China’s debt boom, or “credit boom” in more palatable terms – whose true extent remains purposefully obscure – and what it might do to the Chinese economy and by extension to the global economy is starting to worry some folks at the New York Fed. This is how their article starts out:

Debt in China has increased dramatically in recent years, accounting for roughly one-half of all new credit created globally since 2005. The country’s share of total global credit is nearly 25 percent, up from 5 percent ten years ago. By some measures (as documented below), China’s credit boom has reached the point where countries typically encounter financial stress, which could spill over to international markets given the size of the Chinese economy.

The data points can give you the willies:

- Nonfinancial debt in China has soared sevenfold in a little over a decade, from about $3 trillion at the end of 2005 to nearly $22 trillion.

- Banking assets (mostly loans) have soared sixfold during the same period to over 300% of GDP.

- In 2016 alone, credit outstanding jumped by over $3 trillion; the pace of growth was about twice that of nominal GDP.

The report:

The international experience suggests that such a rapid buildup is often followed by stress in domestic banking systems. Roughly one-third of boom cases end up in financial crises and another third precede extended periods of below-trend economic growth.

The surge in nonfinancial sector debt kicked off with corporate borrowing, mostly in the infrastructure and property sectors. More recently, household debt began to surge, mostly mortgages; again the property sector.

Lending by banks is still the largest component of the credit boom, but as authorities are trying to keep it from spiraling out of control, “shadow” lending by nonbanks (trust loans, entrusted lending, and undiscounted bankers’ acceptances) has surged:

Nonbanks, often in cooperation with banks, have found ways around authorities’ efforts to restrict lending to certain sectors (such as real estate and industries with excess capacity like steel and cement) following the initial surge in credit in 2009.

This shadow credit accounts for about 15% of total credit, or 31% of GDP, up from 5% ten years ago. Authorities have been trying to contain this shadow credit boom since 2013 via macroprudential measures. But where there’s a will, there’s a way: these efforts likely “caused credit to migrate to other lending channels.”

Meanwhile, in line with the house price bubble, mortgage lending became the latest driver in the debt boom: At the end of December 2016, residential mortgage loans were up 35% year-over-year.

But debt may be ballooning even faster.

The increasing complexity of China’s financial system has made it difficult to estimate the true level and growth rate of credit. Official data put nonfinancial debt at roughly 205 percent of GDP. However, adjustments for additional sources of credit not fully captured in the official data suggest total credit could be higher.

One way that the growth in debt could be underestimated:

[T]he pace of total credit growth is higher when swaps of local government-related bank loans for municipal bonds are included. China’s credit measure excludes swapped bank loans but does not add back the municipal bonds they were exchanged for.

The annual growth in the People’s Bank of China’s measure of “total social financing” – which includes bank loans, off-balance-sheet financing, trust loans, and net corporate debt issuance – is now around 12% (about half of what it had been during the blistering surge after the Financial Crisis). That’s the official figure.

But with the muni bonds swapped for bank loans added into the equation, annual credit growth would be above 15%.

The smaller banks are doing it.

Chinese authorities have had some impact trying to control credit growth at the big four state-owned banks, ranked among the five largest banks globally by assets. But the smaller banks “have been growing their total assets at two to three times the pace of the largest commercial banks.” And they have some special products. The report:

Joint stock commercial banks (JSBs), city commercial banks (CCBs), and other smaller-scale institutions have increasingly used less stable funding sources to finance their balance sheet expansion, primarily by tapping the interbank market and issuing wealth management products (WMP)….

WMPs are predominantly short-term investment products sold by banks and nonbank financial institutions that provide investors with higher rates of return than bank deposit rates. WMPs can have a range of underlying assets, including bonds, money market funds, and even a limited amount of bank loans.

Official data on banks’ WMPs show an almost sixfold increase since 2011, to the equivalent of about $4 trillion or 37 percent of GDP.

The growing reliance of Chinese banks on this type of funding has increased concerns over potential shocks to market-based funding, a risk highlighted by the International Monetary Fund in its October 2016 Global Financial Stability Report.

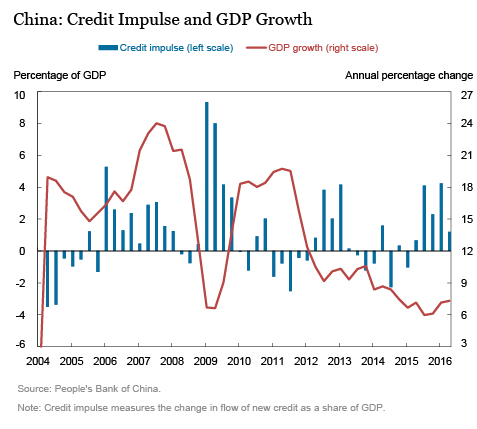

But “less bang for the debt,” so to speak.

