A stock or bond market tantrum might stop the Fed in its tracks. But the opposite is happening.

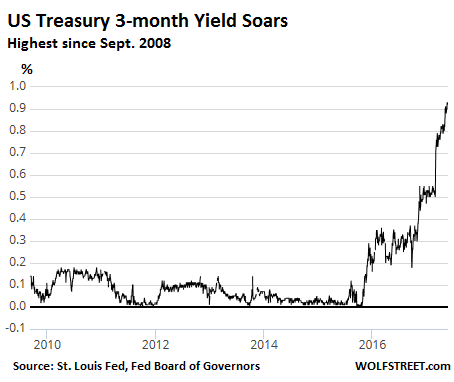

The US Treasury 3-month yield rose to 0.94% by late Thursday, the highest since September 2008. It reflects how the market views the Fed’s next action – to be announced after its meeting on June 14. The short-term Treasury market is attempting to read every quiver of the Fed’s lips, what Fed governors are saying on their speaking circuits, the minutes from prior meetings, and so on. And it sees a large probability of a rate hike on June 14:

This would mean that the FOMC nudges up its target for the federal funds rate by a quarter point, to a range of 1.0% to 1.25%. It would be the third rate hike since the election in November, one hike every other meeting.

Even one of the most dovish Fed Governors, Lael Brainard, said during a panel discussion yesterday that a brighter outlook for the global economy has shifted the risk balance for the US economy. These words are the kinds of signals the bond market feeds on.

And the minutes from the last FOMC meeting show that unwinding QE and trimming down the Fed’s $4.5 trillion balance sheet is moving closer to reality. QE was designed to drive up asset prices and bring down long-term yields, including mortgage rates. Now the opposite is being planned.

Currently, the Fed replaces securities on its balance sheet as they mature. So every few days, it buys Treasuries and mortgage-backed securities. Now the Fed is getting into the nitty-gritty of how it will trim down its balance sheet. The “staff” is working on it and gave a presentation on the “possible operational approach” at the last meeting.

The Fed would allow maturing bonds to roll off the balance sheet without replacement. But there would be “caps” to how much per month would be allowed to roll off so that the pace by which the balance sheet shrinks is “gradual and predictable,” according to the minutes. The caps would “increase” over time, and the draw-down would pick up speed. After this phase-in period, “the final values of the caps would then be maintained until the size of the balance sheet was normalized.”

So they have a plan. It will probably kick off later this year, but perhaps as soon as September, according to JP Morgan’s Chief US Economist Michael Feroli who worked at the Federal Reserve Board until 2006.

The Fed is removing “accommodation,” as it calls this, across the spectrum: at the short end by raising the target for the federal funds rate, and at the long end by allowing QE to unwind. This includes mortgage-backed securities, which would remove some of the support under mortgage rates.

It’s a momentous move. But markets brushed it off.

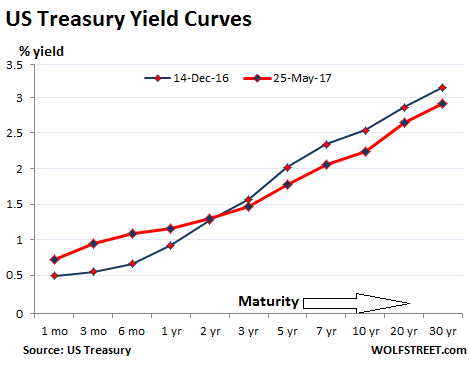

The bond market is going along with short maturities. Short-term yields, such as the three-month yield, have been rising in preparation for more rate hikes. But at the longer end, the bond market is going the opposite way. The 10-year yield and the 30-year yield have fallen. And stocks have hit new highs. Thus, markets are in fact loosening monetary conditions, rather than tightening them.

This has further flattened out the yield curve, with the 3-month yield rising from 0.55% on rate-hike day December 14, to 0.94% on May 25; and with the 30-year yield dropping from 3.18% to 2.91% over the same period.

