do have.

And yes, I have lived right near the poverty line while a student, but enjoyed the privileges of a good public college environment that helped me get through it. I do know what it’s like to shop at the thrift store, have no cable TV, etc. It can be done. (not married, no kids, rode a bike, ate peanut butter and tuna fish, etc, etc, etc)

I can second your comments about college students here in the UK. When I was a student back in the day (early 80s) I remember going to a restaurant only one time in my first year…anyway to cut a long story short, I was lucky ‘cos I had my tuition paid for me, but the idea of going into debt scared the living daylights out of me at the time. Fast forward to today, and I went to check up on some ex pupils at their university (yup I’m a teacher), and not only do they have sky high tuition fees with high interest charges, but they have become totally inured to debt. If you know your coming out with 50+ grand in debt, they figure it does not make much of a difference, viewed over a lifetime, to pay it back. That’s the scary bit, either they have no idea how long it takes to pay back such sums, or they are reconciled to always being in debt. This will end in some very angry people, and the country voting for socialists/or worse communists

Well said tings true.

They kick homeless people right out of the local casinos. If you appear homeless the goons will invite you to leave.

Wolf,

Why call it “credit card balances” when the correct term is “credit card DEBT”?

I realize you probably inherited the term from the source article (wallethub.com?). But still, this strange twisting of the English language is a funny thing. Another example is the term “savings rate”, which used to mean “what percentage of your income that you save”. Now it has taken on the meaning “the interest rate you earn in a savings account”, because that is how banks use the term in their advertising. Banks do not want to remind potential customersthat they may be paying INTEREST somewhere, so they avoid the term when describe even interest being paid to you, the customer. I suspect banks want very much to avoid that the public gets the idea to compare the interest rate they pay to the interest rate they get paid, considering how gigantic the spread has become.

Anyway, let’s try not to use the language of the oppressors and their advertisers/propagandists.

The industry uses terms like “account balance.” You see this on your credit card statement. It never says “Credit Card Debt” on your credit card statement. That would be too scary :-]

There are a lot of terms for “debt,” including “credit.” So we should call them “debt cards.”

Ironically “debit cards” (with an i after the b) are not debt instruments but just a payment card, as a replacement for cash.

The $UST3M @ 1.33% is up 140% in the last year.

The 10Y hardly changed.

In the last three years, the 3M is up by 4,333%, the 6M up by 1,533%, the 1Y up by 704%. They move like penny stocks, like Bitcoin.

The 10y is up by 9% and the 30Y is down slightly by 2.5% in the last three years.

Here is a catch :

1) the Fed rate increase are priced in.

2) When the structure of the US govt debt is extremely in favor of the short duration, the rate increase will be counter by short duration being pushed down, because they are the only ones available. They are needed for collateral.

There is a huge demand for the long duration, but the market is starved.

Today the 30Y @ 2.77%.

Within 5 to 7 years, inflation will bite hard.

The short duration at that time will cost the govt more than the 30Y at 2.77%, today.

– I also would keep an eye on Hong Kong. People over there have mortgages with interest rates to short term rates. And Hong Kong follows whatever the FED is doing with interest rates.

Good point JM.

Many other countries outside of the US have floating rate mortgages linked back to their countries reserve banks rates. I use to have one in New Zealand. Only recently have 5 year fixed rate mortgages become available.

When I tell friends back in NZ that you can obtain a 30 year fixed mortgage in the US their eyes glaze over.

“If the average interest rate on this debt is 20%, credit-cart interest payments alone add $233 a month to their household expenditures.”

For most people this will not be a problem. What ‘good credit’ people do is consolidate their balances and transfer them to a 0% card for an intro period of 1 year. And when that period runs out, they then transfer it to different card at 0%. All done online instantly.

So the only people who will be effected by the miniscule rate raises coming (I guess) are the bottom 20% of credit users who don’t get these 0% offers.

>> “What ‘good credit’ people do is consolidate their balances and transfer them to a 0% card for an intro period of 1 year.”

This is exactly the theory that blew up during the Financial Crisis. 0% credit card goes to 29% and all other 0% offers suddenly vanish. If you don’t have the cash sitting in an account somewhere to pay off the cards when 0% jumps to 29%, you’re engaging in one of the riskier bets a consumer can undertake.

