For the first time in the US since the Financial Crisis.

Let’s forget for a moment the Fed, its rate-increase flip-flopping, and what that might do in theory to the economy, and let’s look instead at what companies are actually doing, how they’re responding to the environment they find themselves in. Because now, something is happening that we haven’t seen since the trough of the Financial Crisis.

Credit growth no matter what has been the mantra. It could never be enough. If companies borrow more from banks, they’ll use that money to invest in productive activities or equipment and grow. That’s the theory. And it would move the economy forward.

So total loans and leases at all commercial banks have soared 40% since the bottom of the Financial Crisis to $9.13 trillion in the week ending February 15, according to the Board of Governors of the Federal Reserve, and are 25% above the peak of the prior credit bubble in October 2008.

But since the week ending December 7, 2016, they have declined a smidgen. So why is that all-important loan growth flattening out after soaring for so many years? And how do companies fit into this?

Of the many categories of loans and leases, one category stands out as an indicator of what companies are doing: commercial and industrial loans.

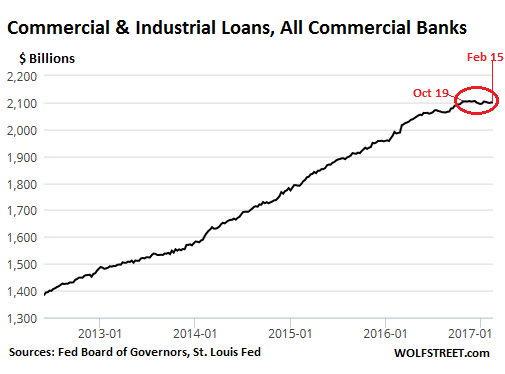

They edged down to $2.1 trillion in the week ended February 15. That’s where they’d first stood on October 19. After ballooning relentlessly for six years straight, C&I loans have now been stalled for four months in a row.

Since the bottom of the financial crisis, there have been periods of four or five weeks of stalling C&I loans, but they were invariably followed by robust loan growth immediately afterwards. So these C&I loans have been booming over those years. But this period from October 19 until now is the first extended stretch of stalling C&I loans since the bottom of the Financial Crisis.

The chart shows C&I loans at all US banks going back to 2012. Note how that four-month stagnation-period is unique in this time span:

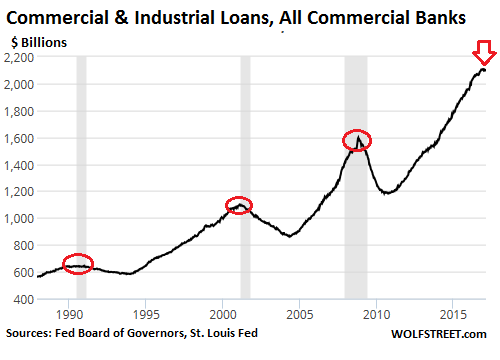

C&I loans are a sign of what businesses of all sizes are doing – from the small company that is borrowing to buy a piece of equipment to the largest behemoth that is funding its inventories. These loans show whether companies in aggregate are expanding their investments or pulling in their horns.

In that manner, C&I loans are tightly connected to the real economy: they grow when the economy grows, and they decline when the economy heads south.

This chart shows C&I loans going back to 1988, covering the last three recessions. The turning points are circled in red:

The turning point during the Financial Crisis was unique – a sudden deep collapse in credit, when the banking system began to seize, rather than a classic turning point that evolved over time, as the prior two turning points exemplified.

The timing of a turning point may not be perfectly aligned with the beginning of a recession, but it’s close.

And turning points become clear only after C&I loans are in a real downdraft. Before then, we just have our suspicions. For now, we have four months of stagnation, a first since the trough of the Financial Crisis, and a sign that companies have become more reluctant to borrow from banks. This period coincides with the Fed’s more energetic rhetoric about “removing accommodation.”

Perhaps it will blow over, and companies will head back to their bankers, and C&I loans will surge once again. But more likely, it’s an early warning sign of a gradual change in the dynamics, just when no one wants to see any red flags.

