The “risk free” bonds have bloodied investors.

The carnage in bonds has consequences. The average interest rate of the a conforming 30-year fixed mortgage as of Friday was quoted at 4.125% for top credit scores. That’s up about 0.5 percentage point from just before the election, according to Mortgage News Daily. It put the month “on a short list of 4 worst months in more than a decade.”

One of the other three months on that short list occurred at the end of 2010 and two “back to back amid the 2013 Taper Tantrum,” when the Fed let it slip that it might taper QE Infinity out of existence.

Investors were not amused. From the day after the election through November 16, they yanked $8.2 billion out of bond funds, the largest weekly outflow since Taper-Tantrum June.

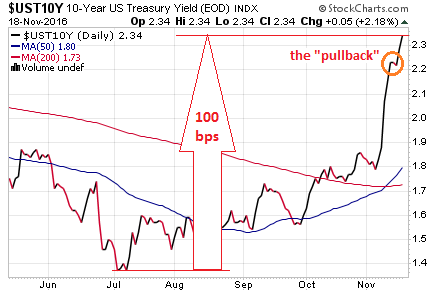

The 10-year Treasury yield jumped to 2.36% in late trading on Friday, the highest since December 2015, up 66 basis point since the election, and up one full percentage point since July!

The 10-year yield is at a critical juncture. In terms of reality, the first thing that might happen is a rate increase by the Fed in December, after a year of flip-flopping. A slew of post-election pronouncements by Fed heads – including Yellen’s “relatively soon” – have pushed the odds of a rate hike to 98%.

Then in January, the new administration will move into the White House. It will take them a while to get their feet on the ground. Legislation isn’t an instant thing. Lobbyists will swarm all over it and ask for more time to shoehorn their special goodies into it. In other words, that massive deficit-funded stimulus package, if it happens at all, won’t turn into circulating money for a while.

So eventually the bond market is going to figure this out and sit back and lick its wounds. A week ago, I pontificated that “it wouldn’t surprise me if yields fall some back next week – on the theory that nothing goes to heck in a straight line.”

And with impeccable timing, that’s what we got: mid-week, one teeny-weeny little squiggle in the 10-year yield, which I circled in the chart below. The only “pullback” in the yield spike since the election. (via StockCharts.com):

Note how the 10-year yield has jumped 100 basis points (1 percentage point) since July. I still think that pullback in yields is going to happen any day now. As I said, nothing goes to heck in a straight line.

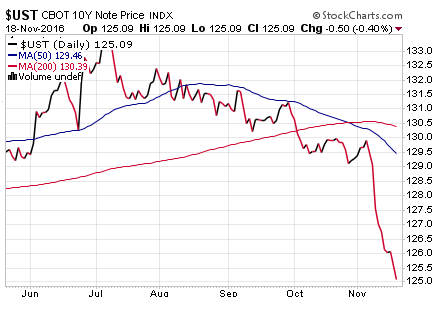

In terms of dollars and cents, this move has wiped out a lot of wealth. Bond prices fall when yields rise. This chart (via StockCharts.com) shows the CBOT Price Index for the 10-year note. It’s down 5.6% since July:

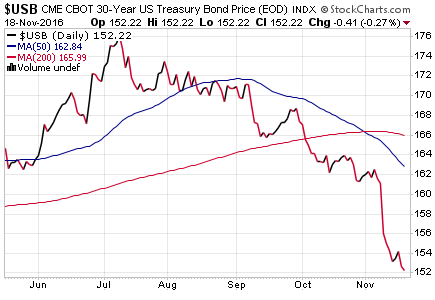

The 30-year Treasury bond went through a similar drubbing. The yield spiked to 3.01%. The mid-week pullback was a little more pronounced. Since the election, the yield has spiked by 44 basis points and since early July by 91 basis points (via StockCharts.com):

Folks who have this “risk free” bond in their portfolios: note that in terms of dollars and cents, the CBOT Price Index for the 30-year bond has plunged 13.8% since early July!

However, the election razzmatazz hasn’t had much impact on junk bonds. They’d had a phenomenal run from mid-February through mid-October, when NIRP refugees from Europe and Japan plowed into them, along with those who believed that crushed energy junk bonds were a huge buying opportunity and that the banks after all wouldn’t cut these drillers’ lifelines to push them into bankruptcy, and so these junk bonds surged until mid-October. Since then, they have declined some. But they slept through the election and haven’t budged much since.

It seems worried folks fleeing junk bonds, or those cashing out at the top, were replaced by bloodied sellers of Treasuries.

Overall in bond-land, the Bloomberg Barclays Global Aggregate bond Index fell 4% from Friday November 4, just before the election, through Thursday. It was, as Bloomberg put it, “the biggest two-week rout in the data, which go back to 1990.”

