In Chicago, rents are getting crushed.

An inconvenient math for housing is beginning to dog Chicago: The third largest city in the US has been losing population for years. Not huge numbers, but it adds up… In 2016, according to the Census estimate, the population dropped by about 9,000 people. Since 2014, the population has dropped by about 14,000 people. Chicago’s fiscal woes, junk credit rating, and the threat of bankruptcy hanging over it don’t help.

Since 2012, nearly 26,000 multifamily rental units have been completed in the city, according to Fannie Mae, which for 2017 sees “elevated volume of new supply, particularly in the Loop/River North/Gold Coast submarkets.” This does not include condos and single-family homes that were bought by investors and have reappeared on the rental market. Over the same five-year period, Chicago’s population has dropped by 9,000 people.

This has some effects on rents.

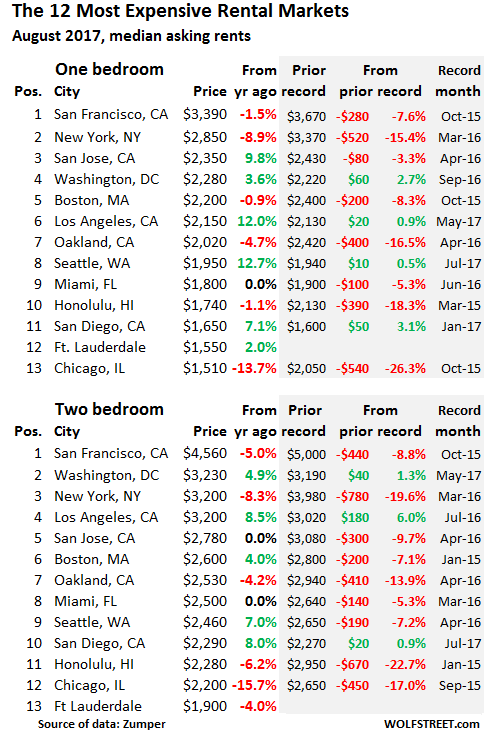

According to Zumper’s National Rent Report for August, the median asking rent in Chicago dropped by 13.7% year-over-year to $1,510 for a one-bedroom apartment, and by 15.7% to $2,200 for a two-bedroom. From their peaks in late 2015, asking rents have plunged 26% and 17% respectively.

These are asking rents in multifamily apartment buildings. Single-family houses or condos for rent are not included. And they do not include incentives, such as “one month free” or “two months free,” which effectively slash the rent for the first year by another 8% or 17%.

In January this year, Chicago was still in 8th place on the list of the 12 most expensive major rental markets. It has since been pushed down relentlessly – though other markets too have declined. And in August, Chicago was effectively pushed off the list into 13th place (so now my list of the top 12 has 13 entries).

This offers some relief for renters – though Chicago remains immensely expensive. But it’s not such a great thing for landlords whose costs are rising due to various fees and taxes the City has recently imposed to avoid falling into its fiscal sinkhole.

Other high-dollar luminaries where rents fell.

In San Francisco, the most expensive major rental market in the US, the median asking rent for a one-bedroom apartment dropped 1.5% year-over-year to $3,390 and is down 7.6% from the peak in October 2015. For a two-bedroom, the median asking rent dropped 5.0% year-over-year to $4,560 and is down 8.8% from the peak.

The last period of year-over-year declines in San Francisco ended in April 2010 after the Financial Crisis. This time, there is only a “Housing Crisis,” where the middle class can no longer afford to move into a modest apartment.

In New York City, the median asking rent for a one-bedroom dropped 8.9% year-over-year to $2,850. For two-bedrooms, it dropped 8.3%. Measured from the peak in March 2016, asking rents — not including incentives — have plunged 15% and 20%.

Given that plunge, New York City’s median asking rent for a two-bedroom has dropped below Washington DC to an ignominious third/fourth place, shared with Los Angeles, which also tells you how expensive DC and LA are becoming.

This table of the 12, well 13 now, most expensive major rental markets in the US shows median asking rents, their year-over-year changes, and (in the shaded areas) the prior record and the change since then:

The other double-digit losers were:

- In formerly red-hot Oakland, which received the San Francisco housing refugees, median one-bedroom and two-bedroom rents plunged 16% and 14% from their peak.

- And Honolulu, with an 18% and 23% plunge from the peak, nearly rivaling Chicago.

But nationwide, asking rents for both one and two-bedroom apartments were up 3.2% year-over-year, according to Zumper. How can this be, given the kind of red ink in the top 13 markets?

The boom in “mid-tier” rental markets.

