It’s always associated with a recession: last time, the Financial Crisis.

Over the past five decades, each time commercial and industrial loan balances at US banks shrank or stalled as companies cut back or as banks tightened their lending standards in reaction to the economy they found themselves in, a recession was either already in progress or would start soon. There has been no exception since the 1960s. Last time this happened was during the Financial Crisis.

Now it’s happening again – with a 1990/91 recession twist.

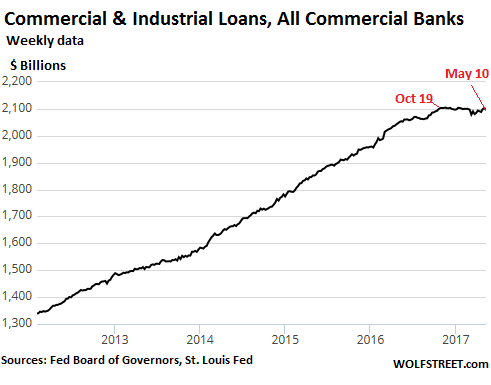

Commercial and industrial loans outstanding fell to $2.095 trillion on May 10, according to the Fed’s Board of Governors weekly report on Friday. That’s down 4.5% from the peak on November 16, 2016. It’s below the level of outstanding C&I loans on October 19. And it marks the 30th week in a row of no growth in C&I loans.

Based on the Fed’s monthly reports, C&I loans outstanding at the end of April, at $2.095 trillion, were down a smidgen from October’s $2.098 trillion and were down 4.3% from the peak in November. This marks the seventh month in a row of no growth in loans.

This chart shows C&I loans outstanding at all US banks going back to 2012. Note how that 30-week stagnation-period is unique in this time span:

Since the Financial Crisis, the mantra has been: credit growth no matter what. Businesses have been exhorted to borrow, money has been cheap, and borrow they did. There have been periods of four or five weeks of stalling C&I loan growth, only to be succeeded by a vigorous surge. But after ballooning in this manner for six years straight, C&I loans have now languished for 30 weeks. And it’s not the oil bust; banks are lending to the oil patch again.

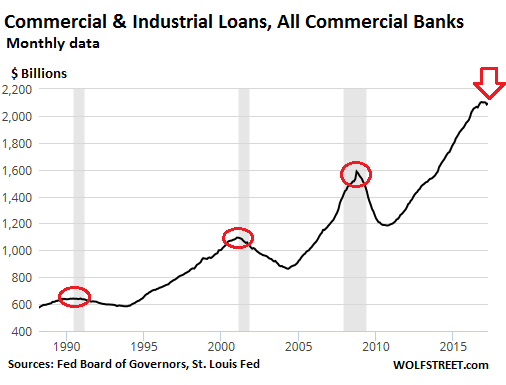

C&I loans are tightly connected to the real economy. They’re an indication of what businesses are up to, from a shop needing a loan to buy a piece of equipment to the multinational funding its receivables. C&I loans show whether companies in aggregate are expanding their needs and activities or whether they’re curtailing them.

The chart below shows how any significant decline of C&I loans outstanding in the debt-addicted US economy is associated with recessions. Note the turning points:

What happened during the Financial Crisis was, let’s say, special: Credit froze up, banks stopped lending, businesses stopped asking for loans, and C&I loans fell off a cliff. More typical scenarios would be the prior two recessions. In 2001, C&I loans peaked in February 2001 and then declined. The official recession began in March 2001 and ended in November 2001. But C&I loans kept falling until May 2004.

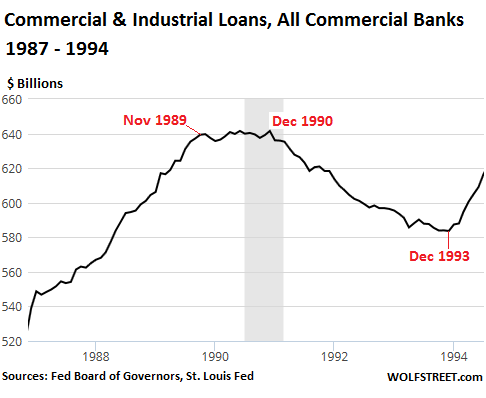

It’s difficult to see in the above chart what happened around the 1990/91 recession due to the destruction of the dollar and the growth of the economy since then. So below is a chart for that period, showing the C&I action in all its glory. C&I loans outstanding flattened out for 13 months. The official recession began in July 1990, eight months into the stall. In January 1991, C&I loans began to decline. The recession ended in March 1991. C&I loans finally hit bottom in December 1993. So the “turning point” was actually a “turning year”:

Going back in the data to the 1960s, we see that similar patterns played out over and over again.

