What will sink the US auto boom?

In the subprime auto loan market, things are turning ugly as delinquencies and losses have begun soaring. Specialized lenders – a couple of big ones, and a whole slew of small ones that service the lower end of the subprime market – slice and dice these loans, repackage them into auto-loan backed securities (auto ABS), and sell them to investors, such as yield-hungry pension funds.

Delinquencies of 60 days and higher among subprime auto ABS increased by 22% year-over-year in August, Fitch Ratings reported on Friday – now amounting to 4.9% of the outstanding balances that Fitch tracks and rates. And subprime annualized losses increased by 27% year-over-year, reaching 8.9% of the outstanding balances of auto ABS.

Even delinquencies among prime borrowers are rising, with delinquencies of 60 days or more increasing by 17% from a year ago, and annualized losses by 11%, though they’re still relatively tame at 0.4% and 0.6% respectively of the balances outstanding.

And according to Fitch, the toxicity level in the subprime auto ABS space isgoing to rise, with “subprime auto losses to pierce 10% by year-end.”

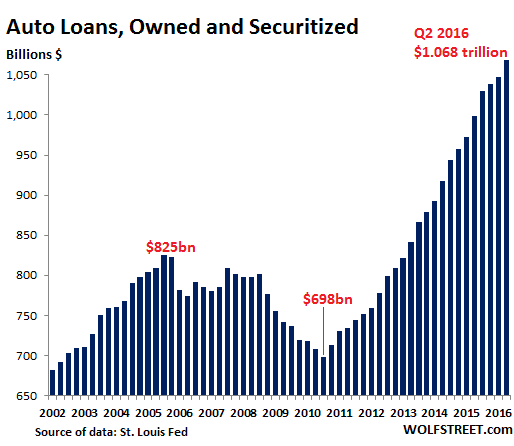

Total auto loan balances, both subprime and prime – given the soaring prices of cars, the stretched terms of the loans, and the ballooning loan-to-value ratios – have been skyrocketing, up 46% from the first quarter in 2011 through the second quarter in 2016, when they hit $1.07 trillion:

Fitch blamed the higher losses on several factors:

- The “weak 2013-2015 vintage pools” – hence the more recent loans, when underwriting standards in the zero-interest-rate environment got increasingly loosey-goosey

- Seasonality

- And wobbly wholesale values of used vehicles.

High wholesale values of used vehicles are a gift from the government to the entire industry. The federal $3 billion cash-for-clunkers program that kicked off in July 2009 wiped out the cheaper end of the used vehicle market, to the detriment of lower-income people. Vehicles they could afford were largely removed from the market. But to heck with these folks. They had to figure out how to scrape more money together or go deeper into debt to be able to buy higher priced vehicles.

That concentration of demand has distorted and inflated used wholesale prices ever since. It tremendously benefited auto makers and the industry overall. The Manheim Used Vehicle Value Index, which tracks wholesale prices of used vehicles, shot up to record highs in 2010. It hit its all-time peak of 128 in 2011, up about 10% from the previous all-time peak set at the end of the bubble in January 2001. After some significant zigzagging since 2011, it was a still lofty 126.9 in August (chart).

{kind=link}

High wholesale prices have been a boon for the entire auto industry. They raised trade-in values, which helped people to buy ever more expensive new and used vehicles. They raised profits for dealers. They boosted prime and subprime auto lenders and their financialized products. They gave rise to a whole gaggle of smaller subprime auto lenders that have crowded into this high-profit securitization market.

And high wholesale values are crucial for lenders when a loan defaults, and lenders have to repossess the vehicle and sell it in the wholesale market. A high wholesale value lowers the loss. When wholesale values fall, losses rise.

Now used vehicle prices are showing signs of wobbling rather than soaring. And they’re scheduled for a descent, according to Fitch:

[D]espite the current strength of the wholesale vehicle market, used vehicle values will come under pressure from slowing consumer demand and rising supply in the latter part of the year and early 2017.

This would come at the worst possible time. New vehicle sales seem to have peaked last year (unit sales were down 0.5% in September year-over-year). Automakers have piled up incentives to move the inventories off dealer lots. And according to Fitch, “used supply is rising fast, driven by higher off-lease vehicles and trade-in volumes.”

These trends are going to hit used vehicle values, and Fitch expects to see “lower recoveries in auto ABS transactions as a result.”