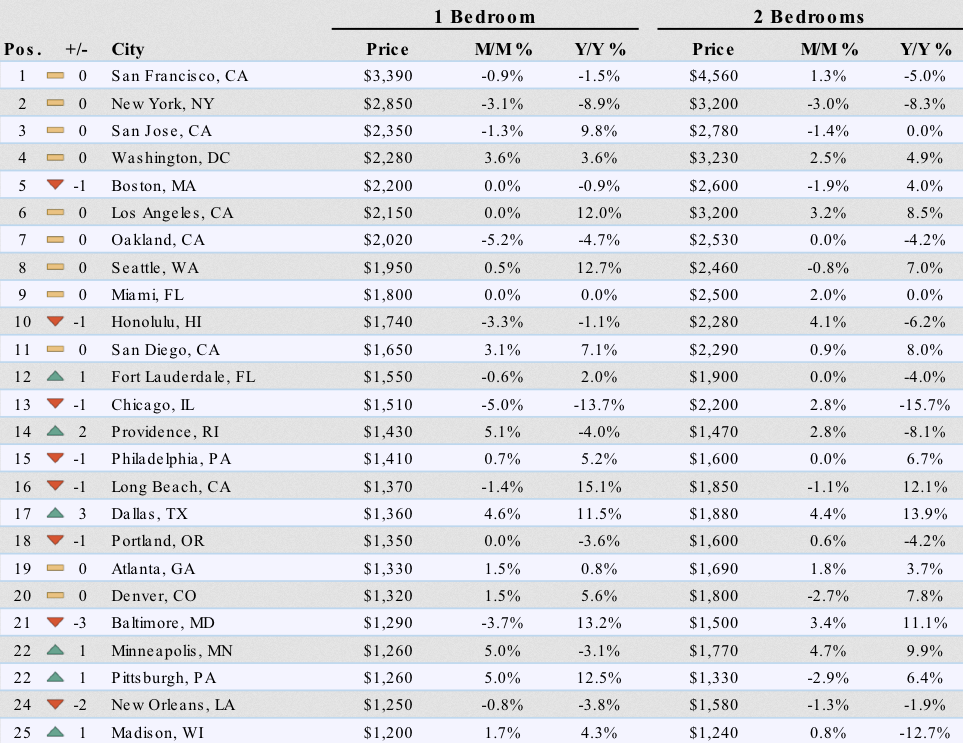

Asking rents are soaring in the high single digits and even in the double digits in many “mid-tier” markets – “mid-tier” in terms of the magnitude of the rent. Here are some of the mid-tier markets with double-digit year-over-year rent increases (one-bedroom and two-bedroom apartments):

- Long Beach, CA (+15.1% and +12.1%)

- Dallas, TX (+11.5% and 13.9%)

- Irving, TX (+10.2% and 13.1%)

- Sacramento, CA (+15.3% and +15.2%)

- Charlotte, NC (+15.3% and +11.2%)

- Durham, NC (+15.9% and +10.0%)

- Richmond VA (13.5% and +13.2%)

- Fort Worth, TX (13.5% and 11.7%)

Note the three cities in North Texas (Dallas, Irving, Fort Worth) on the list. Plano, north of Dallas, didn’t quite make the double-digit list with rent increases of 7.5% and 10.7% year-over-year. The North Texas housing market is hopping.

However, asking rents in some formerly hot mid-tier markets are now declining year-over-year, including Portland, OR (-3.6% and -4.2%) and Austin TX (-2.7% and – 2.8%).