As debt ballooned, its effectiveness in stimulating economic output has declined. The “credit pulse” – the change in the flow of new credit as a percentage of GDP – “appears to be providing less bang to output for each additional yuan of credit, underscoring questions over how much lending is going to unproductive ‘zombie’ companies”:

But authorities might keep the plates spinning for a while longer, and waiting for that financial crisis in China, and what it might do to the global economy, might require some patience. According to the report, China’s financial system sports some features that for the moment lower the risks of “a financial disruption,” among them:

- Unlike credit booms in other emerging markets that ended in financial crises, China’s high domestic savings have funded much of its credit boom.

- Chinese authorities can drag this out with their liquidity tools, “including high required reserve ratios,” central bank liquidity injections, “and a financial sector dominated by state-owned lenders and borrowers.”

- The government gross debt (including off-balance-sheet borrowing implicitly guaranteed by the state) was 60% of GDP at the end of 2016, lower than in most advanced economies. And the government still sits on about $3 trillion of dwindling foreign exchange reserves.

So the government has some capacity “to absorb potential losses from a financial disruption.” But worries persist.

Still, the speed and increasing complexity of the country’s credit growth suggest that there could be significant benefits for China in addressing its banking system and financial reforms.

And do so presumably before contagion spreads to the rest of the world.

It started with a whimper and has turned into a roar: China and other foreign governments are dumping US Treasuries. Read… Foreign Governments Dump US Treasuries as Never Before, But Who the Heck is Buying Them?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“Less bang for the debt”.

The diminishing marginal productivity of debt.

A key “feature” of China’s capacity “to absorb potential losses from a financial disruption” is it’s large population. Calculating the size of the credit expansion, utilizing GDP as the yard stick, may be misleading.

What could be of more importance is to use a per capita base line. In which case the Chinese economy will look much healthier than any of the OECD countries.

As a comparison, the US has 12 cities with a population of one million or more. China has 160 cities of such size! Along with their still sizeable foreign reserves and manufacturing base, it should weather a financial systemic shock in a much better condition, be it local or global.

Two other factors to look at. The Chinese are big savers with a savings rate of 36%. The citizens have 25 trillion saved. Debt must always be viewed with savings in mind to see its relevance.

Also, a lot of the debt was incurred building out China’s infrastructure. They have homes, factories, electrical generating and heating plants, highways, airports, dams, malls, schools, etc to show for the debt. This different than countries that just run up debt to pay off the old debt and get nothing to show for it.

Underneath neo-liberalism is an economics, neoclassical economics, that uses flawed assumption on money and debt.

From the start it contained the seeds of its own destruction and was rolled out globally.

Debt based consumption has real limits as Greece has already found out, but surplus and deficit nations still think this arrangement can continue indefinitely, but it can’t.

It thinks money just circulates within the economy and is neither created nor destroyed. When money is destroyed in large quantities, e.g. 2008, they call it a “black swan”.

It assumes markets tend towards stable equilibriums and as the housing bubbles burst (Japan 1989, UK 1989, US 2008, Spain and Ireland) it sees no need to change its theories.

It’s economists are convinced the Euro-zone is tending towards a stable equilibrium, the real world has had the nerve to disagree with their theory, but they carry on as though its problems will resolve themselves, this is what their theory tells them.

Those that did see 2008 coming attribute it too much private debt.

The Central banks are trying to cure the problem with more private debt.

China itself uses this economics and is blissfully unaware of the consequences of its own debt binge.

Neo-liberalism is an empire built on debt because none of its practitioners understood it.

All that debt has repayments, and was money borrowed from the future; hardly any of it went into productive investment in the real economy.

The legacy of neo-liberalism will be a harsh one.

there’s a difference between monetary sovereign nations, like the USA, and monetary non sovereign nations, like Greece and eurozone nations, and states,like Kansas or Queensland, and the rest of us. We are users of currency and it is created by the federal governments when ever it pays a bill, always with new money as well.

The Chinese central government can buy all its debts and not go broke unless deliberately chosen to do so.

I look at the situation there from outside but I can imagine China in its desperate bid to stay in power, could conceivably demolish all those empty cities and replace them with new ones. It can,could so so and only come unstuck when the needed resources could not be supplied. We don’t yet know when that might happen, but its probably inevitable as it will be for us.

Governments can’t pay debt indefinitely. Do you mean by printing money like Venezuela did? Demolish ghost cities and building new ones? So, in your world energy can be created out of nothing as well.

Debt based economic booms

1) The economy still has resourced that are not actually or perceived as being encumbered by a repayment problem … cause for big recession later as liquidity dries up when problem revealed. See US and Great Recession.

2) Everyone knows how the scam works and someone will be left holding the bag, only that person does not yet know it. Perhaps a game of hot potato.

3) Whoever is buying the debt will tell the borrower to forget about it … implies printed money is behind the boom

Re #1. In China – not likely. Given the stories of empty cities, it would have blown by now if it were going to. Implies #2. Perhaps #3 in addition. Everyone knows China will do whatever it takes to hold it together. A few mandarins may be shot int the head on the way. They’re making macro economic rules that will never be put into textbooks.

US in #2 at this time using central bank liquidity and managed interest rates.

Japan is #3.

Eurozone is #2 and #3.

China is a police state that makes rules it wants to make, so yes, they’re making macro rules that will never be in any textbook.

