The first feeble reactions?

Here is what happened: The Fed has been tightening by raising rates and it has announced the unwinding of QE, with only the timing being still debated – whether at the September or December meeting – and financial conditions should be tightening in response, and the Fed wants them to tighten. But the opposite has happened. Markets have blown off the Fed.

Instead of tightening, financial conditions have been easing. Over the past few months, stock prices have surged, and bond prices have risen too, as longer-term yields have fallen and yield spreads have narrowed. Members of the policy-setting Federal Open Markets Committee (FOMC) have repeatedly lamented this disconnect at their last meeting in June. This became clear in the minutes of the meeting.

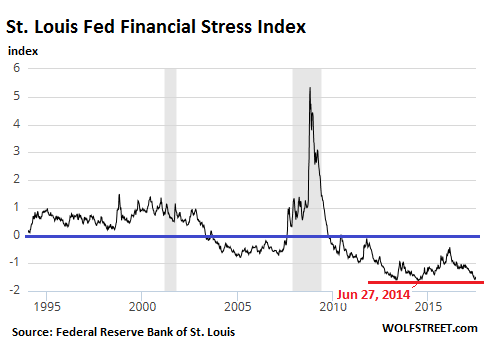

Today’s weekly update of the St. Louis Financial Stress Index shows this disconnect. The index – which indicates whether “financial conditions,” as the Fed calls them, are easing or tightening – shows that financial stress barely budged off record lows (red line). In the chart, zero (blue line) indicates normal financial market conditions. Values below zero indicate below-average financial stress and easy financial conditions:

The index is based on 18 weekly data series to measure financial conditions in the market: seven interest rate series, six yield spreads, and five other indicators, including the S&P 500 index.

What has happened in recent months is that only short-term yields have risen in response to the rate hikes, but longer-term yields have fallen, spreads have narrowed, and stocks have soared.

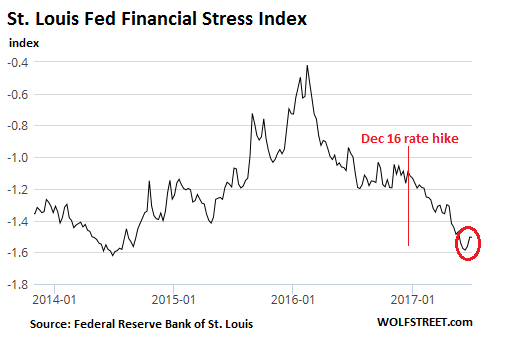

The chart below shows the details of the index since 2014. Note the record low of -1.621 on June 27, 2014, while QE “infinity” was still raging. Financial conditions then ticked up toward “normal,” to hit a still below “normal” -0.419 in February 2016. At the time, the Fed was flip-flopping wildly on rate hikes. But since December 16, 2016, when the rate hike cycle got serious, the index continued to decline to the great frustration of the Fed:

Note that little hook on the right side – the first, feeble reaction in the markets to the Fed. The index rose from the near-record low of -1.586 on June 9 (days before the June 13-14 FOMC meeting) to -1.504 last week, and to an essentially unchanged -1.505 today.

Since December’s rate-hike day, the dollar should have risen, but the opposite happened. On December 16, the dollar index (DXY), which tracks the dollar against a basket of other currencies, stood at 103. Today, it’s at 95. The dollar has fallen nearly 8% against this basket of currencies. Based on UK futures trading, the dollar fell even against the British pound.

In other words, the markets are still blowing off the Fed. And the Fed has lamented getting blown off at the FOMC meeting in June. In the minutes released yesterday, this frustration with the stubborn markets was featured several times, including in these sections (emphasis added):

“Yields on Treasury securities and the foreign exchange value of the dollar had declined modestly, while equity prices had continued to rise, contributing to a further easing of financial conditions…..”

“Domestic financial market conditions remained generally accommodative over the intermeeting period.”

“In their discussion of recent developments in financial markets, participants observed that, over the intermeeting period, equity prices rose, longer-term interest rates declined, and volatility in financial markets was generally low. They also noted that, according to some measures, financial conditions had eased even as the Committee reduced policy accommodation and market participants continued to expect further steps to tighten monetary policy. Participants discussed possible reasons why financial conditions had not tightened.