And the hated dollar – which by all accounts should have died long ago – has jumped since the election, as the world now expects rate hikes from the Fed while other central banks are still jabbering about QE. In fact, it has been the place to go since mid-2014, which is when Fed heads began sprinkling their oracles with references to rate hikes (weekly chart of the dollar index DXY back to January 2014):

The markets now have a new interpretation: Every time a talking head affiliated with the future Trump administration says anything about policies — deficit-funded stimulus spending for infrastructure and defense, trade restrictions, new tariffs, walls and fences, keeping manufacturing in the US, tax cuts, and what not — the markets hear “inflation.”

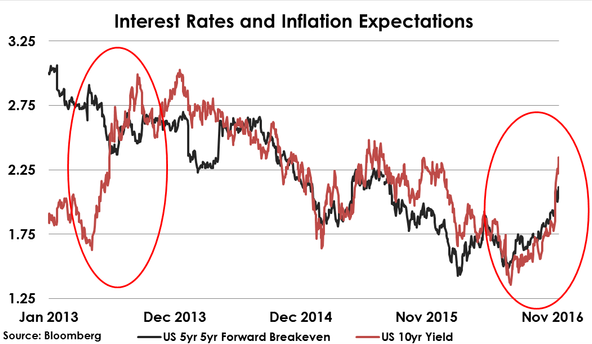

So in the futures markets, inflation expectations have jumped. This chart via OtterWood Capital doesn’t capture the last couple of days of the bond carnage, but it does show how inflation expectations in the futures markets (black line) have spiked along with the 10-year yield (red line), whereas during the Taper Tantrum in 2013, inflation expectations continued to head lower:

Inflation expectations and Treasury yields normally move in sync. And they do now. The futures markets are saying that the spike in yields and mortgage rates during the Taper Tantrum was just a tantrum by a bunch of spooked traders, but that this time, it’s real, inflation is coming and rates are going up; that’s what they’re saying.

The spike in mortgage rates has already hit demand for mortgages, and mortgage applications during the week plunged. Read… What’ll Happen to Housing Bubble 2 as Mortgage Rates Jump? Oops, they’re already jumping.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I think the exact same thing that happened last December is going to happen this December- the Fed raises is worthless rate, and the treasury market puts in a bottom soon afterwards.

agree, that did have the effect of raising short term inflation, this is a dead cat bounce, its going to take a lot more and a lot of time to normalize rates

We are aware that banks have been sucking with the narrow spread. Dumb money thinks banks are getting in the clear. While rising rates are better for their retail spread, their inventory of 10y and longer is being wiped out.

It is getting bloodier before it gets beefier.

Ah…I can see it now in Packed Movie Houses everywhere..that new Hollywood Spectacular…” Wealth of Nations Meets Son of Frankenstein” or as some one said long long ago and in a place far far Away ” Chewy I’m getting a Bad Feeling about This” lolol thanks for reading,aloha

It might be a good time to remember our old friend, “The misery index”. A lot of people have not experience high inflation and unemployment. This environment is very predicable. I will miss it.

Remember it well back in the late 70s early eighties Got laid off in 81 weeks after buying my first home with a 12 percent mortgage from my mother and having a new wife and baby Stressful yes but I pounded the pavement and got it done without a penny in unemployment insurance or food stamps just good old fashioned elbow grease and determination that a 20 something can summon when required

God help the ‘snowflakes’ they know not, what heat really is.

I remember those days quite well, all you say it quite true.

“I pounded the pavement and got it done without a penny in unemployment insurance”

That is great, more for the people who actually needed it.

Wages were way higher then, there were actual middle-class paying blue collar jobs in that era. Those have all but gone…

In an interview on RealVision, Harald Malmgren explains why any major legislation coming out of a new administration takes about 15 months to get passed. That is a long time. But what a pen and phone can do, a pen and a phone can undo so the biggest doing might be what’s undone, at least in the interim.

Thanks Wolf for this article.

I would like to attach an article from yesterday.

Ed Yardeni: The bond vigilantes are ‘back — as zombies!’

Alex Rosenberg | @AcesRose

Friday, 18 Nov 2016 | 8:04 AM ET

The “bond vigilantes” are back, according to Ed Yardeni, the economist and investment strategist who coined the term in 1983.

The gunslinging label refers to investors who demand higher yields for government bonds as compensation for a rise in inflation that is expected thanks to stimulative government policies. As bond yields rise, it becomes more difficult for the government to actually enact these policies — potentially tamping down on actual inflation.

Naturally, this lower inflation is good news for the bondholders, who, being promised a fixed amount of money, fear a decrease in the real-world value of that money.

