The Fed is way behind the curve, but at least it now sees the curve.

Retail sales in February were lousy, and even lousier after inflation, though it was reportedly the warmest February in 100 years, without a big winter storm keeping the all-important consumers cooped up at home instead of shopping.

Total retail sales, including online and food services, edged up 0.1% to $474 billion in February, from January, the slowest increase in 6 months, the Commerce Department reported today. This came after an upwardly revised 0.8% jump in January. General merchandise sales and auto sales showed negative “growth.”

These numbers are adjusted for seasonal and calendar factors, but not for inflation. We’ll get to that in a moment.

On a year-over-year basis, not seasonally adjusted, total retail sales in February rose by $9.5 billion, or 2.2%. Gasoline sales alone soared by $7.2 billion, or 22%, on a juicy 30.7% price increase (more in a moment). And sales at non-store retailers jumped by $3.4 billion, or 8%.

Without those two factors – gasoline price increases and non-store retail sales – total retail sales would have fallen by $1.1 billion from a year ago. And this still doesn’t account for inflation.

As consumers had to spend more on non-discretionary items, such as housing and healthcare, discretionary items got hit: sales at sporting goods stores, general merchandise stores (particularly department store sales), and electronics and appliance stores fell, as did auto sales.

The delay in tax refunds – the IRS has been trying to get its arms around large-scale problems of identity theft and fraudulent tax returns related to certain tax credits – can be blamed for some of that debacle. These tax refunds are immediate spending money for most people.

Inflation can be blamed too: As prices rise in things consumers must have, they cut back on things they don’t necessarily need to have. When prices rise in non-discretionary goods and services, such as healthcare and housing, consumers cut back on discretionary items.

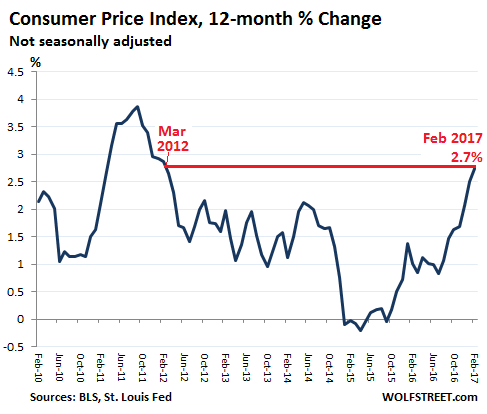

And prices are now rising, particularly in services. The Bureau of Labor Statistics reported today that the Consumer Price Index for all urban consumers (CPI-U) rose 2.7% in February from a year ago, the biggest 12-month increase since March 2012:

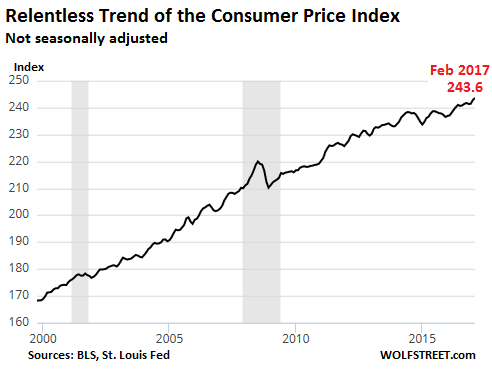

Despite years of scaremongering about deflation, there were only few dips in a relentless upward trend of inflation that is now accelerating. This chart shows the Consumer Price Index, not seasonally adjusted, going back to 2000. Since 2010, CPI has increased 12.8%:

Core CPI rose 2.2% year-over-year. This strips out food and energy. While prices of “food at home” edged down 1.7% year-over-year, energy prices jumped 15.2%. Within that, gasoline prices soared 30.7%. And this too hit people in their pocket books.

Prices of used cars fell 4.3%, which is helpful for used-car buyers, but a phenomenon the new-vehicle industry and auto lenders, particularly those targeting subprime borrowers, have been dreading for a while. Used car values represent the collateral of the loans and trade-in values for new-car sales. Ripples are already spreading through the industry.

And here is where inflation hurts consumers the most: Services. That’s where consumers spend the majority of their money. Prices of services (less energy services) rose 3.1% year-over-year. This includes shelter, up 3.5%; medical care services, up 3.4%; and transportation services, up 3.6%.

