Bankruptcies surge as the “credit cycle” exacts its pound of flesh.

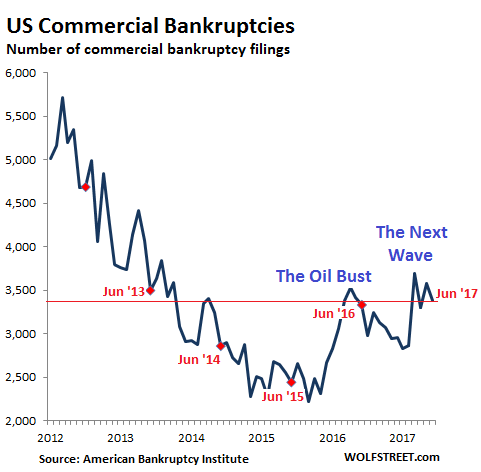

Commercial Chapter 11 bankruptcies – an effort to restructure the business, rather than liquidating it – jumped 16% year-over-year in June to 581 filings across the US. Total commercial bankruptcies of all types, by large corporations to tiny sole proprietorships, rose 2% year-over-year to 3,385 filings, according to the American Bankruptcy Institute. This was up 39% from June 2015 and up 18% from June 2014.

Commercial bankruptcies topped out at 9,004 in March 2010. By that time, credit conditions had been easing for a year, and liquidity was chasing yield. Not much later, even zombie companies – if they were large enough – were able to refinance their debts and borrow more to fund their operations and keep creditors happy. Bankruptcies fell sharply: In September 2015, they bottomed out at 2,217 filings.

Then the energy bust hit. Oil-and-gas companies along with coal companies began toppling, and bankruptcy filings surged. But in 2016, oil prices more than doubled off their lows. New money began pouring into the sector again. And drillers that had been cash-flow negative for two decades and had lost dizzying piles of money were able to refinance their debts and get new money to drill into the ground and live another day. And the waves of energy bankruptcies receded.

But now the next wave is building, with large and small retail operations at the forefront. I’ve covered only the largest chains of the brick-and-mortar meltdown, but there are many smaller operations, mom-and-pop stores, fashion shops, and the like that have quietly given up.

Bankruptcies are very seasonal, with peaks around the end of tax season and sharp declines in the following months. The data, which is not seasonally adjusted, gives a raw and noisy impression of how businesses are faring in this economy.

This chart shows the total number of commercial bankruptcy filings of all types. Note the strong seasonality. Hence, the year-over-year comparisons in red:

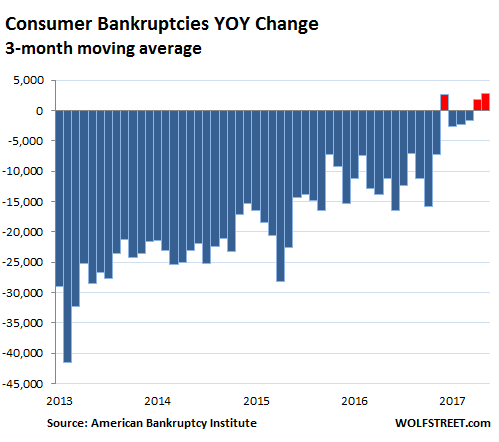

Consumer bankruptcy filings followed a similar pattern, but the turning point occurred a year later – in December 2016 and January 2017 – and was less obvious. Bankruptcy filings rose year-over-year in both months, the first back-to-back increase since 2010. I called it an “early red flag” at the time.

But consumer bankruptcy filings are volatile on a monthly basis, and turning points can take a while to be confirmed. In February, filings fell year-over-year. In March, they surged. In April they fell. But contrary to prior seasonal patterns, they surged in May. And in June, they ticked up 0.6% year-over-year to 63,372.

To filter out some of the monthly noise, I’ve created this chart using a three-month moving average of the year-over-year changes in the number of filings:

The chart shows the trend since 2013: Sharp year-over-year decreases in bankruptcies as consumers recovered from the Financial Crisis. The decreases gradually tapered off, as would be expected – bankruptcies are not going to fall to zero. But now a new phase has commenced: year-over-year increases in bankruptcies.

Clearly, consumers aren’t yet all of them together collapsing under their debts in one fell-swoop, but the “early red flag” is being confirmed as more and more consumers are buckling. Data on consumer delinquencies and defaults, particularly in subprime auto loans, has been cropping up for a year. Now it is filtering into bankruptcies.