Fitch tracks a whole slew of subprime lenders. The two giants, GM Financial’s AMCAR platform and Santander Consumer USA’s SDART platform, combined account for 54% of the index. The remaining 20 or so are second and third-tier subprime lenders, many of which have sprung up during the auto loan boom since 2012, as Fitch put it, “coinciding with the expansion of auto lending, particularly in lower subprime credit buckets that these lenders focus on.”

Turning points like this are just the beginning of a new trend. Given the flood of liquidity and still historically low interest rates, the new trends will fall into place gradually. Eventually lenders will begin to wheeze and investors will balk at taking on ever more toxic securities. And the money spigot will tighten notch by notch, causing a liquidity crunch and soaring losses in that asset class, and contributing to the “so-called car recession,” as Ford had called it in its 10-Q filing.

Other industries that have to deal with the American consumer are already struggling with “very challenging” sales trends. Read… Restaurant Industry, Leading Indicator of US Economy Sours, Bankruptcies Pile up

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The solution to this madness is very simple.

When you buy a car, or a house, you have to put down 20%.

Also, you have to have a clean credit report.

Do this, and this nation will be stable and grow on strength. BUT, why do the “banks” and the Federal Reserve, and the various government ignore this logic? Why. Is there a reason? Is there something going on that we are not allowed to discuss?

“When you buy a car, or a house, you have to put down 20%. Also, you have to have a clean credit report.”

Hey, that’s no way to generate a bubble. And it’s for sure no way to generate fees.

“Is there something going on that we are not allowed to discuss?”

Talk about it all you like. But what can you do about it? You can talk about how booms are profitable – and so are busts, because you taxpayers get to bail them out, also profitably. The big boys have their short strategies all lined up.

TPTB: “Suckers!”

At this point in the economy, being responsible is actually quite harmful. Take out a subprime loan and you can literally drive big banks into bankruptcy.

“Take out a subprime loan and you can literally drive big banks into bankruptcy.”

If only it were that easy.

That’s right Walter. It’s clear now that their “solution” for the economy since 2008 was to create the most massive bubbles possible, in hopes that would pass for an economy.

Duped most people, who believe in whatever puts a paycheque in their hand.

RE: …BUT, why do the “banks” and the Federal Reserve, and the various government ignore this logic? Why. Is there a reason? Is there something going on that we are not allowed to discuss?…

—–

The thing that is not discussed is the falling real inflation adjusted median wage for the last 30 years. When this is combined with the soaring housing costs in most areas [now far in excess of 1/3 of income], most people cannot hope to accumulate a 20% down payment, bringing the car industry to a halt, so its 0% down and 84 month financing or the “rescued” car companies die.

If 20% down were required… that would kick off a deflationary death spiral….

The auto and housing markets would collapse overnight.

People are flat broke. They don’t have 2% never mind 20….

“When you buy a car, or a house, you have to put down 20%.”

Same should apply to medical care and college

Delinquencies do not necessarily impair sub-prime auto loans.

The bank owns the vehicle, which they repossess and sell. If sale proceeds plus payments and fees is greater than their purchase price plus costs, the loan is profitable even when delinquent.

The borrower then returns to the dealer to purchase a used vehicle that the dealer bought at Mannheim (auction) from Santander, financed by yet another sub-prime lender.

Life is good.

I think you forgot the sarc tag: “If sale proceeds plus payments and fees is greater than their purchase price plus costs, the loan is profitable even when delinquent.”

That’s hilarious, actually.

Huh? That’s how it works for sub-prime lenders. Buy the car, collect a few payments, seize it, then sell it. Rinse, repeat.

Do you really believe that Santander needs the borrower to make more than a certain (low) number of payments?

BTW, how many retail car loans have you placed with them? Do you know what they pay for their cars?

Zero and no, right?

You’re confusing “note lots” with the subprime lenders in the article that securitize loans into ABS. Concerning your last question, check out my bio (under the Wolf Richter tab) if you want to know.

Once the supply of good- as- new used cars exceeds a certain point the system begins to break down.

Right now there are unsold 2014 units. This threatens the retail price of new incoming stock. Some dealers have sold new units to themselves, some with ultra- low miles will be called demos, whether they are or not.

The basic reality is that vehicle production exceeds demand- the channel has been stuffed.

Financial engineering (7 year loans etc.) can only delay the point where production must be cut.

Key observation: “The basic reality is that vehicle production exceeds demand- the channel has been stuffed.”