The ten-year yield, at 2.24%, is also lower than it was on December 14. With the 12-month CPI inflation rate at 2.2%, investors are not even being compensated for loss of purchasing power (red line = current yields, blue line = yields on December 14):

A flattening yield curve is considered by some a sign of troubled economic waters ahead. There are a slew of reasons for this phenomenon of dropping yield at the long end of the curve in face of the Fed’s actions and plans, among them:

- There are doubts about Trump’s highly anticipated economic plan and tax cuts – the “Trump trade” – and fears that the goods won’t be delivered.

- Investors might be reacting to rising defaults in consumer debt, such as auto loans and credit card loans, or to the seven-month stagnation in Commercial and Industrial loans, all of which point at potholes for economic growth down the road.

With stocks at all-time highs and borrowing costs ultra-low, financial conditions for companies have actually eased since the Fed stopped flip-flopping in December and got serious about tightening, and they have eased further since unwinding QE has morphed from a crazy idea into an action plan.

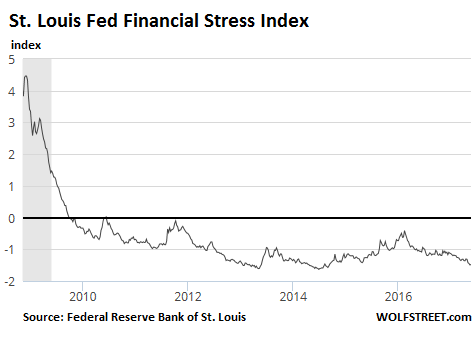

This is corroborated by the St. Louis Fed Financial Stress Index which indicates that “financial stress” in the markets is extremely low. The black horizontal line (zero) denotes “normal financial market conditions.” Values below it “suggest below-average financial market stress.” And now they’re near record lows and dropping as if QE infinity were still the law of the land:

As long as markets are not getting the message and as long as financial conditions in the markets are getting looser, instead of tighter, the Fed has all the more reasons to proceed. A tantrum by the stock and bond markets might stop the Fed in its tracks. But the opposite is happening.

After surging for years, quant hedge funds – where trading is done by machines, not humans – now dominate stock trading. Read… Will Quant Funds Trigger the Next Stock Market Crash?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The ECB/BOJ/SNB/BOE are printing around $150 billion a month– that’s a big tantrum-stopper for stocks. When the ECB quits it’s “game over”– they’ll supposedly taper starting late this year and stop completely by mid-2018. Between now and then though all bets are off. Right now it looks like October ’99 out there!

The ECB will not stop printing … the eurozone will end if they did. Expect it to continue, expand, and end only when it can’t continue …. years and years from now. Lots of people are still true believers in govt integrity. The Eurozone can’t exist on fiscal honesty. ECB QE is their only and last resort to keep the plate spinning.

Don’t believe me? Run a thought experiment on how rates would change without ECB QE and how euro-governments would react if they not only had to pay them, but if they had to live within their means. ECB QE is just more kick the can.

@cdr I think Germany will force the ECB to stop, under threat of Trump tariffs.

If the ECB stops, the euro countries will have to pay their way with normalized interest rates and budgets that can afford to pay them. (Eurozone Moral failure)

Target2 imbalances will continue and Germany will have to change in unknowable ways to stop sucking all the cash from the southern countries … the ECB loans the southern countries cash to make up the short fall that end up with the Germans. No way to pay the loans back. (Eurozone Design failure)

The ECB has already tapered its asset purchases by €20 billion a month this year. There will likely be another taper announcement this year, perhaps before the German elections.

I hope you’re right. I see ECB QE as the ultimate moral failure and a logical band aid / temporary fix / stalling tactic / hail mary for a bad design.

Wolf, I think the Dirty little Mafiosi at the ECB, is try to give the Impression to germans, he is listening to them, about ECB policy, and its safe to vote Not Merkel.

The acid test will be what the ECB does AFTER the German election’s. And also whether Italy is allowed to get away with illegal state Aid (Aid with out bail in) to at least some of its bank’s. After the German election’s.