“Flat sales” in the restaurant industry are now a “welcome change.” The New Normal. Read… Is the US Restaurant Recession Becoming Structural?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Fascinating, Wolf. On the 25-year chart I can only see once where it leveled for about 4-6 months in ’99 then continued to climb. The way I read it, if it falls below that 2016 support level at about 2,075, we’re in trouble.

2075 confirms you in deep, and getting deeper, trouble.

125 point drop on that chart is SERIOUS.

Worrrisome. But it’s also possible that the stalling of C&I Loans maybe due to large corporations getting their financing from credit markets in anticipation of rising interest rates (Inflation had been increasing since early 2016). If the C&I Loans stagnating were due to smaller businesses pulling back this would be inconsistent with data from NFIB Sentiment Surveys covering the same period. But this is definitely something to monitor as more data comes in to confirm one way or another.

The FED survey of Senior Loan Officers on Bank Lending practices is showing a decrease trend in demand for C&I loans to large, medium and small firms since 3Q/14, coincident with the banks increasing loan spreads over cost of funds. i.e. Loan demand decreasing as bank loan rates increasing.

https://www.federalreserve.gov/datadownload/Chart.aspx?rel=SLOOS&series=e64f07187815f0e7ed89237d8cb91eeb&lastobs=&from=03/01/2007&to=03/31/2017&filetype=csv&label=include&layout=seriescolumn&pp=Download

I think you may have inadvertently provided the link for the other consumer loans for autos. But i know what chart you are referring to. I recall for the latest quarter that domestic bank loan demand from large, med, and small businesses did recover (albeit marginally) from the negative dip in prior quarter.

I still think this MAY BE just noise (at least I hope) – “animal spirits” seem to be running pretty rampant right now. But always good to have an open mind and consider the opposite side of a trade.

BW

Oops … sorry. I didn’t realize the chart selections get reset in the link to the Fed site.

However, it is an interactive graph. You can select the different data series to chart yourself by scrolling down and selecting from the list on the left of the screen. You will find the various data series to select for C&I loans including:

o Net percentage of domestic banks reporting stronger demand for C&I loans from large and middle-market firms

o Net percentage of domestic banks increasing spreads of loan rates over banks’ cost of funds to large and middle-market firms

o Net percentage of domestic banks tightening standards for C&I loans to large and middle-market firms

o Net percentage of domestic banks reporting stronger demand for C&I loans from small firms

o Net percentage of domestic banks increasing spreads of loan rates over banks’ cost of funds to small firms

o Net percentage of domestic banks tightening standards for C&I loans to small firms

Also interesting to look at some of the other loan categories like auto loans, credit card loans, mortgages, CRE, etc…

The economy was already in recession in previous downturns on the FRED C&I loan chart. The stock market was already selling off.

That contrasts with what is happening with the S&P and Dow right now. Record high after record high.

That’s because we used to actually have a free market Not so much anymore

There is no such thing as a free market and never has been. Failure to see this fact is a point of religion.

Thank you.

Companies may be issuing public debt rather than getting loans from banks. The interest rate is likely lower on public debt.

I wonder how much this is linked to the odds of the Federal Reserve hiking rates in March. BGG (the index tracking how market partecipants rate the likeness of a rate change) jumped from 10 to 25% between October and November 2016, then slowly but steadily crept to 30% throughout December and January and humped to 50% in February. In short people in the business now think there’s a 50% chance the Fed will hike rates in March, hardly conductive for big debt binge, especially at a time when issuing euro-denominated bonds is ridiculously cheap.

Of course if Janet Yellen performs her now patented comedy routine (lots of words with no substance and, what’s more critical, no rate hikes) expect things to go back to sleep for a while, at least until the BGG starts spiking again.

The hidden secret of money.

Money = Debt

Money is created from loans and destroyed by the repayment of those loans.

From the BoE:

http://www.bankofengland.co.uk/publications/Documents/quarterlybulletin/2014/qb14q1prereleasemoneycreation.pdf

If you paid off all the debt there would be no money.

