Consumer Debt with Negative Rates is “a Perversion.”

I’m not sure what, if anything, Ewald Nowotny, Member of the ECB Governing Council and Governor of the Austrian National Bank, and I agree on in terms of monetary policy. But today he said something that is exceptionally truthful – and a glaring expression of just how hypocritical a central bank and the people that run it are.

Nowotny’s keynote speech today at the European Forum Alpbach in Switzerland was titled (my translation from German), “Low Interest-Rate Policies: Free Money for All, or Savior in an Emergency.”

A rhetorical question which he then proceeded to answer with utmost clarity: Free money, or worse, money with negative interest, is not for everyone. Only governments and corporations are allowed to benefit from it, but not consumers.

In fact, consumer loans with negative interest rates would be “a perversion,” he said to all those waiting eagerly for their negative interest mortgages where they would actually be paid every month for having borrowed a ton of money to buy a ludicrously overpriced house. Even Switzerland, which has the deepest negative rates in the world, has drawn a line.

“I believe it would be a perversion, an economic one, for loan rates to suddenly be negative. It totally goes against the economic nature of a loan,” he said.

And I totally agree. Negative interest rates, or negative yields, go “against the economic nature” of debt. Negative yielding debt is an absurdity that exists only because central banks have created it and forced it upon their bailiwicks.

“In Switzerland that has been ruled out for loan agreements for a long time. Now it has been ruled out for Austrian loan agreements,” he said. So it has been formalized. Consumers shall forever be barred from benefiting from borrowing at negative rates, and thus from getting paid to borrow. So forget loans and mortgages with negative interest rates.

But here’s where the hypocrisy and deviousness comes in: thanks to the scorched-earth central bank policies, governments in Europe and Japan have been borrowing at negative yields for a while, and an ever larger pile of government debt now sports those negative yields.

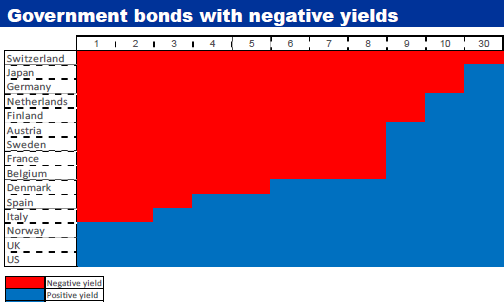

Benoît Cœuré, Nowotny’s buddy on the ECB’s Executive Board, offered this chart showing just how far the negative yield absurdity has gone, with Switzerland (top line) selling 30-year bonds at a negative yield, and Japan and Germany selling 10-year debt with negative yields. In total about $12 trillion in government debt sport negative yields:

In July, Germany has sold €4 billion of 10-year bonds with a zero-percent coupon and at a price above face value. This guarantees that investors, such as pension funds that have to buy these bonds, will never receive any interest payments. And if they hold the bond to maturity, they’re guaranteed a capital loss – not counting the losses due to inflation of the 10-year period.

And corporations, even US corporations with subsidiaries in the Eurozone, are borrowing at negative yields by selling euro bonds, in some cases directly to the ECB via private placements. No market needed. As of July, according to Bloomberg, there were about $500 billion of corporate bonds with negative yields. And that pile is steadily growing.

Central banks have forced this sort of financial repression on investors so that they will lose money not only to inflation but also in nominal terms when they invest in what are considered high-quality debt. To make any income whatsoever, no matter how tiny, investors have to take huge risks.

Central banks have made financial repression their policy. The cash flow of savers has gotten destroyed long ago. Pension funds are next. Financial repression is ugly and discriminatory for the “other side” of the deal. However, when consumers, who’ve been on the “other side” of the deal and have felt the brunt of central bank policies all along, line up for the same absurdities and “perversions” that companies and governments benefit from, well, forget it. Nowotny put his finger on it: Central banks will move heaven and earth to keep that from happening. Access to the benefits of these absurdities and “economic perversions” is limited to an elect group.

Who says the Fed can’t have fun at our expense? Read… The 11 Bone-Chilling Things I Gleaned from Yellen’s Chart

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Negative yielding debt. The cart in front of the horse.

Bonds (debt) are being traded and priced the same way as commodities. Bonds no longer trade on yield but on some future price.

In any market, capital chases yield first. It doesn’t chase price appreciation. Price appreciation is simply the consequence of yield chasing. When bonds are bought for capital appreciation, then they are going to trade like a commodity.