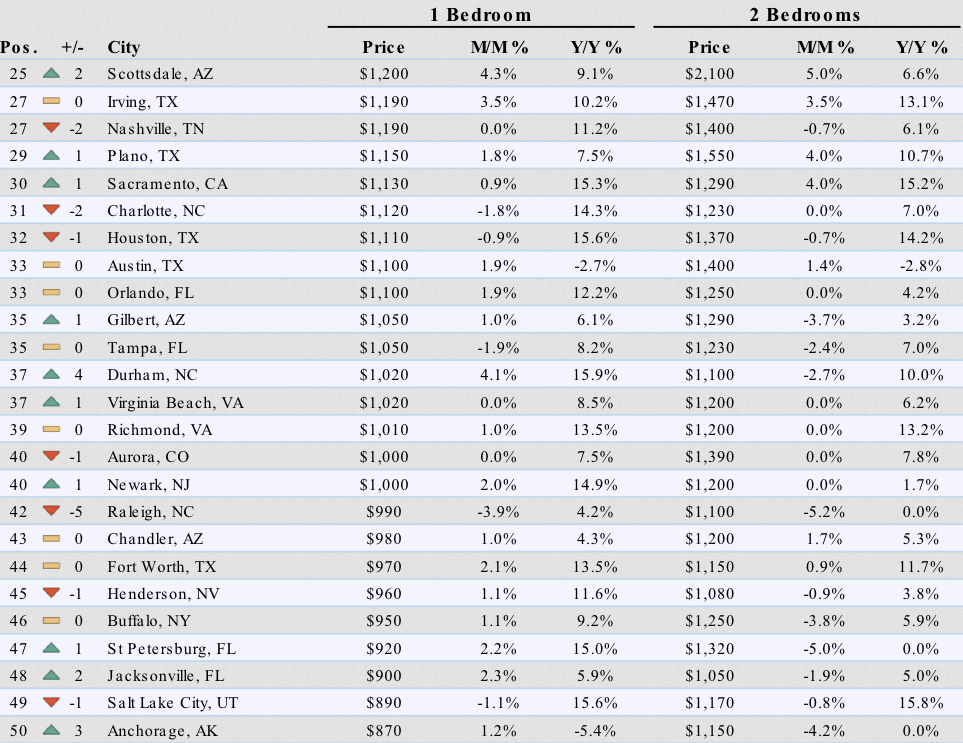

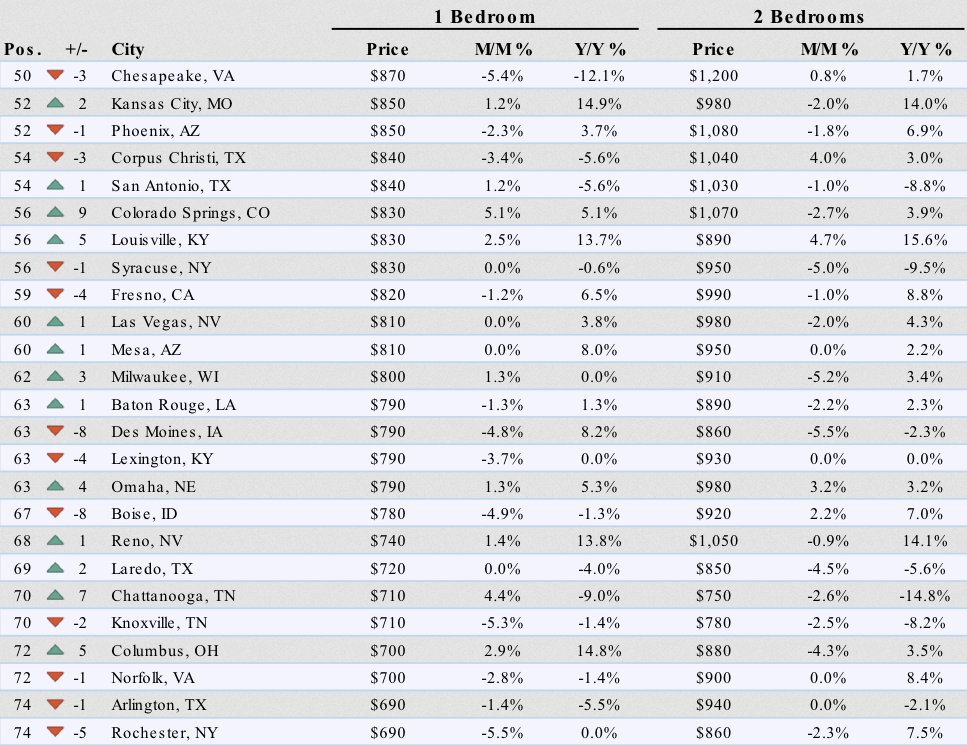

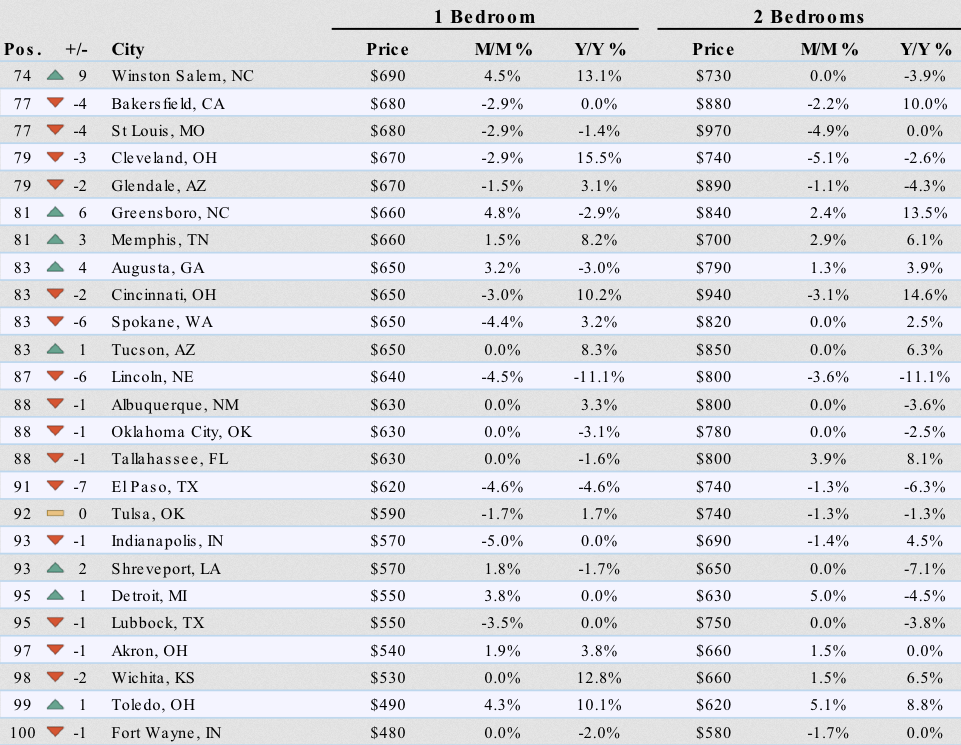

Below is Zumper’s list of the top 100 most expensive rental markets and price movements. Check out your city (click on table to enlarge).

In terms of homebuyers? Read… The US Cities with the Biggest Housing Bubbles

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Investors have been moving to mid tier cities as rents in the first tier cities have met resistance to growth. I have been hearing endless radio commercials for investing in Dallas and Augusta for the last couple of years. These markets will eventually reach their limits.

If you call eviction attorneys in LA area they will reveal without hesitation, the jump in eviction filings and inquiries from landlords the last two months.

The courts in LA county are so backed up a tenant can stay in their apt for 6 to 9 months without paying rent during the eviction process.

LA real estate is in a bubble. The LA economy is in a bubble.

I watch a turnkey re site for a year. They sell atlanta, memphis, other Indianapolis and now salt lake city props.

prices are to point where yield is only 6% if you pay all cash.

Looks like a bubble. Landlording has fat tail risk ( Tenant trashes and wipes out 5 years cash flow )

Hi Wolf,

I’m hoping you can do something with incomes as well so that we can get a sense of how much take home pay people have in relation to the mortgages and rents.