My old man is a retired auditor for TX – VN Vet, scrappy oil field white trash, and masters of Finance from UT – we didn’t talk for many years, but sorted things out somewhere along the way – maybe we just got older.

Our consensus is that Germany is doing financially what they failed twice to do militarily.

Her on WS, we know it isn’t going to work out – but me and my old mans thinking is at least past that mile marker.

Would love to hear what other here think along those lines.

Regards,

Cooter

I’ve heard that theory. It’s probably not true. Perhaps in the design of the Euro, Germany thought they would be king of the hill due to their productivity and moral superiority while the rest of the Eurozone sent them money due to flaws in the design of the Eurozone (target2 imbalances).

The invention of negative rates might tilt the theory more in your favor. The end result of them is to confiscate savings to replace tax payments that don’t cover public living expenses. However, negative rates hit Germany worse than the rest of the Eurozone, so the net effect is to return flows back from Germany to the south.

In theory, this actually closes the loop and might make the Eurozone viable economically … Germany repays target2 imbalances by having savings confiscated due to negative rates. However, ECB QE is needed to keep rates low in the first place and no Eurozone country lives within its means … meaning public debt is constantly monetized. This will undoubtedly continue forever until it can’t. Draghi will spin new reasons why it must go on and a gullible public will think it’s backed by integrity as opposed to being public finance fraud.

Actually, this was foreseen at the time the Eurozone was created but ignored because the Utopians thought it would kumbaya itself away somehow. Now its smoke and mirrors and BS and Europeans who like having a free lunch while keeping the plate spinning using “Whatever It Takes”. The rest of the world is basically stupid for going along.

Cooter, your comment meets exactly the point. The Eurozone is ‘Grossdeutschland’ and a giant redistribution system of taxes collected from all citizens and channeled to the elites of each country. The money is then spent on luxury cars from Germany. This system by-passes most of the population, which has to pay taxes, yet receives only a fraction of it back. The challenge to keep the system running is the revolting popultion, which kicks most of incumbent politicians out. Therefore, the Bureaucrats have to fix the system, so that there is no going back. Too bad the UK did smell the rat and bailed out early.

Not true, but circumstances have worked in that direction.

1. Germany was quite a sick economy when it entered the Euro: stiff labour market, and unification costs. It tackled those problems.

2. Since WW2, German leaders have tried hard to be a good European citizen, deferring to France whenever possible.

3. At the time, it had a leader that was quite capable of understanding the hegemony problem, and had hands full with reunification.

The crisis management (including crisis of her own creation) threw all those policies out of the window.

CDr I’m not so sure The weak Euro has helped businesses in the EU over the last couple years

Systemic Fragility Abounds

The stock market is remarkably thin, 55% of the stocks on the NYSE are below their 200 day moving average. While just 4.37% of S&P 500 stocks are at 52 week highs and nearly 62% of ALL NYSE stocks are below their respective 50 day moving average.

This despite the facts that the SPX hit a new all – time high and complacency (VIX) is ultra low at a single figure!

What could go wrong? Party on Garth.

“Mr. Travers, how can you be bearish with the market so stiff?” and Travers

retorted, “Yes! Th-the s-s-stiffness of d-death!”

The BOJ and Swiss Central Banks are said to be propping equities when they fall. The Fed has a reputation to be namby to an excessive degree. No matter what they do to tighten, it will come across as more QE. They will apply the lightest touch for the longest time and tighten in name only for as long as they can. This, however, is an improvement to a year or more ago.

The public finance fraud commonly known as ECB QE will keep the cash flowing until they can’t and this will last and grow for years more.

Algos need cheap credit and a fast turn to make money. Others just react to the appearance of the Fed put, aka Bulllard and day to day market support so that nothing ever falls.

To affect the financial markets even a little, it will take much higher rates applied with surprise and a selloff of the Fed Balance sheet without equivocation or namby limits to even hint at making a difference so that the Fed didn’t look like a captured entity. Providing Bullard doesn’t make some promises at the same time.

Every morning I awake with the hope that today things will normalize. I expect to be disappointed for years.

