But upward pressure on already crazy home prices persists.

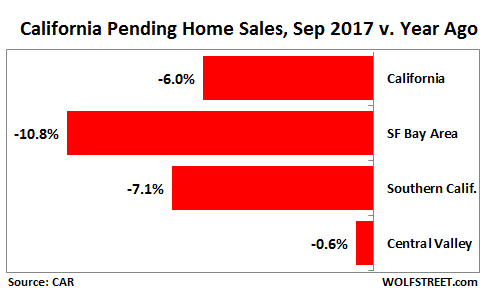

Pending home sales in California fell 6% in September compared to a year ago, the third month in a row of year-over-year declines, after having dropped 3.5% in August and 2.6% in July.

“Entering the fall home-buying season, the housing market momentum waned,” the California Association of Realtors said in its report. Brokers “reported slower open house traffic, and listing appointments and client presentations fell below positive territory in September.”

The report cited “continued housing inventory issues and affordability constraints,” as home prices have moved out of reach for many people, despite historically low mortgage rates. This “may have pushed the market to a tipping point.”

Pending home sales are an indication of what actual sales might look like over the next few months. They’re notoriously volatile. But in the San Francisco Bay Area, pending homes sales have been plunging in the double digits for months. And now Southern California is catching the cold.

In the San Francisco Bay Area, pending home sales plunged 10.8% year-over-year, after having plunged 11.6% in August, and 11.5% in July. It was the 12th month in a row of year-over-year declines. In the two counties that make up Silicon Valley, San Mateo and Santa Clara, pending sales plummeted respectively 22.4% and 23.5%!

In Southern California, pending home sales fell 7.1% year-over-year, after having fallen 3.8% in August. In July, they’d still inched up 1.4%. The counties with the sharpest declines were Los Angeles (-8%), San Diego (-11.5%), Riverside (-13.4%), and San Bernardino (-11.6%).

In the Central Valley region, pending home sales edged down 0.6% year-over-year, driven by the 16.8% plunge in Sacramento County.

Of the homes put under contract, 26% had had their listing price reduced before buyers got interested. And after that:

- 29% sold above asking price – at an average premium of 13%

- 28% sold below asking price – at an average discount of 15%

- 43% sold at asking price

Already, sales growth is in trouble. Earlier, CAR reported that actual sales in September had inched up 1.7% year-over-year for all California, but that sales of condos and townhouses had fallen 4.1%, that sales in the Bay Area had fallen 4.2%, and that sales in the Los Angeles metro had fallen 2.5%. The current pending home sales decline will continue to pressure actual sales downward over the next few months.

But upward pressure on prices persists: Home sales, though declining, are still outstripping new listings that are declining even faster – as “the supply of homes available for sale continued to drop.”

This has led to some crazy prices. In September, the median house price (not including condos) reached these levels:

No wonder that “declining housing affordability/inflated home prices” was the biggest concern of 44% of the brokers in the CAR survey, along with “rising interest rates.” At these prices, even slightly higher mortgage rates make a large difference for already over-stretched buyers.

The lack of homes for sale was cited by 35% of the brokers as their biggest concern.

So, as they say, it’s complicated. In these expensive areas, sky-high prices have moved homes out of reach for most homebuyers and thus strangle sales. At the same time, those sky-high prices are locking homeowners into their current homes that they bought a few years ago at much lower prices because they cannot afford the mortgage payments that would result from buying an equivalent or larger home in the same area.

And so the market is in a stage of slowing down, where many current homeowners cannot afford to move up or even sideways, where new buyers cannot afford the prices, and where prices are still propped up by a lack of supply because current homeowners are stuck and cannot put their homes on the market even if they’d like to move because they cannot afford the payments of that new home.

Here’s how our extraordinary asset price inflation is developing in all its beauty. Read… The US Cities with the Biggest Housing Bubbles

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf, the beauty of housing’s “comparable appraisal process”, all it takes is a few sellers or buyers within a large geographic area to reprice all house lower or higher.

It works great on the “stairway up”. But, “elevator down” is painful and spreads like a virus.

By the way, stratospheric prices that caused a massive slowdown in demand amidst rising rates are exactly the conditions circa 2006/07.