The problem with income figures is that they’re always old. Currently, we only them for 2015. The Census will come out with the 2016 estimates in September 2017. I’ll write about it then, as I did in the past, but data on monthly changes doesn’t exist.

Copy that. Thanks, Wolf.

If you remember at that time, I think it would be great to see estimates of take home pay, factoring roughly for Federal/FICA/State Taxes, against the mortgages and rents in these areas. I want to know just how well or how poorly people are getting by.

I might write a couple of articles on it, to look at it from different angles.

If I remember correctly, a form of net household income is included in the data. This would be income from all sources for this household, minus required payments such as taxes. So a measure of: “This is how much money this household can spend or save.”

In the last two houses we rented in south Florida, the rent for the last one was over 50% of take home pay and the one before that was just under 50%. Our last rent increase would have put us well over 55% and was the last straw.

I would like to point out, that our mega landlord asked us for proof of income when we moved there, so they were well aware that we couldn’t afford an increase. On top of that we had a decrease in income in the last few months, so moving was the only option. We are hardly unique in Florida where income is actually dropping. We were already living on a street with multiple generations packed into the houses.

In in Warsaw I have a gorgeous 900 sq ft apt in the best street in the city and my tenant an international attorney for a British law firm fights with me if I try to increase the rent 5 percent The situation in the US is unsustainable People deserve an affordable place to live I left the states partially because of the coat of living

You don’t understand Americans, getting hit with baseball bats is ok now, they have grown to accept it. Some expect it on a regular basis and turn and shrug their shoulders.

They will do nothing unless it interferers with the video game, cell phone, or Netflix. May be not even then actually.

We’ve been drilled and drilled since childhood that capitalism is best ism, so when we’re living in our cars, or in a warehouse with no running water like I do, or under an underpass, we still repeat the mantra: Capitalism is best ism.

I talk to many homeless people and they still believe this. And it’s not just Willie the Wino out there these days, it’s people who had jobs, were teachers, flower shop owners, electronics techs and engineers etc. In the US we’re all one layoff or medical emergency away from joining ’em under the underpass.

Alex, capitalism is the best ism. The prob is the US doesn’t have it. We live in a “mixed” economy (((fascist))). Capitalism does NOT include central banking, nor a country-wide regulatory system that is captured by multinational corporations, nor a tech sector established, funded and nurtured by the military/spooks, nor a food system controlled by chemical company giants. I could obviously go on. In no economic or political textbook even in this country will you ever find a definition of capitalism that includes these corruptions.

Your wino friends happen to be correct.

Marty,

Pure capitalism ends in monopoly — which results in as you said “a country-wide regulatory system that is captured by multinational corporations” and “a food system controlled by chemical company giants”. It’s not corruption as you state, it’s how capitalism works as it reaches the end-stage.

What I think you’re looking for is regulated capitalism. Something like fire. Fire is a great tool if you control it. Let it get out of control and you burn your house down.

But capitalism in its pure form always ends in monopoly power. You have to prevent that like you keep a fire under control.

I second the income dropping in Florida notion. In 2010 I made $75k/year in my STEM job. Now I make $56k/year, about the same as when I got my first job out of grad school in 2005. Every time a grant ends and I have to move on the offers get lower. Except for gasoline, everything costs 20-30% more than it did back then. Rent is getting stupidly expensive where I live (Tampa) but there are no houses under $400k unless you want to live in a neighborhood where you have to sleep cradling a 12-gauge with one eye open.

Last year when Sam Zell sold his stake in Florida rentals, I thought it was because he could see the incomes in Florida dropping. I think he got out just in time.

I graduated in 2000, and got a job in IT right away with a great salary because I was an A+ student. Since then I have kept learning non-stop to make myself more valuable. Guess what, my income has dropped by 50%.

Last year, I decided, I will learn the most difficult, but in demand skills so that I can at least make what I made in 2000. After learning a few extremely difficult technologies, a couple of weeks ago I started to look for a higher paying job; guess what? In interviews, they basically ask you to write programs that take hours to write in 10 minutes; if you can’t, you don’t pass. However, the whole IT industry is full of Indians; managers, developers all Indians. So, why would they ask me easier questions? They reserve easy interviews for their Indian cousins.

We are being discriminated against in our own countries. There is no way American kids fresh out of college would land an IT job unless he is a genius.

It’s a feedback loop; you have Indian managers all over who hire only Indians; these new Indians on the job keep learning, and get better while American kids will end up serving fries in Mickey Dee’s. These new Indians in turn become managers, and hire other new Indians. The story continues till there is not even one American kid who can write 2 lines of programs. Well done big business for selling out America.

R2D2: And yet no one asks how come these companies have 90%-95% Indian employees. If you have a company who hires only whites, or only men, then there will be dozens of law suits against the company. But a company has 95% Indian employees in the heart of the United States, and no one even question it.

By the way just to add, in my view, the tech job market in Bay Area, regardless of all the hype is so dead. It really reminds me of the job market in 2002.

The only company hiring seems to be Walmart for their online store. Google, Facebook, HP, etc., none of them are hiring.

As soon as Walmart posts one job, 30-40 Indian recruiters contact you and ask to submit your resume for the job. Anyone else is in market for a new software/IT development jobs in Bay Area who feels the same way?

R2D2,

Folks in IT don’t want to hear this (I work in IT) – but we are like the machinists in the 60s – life was/is good, but the future isn’t.