Bonds are traditionally bought for safety and yield. When they provide neither and trade like gold, (which is traditionally bought purely for safety and offers no yield) then the cost of owning bonds becomes more expensive than the cost of owning gold. Gold becomes cheaper to own even while it’s rising in value!

Just look at all those Japanese, German’s, Swede’s, etc. That are buying home safes to keep their currency in, because the banks are charging interest to keep your cash! What will happen when cash is outlawed?

Own the only real money. GOLD.

I believe someone has just introduced some shoebox-sized safes and they’re selling into a nitch. Meanwhile someone else is making a big deal of it?

When TSHTF, level 1 currency will be anything that serves our carnal nature LOL. So, send to NC for all the cheap cigs you can afford. Buy up all the cheap booze you can lay hands on – in small bottles. With these you would be surprised how much work others will do (while you sit on your porch outlookingin) maintaining your garden/greenhouse for a little food, level 2 currency. LOL.

Gold/silver, I prefer fungible silver in small denominations; level 3 currency. Gold: level 4 currency. With this, and passport in hand, you can bribe your way the hell out Dodge or into Timbuktu.

Have fun with this.

Wouldn’t it be so very decent to give negative interest rates to our students?

why? in Netherlands the rate for student loans is now 0.14% per year. The result: students borrow loads of money for a car, an exotic 1-year vacation or a downpayment for an apartment just because they can. Nobody wants to know what they spend the money on, you just click on a web application what you need. It’s extremely popular especially with students with foreign (e.g. North-African) background who discovered you get access to loads of money to finance a lavish livestyle or a drugs business; they don’t care if you really show up for studing.

Most of them assume the money will never have to paid back (and just like in the US, it is suggested that if you can’t pay within 5 years or so after graduating, the taxpayer gets the bill).

With negative rates I’m sure many people would start ‘studying’ instead of working…

NHZ: Good point about the use of student loans for non-educational purposes. I haven’t heard many bring that up in the US. Although, working with a large number of students over the years, it does go on here. Unless, they give credit for spring break in Cancun now days. And then there are the plush condos many students occupy in our University town. And dining out in high-end eateries. Being a student these days is way different than it was when I came through.

Not saying it is the same experience for all students, but many are, or have, worked the system. So, yes, I think they should pay back the money they borrowed. And hopefully, get a feeling for the moral hazard of over-borrowing.

This new student lifestyle is not universal in my country either, it’s still just a minority doing it and probably most of them are not real students (guys with North-African or Turkish background seem to be especially good at working the system and pretending to be studying). Clearly politics doesn’t want to know how much abuse is going on, just like they aren’t really interested in the massive fraud that occurs with e.g. disability benefits or mortgages. Just like in the US some politicians are already promising debt forgiveness for student loans on very easy conditions.

When I studied in the eighties only those with very rich parents had a car, and a few people with low income background who got very generous, totally free funds from the government. Most students only had a very basic, small room with shared kitchen etc.. Nowadays many students consider it normal to have a car and own an apartment (or in a few cases, rent a luxury apartment), and have a few exotic vacations every year, and partying and eating out several times a week …

Cheap shot going after students.

I don’t know what students you’re talking about. My son just spent $800 on text books and school supplies. One math book alone was almost $400. He won’t have enough money left over to buy lunch for a semester.

The students are smart. They are gaming the system just like BANKERS, CORPORATIONS and POLITICIANS. It would be even better if students could declare bankruptcy and not pay back the student debt!

It would be even better if the bill for all this fraud went to the bankers, corporations and politicians. Unfortunately, the bill for all these students who are gaming the system will be presented to the average citizen who has not enjoyed any of the benefits.

You can call it smart but IMHO it is more crooked; a dubious start of a white collar career.

Problem is that the lenders of student loans are not really evaluating if the borrower is “really” a student who is seriously attending classes and on a degree trajectory or a borrower fronting a gangster looking for easy fast money to do all those things you cited, you also need to be more discriminating lumping gangsters in with serious students.

@ sandy wess:

“you also need to be more discriminating lumping gangsters in with serious students.”

Reality isn’t like that. There are many shades of honesty in ‘gaming the system’ and although there are many honest students, many others simply do what they can easily get away with, take what they can get without drawing too much attention. Many of the people who took out loans worth thousands of euros for an exotic vacation or a new car are real students in the sense that they do visit the university and probably plan to graduate at some indefinite time.