Money and debt are opposite sides of the same coin, matter and anti-matter.

The money supply reflects debt / credit bubbles.

When credit contracts the money supply contracts and this is the way to debt deflation.

The impossible boom before 2008 as seen from the money supply:

http://www.whichwayhome.com/skin/frontend/default/wwgcomcatalogarticles/images/articles/whichwayhomes/US-money-supply.jpg

Everything is reflected in the money supply.

The money supply is flat in the recession of the early 1990s.

Then it really starts to take off as the dot.com boom gets going which rapidly morphs into the US housing boom, courtesy of Alan Greenspan’s loose monetary policy.

When M3 gets closer to the vertical, the black swan is coming and you have an out of control credit bubble on your hands (money = debt).

The theory, which is outside the Central Banker’s neoclassical economics.

Irving Fisher produced the theory of debt deflation in the 1930s.

Hyman Minsky carried on with his work and came up with the “Financial instability Hypothesis” in 1974.

Steve Keen carried on with their work and spotted 2008 coming in 2005.

You can see what Steve Keen saw in the graph above, it’s impossible to miss when you know what you are looking for.

A “black swan” for the ignorant.

A ‘ Black Swan ‘ indeed . Though I’d say both for the ignorant , deluded as well as the volitionally stupid

PS ; A nice addition to Wolf’s article

On a macroeconomic level, I have no debt but I have money.

It’s called “savings”, not very fashionable right now, but my money (admittedly not very “safe”) is at least not debt.

Woops! “Macro” should be “micro” …

Which makes the likes of you and I anathema in the eyes of the banks , mortgage companies , real estate … and the especially the government . To put a point on it a close friend in the Intelligence community who is sympathetic to our stance and is in the same position himself has said from the Government’s point of view the likes of you and I are the worst threat imaginable by those in DC should more follow suit beyond war and terrorism . Why ? because from their point of view our being debt free makes us less malleable and controllable as well as having too much Freedom … in their eyes

Correct. A heavily indebted person has no freedom at all : he/she is a slave of the banks, their customers and/or their employers because of TINA. If such person gets critical about how things are being managed, he/she runs inevitably into trouble. Job/customers loss, default on debt repayments and followed by repossessions/bankruptcy. Credit and debt is the road to enslavement – and anyone can avoid this by being more patient and buying stuff only when you have the money for it. That’s what I did and never had expensive stuff while being young nor traveling the entire planet just for the fun of it, but now ( 60+ ) I am FREE.

Ah, but you did not conjure it from the air as the banks do.

And many in India said the same thing about their paper rupees safely stored away.

I prefer not to live with zero debt. I have substantial debt but it is paid by a stream of rental income. I am hoping to get even deeper in debt as this year progresses.

Having no debt = personal freedom. Having cash simply adds to that freedom.

I have mentioned this before on this forum. Our company had a very good logging customer. He was very successful. In fact, he was extremely rich. One day he remarked to us, “It’s not what you own, it’s what you have paid for that counts”. Another customer of ours commented on a recent house purchase by a deckhand working on the tug we were staying on. At that time the mortgage payments ‘the buyer’ would make were going to be $1200/month…in today’s dollars $2500-$3,000/month. My very well off friend “Art” said, “It isn’t what you can afford when you are working that is important, it’s what you can afford when you are not working. That lower amount should be your payment.”

I followed those gems of wisdom and retired at 57; sleeping very well most nights along the way. Of course, I also remember my mortgage rate ballooning to 18% in the late ’70s when I was 24 and had a young family to provide for. Those who experienced that wonderful shock know very well that anything can happen and that it is best to be prepared and live below your means.

One day, interest rates will increase for whatever reason. Those in debt better be willing to walk away from what they think they own. Those who think it cannot happen will be very surprised, indeed. Certainly, there will always be people needing a place to rent. But in tough times you can only ask what the market will bear. For many years us ‘savers’ have been shafted. That much is obvious. It’ll be someone else’s turn down the road.

regards

I love your deckhand story and have told it multiple times to my three sons (ages 19-24).