“If the fiscal and monetary authorities won’t regulate the economy, the bond investors will,” Yardeni wrote at the time. “The economy will be run by vigilantes in the bond market.”

The term has cropped up again in recent days, as Treasury yields have surged in reaction to Donald Trump’s surprise victory in the presidential election. Most have pegged the rise on Trump’s proposals for new infrastructure funding, which some see as likely leading to economic growth and a spike in inflation.

The bond vigilantes “are back,” Yardeni said Thursday on CNBC’s “Trading Nation.”

After years of being “buried” by central bank policies aimed at tamping down yields, including the outright purchase of bonds, the vigilantes “maybe they’re coming back as zombies, the living dead,” he quipped.

Of course, the reference to central banks points to another potential driver behind the recent bond move. Trump has stated his antipathy to easy-money policies, and if his appointments lead the Federal Reserve to become more hawkish, rates will have another reason to rise.

Meanwhile, when it comes to inflation, Yardeni points out that modern-day vigilantes may be onto something.

On top of fiscal stimulus, “we might have trade protectionism, we might have fewer workers if immigration is cut back, and all these things are inflationary,” the strategist said.

“I would think that what’s really changed is that it’s very unlikely we’re going to be facing deflation or still lower inflation, and very likely we’re going to see inflation moving higher.”

Interestingly, Trump boasted during his campaign that “I’m the king of debt. I’m great with debt. Nobody knows debt better than me.”

But as Yardeni’s heuristic makes clear, if the king of debt runs afoul of the kings of bonds, things could get pretty interesting.

The big difference between the inflation of the late 70’s to 80’s is that even though the paycheck was hard to stretch, at least you had one. Employment was still plentiful then, not now.

The Micheal Milken high yield junk bond era was possible, because we still had companies we could finance, not now. The inflated asset bubble is partly because all the money is being poured into a small universe of companies. You can either own the equity or the debt, I don’t think there’s money for both anymore. Most people can’t afford either.

I recall the inflation of the late ’70’s as labor union driven. Remember COLAs? When inflation was 5% everyone got a 5% COLA and then a regular pay bump, driving inflation even higher. I remember my father saying he needed to buy a new car right away because the price would go up tomorrow.

There are no unions today. Millions remain unemployed and under-employed. And I can’t believe a Republican Congress is going to want to add yet more trillions to the national debt.

The Republican Congress has no choice but to go with an infrastructure bill. The election was a repudiation of both parties. If they sit on their hands, next time the primaries will be an embarrassment of riches, with many candidates running for each slot. The Louisiana senate race will be decided in a runoff because over 20 candidates were on the ballot and nobody got the required 50+%. This will happen everywhere if they don’t get to work in DC.

I think a major tell will be how Ryan reacts to the idea of a spending bill now that trump is in office. But if you look at trumps, plan it’s a “public-private” partnership scheme and not a big gov spending spree. Success of which is dubious.

Greatful again:

I’ve always thought of “public-private” “partnerships” as a scam (pay with tax dollars into the pockets of private entities).

That’s just my attitude because the potential for abuse is so huge (loopholes tend to get exploited). Am I wrong?

Kent, I really doubt that the 1970s inflation was driven by unions. My guess it was caused by monetary expansion following Nixon taking USD off the gold standard. Unions were just responding to price inflation, and rightly so.

Blaming unions for 1970s inflation I think is similar to blaming poor people (via CRA law, supposedly) for the 2000s housing bubble. In another 45 years, we may know whether the propagandists made that blame stick or truth prevailed!

Over here in Europe we don’t need unions for inflation, we just need government workers who collectively decide that they need another 5% pay increase despite official 0% inflation…

Even social security payouts are rising more than inflation in my country because the government can borrow and get paid for it. Pensioners might get a little less next year, but if the current Trump yield spike lasts until end of the year they will escape the reckoning again. And of course there is the legion of migrants who have so much free money that they can spend half their day in the shops … The middle class and savers get crushed but for government workers and many others the party is just starting.

The inflation of the 1960s and 1970s had its origins in the Vietnam war. Johnson’s relentless printing of money infuriated the Europeans particularly DeGaulle. That led to a lot of the run on gold and as the supplies ran low, to Nixon’s ending convertibility. It kept getting worse, and the measures used to fight it more ludicrous. I still have my “WIN” (whip inflation now) button. Finally, “Tall Paul” Volcker slammed on the brakes. The recession of 1981-82 was a doozy, but it killed inflation for a while.

Globalization and H1B people have kept salaries down bigtime My ex bosshas ten undocumented latinos that he pays ten dollars an hour for seasonal landscaping work Try getting Americans to go for that

The inflation of the 70’s 80’s actually started with the Johnson era of guns and butter. And continued thru the end of the Viet Nam War.