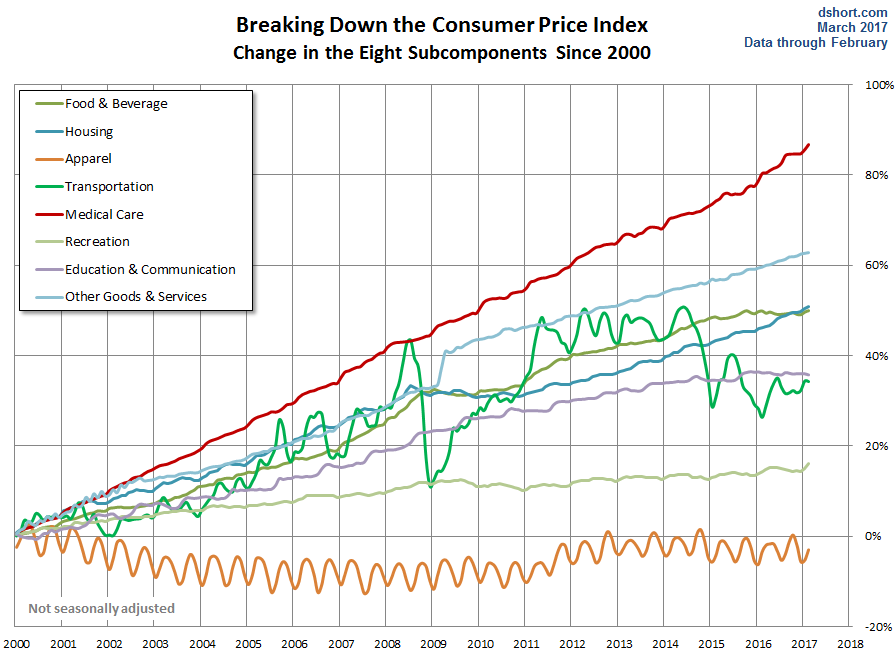

This chart by Doug Short of Advisor Perspectives, shows inflation trends for different goods and services. Healthcare (top line, red) has skyrocketed 87% since 2000:

The Fed is still way behind the curve. Its target for the fed funds rate is still low, despite three mini-rate hikes since December 2015, including today’s. At 0.75% to 1.0%, the target rate is still highly stimulative. And it has been outpaced by inflation.

If the “effective” fed funds rate is 0.9% going forward, it will imply a real (inflation adjusted) fed funds rate of negative -1.8%. Even the 10-year Treasury yield, currently between 2.5% and 2.6%, is below the rate of inflation and no longer compensates bondholders for inflation. Inflation is outrunning them all. There is a term for this phenomenon: “Financial Repression.”

That’s why the Fed is a mile behind the curve. But at least it has now acknowledged seeing the curve in the distance.

Mortgage rates too are behind the curve since they’re mostly a function of long-term Treasury yields, which are behind the curve. They all have a long way to go. But mortgage rates have begun to rise, from their historically low levels.

Fixed 30-year mortgage rates averaged 4.5% in the week ending March 10, the Mortgage Bankers Association reported today. This is the highest rate since April of 2014. But by any standard, rates are still very low, given that inflation is at 2.7%. And they’re likely to zigzag higher.

Everything will now be seen in the light of inflation: savers might make a little more money as rates edge up, but that will be more than swallowed up by higher prices. Inflation will eat dividend yields. And it will eat into wages. These are income streams consumers count on for their spending money. But these income streams are not keeping up with price increases. So consumers either cut back where they can (discretionary spending), or they borrow at rising rates to fill the holes, thus building up an increasingly costly debt that will down the road raise their costs of living even further.

Inflation can have a pernicious impact after years of a super-low interest-rate environment. As markets adjust to higher rates, our super-inflated asset prices across the board, and especially in highly leveraged sectors such as residential and commercial real estate, are likely to struggle for years to come.

But with impeccable timing, after a blistering 7-year price boom in commercial real estate, and just when it hit the ceiling, foreign investors jump in at record pace. Read… Foreign Investors Pile into US Commercial Real-Estate Bubble

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The red line…how appropriate!

verb

verb: red-line

1.

drive with (a car engine) at or above its rated maximum rpm.

“both his engines were redlined now”

2.

refuse (a loan or insurance) to someone because they live in an area deemed to be a poor financial risk.

noun

noun: red-line

1.

the maximum number of revolutions per minute for a car engine.

The automotive term you’re defining is spelled redline [one word] Whereas the phrase used here ; Red Line [ two words ] is defined as ;

” The Red line, or “to cross the red line”, is a phrase used worldwide to mean a figurative point of no return or line in the sand, or “a limit past which safety can no longer be guaranteed.”

Or for a more detailed definition as well as the origin(s) of the phrase ;

https://en.wikipedia.org/wiki/Red_line_(phrase)

And yet despite everything … the Stock Markets are once again on the rise . Kind of makes you think that maybe somehow the economy’s failure is Wall Street’s gain ?