“The economic challenges weighing on the balance sheets of struggling consumers and companies, especially retail businesses, have them seeking the financial shelter of bankruptcy,” observed ABI Executive Director Samuel Gerdano.

So the credit cycle has turned for both, businesses and consumers. This was inevitable. Credit cycles always turn. Easy money has much to do with it. It encourages borrowing for consumption or to fund business losses or unproductive investments. Years of too much borrowing lead to difficulties in servicing these debts and eventually to big losses for creditors.

Consumers seeking bankruptcy protection are those with piles of debt they can no longer handle, given their stagnating or declining real incomes, or perhaps the loss of income. This data shows that more consumers are facing these conditions, and the first wave is throwing in the towel.

Mortgages are not the cause. Home prices have been surging for years. By now, most homeowners can sell the home and pay off the mortgage. And if they can’t, and the bank forecloses on the property, it will rarely try to obtain a deficiency judgment in the 38 or so “full recourse” states where it is allowed. And in the dozen “non-recourse” states, the bank cannot even try.

The $1.4 trillion in student loans, though they now have sizzling default rates, are not the cause for bankruptcy filings either because they cannot be discharged in bankruptcy. But they contribute to driving people into bankruptcy.

Medical debts play a role – but not in the increase in bankruptcy filings. Some bad luck and one major emergency-room type event, without insurance, followed by a six-digit rip-off bill will do the job. But unless unemployment surges, the level of medical bankruptcies doesn’t move with the credit cycle and remains fairly constant.

The primary causes for the increase in filings are the $1.12 trillion in auto loans, the $1 trillion in credit card debts, and other consumer loans. Those loans fired up consumer spending in prior years. Now the bill is coming due.

Private equity firms bought out numerous brick-and-mortar retailers in past years. Now their finely tuned protocol of asset stripping bears fruit. Read… Brick-and-Mortar Meltdown in June: Who Got Crushed?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Negative Rates like now!!! Consumers and businesses need to be paid for being courageous and hopeful.

>>Consumers and businesses need to be paid for being courageous and hopeful.

…just like the founding fathers intended

(that’s what she said)

Negative rates on consumer debt seems, on its face, seems like helicopter money, but worse.

You’ll have stupid amounts of money dumped into the market, especially into real estate while making this surge cash-flow dependent. You’ll blow already eye-watering real-estate prices into the stratosphere seemingly overnight and set-off the single largest blow-off top in human history.

Tulip mania, but this time instead of flowers it’ll be a 3/2/2 in Quartzsite Arizona for only $2.4 million. The worst part of it all would be the inability for the Fed to take away the punch-bowl.

While you can have champagne and caviar with a few dozen bank and fund managers to keep the party going, bribing the consumer, en masse, to keep spending as inflation creeps from real-estate into anything and everything not nailed down would be impossible.

It would completely destroy any fiat — and its all continent upon the consumer getting a piece of the pie that they have been deprived of since 98.

We live in interesting times.

Long land, antiques, AG, AU, fine art, collector cars, booze and short everything else.

Hausa Where are you seeing negative rates on consumer debt I’d like some if that were available I’m not seeing that whatsoever The only people getting the free money are the big banks and corporations perhaps

” Long land, antiques, AG, AU, fine art, collector cars, booze and short everything else. “.

Some of those items seem to be catching a top, others are looking down and can see the bottom with dread. Collector cars to start with, then booze, then antiques, and flowed by fine art, until…

You forgot the most inflated balloon that is already losing air…….land and housing.

Agreed, I would go fit her and just day I am dubious of most actions that equally inflates the spending power of a group already well off people. For the reason you say. GiveING a bunch of people more money doesn’t change demand, it will just mean we can all pay more for assets like a home thus prices will quickly grow even higher and faster.

The flip side I suppose is that not all items will inflate into tandem with such an infusion, but I think the ones I care about would.

Fed conjured money/credit out of thin air, fractionally multiplied by “in the magic circle” Megabanks, creating loans to be repaid with real earned money.

What a scam.

I would add, short globalisation. When this blows, it will be over like a distant memory. Also, long guns. Globalisation isn’t meant to bring people of the world together, quite the opposite: to create tribal frictions to rule more effectively.

You want negative rates?

My main bank just introduced a function in online banking that allows you to see what real interest on bonds is after capital gain taxes, assorted fees and all other expenses.