Of course the lenders don’t care if the students are ‘real’: if they can’t collect from the individual the taxpayer will get the bill. And that’s why such loan systems (at least those without serious oversight, as is common in higher education in the West) are a patently stupid idea. It’s inviting people to commit fraud, many of them will even argue that the debt is not their fault because it was too easy to gobble up loads of money that they can never pay back (two Dutch students used this defense in court, don’t remember who won).

Education is an investment and should be free at the point of access, complicating everything with loans etc is totally unnecessary and unproductive.

… free money … is not free ….

it is, as long as someone else gets to pay the bill; as is pretty common nowadays thanks to central banksters and politicians.

More and more services that used to be provided by the government are now being performed by corporate interests (because corporations naturally do everything better). Besides that, corporate lobbyists now have the most influence on government spending anyway. So couldn’t the headline be changed from “free money for all only corporations & governments” to “free money only for corporations”. The only problem with our government is the undue corporate influence on it. “We the People” need to take it back. (And getting Ronnie Raygun’s name off everything wouldn’t be too bad either).

I believe this is all about global warming.

High bond prices never last forever (that is, they don’t last until the instrument matures). At some point the prices fluctuate … and the buyers at the high price will everything.

This includes the central banks who plunge in along with the rest of the market. Why not? To do otherwise is to look foolish, to not be in control.

That potential loss … the risk that right now has no price, or rather, cannot be given a price.

What a strange world, where pigs fly …

“Free money, or worse, money with negative interest, is not for everyone. Only governments and corporations are allowed to benefit from it, but not consumers.”

Just as honest as the recent comments from FED’s Fisher about FED policy (if it keeps stocks rising they are doing a fine job, even if it means killing all the savers and pensioners – after all it’s only the speculators and banksters that count and not the little people).

However, many ordinary consumers are also partying thanks to almost free money that is raining down since 2008. It just varies very strongly between individuals. The most obvious example is homeowners with a maximum mortgage who pay almost nothing for their home (in my country just 10-25% of the equivalent rent, if they have a recent mortgage). I know this varies between countries, but some of the free money does end up with voters and they will vote to continue on the current trajectory. Free car loans, student loans, there are many other examples. How many people really expect that they have to pack back the loan at some point? Politicians have made it clear that if you are ‘in trouble’ or simply ‘disadvantaged’ the taxpayer will get the bill, and not the person who enjoyed the benefits of the money. Much of these loans will turn out to be free money, no doubt about it.

Seems this has been going on for some time. Free stuff recipients are now in the government, and see no problem with providing free stuff.

It’s interesting to note consumers actually got closer at having “free money” loans in 2003-2008 than right now.

Back in the days the average EAPR on a car loan here in Europe was 2.5%. Right now, despite Euribor deep in the negative as far as the eyes can see, you cannot take out a car loan at less than 4% EAPR.

And here’s the kicker: the smaller and cheaper the car, the more expensive the loan. The only brand presently offering 4% EAPR is Audi, which doesn’t exactly sell transportation for the masses. Ford won’t give you a loan under 5.8%, no matter how good your credit rating, while PSA (Peugeot and Citroen) has car loans starting from 8% EAPR.

By contrast you run of the mill €200,000 20 year mortgage (which won’t buy you much in most countries) has now sunk to as little as Euribor 6 Months plus 1%. With Euribor deep into negative territory it means this average mortgage has less than 1% interest rate.

It’s no small wonder banks such as Credit Agricole and Santander have dived into “consumer credit” to prop up profits slaughtered by yield compression, albeit consumer credit is always risky, especially now that personal bankruptcy laws across Europe are slowly being modified to reflect a US model. In fact I am genuinely surprised banks aren’t fighting these much needed reforms tooth and nail. Guess they are too busy hiding bad loans and risks from shady derivatives.

I don’t know the details, but here in Netherlands I see car loans that are 0% for the first 1-2 years. It usually isn’t easy to find out the cost over the total duration of the loan, but my impression is that there is little incentive for paying ‘cash’.

For mortgages we now have 10-year fixed for below 1%, and a significant chunk of adjustable rate mortgages at Euribor + 0.7% (these are very close to going negative, they might be before the end of the year).

Another interesting note is that VW established a car lease/loan company in Netherlands that is officially considered a bank (so they enjoy all the ECB benefits and taxpayer protections). No doubt this helps pushing their products into the market.