As long as stocks continue to hold up, the Fed will continue to raise rates. It’s only when stocks begin to tumble in a serious manner that the Fed will get second thoughts. Today’s rally is one more reassurance for the Fed that it can continue to raise rates.

I wrote about this before, and it keeps getting confirmed…

https://wolfstreet.com/2017/03/02/stock-market-dow-30000-assures-fed-rate-hikes/

What is your opinion of David Stockman’s opinion on that factor – which is essentially a 350 Billion draw down in cash at the Treasury since October?

https://dailyreckoning.com/mystery-treasurys-disappearing-cash/

Personally, that is the first data-centric opinion I have seen since the “y-uge” ramp that makes any sense at all.

But, I have been calling it wrong for years and years now – sort of used to it – just looking for perspective.

Regards,

Cooter

I saw that too. I guess the administration wants to be in a position of strength when the debt ceiling issue comes up. No money means a higher ceiling. To infinity and beyond!

The president directly or indirectly is forcing the fed to abandon ship????

Wow for a minute I thought you were about to say the fed was willing to drain liquidity.

My bad!

Bigger chucks of interest rate hikes until the fed balance sheet MUST be taken from john q. Jr. In the next decade

Rinse repeatttttt….

I think Doug Short’s chart looks about right. The real story is that there is a segment of the economy that has been adversely affected by the chart, and a segment that couldn’t care less. The divide in the country is between those that look at the chart and get disgusted, and those that don’t need to care.

I think his chart looks about right, too, but I don’t think the divide in this country is where you think it is, as both my conservative and liberal friends are frustrated by the impact of this chart.

The divide in this country lies in both social issues and the opinion on who is equipped to deal with the chart above (if anyone).

Yep but Petunia will never admit that LOL. She is blind. Its always the Gov or bankers fault when folks make their own bad decisions. The game has always been rigged and Trump or the Fed wont change that. So few learn reality.

Until then I rent my properties to those who can pay gay or not unlike Petunia.

Personal attacks are inappropriate on this site. This is not ‘fight club’ or Twitter or Facebook or main street media. There personal attacks are common with or without cause or facts.

The wisdom that Petunia has demonstrated over the last year is, as always, on target.

MI,

Thanks for your kind response.

TR,

Liberal policies are destroying the greatest nation on earth. Eventually, it will reach you as well. Enjoy what you have, while you can.

“Liberal policies are destroying the greatest nation on earth.”

Should read

Liberal policies, Combined with a Globalised Vampire Coprporate (Currently allied with china) owned duopoly, are destroying what is left, of a once great American nation .

The rmbs market had been getting crushed for weeks when housing prices lost 8-10% “over night?”

Congress bailed out homeowners twice before Fannie and Freddie went under….

And than they made a single accounting change and the rides started up again……..

What accounting change they going to use when ” mark to fantasy ” stops being the golden rule?

One man’s chuckle is another’s belly laugh!

Okay. Let’s see. Autos (20% of total sales) are down January and February.

We know Restaurant comps were down 2.7% in February.

We know the shopping mall story at this point. We know Costco, Walmart and Target are reporting declining y/y profitability.

The ususal bright spot : Non store retail up 8%. – Not exactly firing on all cylinders.

Housing costs and medical may be playing an even bigger role in this slowdown than people think.

“Housing costs and medical may be playing an even bigger role in this slowdown than people think.”

It hit a wall. But thats what happens when prices are ratcheted up 300-400% over the long term historic trend. Now the real pain begins as prices return to long term historic levels. At least for housing.

Bottom is a long way down.

Notice that these charts NEVER include taxes, the single largest expense for the majority of people. Gee, I wonder why…

This inflation is transient. Painful, but transient.

Do you think the stock market is in a bubble?

Do you think housing is in a bubble?

If you answered yes to both (or either), and you think inflation is the big problem… you’ve got some serious cognitive dissonance going on.

Pointing to the immediate inflation we’re experiencing is completely missing the forest for the trees. Stock market crash, housing crash, problems in credit & oil… if you believe any of these things are on the horizon, deflation should be your biggest concern.

Never conflate and confuse inflation with rigged markets and grossly inflated and fixed prices.

Prices have a long way to fall my friend.

Yes, but most Americans couldn’t care less about the stock market. They have no money in it. And it barely impacts the real economy – on the way up and on the way down. But inflation impacts the real economy in myriad ways. If it is not at least matched by wage increases, it will cut into consumption in a big way.

Interest rates and yields follow the movements of inflation over time. What will the housing market do when 30-year fixed rate mortgages run at 6% with today’s high home prices? That will impact the real economy. And commercial real estate too. Both of these markets have engendered a construction boom that is funded by cheap debt with expectations of high selling prices. None of these highly leveraged equations work in a scenario of rising inflation and rising interest rates.