You have to scroll down a very long way to find a plus sign, and even then you need to remember the yield is not inflation adjusted. Unless you believe in deflation (kinda like the Ark of the Covenant and the Holy Grail everybody speaks about it but nobody has ever seen it) negative rates have been here for quie a while.

It amazes me we’re anywhere near full employment and wage inflation is a concern.

You are in dreamland. There is nothing like full employment and wages stink. What planet are you living on?

You missed “mean chicken’s” sarcasm.

Chicken Full employment really? If that were true I would still be in the states I worked from 13 years old in 1967 and yet couldn’t find any worthwhile work since 2010 in the Hamptons area of NY My wife was 36 then and didn’t get even a single callback on Jon interviews Full employment indeed And we wanted to work No drugs no alcohol good education but we don’t speak Spanish

You’re not the only one who missed mean chicken’s bitter sarcasm.

But your story of you and your wife not being able to find a job is one that many people experienced. It’s a terrible fact that keeps getting brushed under the rug.

That’s sounds pretty shitty, what job sector were you both in the knowing Spanish was a factor? I live in Socal and have never been asked to know a second language.

But I agree the term full employment is a real stick in the eye for people who has seen all their job prospects dry up. The effort to rectify changing or disappering job markets seems minimal or not an important issue politicially.

In Miami every job requires you speak Spanish.

Half the jobs in SoCal require Spanish or working expertise. I suppose if you’re in the upper eschelon, you don’t have to deal with the riff raff.

Construction is one of those fields. I walk by a number of construction sites regularly (building boom here). These are highly skilled and well-paid workers who put these buildings together, work the rebar, pour concrete, or whatever, and I have yet to hear any English from the workers. Occasionally when the boss guy or architect or whoever shows up that isn’t dressed like a construction worker, you might get a dose of English.

Interesting to know… I would be pissed too, shouldn’t have to learn Spanish to do a job who’s primary skills have nothing to do wit language…

Although Miami is technically in the US, its natural geography is that it is the capital of the Caribbean, including Colombia and Venezuela. Spanish is appropriate. California was part of Mexico170 years ago; before that it was part of Spain. It is reasonable that Spanish is commonly spoken here along side of English. While in my district (Sacramento Valley) many workers speak Spanish, I know of almost no jobs that require Spanish language. Those people were hired because they’re good workers, just like the construction workers in San Francisco that Wolf mentioned. It would be illegal to require Spanish language skills if they are not relevant to the job.

I had a rigorous traditional education in which between boarding school, college, and grad school I was taught Latin, Greek, French and German; when I returned to California I learned Spanish in order to be a full participant in my community. It’s not difficult.

Whatever the language on a heavy construction site, it should be the only one.

Confusion when working under cranes etc. is dangerous.

I’ve lived in socal and speaking Spanish seemed to be required for tons of jobs from the phone company to any sort of machine shop work, any of the solid blue-collar professions. Gringos not welcome!

Frederick – you’re 20 years older than your wife? More power to you buddy!

You talk about smaller shops giving up quietly but who has ever said a shopkeeper should carry on indefinitely? In 2003 when we had a small shop our plan was to run the business (which we set up from scratch) for 6 years then stop. We did.

The only reason larger retailers continue beyond their shelf-life is because their debt commitments force them to keep going regardless. Having run out of ideas the founding owners sell up, take the money and leave the dying embers for someone else to nurse.

When a smaller shop goes bankrupt, it’s not because it’s successful and the owners are now ready to retire. It goes bankrupt because it cannot meet its obligations any longer.

By “quietly,” I meat going bankrupt without national media attention – in contrast to the big chains.

The second to last paragraph resonates with me because just yesterday I received what I thought was an odd “agreement” change letter from one of my credit cards. It stated that when a payment is made to reduce the balance it may not re-instate that credit and they reserve the right to restrict it for “risk management”. Note that I have zero CC debt and in a decent spot right now so I don’t believe it was me that prompted the change.

Always great reporting Mr. Wolf.

You mention credit card debt, indeed. Medical bills, medical insurance and food are now a big part of that debt. Some slight reduction in some rent data is not countering 10 to 20% increases in insurance premiums, or a $2,000 emergency room visit because you have no insurance. Go have a baby as see how much that costs this year vs. 5 years ago, anything for that matter.

