The hedge fund manager is all over this energy MLP theme.

By Alex M., Founder of Macro Ops:

Range-bound markets over the past year have made it difficult to earn good returns. Most investors haven’t made any money at all. And this reality has forced them to pile into high-yield products to make up the difference.

One popular area to reach for yield has been the energy space. The general belief is that crude has hit a bottom and that energy companies are now a safe bet. Especially with the dividends some of them are offering.

Billionaire hedge fund manager David Tepper is all over this theme. His interests lie specifically in Energy Transfer Partners (ETP) and Williams Partners (WPZ). Both these companies are master limited partnerships (MLPs) and both operate in midstream energy assets such as storage and pipelines.

For those unfamiliar with the energy space, the industry can be broken up into 3 segments:

- Upstream: These are the exploration and production (E&P) companies that include drillers. They find and extract energy products.

- Midstream: These are transportation companies that move raw product through their pipelines. It’s in this segment that we find our MLPs.

- Downstream: The transportation companies move raw product to downstream companies that act as the processors and distributors of the final product. Refineries are in this segment.

If you take a look at Tepper’s latest 13F filing, his top buys are ETP and WPZ. Both these companies are also part of his most concentrated holdings. Tepper is betting big on the MLP theme.

Energy Transfer Partners (ETP) is an MLP that started with natural gas pipelines, but later expanded into natural gas liquids (NGLs), refined products, and also crude oil. It currently has a dividend yield of 11.49% — exactly the type of yield investors would love to earn.

Williams Partners (WPZ) is another MLP that’s focused on dry gas pipeline transport. It’s dividend yield is 10.82%, also pretty juicy.

With dividend yields like that, this play may seem like a no brainer, but there are actually significant risks. Both these MLP’s have credit ratings one level above junk status. The reason is because both are leveraged and have debt servicing costs to take care of. They’re exposed to energy prices. If prices drop too low, these companies will have a difficult time servicing their debt.

And being so close to junk status, another downgrade would have significant effects on their current cost of borrowing. A further increase in debt servicing costs would put pressure on their dividend, which would likely be first on the chopping block to pay off debt costs.

Tepper knows this. But the reason he’s still interested is that WPZ and ETP are currently in the middle of a merger. This merger would increase the odds that the combined company could maintain their dividend regardless of volatile energy prices.

The probability of the merger going through has recently increased in the eyes of merger arbitrate specialists: The spread between the share price of WPZ’s parent company and the price of the deal has fallen by half, from over $8 in May to $4 more recently. A higher spread indicates that investors are less confident in a successful merger, while a lower spread suggests that the market is more confident in the merger’s success.

This is all well and good, and a merger may make sense, but now is still not the right time to enter this trade.

A big part of this MLP thesis rests on the idea that energy prices have bottomed. But we don’t believe this is true. The bullish US dollar trend is still intact. And because commodities are priced in dollars, a stronger dollar means lower commodity prices.

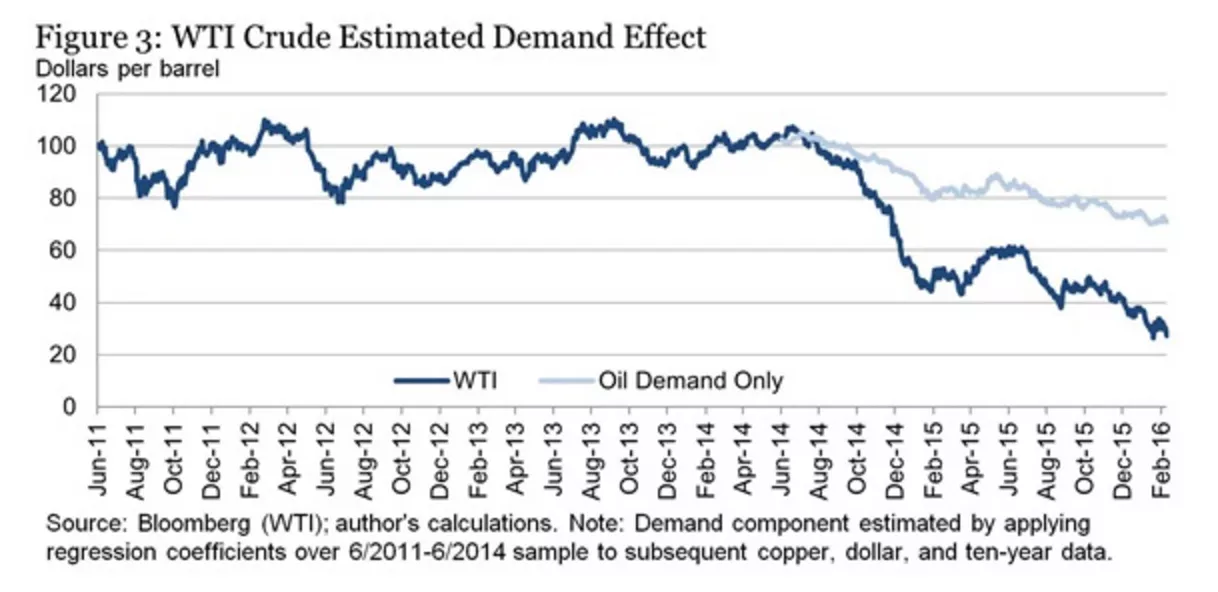

Just looking at the relationship between oil and the dollar, dollar strength has historically accounted for 30-50% of oil’s price movement. Take a look at the graph below. It isolates an estimate of the price of oil based only on demand. It then compares it to the real price of oil in the market. The gap you see between actual prices and demand exist because of the impact of USD strength.