My recommendation is to stop chasing technology – which is a treadmill – and start developing other skills which compliment your technology skills.

As an example, I chose accounting – and am working IT doing a wide range of work – that requires a working knowledge of accounting. Think billing systems, financial reports, and the like. I like this path because every company has books and computers – but not necessarily the technology I chose to specialize in.

And if you try to do that in the big tech hubs dominated by Google, Apple, Amazon, and so forth – those are powerful interests concerned mostly with cheap labor – pack up and bail – because you can’t win there.

Try some place like Iowa that is off the beaten path a bit. Do your homework.

Regards,

Cooter

Harembe, R2D2, Davis, et. al. – I’m in San Jose and electronics techs are making something like $12 an hour. My employer had a circuit board house do some work for him, and the price he paid for the boards – all finicky surface-mount teeny parts – were so cheap I wonder if their assemblers were making closer to $10 an hour. It wasn’t a “run” big enough to set up the pick-and-place machine, so it was all hand done.

Electronics repair tech is my skill set, but like the old guys who couldn’t make the transition from tubes to transistors, I didn’t make the transition to surface-mount. Oh, I could have, I could have gotten kits that are surface-mount and built them for fun and learning on my own; at least in the 80s no one gave a shit if you had a soldering iron going (with good old traditional lead solder and rosin flux) in your apartment. But I didn’t. And now I don’t even regret it given how little people with that skillset are paid.

Now my interests are in woodworking, sign-making, you know, “crafts”. The things the “less-brainy” kids in high school were steered into Shop class to learn to do. I have a wooden thing in mind, another thing of carbon-fiber so that’s kinda modern, in mind, and then although I’ve done some signs in the past, I’ve gotten myself some real lettering brushes and paints, and am going to have a try at that. Sign-painting was good enough for Mohammad Ali’s dad.

It still dismays me to hear of you modern STEM guys enduring these decreasing wages for years now. I didn’t think that was happening. I thought for people with a STEM degree, pay was rising.

And yeah I agree …. I’ve been in workplaces where I was the token white, but somehow I – at the lowest pay and generally treated like dirt – was the “oppressor”.

Cooter: Thanks for your advice; you are quite correct. I even regret going into engineering field in the first place. I have this old, rich, but hardly literate uncle in Texas who had told my mom why is he going for software engineering; at least he should go to medical school. Now, I see how wise my uncle was back then.

I definitely need to rethink this whole issue since there is no way to win; I keep learning, but landing and keeping IT jobs are becoming more and more difficult each year.

alex in san jose- I think all the rumors about the salaries of educated people rising, at least in tech, are fabricated by tech giants and colleges to keep getting the shipple stream into tech so that they have a bigger pool of fools to hire and thus pay them less and less. The only people who are benefiting are Indians since otherwise they would be in India earning $2000/year.

I hear registered nurses are the same thing; they keep feeding people these fantasy numbers to swallow huge student loans which at the end do not benefit them at all.

Well, when I was made redundant a few years back I kept looking for a job that had similar pay and conditions – couldn’t find one.

Heard every excuse under the sun.

As one can not keep depleting the savings account I finally found something. Worst job I’ve ever done and it ruined the body.

I paid more in income taxes in my previous job than I made in that one.

In terms of what I made in Japan 22 years ago it was about 1/8th of that…………….

At least here in Australia we have a decent medical system and national health insurance system.

It beats the US Medicare system hands down.

– In 2014 the state of Illinois had over 11,000 people who had a state pension of of more than $ 100,000 and more than 74,000 people who had a state pension of over $ 50,000. And people are surprised that taxes have gone through the roof in Illinois and people are fleeing Chicago & Illinois ?

– One also should also blame the succes of Healthcare of the decades. It meant that people are living longer and have to receive for more years such a generous pension.

One word ” unsustainable” As Larry Silverstein famously said ” Just pull it”

It isn’t the pension or retiree that is the problem, it is whatever Govt. entity that negotiates said pension as part of a wage package, and then does not follow through ensuring the pension is adequately funded using experts/actuaries as per the amount both parties pay into it. Most important, said organizations must be forbidden by statute ensuring they cannot raid pension plan for current spending programs for the entire population, especially at election time.

The 3rd party actuary system that monitors/administers the pension should be consulted BEFORE the pension is agreed upon during contract negotiation.

Private companies also raid employee pension plans, indeed, Bain Capital and the right wing darling Mitt Romney is famous for it.

Just one source:

https://sandiegofreepress.org/2012/07/how-mitt-romney-drove-companies-bankrupt-raided-pension-funds-and-paid-himself-handsomely/

I worked most of my life in the private sector, but did spend 17 years working as a BC public school teacher. When I started teaching I was 40. I had to return to school and earn my degree, (no debt as I was working at the time while attending Uni), and then my starting salary was 50% of my previous wage. In fact, I refused to work for our local District until they raised my salary on the grid to reflect my Industry experience. I ended up getting an additional $500/month…but it was something, anyway. We also paid in to our pension $1,000/month approx. Paying in to the pension was non-negotiable. Everyone pays into the plan and receives the pension upon retirement. Previously, the right wing Govt. (Social Credit…populist coalition) used to “borrow” from all BC Govt pension plans to fund infrastructure construction such as the Upper levels Hwy in West Vancouver, etc. It was a highways building Govt. and was in power for over 20 years. Seeing how this practice was a ticking time bomb for pension members, it was eventually put into law that this could no longer be done. Voila, Govt. pensions in BC are self-sustaining and currently funded to 105%. They do not require tax increases to fund the recipients, although currently new highways and bridges do. :-)

After 17 years of teaching and obtaining lots of self-paid training and another degree I retired back to a more private lifestyle. I am currently building a small rental by myself, which will one day supplement our pension income. My point is that is in error to demonize the pension recipients as your rancour is misdirected (in most cases). Instead, point the finger at the dishonest or inept politicians who make promises with everyone elses money, and then fail to keep them.