I’m not one bit worried about deflation. I’ve been through three huge crashes since the 1980s, and we had consumer price deflation on a year-over-year basis for only like three quarters or so. Deflation isn’t a thing in the US. I wish it were. When money gains a tiny little bit of value or remains stable instead of losing value, all kinds of good things start to happen, including rising consumption because wage increases won’t be eaten up by inflation (OK, over-indebted speculators and governments will have a harder time, but so be it … they should have figured this out before).

Oh, and as the second chart in the article shows, inflation is never “transient” in the US. It’s a permanent fixture with a few moments of reprieve.

Housing inflation seems transient, based on the collapses we’ve experienced in past decades. This time it seems a big bandaid was applied that enabled rent sskers, I’m no expert but it’s doubtful wage increases have kept pace?

What about people’s 401Ks and IRAs Those are in the stock market

Yes, but people don’t spend this money until after they retire.

Perhaps i should not bring this up, but Mish Shedlock seems to be a long term die hard believer in an impending deflationary US economy.

Real US GDP growth has registered at 1.35% annually over the last 10 years. That looks deflationary.

US stocks, bonds and commercial real estate have climbed a lot. That appears inflationary.

IOW, i have no clue.

“Deflationary” means CPI actually declines, and year-over-year inflation rate is negative. The 1.35% annual average over the past ten years is a positive number, so inflationary. 0% would be neutral. -1.35% would be deflationary. But there were a few quarters of deflation mixed into the 10 years followed by some quarters of strong inflation (over 4%).

Mish and Dan Amerman had an inflation/deflation debate years ago–I think it’s still on Mish’s or Dan’s webpage–and Dan wiped the floor with him. Mish had to finally admit that he was wrong primarily for the same reason all the “deflationists” are wrong, i.e. they are calling the falling of asset prices after a crash deflation. It is not.

Deflation is a decrease in the money supply. Inflation is an increase in the money supply. These are monetary events, not price events.

Prices are the reflection of the money supply and a lot of other things, therefore measuring inflation/deflation by using prices is difficult, and can be purposefully deceptive.

Wolf is 100% correct, deflation, properly defined, has rarely happened in the US economy since the 1930s, and hasn’t happened on a yearly basis at all.

The raison d’etre of the FED is to create inflation not to fight it. They are great at their jobs.

“Inflation is always and everywhere a monetary phenomenon.” Milton Friedman

@Marty

“Deflation is a decrease in the money supply. Inflation is an increase in the money supply. These are monetary events, not price events.”

So despite many areas of the Eurozone being stuck in a deflationary rut for years since the global financial crisis, they aren’t actually experiencing deflation because the supply of money went up. That’s what you’re arguing.

It’s wrong, unless you take the very narrow view that inflation/deflation is simply a monetary event. In that case, sure. Money supply up = inflation, money supply down = deflation.

Ignore velocity of money, ignore demand side factors, ignore savings rates.

Let’s say another crash hits, and people stop consuming and begin saving more. Less demand, lower prices. And people get laid off. Less demand, lower prices. And oil plummets due to aforementioned lack of demand; lower prices. And the Fed responds by jacking up the money supply, yet because of the crash, and lack of confidence, nothing much changes. Prices continue to drop.

We experienced hyperinflation after 07-08 according to your definition. It’s a bad definition.

Falling prices is a good thing. A very good thing.

Remember….. Nothing accelerates the economy, creates jobs and raises the standard of living like falling prices to dramatically lower and more affordable levels. Nothing.

smingles,

This is not *MY* argument, or some kind of personal idiosyncrasy. This is question of definitions and the definitions of inflation and deflation were widely accepted in econ, finance and biz until the US went off the gold standard. I vividly recall my high school text book in econ giving these very same definitions.

You have swallowed tptb’s propaganda. They purposely confuse the terms inflation and deflation with price movements to make it seem that they aren’t the source of the problem.

If you reread my post, you’ll see that I said that price movements are influenced by many other things in addition to the total money supply, which is how you know that RISING PRICES ARE NOT INFLATION AND FALLING PRICES ARE NOT DEFLATION. Essentially, you are confusing cause and effect. You get nowhere mislabeling these phenomena.

Europe has not had deflation. The US didn’t have deflation in 2007-10. We experienced something far worse. We had crashing asset prices, a rising money supply (inflation) and an increasing cost of living (result of inflation). If the deflationists were correct, we should have had a falling cost of living, which would have eased the pain of the asset crashes. But we didn’t.