Access to the net and phone is an expense that many feel is a utility now, and it was not in many peoples budgets or thoughts 10 years ago. That $30 bill has grown to $150 and more for many families, especially ones that feel little Jonny or Suzie needs a phone to take to elementary school.

Don’t have the cash at the post office, gas pump, grocery, tax collectors office….no problem, just charge it. Americans have been conditioned to the idea of the ‘minimum payment’, so living large is easy. Until it isn’t. We have been taught by the media, government, and business…don’t worry be happy.

You mention Amazon and the like….they will be the next brick to fall from the wall as online sales grow…..weaker. All those web companies the VC said are worth billions, may not be near that in the end.

Meme, Amazon is not a real store….Its the MIC’s attempt to control most internet commerce and commerce in general…It is known that the owner Bezos owns WaPo as well and is a public member of the MIC…

…”Defense Secretary Ash Carter established a Defense Innovation Advisory Board and has asked Amazon Founder and CEO, Jeff Bezos, to join others, including astrophysicist Neil deGrasse Tyson and former Obama administration official Cass Sunstein.”

I dont think people on this website are hip to the fact that you have a small mafia going on a power grab disguising it as legitimate business takeovers (think whole foods) …Its not….These guys made bad bets, dont want to own them, and out entire financial system is upside down but nobody wants to point any fingers….They dont want to own them because they are trying to build more control, but on the outside it looks just as though they dont want to lose the money..Not so…Looks at Amzn’s profits and explain that to me Wolf.

Amazon has never posted a profit in it’s entire existence

You should check Amazon’s earnings reports to get illuminated. Over the past 11 years, Amazon made an annual net profit every year except 2012 and 2014. In 2016, it made $2.4 billion in net profit.

Granted, for a huge company, it doesn’t make a LOT of profit, and it makes very little profit in its retail operations, but its AWS division is very profitable, and overall Amazon is profitable.

Medical bankruptcies have halved in an almost straight decline between 2010 and 2016 (http://www.consumerreports.org/personal-bankruptcy/how-the-aca-drove-down-personal-bankruptcy/). Between 2013 and 2016 there were about 280.000 fewer which corresponds to a 7800 decline per month. An interesting thought is shifting the graph by that upwards. In any case the bankruptcies for non-medical causes have been increasing for a longer time than the overall bankruptcy graph indicates.

Good points. I think there are two factors in the trajectory of the chart in the article you linked, not just one:

1. As the article points out, the rise in the number of insured people;

2. Medical bankruptcies in the chart peak in 2010. That was the peak of the unemployment crisis, when official unemployment was over 10%. Unemployment also leads to loss of insurance (people can’t afford COBRA or it runs out, and they can’t afford to get insurance on the insurance exchanges…. because they have no money at all). That’s why unemployment is the biggest driver of medial bankruptcies. And when unemployment drops and people get hired again, they pick up insurance from their new employer, or they earn money to buy insurance on their own, and medical bankruptcies subside.

So the explanation in the article you linked seems to be slightly one-sided.

A big part of the decline in medical bankruptcy is believe or not Obamacare. Hence why the Republicans are having such a big trouble trying to tear it down.

The general consensus seems to be that any change to health care much like entitlements are taken very negatively. And usually for good reason because it is very challenging to alter this systems while not harming large groups of people.

So now that the ACA is in further changes become even more unpopular.

Technically I wouldn’t say it’s been difficult for the Repubs, all they have to do is sway 4 votes and they are home free. I think there is a good chance they will get that done in the next few months. So while I think what they are trying to pass will be unpopular, it won’t be all that difficult.

As with most Repub plans they get the tax cut and spending cut right, but fail to put in a solid structure to help decrease costs and increase market competition to goad the free market into filling the gap in services and options.

“As with most Repub plans they get the tax cut and spending cut right, but fail to put in a solid structure to help decrease costs and increase market competition to goad the free market into filling the gap in services and options.”

The vaunted Free Market which solves all problems seems to always just be inches away. I think, by default, putting “in a solid structure to help decrease costs and increase market competition” would by default, not be a free market.

The strip mall near me had a franchise type real estate office close in the last few months, before that the pizza place had closed. Now the strip mall is about half empty. The big mall is a major employer and as the chain stores close you can see the spill over on smaller businesses. Those newly unemployed employees are disappearing from the rest of the retail universe.

later that day, a ghetto popped up.