Ed,

China’s cops are unarmed, it has the lowest incarceration rate and the lowest recidivism rate in the world. That doesn’t fit the profile of a ‘police state.

The U.S., on the other hand, has the profile of a police state. The highest incarceration and recidivism on earth, the highest rate of police violence, the most heavily armed police on earth…

“China’s high domestic savings have funded much of its credit boom.”

Domestic savings are bank liabilities, not assets to be “lent out”. In a fiat monetary system, bank lending creates domestic savings, not the other way around.

Regardless, the question is what will cause a classic bank panic in China? Especially one that the government will refuse to step in an monetize?

kent, if banks don’t lend they go out of business. There’s no reason to have a bank that does not lend. It’s the definition of bank.

So, if no banks, what to do with savings. No loans so no expansion so no to very few jobs. No reason for cash either since unless you want to pay for storage and possibly trade warehouse receipts. warehouse receipts will be the new cash. No expansion unless new gold or other plunderable assets are found or commodities are exchanged. Also, if no cash, how do you sell a cow? If you sell a cow for cash, what do you do with the cash since banks can’t lend?

Mises and the real true money folks are terrible economists.

I’ve said this before, but the US or some other countries will have a crisis first before China. It’s all about “face” in China. There’s an article out there about how the breakup of the EU will hurt China. Sure it will hit the general population, but the elites are secretly hoping for any sort of crisis from the Western world. It serves a number of purposes:

1. They can point to the West as the source of the crisis.

2. It further legitimizes whatever it is they are doing i.e. our system works, except the part that has some Western connection.

The Chinese government wants the Yuan to devaluate, for the property market to burst, etc, etc, they just can’t be seen as the one that causes it i.e. their own bad decisions.

Completely off topic, but the Financial Transactions and Reports Analysis Centre of Canada (FINTRAC) has fined Manulife Financial for violating money laundering rules, and fined the insurance corporation a momentous sum of 1.15M (no charges).

Given the track record of this agency, these transactions must have been as difficult to find as (to paraphrase) hay in a haystack.

http://www.cbc.ca/news/business/fintrac-fine-name-secret-1.3999156

Max,

I like the section “‘Mickey Mouse’ watchdog.” It’s no mistake or oversight on the part of gov’t to hide their (Manulife’s) name. I wonder what the fine would be in the USA?

Canada is funny. A whole 1.15M fine for potentially tens of billions of dollar in money laundering; the poor company. Did they ask for the whole thing to be pain in pennies?

Oops, I meant paid; me and my fat fingers :).

That’s OK, it’s called subliminal messaging. At the moment, that’s how it feels in Canada.

R2D2, that “apparent” irregularity is nothing in this country. You should read up on the Bre-X ripoff from the mid-1990s (https://en.wikipedia.org/wiki/Bre-X). Twenty years after the fact, the case was still in some kind of court proceeding. Many people lost everything (not me).

Then if you get bored of that story, read some of these:

http://business.financialpost.com/executive/canada-now-dominates-world-bank-corruption-list-thanks-to-snc-lavalin

and

https://www.thestar.com/topic.charbonneau_commission.html

After reading the articles that you pointed out, I have to say, I’m sorry; I underestimated Canada; it’s much funnier than I had previously thought.

China’s problems seem small potatoes in comparison with us waste on military, added another 56B today.

When I was in the Navy we were told to dump all the office supplies including the file cabinets and desk/chairs into the ocean so that we could request more money for the new fiscal year. That is how tax payer money is well spent lol.

Aloha Friends…I know I might be taking a very simplistic view and approach here…..However,since most of the DEBT is in one way or another,Owed to the State(Large State run Banks)..why not,Over-time Forgive parts of the Debt…to re-establish Long-term Liquidity..? thanks for reading,aloha

Nik- In a much simpler time, long, long ago, that is recorded as the actual practice.

https://en.wikipedia.org/wiki/Jubilee_(biblical)

A word from the gnomes of Berne: The Bank for International Settlements (BIS) gives the following ratios for debt to GDP [http://www.bis.org/publ/qtrpdf/r_qt1509g.pdf]:

Japan: 393 %

USA: 239 %

China: 235%

Many thanks for your interest in the BIS credit statistics. We will release an update of this database on 5 March, 2017, where the latest data point refer to Q3-2016. To see future releases of BIS statistics, please see this link: http://www.bis.org/statistics/relcal.htm

Since China’s loan numbers keep going up, it’s very possible that most of the WMP’s are being used to pay the interest on previous loans, at ever higher interest rates. To what extent these loans must be paid in dollars is up to conjecture, but there’s no doubt that officials are spending an inordinate amount of effort trying to source dollars from wherever they can. If China had maintained an independent currency, it’s possible that debt could have been shuffled off into zombie banks. Unfortunately, China decided to peg its currency to the dollar, and consequently, China’s authorities have no power whatsoever to do anything but slow the coming train wreck.

That’s the source of all the money that they spend on real estate around the world is coming from; they are borrowing and buying like gambling addicts in a casino. They are going to cause a massive bubble burst in the global economy, and we all will pay the price for addictions.