Where does that leave us today? In the first quarter, GDP grew at a desperately anemic 0.7% annualized, meaning that at this rate, growth for the entire year would be 0.7%. But it’s not a decline. This type of stagnation would be far below the lamentably anemic 1.6% growth in 2016 and the standard issue projection by the Fed of around 2% growth in 2017. The second quarter looks better though there isn’t nearly enough data so far to support this assertion with conviction. Nobody is projecting a recession.

The experience of the 1990/91 recession could turn out to be instructive. A while after the recession was over, the NBER, which calls the official recessions in the US, determined that the recession began in July 1990, so eight month after C&I loans began to stall.

The current seven-month stall is a big red flag – though it is unlikely that history repeats itself in that level of detail. These stalling C&I loans don’t fit at all into the rosy credit scenario. Something is seriously wrong. So economists might be assuring each other that C&I loans are now a meaningless indicator, that times have changed, that C&I loans no longer matter, or that they’ll begin to surge once again. And who knows; we live in crazy times with way too much liquidity, and they might be right. But there are other signs out there that speak of changing dynamics.

The #Carmageddon data is just relentless. Read… Used Vehicle Trade-in Values Sink, Hit New Vehicle Sales

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

First quarter 2017 Nominal GDP was 0.7 percent…Since 2008, even when including ALL forms of credit expansion, a case can be made that Real GDP has been essentially recessionary when TRUE inflation numbers are factored in.

I’m still trying to figure out how anyone believes we exited the last recession

It’s a tale of two Americas. The one untouched by adversity and the other absorbing all the pain. For the losers it will not be over until they are made whole, brought back to where they were before it all started. And since that is unlikely for most, it will continue.

are you the same Petunia that contributed to the discourse on the peak oil forums?

No.

What risk?

Interest rates were used to price risk, but under the current interest rate regimen, the risk – pricing mechanism is broken.

The CB’s have been trying to force price inflation when there is no wage inflation. The majority of the population is experiencing high debt loads, with attendant wage deflation, resulting in shrinking demand and stagflation.

The gorilla in the room (that most ignore) is still debt.

Cross – asset correlations are at or near multi – year crises extremes. It is this inter – connected web of shadowy financial products, that amount to +$70 trillion in G10 debt, which is used as collateral for +$700 trillion in derivatives!

The dollar reflation has now failed again and there is nothing the Fed can do about it., as there is no additional marginal banking capacity. The diminishing marginal productivity of debt has reached its vanishing point. The is reset is imminent and will be epic.

I honestly wonder if the numbers matter any more.

Next up a flood of liquidity to keep the shell game going.

This story should have ended years ago and yet……….

We will not have honest markets or sound money as long as the criminal private banking cartel known as the Federal Reserve controls our money issuance.

You are wrong about this..” we will not have “..

We already don’t have honest market..its all manipulated..

The numbers don’t matter any more..

“The numbers don’t matter any more…”

Until… They do!

http://www.srsroccoreport.com/the-everything-bubble-code-red/

You just have to package this message to an easily digestible soundbite for the plebs, and will you have a revolution.

The CL & the stock markets have the same look.

Both have reached a mad climax, and from here banks asset will fall.

A fast, sharp downtrend , that will take few good years, or decades,

to evolve. Banks CL and other loan will shrink, not because they will get fully paid, or because they refuse to lend.

They will have plenty of write off to do, forced to clean their books.

Write offs have a different name. They are debt jubilee for the forgotten men, the new debt slaves.

When the smart money rich, will lose some money on loans, they will still make plenty on government bonds.

The usual suspects, as usual, will be the people in between.

They will lose their retirement, saved money and few other asset, to keep them running when they can hardly move.

“They will lose their retirement, saved money and few other asset, to keep them running when they can hardly move.”

That is already, and in fact has been, happening for some time. Wolf has posted many articles about this.

When I look at those charts and I place top and bottom bands on them, my eyes popped. This is going to be a free fall like the first crest of the roller coaster ride.

Perhaps the Banks will loan again once the politicians realize that credit is not expanding because of the Consumer Financial Protection Bureau (Dodd Frank), and vote to repeal a good chunk of it.