When local City Govt fails, it is not the fault of the employees, past or present. Look to who runs things for laying blame. Employees of any organization have little say in policy or direction.

Those who consistently want to cripple the government also want to be running it. What they actually want is to collectivize risk and privatize profits for their corporate masters while legislating what people do in their bedrooms.

Pensions are not “entitlements”. They are deferred earnings.

Thank you.

It is the same w/ Social Security. It is deferred earnings also, but many people are blaming Baby Boomers for problems that are actually caused by politicians.

Nanaimo firefighters recently settled for 95K after 5 years on the job which no doubt begins at 50K

The mayor opined that it seemed rich but there was ‘no point’ taking it to arbitration because the city would lose.

The arbitrators can only use public sector settlements as guides.

The fire and police guide lines were driven though the roof by $100 a barrel Alberta. Now with oil below 50 its credit is being downgraded and the provincial deficit is growing.

So are their firefighters and police out of luck?

No, the arbitrators will use BC numbers, maybe even Nanaimo’s.

This is the familiar ‘leap frog’ employed by the arbitration industry.

These young guys in their 20’s should be well paid.

But hitting almost 300 % of the average income while still in their 20’s or early 30’s is over the top for a job requiring no education past high school.

Of course the same employees could be hired for 30% less.

In fact, if the positions were offered at that rate, in an OPEN competition there would be hundreds if not thousands of excellent applicants.

So I guess we have to deal with the inevitable mantra: ‘how dangerous the job is.’

Instead of anecdotes ask a life insurance actuary.

Funny, the firefighters I know are constantly in training, because they face terrible dangers every day. In addition they are frequently targeted for litigation. So they are physically fit first aid emits who are trained in fire physics, chemistry of fire, hazmat, logistics, communications, languages, community outreach, and operating heavy equipment. Most have degrees, some postgraduate, because they do all that on public money, so they have to attract a very select group of candidates who will work cheap and risk death and torts while working for a jerky public.

Languages, operating heavy machinery, physics, post- graduate degrees????

Ok, I told you where my fire guys are, where are yours?

More ‘Detroits’ will be happening across the U.S.

They already are . Detroit may be leading the way down the path to perdition but cities like KCMO , Cleveland , Buffalo etc are closing in fast with no real hope of reversal in sight .

Take a drive across this great nation of ours … especially along the ” Blue Highways ” ( an idiom for the backroads and secondary highways as well as the title of a book .. not a political reference )

Guaranteed from small towns to once prosperous cities you’ll be shocked at the proliferation and level of decay and degradation from coast to coast and all places in between

I’ve heard one-third of U.S. counties have declining populations. I personally check demographic trends for TX counties because often I see low-priced homes that could be great rentals. But if they’re sitting in a declining county, I avoid them. Not everyone is checking and often Austin ‘home-flippers’ will venture north to neighboring counties where there’s not price appreciation in real estate.

When on ‘Highway tours’, I see construction for just two cartels (U.S. industries): healthcare services and higher education.

I live and work close to Orlando. A 2 bedroom flat shows on the list as $1250/month or $15,000/year. A quick google of median household income for the city shows $41,901. Let’s say that puts you in a 15% tax bracket. That moves your household take home to $35,616.

So the median renter renting the average 2-bedroom is spending about 42% of his/her/their take home on rent. Leaving $20,616 for all other expenditures. Subtract out ACA for a small family of 3 and you are probably living pretty close to the edge.

Medians incomes and median rents for a whole city are pretty useless for gauging how people make it. What you end up seeing are neighborhoods have clusters of people of similar incomes.

For instance in a more expensive area of San Diego the median incomes is around $120,000 a year. Which it’s better with the $600-$700k homes. (Still way overpriced considering where things were in 2013 and no major income changes)

If you were to take the median income of $70k things would look far more dire.

There are still many pockets in San Diego where homes are cheaper if you take a long commute. And a lot of lower income people share section 8 housing with a partner or roomate. The people I have meet in that situation tend to leave the state if they have family or job opportunities in a cheaper state.

Still even if most median income people can atrain housing below median prices, they probably still mostly live paycheck to paycheck.

Umm, an income of $120k is not enough to afford a $700-800k home. The downpayment alone is $140-160k. It would take an enternity to save that on an income of $120k in California, especially if you’ve got student loan payments as well.

That’s assuming people paid that amount for the home. Which they probably didn’t, since they have probably lived there for a while and paid less for it.

That’s also assuming they didn’t sell their other home to help with the down (trade up transaction).

Also, you would be flabbergasted at the amount of help parents give their kids for down payment.

One would be surprised how folks get Section 8 housing assistance. Lot of newer apartments in nicer area in SF east bay have income limits as well – higher income? No soup/flat for you!

It would be interesting to compare the SF/OAK/SJ price decreases with new builds as I think there has been apartment building boom in the bay area. That is supply catching up with demand.