During the early days of Queen Elizabeth II’s reign, Winston Churchill had some health problems that were hidden from her. The monarch took her oath regarding governance seriously and questioned him and his advisors about their actions. They were reminded about the primacy of trust, and were duly shamed into reform. That was in an era when service to Queen and country meant something, certainly more than it does today.

There is no comparable institutional mechanism in the US for such shaming or similar. The concept of public or private trust seems to have fallen out of fashion, and has been driven out by media and other cultural and political actors and collaborators.

None of that indicates a desire to return to the mid-1950s, although some reflection and re-dedication to duty, service and transparency would seem to foster the greater good for all.

” Most have pegged the rise on Trump’s proposals for new infrastructure funding, which some see as likely leading to economic growth and a spike in inflation. ”

This is getting repeated over and over again which is exactly what someone wants.

Explain to me how the current administration can take the national debt from about 4 trillion to 20 trillion in 8 years and NOT spike inflation? I just read that actually this year will be 2.4 trillion not just under one trillion. Granted we all know full well that inflation is significantly bigger than the fake data that the government prints and everyone pretends to buy hook, line, and sinker. Show me where all that money went to improve this country, show me where the jobs ( less bartenders and waitresses) were created, show me how Americans are better off. Please show me.

Now everyone is on this bandwagon, before this man IS EVEN sworn in, at how rebuilding the roads, bridges, buildings, etc (that ALL the presidents have let go to ruin) that he will create inflation by adding ONE TRILLION IN DEBT. That 20 trillion meant nothing right? None of any of us even know how he plans to finance it….like savings bonds? like special coupons? like a gas tax? Get a grip, we are not in junior high school.

IS EVERYONE AWAKE? or just repeating the current slogan that is popular on worthless media?

The MSM sure are presstitutes as Gerald Celente calls them Thank goodness for people of truth like Wolf and Mr Celente

Because little of this debt did anything other than replace debt that would have been defaulted on.. It wasn’t only the banks that created the debt either. So little of this borrowing actually trickled down to Main Street. It was recycled thru Private Equity and Hedge funds along with the other TBTF institution into oil drilling, large scale purchases of foreclosing real estate to be reused as rentals (both residential and commercial), war, and stock buy backs.. It has been Socialism for the elite on steroids.

The taxpayers are on the hook for it and that was why and is why those in power keep giving tax breaks and subsidies to the elite while raising fees and hidden taxes on the middle class. They deserve and are the ones.. We are just the peons. It is no wonder world trade is faltering.. The next big crisis is just around the corner waiting for some trigger.

“Explain to me how the current administration can take the national debt from about 4 trillion to 20 trillion in 8 years and NOT spike inflation?”

You ask a very profound question. The answer lies in the fact that with massive amounts of debt in the system, we should’ve had a significant deflation and depression, and the stock market should be about half what it currently is. We didn’t get the deflation/depression because of the money that was poured into the system.

A simple example: Chase Bank was bankrupt. The shareholders, bond holders, and many of the account holders should’ve been wiped out, and the assets of the bank liquidated. Instead, courtesy of taxpayers (and non-taxpayers via inflation), voila, everyone was made whole.

You know, this could be Herbert Hoover – 2.0 hopefully not.

The probability is high. Big bubbles coming soon.

Big bubbles have been here for the past nearly 8 years and are NOW BURSTING, especially with prices in the bond markets which are much larger than the equities (stock) markets.

https://en.wikipedia.org/wiki/Causes_of_the_Great_Depression

They don’t mention Hoover much at all as far as causes of the Depression goes. He was basically given bad circumstances which he had little control over. Did a lot to help Europe, and was against war. If the current and future President were more like him, the world would be better off.

The existence of Hoover is not a cause. Economic policy of the time wasn’t up to the task and the policy makers were too locked into their ways of doing things. It was the massive spending of WW2 that ended the Great Depression. Don’t they still teach in middle school that Wikipedia is not a source to be cited?

If a kid is looking up anything anywhere other than TV he’s ahead of most.

Most teachers will have no opinion or knowledge of Hoover or the Depression. Oh, sorry, the fact of the Hoover Dam may ensure him a certain place in their minds.

As for Hoover and the oft criticized Fed, Keynes was not yet influential, the Depression had just started but would turn out to be unique for its depth and length.

The idea that credit or money could be created without being backed by gold or at least something was in the minds of visionaries, not government.

The informed citizen would have thought the idea highly suspicious, if not insane. Didn’t the bill said: Pay to bearer.

Pay what?