As the dollar strengthens, commodities in general (including energy) will take another trip back to prior lows. The pain in the energy space is not over. The “blood in the streets” moment has yet to occur. There were not enough defaults and there are still too many companies hanging on by a thread. There needs to be another washout once energy prices drop again.

Some may argue that these MLPs should be protected because most of their exposure is in natural gas instead of oil and their position as midstream operators is not directly affected by energy prices. These points may be valid, but they don’t matter. This reasoning didn’t save MLPs in the recent energy downturn, and it won’t save them in the next one either.

Regardless of these MLP’s position, they tend to fall victim to the classic case of the baby being thrown out with the bathwater. When energy prices drop again, investors will bail on anything energy related. All the selling creates liquidity issues that force funds invested in these MLPs to exit their holdings. Their margin level restrictions trigger and they have to sell. MLPs end up getting dumped along with every other energy play.

MLPs may make a great investment down the line, but not right now. The dollar trend has to play itself out and there needs to be a bigger washout of energy companies. At that point we’ll be interested in jumping into MLPs for the long-term. By Alex M., Macro Ops.

Commodities Rout Not Quite Over Just Yet. Read… How We’ll Know When to Buy This Hated Commodity

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

This unhealthy industry is an an undulating plateau of production. There is a huge supply crunch coming as consumption is currently 10X the rate of new supply discoveries. However, betting that shortages will ramp up shale production, that is unprofitable under $110/bbl, and that society will be able to long-term afford expensive oil, is very very risky, imho. More likely is there will be surge of new investment with a new econmoic crash, and new bloodletting as player once again go broke. Or, the economy stays anemic and the expensive oil is simply not needed.

Or?

You could take advantage of the Deutsche Bank offer of 5% return on a 90 day deposit, as they approach their Lehman moment! Risk?

Thank you. This is really practical information just as I was desperately contemplating transferring to a more risky account.

This indicate that the bank has a funding problems.

When is the government bailout coming?

The bond market is telling you that for the next 5, 10, and even 30 years that money is dead. You have a world crashing in debt, wages dying, automation and machines replacing humans in geometric proportions, unaffordable rents and even unaffordable home ownership, ‘live-at-home’ or live close to work to save transport costs, a completely unpredictable future for security and or wealth, and on and on and on.

So who is going to be using all this energy and how? India? China, Brazil? It will take generation ( there is the 30 years again) for the financial mess to cure itself IF it does at all…no money, no buying cars, trucks, buses, white goods, bla bla bla.

I flat tell you that living in a popular tourist town that required you to drive or fly in, the raise in fuel has sliced off 20% plus occupancies in 30 days, and restaurants half empty, attractions with employees pacing back and forth . Go and speculate the cost of energy upwards, and may you loose ever nickel you have.

“One popular area to reach for yield has been the energy space”…indeed the endless greed will kill us all in the end.

++++++

I would assume Tepper bought these in the first quarter when they were 60-70% lower. Following his lead now is probably way too risky. I can’t see those dividends not being cut at some point in the next year.

MLPs generally have to go out and borrow their dividend in order to pay it. Due to their restrictions they don’t have retained earnings since earnings are paid out in dividends, so they have to borrow at the worst times. Check out Kinder Morgan’s dividend cut. Contracts to carry oil and gas can sometimes be voided in bankruptcy as well. Dividend sounds great but there’s a reason to be cautious.

Not true of all MLP’s, thus the decline of the entire space due to retail misunderstandings…the foundation for long-term outperformance. Thanks again retail investors.

Exactly. They are not directly exposed to the oil or natgas price. They are toll roads.

Instead of individual names, buy an ETF. I bought ZMLP. also MLPI. If they roll over big time, dump em. for now the trend is up.

These stocks almost tripled since Feb 2016, Tepper has already profited nicely, this is not a good entry . What I disagree with the article is that the USD has topped in my opinion.

The Key word in that head line is “Follow”.

When you “Follow” a Hedge Fund, or a Trader.

You “Follow” them over a cliff.

Or feed them profit, as they have already brought. Effectively front running you.

Or even worse let them out, and go over the cliff, for them.

Being Two steps behind a guy negotiating a mine field, is relatively safe.

Being One step behind a market Trader/Fund can be very Expensive/Dangerous.

As they say, “what do they do here? They already did it”

He’s made his money. Now talk the book.

isn’t the smart money now on the ETE-Williams merger to fail?

http://www.tulsaworld.com/business/energy/letter-to-williams-cos-shareholders/pdf_a5b3e8c2-987a-5819-bb6a-588eb7304e06.html

Thanks. This is an amazing letter by three former CEO’s of Williams Companies against the Williams/ETE merger. I don’t know how much leverage they have, but still…

Reading the letter.

They Really dont like Kelcy Warren and on the surface their position seems more than justified.