As long as they replace it with Glass stegall all should be well.

We can either manage the economy (more exactly the financial “services” sector) or the economy will manage us. We do not allow reckless or DWI driving on our public roads, so why do we allow the equivalent in our economy?

Financialization.

The FIRE economy – Finance, Insurance, Real Estate

Upsidedown. The financial sector used to service the economy. Now the economy services the financial industry.

The Titans of FIRE better hope that Johnny/jane Q. public don’t .. uh .. ‘trip and bit down HARD … as they continue their force fellatio into penury …..

lol

Gives new meaning to; “Off with their heads”

Historically, the financial sector accounted for 5% to 8% of the economy. Today this is closer to 40% utilizing debt as the foundation. What could go wrong?

When you look at the stock market indexes, you will see where it took off, beginning nineties when Greenspan took over the FED, and deregulation was on. The real estate is a result of that deregulation, too. Many other countries followed the lead – not to be left behind in the GDP game.

These are the last days of Western economies, the engine is revving but its not moving much, Economists now understand that all market based economies follow a bell curve. Policies have little influence on this scenario.

That’s like saying that “There Is No Alternative”, which is totally wrong. Policy matters. Economy and policy always go hand by hand… and the sad thing about the west is that it has willingly let its advantatge over the rest of the world go.

“On a monthly basis, …”

All of the graphs in this article show the total loan balance, a cumulative number, right? The text is mildly ambiguous about this at times. Said in another eay, the sampling interval is monthly, the number is cumulative.

Total balances outstanding at that point in time. The weekly numbers are at the end of the reporting week. The monthly numbers are at the end of the month.

I agree, the way I phrased it was vague. I have now adjusted the text in several places for greater clarity. Thanks.

Wolf:

Do you have comparative aggregate debt of all kinds vs. assets of all kinds, say, over the past 30 years. And in the asset category, paper assets, that is- paper claims.

Someone probably has this data (or estimates of it)… I’d have to piece it together laboriously, and it might never be complete.

Note the increasing magnitude and slope of the roughly symmetrical increase and decrease in C&I lending peaks in the 2nd chart. This correlates with increasing debt over the same time period. It would be good to see a real (inflation adjusted) curve as well. Based on these trends, the next downturn would be expected to be especially severe. I have two theories here: 1) The Fed + other CBs cause more extremes in the economic cycle that if they didn’t exist otherwise, and 2) The severity of the contraction is proportional to the amount of credit/debt incurred (all cohorts) on the way up. We’ll know more in probably less than 1 yr. Note that under (1) the inference is that CBs are not only useless, but actually detrimental to the economic system of nations.

The public theory is that Central Banks can “smooth” the hills and valleys of the economy. In practice Central Banks look after their ilk. If this wasn’t so, then our economy would be booming.

WTH aren’t stock and bond markets part of inflation calculations?!

Why is 20% unemployment considered full employment? Why is debt not included in GDP figures? Why is no distinction made in national accounts between the real economy and the Financial Industrial Complex that parasitizes it? Why is there no accounting for environmental assets?

It is because those who have power in the world want it to be this way.

” Why is 20% unemployment considered full employment? Why is debt not included in GDP figures? ”

Its all about which numbers they chose to focus on . For instance with unemployment the numbers given only reflect those still eligible for UE benefits .. not how many people are actually unemployed .

Thats the problem with statistics especially when given out of context . You can make them say anything you want with a flick of the wrist or wave of the magic wand

The the real problem though is the sad fact that the majority of we Americans no longer so much as know what Context is … never mind comprehend why Context is so damn critical and important

Why is “Government” “output” part of GDP? The income captured by government edict from the private sector certainly isn’t dollar-for-dollar output in the economy.

IMNSHO the problem with GDP, and the earlier GNP, in the current socioeconomy is highly misleading as it has gradually become “debased.”

This appears to be mainly an accounting problem and the way it is calculated. Specifically it is defined to be the the monetary value of all the finished goods and services produced within a country’s borders in a specific time period.

The major problem is that the “monetary value” is calculated by summing the “monetary value” as reported by the producing organizations. Not only is this subject to “errors” and “abuse,” e. g. Enron, this also assumes the externalized costs of the reporting organizations disappeared, when in fact these costs are being paid by someone, sometime, somewhere, somehow. “Cost externalization” [and tax evasion] has become a fine art, and it (and Enron style fraud) appear to be grossly inflating the GDP/GNP.