Asking why the Fed in 1932 did not do a massive QE is like asking why airliners at the time used piston engines instead of jets.

Herbert Hoover was a poor but brilliant Iowa farm boy who went to Stanford, became an engineer, and became wealthy and famous as a mining engineer. He led humanitarian relief efforts in Europe after WW1 and later became Commerce Secretary. His political experience was limited. Exactly right that the idea of just printing money would have been laughed out of town in 1930. The government reacted with the tools that they understood they had. Poor Hoover gets all the blame.

Herbert Hoover was just the patsy. He inherited the bubbles – in the real estate and stock market. Sound familiar? Watch it happen again.

Still speculation that massive spending will occur. I took a look at the trump infrastructure plan yesterday and it seems rather implausible. When reality sets in that things aren’t really going to change much and that 95M eligible workers aren’t going to work…back down it will go

Real estate market has been getting frothy here in small city rust belt metro area in IL. Low interest rates must be driving it, but only so much house can be purchased on a fast food or retail wage. Increasing mortgage rates will kill the real estate market here fast. Industry here continues to downsize and/or automate or relocate. The job base may be holding steady or even increasing while the average wage goes down.

Yes and the automation and jobs leaving was not the Dems fault at all. No party will stop it but the sad uninformed and undereducated base of Trumps will continue to suffer as the jobs they need are sent off or automated. He can villify trade all he wants but US trade with the world has been declining for some years now.

His so called infrastructure plan is a wealth transfer. Period. Its a joke and has not full support in Congress. It sells well now but the Congress are not fools in terms of political survivial. They all face reelection in the House and 30+% in the Senate. That plus Trumps lack of a strict voter mandate. He lost the popular vote by 1.7mil as of today. He has a small window to get anything done and he faces a Congress intent on taking back the Executive Order privilege Obama has enjoyed.

Sen McConnell said it best about ‘drain the swamp’ – We have elections in case Trump was not aware. We already have term limits. Lesson – they fully know Trump is temporary to say the least LOL.

Smooth sailing my asssshhhhh

On 8/24/16, the Franklin California Tax Free Income Fund had a net asset value of $7.82. Yesterday (11/18) it closed at $7.38, for a drop of 5.6% in less than 3 months. In the world of retail bond funds, this fund is one of the largest. As my wire house desk partner used to say, “Last chance to get out.”

Its not the election and its not the dollar and it isn’t those last few bargain hunters looking for the last deal in a bigger house.

Its when the fed said, “they would allow the economy to run hotter than 2% inflation. Like say 4%?

The market instantly realized these fools at the fed are Crazy desperate and started reflating in anticipation of the fed doing QE 4?

This QE is going to be dicey but what are the alternatives. A collapse in loan originations and deflation in prices?

If the fed is to play ” buyer of last resort” they would want to know they are getting decent bargains? The fed likes undervalued credit a lot more than buying overvalued shares!

The Federal Reserve versions of QE (Quantatative Easing) fully ended on October 31, 2014, and there will be no further QE. All of those QE funds were merely used to purchase EXISTING SECURITIES consisting of US Treasuries and MBS instruments from member banks with the proceeds deposited into the reserves accounts of those member banks inside the Federal Reserve which is where those funds remain. QE has no impact whatsoever on the US economy as it was a CLOSED LOOP series of transactions with none of those funds going anywhere other than into the reserves accounts of those member banks inside the Federal Reserve where their earn IOER (Interest On Excess Reserves) and where those funds have always remained parked.

QE is a closed loop but it supresses interest rates, which impacts the economy. There is no doubt about that. If a law were passed today outlawing future QE, interest rates would skyrocket.

While rates have increased by 100 basis points,one must consider how low a level rates were less than 6 months ago. U.S. interest rates were at or near 200 year lows during the summer,while rates in Euroland/Asia were at 5.000 year lows.

REAL yields on the 10 Y were only 15 basis points on Nov,8.Today they are @ 44 basis points.

10y breakeven inflation rates were at %1.34 on 6/27,%1.73 on 11/8 and ~ %1.90 yesterday

The Republicans will control the Congress and the Presidency.Almost all in Congress are amenable to infrastructure projects in their own district/states.They can vote for such spending bills without worrying about giving credit to the Democrats.Many desire more military spending also.

The large additional factor is to what extent will the Trump trade policy result in a trade war ,especially with China.It appears that China has already started to sell off some some of its huge horde of Treasuries as its first salvo in such a war.If Trump is really serious about forcing the Chinese to play by the rules,more selling will probably happen.