In the US, we’ve had 0%-financing for cars since, well, when I was still in the business. But these 0% loans were promotional. They were subsidized by the automaker to sell more cars, instead of a discount or “rebate,” as it was called then. Those weren’t true lending rates.

The same still applies. All kinds of consumer products are offered with 0%-financing as a promo, subsidized by the product seller. This is very different from a customer walking into a bank and taking out a 0% loan.

I was keeping it for another day but… the reality of the automotive market is that since 2009 there are major, and I am not joking, incentives at buying cash. Only they are not advertised.

I won’t name any names but I can tell you from direct experience (read: I got the quotes earlier this week) two well known manufacturers now offer 5-10% off in case of a loan payment but over 20% off in case of cash payment. And that’s without haggling and without going through the options: obviously if you buy a car the dealer has “ready for delivery” there’s an extra incentive in form of extra money off or a free set of tyres or insurance for a year etc.

Yes, the manufacturer has every incentive to push a loan but the dealership has every incentive not only to sell a car but to take the cash as quickly as possible. Always remember dealerships are not merely under tremendous pressure to “deliver” sales figures no matter what, but their stock of cars, vans etc is paid for in advance.

I have some experience with lease/loan in the agri sector and, honestly, I have very mixed feelings about it.

John Deere pretty much invented it and at the beginning it seemed like a good idea. However Deere’s two main competitors (CNH and AGCO) started doing it as well and the end result is what happens when you introduce competition on any market: prices and profits are freefalling.

To this it must be added very few have ever taken Deere’s offer of buying their machines at the end of the lease and nobody has bothered since the competition arrived. This means Deere, CNH and AGCO are sitting on a growing pile of relatively new tractors, combine harvesters etc they spent money on refurbishing in the hope of selling. My local CNH dealership always has a “selection” of these refurbished machines for sale (selection means at least a dozen). Mind we are not talking lawn tractors here but the big machines over 100hp.

Mercifully Italian and Japanese manufacturers of smaller (under 100hp) equipment haven’t started leasing (yet) but Foton Motor has arrived on the European market. If the name sounds worringly familiar, it’s because it should be.

This is nothing more than the agri arm of BAIC, the Chinese State-owned automotive titan. They are already implementing the tactic that allowed them to win over the Latin American market, meaning they’ll be assembling here in Europe tractors from knockdown kits shipped over from China.

It’s going to be a slaughter.

interesting that you do get big cash incentives when buying a car in the US.

I don’t have a car and probably would not be good at negotiating with a car dealer anyway, but I heard from a friend who is very good at buying lightly-used, high end BMW’s from their official dealers at huge discounts (60-70% off compared to new price) that he doesn’t get any extra discount for paying cash. With his latest purchase last month he decided to pay cash anyway as he doesn’t need the financing, but we both thought this was strange and suggests that the car dealers/manufacturers have access to free money.

Or maybe NIRP is taking its tall; some day companies may be begging us to delay payment ;-(

These are euro-area offers. I used to live in the US, in a place most people would kill for, but you cannot pay me enough money to go back there.

Those “lightly used” cars are what Italians and French call “semestrals”, meaning cars dealerships register every six months to meet their sales quotas and to reduce brand new inventory (and hence taxes they have to pay on it).

Most of these cars are brand new. Often dealerships put one or two miles on them just to show they are “used” and are offered at ridiculously low prices. If you like the color, trim level, engine etc and, much more critically, don’t mind buying what for fiscal reasons is a used car, you can get yourself a good deal.

Now, the problem is what happens to these “semestrals” that do not get sold. There are all sorts of crazy rumors and I have seen a parking lot full of brand new Nissan’s rotting away myself, but it seems they are quickly demolished and recycled without too much fuss.

Insert your “They Live” joke here.

So you simply take out a property loan, at as you say euribor + 1%, use the cash to buy car at steep discount. Voila. Evade the high auto-loan interest rate. “What is this loan for?” “It’s for, uh, uh, renovations, yah, yah, that’s the ticket, renovations.” (renovation of transportation that is, but they don’t need to know)

Perversion is indeed the operative word for what Central Banks are doing, and thank you Wolf for reporting the obvious truth that mainstream/corporate media gloss over.