“By the way, stratospheric prices that caused a massive slowdown in demand amidst rising rates are exactly the conditions circa 2006/07.”

Agreed. Price will eventually follow volume. Although this cycle has been unbelievably stubborn for obvious reasons.

Another thing: if the Nasdaq rolls over, the above monthly housing numbers coming out of Digital Detroit will shock even the most bearish among us.

Nicely put,”Digital Detroit”,LOL

The only difference is, this time, will the Government treat residential real estate the same way it treated commercial real estate in 2008–that is, bail it out. And how will that work? After all, it’s easy to say, “If you have a master lessor, say on all your filings you are fully leased.” But how do you do that with residential units? Especially when everyone will know that no one is living in the units.

Of course, the next meltdown will be unlike any other, since we have–what?–quadrillions floating around in the dark pool.

Will we some day simply wake up to no jobs, no money, no assets? If so, exactly what day will that be? Same question which has been asked for the last eight years.

Ppp,

The foreign buyers and low interest rates get most of the press.

But there’s nothing I’d love more than to see the reits get punished badly. They’ve hurt average Americans and our housing costs terribly.

But there’s nothing I’d love more than to see the reits get punished badly. They’ve hurt average Americans and our housing costs terribly.

Agreed. The silver lining of the coming financial crash is that John Q Public might finally get pissed off enough to do what should’ve been done after 2008: end the Fed and jail the banksters, regulators, enforcers, and politicians responsible for causing the US and global financial crises.

“Will we some day simply wake up to no jobs, no money, no assets”

I’ve been living that dream for almost 2 decades now. There is no future in the USA.

Everyone should just move to CT it’s super cheap and getting cheaper. Prices at 15 year low.

prices are high, affordability is down.

democratization of credit for those who own the democracy……prices out those who don’t.

Housing Bubble 2.0 is *complicated*. We have tighter underwriting, lower interest rates, and less inventory than Housing Bubble 1.0.

Correct, and also 1.0 involved the chicken/egg issue of mass securitisation of junk loans (subject to no underwriting). I think that screwed massively with traditional supply/demand metrics.

This current run seems more “traditional bubble” in nature. Also feels overvalued of course.

Local factors – now as ever – would always be of highest importance.

It ends when:

Airbnb no longer works as a way to help with carrying costs either because of regulatory restraint or lack of travel demand.

The large investment pools that purchased single family housing in bulk find that the economics don’t work or finally take profits.

Personal economic situations deteriorate and result in forced selling.

A lot of non purpose lending against stock portfolios has been done. Even lending against non public (unicorn) shares. (I’m looking at you FRC) Some of that cash has ended up in real estate. Some of it reinvested in other unicorns.

I remember this happening in Housing Bubble 1. Mean and median went up as volume fell. If I recall correctly, it’s because volume at the high end is far more stable and tends to pull the price statistics up when volume at the low end finally starts to crash when it hits the affordability wall.

Could the slow down be from China’s new regulation on limiting their outflow of money for foreign investment? They were a major cause of these ridiculously house price bidding war since the housing crash.

Perhaps it’s that coupled with a loss of jobs in the Bay Area for the second straight month.

http://www.mercurynews.com/2017/10/20/san-jose-san-francisco-oakland-job-losses-hammer-bay-area-employers-slash-thousands-of-jobs/

RoseN – I don’t even tell people about my part-time job paying $16 an hour as a 1099 and getting to live in the warehouse, because invariably they’ll get this look of hope and desperation in their eyes and ask if “they” are hiring or if “they” need anyone else.

I was recently talking to a guy who’d apparently come out here from Iowa, and was staying in a hotel (he got off the light rail at the Gish station, where there’s a huge cheap-ish hotel) hoping to get a computer job out here. I guess he’d saved up money shucking corn or whatever they do in Iowa, taught himself some Pascal and FORTRAN and was hoping to get a job out here. I really hope he’s successful, but I told him about Labor Ready and places like that, because that’s about the only work that’s easy to get out here. Otherwise you really have to know someone.