“We experienced hyperinflation after 07-08 according to your definition.”

You’re the one with the bad definitions. Hyperinflation requires more than an increase in the money supply. The way the central banks printed money in 07-now has kept most of that money bottled up in the banks and financial markets.

For there to be hyperinflation, the expansion would have to be huge throughout the economy, which would then drive prices higher, followed by a cry from the population that they don’t have enough money at the same time they are spending their earnings as fast as they can because they have no confidence in the future value of the money.

I don’t anticipate hyperinflation any time soon. I do anticipate financial repression for a long time to come, unless there’s an “accident.”

There is another compounding factor in this.

American wage workers under 80 K, have effective been in wage deflation cycle, since the beginning of the 80’s export that job, Corporate Position, which has still not really changed.

The good job was lost, and the replacement is minimum wage, and minimum hours, with no benefits, all across America.

May times this “JOB” or “JOB’S” have to be subsidized, with food stamp’s.

How do you expect to get consumption growth, from such a wage structure??.

Clothing in that chart shows this. Poor (economically constrained) people, will buy from charity shops, and wear until it falls apart. Warm is the issue, not look’s, they will also pass on and around, that which no longer fit’s.

Which hammers clothing importers, and manufacturers.

The amount of older women seen in public, in low quality stretch legging’s, that they do not look good in, is not poor fashion sense, its economics’s,

They can get away with wearing cheap trashy clothing in public, even though it does nothing for their appearance, so they do.

And they still blend in, as many others where they go, are doing the same.

Women’s clothing was at one in time in America, and the entire west, an economic engine, in its own wright.

Now it’s very sick and definitely not running on all 8, not even 5 in fact.

d, regarding: “Women’s clothing was at one in time in America, and the entire west, an economic engine, in its own wright.”

That was before Private Equity started buying out the brands in the 80s. Once in the hands of the bean-counters; the quality goes to crap. I could always tell when a brand was sold without reading about it because the quality, fit, and consistency in size diminished so rapidly. It has all become the same ole cheap ugly crap but has a different “brand” name on it. I have a hard time finding anything worth buying. Shopping has become a chore instead of an exciting event. No more beautiful fabrics, no more impeccable fit, no more all leather shoes…. So the ladies just put the leggings back on and go about their business.

d,

You are right about clothing being recycled and worn whether in fashion or not. Yesterday, I was wearing a 20 year old jacket around town. And your remark about the stretch pants made me just a little paranoid. Replacing items is always a chore, because if I can’t find a better quality item on sale, I mostly do without.

It’s not just clothes. I’m a big reader and buy most of my books second hand, at thrift stores, or garage sales. I did this even when I had more money. I also recycle them because we have downsized.

Dona,

I saw the weirdest headline yesterday about yoga pants killing sea life. Yes, it was a Flori-duh story, but still. The quality of clothing is sooo bad, when you thrown it out, it contaminates the environment.

The Stock Market IS the “economy. ”

For investors profits, workers are forced into a race to the bottom. Soon, there will be no disposable income for most. If lawyers and collection agencies are going to go after people who make $25k a year and refuse to pay $7k for the health insurance racket, people will start losing their homes, and the ensuing popular uprising will perpetuate oppression.

Given the massively inflated prices all these suckers paid for houses in the last 20 years, “losing their homes” would be doing all of them a favor.

Can you imagine the losses these people will rack up if they continue paying the massive mortgage payments?

I own a $15k house that I bought with cash in order to avoid having to pay rent. My annual tax is $300. And yes, they can take it from me.

I care about the stock market in that that is where my 401k is tied up for at least the next 10 years. I’m assuming that the market and its value will both crash between now and then. My 401k is like my house-not worth anything until I sell

But your house isn’t worth much whether you sell it or not.

Well stated. However, I wonder if deflation won’t be more permanent when public pensions and entitlements can’t be maintained.

Or will the Fed just keep printing money until the debt is $100 trillion or $200 trillion, to keep everything going.

At some point doesn’t monetary expansion become more destructive than whatever positive effects we expect from it?

They will print the FRNs required to meet those obligations, inflation be damned (and kept low in official CPI terms).

Look at how much difficulty the GOP is having now in trying to return to the health care insurance situation of just a few years ago. When a united government can’t roll back an entitlement that’s barely 7 years old, how in the world will they cut benefits that are decades old? The won’t, and they’ll devalue the currency to the degree required to make the math work. Besides, those promises were made in FRNs – not purchasing power – so you can’t say the government is really defaulting on its obligations.

And if you’re an elite who’s “all-in” to the stock market and real estate, valuations will rise tremendously in nominal terms, but in inflation adjusted terms not so much…their wealth is preserved. Problem solved.