And the Fed is fretting ever more vociferously about asset prices and what they could do to financial stability, with a special emphasis on unwinding QE:

“[I]in the assessment of a few participants, equity prices were high when judged against standard valuation measures. Longer-term Treasury yields had declined since earlier in the year and remained low. Participants offered various explanations for low bond yields, including the prospect of sluggish longer-term economic growth as well as the elevated level of the Federal Reserve’s longer-term asset holdings. Some participants suggested that increased risk tolerance among investors might be contributing to elevated asset prices more broadly; a few participants expressed concern that subdued market volatility, coupled with a low equity premium, could lead to a buildup of risks to financial stability.

“A few participants also judged that the case for a policy rate increase at this meeting was strengthened by the easing, by some measures, in overall financial conditions over the previous six months.

So the Fed is focused on asset prices that have reached levels that threaten “financial stability” – which is Fed speak for a bubble that might implode in a major crash that could trip up the financial system.

It wants these asset prices to ease down, and it wants longer-term yields to rise (as bond prices fall), along with mortgage rates and all manner of other interest rates. It wants borrowing to get just a little harder. And it wants risks to be priced in a little more. And it will likely pursue its very gradual tightening until it sees some success in that department.

The Fed also confirmed in the minutes that there are two possible policy actions it could undertake this year in the two remaining meetings with press conferences: there is unanimous support of “balance sheet normalization,” as it calls its unwinding of QE, with only timing still being discussed – September or December. And there is some opposition to a rate hike in September. So at this point, it still looks like the Fed might make an announcement about the kick-off of the “QE Unwind” in September. And another rate hike could be in the cards for December. With more to come next year.

When QE was started in late 2008, its purpose was to inflate asset prices. The “wealth effect,” as Bernanke called it. And it worked. Unwinding QE is likely to have the opposite effect. And markets have just started to react in the slightest possible ways, with stocks in recent days easing off but hovering near their records and with longer-term yields and mortgage rates ratcheting up just a little over the past few days. But it doesn’t look like these tiny movements are enough to satisfy the Fed.

A July rate hike for Canada is “in the bag.” The Bank of England and the ECB are scrambling. Read… “Tightening” Slugfest Erupts behind the Fed

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The market is just goading the Fed to stop. VIX needs to go to 40 before the Fed does something, otherwise the Fed will not take it seriously.

https://www.bloomberg.com/news/articles/2017-07-05/now-fed-officials-are-starting-to-wonder-if-the-vix-is-too-low

The VXN (Nasdaq VIX) is up from 11.5 to 17. Will the whole market follow?

A column in the Globe biz section two days ago opined that the BOC almost has to do .50 % next time to match Poloz’s new hawkish religion and catch up to US.

The Canadian banks were not happy with his last move: a .25 % cut.

Reality ‘ Disconnect ‘

That pretty much sums up the basis and foundation of every problem we’re now facing or about to face .

Reality Disconnect – Where on one hand you have the cold hard facts staring you in the face . On the other what everyone prefers to believe … with belief presently usurping the facts at every turn .

Hmmm … what was that little gem my ole philosophy professor/mentor once gave us ? Oh yeah ..

” Theory and belief are all well and good until they become crushed by the cold hard weight of facts “

I like the Mike Tyson version of that quote:

“Everybody has a plan until they get punched in the mouth.”

http://articles.sun-sentinel.com/2012-11-09/sports/sfl-mike-tyson-explains-one-of-his-most-famous-quotes-20121109_1_mike-tyson-undisputed-truth-famous-quotes

“In theory, there’s no difference between theory and practice. But in practice, there is.”

Jan van de Snepscheut

“It’s such a fine line between stupid and clever.”

David St. Hubbins

Hubbins, the patron saint of quality footwear.

The Virgin Mary isn’t selling anything these days. Probably an oversight.

Man plans and god laughs?

I prefer the German phrase, “der mensch denkt, Gott lenkt”.

And that has been replaced by “what the bots use as data points to buy and sell.”

Two or three weeks ago I commented that I didn’t think the Fed would ever raise interest rates significantly. My rationale was based on the fact that today the entire economy is dependent on cheap credit. Debt is no longer looked on as something to ever be paid off and everyone, from the poorest person with a credit card, to the top of the 1%, will not do well if interest rates increase significantly.

So clearly I am not the only one who believes this. What your article so logically shows is that the Fed is going to have to do a lot more than fractional interest rate increases per year and jawboning to get anyone to believe they will actually do anything significant to change the status quo.

