The Biggest Sinners in the Dow.

All 30 companies in the Dow Jones Industrial Average have now reported earnings for the third quarter. As required, they reported these earnings under Generally Accepted Accounting Principles (GAAP). These standardized accounting rules are supposed to allow investors to compare the results of different companies. But that’s too harsh a fate for many of our corporate heroes, and so they proffer their own and much more pleasing accounting strategies – as expressed in “adjusted” earnings and “adjusted” earnings per share (EPS).

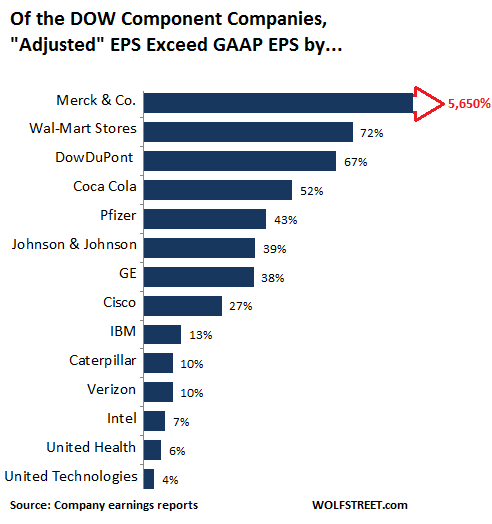

Of the 30 companies in the DJIA, 14 reported “adjusted” or “non-GAAP” earnings in Q3 that were significantly higher than their GAAP earnings. Total “adjusted” EPS of these 14 Dow components exceeded their total EPS under GAAP by 26%! Nice work!

“Adjusted” earnings are the great American fiction conceived to serve the great American passion: inflating share prices by hook or crook.

The biggest sinner: Merck & Co. miraculously turned its loss of -$0.02 per share under GAAP into an “adjusted” profit of $1.11 a share. This is not a “one-time” event either. Merck keeps showing up in the ignominious top five Dow earnings adjusters time after time. Among the repeat offenders in the top five are also Pfizer, Coca-Cola, and GE.

So the theory that these are “one-time items” that should be excluded – even if that theory ever made sense – falls apart if it happens quarter after quarter.

The chart below shows the 14 Dow components with EPS that have been inflated by adjustments, and the percentage difference between their EPS under GAAP and their “adjusted” EPS. I cut Merck’s bar off because it goes to 5,650%, which would be about 12 feet beyond the edge of the chart. Wal-Mart Stores inflated its earnings by 72% and DowDuPont by 67%, and Warren Buffett’s favorite beverage company by more than half:

Under increasing pressure from the SEC, some of them disclosed GAAP earnings upfront in their earnings report, before pointing at non-GAAP earnings. Others were not so forthcoming. J&J’s GAAP EPS was particularly cumbersome to dig up, buried in the earnings release all the way down in the Non-GAAP reconciliation schedule.

These are among the large companies in the US that are deemed to be the most representative of their industries. They tend not to go entirely crazy, unlike smaller companies that haven’t yet figured out how to make money and that desperately need to show some kind of positive results.

Twitter is a good example. It’s not in the DJIA. It loses money every year, but after its adjustments, there’s always a fat “adjusted” profit. In the last quarter, it lost $21 million under GAAP, on declining revenues. But after it got through “adjusting” a lot of expenses out of the way, its non-GAAP income was $78 million. This took its loss per share of $-0.03 under GAAP to an adjusted profit of $0.10 per share.

These kinds of tricks work miracles. They’re promoted endlessly on Wall Street. And many companies use them. Even though GAAP gives companies a lot of leeway to beautify their results, it’s just not enough to hype stock prices sufficiently.

Some companies show alternative measures to GAAP earnings, after they show GAAP earnings, to show for example how the core portion of the business is doing. In many cases, these “core” earnings are lower than GAAP earnings because they cover only part of the operations. Such additional metrics, if presented as additional metrics, might make sense. Pointing out particularly ugly items that impacted earnings also makes sense.