Petunia, I don’t think most folks have seen what happens when the community backbone dies. We both know that Miami could start a tour for visitors on ‘this is what happens when your community has no continuity”. Of course, America is full of examples of this, but shuuuch, we don’t talk about such things without being called names or shaking the status quo. Take a look at Houston, Baltimore…just for starters

This past week was our summer holiday. We had originally planned to visit New Orleans for a couple of days. But after reading about all the crime against tourist in the tourist areas, we stayed home.

As the economies of cities start to show economic stress, it plays out on the streets, to their determent. I’m sure they won’t miss our business, but I’ll bet we are not the only ones not going there this summer.

Petunia – New Orleans is a truly scary place. I’ve been following the blog of a street musician there for years, and reading about the place in general like on Reddit, and sheesh, it’s like … some tourists make the mistake of turning right instead of left coming out of their very nice hotel and oops another murder statistic.

My father owns four small (5-7 stores) retail strip malls in central Florida and one at the space coast. Mostly small businesses like insurance agency, beauty parlor, small florist, etc.

Demand has dropped significantly since the good old days or pre-08. Only the well established businesses have stayed and filling vacancies is slow and often potential tennants are rejected based on business type.

Since the buildings are owned outright, and my Dad isn’t a greedy landlord, the rents are very reasonable. Even with that though, about 1/4 of the units remain vacant. The buildings are in good areas and are kept up (not slummy). In the 70s through early 2000; never had a problem keeping rented.

Just a confirmation of where things have been and are headed.

Small business ownership has gotten flattened.

As a ( very ) ” Small source of Comfort ” knowing yours is not the only case :

Every mall in the greater Denver/Boulder area be it prestige luxury indoor or common variety strip mall have a plethora of vacancies ( including anchor spaces ) with little or no interest in filling them … at any price .

Yet … those very same malls continue to raise their rental rates exorbitantly … as well as with malls like Cherry Creek ( our pretense of a luxury mall ) diminishing many services and amenities now charging for covered parking that used to be free .. etc – et al – ad ( major amounts of ) nauseam .

And just to add insult to injury . More than one outside and foreign ‘ developer ‘ is currently vying to build new malls across the area .. with the proposed mall in Greenwood Village .. one of the few municipalities that puts such expansive development to the vote … being shot down by 65% of the voters .. ( a case of the voter being smarter than the city counsel )

Brilliant ! Lose your tenants and anchors .. make the consumers lives more difficult and expensive … all while making moves to build new malls ….. yeah … that’ll work out real well .

Did I say 1929 in a previous comment ? Hell .. if this all goes down the way its looking right now we’ll win up making 1929 look like a walk in the park in comparison .

As per my comment yesterday in relation to all the financial news of late so closely resembling that of the late 1920’s paraphrasing an old Prince song lyric ..

‘ Tonight we’re gonna cry like its 1929 ‘

the song that comes to mind to me is “Money for nothing and your chicks for free “

Malls are disappearing because their prices are high and they tend to be far away. Some malls are by law, a few miles outside the city. When you can just order anything online and have it delivered home or just go and pick it up, is no wonder malls are going the way of dinosaurs.

Not to mention renting a space in a mall tends to be expensive, so that raises the price of oroducts and in fact I have learned that you can find the same stuff cheaper elsewhere. So even without bubbles bursting, they have been in decline for a while. Now even more with oil prices becoming higher. Why waste fuel to go to the mall when you can go local or buy online?

Online shopping allows people to shop at work

I asked the GNC guy to match a price from amazon and he laughed at me about having to pay rent,advertising,utilities,etc. Amazon is a killing machine.

Errr … well … here’s the dirty little secret when it comes to Amazons so called …. ‘ discounts’ ;

1) Not all Amazon sells is below retail price with Amazon more often than not pulling the ole Walmart bait and switch of putting on display the few things that are seriously discounted in order to convince you everything they sell is … when in fact a fair amount of it is above average retail

2) Every time you buy from Amazon you’re taking a dollar out of someone in your area’s back pocket as well as the tax revenues that pay for your roads , schools , police , fire departments etc .. which then creates either higher property etc taxes or vastly diminished services … including your kids/grand kids K-12 education

So remind me again whats so wonderful about those occasional short term discounts in light of the long term and very serious consequences ?

Think about it ….

And yet Amazon is not the one responsible for the retail chains price war. Without that prize war retail chains would get way more than the 1% or 2% profit the chains that aren’t losing money are getting.

So really they are ruining themselves, online stores just made it faster.