The Fed has been filling the opium pipe for nigh on 10 years. And they wonder why people can’t see the real world?

The greatest misallocation of scarce resources in our lifetimes. Productive/Income-Producing assets and producers have been strangled in favor of churning and skimming financial paper.

Mr. Market is betting heavily against the Fed, and it’s a bet he’s likely to win. Ever since Paul Volcker left, the Fed it has been staffed by academics who love the adulation they receive. But none of them has the courage to “take away the punch bowl” and face the criticism. If they did, the party would have ended years ago when it became obvious that wealth effect was not having the desired effect on the economy. When Mr. Market pushed back, the Fed will cave.

The Federal Reserve FOMC couldn’t care less what fools in the markets are doing or “think” and has very clearly and transparently stated their position that the Federal Reserve balance sheet will be cut by around 50% between now and the end of 2018 and that the 3 interest rates that the Federal Reserve sets will move to the 3% range by the end of 2018.

OE, Yes BUT even 0% interest rate debt has to be serviced. When money is borrowed and mostly invested in non productive enterprises (mergers, acquisitions stock buy backs) or just out right consumption, that is a lot like eating your seed instead of planting it.. There will come a time when there just isn’t enough seed left (revenues/profits) that nothing can be done other than default.

Those who realize this will inevitably try and save as much seed (cash) as they can before it is all eaten up. Thus Fear will eventually over come Greed and the markets will crash… Just read Minsky. He was right on!

Are we there YET? Your guess is as good as mine.

Please correct me WS if I am wrong, but it is NOT the guessing of where rates go that drives this “lovers sedan” over “lookout mountain”, but the incentive.

The horse is long, long out of the barn – pain is coming. It is important to understand this point.

https://www.youtube.com/watch?v=5ct-D6DzvfA * See below signature

If I may, to illustrate, let us assume that fair rates for money are 10% for money (or something other than zero).

I know, maybe I just put the “decimal” in the wrong place (ahem). Or something.

But, taking this misplacement of the decimal as a baseline for discussion.

FACT: No business would ever invest in anything that yielded (according to their business plans – things that CAN’T NEVER go wrong **) less than was LOWER than the cost of money.

That’s dumb.

This is the low interest rate game – DUMB INVESTING 101 (and don’t start me about where I can put the decimal on this game).

At a high rate of interest, the economy is “held back” but only the most productive ventures are funded. For all the bitching, wealth is genuinely created, albeit at a slow rate (the rate of real opportunity – kind of complicated in real life).

At a low rate of interest, we get shit like Tesla. Or Amazon. Or shale oil companies. These companies raise HUGE amounts of money – at no cost – to do … what exactly? Cannibalize other businesses? Skim for the execs and upper employees? Destroy margins? Oversupply the market?

Buy up all the real assets left with free money so when the inevitable crash happens the core shareholders own the world?

And so on.

Low interest rates are (paraphrasing here) akin to cancer – they eat away at the REAL BUSINESS that produces REAL VALUE in the economy – until no one knows when to start a sandwich shop that is going to make 15% (and be VERY un-glamorous but successful with piles of hours and hard work) from the soon-to-be colonization of Mars. At a 0% bound, folks choose Mars over the sandwich shop – and real productive enterprise suffers (and jobs).

Checks are being written against society right now that WILL BE PAID.

SOMEONE is going to eat it. There is no FREE.

Buckle up.

Regards,

Cooter

* Forgive my spelling, but Paulo heckled me about Merle on my show a few posts back. This is one of my favorite Cash songs. The kind of stuff I might play – the stuff that is great and never gets played. :-D And … damn … if it ain’t apropos! 99 down, 99 a month! Yuk yuk.

** Yes, it is on purpose.

“everyone, from the poorest person with a credit card, to the top of the 1%, will not do well if interest rates increase significantly.”

This is certainly not true. “Everyone” is much too strong. Some people will do quite well, though perhaps not immediately. For instance, anyone with a savings account or a bond ladder (not selling, just rolling over) will benefit from higher rates.

But the details will depend on what else changes in addition (in consequence of) the interest rate changes.

Finally, keep in mind that higher interest rates imply lower overall levels of credit (per person, per unit of GDP, whatever). Over the very long term that that is actually good for everyone, for a whole bunch of reasons. Perhaps the largest of which is that it would halt the malinvestment bubble-bust cycles.