The unicorn and start-up mania are cooling down as well with VC spigots slowing down with more start-ups closing shop.

Hooray for renters! In Chicago, they’re still building (several 70-90 story behemoths are still under construction), and I believe Chicago currently has the most number of active construction cranes in the nation. Which means even more supply in the pipeline.

Whether a few of these developers or investors go bankrupt when their rent projections aren’t met is not a concern for the average Joe, who will finally see some trickle-down benefit of the massive liquidity and search for yield that’s driving these construction projects.

” I believe Chicago currently has the most number of active construction cranes in the nation ”

Denver had Chicago beat hands down till just recently when out of the blue the plug seems to of suddenly been pulled with no new cranes going up and several existing ones coming down with no viable explanation currently on offer . Go figure .

Well, unlike the last bubble, this one is a much slower, death by 1000 cuts type assult on the working class. The “investors” are much more keen to maintain scarcity as their justification for price gauging and collusion.

When the price resistance is met, they will keep the throttle on full speed until they are tipped off that their serfs are about to lose jobs. Then they sell sell sell. Notice the berkshire for sale signs?

Whats disturbing here in Denver and part of whats kept us out of buying since returning is the high percentage of rentals in most single family home neighborhoods especially in upper middle and upper class areas .

As an example .. In the upper middle class ‘gated ‘ * community we’re presently renting in the percentage of rentals exceeds 40% ( in a neighborhood of less than 50 homes ) with at least three I know of being private equity owned furnished ‘corporate ‘ short term rentals that more often than not are being rented for 10 days or less

In the previous neighborhood we were in ( once again gated * upper middle class ) the rentals exceed 50%

* security theater at its finest ( sarcasm fully implied and intended )

Most of the summer vacation rental properties in my local area are in ungated. communities but many of these communities have formed HOA’s over time.

Many of the highest end properties are actually corporate owned.

AirBnB?

Sarasota, Fl

Aug 31, 2017

1 bed $950

2 bed $1500

This list is way off and useless.

With a tiny population of just 56,000, Sarasota isn’t big enough to be on this list. A city has to be over 215,000 to make the largest 100 cities.

A city with a population of 100,000 will just get it into the largest 300 cities.

Sarasota may be around the 1,000th largest city in the US or something.

“In Chicago, rents are getting crushed.”

Sounds like good news everyone, proof long-term globalization trickle-down economics actually transmogrifies to improve the standard of living!

The rent/wage issues in places like Seattle is a problem too, but it’s currently being masked by stock compensation. For example, the employees of Amazon are largely paid with stock compensation, and the stock has been rising faster than rent. If the stock price were to ever drop significantly, a whole lot of Amazon “wages” would evaporate into thin air. Seattle employees, as a whole, thrive on their stock compensation. Thus, the real estate and stock markets are tied together in many markets, especially where the tech industry is present.

Seattle has a population of 800K nearly.

Amazon hires 25K.. may be 100K more in other tech companies…

the ratio is way off then

I live in one of Sydney’s top harbourside suburbs [Mosman]where the median house price is over $A3million. I rent in an older 1960’s block of 12 and pay $A1900 monthly for 2 bedrooms. It’s less than average. Newer flats rent at $A2500 and up. Water views more again. It sounds a lot less disturbing than the US situation.

John,

Move to Melbourne……………………..

You know you want to!!!

In the UK there’s been documentaries recently on how violent Chicago is-has been.

Surely that must have an effect on:

a) people actually moving to Chicago and effectively having an impact on rental prices?

Gosh, I just read this article about NYC apartment rental rates yesterday.

Up, down. Who knows?

http://www.nbcnewyork.com/news/local/NYC-Rents-Hit-an-All-Time-High-in-July-442217563.html

Funny, isn’t it? In the eye of the beholder…

The rental data in StreetEasy’s report is based only on rentals listed on StreetEasy’s website. And they’re based on the “repeat rental approach,” which compares the same rental unit to when it was on the market the last time, years earlier. An algorithm and adjustments convert that into a “median rent” that the media then pick up without explaining what it is. So this is based on quite a different data set, and quite a different method than unadjusted median asking rents across the board.

Since this data is based on “repeat rentals,” it also completely excludes the impact of new units coming on the market.

Here is the original article. It explains some of the unique methods. At the bottom is a link to a detailed explanation of the methods:

http://streeteasy.com/blog/july-2017-market-reports/

also. it’s worth noting that steeteasy is owned by zillow. my experience with zillow suggests that it acts as a cheerleader for real estate and that it’s estimates are obviously inflated.

that being said… my landlord is soliciting me with money offers to get me out of my long-term manhattan residential rental lease. the apartments on either side of mine are currently being gutted and redone to squeeze more bedrooms/amenities into the same space and re-rented at a premium.

nyc as a whole maybe down but lower manhattan is still hot. my estimate is $4k for a 1 bedroom and $5.5k for a 2 bedroom / 1.5 bath in tribeca.

There are a lot of interest groups; they massage the data anyway they want and publish articles to drive their own points and bias. For example, do you think real estate industry would ever acknowledge drop in real estate prices, unless they absolutely have no choice?

Thanks wolf.

I read an article recently (do not have the link right now) that cautioned too much reliance on Zumper’s National Rent Report data.

NYC is a crucial apartment rental market (500k units) so it’s probably a good idea to compare and contrast as much fresh data as time permits.

