Autos impact various parts of the economy in a big way.

By Larry Kummer, Editor of the Fabius Maximus website

One theory of the bulls – who don’t see a recession in the future – is that the slow recovery since 2008 means that there are few imbalances in the big sectors of the US economy whose busts could cause recessions. The idea is that they haven’t been inflated to risky levels.

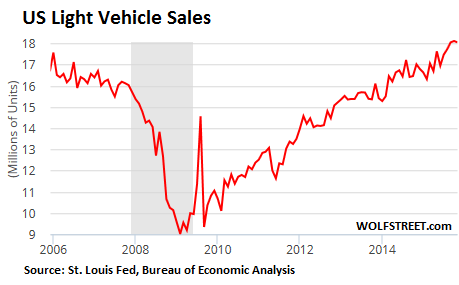

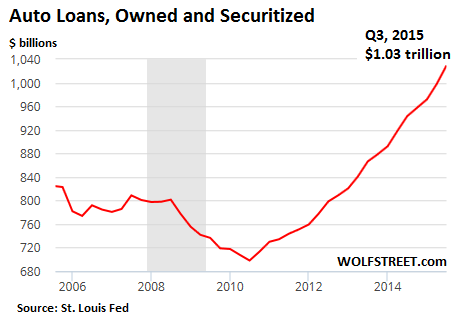

That is not correct. Here we look at one: automobile sales. They’ve been booming, and loans associated with them have been soaring:

To achieve this, lenders have taken car loans and leases beyond any sensible level of prudence, as documented by data from Experian’s Q3 State Of The Automotive Finance Market and the Fed’s quarterly Consumer Credit report.

- Record high average amount financed for new cars: $27,000, 50% of median household income ($54,000).

- A record 87% of new car purchases are financed.

- Of those financed, 27% are leases, with short maturities (average 27 months) to people with strong credit, but not building any equity.

- Car loans with record long loan maturities: 44% with maturities of 61-72 months, 28% of 73+ months.

- Record high loan-to-value ratios (LTV) for new and used vehicles, exceeding the value of the vehicles by a large margin. Even regulators are warning about it.

- With long loan maturities and high LTV’s, these cars have negative equity for many years, and owners will have difficulties trading out of them to buy the next car.

- 11% of new car loans are to people with subprime credit (scores of 600 or below).

This is how auto loan balances outstanding have ballooned from record to record, hitting $1.03 trillion at the end of the third quarter:

So far, delinquency rates remain stable: 5.2% of outstanding loans are 30+ days past due as of Q3, down year-over-year. After all, loan defaults result from economic downturns, not lead them.

Like the boom in student loans, auto loans boosts the economy (education and autos are two of America’s major growth industries). Both look unsustainable at current levels. But their eventual ill effects will be unlike that of the 2008 housing bust.

First, auto lenders need not fear mass defaults: no “jingle mail” as when people default on their mortgages by mailing the keys to the bank. Many first mortgages are non-recourse to the borrower (the lender cannot chase the borrower for deficiencies); that’s not so for auto loans. Home foreclosure can take months or even years following default. New technology makes repossession of cars fast and cheap. People can more easily find a place to live than survive in America without a car.

Second, outstanding auto loans are a small fraction of mortgages. In 2008, outstanding mortgages reached $10 trillion (70% of GDP). Auto loans are just over $1 trillion (6% of GDP). The mortgage default rocks the nation’s financial system. A severe recession might cause auto-loan defaults to spike, but it won’t be a catastrophe for the financial system. That’s the good news.

The bad news? All these imprudent loans will likely produce an overreaction by lenders when the losses arrive during a recession — a drastic reduction in lending, a hammer blow to auto sales. That will hurt because auto sales provide a more powerful boost to the economy than home sales. In 2014, total new home sales were approximately $151 billion. New car dealers sold $72 billion in product in the single month of October this year (roughly 20% were imports).

Auto sales also support a vast US manufacturing machinery, from raw materials to final assembly. They support transportation activities (rail, truck, ports, etc.), finance, insurance, and other services…. They impact many parts of the economy.

But someday, without warning, car loans will become a drag on the economy. That might happen when a large fraction of households max out on auto loans, when they can no longer roll car loans with negative equity into new loans. And the subsequent slump in auto sales will help trigger a recession. Or worse, when defaults spike during a recession and lenders raise lending standards, as they tend to do during the recession. Then auto sales will roll over, causing ripples of unemployment to radiate through the economy, affecting materials, manufacturing, transportation, finance, services, and sales.

Our reliance on consumer debt — now taken to mad levels — makes our economy dangerously unstable. That’s why car sales quickly dropped from 16 million in November 2007 to 9 million in February 2009 (-45%). Now they’re running at 18 million, with lending even more extreme. They probably will drop at a similar rate and just as much in the next recession.