But EPS is a final summary figure that underlies the all-import price-earnings ratio which is used to value shares. Wall Street analysts and the media put these “adjusted” numbers into the headlines, which are all many people and trading algorithms read. Data aggregators use these “adjusted” numbers in their reports and charts about the stock market overall, such as the aggregate earnings multiple of the S&P 500 companies. These “adjusted” numbers are everywhere, drowning out any sense of reality.

Even the SEC has lost patience with companies promoting their beautified non-GAAP measures. Since last year, it has been admonishing them about the prominence of these “adjusted” numbers in earnings presentations and in press releases. Some companies have since abandoned “adjusted” earnings. But many others – including about half of the Dow components – are still doing it.

Wall Street loves nothing more than to tout these “adjusted” earnings and how they “beat” expectations that have been lowered in prior weeks so that they could be beat. And given the grossly inflated stock prices, boosting earnings with “adjustments” is a game that is just too good to stop.

Finally time to make some easy money by betting on the collapse of certain brick-and-mortar retailers, years after it began? Here’s a grisly thought: there’s an ETF for that. Oh Lordy. Read… Wall Street Discovers the Brick-and-Mortar Meltdown

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Given that their earnings are so meager, you have to wonder where the funding for share buy backs is coming from. Silly me I know, they are borrowing it. But the combination of poor earnings and heavy debt loads would be pure poison if the economy hits a rough patch. Naaah….that couldn’t happen could it ?

Poison for whom? “They” have things figured out i.e. “you” will pick up the tab. After all Murica picked up the tabs for the banks last time. This time around it will be for the entire 1%. Ain’t life grand?

I don’t think they can pull it off a second time (if you count the dot com bubble, a third time) without grave political and economic consequences. Although I have been a staunch advocate since 2007 that deflation was in out future, even I would contend that another infusion of 12-20 trillion in liquidity would induce massive inflation, and bankers hate inflation. I’m expecting frozen accounts, credit card rationing at a fixed percentage of your credit line per day, lines at ATMs for $60 a day, bail-ins, and naked immiseration next time.

I would think the Bankers love inflation. It makes loans easier to pay back. That makes the risk of bank panics lower. They get more nominal dollars when they lend out under inflation. It makes their debts easier to pay back.

The natural deflation from an innovative society destabilized the fractional reserve lending racket. With the monetary inflation generated by the FED and the Government’s constant expulsion of debt, help assure that future bank panics don’t come to fruition.

IMNSHO what we are seeing is the “new normal” in international business accounting, whereby the “profits” accumulate in tax havens and the “costs/expenses” accumulate in the high tax areas, where these are deductible business expenses.

The problem [for corporation management] then becomes how to get the tax free money back into the domestic corporate coffers and on to the stockholders in the high tax area without incurring taxes. Stock buy-backs are the vehicle of choice as the buy-back qualifies for capital gains tax treatment, rather than a dividend taxed as earned income.

One way this could be done is for the off-shore funds to be “lent” by a tax haven bank back to the parent corporation, possibly at high interest rates. The money is repatriated tax free, the interest is a domestic tax deductible business expense and with prior agreement most of the interest paid to the off-shore bank can be credited to the off-shore account, or indeed “skimmed” ala Enron, by the corporate management. [Performance bonus? Profit sharing?]

Of course this is highly illegal, but only if you get caught, and it is possible for Corporation “A” (and their off-shore bank) to lend to Corporation B, and corporation B ( and their [different] off-shore bank to lend to corporation A, thus everything appears to be at “arms length.”

Of course Option B is to have a national tax policy that is not so punitive. The USA has among the highest (if not the highest) corporate tax rate in the industrialized world.

Why should companies like Apple or IBM, who sell most of their products & services outside the USA, be expected to bring those international profits back to the USA (and the 40% higher-than-average corporate tax rate)?

I suggested that scheme to General Electric back in the early ’90’s when I was a share holder.