“or whatever they do in Iowa”. Oh, please. There used to be a saying that was repeated ad nauseam encouraging young Iowan graduates to go to golden CA, “Tell them you’re from Iowa, you’ll be hired on the spot.” He must be the lone Iowan venturing to CA—NO ONE from Iowa goes there anymore. And I mean no one. They’d rather see it fall into the ocean than partake in the sh/tshow it’s become.

P.S. “Who made first computer? An Iowa State professor.”

http://www.dailyherald.com/article/20110823/news/708239874/

oh, the irony!

@RoseN

Thanks for the link. The article and the comments doesn’t mention if the job losses could be attributed to slight changes in the visa requirements. Could it be that too?

I wish we could get some numbers on non-resident Chinese investors. All I have are anecdotal tidbits from a couple of brokers. These homes are still aggressively marketed in China by all the major brokerage firms. They have all set up operations in China. And they probably have a good sense of the trends, but they’re not saying.

A San Francisco realtor friend told me the Chinese buyers left a while ago. But it’s hard to know what to believe.

I see that a San Francisco house sold for almost 1 million over asking. The buyer’s agent states that she has 15 years of experience working with Canadian developers, so perhaps wealthy Canadians bought this house. It’s safe to assume that the Bay Area has world-wide appeal, and there’s a lot of wealthy people on the planet.

http://www.businessinsider.com/san-francisco-home-sells-million-over-asking-2017-10

Anecdotally, it’s a wild ride if you look at individual homes.

For example, this is a home in my neighborhood – I walk by it every day:

– First listed in October 2016. At the time, they sent out a glossy flyer to promote it (I got one too).

– Listing removed in Dec 2016.

– Relisted in January 2017 with a $411,000 price cut (decimal in correct place).

– May 2017, price is cut another $613,000…

– In July, listing was pulled.

In other words, during the year when they’ve been trying to sell this home, the price has been cut by $1.02 million, and no one bought. This may go through a few more iterations before it sells. If it sells, none of the prior listing prices and price cuts and relistings, will make it into the CAR stats.

There are a lot of sellers at the higher end that go trough this process, trying to find the maximum price, aiming high and having to lower their sights.

I’ve written about that phenomenon at the super high end and called it “aspirational pricing” (homes in the $30+ million range). This place in my neighborhood doesn’t fit into that category, but it’s priced way above the median for SF, and it’s also much larger than median.

“There’s a lot of wealthy people on the planet” absolutely,the problem is,most of them are fairly smart and they will switch their investing decisions in a New York minute. if they decide RE has played out and the new thing is Treasuries,Gold,Oil or whatever,that’s where the money goes. Capital will be “re allocated” and in this digital new world that can happen fast. will they sell at a loss? sure,it’s a tax write off.

Overseas all-cash Chinese at this point are less than 5% of all buyers.

Point here is if you cannot put 20% down and are driving (to-me) unsafe cars with little kids and buying million dollar shacks with no guarantees to be able to enter and work in this country (H1B) – the market is closer to an inflection point.

Also – Wolf: I have anecdotal experience of house prices rising 100K in roughly two months in Fremont – talk insane!

This is hypothetical and sorry Wolf its sort of off topic, perhaps they figured out laundering money through real estate is not profitable anymore. Hence recent exponential growth of Bitcoin value for laundering money?

Apparently there are a LOT of Bitcoin-type fictional currencies, and if they work to launder drug/corporate crime/human trafficking/etc money then they work … I guess you’d just have to hold the fictional currency long enough to be able to say, “See? I ‘invested’ in BubbleGumCoin and that’s how I got this pile of cash”.

I really wish our government would do something to address these foreign investors but at this point I think I have a better chance riding a unicorn than seeing this come to fruition. My only other wish is for this market, especially in California to crash harder than it did in 2008 so it can teach these greedy foreign investors a lesson or perhaps their own chinese bubble will burn and crash as well…given how things are looking though, perhaps another wiseful thinking..

Title companies might have this data—they do a lot of reporting. Maybe one of your broker friends could introduce you.

Well deserved, Silicon Valley has no one to blame.

Strangely enough here in Denver a plethora of For Sale signs are popping up on homes across the city ( in all price ranges ) despite us having firmly entered into our traditional real estate sales slump ( October – February ) More in fact than appeared the entire summer !