One example is our highly subsidized arms industries. Another is the growth of industries such as fast foods and big box retailers which rely on minimum [below living] wage employees, with the result that a significant fraction of their labor costs are paid by the taxpayers through food stamps, section 8 housing, and social services medical care.

One example is Wal-Mart, which on paper earned an 11 billion dollar profit, but whose employees received an estimated 11 billion dollars in social assistance, which does not seem to be included in (subtracted from) the GDP calculations.

We need a new definition of GDP [net gross domestic product?], based on holistic or aggregate accounting of the entire economy, which includes *ALL* costs, e. g. governmental and externalized, as well as verified monetary value produced.

It all starts with the Fed- what are the goals of the Fed? Who benefits?

This is not to say the financial situation lies only with the Fed. Even if they had goals that were centered around a vibrant middle class, you still would need something other than an idiotic public and politicians to match.

Because you wouldn’t be considered a serious eCONomist if you thought outside of the box.

I believe it’s just conventional thinking. We think of inflation as a situation where prices have got out of line with values, and things have started to “cost too much.” With financial products like stocks and bonds, the price is the value, so it follows that there’s nothing to get out of line. QED no inflation. Like I said somewhere else, if oatmeal were a financial product, and the price of oatmeal doubled, people would be delighted at the opportunity to eat oatmeal that was twice as valuable as it used to be.

The mistake is thinking price, per se, reflects value. Amazon at 187 times earnings means you had better hope for a greater fool. Strange things happen when the price of money (interest) is choked by government edict. (The Fed only exists because of government edict.)

Price doesn’t represent value it represents demand. When you get a bargain you know the value is greater than the price. Same thing when you know you are paying too much, you are expressing demand not value. Pairing price and value is a desired outcome but rarely happens. Inflation can be expressed as an excess of demand.

So if the manufacturer jacks up prices by charging the same amount for less product, thereby creating inflation (price relative to quantity), to keep the same profit despite decreased demand…how does this equate to price is proportional to demand? People are being made fools as they fail to realize that they are creating “artificial demand” because they are paying more for less.

“Inflation can be expressed as an excess of demand.”

Or shortage of supply deliberate or otherwise.

Hence the WTO free trade housing bubbles, in countrys that are consider a “stable” place to hide money. By the populations of devious nations.

Aided by the WTO, that forced many of these places to open their housing markets. To unregulated foreign investment.

Proof of this can be found in the Philippines. Where Foreigners can not wholly own stand alone family houses. Industrial and agricultural property’s, or the land under either. And No bubbles in those markets. (How strange no???????)

The only part of the Philippine property market, to see anything likely the bubble seen else where.

Apartments, which foreigners can own 100 %.

PT,

I never said price is proportional to demand. A seller can price anywhere they want and a buyer can buy or not. Shrinkflation is a price increase but you don’t have to buy, I frequently don’t, but sometimes I buy anyway. You are correct that when buyers pay more willingly they are contributing to inflation.

d,

You are correct that inflation can also be expressed as a shortage, artificial or otherwise. That’s why I used the word CAN.

Follow-up.

C&I loans are short-term loans for operations and cap ex. to businesses; not for stock buybacks, for example. These are then one of the few loans being used for actual business expansion, which hasn’t happened much since many Cos. have instead done stock buybacks with cheap long-term debt instead of using the money for cap. ex. This (C&I) loan type then seems like a good indicator for actual business conditions on “Main St.”. If C&I loans are topping out, then that’s a pretty good indicator on the real economy.

There’s so much malinvestment in the (unreal) economy due to ultra-low rates and easy money/excess liquidity that it’s hard to know what’s going on based on other “loans and investments”. The natural interest rate is higher, but we now have “unnatural” rates. Price discovery is also unknown, for now. Do the Fed and other lunatic Keynesians really think this will end well? Been there. Done that! From bubble to bubble to bubble… Madness.

“Oh, what a tangled web we weave…when first we practice to deceive.” – Walter Scott, Marmion

“Insanity: doing the same thing over and over again and expecting different results.” – Albert Einstein (misattributed) – Narcotics Anonymous

“You cannot spend your way out of recession or borrow your way out of debt.” – Daniel Hannan, Member of the European Parliament

1) http://www.dailynews.com/opinion/20170519/record-debt-easy-money-a-bad-recipe

Record debt, easy money a bad recipe

By The Editorial Board, LA Daily News

Posted: 05/19/17, 4:54 PM PDT | Updated: 2 hrs ago

“Total household debt reached $12.73 trillion as of March 31, eclipsing the previous record of $12.68 trillion set during the third quarter of 2008, the Federal Reserve Bank of New York’s latest “Quarterly Report on Household Debt and Credit” revealed.”