“Stock buy-backs are the vehicle of choice as the buy-back qualifies for capital gains tax treatment, rather than a dividend taxed as earned income.”

Call this sanctioned fraud exactly what it is: fascism.

“Call this sanctioned fraud exactly what it is: fascism.”

What absolute garbage.

Huh? Do you even know what fascism is?

The SEC is apparently close to useless.

There is a great scene in The Big Short where an SEC regulator is bedded by the Goldman Sachs grifter she’s supposed to be overseeing because she wants a job with the Vampire Squid. Very apropos of the relationship between the singularly worthless SEC and the financial firms it’s supposed to be regulating.

Michael

It undoubtedly comes as a huge surprise to you that the SEC is NOT ACTUALLY in charge of how companies run their business (they are only responsible for accurate GAAP reporting.

Frankly, 95% of investors cant’t read a financial statement to begin with, but I would agree that any “adjusted” earnings should be preceded by a statement of GAAP earnings.

Every sizable company in the world has “non-recurring” or ‘extraordinary expenses” that, if excluded, make “adjusted” earnings look better…if you’re stupid enough to fall for this.

I personally can say the above is true and saw GE “cook the books” before each earnings release with a team of 100’s of accountants. I did their new billing system as a Systems Analyst and they were billing a off-shore paper company at different rates than other regular companies. I asked the simple question of what was their billing address and it took weeks to get a firm answer, and it wound up being a P.O. Box number, off-shore, of course, that didn’t exist, and was told this was internal accounting purposes only – LOL

Not surprising. I remember Immelt saying to a CNBC talking head a few years ago that we “give the analysts the earnings estimates “.

GE has a $300 billion balance sheet and yet it can give analysts their estimate.

Berkshire Hathaway is another monstrosity of a balance sheet that has never “seen no evil, nor done no evil.” Wink. Wink.

As for Jamie Dimon. He’ll tell you that JPM’S fast approaching $3 trillion Balance sheet is as robust and pure as the driven snow.

akiddy1,

Yep it’s true, back when Jack Welsh was king. Worked with a kid just got a Masters Degree in accounting, who argued their Debits and Credits weren’t being reported correctly.

He was told this is the “GE Way”, – get used to it or walk, and remember the accounting people working feverishly to make figures look good, 24/7

JPM and cohorts drip with sleaziness.

There will be a horrible reckoning one day by another default like Bear Stearns, a chain reaction of credit defaults, margin calls, derivative crashes, like we never seen before –Oh yea don’t forget Bitcoin stuff – LOL

Bear Stearns was the investment banker for GE, this was when GE owned NBC. This is why nobody had a clue what was really going on at either firm. All those “independent” journalist talking up their books.

With the implementation of “block-chain” we can now have an economic collapse in a matter of minutes.

D B Cooper

There is no such thing as the “real, accurate and true” cost of anything in a corporation.

Different way of reporting product cars (absorption accounting, ABC accounting, marginal variable accounting, etc, etc) all have their place.

You, an IT dude, have self-admitted seeing “cooking of the books” – implying illegal, immoral & unethical behavior. Did you report this to the SEC?

Just exactly what is your considered opinion of the “one true accurate & correct” way in which to calculate internal transfer cost accounting?

May I suggest a new metric, namely Net Taxable Earnings per Share [NTEPS].

‘Murica, the land of the fraudsters and the foolish and the willingly stupid or gullible.

I finally understood what the “American Dream” truly means.

And an F150 or similar cowboy truck for an office worker; opioids from Jamal on the street or Dr Patel or Dr Chow; hooters; 64 oz soda and the king of all – a credit card ; and no universal health care.

George Carlin cracked the code on the American Dream years ago.

https://www.youtube.com/watch?v=-14SllPPLxY

Here is one very similar…George Carlin was ahead of his time..

https://www.youtube.com/watch?v=i5dBZDSSky0

In that video, the point is that Americans are too uneducated to know.