Markets expect the Fed and its peers to support them indefinitely and without reservation. They bet billions on it daily and appear to win daily.

‘Markets’ are defined by me to mean the fast money paper flippers who need cheap credit and massive amounts of borrowed money to make a buck.

I think of myself as a saver who has been eviscerated by Fed monetary policy and as someone who the Fed not only ignores, but is probably contemptuous of.

If the Fed wanted to look as if they were in control, In June they would raise rates by .25% and comment about the need to keep the increases coming possibly every meeting until they see a reason to stop down the road. They would also announce an unequivocal balance sheet reduction policy where everything runs off to $0 with the possible exception of short term transactions to accomplish short term accounting and bank support transactions.

Of course, Bullard represents the group-think and my idea is nothing but a waste of electrons.

The Banque Nationale Suisse (BNS) has a different structure than most central banks.

Without entering into the details, it’s controls the currency but it also acts as the Cantons’ hedge fund. This is not something they do on the margin: it’s written in their statute and one of their duties.

The BNS may indirectly prop up stocks because their purchases are so massive, but its first and foremost scope is to make money which is then distributed to the Cantons at the end of the fiscal year. If they could make money shorting and selling securities, they’d do it in a heartbeat.

A big part of the reason the BNS was forced to float the franc against the euro was because they were accumulating tons of euro denominated assets which turned out to be only marginally profitable and which risked blowing up their balance sheets: again, the BNS cannot “print” euro any more than the Banco de Mexico or the Reserve Bank of India.

The BNS has to be profitable for the simple reason it risks punching a hole through the Cantons’ budgets, many of which are completely dependent on the BNS for even basic services such as paying their police officers’ salaries.

Switzerland has no problem issuing debt at negative yields these days, but due to the peculiarities of Swiss policies running US or even Spanish-sized deficits at federal level would be a sight to behold. From a safe distance.

To reduce confusion The (BNS) is commonly referred to, as the SNB.

The SNB wanted and still wants to take on more gold.

The cantons citizens said no.

There are only 4 currencies in the world worth ‘Holding” if theUS $ gets to much Dumpinstability injected into it, we will be left with only three, Yen, Sterling, and CHF.

You know the old joke about residents of French-speaking Cantons refusing to speak German (technically Schweizer Deutsch) and residents of German-speaking Cantons pretending not to know French? ;-)

Its a bit like the CNY/RMB thing.

The new red guards, from the unannounced new cultural revolution, know its listed on all the Western and Major Board’s as CNY.

But they insist on using RMB, to be difficult.

Because they can.

Which sows confusion.

Pathetic really.

When talking banking and finance, which is full of confusing and conflicting acronyms, one should not go out of ones way, to sow confusion, simply as one can.

Swiss Franc hands down !

Why ? The British £ is a losing proposition in light of BREXIT and the Japanese Yen though somewhat stable is being held up by mere threads , Elmer’s Glue and a whole lotta wishful thinking

Not to mention the fact that some 60%+ of the worlds wealth is invested in CH banks .

Which is to say … same as it ever was [ thru two world wars , a worldwide depression and multiple recessions ] And the same as it ever will be .

The only problem with the Japanese Yen is the level of government debt in Japan.

The only problem with Japan is the shrinking population.

People have a huge amount of savings. The various governments and quasi-public entities have a huge amount of debt.

Most debt is held internally and most funding is domestically based.

The biggest problem Japan faced was the huge flow of funds out of the country to pay for increased energy imports because of the shut down of its nuclear reactors after the Fukushima disaster. The numbers were huge and had the situation not changed it would have caused a crisis.

Two events in the market have prevented the problem from becoming worse:

1. Reactors are slowly being brought online. A couple more were just approved last week so that trend is continuing and will eliminate more demand from the market and a fall in fund outflows for products.

2. The fall in the price of energy has reduced by a huge amount the cost of imported energy.

Two additional factors that also need to be considered in regards to Japan’s economic condition are:

1. The fall in the population which has both negative and positive impacts. One positive is that are more than enough jobs for young people entering the market unlike many other western economies.