“While the debt bubbles began to re-inflate after the aftermath of the Great Recession, the composition of that debt has changed, with mortgage debt making up a smaller share and debt from auto loans, and especially student loans, much higher.”

2) https://mises.org/blog/six-graphs-reveal-big-problems-student-and-auto-loans

Mises Wire

Six Graphs that Reveal Big Problems for Student and Auto Loans

03/26/2017

Jonathan Newman

“In fact, the numbers make it look like the housing bubble was almost exactly replaced by new bubbles in education and cars.”

“Of course, this is more of an intended feature than a flaw of the Fed’s monetary policy since the housing bubble popped. Expansionary monetary policy can only replace bubbles with new bubbles. Malinvestments are not totally liquidated, but shift from one sector to another. Consumer debt is not directly paid off, but transferred from one type to another.”

Total mortgage debt is a little less than it was in 2008 but so too is the home ownership rate.

Also, the population has grown a few per cent since 2008 but if we factor in mortgage debt written off as well as the mortgage holders that had their Principals reduced, i would guess that debt per mortgage holder is not that much less in real terms ( maybe 5-10%) than it was at the peak in 2008.

Not only that, i would bet that homeowner equity levels are still hovering at or near record lows.

Overvaluation, excessive debt and slow growth is a very disturbing combination.

With all the retail bankruptcies I would expect commercial loans to be written off. Wasn’t it the fact that all these companies were over extended with debt what took them to bankruptcy in the first place, even more than lower sales. Nobody is looking to expand these days, so a contraction is/was to be expected.

Is there any data that separates student loan, debt level and delinquency rate between those individuals who have obtained a degree and those who have not and probably never will obtain a degree. Those people without the degree but have the debt will have a big problem paying it back. It would also be interesting to require schools to post loan amounts and delinquency rates. That information might make some people think twice about taking on the debt.

That commercial and industrial loans chart peaking out at about 2.1 billion tells me the economy has been firing on all cylinders the last couple of years.

Or it could suggest that when interest rates are zero all those net present value evaluations of business investments are now ‘good investments’. Do businesses really follow NPV as slavishly as it appears???

Is net present value worshiped as a kind of delphic oracle?

Or, as in the case in the real economy, even if you didn’t charge interest at all on the debt, the project wouldn’t produce a payback to even recover the capital spent.

It is only in the momentum of the economic flywheel where, when the crowd keeps buying, do prices rise enough to recover capital/debt with interest/profit (for some, especially the front runners).

– I would like to point to Steve Keen’s work. He came up with the following formula:

GDP = change in debt + income

He multiplies that formula with “change in” and then the formula becomes:

change in GDP = change in (change in debt) + change in income

Now let’s assume that the “change in income” is Zero, then the formula becomes:

change in GDP = Change in (change in debt).

In other words when one wants GDP to grow then debts need to accelerate (for ever).

Using this formula one can argue that the US is already in a recession because the growth of debt is (close to) zero.

Sources:

http://www.debtdeflation.com/blogs/

(Keen held a number of presentations and those can be found on YOUTUBE)

That “debt increasing forever” idea has occurred to me, in a less structured way than in Keen’s mind. If it were sustainable “forever”, all wealth would eventually be concentrated in the control of creditors.

“In other words when one wants GDP to grow then debts need to accelerate (for ever).”

This can only work if the “Debt” is invested in something “Productive”.

Debt, invested. In Paper Assets, or metals, is not productive. And that is where so much of the “Debt” has been “Invested”.

“Using this formula one can argue that the US is already in a recession because the growth of debt is (close to) zero”. ?????????/

Is it ?????????

The US is borrowing huge Amounts via Bond Issuances In Europe.

This ” Borrowing” (Debt) is not all in the US stats.

“If it were sustainable “forever”, all wealth would eventually be concentrated in the control of creditors.”

No

Debtors.

As all the creditors would have. Is a fortune, in “IOU’S”.

When everybody owes, you.

You, are the one, with. A problem.