In this video, the point is that Americans do not want to know, to face reality:

https://youtu.be/Sed9R2k4LgQ?t=2m23s

Both true.

I run my own dashboard of data for every stock I own and all I look at is “owner earnings” (a stricter version of Free Cash Flow) and Enterprising Earnings (money spend on intangibles like R&D and Advertising for growth).

I feel completely free to ignore the metrics posted by these companies in their official versions. Coca Cola, etc. show up very different EPS numbers to Owner Earnings.

IdahoPotato

As long as you are one of the 3-5% of investors what can read financial statements & dissect them for a more sophisticated understanding – go for it.

If you’re one of the mob who goes for EBTIDA because you’re “too cool for school”, you probably think Uber has actually made an “adjusted”profit.

I’m thinking the opposite of this ETF. In fact I have been making money buying these retailers. They are oversold.

I think you posted this comment under the wrong article. It should be under this article…

https://wolfstreet.com/2017/11/16/etf-to-bet-on-brick-and-mortar-meltdown-emty/

If you would like, you can repost the same comment under the correct article, and after you do this, I’ll delete this one here to keep things clean. Thanks.

Excellent article, as usual. It would have been interesting to include (or have in a follow-on article) what the current market P/Es would be based on GAAP earnings. Ratios such as the CAPE are, I believe, developed on historic earnings, which would have been GAAP based. Would it be that current CAPE, which is high, would be astronomically high were we to use GAAP earnings?

Discouraged

It is my understanding that all stock exchange reported P/E numbers are, indeed, GAAP

EPS and PE ratios that you get when you look up individual companies on Yahoo, MarketWatch, etc. are based on GAAP.

But FactSet, for example, uses adjusted earnings as base for its market metrics, such as the EPS, or the aggregate EPS for the S&P 500 companies, etc. I know because I asked them, because I use their data and charts from time to time.

Never mind last comment, it is covered in ZeroHedge.

Many hit on the chinese state for the fairy story Economic data it regularly releases.

Yet this non GAAP BS that the American Corporates regularly pull in their a reports make the CCP look innocent. That in itself is a serious achievement not to be claimed.

The SEC needs to go to Congress and tell them. “Give us teeth to deal with this non GAAP reporting BS,or wind us up as in the currently situation we are almost worthless”. Nice foolish non American dream that.

They will have to cut costs. One is real estate costs, the other is liquidate inventory which is the main trigger for a recession.

So the question becomes “does prominently featuring non-GAAP earnings have any net effect on share price?”. If it enhances it, then why not? Isn’t that what the Free Market is all about?

It didn’t help GE which is rapidly swirling down the crapper.

Plainly put GE as a whole is too healthy to crash and burn: it’s the same thing as in 2008.

The company as a whole had no big issues: it was the financial division which was to be put out of its misery, but to do so would have required shareholders to eat their losses through reduced or no dividends for a few years. And that would not fly with Jeff Immelt who managed to have several people at the US Treasury running around with their hair on fire. One of the most shameful shows I’ve seen in my life, which says quite a lot.

But this doesn’t mean GE hasn’t got some worrying issues.

GE owns the largest commercial airline leasing company in the world, GE Capital Aviation Services (GECAS).

Traditionally GECAS has owned only aircraft with GE engines, and this was fair enough and given the size of GECAS fleet it meant a lot of work for one GE’s core divisions.

But recently GECAS started ordering and buying aircraft engined by GE’s direct competitors such as Rolls-Royce, Pratt & Whitney and IAE (a joint venture between P&W, MTU and a consortium of Japanese turbine manufacturers) .

A frankly incomprehensible decision, especially given how heated the competition in commercial aviation is getting: Rolls-Royce didn’t get an exclusive with Airbus for the A350 engines just by asking very nicely. It’s brutal out there, and with the Chinese ready to enter the fray in force it will become even more so.

Mercifully it seems China is directing all of her considerable retro-engineering and designing might into military engines, leaving GE, P&W and the rest of the gang some breathing room.