Seems like an logical argument to me. Meanwhile, central banks are preparing by raising rates and ending their QE programs.

Are banks in a position for lending into such a market of falling real estate prices, are bank loan requests expanding?

“Are banks in a position for lending into such a market of falling real estate prices,”

Yes on their term’s

“are bank loan requests expanding?”

Yes but those requests do not meet bank condition’s.

Particularly outsid the US The Ecb has been trying to force bank’s to lend by lowering their condition’s again.

With not much success.

Banks are back in ” only lend to those that don’t really need the loan, or restrict the loan/equity % so that we cant possibly lose on it”, mode.

As the double the size of the requested loan, as long as they invest 50 % of the loan in bank stock, and cant sell it until the loan is paid off” loan model. Has been curtailed in retail loans, in Europe.

The Gignourmous Real Estate Market, Bond Market and Stock Market were the only thing huge enough to consume the Trillions of fiscal steroids the Fed was injecting into the economy. All by themselves they gorged and bloated without triggering inflation in the day to day economy. Those markets now exhibit rising toxicity all those trillions may begin flooding into the broader economy. Up to this point the bubbles acted like financial dykes, leaching out at a comfy %2.00

“Up to this point the bubbles acted like financial dykes, leaching out at a comfy %2.00”

The question being how much leaches out and how much “Evapourate’s” in the coming corrections, to those sectors.

“Despite years of scaremongering about deflation”.

Remember those years of scaremongering about runaway inflation? It’s a tug of war that deflation will finally win.

Some of us are old enough to remember the last time inflation won – a 20 year period from 1970 to 1990. Inflation had mostly been tamed by the mid-80s, after a severe recession, but rose up again after the 1987 stock market crash and Greenspan’s response; he cut the Fed rate by 200 full basis points in a single day, which ignited a new inflationary cycle. (Those of you who think a pending stock market crash will be a deflationary event aren’t paying attention to recent history.) Another tightening cycle was needed to finally get inflation to stick near the 2% target. That tightening caused another recession in the early 90s.

On the other hand, when is the last time deflation was an issue? Not in the post-war era, that’s for sure. You’d need to go back to the Great Depression for that. It appears “scaremongering” about inflation is a lot more realistic. Certainly its place in our collective memory is much fresher.

“On the other hand, when is the last time deflation was an issue? Not in the post-war era, that’s for sure.”

Yes, let’s compare the post-war era to today.

Demographically, the post-war era was dominated by demographic, industrial, and then technological booms. Those all contributed to record growth, and -we will never see that again-

Today, we face a massive generation of retirees and those about to retire. Our birth rate is at historical lows (as are most of the world’s), and no signs of this changing. Hugely deflationary.

You’ve got pensions that are underfunded by TRILLIONS and taking on ever more risk, setting up what will become a massive disaster. Already happening today. California pensions alone are underfunded by $1 T. T for trillion. That too is hugely deflationary.

Technology has become a massive disruptor to jobs around the globe. Lots manufacturing jobs aren’t coming back, and the trend towards automation is seeping into even the service industry. Deflationary.

And lastly, you’ve got record debt bubbles around the world– governments AND households alike. This constrains spending, and an actual credit crisis would be again, hugely deflationary.

You’re trying to drive looking in the rear-view. The US economy from 1950 – 2000 bears little relevance to what we are headed towards in the future.

And you’re painting dragons on the map, just like the ancient map-makers did when they didn’t know what lay beyond a certain point. “Don’t go there – there might be dragons!” “Danger! Deflation ahead!”

I look to the past, because the past is the only reference we have. No one has a crystal ball, prognostications about demographic shifts notwithstanding. And here’s what I’ve seen in the rearview mirror:

I’ve seen recessions with double-digit inflation (early 80s), and I’ve seen recessions with very little inflation (early 90s). I’ve seen growth periods with high inflation (70s and late 80s) and I’ve seen growth periods with very low inflation (mid-to-late 90s). You know what I haven’t seen? Deflation. Ever. Forgive me for being skeptical when someone tells me deflation is just around the corner because “things are different now.” Economists have been warning about deflation since the last time we saw it in the Great Depression. I stopped listening 30 years ago.

“Economists have been warning about deflation since the last time we saw it in the Great Depression. I stopped listening 30 years ago.”

The Majority of “Economists” are in the “Wealthy” group.

To their group, the type of “Deflation” we need is a horror story. As it is “Asset deflation” we need, LOTS OF IT.

Land, Housing, Farm’s, Stock’s, Gold, Silver, all the grossly overpriced stores of wealth, some of which everyday people need the use of to survive.