And then we have potentially the biggest issue of all ,the black swan ;how much and when will the ~500 trillion in derivatives be affected.As rates move higher and currencies move ,it is inevitable that there will be some pain among some derivative players.How much blowback will this cause in the markets no one knows

I have mentioned that I am a trader and have been consistently profitable trading TLT. UNFORTUNATELY ,I started to build a small long position @~123.5. Friday was very interesting because it was quiet most of the day.Then all of a sudden stocks, gold and bonds were hit at the same time,while the dollar rallied.Somebody was a large seller and my guess it was the Chinese.

“… what extent will the Trump trade policy result in a trade war, especially with China. It appears that China has already started to sell off some some of its huge horde of Treasuries as its first salvo in such a war.”

China’s monetary and fiscal policy is not all that heavily influenced by “Trumpism”, I think.

For example China began dumping U.S. debt well before Trump “exploded on the scene”:

http://www.zerohedge.com/news/2014-02-18/china-sells-second-largest-amount-us-treasurys-december-and-guess-who-comes-rescue

No one is going to let Trump that close to the controls of the economy. His supporters are in for a big surprise.

China’s holdings of US Treasuries have remained in the range of $1.2 trillion to $1.3 trillion over the past 8 years and are barely changed. That amounts to less than 7% of the total outstanding amount of US Treasuries and China needs to hold these to back Letter of Credit for global trade transactions and the total amount that China holds is highly unlikely to change to any degree of significance in the foreseeable future. The same is the case with Japan as to their around $1.3 trillion in US Treasuries.

I don’t know about that. The rest of the world is desperately short of dollars, and the easiest way for countries like China, Japan and Saudi Arabia to obtain dollars is to liquidate their U.S Treasuries. China especially has spasms of treasury selling every few months related to the increasing difficulty China’s banks are having in obtaining dollar funding. It’s only a matter of time before the dollar shortage reaches a critical level, and the treasury sell off reaches a more serious stage.

There is no “shortage of US dollars” at all, and the only issue regarding US dollars is the exchange price between other currencies and the US dollar is soaring in exchange value and is now at 100.35 on the DXY which is the new high for 2016.

Saudi Arabia owned very little in the way of US Treasuries and it doesn’t matter a hoot what they do with them, but the fact is that they need them to support LETTERS OF CREDIT for their oil trade and they would be hard pressed to find any acceptable replacement for them.

Saudi Arabia ONLY OWNS $117 BILLION OF US TREASURIES (government debt) and not $1 trillion at all.

U.S. Discloses Saudi Holdings of Treasuries for First Time

Treasury Says Saudis Hold $117B of US Debt…

http://www.bloomberg.com/news/articles/2016-05-16/u-s-discloses-saudi-arabia-s-treasuries-holdings-for-first-time

Total outstanding US government debt in US Treasuries is over $19.5 trillion and $117 billion is like a ROUNDING ERROR and of no significance whatsoever. The annual US Treasuries market is a $12.8 trillion a year market and more than $7 trillion in NEW US TREASURIES are issued each year and US Treasuries are the MOST LIQUID BOND MARKET IN THE WORLD.

The OTC/MBS and CMBS derivatives sphere is in turmoil.

The main fear is beginning to show, as foreclosures are on the rise.

This is putting pressure on the very financial instruments, that the sectors derive their so-called ‘value’ from. Now, mix in the global lack of liquidity turmoil in the bond markets, higher inflation, falling real estate (residential & commercial) values and we have the formation of a “perfect storm” brewing. Each “feeds” on the other, completing the downward spiral cycle.

Sounds like a plausible scenario.

I wonder how these developments will affect the bonds issued by companies for the noble purposes of share buybacks and m&a.

Realist: The outstanding bonds of these companies will go down in value along with all other bonds. Pity the fools who bought Italian government bonds due in 2047 with a 2.7% coupon at a price of over 108 in early Oct. 2016.

Yields (interest rates) will rise significantly on these bonds issued by corporations as RISK OF LOSS IS INCREASINGLY PRICED IN and that should have been the case all along. Corporate debt is now around $14 trillion and vastly exceeds the amount of cash held by corporations in the US.

Trump’s infrastructure plan is not going to create any new infrastructure, it is just going to take plans that were already in place and now make them tax free. The big con being exposed daily.

https://www.washingtonpost.com/opinions/trumps-big-infrastructure-plan-its-a-trap/2016/11/18/5b1d109c-adae-11e6-8b45-f8e493f06fcd_story.html

I’m not so sure.

It might be that Trump will (as Trump often does) do the unimaginable.

For example, he could decide to put broadband via glass into every U.S dwelling (shades of the REA).