Hmmm ..

The plethora of For Sale signs. I remember that happening here in Tucson during Q3 2005. The first obvious sign that our Housing Bubble 1.0 was over.

2 year note at 1.60% looks PHAT too?

One way to tell the suckers is to observe who shows up at open houses in Alameda county.

I would guess 80%+ are working professionals on H1B visa who are killing themselves to buy the house.

Most of them are from India. I can tell because I’m Indian origin. I can also tell that they have been in the country for less than 5 years and it is easy to observe that the drive 20 to $30,000 cars. They are buying million dollar houses while slapping their children would be unsafe Toyota Corollas or Honda Civics.

I have also spoken to a lot of agents and according to them most offers are with 10% down payment with another loan covering 10% and the remaining 80% mortgage.

Now you juxtapose these facts with the following 2;

1. A lot of these Visa holders are working for unicorns or.com apps that have a negative cash flow and don’t make any money

2. Trump is making it harder even to extend this as previously approved for the same job something that came out yesterday

What this leads to is just a little toppling of the tech sector which one are under a lot of these homeowners unable to find a job on the Visa and therefore starting to Cripple the Home sector.

I get no joy in seeing the misery that is going to befall this hard working lot.

Also, This would also reduce the pool of homebuyers who would want to buy homes from the older generation.

Very very highly paid Apple Google Facebook employees live in Santa Clara County or San Mateo County more or less immune to these pressures.

Could you replace the fake Spanish from the Google bot with some real handmade English? (The sentence that starts with “I have also spoken”). I’ll insert the fixed sentence.

The H1B visa couples from India are buying houses from Taco Tuesday Baby Boomers in a lot of cases.

Fremont is now a majority Asian city.

As a renter in Sacramento this just happened to me. Old landlord sold us and all five of our neighbors (good timing if you ask me), then we got picked up by a Indian guy who works at Intel and his wife. He said he paid twice the previous price for this place and this and three other houses are his “retirement”. I get the impression that everyone around him are pushing RE as THE investment. I’d feel sorry for him is he hadn’t raised the rent to $1750, though he claims that isn’t even enough to cover the mortgage and taxes.

I’d love to see these greedy bastards burn… The best of this story is that even a 10% decline in prices and rents will make him bleed money…

If the tide changes.. Sac will fall even more that any Bay Area nabe…

@truth always :”2. Trump is making it harder even to extend this as previously approved for the same job something that came out yesterday”

This is the hottest topic this week because it catches items in the initial visa processes that may have been missed such as fake ‘you name it’ and puts the proof on the visa holder and not the employer.

I have a question about Bay area real estate. Both houses and rent seem to be much cheaper in the area around Vallejo city in comparison to Peninsula or South Bay. I’ve been to Vallejo city only once and it doesn’t seem to be a bad city. So, how come the prices are much cheaper. I just want to understand why real estate price is cheaper in that area.

You’re trying to compare apples and oranges. They’re very different – including the commute from Vallejo to the Peninsula and the South Bay and a million other things.

But plenty of people make that trek every day.

My friend, Vallejo and all the straits communities are in what is known as Cancer Corridor. It’s because of the refineries. You don’t see them emit this junk because they do it at night. But Cancer Corridor has hella health problems. Don’t EVER live there. I mean Richmond, Pacheco, Vallejo, and all the way up including Clayton. Just stay OUT of that corridor.

And the crime in Vallejo and Richmond is the reasons why these are cheaper places to live. Look at Benicia, in between vallejo and pittsburg, which is way more expensive because of the small town feel and its safer.

Jordan – there are places that are just far enough away that the commute is just too long and they’re a lot cheaper. Like Stockton, or Salinas.

Vallejo also has long been noted for things like stupendously high crime, and the city went bankrupt not long ago.

I’ve been through there and it’s a dump.

Vallejo has some hard areas. I have friends that live around Broadway and Tuolumne St. It’s not uncommon to hear gunshots and night and more than once, on the way to my car, I’ve run into police who are pursuing someone on foot. As a bedroom community for the tech nexus, it definitely is not Pleasanton or Walnut Creek.