The wealthy group, hold’s and HOLD’S UP, the price on those thing’s.

The only deflation they are interested in, is wage deflation, something America and the west has been forced by them top experience since the 80’s, and in spending power term’s is still experiencing.

Everything everyday people need, is going up (inflating) in leaps and bound’s, except wages. They are DEFLATING.

The list of retail stores closing as the retailers file BK has become a steady drumbeat.

I’d expect when ECB officially joins the higher rates parade and begins tapering their QE, bond prices will likely be smashed?

Number of construction workers have gone up through, so it’s obvious, people are no longer consuming. They are constructing ….. perhaps even the Next Generation Mall.

So the IRS is finding excuses to delay tax refunds? Too f*cking funny.

Of course I’m not surprised that clown-show USA would pull these banana republic stunts.

Not excuses. It was major problem of ID theft last year, affecting 40 million taxpayers. Blame e-filing. I think the IRS has beefed up security measures and has gotten this under control, but it was a huge mess.

Well sure Wolf, I hear you. But sometimes you have to wonder what lies beneath these “big events”. Phrases like “accidently-on-purpose” and things like that. Just being open-minded.

You’re probably still worried about the grassy knoll in Dallas, too.

Good to know somebody keeps up with all this.

So buy precious metals and go short sovereign debt?

What bothers me about PM is taxes…Federal and state. Why this has not gone to court is beyond me. PM is taxed at a rate higher than just about anything else.

The Fed raised rates. $Libor is up, but otherwise, Us bonds & notes

% rates are down, today. Surprise !

Mortgage rates are rising, but the smart money is moving in,

including into Germany.

$UST1M,$UST3m, $UST2Y, $UST10Y & $UST30Y are ALL down.

The curve is a flatbed.

What makes the smart money so frightened, that in the day, when

the Fed raise % rates and they signal that they will do more of the

same, they seek a costly refuge, here, with the US / Trump

government

Wolf – You may have addressed this before – I don’t recall. What are your thoughts on the pending decline in the US working age population and the fact that the fertility rate in the US is below the replacement rate? This has been covered eloquently and in much detail by this guy….

https://econimica.blogspot.com/2016/06/why-this-time-is-completely-utterly.html

…who seems to be serious in his studies of this topic.

If his numbers are right, I don’t understand how we are going to be able to grow the economy unless we have extraordinary increases in productivity. Even then, who is going to buy what we produce? (He asserts that the entire developed world is in pretty much the same demographic situation. Is this why Germany was welcoming immigrants?)

And any mention of demographic headwinds for the economy always seem to be dismissed (by whichever pundit is writing) as some kind of mildly interesting and academic afterthought. It seems to me those changes are fundamental and represent a paradigm shift, not something that rates a footnote.

Your thoughts would be appreciated.

Curious Car, I agree, there are clearly long-term demographic issues out there. But from my point of view, it isn’t bad because in the end, the economy as we feel it, is on a per-capita basis. That’s what matters to us as individuals.

Also, demographics are long term. They play out over decades. They make no difference tomorrow, next month, or next year. So it’s hard to consider them for investing purposes unless you look at a 30-year investment, and no one can foresee what will happen over those decades.

I think Curious Cat brings up a serious problem facing all developed nations.

Lack of population growth and Artificial Intelligence replacing workers is a huge problem that gov’t currently has no answer for.

Big companies continue to eliminate jobs because they are efficiently run, and will employ AI wherever possible.

The ratio of workers to retirees is falling, and wage growth is poor for most workers. Yet entitlement costs are going up about 9% a year, I have read.

The high inflation in health care is magnified by the growing retiree population, which I am a member of.

Ultimately, we need a vastly better-skilled workforce, which will be better compensated, to cover societies costs. Also, people will have to be more responsible for their own retirements.

I don’t see this happening, in my lifetime. I think the problems get worse for some time to come.

“And any mention of demographic headwinds for the economy always seem to be dismissed (by whichever pundit is writing) as some kind of mildly interesting and academic afterthought.”

Those pundits were spoon fed the ever increasing population base and consumerism economic model from birth.

They are in lockstep to it, as to consider chage to it means the death of several of the Globalised Vampire Corporate’s who pay for their reports.

chinas XI just reiterate he supports globalisation and free trade.

Of course he does.

china is the main beneficiary of it.

And the west with America at it’s head, are the main loser’s.

Free trade and globilisation can only work, when everybody has the same rule book.

And everybody stick’s to the rules.

china never abides by either of those condition’s..