But yes “Scamazon” is a scammer it has been from the days it just sold books.

Lets not forget that Amazon now has a new granted U.S. patent that allows it to openly conduct surveillance on YOU, track you purchases by like, kind, and price. If you are one of those folks who walks down the isle at some store and just puts thing in your basket without looking at a price…lets say a grocery, the prices will be customized to your spending habits and how much you pay for this or that. You know that $14.95 bottle of wine, it will cost you 19.95 at the checkout because of the tiny jar of caviar you picked up and held for 14.3 seconds.

Surprise !!!!

I think “dynamic pricing” or whatever they’re calling it is going to go over like a fart in church.

People, even animals, are deeply, instinctively, interested in fair play. There are numerous animal experiments, many of which you can watch on YouTube, that show this. Our sense of fair play and justice is a much deeper thing than many think on the conscious level.

People will “stay away in droves” and also, I believe there are laws against that kind of shit. In fact in some stores, if it shows as $1.99 on the shelf and it’s $2.99 at the check-out, it’s free.

Alex,

I use coupons and have gotten good deals with them but the concept bothers me. I don’t like the idea of customers getting charged different prices at the same moment in time. It seems unfair because it is.

This is how bad business is out there. I get coupons all the time from a big box store that sells home goods and if I didn’t use them before the expiration date, I would thrown them out. I found out they now accept expired coupons no matter how old and they also accept multiple coupons on the same transaction. I recently used two $5 off on one transaction which was good but somebody else buying the same thing paid $10 more. If I hadn’t had the two coupons I would have paid $10 more. In fact, I wouldn’t have gone to the store without the coupons.

It seems illogical in the extreme that our society expends vast amounts of money and effort to control the importation, distribution, and use of addicting/habituating substances such as drugs, tobacco, and alcohol, but does nothing to control the even more destructive phenomenon of “debt.”

We have enacted speed, size, and weight limits for vehicles operated on our public roads, with special licenseure requirements for the operators of “large” or commercial vehicles [CDLs] with special endorsements required for HazMat, etc., so should analogous limits be placed on “debt?”

What should we as a society do? Should “debt” be available only by “prescription?” Who should decide? How much accountability should the lenders have when things go wrong on both an individual and aggregate/holistic basis? Can “central planning”/regulation moderate the “credit cycle?” Should it?

Good lord ! Profound doesn’t even come close when describing your comment today McDuffee . That cuts right down to the bone and thru it proving once and for all the truth when delivered well really can hurt .. damn !

Comment of the Week in my ( hardly ever ) humble opinion . Hell … maybe even comment of the month . Damn …

You can’t repeal history. Our entire financial system is based on debt and always has been. In colonial times farmers would get script for selling their crops which was an IOU they could cash at a bank or use to pay taxes. Warehouse script would be cashed for bank script and so on. They preferred the scrip to gold and silver which was hard to use.

Those of you holding gold and silver take note, even now people are buying into the crypto currency scams because of portability.

RE: …You can’t repeal history. …

—–

Sure we can. In the US at least, slavery has been abolished, and women now have the franchise, and an increasing degree of socioeconomic equality. Plagues and epidemics have been largely abolished through public health measures such as pure food and drug laws, clean water laws and mandatory immunization.

We no longer passively accept the social injustices of slavery, or women as second class citizens, or the periodic outbreaks of disease as “the will of god,” so why do we continue to accept the debt/credit cycle as “the will of Mr. Market?”

Alexander Hamilton was “the” founding father. He was also a banker. The constitution says a lot of things, but the most important part, to him, is Section 10, Article 1:

“No State shall enter into any Treaty, Alliance, or Confederation; grant Letters of Marque and Reprisal; coin Money; emit Bills of Credit; make any Thing but gold and silver Coin a Tender in Payment of Debts; pass any Bill of Attainder, ex post facto Law, or Law impairing the Obligation of Contracts, or grant any Title of Nobility.”

This part was meant to fix the fundamental flaw in the Articles of Confederation: the fact that the states could print their own money, and invalidate contracts overriding federal law. This clause made national level banking possible and allowed for the massive concentration of wealth in banking.

Hamilton was the key driver behind the constitution and the formation of the USA. And he did it primarily for his personal self-interest as a banker.

One little truth is that Hamilton convinced the states to accept the new constitution by having the federal government assume all of the revolutionary war debts of the states and gave the officer corps of the army and militias free treasury bonds.