Interest rates will mean-revert, because that’s what they do, so the crucial investing question for anyone with either assets or debt will be figuring out how to get from here to there with as little damage as possible. Fortunately it will take a long time to complete the whole process.

These are uncharted waters , never before has there been so much liquidity injected into global markets. Possible reasons for a sanguine market reaction:

1.) rate hikes already reflected in current valuations (baked

in)

2.) markets realize that current weak economic conditions

will require additional easing down the road.

3.) The quantitative tightening schedule is minuscule.

4.) The feds are just “jawboning”.

5.) The quants haven’t adjusted their algos yet .

6.) Foreign liquidity is propping up markets.

what ever it is, the feds’s historical models will be challenged. Could they be losing control ?

It could be that The FED is unaware of the unregulated markets :).

http://www.isda.org/statistics/otc.html

There is 430 Trillion “notional value” sloshing about in there.

If The FED raises rates and some of those positions must unwind, that money will be piling into the markets, driving prices higher.

The FED probably does not model the OTC market, how could they? It’s all proprietary, unregulated.

So they are running the battle plans of the last war, acting on what they know.

In my mind, the Fed is taking very muted steps, all the while telling the market that the economy must be getting better, or they wouldn’t be increasing rates.

How should the market react? Things are getting better! Rates are still low! And won’t be going up much faster down the road!

???

Profit!

Great comments!

Who controls who? Market controls the Fed or the Fed controls the market? Both believe they do. I believe neither. It’s the economy that determines everything. Profit calls the tune.

Wikipedia says this about the Fed:

” It was created on December 23, 1913, with the enactment of the Federal Reserve Act in response to a series of financial panics (particularly the panic of 1907) that showed the need for central control of the monetary system if crises are to be avoided.”

Even if we assume that that’s the mission, has the Fed managed to avoid crises? Indeed it has managed to make every crisis more horrendous than the previous one. Hubris & delusion!

If FED were the only game in town, the unwinding of QE would have mattered. My understanding is that there’s a QE from Japan, China, and the Swiss bank. In fact, zerohedge listed how the Swiss bank owns a sizable chunk of Apple and more shares than Zuck in Facebook. If QE were to be unwound, wouldn’t the Swiss bank lose money? I am guessing that these other players will not let the market unwind. At least that is how I read the daily drops in the market followed by mysterious upticks with no news.

If this were true, there’s no such thing as quitting a QE mafia.

The Swiss will still probably make money on the rise in the U.S. dollar vis-a-vis the Swiss franc.

I don’t buy it. This is exactly what the Fed wants. If they didn’t then they wouldn’t be buying trillions in assets to inflate prices and keep interest rates low.

They are just frustrated that wages won’t keep up with assets. They created artificial demand but can’t figure out how to maintain it. Must suck being backed into a corner the say they are. Hope the whole system falls apart beneath their feet. Unfortunately, the middle class will be finished off in the process. Idiots!

Forget about what the Fed says. Just follow their actions.

“Just follow their actions.”

Indeed: 4 rate hikes so far. A plan to unwind QE, and that plan is now public. Only debate is when to kick it off…. that’s a lot of action. Last year, economists (including Bernanke) were saying that the Fed would NEVER unwind QE. How things have changed!

Yes, indeed they have in that the Federal Reserve has clearly done exactly what it said it would do!

A very good article. It is interesting that liquidity is being defined in terms of asset valuations. Perhaps this is related to collateral values. However I am not sure that asset valuations are a source of excess liquidity rather than a symptom.

The perception appears to be that the greatest risk to the economy is not the normal business cycle but an event effecting extended asset valuations which for the most part is due to the actions of central banks. The possibility of addressing the next downturn through negative interest policies and helecopter money is fortunately looking less realistic as an option. Therefore the only game in town is not inflating the asset bubbles any further, building up some reserve firepower in the form of higher interest rates and QE options with the expectation that very little can be expected on the fiscal side next time around. Though I suppose a large QE program does accommodate fiscal expansion.

By avoiding exuberant economic expansion, if that is an appropriate term in today’s circumstances, a muddle through may be possible. These asset bubbles are rightly seen as increasing risk and fragility in the system and hence the need to reduce accommodation.

The Fed in pursuing this policy seems to be forcing the other central banks to follow. A risk off tantrum is likely at some stage and some backtracking will be necessary.

The problem is the average American will spend their helicopter money on lottery tickets and booze.