” Curious Cat

Mar 15, 2017 at 8:00 pm

Wolf – You may have addressed this before – I don’t recall. What are your thoughts on the pending decline in the US working age population and the fact that the fertility rate in the US is below the replacement rate? ”

One wonders if the historic view of demographic trends is applicable in the near future. What would be the effect of creating as many hard working (24/7) workers as we want? IE, what is the effect of AI, robots and automation going to be?

“IE, what is the effect of AI, robots and automation going to be?”

If society, particularly American society, stays the way it is .

A lot more unemployed, unemployable, homeless, angry, people.

Indeed! Japan may be one of the countries best able to deal with the automation of everything. It has a rapidly shrinking workforce, and it is a leader in robotics and automation.

On the basis of GDP growth per-working-age-person, Japan is far ahead of any other country in the world.

“On the basis of GDP growth per-working-age-person, Japan is far ahead of any other country in the world.”

Japan is one of the few countries in the world (Possibly the only), not wedded, to an ever expanding, national consumer population base. It understands, the ever expanding population model, is not tenable for it, or the planet.

Most annalists still measure it, with and ever expanding population base consumerism ruler, so get an incorrect reading.

“IE, what is the effect of AI, robots and automation going to be?”

As stated earlier immediate effect will be more unemployment, but in this scenario the ultimate effect will be a major change in the way of tax collection.

Corporates are taxed in ways, employees in others. All in all, one can discard employee taxation totally and instead tax corporates a bit more. Corporates pay exactly same money as they did earlier, employees get smaller wages but they don’t pay taxes anymore. Lay down 50% of your employees, nice trick, wage costs go down and stock valuation up but taxes do not drop at all. Actually taxes can even rise if there’s hint of a social responsibility included, which there likely will be.

That’s what’s going to happen as quickly as PTB realizes this. All in all there’s no reason and no rationality to tax every phase of single income generation process chain as one only needs to tax start point and end point of chain. And if it’s done correctly one needs only to tax either start or end point of chain.

– Harry S. Dent has done some VERY good research on the relationship(s) between demographics and the economy (e.g. our (US) economy)

He looks at the socalled “Family Spending Cycle” and that Cycle is so extremely powerful that it overwhelms any govenment action.

http://nypost.com/2014/02/08/thanks-to-aging-population-its-all-downhill-from-here-for-usa/

Perhaps rate increases will lead to the Swiss Central Bank (SNB) to begin selling their AAPL position (and others, presumably)?

“that’s why the Fed is a mile behind the curve. But at least it has now acknowledged seeing the curve in the distance.”

No way. The dollar dumped today and stocks jumped because the FED is dovish. Quarter point rate hikes in an economy that is booming? It will all be reversed within a year. It’s the only button they know how to push.

Yes you point out people have less discretionary income. So how is this going to stimulate growth? I see no story for rate increases based on the revelation that the Fed now knows it is blowing bubbles. That would imply all their previous policy decisions have been biased or wrong.

The only story playing out here is the one that has been told all along. More inflation and cheaper money to come!

Off topic but I live in Boise, Idaho where Micron is a major employer. Today apparently I need to buck up and fix what hasn’t been done in seven years. Apparently there are a bunch of patents that haven’t been paid attention to. And yet home prices here are out of control because “you work for Micron.”

– Nope. The FED is NOT – I repeat – NOT behind the curve because the FED follows the 3 month T-bill rate and that rate recently went higher up to 0.75% and that meant that the FED had to follow. Like the FED had to follow short term market rates in late 2015 & late 2016.

– Small investor are no pouring into the stockmarket and that’s a GOOD sign that we’re fast approaching the top of the bullmarket that started in March 2009. They’re selling those T-bills and buying the market (e.g. ETFs). Hence the rise in short term rates.

– Although when I look at the 3 month T-bill rate today then I think now that the next move of the FED’s fund rate will be a rate cut.

– CPI is a joke (as more than once before). The weigthing of Healthcare (HC) is way too small in CPI. HC account for about 17% of GDP but in weighted only for about 4 to 5% in the CPI.

I look at this as simply as I can understand it. With a 20 trillion dollar debt (at least what we are told) and a yearly 500 billion dollar deficit(on average), we would need have to have a trillion dollar a year swing to post a yearly half billion dollar surplus in order to pay off the debt in 40 years. Not going to happen-EVER.Clinton had the DotCom bubble, Bush had the Housing Bubble and Obama had the QE bubble. What will T Rump have? The War Bubble?

Always get a giggle out of the fake data coming out of these agencies.

Retail sales up. LOL!!

Thousands of stores closing almost weekly, companies like Sears imploding as we speak, and they’re reporting that sales actually increased, albeit by a tad.

Laughable.