>0% credit card goes to 29% and all other 0% offers

>suddenly vanish.

aka Universal Default.

“If you don’t have the cash sitting in an account somewhere…”

There are exceptions.

My son used such cards instead of construction loans from banks, when he built houses to rent. He finished each house within the year and paid off the credit cards with financing from a normal mortgage on each finished house. The mortgage payments were then covered from rent paid by tenants in the houses.

His strategy requires a very reliable rental housing market, which he found in a medical college where the medical students are responsible for housing themselves.

The amount of smug moralizing going on here is sad to read. Sure, there are people using credit to live beyond their means, but many, many more are in debt because of a layoff, downsizing of salaries, or a medical emergency. Especially as they pass the big 5-0. I know. I’m one of those. I’ve saved, I have assets, we’ll make do. Others are not as fortunate.

Amen, brother. The Bootstrappers rarely seem to realize that they are so much closer to the precariat that they look down upon than their Lords and Masters whom they tend to identify with (or, sadly, resent as much as they detest those below them–a nasty psychological bind).

Luck and a wonderful family have provided for me at least as much as any effort I put in. I’ve never used government assistance but am damned glad it exists. And having moved to a rural area I can say that there is no correlation between hard work and financial success (I saw the same thing when I was young living in Jersey City where the Hispanic families worked like dogs and had nothing). When I was a full-time professor I brought my kids to university one day and pointed out to them that the hardest-working person I knew was the lady who ran the Starbucks kiosk; she worked huge hours for nasty kids and condescending profs, was divorced with two kids and had to bring them to work with her when they were sick because there was no one to take care of them, and got paid crap compared to the profs and administrators who disgracefully looked down on her or didn’t notice her humanity at all. I wanted my kids to be very clear about who is doing the work and why they bloody well better treat them with respect.

Awesome. To avoid diluting it’s meaning, I reserve the use of the phrase “hard-earned money” only for the incomes of people like your kiosk worker.

I urp (figuratively speaking) every time I see a TV huckster telling viewers they “deserve” to buy his crap with their “hard-earned money”

Pleasantries help folks kike the Starbucks kiosk workers, I think.

For me (and her – she laughs) I tell the cashier at the pizzeria to charge my credit before I return to pick up the pizza, so if I die before then, she’ll get paid (I’m 86).

Well…professors etc. do perform real work. But they have obtained the credentials to perform less physically demanding work and get paid more for it. That is the real lesson for children: You can earn a low income the physically hard way or you can acquire the knowledge and skill to earn a better income in a physically easier way. I came to this realization in my 20’s when I was worn out from the poverty grind.

Alb, I’m inspired by your comment, but the hardship case isn’t convincing. One needs to revisit Thorsten Veblin’s, “Theory of the Leisure Class”, to be reminded that the impulse to rise in an ego-driven social system keeps the hamster wheel spinning. Unless the sheeple have enough self-esteem and gumption to pull away from the forced-march of conspicuous consumption (sort of rhymes…) they are doomed to indentured servitude to the Trumps of this world. Yes there are sudden and tragic debt catalysts, but the majority of debtors, I’d guess, have little self-control, are emotionally “needy” and are steered by their need to gratify rather than think, plan and reason.

Work hard, live below your means, save, invest…. Its not get a job, get a car loan, buy a too-big house with little down and big mortgage, use the CC to finance vacations, etc.

The root of frugality is fruit, as in enjoying the fruits of your labor. The guy that cut Cox is right-on. Read Your Money or Your Life, A Return to Thrift, etc. Security is not driving around in a leased MBZ, its being able to never HAVE TO work ever again.

People are just stoopid trying to flash fake wealth. They live beyond their means even if they don’t go bust right away.

The FEDERAL RESERVE is not federal; they stepped in to save the banks not peeps. And they don’t have reserves either.

Money is losing it’s relevance. Stop worrying about working hard and saving money (hoarding as Ben calls it). Borrow as much as you can and pay it back later after it has much less value. If possible invest in assets that will commit (enslave through contract) workers to pay you a portion of the fruits of their labor forever.

The rules have changed – stop saving money and start accumulating assets. Debt is meaningless.

I think one of the points that is missed in the “people shouldn’t go into debt” arguments, is that sure, people /shouldn’t/ go into debt.