Trump isn’t going to do any such thing. Trump has no political experience, doesn’t know how the game is played, and even right now is totally being used and played by a variety of political players on the right. Trump is going to get what Congress is going to give him. Congress gets to decide if they are going to stick to no wild deficit spending or are they going to reveal themselves as total political hypocrites and go on a wild debt/deficit spending spree. Trump, like that other political neophyte Herbert Hoover is going to get stuck with it when the whole thing blows up if Republicans spend.

We’ll see.

I predict that by mid July 2017 we’ll see the Trump Administration and various factions of Republicans and Democrats in Congress involved in an ongoing fight with each other and accomplishing very little. That isn’t necessarily a bad thing.

Trump and his advisors know perfectly well “how the game is played” and they will changing the rules of that game very substantially over the coming 4 years and then likely over the following 4 years!!!

… one good flush … deserves another … and away we go ….

Now is the time to Finally buy Gold and Silver if you believe “money” will be worth anything in the future. I say that as someone who is not a goldbug, but someone who recognizes the modern monetary system as a comedy of the absurd.

Those EXTREME RISK COMMODITIES are already massively collapsing and are preposterously overpriced and are headed for massive further falls as they revert to their means of around $456 per ounce for gold and around $8 per ounce for silver.

“extreme risk commodities” are already massively collapsing,so your Logic tells you there is no more “Risk” in the markets? makes perfect Sense,Lol. I am especially intrigued by your brave Forecast of 465.00 per oz of gold,were you struggling with 367.56 VS 486.76 but your extensive research led you to settle at 456.00? Fascinating,keep us up to date,would love to buy more Gold Eagles at 87.00 may even wait for 25.00 ? hopefully yours….

The same money that was used to bid up stocks and real estate was used to bid up commodities. Money was cheap (low interest), now it is less cheap hence the rising value of the dollar.

Also, the price of any metal is largely set by the price of extraction (energy). Energy is cheap, so on that basis metals are over-valued.

The current arrow for metals ‘right now’ is they are set to fall further.

But we could easily have another war in the middle east if the Putin-Trump bromance vanishes and it’s likely Trump’s spending plans will be blocked.

So what’s that all mean? – It’s a traders market for metals until further notice with a downward bias.

Also, if US dollar tanks then buying real things now is a better plan of action – particularly freeze dried ice cream and ammo.

Gold will very soon be well below $999 an ounce and headed much lower. $456 is simply the MATHEMATICAL MEAN of the price of gold and it may go as low as $232 per ounce. Silver’s mathematical mean is $8 per ounce and it may go as low as $4 per ounce. When other financial assets fall in value that drags down commodities sharply and gold and silver are just 2 of the major 27 commodities in the world.

Adam that is a preposterous hypothesise in my opinion With the amount of money in circulation those numbers are unrealistic Why do you hate honest money so much?

Gold and silver have NOTHING WHATSOEVER TO DO WITH MONEY and are just preposterously overvalued little niche collectible fungible commodities with no monetary value or utility whatsoever in our modern electronic digital money world. They are not accepted anywhere in the world for anything other than the face value of coins they are denominated in and in the case of American Eagle 1 oz. gold coins that is $50.

If the economy crashes to such a level, a bag of beans will be worth more than an ounce of gold. In fact, gold and silver would be as worthless a dollar bills.

lets make a Deal Ed! when “the economy crashes to such a level” i will trade you 10 bags of Beans for your 10 Ounces of Gold,assuming you own 10 Ounces of Gold,I’m a Sucker for a Bargain!

Silver is also amazing as an immune booster, wound healer, virus killer, you’ll be lucky to buy any if the economy crashes.

In a crashed economy, silver could fall all the way back down to around $2 per ounce.

Can’t wait to see rates rise in Europe too; until now it’s around +0.1% for mortgages which is relatively big but doesn’t threaten the bubble; we need rate increases of 0.5-1% for that. And probably even more before the current company bond bonanza stops, and big business has to actually produce something useful to stay afloat. When finally EU governments also have to pay serious money for issuing debt, we will finally have the first requirements in place for healing the economy.

Not much chance of that yet in Europe, but it’s encouraging to see this happen in the US, so people realize that central banks cannot stick to ZIRP/NIRP forever and that government bonds and below-1% mortgages are not risk-free like the banksters and politicians want people to believe.

nothing goes to heck in a straight line.?

DRYS – Dryships Inc . – for a while it did

Please avoid any references to the fake media “Washington Post” as you run the risk of being characterized in the same bucket

Yeah,let’s hear what the New York Times has to say about that Trump Guy,you can always count on their unbiased and fair Reportage as well,”if it’s fit to print,it’s News” or something….