Another is that reduced population results in less demand for energy and other imports and reduction in fund flows out of the country.

2. A huge inflow of tourists into the country. With well over 20 million tourists visiting Japan this has created a huge market internally for goods and services. When I lived in Japan the number of visitors was around 4 million or so. A huge success.

We’ll help them out in that regard later this year too.

As long as Japan can keep enough funds flowing into the country to service its debt there will be no problems for the Yen in that area.

The level of debt though is huge and one wonders what value the Yen should trade at in order to to be able to fully service and retire that debt.

With the ‘energy’ crisis I thought that 150 Yen per US$ was about the right answer. Now I have no idea…………

(By the way contrast Japan with the USA:

1. Japanese people have lots of savings – ordinary Americans have very little, if any.

2. America has a huge trade deficit – Japan usually runs a surplus.

3. Both governments run huge deficits and have huge levels of debt. Most Japanese debt is held internally. Most US debt is held overseas.

4. There are very few student loans in Japan. The USA has a huge amount of student loans outstanding. IMO many USA educated university students are really, really dumb. IMO Japanese are much better educated than Americans. A waste of money.

5. Japan has a reasonable national health insurance system and a reasonable health system. The USA’s is out of control in terms of cost and coverage.

6. Japan has a well implemented system of border control. The USA’s is a train wreck.

7. Japan has a very, very small drug problem and a very, very small gang problem. The USA? Well, to put it plainly – it’s disgusting.

Japan has crime and its generally under-reported, but nothing like the USA.)

So which is better positioned for the future: the so called country with the lost decade or the down in dumps USA?

All eyes are on credit – when it genuinely stops expanding – things are going to go south and not before then. WS has it right – housing is a biggy, so are autos – great blog (even if my two cents is poorly bet).

Right now it is incredibly easy to buy old cars, new cars, houses, and hell – i haven’t seen it, but someone out there has probably securitized pot bonds so we can pull forward weed demand in CO. Think of the profits!!

This sort of thing fails when it runs out of air – when – who knows – but it will.

I have been wrong, wrong, and more wrong about markets for years now. I am right in principle. But I can’t, nor can anyone else (without insider info). In the long run I will be right – but I will also be dead in the long run too.

Neither are good trading opportunities. I don’t try to trade, I try to get out of the way – and figure out how to prosper after the fact.

How many investors here are thinking about how to deploy capital after this Titanic hits the iceberg and all sorts of very linear, knowable, in-your-face s**t hits the fan?

Wife on my butt … gotta go …

Regards,

Cooter

Here are some examples of Titanic.

My newspaper was 10 times fatter than normal Thursday. I thought is was weekend sales. It was tax certificates for unpaid real estate taxes. I knew some of the names and ask two on that list what gives…I know you have the money. The reply was ‘why pay the tax of 10 grand when I can make so much more in the markets than what ever the interest rate bid is on the certificate…beside I have 3 years to pay and it takes several certificates to make a claim on my house”.

So there you have it. Across the country you have the same folks doing the same trick. Look at Connecticut for example, so bad they can’t float a bond. City after city with budgets that can’t be met, including pensions they can’t pay. My county….they can’t afford to hire another school bus driver until the RE taxes get paid.

The disconnect between the (now dangerous) real world and the FED’s and stock market fantasy worlds could not be farther apart.

Indeed, this year may well blow up in an unexpected way.

A good point worth mentioning , Tax certificate sales are a good point worth mentioning and certainly seem to be under reported . I think i counted 7 thousand last year here in citrus county FL on a similar publication. I don’t know if this a “normal” number or not but the data would be a good leading indicator on economic health. These properties are probable not mortgaged since a mortgage payment contains escrow amount for property taxes

Are you saying they do not pay their property taxes until they are threatened with repossession?

Reply to Maximus Minimus

Yes, exactly. And one of those people is a retired judge who over saw some foreclosures. How is that for making sense.

The idea that you would put your home up as collateral ( the tax certificate) for holding up an over priced stock market bubble, is just as dumb as using your home as a ATM for the same thing. But that is what low interest money temps folks to do.