Of course they ignored me…

But I still hold out hope.

C&I stall. Credit freeze. Yikes! ‘Been waiting for this. Bad news.

Good Morning.

American Consumer Confidence soars to 16 year highs.

US home prices rose at 5.58% year-over-year in December.

Chicago PMI highest since Jan 2015.

The Muppets are destroying all Doomers and Gloomers. LOLOL.

The shape of the curve is interesting. Aside from the insatiable growth of credit, the main trend is the length of the upward swing from the trough. It is the longest for this period. A more intriguing question is what to do when interest rates are already zero while there was still something to cut previously.

The world economy seems to be in a growing oscillation. With each cycle, excursions are getting larger and more uncontrolled. The recession “fix” used to be just lowering interest rates, then deficit spending, then pegging interest rates at zero for years, then quantitatively easing (printing) of trillions of dollars.

The future? Japan and the EU show where we are heading in the next recession: negative interest rates, direct central bank purchases of equities and of course much more quantitative easing (purchasing of defaulted bonds).

It would take an interest rate shock similar to the early 80’s to stabilize the financial system. Not likely to happen.

Wolf, seems to be following interest rates and shows the floor we have found recently. Businesses can keep leveraging more and more as interest rates drop and cost of carry decreases. Interest rates rising will be bad for corporates but nothing a good chapter 11 can’t fix!

I have personal experience of why the C&I loans have flattened.

4 months ago I had an “agreed” refi loan on some rental houses where the small local bank changed the terms just before ordering the appraisals.

They changed from the agreed 15 year term and 75% LTV with cashout to 12 year term and 65% LTV.

2 years ago they were begging for me to borrow money. So I did a big refi 4 times bigger than the “agreed” one last November.

By last November, I had been doing business with them for over a year, our financial results were up 20%, we made our payments early, or at the latest on the day they were due, and kept over 10% of my loan balance in cash in their bank.

Their reasoning… they are worried about the future. Not me, just everything.

So I told them to get lost and did my part to contribute to the C&I loan volume stagnation.

Multiply this by thousands of banks and millions of customers and it becomes a SELF-FULFILLING PROPHECY.

I believe there would be an economic boom for some if marijuana was legalized. It is an excellent food, fiber and energy crop. Another crop we need is castor bean for energy.

The medical industrial complex including drug mfgs have been fighting it along with lawyers, big tobacco, police, armament manufacturers, police car mfgs, prison builders and operators, bail bondsmen, etc. would see great loss.

Imagine all the savings to the people who could switch from expensive medicine to natural God given medicine. The insurance companies would save a lot but then the need for the insurance companies may greatly decrease.

Win for the people, lose for those that screw the people.

“I believe there would be an economic boom for some if marijuana was legalized.”

Problem being its a major element of the hippy-trippy drop out life style.

Who pay for all the infrastructure used by all the cannabis using, hippy dropouts, who pay no tax, and produce less than they consume, continuously.

Cannabis itself, is not addictive, or a problem. The hippy dropout lifestyle, that goes with it, is both.

Sorry, but I think you are painting with too wide a brush. I know many through the years, myself included, who would partake and were very productive members of society, not your hippie drippie lifestyle as you describe. I believe you would find some of the most successful and productive members of society use MT but are in the closet due to the false narrative that it is bad for you.

The brush I use is to narrow, the occasional social user, just like the occasional social drinker, is a small minority, of the user population..

Legalisation at this economic point, will legally enable, a huge drop out segment of society.

Thats before we get to the Legal damage, it will do to Native American youth.

Just being natural, does not automatically make it good.

Rape is also natural. There are good reasons it is illegal.

Cannabis if it is to be legalised, it need’s to be legalised at the bottom of an economic upswing. So that when the upswing is over. Its just 1 more legally abuseable substance out there, abused by loser’s, and no longer the new, cool kid on the block.

I actually support legalisation, with heavy taxation, at the economic wright time.

Now, is not the economic wright time.