For how long remains to be seen.

Having worked for GE, I would share the following observations…

Their ‘operating rhythm’ is beyond lean, meaning that they have perfected the art of leaning-out their businesses to the point where they’re very brittle. Each quarter, with no exception, we were given a ‘task’ to shore up the corporate numbers, so what we reported would look healthy. This takes an extraordinary toll on the business, and makes it just about impossible to grow organically. So they acquire their competitors. This gives them their much-needed synergies, as they hollow out those new acquisitions to run at the same ‘operating rhythm’ as the core GE business. And so the machine keeps running. As long as they can continue to acquire, they can continue to come up with the quarterly numbers (plus task) to feed the beast…

If they ever (are forced to) stop acquiring, the brittle, hollowed-out beast will keel over.

It’s all part of the Totalitarian Oligarchy we live in. Everything false and completely fabricated to protect the War Party Of The Rich.

Keep voting billionaire. Demopublican or Republicrat.

Yeah baby!

Marco

I assume your statement stands as so charged.

It’s a cold, hard reality that there is hardly ever any such thing as “the truth”.

The concept of taking a multi-billion-dollar corporation and reducing it to a two-decimal-place accurate earnings per share is simply ludicrous. The best you can do is track the same company’s financials (calculated more-or-less) the same way over a period of time.

Wolf,

Your analysis is the best summary of the ongoing deceit in earnings I’ve seen in a long time. Thanks.

– I read a story that GE Always manipulated their EPS in the 1990s. GE miraculously did beat EPS by one or two cents. People thought that GE Always sold a (small) part of their financial assets in order to beat those estimates.

– Did the readers of this thread notice the fact that GE has cut its dividend ? And the stock(-price) took a significant hit. Seems the earnings haven’t been that good lately. Another sign of a difficult US economy.

@W. Richter:

– Do you have an idea what the main reason is for these “adjusted earnings” of these companies ? Excluding write-offs ? …… ?

– GE: a subject for a new blogpost ?

Without stock buybacks and “adjusted” earnings, who knows what the true value of stocks would be. But this isn’t the kind of truth stock promoters in the media, financial industry and the Fed care to talk about. The world needs more Wolf Street and less Cramer. One thing we do know is, the higher stock prices go, the more they will fall when the next crisis hits, which will only amplify the effects of the crisis. But the artificial inflation of assets, followed by their inevitable crash, is now a fundamental quality of a worldwide economy run by central bank “planners.”

Corporate tax shoud be changed by calculating by 50% on GAAP earnings and 50% on adjusted earnings – that would quickly change the game. Some years later we would enjoy healthier balance sheets. But that’s not wanted.

Lobo

Mixing 1/2 gallon of the world’s best ice cream with 1/2 gallon of pure cow poop does not give you 1 gallon of anything resembling ice cream.

LOBO

And besides, corporate tax is never calculated on GAAP, or another made up earningIncome tax is calculated using RAG (Regulatory Accounting Guidelines) – the IRS makes and enforces the rules.

Someone should write the history of gadget earnings, in the late 90’s proforma earnings supposedly added 20% to the markets value. First I gave up on studying fundamentals, then I threw away my books on TA. It’s a simple fact of life, if you don’t understand what they are doing, stay out of the investment. (if everyone followed that advice no one would own a bank stock and the banks would be forced to regulate themselves)

Year to date the Generally Accepted Accounting Principals Dow has increased by 20%, while the non-GAAP Dow grew a little over 9%. Cynically expecting just the opposite.

I don’t know how you find time to do this research,Mr wolf……….but please don’t stop!

US corp margins are down 15% from the cycle highs of 10% down to 8.5% just as wages as a % of GDP start to rise and Fed hikes.

https://fred.stlouisfed.org/graph/?g=fOBe

Has been some internal weakness in things like leisure and retail sector for wages though recently.

https://www.frbatlanta.org/chcs/wage-growth-tracker.aspx?panel=1