Point is, debt is the driving force of the country. Always has been. So you are fighting some very, very powerful forces.

Kent,

You left out the part where Hamilton bribed congressmen with stock in the Bank of the United States in order to create the bank in the first place. Some traditions are still strong.

Interesting comment on Hamilton Kent.

Hamilton was indeed a banker. He and Isaac Roosevelt (yes, same family tree as Teddy & FDR) founded the Bank of New York in 1784, and in 1792 the Bank of New York was the first publicly traded corporate stock on the NYSE.

In 1791, Hamilton orchestrated the set up of the First Bank of the United States which was given a 20 year charter, and effectively put the issuance of the dollar in the hands of the Rothschild empire. Kent, please correct me if I’m wrong on this piece of history, and thank you for your comment.

Certain amount of credit and debt is acceptable, and always has been part of life. Some borrowed because they could collect their own taxes, like kings and nobility.

When they introduced diners card, they did not mean to put a credit card into the hand of the common man.

Now, credit has been perfected into a fine art keeping millions on a razor’s edge, one wrong step away from ruin. The economy depends on it like on oxygen. And when dominoes start falling, there is no stopping it.

Max Min,

I hate all these elitist theories about credit. Before credit cards my working class parents had credit with all the merchants they did business with. As a child I went to the grocer every day to pick up items for my mother. The amount of the sale was written up in their account book and I was given a receipt. My parents would settle the account later. We also had furniture bought on credit, they would send a man to collect the money monthly. I could go on and on.

This notion that credit didn’t exist until credit cards is uninformed. The whole point of my original comment was to point out that Colonial America functioned almost entirely on credit instruments.

” so why do we continue to accept the debt/credit cycle as “the will of Mr. Market?”

George,

BECAUSE it is the will of the market….

This debt addiction is spreading to the rest of the world. I have relatives in India who take auto loans. This was unheard of even 15 years ago. You couldn’t pay cash for a car? You took public transport (which is plentiful).

It’s considered “normal” now to take loans for weddings, vacations, etc. My bank in India sends me notifications ever so often about “festival loans” and “gold loans”. Yes, I apparently need to take loans to go out and celebrate a festival and buy jewellery ‘cos they said so.

The older generation in my family can’t believe how indebted their children are, and willingly so.

I was going to comment before when you shared that India is a nation of savers (which I admire), this sounds like fertile ground ripe for harvest.

Banking is not rocket science. Verify employment; Verify collateral, and in doing this discount recent asset inflation; Require substantial down payment, or skin in the game.

Lending standards went far south in 2004, recovered some post Gfc, and has badly degraded again.

Problem is bankers allowed to book profit as soon as loan is on books, if it all goes south gov bails out bank and bankers keep both jobs and bonuses. Until this changes deep recessions will persist.

Another factor in this is the gradual change in the economy from a discretionary to a tollbooth economy. The average person now has most of their paycheck, beyond debt payment and taxes, go in to fixed monthly payments such as cell phone bills, internet, car insurance, medical insurance, rent, hoa fees, parking costs, health club membership, etc. This leaves little left over to spend at business’s in malls or online, and makes it much more difficult for these consumers to cut back quickly in hard times leading to more bankruptcies for them and the business’s where they spend what little discretionary money that they have.

I vividly recall in the late 1980’s my home phone cost $11/month and my cable bill was $36.

Now my 3 cell phone family is in for $105/month and cable/internet is $141.

And no, it is not that much better.

Our 2-cell phone family used to pay $75 a month to Verizon. Now we have Ting. No contracts, $30 a month. Good service.

I use cellnuvo for cellphone service

Completely free.

.

I have 23 and 25 year old boys. They are not nearly as interested in the “things” that I was interested in at that age-things pertaining to the “American Dream”. A small apartment in the city, smart phone and NO car or car payment and they are happy as clams

I guess everyone is different My nephew and his wife just bought a home in a very expensive suburb of Boston and have two cars

Hey, I was the same way…until I met my spouse at age 30. LOL Heck, she was the same until that time, too. I think getting married and starting a family is what accelerates it, and people are simply doing that later in life these days.

We’ll see what those 20 somethings are doing in another 10 years. ;)

– Illinois’ debt downgraded to “Near Junk” won’t help to decrease the amount od bankruptcies either.

– @Wolf Richter: What happened to the level of interest rates Illinois has to pay as a result of this down grade ?