Also, hotel room rates are down Y/Y in Manhattan due in part to the overbuilding of rooms over the last 10 years. Airbnb may also accelerate the price pressure by gaining traction.

Meanwhile, the flying monkeys at the central banks continue their dissembling about the need to normalize interest rates, knowing full well that any interest rate hikes would implode the central bankers’ Ponzi markets and asset bubbles, and therefore Yellen, Draghi, Carney, et al. will go on jawboning incessantly about mythical pending rate hikes, but will always come up with creative last-minute excuses to defer.

Meanwhile, gold hit $1321 today despite the best efforts of the central banks and their bullion bank accomplices to suppress the price with empty chatter about raising interest rates just as soon as “the data” supports a hike, or when Jesus returns, whichever comes second. While the infinitesimally small but rapidly growing of awake and aware people who see what criminals and fraudsters are running our central banks for the exclusive enrichment of their oligarch pals are happy trading their worthless green Fedbux backed by nothing for physical precious metals.

Before the financial crisis gold was ~$500 an ounce I think, or thereabouts. It peaked somewhere around $1800 around the peak of the financial crisis.

I have been watching the price of gold with interest because it remains stubbornly high compared to pre crisis. I am no financial expert but the elevated price seems to indicate a lack of trust in the “recovery” from the great financial crisis.

The building that I live in now has “1 month free bonus” all the time on Craigslist. But, even that gimmick doesn’t work anymore. They have a few apartments which have been vacant since more than a year ago.

If these landlords had to pay real mortgages and real interest rates, they could not have afford to leave their apartments empty and would have had to decrease the rent to find tenants.

THIS

Here in north Denver I found a very nice apartment built in 2012, loads of square footage and everything perfect. They wanted $2K/mo for a 2/2 and $1500 for a 1/1.

I came back after the sun went down and most… like 3/4 of the units had no lights on. Presumably, the inventory is sitting empty in many of the complexes, just like the shadow inventory/delayed forclosures on the housing side.

Wolf, would it be possible to combine your rent data and housing price data to present a “price to rent ratio” which could give an indication of where real estate prices sit in certain markets with respect to rental costs, providing better context about which markets may be overheated and which probably lack sufficient supply to keep up with demand?

Rich Pensions, lack of state budget, tax like mad, and now people vote with their feet. Less people, rents go down. Simple.

Those pulling the wagon have decreased, and more riders have jumped into the wagon.

Which central bank-blown asset bubble will be the first to implode?

http://www.scmp.com/news/china/economy/article/2109197/china-house-prices-grow-fastest-globally-12-months-june

Gee, I’m really disappointed that Melbourne only made it to 21 on the list.

But that is better than Sydney – they came in at number 29.

Not one city in Japan made the list.

http://www.hurun.net/EN/Article/Details?num=9086B256CC78

Sarasota msa includes Manatee co (where the airport is located) has a population of over 700,000. There are also over 5 million visitors some who stay for months each visit.

The report doesn’t look at counties or states or MSAs. It looks at the largest cities. The North Port–Sarasota–Bradenton metropolitan statistical area, which is the MSA you’re talking about, consists of Manatee County and Sarasota County.

How much of the decrease in Chicago rents is due to people fleeing the violent sections like Austin, Garfield Park and Englewood? I know the articles states that there is a lot of new supply coming online downtown, which could be responsible for the decrease in rental prices, but Chicago is really two very different cities. I live in this area. It is full of people and seems in demand.

In July, the Tribune ran an article saying that Austin’s population dropped from nearly 118,000 people in 2000 to 97,600 in 2015. For the first time is 45 years, Austin is no longer Chicago’s most populated neighborhood. Such a loss of population leads to a drop in demand for rentals, which lowers the cost of low end rentals. Could this be dragging the Chicago median price down?

It would be informative to find household size numbers. I’d guess as rents go up in an area,

the number of people per unit increases. Basically a lower standard of living which doesn’t

show up in the income stats.

But instead rents are plunging.

So if renters are still doubling up …

Unlikely with prices falling and inventory ballooning.

So, what are the main reasons people are leaving Chicago?

Young adults better get used to living with their parents, thanks to unaffordable housing and a “gig” economy.

Heckova job, Ben and Janet.

http://www.businessinsider.com/maps-young-adults-still-living-at-home-2017-9

The problem with this analysis of Chicago’s rental market is that it uses population figures for the entire city when the rental market construction boom is happening in Chicago’s central city, and nearby communities like Wicker Park. In Chicago’s West Loop the population doubled from 5,000 to 10,000 residents between 2000, and 2010, and according to the 2015 U.S. Census ACS estimate, grew by 5,600 between 2010 and 2015. The population of Chicago’s South Loop doubled from 10,000 to 20,000 between 2000, and 2010. Chicago’s building boom in the central city is driven by a host of major businesses relocating corporate headquarters to Chicago from vacuous suburbs.

The speculators are busy killing the goose that laid their golden eggs, but they don’t seem to realize it.

They have destroyed the US in their quest for more and more money. Rents in this case cannot rise forever. Not without a corresponding increase in worker wages.

Rents have risen huge because low interest rates have boosted housing prices. Yet incomes are falling in many tech areas. Fifteen years ago I worked as a software engineer coding Oracle database apps for a major employer and had great benefits. I earned $72k/yr. Programmer salaries haven’t risen 1% since then while housing costs have more than doubled.