“The problem is the average American will spend their helicopter money on lottery tickets and booze.”

Not all of us. I like more permanent things. I have some bare skin left, and some really gnarly tats would be so cool! If the helicopter drop was sizeable enough, I may even consider some more piercings too! Gotta keep those self-employed “artists” in business, ya’ know. Of course, anything else left over *could* be used for booze and drugs. But, you gotta get the important stuff paid off first.

“Gradualism” doesn’t inflict enough pain.

There’s plenty of time to game the system on the way up.

Different problem (inflation), but Paul Volcker’s treatment was sufficient to solve it: 20% interest rates!

https://www.thebalance.com/who-is-paul-volcker-3306157

It apparently never occurred to the “economists” at the Fed that inflating asset prices may not lead to an economy that works for everyone, instead of just the few. But these same “economists” never bothered to question their “wealth effect” theory, because their brand of economics is based more on faith than reality. Eight years later and they’ve only now realized that nothing they have done has worked! Why are these people allowed to make decisions they aren’t qualified to make?

“Why are these people allowed to make decisions they aren’t qualified to make?”

Look at who owns and controls the Fed, and who benefits from the Fed’s decisions (hint: not you) and you’ll have the answer.

You’ll have to look behind the scenes — not at the entertainment-disguised-as-news that’s being staged for you.

Precisely because they are nor qualified. As I read somewhere, not knowing about economy is a prerrequisite to work for the FED

“Why are these people allowed to make decisions they aren’t qualified to make?”

There is profit both in failure and in success, the “short” and “long” of management teams, if one likes to put it like that.

There is an additional twist on the “short” side in that Corruption is very hard to distinguish from Incompetence. I believe there is an art to it. The good “failure consultants” are never short of work or new opportunities.

It took me years of frustration and fighting against windmill to finally work this pattern out. You see this guy, doing fantastically crap procurements, stakeholder meeting with 30, 50 people in locations it is impossible to get direct flights to, millions going down the drain easy, his projects never delivering, always there is new money thrown into the pit, and yet, he is still there. Even growing his retinue of useless people.

He is there, Because, this is his job. He is basically “short” the business, feeding whoever is “long” on the consultants servicing his failing project. That person is probably on the board, judging from the fallout over the last time someone took it upon themselves to clean up the mess.

Once one sees the pattern, a lot of unnecessary work related stress goes away. It all taken care off. One just avoid having ones name on any of the paperwork, mail and meeting notes. In case of the eventual inquest.

When playing chicken with the stock market, the fed will always chicken out first.

one could have seen the wave would come with the gradual slight tightening and a discussion about going to runoff or selling down.

jeez. just another day at the beach, less cash lapping at the shore……though a banana peel might be lurking.

Simple solution all the FED has to do is lie about the jobs figures each month and state them on the extreme high side. That would take care of everything.

Japanese bonds are falling in value as well today.

The 10 year bond just went below par to join the 20 and 30 year instruments there as well.

Long way to under par for the 5 year, but now only ‘yielding’ – 0.05%. 2 year is at – 0.10%

Well, that didn’t last long:

“The Bank of Japan asserted control over the nation’s bond yields, sending borrowing costs lower with its first fixed-rate bond-purchase operation since February after a global debt selloff.

No bids were tendered after the central bank offered to buy benchmark 10-year notes at 0.11 percent, it said Friday. Yields dropped to 0.085 percent after having more than doubled in the past week, while the yen swung to a loss.”

Why wait until September to unwind their balance sheets. Why can’t they do it Now?

I’ll believe it when I see it. Yellen will never run out of excuses to keep screwing savers out of interest income or print more trillions in funny money QE for her oligarch patrons.

the feds might accelerate their proposed schedule to show the markets “they mean business” . in the interim the dollar weakens . go figure

The bond market is going to force Yellen’s hand. Investors are belatedly demanding more yield for securitized debt that is going to be printed away by the Fed and central banks. As bond yields start to soar, Yellen will have no choice but to hike interest rates correspondingly. And then it’s Game Over for the asset bubbles and and Ponzi markets created by QE-to-Infinity and ultra-easy credit.

Wolf,

No pun intended… but my first response to this article is:

“The Fed who cried Wolf”

But seriously, I do not attempt at all to find logic or reasoning behind any market activity.