The market will go south, likely hard, and when it corrects, will these fools have the money to buy the certificate or enough to go rent somewhere else and start over again.

This is in Florida, but it is nationwide and just like the 2007 crisis, this one will catch the country by surprise.

Thanks FED for all you do (sarc)

Credit will exist as long as people are willing to actually extend it and liquidity exists. People with too much debt will slow it up a little, but not stop it entirely.

A working capital shortage caused most of the last recession. Had sufficient liquidity existed and had banks been willing to lend, the great recession would not have happened.

The stock market crash was just a side show, but loud and powerful cry babies and fantastic, made up economic theories created QE and ultimately captured central banks world wide. It was a magnificent example of never wasting a crisis. One might even postulate that the working capital shortage was intentional so that the end result we now live in happened at all.

– A flattening yield curve is actually a good sign (investors are increasingly willing to take risk) whereas a steepening yield curve is a bad sign (investors become less willingly to take risk).

– Since say early 2017 the yield curve actually didn’t move that much (neither a clear steepening or flattening). It signals that the market(s) haven’t made up their mind in which direction the economy/markets are going in the (near) future.

– One Wolf Richter knows my opinion regarding the FED and the 3 month T-bill rate. And that opinion clearly is different from Wolf Richter’s opinion.

Big players in the market don’t really take any risks because it OPM. The recklessness is only going to increase until it can’t continue and that doesn’t seem to be anywhere on the horizon. Even Jon Corzine, who stole/borrowed 1.6B of his customer’s money, is back in the game. When there is no downside to the recklessness it will continue.

I don’t think of the markets as markets anymore. It’s a virtual reality game played in real time. Nobody ever really dies, they keep coming back, and the score keeps increasing. The real losers are the ones who don’t get it.

REGARDING : “It would be the fourth rate hike since the election in November, one hike every other meeting”.

I was somewhat startled when i read this . It seemed an overly aggressive hiking timeline . maybe i am wrong

but here are the rate hike history dates

DEC 2015

DEC 2016

MAR 2017

https://en.wikipedia.org/wiki/History_of_Federal_Open_Market_Committee_actions

Indeed, it be overly aggressive, so to speak :-)

Thanks

But from a very very low base

Well the people in the Australian Forex market are certainly ignoring the Fed and a host of other negative economic data out of Australia, China, and the USA.

In December 2016 the A$ was around 1.40 to the US$. Over the next month and a half it soared to $1.29 to the US$ as iron ore surged to around US$93 per tonne.

Since then it has weakened slightly, but traded consistently under 1.35 only to be bought hard every time it has fallen under 1.36.

Data the market is ignoring in regards to the exchange rate are:

1. New car sales are soft with the two biggest listed dealerships having downgraded profit expectations.

2. The unemployment rate is was down to 5.7% from 5.9% the previous month, but the increase in jobs was in the area of part time jobs replacing full time jobs. Hours worked over the past six months and year have fallen. Those pert time jobs just are not the same as full time jobs in terms of number of hours worked and pay.

3. Iron ore stockpiles at Chinese ports have risen to the highest level in 13 years. The price of iron ore has fallen from that February high level of US$93 to US$60 per tonne. Shipping data from Australia indicates that exports of iron ore to China are also increasing.

4. Housing construction has fallen at the fastest pace in 16 years in the first three months of this year. Residential construction fell by some 4.7% and was the biggest quarterly decline since December 2000. Total construction for the quarter fell 0.7 per cent.

5. Consumers are going to get hit with higher energy prices…………….. AGAIN.

Imagine that – in a low energy price environment and in a country that has huge coal and NG resources the price of electricity keeps going up. The price rises are finally going to start affecting retail grocery prices as this is the 3rd largest cost center after rent and wages for them.

5. China’s credit rating was downgraded – the A$ initially fell and less than 12 hours later was actually higher. Ho hum. Nothing to see there.

6. Retail sales fell in March and retail sales growth is the lowest in five years. This is against a background of the Australian population increasing at a rate of over 2% a year.