Thanks for all the info. I didn’t think that commute alone can be the reason since some areas in the peninsula have the same problem since if you live there, then in most cases you have to travel to San Francisco, or areas in Santa Clara county for work.

But couple the long commute with crime, and the risks from refinery air pollution, and now the real estate in Vallejo area seems too expensive.

If rates go higher its a win, because buyers will rush to get the deal done. If you believe in the efficacy of long term low rates buy now while rates are up and REFI later when they come down. Also some sellers may be taking property off the market, I mean LET IT RIDE! Sell my house today for 1M when it might be 2M a year from now? Rent it to family or something.

This is a bull market in housing, BUY THE DIP

I saw the same story in 2007 as well.. Usually lower transactions, higher inventory is precursor to drop in price… it all depends on cheap money and general economy…. let’s see

“rent it to a family or something”. Thanks for the chuckle,needed one today but you surely forgot to put the sarc disclaimer on your post? funny stuff though!

If only there was a way–any way–to increase supply of homes to move into. Perhaps homes that people don’t already occupy, maybe? Gee, I’m stumped!

Watch the supply surge, as it always does, when prices head south and the selling starts. Housing markets become illiquid when prices drop. No one wants to buy, and a lot of people want to — or have to — sell. It’s the opposite of the current condition. This includes a lot of investors that are now riding the market and that then want to sell when they can’t.

In short, what we will see is the housing sitting empty and the people sitting homeless. Homeless advocates love this, because if the condition persists and everything goes bankrupt, the housing goes to a local government and just goes to public housing.

I remember when a social worker told me that the trendy “urban infill” movement would mean one thing: massive urban slums. I didn’t understand the connection.

I do now!

If the collapse is massive enough (and this is on the legal side), we will see a rise in the Constitutional level of scrutiny for housing, which now only enjoys minimum scrutiny because of Lindsey v. Normet. N.B.: minimum scrutiny for housing is the only thing which permits housing evictions.

But Lindsey is nearly fifty years old and remember its factual bases:

1. housing is not an unchanging fact of human experience

2. fairness is not in fact a component of the property indicium of housing.

Now read Lindsey again, and note what the Court is assuming and arguing in deciding that housing only enjoys minimum scrutiny.

What is the relevance of the level of scrutiny? Facts which enjoy only minimum scrutiny are not individually enforceable rights (West Coast Hotel v. Parrish, U.S. v. Carolene Products).

Facts which enjoy a higher level of scrutiny (intermediate or strict), are individually enforceable rights. Ask any lawyer or judge.

Now read online, the U.S. Government’s Statement of Interest in the Boise homelessness case–which supersedes Number 1 above–and the Affirmatively Furthering Fair Housing Rule, which supersedes Number 2. No one, not even Trump, is about to reverse the AFFHR because, although they hate it (public housing in Walnut Creek??–NEVER!!), there is no arguing with its compelling factual basis. Read it thoroughly and you will agree. Put your NIMBYism aside.

If the level of scrutiny for housing is ever raised, you will never see another housing eviction again. Go over the levels of scrutiny (you will find a discussion on Wikipedia), and then tell me why that will be so. It will be so.

A true collapse in the economy would see the level rise, because there will have to be some legal principle intervening between foreclosure or unlawful detainer and eviction. The Government will simply have to find a way to keep people in housing.

We’ve done it (for most people) on the principles of fear, voodoo economics, sentimentality and good ole American corruption.

But those will no longer serve in a real collapse.

By the way, the Court is lining up Carolene Products for overrule. One more Justice….

You just have to know where the bodies are buried in this AWFUL country.

The difference between property and housing is profound. You make the point, “have to sell” which means in parlance anything “margined”, which is any mortgaged property as well. I cannot take out a HELOC on vacant land. A general market event, when all assets lose value, like 2007 is all that is going to end this housing bubble and the stock market bubble will not end until counterparties no longer respect (bond) leverage. To the extent that physical gold cannot be margined, (just rehypothecated by large and corrupt institutions) that means it also is somewhat bulletproof in a general market downturn [if only for the ETF] ). That said, in such instance the price will fall and supply will disappear. So if you want gold (or vacant land) you should buy it now.