NEW YORK SLIMES PROMISES NOT LIE QUITE AS MUCH ANYMORE…

NYT publisher vows to ‘rededicate’ paper to reporting honestly…

http://www.foxnews.com/politics/2016/11/12/new-york-times-publisher-vows-to-rededicate-itself-to-reporting-honestly.html

Wow, I’m happy to have found this site, insightful comments like I used to see on zerohedge.

I strongly believe Trump is being used to crash everything. The world couldn’t possibly recover from this level of debt, and the masses are so ignorant they will believe it all Trumps fault (not the bankers).

In Australia if the banks raise rates (instead of keep dropping them like everyone thinks) there will be chaos by Easter.

No, the US and global markets are RIPE FOR CRASHES due to extreme MANIC SPECULATION on false perception and hopium over the past 7 years since March 9, 2016 when FASB Rule 157 (“mark to market”) was essentially repealed. No regard at all to RISK OF LOSS has existed and now the RISK OF LOSS is higher than ever and the commodities, equities (stock), and real estate markets are all going to come crashing down as interest rates with PROPER PRICING OF RISK return to the bond markets in the US and globally which is precisely what is happening now.

Exactly. Lot of hot money looking for yield but not going into anything all that productive. Just a lot of speculative action as has been mentioned here such as farm land, car loans, residential and commercial real estate.

just think about it. It Trump fails then so does capitalism and the republicans…the party will NEVER be elected to higher office ever again.

what would come after a failed Trump administration scars the living shit out of me……..pure 100% socialism.

Some would argue that capitalism has died a lot already. What with taxpayers bailing out big corporations and other forms of corporate welfare. It appears to me that the main question is how much socialism you want in your capitalism, or how much capitalism you want in your socialism. And that seems to depend on whose biscuit is getting buttered.

As it always has been.

Capitalism is now Crony Capitalism which means a totally corrupted version or as some would say Fascism is what we have rather than Capitalism.

i couldn’t care less what rates are, I’ll never be able to afford a home no matter what the damn rate is.

What if the mortgage rate is -2%, as it might be someday in NIRP Absurdistan?

That’s the big question isn’t it! will we get QE 4 and 5 or will inflation force them to ratchet up IR pronto. i am usually the optimist,but my hunch is the worst of all scenarios,STAGFLATION,then what?

Sounds alot like 1980 milking What was Adams gold price again 456.?

Interesting historical chart,inflation adjusted price of gold,Frederic,notice the two spikes,1980’s inflation and the the ramp up to the 2008 financial crisis. would be fun to overlay with the real estate price chart as well? https://snbchf.com/chf/chf-history/volcker-shock-oil-glut-emerging-markets/

I feel your pain,living in Californica i remember when the average worker could easily afford a home mortgage despite much higher interest rates (80s and 90s),my only conclusion is that something went seriously off the rails.I’m not smart enough to pinpoint the cause but my best guesses are the TRUE unreported inflation,massive population growth via legal AND illegal immigration and of course the money printing frenzy of the last 10 years. i am in the construction business and have seen a crazy influx of foreign money especially in the last five years and i am the last person to complain,it’s been a great run,just have a feeling this will somehow correct back to “normal”. i have several Chinese clients who own multiple properties in mainland,HK and Cali,money is usually no object and properties are bought cash,2.4 million $ bank wire. the party goes on,how much longer is the big question.

Easily afford a home mortgage? Thats not the memory I have but maybe I was the inomaly

“Easily afford a home mortgage?” Well, that is what the realtor said.

I guess that is a judgement based on one’s perspective and is related to tolerance for debt, income expectations, financial obligations and what else one has to do with one’s money.

well,perhaps i am just going by my recollection of things,bought my first one BDR condo in SD in 1990 for 36.000,that same condo would sell for roughly 275.00 today. did wages and income go up 7 fold since then? not as far as i can tell,of course i understand that the same may not be true in other parts of the country,i’ll give you that.

This recent turmoil in the markets is nothing more than so called ‘smart’ proving that in fact they are really, really dumb.

All those so called ‘smart’ people were banking on their ole bought and paid for gal, Hillary, to get into the White House (Instead it may be the other house) and based their investment strategy on that idiotic assumption.

It didn’t happen and now we are seeing the results.

Any of Trump’s spending plans are far enough into the future so we’ll see them coming.

Just another bout of induced market panic by a bunch of snowflake investment managers.

Give it another month and it will settle down

With the end result being much higher and increasing yields (interest rates) in the bond markets and that trend will continue out through 2017 and 2018 as they move upwards towards proper normalizing at around 5.25%.

It is always, Lather, Rinse, Repeat. Until one runs out of shampoo.

Shampoo is ultimately confidemce, since money is conjured.

Reversion, then inversion? Or is it the other way around. Dont tell me. I want to be surprised. Think my grandparents saw this movie, or. Was it 1860?