And more are coming on-line all the time. One first step is to prohibit using tax exempt [economic development] municipal bonds to finance additional automotive assembly and component factories and/or granting tax preferences/exemptions for automotive assembly and component factories as this can only cannibalize existing operations and will generate no net new jobs.

I just sold an old Klepper Kayak to a guy who came over from Vancouver to Nanaimo on Van Isle to buy it.

He was driving a 2012 Mazda 5 SUV that he’d paid 12,000K C$ when it had 12K kilometers on it- practically a demo.

I doubt he bought it from a lot but don’t know.

The catch is you have to have cash to get deals. He’d probably used a HELOC where the house borrows the money.

LMAO… Most loans on these overpriced cars will be under water… 0% down ring a bell?

Buy any new car at the dealer and drive off the lot with 0-5% down and as soon as you drive off the lot the car price dropped 20% in respect to value to loan…

After repo fees, and is all said and done noway the bank makes money.

bunch of millenials living with their momma driving Bimmer, Benzos and Lexuses. uhhh and I almost forgot… bunch of idiots driving lifted HUGE pick ups that I see on the 101 and 280 in the Bay Area. One thing is to see those on the 99 central cal, as many are ranchers… but in San Jose… LMAO…

Every day I listen to the radio here in SF Bay Area some annoying advertising from “Paul Blanco” :No credit OK, bankruptcy OK, NO money down OK, No Payments for 3 months… and the list goes on…

One of my friends is in the business and he says he get his money back on a used car with the down payment. The monthly payments are just gravy. He finances the whole thing. He expects to repo 70 percent of the cars and then sell them again to someone else. I think that is the way the car business is at the low end. So your statement makes sense. The consumer jsut becomes a debt slave to the car dealer since they need cars to take their six kids to the MediCal dentist appointments for braces or Obama Care contractor pediatrician.

One other issue-a person with a recent repo has one choice-a buy here-pay here that keeps a copy of the key and many have interlock systems. Even after some time has passed, a repo is one way for a loan to be turned down or offered at a significantly higher rate. They can’t return to a dealer to get another car right afterward. Heck, everybody’d get repo’d then!

We have a dealer’s license and frequently buy at the Manheim auction in Portland. A lot of repos come through there. Some (not all, but a good many) of the cars are pretty trashed, sold as is of course, and need a lot of repair, so those ones sell for pennies on the dollar.

On a side note, I’ve seen a lot of those Mercedes Smart Cars at auction lately– I’ve never purchased one tho.

Kasadour :

Do you know anyone in the Seattle/Portland area that works as an intermediary for auction purchases? Im looking to pick up a 2013 RX350 and I’d like to hire someone with a dealer license to purchase one for me.

I know quite a few (besides myself) in the Portalnd where I live.

You can email me for details at [email protected].

Because MB Smart is dumb, especially when they came out- 22 K? $C.

And now a Nissan Micra is $9999 $C

I don’t care what kind of software is on board. there is no way I’d take one of those things around a corner over 50 MPH.

My husband hates them. But then again he lives for big and fast cars. We recently purchased a BMW Alpina B7- Turbo. 8 cylinder. It’s one bad a$$, mofo car.

Humans are the only animals you can skin more than once. Anonymous.

Great comment. Voters for both Dems and Repubs are proof positive.

I’m not voting anymore unless the candidate is Mr. Nobody.

“I’m not voting anymore unless the candidate is Mr. Nobody.”

You can buy a t-shirt that will come in handy in a few months: “Don’t blame me. I voted for the meteor.”

http://thehill.com/blogs/blog-briefing-room/news/giant-meteor-of-death-hitting-earth-poll-voters-prefer-over-hillary-clinton-donald-trump

“More than 1 in 10 voters say they’d prefer a giant meteor hitting earth over supporting Donald Trump or Hillary Clinton.”

You could look at the bright side. Except there isn’t one.

The meteor will be very bright for a few moments. That is a small bright side.

They have lived sheltered lives.

We need a law to create a fictitious party called The Big Fat Finger party. That would be my favorite party to vote for over the current choices. Small comfort, but still a progress.

“The federal $3 billion cash-for-clunkers program that kicked off in July 2009 wiped out the cheaper end of the used vehicle market, to the detriment of lower-income people.” Thanks Wolf for pointing out some of the negative repercussions of that program. If memory serves me well, the Germans implemented a similar, wildly popular program. Can’t help but wonder if they also sold themselves similar emissions-faulty vehicles during that period? If so, that is a heck of a lot of repairs they need to make!