J Bank,

There are plenty of units for habitation. The term ‘shortage’ is being misused these days.

There is a shortage of affordable places to buy. There is not a shortage of living spaces. We don’t have 100’s of people going homeless each day.

Thank the reits, low interest rates, foreign investors, and domestic speculators for the lack of buying opportunities. But as Wolf says, if a downturn comes, get ready to see a huge supply appear like magic. All of the sudden, there won’t be a need to build hundreds of crap quality, pseudo luxury condos and apartments.

“We don’t have 100’s…” Yep in San Jose we have thousands.

The reason why the prices are still crazy is because it seems to be part of the selling strategy. You have a 29% chance of selling above asking price (even after lowering the price once) and a 43% chance of selling at asking price that was only lowered once.

Or it just seem that way. In a lot of cases houses prices actually get lowered more than once before they finally sell.

Because of that apparent 29% chance of selling the house well, the market is inflated. But the truth is that since houses prices get lowered more than once, the chances of getting that “increased profit” are actually quite low. Anyone here cares to do the math in cases were a house price has been lowered at least two times? Because that seems to be the norm from what I have read.

If I lived in SF, my mid-west 2400 sq ft Victorian knockoff home with over improved kitchen, private back yard, wood floors throughout, cat6 wired, and more would be worth several millions. Here, it’s an ordinary house worth a fairly low amount. To me, it’s an easily paid-for retirement refuge.

I just don’t get goofy California home prices. When I watch House Hunters, I am astonished at the hovels <1000 sq ft and slightly better, that cost $600 thousand and up. Often way up. Nuts. Why do people allow themselves to be abused like that? Is it a California thing the rest of us would not understand? I'm seriously glad California is out in the wilderness from here as having the oddities who live there call the shots for the rest of us would be a nightmare for the other 49 states. Weirdness seems institutionalized.

“I’m seriously glad California is out in the wilderness from here as having the oddities who live there call the shots for the rest of us would be a nightmare for the other 49 states. Weirdness seems institutionalized.”

Mark Zuckerberg and Tim Cook live there. In some ways it does feel like they call the shots for the other 49 states.

I get your point and don’t disagree.

Fortunately I don’t use any Apple products and only have a Facebook account because I wrote a how-to on-line book and thought it would be good to have a Facebook reference. I don’t remember the password to it and don’t want to expend the effort to look it up in order to delete it. Probably someday.

Without Steve Jobs, Apple is a monolith operating under inertia today. Facebook is a Google wannabee. Apple is pre-IBM without the consulting firm division at this time (expect it in a couple of years). Apple has introduced no innovation in about a decade. Consulting is their only remaining refuge.

Neither will be remembered for much in a couple of years except for whatever their PR supporters can think up to push.

you can never delete you facebook account…

Memento is right,you can never delete your FB account,you will pay your taxes and you will die,so there…

In Soviet America, Facebook delete you!!!

Househunters? Just an infomercial. People buy for $800k walk in and say “Its all gotta go!” I love when the Realtor says “What do you want to offer? FFS! What is the Relator’s exact purpose there? And the Yanqui buyers abroad, particularly in Mexico, drop hundreds of thousands of dollars like its nothing. Mexico is so risky its not funny… an $800k condo in southern mexico is INSANITY! No arguments, I have done real estate in Mexico and I have seen gringos get fleeced big-time. At least in EU property rights are upheld. Mexico… crazy!

http://www.sfgate.com/bayarea/article/Bay-Area-residents-moving-to-Sacramento-relocating-11243395.php

Potentially not utterly hopeless. But only for the adventurous? Financial flagellation for the rest?

We call them bay area refugees. I hear more people complaining about them now, though I can hardly blame them for moving, you know, literally anywhere else.

Number 1 excuse of realtors for anything that happens in real estate market: “lack of inventory.” Even if there are a million properties listed, realtors will say “lack of inventory.”

They were saying the exact same thing in Toronto, and they are still saying it. And of course, let’s see what happens in Toronto as rates keep going up.