This is actually good news. It means the markets may be able to sustain a more aggressive qe unwind. Last time the fed even hinted at selling qe the markets swooned and the fed had to back off. If the response to rates hikes is to lower the 10-yr yield, then all the more reason to start the unwind sooner and faster, until the yield start to increase again.

I still stand by my theory that the unwind won’t do much to interest rates or credit availability until the Fed’s balance sheet reduction exceeds the excess reserves (1.5tril) that banks have parked with the fed. Only then will a meaningful retraction in credit, and concomitant rise in yields, occur.

If the Fed inflates rates and eventually the markets crash 20% it will a good excuse for the Fed to cut again. The Fed is Wall Street, so I’m not certain why this is a point of confusion.

If you know that rates will be cut sometime in the next year (highly likely) and cheap money will floods the system to save you there’s no reason to liquidate your at risk positions in the market.

You just wait. Which is why no one is really panicking. The FED has raised a whole generation of Fed dependent traders who have no concept of value.

And if N. Korea explodes the Fed will cut and if volcanoes in the western USA blow the Fed will cut and if a kitten doesn’t get its ball of string the Fed will eventually cut.

I think the omnious tone set by many websites recently – ‘the Fed is getting serious!’ – is contradicted by all known facts of Fed past actions.

Clearly, you haven’t been through – or you don’t remember – the two most recent tightening cycles. Check out the one before the Financial Crisis. Or check out the one leading into the dotcom crash and the 2001 recession.

“Check out the one before the Financial Crisis. ”

On Feb 1, 2003 the nasdaq was at 1324.

On Sept 1, 2007 it was at 2596.

The Fed funds rate has not hurt stocks for a substantial period of time since the 1970s. Short term yes, long term not so much.

https://fred.stlouisfed.org/series/FEDFUNDS

After each of the last two tightening periods, there was a financial event that wiped out a lot of investors.

It is not unusual for asset prices to increase during the beginning part of a Fed tightening cycle.But during EVERY previous cycle of Fed tightening, I repeat EVERY, has ended in pain for financial assets before it is over

The downdraft in TSLA is just a small precursor for the move in the entire stock and bond market

i find it interesting and am attempting to follow some trends, in respect of the fact that global debt to GDP hit a new high of 327% for corporate personal and government debt.

Taking the fact that global average debt interest on this total debt is almost exactly 2 % gives you the inevitable mathematically correct figure that total global growth needs to b 6.52% in order to simply service that debt.

Also given the fact that very few countries including China are highly unlikely to match that growth level, and those that do claim high growth is almost certainly due to manipulated numbers, then you have to reach the inevitable conclusion that debt service can only be achieved either by liquidating assets or printing money or increasing debt further.

Only those countries with sufficient growth and low enough debt to GDP can possibly prosper, and the question in my mind is to what extent places like the US and euro area are now looking at those countries that have manageable debt to effectively force transfer payments from them by currency and other manipulations including debt manipulation as it does appear that this type of activity is ramping up.

No matter what, whether those responsible countries can protect themselves from machinations in the west or not, global GDP growth has no prospect of ever reaching a level over 6.5% and probably well over that as the global debt to GDP rises inexorably and is compounding by rising absolute and rising interest rate and risk factors at a frighteningly accelerating rate, meaning that it can take less than 3 years now before global GDP growth would need to hit over 10% to start to actually pay down any debt.

A complicated equation, but an answer would tell me where I want to be, how high the central banks could stand global growth requirements to balance the books, is it 20% of GDP 30% 100% before the system crashes and what amount would need to be printed to cover that shortfall.

Scary times.

I think anyone who believes that in any way a solution without a massive debt repudiation and global bankruptcy and meltdown coming is absolutely deluding themselves.

It is like the Ruby Red slippers. The FED has always had the power to control the stock market bubble and they do not need to use interest rates to do it. The FED has the power to change the margin ratio currently at 50%. Right now you can purchase $2of stock for ever dollar of capital.

If you want to see the bubble come out of the market, take away the “make believe” demand spurned by 50% margin and make the margin ratio 100%, where you can’t lever up with debt to purchase stocks.

My assumption is that the FED wants to preserve the stock market and asset prices while slowing speculation by resorting to threats. They will sit on their hands and raise rates slowly until something breaks.

Not sure why the Fed gets frustrated, they create the conditions for the market to ignore them. Look at Yellen’s testimony today. Basically let everyone know the Fed Put is guaranteed and perpetual.