This time is different :-)

No … actually its just another SNAFU in the merry-go-round of life .. repeating the same mistakes over and over again albeit with a minor twist here and a slight variation there … but still the same as it ever was .. because we learn nothing and ignore history e.g.

” Todays mistakes and errors are yesterdays history forgotten or ignored “

Gasoline demand started dropping towards the end of Obama’s term before the election and continues today. Is it possible you’re in recession and the government isn’t acknowledging it?

According to the economic reports compiled by John Williams at Shadowstats, we never left the recession that started at the end of the W’s term. That is far more believable to me than anything the government says.

Our Soviet-style CPI and BLS inflation and unemployment stats do not correspond to the reality ordinary people can see all around them.

This must be what the final days of the USSR Empire of Lies felt like.

“According to the economic reports compiled by John Williams at Shadowstats, we never left the recession that started at the end of the W’s term.”

Try 2000 which was actually part of the AFC of 1997.

This whole mess has been slopping round, getting worse since then, as too many debts were not written off, then.

Just a the current Euro banking issue’s in, Italy, France, and Spain, have their roots in the greek frauds that started the Euro crisis, which is Still truly not over..

As again the write off’s and Bankruptcies can. Has been kicked and kicked whilst the kicker prayed for a miracle off growth, or inflation.

Not willing to admit the Zombies being kept alive in Asia and Europe by the can kickers. Are sucking the global economy dry.

china is the biggest offender in this. Until Zombie over capacity is rectified in china. The whole world will remain sluggish as these chinese Zombies are dumping, killing those healthy non chinese companies.

china does not continue this policy by accident. china will not reduce supply until it owns, or has destroyed, all western competitors of any consequence.

The west will have to force china to do this, or allow itself to be owned by china.

Currently it still looks like, owned by china. Is the only option on the table.

Free trade is good, as long as it is fair, and balanced.

china has no interest in, fair, balanced, free trade.

Mao to the CCP

“We are going to totally dominate this planet. Without fighting a major conflict to do achieve that.”

That was Maos, objective. It is still Mafia State chinas objective.

“If the American people ever allow private banks to control the issue of their currency, first by inflation, then by deflation, the banks…will deprive the people of all property until their children wake-up homeless on the continent their fathers conquered…. The issuing power should be taken from the banks and restored to the people, to whom it properly belongs.” – Thomas Jefferson in the debate over the Re-charter of the Bank Bill (1809)

That’s you, Janet Yellen. You and your ilk were what the Founding Fathers warned was going to happen to us.

It’s probably another blip, a little bump in the road to heaven. I expect the new iPhone will sell in historic quantities. There will be the usual many new cars stacked up at the fried chicken window. Happy hour will be elbow to elbow. If perchance consumption should flag then I expect the bobbins to double that Fed balance sheet with QE4-7 as variously predicted by Rosengren and Bullard. There really is no limit to what they can do with their computer models. I believe our savior Bernanke indicated deflation was simply a failure of will. So buy the dip, stocks have room to run.

There was a period from November 1998 to May 1999, however, with *almost* zero C&I loan growth not leading to a recession. After that period, solid loan growth continued for over a year.

https://fred.stlouisfed.org/series/TOTCI

Thats the American slow down forced by the 1997 AFC. Which is where it all Started.

talk about pushing on a string , almost $1 trillion increase in C&I loans post 2012 , 600 billion increase post last peak

and anemic GDP growth. These loans are of a short term nature and are collateralized, to be used for working capital or capex, but apparently has not fueled any organic growth. What ever happened to a company financing its growth via retained earnings/profits ?

Illusory wealth and prosperity in a world increasingly full of spin and illusion it seems.

Life in the midst of a bizarre debt cult stumbles on…

The USA and UK have entered the same kind of necrotic financial environment the Japanese entered a couple of decades or so ago.

But as long as the value of their houses keep going up (the best way it seems to get elected), few seem to care.

Wolf: how do you think the dollar will fare against other currencies over various time frames given the failure of credit to grow as you described in your article ?

Thanks

What we are preparing for is a change in the Constitutional regime. West Coast Hotel/Carolene Products is over. We have a much better test for which facts are rights. The Constitution will be over thrown if so much power over so many facts remains in the political system. The scrutiny regime simply does not work.

So look for new rights in medical care (that is just around the corner), housing and other facts.

In short, the political system will not be allowed to threaten people’s survival.

Finance will also be redefined.

Big deal !

These charts and numbers mean nothing anymore.