The potential to unleash “third phase” of the Global Financial Crisis.

By Don Quijones, Spain & Mexico, editor at WOLF STREET.

It seems like only yesterday that a cacophony of voices — our own included — was warning about the dire threat posed to global economic stability by unraveling hard currency-denominated emerging market debt. Then, roughly six months ago, everything went quiet.

And the debt began growing again.

So far this year $153 billion of new EM corporate foreign currency debt has been issued, according to Citigroup. That’s 7% higher than the same period last year. No reason to worry, say Citi’s analysts W.R. Eric Ollom and Ayoti Mittra. So-long as the appetite for high-risk debt remains unabated, indefinitely, EM companies should be able to handle their need to roll over their foreign currency bonds and loans.

“The TINA trade (‘There Is No Alternative’) remains a strong force in the market as investors search the world for higher yields in a low rate universe,” the Citi analysts conclude. “We recommend investors remain long the asset class.”

The Third Leg Down

Not everyone’s quite so sanguine. According to a sobering new report launched yesterday by the United Nations Conference on Trade and Development (UNCTAD), a collapse of emerging market debt is not only a very real, present danger; it has the potential to unleash the third leg of the Global Financial Crisis.

This third leg is likely to be even worse than the first two: the collapse of the Subprime market in the U.S., in 2008, and the unraveling of Europe’s sovereign debt markets, between 2010 and, well, today.

Thanks to an unprecedented “deepening of the financial integration” of developing and emerging market economies in recent decades, coupled with “a deluge of financial flows and cheap credit since 2009”, emerging markets are poised for a year of living dangerously, the report warns. The International Monetary Fund (IMF) has already warned policymakers to be alert; UNCTAD now suggests that it is time for them to be “alarmed”:

Alarm bells have been ringing for a while over the exploding corporate debt incurred by emerging market economies. According to the Bank for International Settlements, the debt of non-financial corporations in these economies increased from around $9 trillion at the end of 2008 to just over $25 trillion by the end of 2015, and doubled as a percentage of gross domestic product (GDP) – from 57 per cent to 104 per cent – over the same period.

Between 2010 and 2014 the dollar-denominated debt of non-financial corporations in 13 selected developing countries increased by 40%. During the same period their debt-to-service ratios also soared ‒ a “solid warning indicator of systemic banking crises in the making,” the report warns. Worse still, much of the money that entered developing and emerging economies has fueled real estate and financial asset bubbles rather than long-term productive investment projects.

Insanity Squared

The emerging market debt crack-up has reached such mind-boggling proportions that last year saw the birth of one of the craziest financial creations on earth, available only near the peak of enormous credit bubbles when nothing can ever go wrong: 100-year bonds issued by governments or companies in emerging countries, in currencies they don’t control.

They included Mexico’s fiscally-challenged government and Brazil’s scandal-tarnished oil giant Petrobras. As WOLF STREET reported at the time, the 10-decade bonds they issued were greedily gobbled up by desperate yield-famished investors “driven to near-insanity and drunken benightedness by the zero-interest-rate policies of central banks around the globe.”

It was the peak of the emerging market bubble, when the amount of debt that low-income developing economies could have sold to eager investors seemed almost limitless. The main reason for this unprecedented surge in appetite for EM debt was the huge monetary expansion unleashed in many of the world’s major economies, led by the Federal Reserve’s QE program. The result was the now-all-too-familiar reality of anemic (at best) yield opportunities in developed markets, prompting investors to seek out much riskier emerging market assets.

The moment the Fed turned off the spigot, in mid-2014, the flow of funds began to reverse, according to the report, creating ripe conditions for a “prolonged commodity price shock, steep currency depreciations and worsening growth prospects,” which have “quickly driven up borrowing costs and debt-to-GDP ratios.”

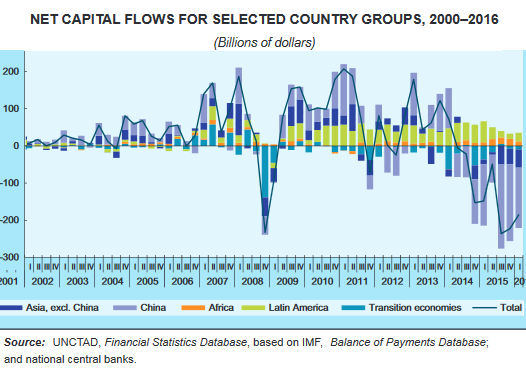

For the first time since the Latin American debt crisis in the second half of the 1980s, aggregate net capital flows entered negative territory. Aggregate outflows reached $656 billion in 2015 and $185 billion in the first quarter of 2016. The capital flight was particularly pronounced in China and other parts of Asia. Note how capital flight heated up in 2014 toward the end of the Fed’s “QE Infinity”:

The Hangover Begins

There was a brief respite in the second quarter of 2016. On the surface, to global banks like Citi’s delight, there’s still some life in the party, as a recent revival of risk appetite in global financial markets has begun luring investors, once again, into high-risk EM assets.