The reason you don’t have 20% down payment is because the majority of people don’t have the available cash. Stop bailing out banks and this kind of lending will disappear.

Automobile prices are outrageous. The value and quality are horrible. Had one of the Nissan Murano’s that burned. Value dropped about 20% right off the lot, had it 6 months, then it burned, lost my down payment, lost my shorts. Something is wrong in America. Can the 10 year auto loan be that far off?

Nissan Murano – Caution – Flammable https://www.youtube.com/watch?v=kuDpbF7hs-I

Summary

Nissan North America, Inc. (Nissan) is recalling certain model year 2016-2017 Nissan Maxima vehicles manufactured February 10, 2015, to August 19, 2016 and equipped with Intelligent Cruise Control, 2015-2017 Murano vehicles manufactured August 22, 2014, to August 19, 2016 and equipped with Intelligent Cruise Control, and 2015-2016 Murano Hybrid vehicles manufactured August 22, 2014, to July 19, 2016. The affected vehicles have Anti-Lock Brake (ABS) actuator pumps that may allow brake fluid to leak onto an internal electrical circuit board.

Consequence

A brake fluid leak onto the circuit board will cause your car to ignite.

Advice

Park outside. Do not buy this car, new or used.

That’s why you don’t buy Nissan. They’re about as reliable as the domestics. They’re like the Japanese Chrysler. No car company is perfect but some tend to be less perfect than others.

I’ve got a Lexus here with 250K miles on it and a Honda with 203K. Neither one has had any major repairs. It’s possible to buy a decent car, you just have to be picky.

I happen to know the Versa is a pretty tough piece of machinery because I know a young guy who has treated his girl friend’s brutally- 2008 still no majors.

And I mean brutally.

Of the car loan goes into default, do the banks actually repossess the car and sell it on the open market? If so, cpull there be a glut of 3 and 4 year old are cars on the used car market in the next couple of years?

No. The Bank calls the guy, the guy calls the repo industry rep, they get it done….

That’s how the bubble bounces……

.

If anyone is interested, I’m selling gambling debt backed securities. Let’s crank this baby up to 11!

I’m selling Ferengi futures …….

….any takers ??

i LOOOVE love love and LOVE the Ferengis!

Car sales declining year over year: http://www.detroitnews.com/story/business/autos/2016/10/03/september-auto-sales/91460716/

Ford appears to be the big loser. Check out the declining fleet sales.

Back out trucks and all the Big Three are in trouble- especially GM.

The ads are getting nasty!

10 years ago you never mentioned the competition- now it’s a bitchy cat fight.

Have you seen the one from GM where they throw what looks like an ordinary tool box into an aluminum box (Ford 150) and it rips a hole in it?

Assuming it’s not a fake- can you imagine what’s in that tool box?

I wouldn’t be surprised if it’s 100 lb of lead, and the tool box has been reinforced to prevent it bending.

I can guarantee Ford is taking a LONG look at the ad. If it was faked- law suit.

I’ve been tempted to use a drone to monitor the progress of car sales at my local dealerships. These lots are overflowing with cars, to the point of dealers leasing adjacent property to park the inventory. Literally, in a 3 mile stretch, thousands and thousands of new cars-in a state with 1,000,000 population

Haha. Same here lol. I am at ground zero when it comes to subprime lending. I work at a Nissan dealer in Dallas/FtW. Anybody that walks in drives off in a new car. Not enough offices for the sales people. Crazy what’s going on here.

Even delinquencies among prime borrowers are rising, with delinquencies of 60 days or more increasing by 17% from a year ago, and annualized losses by 11%, though they’re still relatively tame at 0.4% and 0.6% respectively of the balances outstanding.

Holy MOLY. It looks like there is a loooong way down.

Got any insight as to how the new Credit Risk Retention rule will affect auto sales?

was this John Oliver link posted here on this site before? it’s his almost-18-minute routine from his show, Last Week on Tonight, on subprime auto lending. it’s as horrifying as “million dollar shack” and way more hilarious because of the silly hats and accents.

https://www.youtube.com/watch?v=4U2eDJnwz_s

Maybe it’s too late to get an answer here, but I’ll ask regardless.

If these lending institutions securitize all these loans, how would they be liable for any defaults? Wouldn’t that fall on the pension funds or whoever bought the ABS securities? Isn’t that the very reason they sell them…to realize immediate profit and minimize any risk?

Who actually holds title on ABS or MBS security after sales?