In China, the government has been caught buying homes to support the housing market: http://www.zerohedge.com/news/2017-10-21/unprecedented-housing-bailout-revealed-china-property-sales-drop-first-time-30-month.

Don’t worry, the Fed will do the same in the future.

The Fed will not and cannot buy homes outright. But it doesn’t need to either. It buys mortgage-backed securities, that are government guaranteed, and thus the Fed and the government are helping to push down mortgage rates, which is a huge subsidy for homeowners. And the Fed, in 2011, made cheap money and a lot of encouragement available to private equity firms to buy up single-family homes out of foreclosure. These PE firms then bought several hundred thousand homes and now rent them out. Other investors have jumped in behind them. The point is: the Fed doesn’t have to buy homes, it can get finance firms to do that with the nearly free money it makes available to them.

Like to keep my comments upbeat, but ‘the Fed and the government are helping to push down mortgage rates, which is a huge subsidy for homeowners’-??

That is my sore spot along with mortgage interest tax deduction bashing.

They’ve taken away every other place to get a positive return on my investment except the stock market (possibly lose it all), and the Fed and the government are doing me a big favor with a huge subsidy?

Homeowners are sinking a lot of down payment, principal, interest, maintenance, improvements and personal labor into their homes. And when pensions collapse they’ll know right where to send the bill for my portion of the bailout.

There are plenty of injustices in the banking and gov’t worlds that both residential homeowners and renters can get worked-up about without pitting us against each other.

Thanks that was therapeutic.

I get your point, but I think Wolf was implying the homeowner subsidy is a boon for investors, not residential owners or renters?

I dont think prices will come down for the forseable future. Any reasonable person with money would buy a house. As long as trillions printed by the FED are not put out of circulation, that money will flow somewhere.

So far, it has been flowing to stock market by the big guys and to real estate by somewhat smaller guys with less money.

By the time QEn is sterilized, (maybe in 10 years, maybe never) inflation would catch up with evth else and RE prices will stagnate at much higher prices.

Imagine you have 3million in your account, where are you going to invest it to get some return and protection from inflation? When you answer that question, you know why RE is so expensive.

This is an unreasonable comment. The Fed is not money in anyone’s account. The working stiff still need to pay their mortgages.

I don’t see corporate investors buying houses in the SF Bay area – why would they if they can get better returns elsewhere.

The trillions are chasing stocks , bitcoins etc.

But stocks and bitcoin are volatile. To make long term good returns you have to be a player every day. RE doesn’t disappear or require that kind of attention, even if it suffers bubbles.

Watch for a big surge in inventory. Until then, the party will likely stumble onward. Underwriting is still responsible and interest rates are very low. This will probably take the more traditional problem to bring down the realestate market, a recession.

I don’t understand what is behind this housing bubble. A basic 3 bedroom townhouse in my San Mateo neighborhood sold for 350k over the asking price of 1,000,000 on the FIRST day. No yard front or back.

At least subprime explained most of the last one. Where is the “money” coming from this time? PE? Tech? Satan?

FYI: 40 Barneson Street San Mateo unit C

Let me explain.

Let’s simplify the model into 3 group of people, W2 buyer, Rent seekers and true business people.

The W2 trade labore for money and pay living expenses.

Rent seeker pool money from markets and take control of assets and seek rent out of W2.

Business people pool money and start business and hire W2 folks.

The FED is printing under the name of helping business people since they pool money and low rates help them to pool money, therefore, more business.

The rent seekers also pool money. Since the W2 do not know how to pull money, they’re buying power stuck. So the rent seekers pool lots of money, raise the house prices up, compete out W2 buyers and make them into renters, then they raise the rent to squeeze maximum out of the W2 renters.

What you saw is either a rent seeker pooled money to compete out W2 buyer or a W2 finally taps out and risk 30 years of labore obligation to compete out rent seekers in the hope of rising home prices and off load it to other W2 suckers later on.

Got it?

If you keep thinking about W2 buying power, it makes no sense. But if you start to think about pooling money at low rates and seeking rent out of W2 folks, you will start to understand.

My reply is below, on the wrong post

This weekend in Melbourne there are 1700 houses up for auction. That number is a record.