But there’s considerable variation across countries and regions, and the downside risks of deflationary spirals, currency devaluations, and plunging asset prices continue to grow. In some very large emerging markets, including inflation-plagued Nigeria and recession-hit Brazil, the hangover is already being felt. Eight countries — Angola, Azerbaijan, Ghana, Kenya, Mozambique, Nigeria, Zambia and Zimbabwe — have already asked the IMF or World Bank for bailouts or are in talks to do so.

It could be just the beginning. If the global economy were to slow down more sharply, things could turn very ugly, very quickly, the report warns:

“There remains a risk of deflationary spirals in which capital flight, currency devaluations and collapsing asset prices would stymie growth and shrink government revenues. As capital begins to flow out, there is now a real danger of entering a third phase of the financial crisis which began in the US housing market in late 2007 before spreading to the European bond market,” it said.

In such a scenario a significant share of developing-country debt incurred since 2008 could become unpayable and exert considerable strain on an already deeply debilitated global financial system. And as U.S. economist Michael Hudson once wrote, debts that can’t be paid, won’t be paid.

In the face of a disorderly, potentially catastrophic global economic meltdown, the world’s policy makers, bankers and central bankers will have little choice but to prepare ways to manage debt workouts in “a faster, fairer and more orderly manner,” the report concludes. Unfortunately, as any Greek citizen will attest, these are not exactly words — in particular the second “f-word” — that you’d normally associate with our wise masters and mistresses of global financial and monetary policy. By Don Quijones, Raging Bull-Shit.

A recipe for a debt crisis. Read… Mexican Peso Plunges against Dollar, in Toxic Cocktail of Forces

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I guess if the IMF insisted that the eight basket cases asking for help (Nigeria with all that oil should be ashamed) reform their governance, there would be an outcry about ‘overthrowing democracy’

Look, this mess has been growing since Independence. If it could be put to a vote, without tribal elites involved, most of these places would choose trusteeship. (This desire has been freely and overtly expressed by older Africans to famous travel writers with zero political interest: e.g, Dervla Murphy, who biked across Africa)

Although we weren’t discussing this idea I have personally talked with an older Ethiopian who told me the rule of King Selassie was regarded as Ethiopia’s golden age compared with the Marxist Peoples’ Republic.

The connection: a preference for the past.

How about this idea- the G20, including former colonial powers each adopt a country ( with their consent via UN supervised vote) and administer it for 20 years. Why 20? Because it gives time to train new leaders- not so much in literacy, Nigeria has many PH.ds. but in the concept and practice of separating public office from private gain and overcoming tribalism. Yes I know the UK has tribes but England alone had dozens at the time of the Roman conquest, mostly warring with each other.

When Independence came to Africa almost overnight in the 50’s there were only a few literates. Fundamentally a result of WWII, Independence came too fast.

The idea for the former colonial powers would be to atone for previous exploitation.

A model from the business world: many hotels are not managed by the owners. One similarity: both profit. Nigeria for sure has seen such immense wealth stolen and squandered that the administering country could cover its costs and still leave Nigerians much better off.

Then when 20 years are up it’s back to the locals and the administrators can debate who did the best job. It could be a contest !

Off the wall eh? Or maybe another rock concert will end this ongoing downward spiral.

This is off the wall. Nigeria will be just fine, they are still growing at 3%, which is slow, but in the right direction. Your neocolonialist ideas wouldn’t get very far on the continent these days, Africans are actually much more open to neoliberal, globalist policies than you may realize. At heart, Africans are merchants, traders, and entrepreneurs.

Then why why why does this vibrant economy growing at double the rate of the US need a loan from the IMF?

Don’t you understand the IMF is the lender of LAST resort?

Nigeria is broke- it couldn’t sell a junk bond- well, these days you might get a nibble at double digits.

My ex (a best friend) taught in Nigeria for 8 years. Several of African friends (and new husband) visited. I learnt from them about the rampant corruption- rule by kleptocrats. The oil wealth from the sweetest field, Bonnie, has all been stolen.