That the ECB buys corporate bonds from companies at zero or negative interest is a pure and simple cash gift to the select few who’re connected and receiving Euros from Draghi. The current actions of Central Banks are akin to malignant cancers, and just like a tumor in your body, CBs need to be excised and discarded!

how do negative interest rates affect the derivatives markets?

WOW what an interesting question. Just off the top of my head I can tell you that a mortgage derivative might be impacted in a very positive way. The problem with most positive interest rate mortgage derivatives is that the life of the mortgage pool is much shorter than the income streams they sell. This means that the pool runs out of payers faster than investors expected. That’s how you land up with worthless securities rolled up into a another pool, like a CDO squared.

With a pool of negative interest rate mortgages a portion of the pool is self amortizing. The mortgages pay down to some degree without having to do anything. This would increase the life a pool(a good thing) by incentivizing home owners to hold on to properties. The other good thing for the derivative pool creator is that they lock in a profit when they buy the mortgages and they can also get paid to service the mortgage. This can mean that investors in negative mortgage derivatives may have much less risk exposure than in a positive rate environment.

Wolf, there is one “real” way for ordinary consumers to get from one to five percent interest on their “banking”: Use a cash-back credit card and pay off the balance in full each billing cycle.

It is partly “out of the hides” of merchants, of course, who have to pay a swipe fee on each transaction.

But the consumer does get some RELATIVE benefit, compared to consumers who us debt longer than 20-30 days, the length of the billing cycle on credit card debt.

Yes, there are many ways to get 0% financing, or better, but they’re all subsidized by the vendor.

A credit card is a big (I mean HUGE) profit center for banks, so they use incentives to lure people into getting them. The merchant pays a fee for every transaction even if you pay off the credit card balance. So the merchant subsidizes your good deal. But try to go to your bank and ask for a 0% or negative-rate loan.

Wolf, awhile back their were reports that banks did not like cardholders who pay off their balances in full (No “HUGE” profit from us).

Since there’s NO WAY us payoff folks are going to slip into their high interest web, do you have any theory why banks are continuing to offer them to cardholders with excellent credit ratings?

Is it simply a matter of preserving market share, or taking a little bit of swipe fee income, you think?

The fee to the merchant can be up to 2 to 3% depending on their volume. So it is not a little bit of fee income, it is a lot of fee income.

If you spend $10,000 with your card per year, the bank makes 1% to 3% off it, so between $100 and $300 per year, without having to do anything. Pure profit, no cost.

Many cards also have annual fees, so that would go on top.

I had a no-fee card I wasn’t using at all. After a few years, the bank sent me a message that they’re going to close my account (I had the card for over two decades). Not using the card is what they don’t like. But once you’re spending money with your card, they love you.

The card payment fee is not really paid by the merchant, it’s tacked onto all the merchandise. The final customer always always always pays for everything.

Sandra, the student loans are not meant to buy an education but to buy votes. Falls under the heading of TANSTAAFL. In fact, the purpose nowadays is not to teach critical thinking but to cripple it. For a government seeking to control every aspect of your life, this is a win-win for the powers that be. The anarcho-capitalists are correct: government isn’t a necessary evil it’s just evil. Regards, Julian

agree, free money has replaced free thinking in higher education.

True, force a student into debt for their education, stops them protesting ever again.

Look at the number of student protests since student loans.

Of course it wrecks the country’s economy in the medium to long term, but no banker ever cares about that long into the future.

Those cbs are destroying capitalism. Not only is the Schumpeter turn over/renewal/creative destruction (or whatever it’s called) prevented, they are also destroying the effect of the discount rate on innovation. So they’re keeping the zombies alive, and preventing entrepreneurship. Zirp/Nirp means stagnation, and crash.

Consumers are able to get negative interest rate loans.

Chase Freedom = 5% cash back in some categories

Discover = 5% cash back in some categories

Amex Everyday Cash = 3% cash back on groceries

Citi Double Cash = 2% cash back on everything

Just pay your balance in full each money.

2% to 5% negative interest rate on a short term loan. Great deal.

“Consumers shall forever be barred from benefiting from borrowing at negative rates, and thus from getting paid to borrow. ”

Can we start a proprietorship firm and borrow then? That these rascals are allowed to talk and not stoned or shoed (aka Bush) when they sprout (and implement) such obviously inane ideas is what makes my blood boil. I am all for mob justice when dealing with scoundrels. Negative rates, my foot!

S&P rascals who rate negative interest bonds as IG should also be dealt with similarly.