7. The budget was released and the lower end of the income brackets are going to get hit with a one half percent increase in the Medicare levy while the top end doesn’t have to pay the 2% ‘deficit reduction’ levy. So in effect they get a 1 1/2% income tax reduction.

The new levy will also start at lower rates of income – A$21,000 a year. Gotta make those low income scum pay.

This is similar to the last budget when the government reduced the tax on those making over A$80,000 a year and eliminated the energy supplement for new pensioners and those on other welfare payments.

8. US – Australia bond spreads are the lowest since 2001 with the 10 year spread now at 16 basis points.

9. The banks are increasing rates on interest only RE loans and the big five banks are being hit with a 6 basis point levy. Of course the banks are screaming bloody murder and vow to pass the cost on to consumers. The smaller and regional banks were not hit with the levy.

So what happens? Big bank shares plunge and then one of the ratings outfits DOWNGRADES the smaller and regional banks thus in one stroke eliminates any competitive advantage gained by the move. The big banks ratings were unchanged as they would be ‘backstopped’ by the Federal government here….TBTF.

10. Automobile production ends in Australia this year.

And finally,

11. Governments at the Federal and state levels are hitting foreign buyers of Australian real estate with new taxes, charges, fees, and other restrictions.

This is one area of the economy that has provided support while others tanks.

Really a dumb move when the economy is tanking in other areas.

IMO the A$ should be heading south big time, but then what do I know……….everything is perfect in the wonderful world of OZ.

Unlike china and Europe.

Australia is still a place, people with medium wealth, along with every destitute economic migrant and terrorist on the planet, want to go to.

I’ve been telling everyone the AUD will dump for the last 2 years.

The old saw: The markets can stay irrational longer than you can stay solvent.

Others on HotCopper have been saying the same thing.

Article in the Age newspaper today pretty much reflects much of what I have been saying, but the A$ once again was bought hard this afternoon after falling to $1.348 it zoomed back to 1.3434……………..

http://www.theage.com.au/business/markets/australia-getting-left-behind-as-dollar-shares-lag-20170530-gwg68v.html

The FED is still at an emergency level interest rate and the market is calling its bluff. It seems to me that it would take a significant number of .25% rate raises to make any significant difference get to any real interest rate.

Yellen will never run out of creative excuses to keep punting on interest rates. Bilking savers out of interest income and forcing them to play in Wall Street’s rigged casino is too lucrative a racket for the Fed to ever give up of it’s own volition. The Fed will not hike unless/until it’s hand is forced by the bond vigilantes.

Should the Fed try to sneak in a 50bp hike while it can? If it is trying to “normalize” rates, signal to market participants that asset price inflation needs to slow down, and build a cushion for accomodating next recession, June would seem to be a good time.

If the US enters a recession in 2018 (or sooner), they need to get rates higher while they still have time.

A 50bp hike would be a “monetary shock,” which is precisely what some folks are now advocating. They think it will take this type of monetary shock for markets to take notice and start tightening monetary conditions. These people say that if the Fed keeps going in these small increments, markets will continue to ignore it, and the Fed will keep going, and do so too far too long because markets never react. And one day, there will be a sudden huge market reaction that might turn into a crisis, which everyone wants to avoid.

150 would shock them 50 would only upset them for a few hours as they are simply to low.

50 will only bring you into the 1.25 -1.50 % band still way to low to shock markets for long.

Markets will react went old and new medium and long term rates start to meet.

As you FSI index shows there is still way to much cheap money around out there, looking for work, way to much.

Good point. People forget how ‘trained’ traders are today.

A trader in their early 30s ( and many many are in their 20s), only know low interest rates and the fact the FED will protect the markets at all cost. A 150 bp rise would be unthinkable.

I see nothing but 0.25 raises until it’s time to cut again. Why would the FED suddenly become concerned about asset inflation when asset inflation was the whole point of the low interest rate policy?

Sorry, don’t buy the fact that people’s salaries are rising by miniscule amounts as being the reason they’ll raise.