Government ministers as in most of Africa, tend to be from the same tribe.

The village where she lived near the town of (sounds like Mydoogree, it’s been a while since I’ve seen it spelled) was recently the scene of some terrorist attack. The government has generally lost control of several areas, including the one where the school girls were abducted.

The main airport at Lagos is no longer safe for new arrivals- don’t get into a taxi. The US State Department has an advisory about it.

Nigeria will be “just fine?” Are you kidding? Nigeria is in a deep recession this year. Its currency (naira) has collapsed 44% since early July. Pandemic corruption is eating the economy alive. All kinds of mayhem is breaking out…. Not to speak of the mess in norther Nigeria.

Labeling failed economic systems as “socialist” and “Marxist” and then using it to blame “Socialists” and Marxists for economic disasters is really without merit and opportunistic . Let’s not forget to mention the accomplishments of the “Marxist Socialist” China, Vietnam, Cambodia, and Laos. Yes state intervention and ownership is widely practiced in those countries and they are capitalistic. On the other hand there are those following the model advocated by the IMF/World Bank an example of which is Nigeria. Neoliberalism.

Vietnam is a former colony and fought hard to get its independence. It seems to me that they’ve done well for themselves given the level of destruction imposed on them for so long.

And btw, one of the so called G20 countries is India, a former colony with a strong pervasive cast system.

Saudi Arabia is another G20 country. Need I say more?

Nigeria isn’t following any economic model- unless you call theft an economic model.

It is so bad that given its oil- it would be better off with Cuba’s old style communism.

Just to be clear- this is close to a failed state- with one civil war not that long ago and today riven with ethnic and religious fault lines.

As for neo-liberalism whatever the hell that is- do you mean the system in Western Europe, the UK, the US, where society is not collapsing and it IS safe to take a taxi at the international airport?

100 year bond….. what are the chances of ever you getting your money back.

LOL

Debt slavery will allow corporatist neocolonialism in Africa to accelerate. The continent has plenty of natural assets to strip. Now all the corporatists need are markets to sell the plunder into, but unfortunately those have already been stripped as well.

Such a quandary. Too bad there’s no way out. There’s certainly none for Africa.

EM corporate debt based on dollars is a dangerous game. They can borrow in USD at a lower rate than their own currency, but they have no control over exchange rates. If the Fed put through another 0.25% increase for September, this probably would have caused the dollar to rise, and make servicing their debt even more difficult.

As I write, the DYX is at 95.40, and it has been just over 100, and down to 92 within the last twelve months. Correct me if I’m wrong, but that’s an 8% swing in the cost for dollar based EM corporate debt service, which at today’s interest rates is quite a lot.

You hit the nail on the head Dan. EM debt based on dollars. That is why the FED didn’t raise rates. If they do, it will cause the dollar to rise. It will crush the EM world filled with dollar denominated debt. The FED has become the de facto World Central bank with all the dollar denominated debt around the world. Domestically the FED needs to raise rates to have any hope of saving the pension funds. Rock/FED/Hard Place

100 year bonds ARE A GOOD move . There will either will be a new world currency in a 100 years and the USD will be devalued to eliminate US debt, OR all debts will be forgiven in a 100 years .

Many theories- one thing is for sure- repayment if any, won’t be a problem for the guys negotiating the loan

Those investors are betting civilization won’t have collapsed in 100 years even though all the trends say otherwise, when they should either be getting their affairs in order or partying like there’s no tomorrow.

They are a good move for the issuer ( borrower) they are a lunatic investment, unless you could justify them as a perpetual (never due) which means you are very confident the issuer will never fail to pay a coupon comfortably above inflation.

I have an issue of zero coupon perpetuals coming to market soon. Apply through primary dealer WS.

“It could be just the beginning. If the global economy were to slow down more sharply, things could turn very ugly, very quickly, the report warns:”

As Jimmy Durante said….ya ain’t seen nothing yet !

Lets see: insurance increases of 20 to 53%, cell phone giga usage is going up 50% from 10 to 15 each with ATT (thieves), Taxes are up, ( actually they are all thieves), and then there is the Misc charges…so who is going to support the global economy? If you think it is Americans, you best hope it is the 1% because the 99% are broke.

Interestingly, while everyone warns of sky-rocketing EM debt, there is no break-down by country. Of course, we hear about such countries as Mexico and Brazil, certainly Turkey, but who else? These could not have ammased that amount of debt. Chinese corporates have been borrowing a lot in Dollars, but Chinese debt is hardly an issue.