People also shouldn’t drink, smoke, drive too fast, along with a whole lot of other things. But the fact remains that this isn’t how the world works.

Same with debt. Society is structured in such a way that most people are unable to resist the pressures of using consumer debt – it’s designed that way, most people are going to be in debt. It’s an open question which 80% of the population constitutes this crowd, but that 80% is by design.

Good for you if you’re not, but it’s because you’re wired differently – that’s all..

Great comments people, most of them fairly respectful. The problem is we having been collectively living above our means for several decades. Along the way millions have been marginalized and end up living in misery, (usually for the benefit of the 0.01% ultra rich). Succeeding in this environment is tricky, you might seem to be okay living the high life during you prime earning years but odds are reality will catch up with you and send you down a peg or two. This can be humiliating and heartbreaking.

We have to learn to get by on much less. Forget about new cars and cable tv, stylish cloths and eating out. America is extremely wasteful. The rest of the world is fed up and change is in the wind. Voluntarily reduce your expectations before the market does it for you. Living with less can be liberating, and offers a sense of self that the consumer lifestyle desperately tries to extinguish. Good luck out there.

Blaming poor people for being poor lets the Fed off the hook for its actions. Millions of American jobs could not have been shipped overseas without the trillions of off shore “dollars” created by foreign banks, especially in China. The fact that the Fed never knew about those off shore “dollars” (about 25 trillion, give or take a trillion) shows just how incompetent the Fed and most economists are. Those off shore “dollars” are never going to be matched to actual dollar assets, so it’s a time bomb at the center of the world financial system . The Fed raising rates will ignite that time bomb, but the Fed is to blame for letting things get so bad in the first place.

Drango,

Eric Townsend at Macro Voices has done a series of interviews With Jeffrey Snyder on EuroDollars. Very enlightening. Greenspan was clueless.

QQQBALL,

Jeffrey Snyder’s Alhambra Partner posts and Wolf Street are the only two economic sites I read on a daily basis. There are too many sites that let politics cloud their judgment, or are just plain clueless. Just like Greenspan.

Jeff Snyder is one of the best out there, without a doubt.

His commentary on the EuroDollar system is enlightening and should be required reading for anyone who wants to opine on today’s economy, the Fed, inflation (or lack thereof), or markets.

He mercilessly takes down the Fed at every turn, without being a gold bug, inflationista, or conspiracy theory peddler. It’s not that he is against central banks, he just realizes that they’re enormously incompetent.

The only problem is he writes a ton of posts, often on somewhat complicated topics (e.g. EuroDollars), and so it can be a bit of a slog to actually try to educate yourself to the point where you fully understand what he’s talking about.

Here’s a fascinating post from earlier this week (Wolf please take down if you don’t want me linking): http://www.alhambrapartners.com/2017/12/11/bonds-vs-economists-the-means-to-the-end/

It talks about the disconnect between actual market participants (e.g. traders) and economists at primary dealers (banks). And when the Fed surveys the “market” they’re really surveying the economists, not the actual people involved in the market. For example, during the taper tantrum of 2013, Fed surveys of economists saw– overwhelmingly– the consensus that rates were going way higher… meanwhile, traders at those very same banks disagreed and were buying treasuries at a rapid pace, expecting rates to go down. Guess who was correct? No surprise, but it was not the economists. Yet, it’s the economists who the Fed listens to, creating a massive echo chamber disconnected from the actual reality of the market.

Increased costs for consumer credit is the third point of dismay for populist anger. Tax cuts for the wealthy, and no healthcare healthcare reform were the first two. While the Democrats build their vision of Herland, constituents have no place to turn. For once its not the Feds fault, governance has ceased.

As a side-note, I was just noting that the fixed rate component of I Savings Bonds is still 0.10%.

wtf?

Just forget those.

Grew up very poor before food stamps (mother had a heart defect) … ate surplus food, flour, sugar, cheese, oatmeal & powdered milk. Went off to war in Southeast Asia; saw how poor lived there and knew I had been rich. Invested 100% of all my wife & I had earned into a custom home on a golf course in July 2007. 25% down on a property valued at $1,068,000.00. It went down 62% in the housing bubble; my job disappeared; could not sell; realized that I was a SLAVE. Took five years to sell. Left the US and paid off credit cards. I’ll never go back to debt.