Any raise people got was instantly consumed in a blazing furnace of health insurance and housing costs!

Yes. That plus running the balance sheet to $0 via maturities would be a running start. That would be a good start.

Of course, this is just dreaming. Anything they do will be mitigated by Bullard as often as needed. They want the appearance of change with as little actual change as is possible. Their words and actions disagree with regularity. Their actions speak to working at the glacial speed of molasses and doing nothing if they can get away with it. All to protect the fast money paper flippers and central banks that prop the equity markets, and of course, keep the ECB from whining about how they are hurting the ECB free lunch.

I think the Fed can get away with doing nothing as long as people think the current conditions are good, and hopefully things will change on that front. The election of Trump is an indication that things are not good, but the Federal Reserve has managed to stay out of the limelight so far. The average Joe has trouble understanding supply and demand, let alone monetary policy. It will take some time for sites like this to produce higher thinking by the public, that allow leader like Trump to figure things out.

I am surprised there aren’t more mainstream articles lambasting the Fed about the unfairness of it. What they are doing is plain immoral – denying people the ability to save for future necessities, sacrificing the economy’s long-term viability to avoid short-term pain, promoting bad financial and life decisions, creating financial slavery conditions for Millennials, providing windfalls to speculators, telegraphing their actions to the top 1%, creating two economies, and feeding the leeches on Wall Street.

Add it all up and it smells like crime to me.

I’m not so certain that “everyone” wants to avoid a crisis Not convinced of that at all Removing foil hat now

100 bps increase should shock the market.

A 100bp hike would bring everything to a halt, including mortgage lending. It would unleash political, economic, and financial fireworks that would be difficult to endure. So maybe better not

:-]

Maybe “shock Therapy” is exactly what is needed. Despite jawboning and small increases Mr. Market hasn’t even blinked so far. Left to his own devices he will keep inflating this financial balloon until the results are catastrophic. It’s like a car whose brakes have failed. It maybe dangerous to jump now, but it will be worse later.

Brexit was supposed to wreak havoc in the global financial system. Markets hit all time highs.

A certain former Reagan budget director warned his readers to get out of the casino at the beginning of the Fed tightening last year. Market at all time highs .

1% increase in rates ? I agree. That would be tough to digest, especially for today’s fragile and leveraged Auto industry with existing delinquencies at 3.82%

There are two separate economies in the U.S. and only one of them is overheated.

A market that can’t take a 100 bps is a faulty market anyways. Especially since the base is super low. If today’s rates for the 10 year is 6% and above then I’d agree that 100 is excessive, but the market itself is telling the Fed that they are behind the curve.

Responsible central banks acting in the national interest do not exist anymore. Instead, we have “former” Goldmanites with one mission: to serve as the oligarchy’s chief instrument of plunder against the 99%. Everything the Fed and central bankers do make perfect sense when seen through that prism – especially their engineered pump & dump scams every eight years or so that loot and asset-strip the middle class and transfer their wealth to the Fed’s .1% accomplices.

Bingo

Globalization is a big part of the picture, too. The redundants (deplorables?) attempted a rebellion but the Fed’s still in the saddle and there is no effective protest because the Fed delivers us from evil in the tiny minds of most voters. There’s scarcely a sound coming from the Capitol, so our representatives are also genuflecting. Only an accident can change the narrative and I have no clue what that would be.

The Federal Reserve cue card:

Step 1: Create fake money stealing value from everyone

Step 2: Loan the fake money to people with interest

Step 3: Take people’s stuff when they can’t repay the debt

Step 4: Get government to enforce our fraud

Step 5: Plunder humanity

What I find pretty amazing , it is how lying and being a crook is now an accepted and expected behavior from elected official, politician, salesman and bankers.

I understand now why ancient society were cutting the tongue of liar in order to restore social justice and morality.

You cannot believe anything from anyone anymore. I expect them to keep printing and trying to match the exponential debt curve. I expect bigger and bigger banks profits because they are the ones having access to the printed money first, therefore are the beneficiary of inflation.