Clearance rates should be in the mid 70% area for a very successful result. Less than 70% and the market is in trouble.

Update us on the auction results when they’re available. Thanks.

“What you saw is either a rent seeker pooled money to compete out W2 buyer or a W2 finally taps out and risk 30 years of labore obligation to compete out rent seekers in the hope of rising home prices and off load it to other W2 suckers later on.

Got it?”

Er, no. You are essentially saying the house was sold to a rent seeker or a wage slave. Okay, but my question was, without subprimes, how many “W2s” can rent seekers hope to exploit? I’ve lived here in silicon valley nearly all my life and I knew during the last bubble that people could not afford the houses. What I didn’t bother to find out was how they were getting in to them. Now we know.

Maybe there are, in fact, enough well-off “suckers” to account for the current bubble.

My question stands.

Sorry, this comment was meant for JZ

The buying power of rent seekers is NOT constrained by their salary, it is by the loans they could pool under what interest. So if the house was sold to a rent seeker, then there is nothing strange about it, although you judge the house to be out-of-reach based on W2 income.

Once W2 is priced out as buyer, they pay rent. W2 do not need subprime mortgages to pay rent. They simply pay rent out of their salary. That’s how rent seekers seek rent. Rent seekers do not need to off load to W2 buyers at a capital gain. All they need is the rent cover the interest on the money they pooled, so called positive carry.

Of course, there are W2s that is way in over their head and take the risk of taking on loans based on their W2 income that they may lose almost for sure in the next 30 years during a down turn. People are bad at considering risk in the future.

My point being this, if the FED do not print money, business would have died and W2 will lose their salary. If the FED print, W2s will get a job but their salary will be squeezed by the rent seekers.

W2s are indeed constrained by salary in the loans they qualify for… unless they are liar loans. And obviously rent seekers can extract literal rents from RE, everyone knows that.

Your explanation for the current bubble is that investors are snapping up RE and driving up prices–do you have any statistics on that? I still don’t know who bought the condos on the other side of me for 1,500,000 although I suspect it was investors because of the timing–before the PRC stopped the flow of RMB–and foreign investors like new construction. The other townhouse that went last month for 350k over asking is old and I don’t know who/what bought it.

Incomes are flat in the bay area which is also getting hammered by job losses for the second straight month. It’s entirely possible that investors don’t care and are buying up anything nailed down. Nobody really knows.

In terms of investors — from large institutions to mom-and-pops operators — buying homes, the percentages are very large in certain markets. This article is from 2015, so very dated, but it gives you a feel. I may have a more recent one but couldn’t find it:

https://wolfstreet.com/2015/05/01/housing-bubble-2-investor-purchases-hit-record-small-investors-pile-in-as-smart-money-gets-out/

Thanks for the article Wolf. This is what I was after.

“Institutional investors may smell a rat in these prices. For them, the math of buying high and then renting the place to struggling consumers may no longer work. But for the intrepid small investors, including those that have learned the art of real estate investing from once again hot radio shows, it’s a debt-fueled, high-leverage paradise where only the sky is the limit.”

Besides the group of W2 buyer, and rent seekers, there are still other groups of money laundering (the condo will be churned out within 12 month for no or little gain) or even price insensitive buyers who simply do NOT care price and park their cash. For that specific condo, any of the 4 buyers could be it. All I am trying to point out is that if you judge the price as out of reach, you are only focusing on the W2 group. For the other 3 groups, low interest rates and QE increased their buying power a lot and that enslaves the W2 as renters.

The proceeds from my tiny, ratty 2br1ba home in Sunnyvale are buying a just remodeled 4br3ba home in one of the better neighborhoods in Union City. Both currently pending. It takes some work to figure out how to do it, even more work to get thru the process, but a homeowner in this Bay Area can make a move up without falling into debt prison.

There are still more buyers than sellers in this market, hence, the “inventory” line.

The price reductions are probably on properties that came to market way over priced to test, and are now settling into reality. A property that is appropriately priced will go fast.

That’s just the market reality right now.

With record low housing demand and skyrocketing inventory, the price reductions are ramping up. At least here in my little burg in the bay area.