The most important fact about the 2008 bust was the surprise. Many economists saw the US housing bubble and the high likelihood of a recession. I have found none who predicted that many of the world’s banks would collapse like card houses, plunging the world into a situation much like 1929-32.

The next recession will have different dynamics. I suspect it will surprise us just as much. By Larry Kummer, Editor of the Fabius Maximus website.

The slowness of this recovery has been its most amazing characteristic. Read… Recession Watch: Hidden Messages in the Jobs Report

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Its hard to believe the audacity being displayed in some TV auto sales advertising.

A local car dealer here in the NY State capital region has been airing TV ads for several weeks telling viewers that his bank has been telling him that it has lots of money to lend. This loud mouth is not merely soliciting credit buyers for his cars, he is soliciting buyers that he characterizes as “credit criminals” assuring them that if they come into his showroom he will “get the deal done, guaranteed.”

It takes very little comprehension to conclude that neither this auto dealer nor his bank has any expectation that the “buyer” will make payments on the loan. Obviously, the lousier the credit history the higher the sales price. That’s great for the car dealer who sells his clunker for an incredibly excessive price.

That’s also great business for the bank. These “credit criminal” loans are included in the investment grade securitized debt that the banks are peddling. They would not be making such loans if they had to retain them on their own books. Moreover, if a casual TV viewer like me is aware that the borrower is a “credit criminal,” you can be sure that the bank is fully aware of that fact, and is profiting to the maximum by demanding a huge discount on the bank’s purchase price of that debt, while it resells the same soon to be bad debt for full face value into a finacialized security.

Its mind boggling that this kind of advertising and the sales, not just of the car but of the lousy debt, is passed off as legitimate business practice when it is a transparent conspiracy to commit fraud on the investor public.

What you don’t seem to realize is that most people in America today have bad credit scores as a result of the financial crisis. I do and I am not even embarrassed about it anymore, because when I tell anybody about it, they tell me they have been through it too.

Here is how you become a “credit criminal”. You lose your job and tell the car loan people you need an extension, maybe just 30 days, they say alright then repo your car. Then you get another job and now they are suing you for a car they never would have needed to repo if they had waited 30 days. It happened to us and they landed up doing us a favor by taking back the GM car, a POS, but the only one we could afford at the time.

Getting another car after getting a new job was no problem. We had to buy used and they had private funding. Most of us out here in the real economy have bad credit and nobody has job security. There is an entire universe of financing and retailing servicing this demographic. Your so called credit criminals are people who go to work everyday trying to survive while the entire system is trying to screw them.

If the investors of securitized car loans get screwed, it is the bankers doing it. They can not maintain the system without taking on the credit risk and passing it on to you. You don’t have to chase the yield either.

I think by ‘credit criminal’ he may be referring to people who know they ‘re going to default. The ‘cash back’ schemes seem designed to attract them.

Back during a financial crisis ( 80’s) a relative was bidding on a large electrical job. He was puzzled when the winning bid came below his cost. About a year later, the puzzle was solved. The low ballers knew they were going to declare bankruptcy- so they could make bids that didn’t include paying their suppliers.

So there are the honest bankrupts who went down trying and there are ‘criminal’ bankrupts- who of course usually operate technically within the law.

When its big boys screwing each other so what but at the same time as the above a large resort hotel here on Vancouver Island went bankrupt. But they had good timing- they waited until the project was finished and went bankrupt the next day.

A year later I was yacking to a back hoe guy and asked him how was bus? Not bad he said but I used to own this machine now I rent it.

The bankruptcy took down about a dozen smaller outfits.

On Wall St. they merge the bankrupt company into a healthy one and the M&A guys make a fortune. Funny, no one calls them credit criminals.

Petunia is right on. Of course the solution would be for everyone to have a steady job with benefits. If Petunia can’t find a steady good paying job because she is competing with a starving Pakistani in Lahore, which she is, and the US as a nation wants to maintain a higher standard of living than in Chittagong maybe we need a guaranteed annual income. She can still do the work of a Pakistani but by birthright she gets the GAW. If our liberals think we need to have the same standard of living worldwide……we are headed there. Right now the only growth industry in America is financial fraud……done legally with the help of cadres of Ivy League attorneys and MBAs and their employees, the Congressmen.

The only Pakistan export to the US of any volume is budget apparel- not an area where most Americans want to work.

A more promising inquiry would be why the domestic auto manufacturers continue to lose ground to imports.

This must be the Huge Guy from Central New York that you are describing. I would think the supply of suckers would have dried up by now but he has been doing this for 24 years with no slowdown.

d profit,

Your ID of the guy is correct.

I have been casually looking for a used pickup truck using carmax, carfax, and other such on line sources. I cannot believe the asking prices for these vehicles. Even 6 – 8 years old and 100k+ miles the prices seem to hover in the 15k range. Just for fun I found a 2015 Nissan Frontier at carmax that was priced at $27k and my payments on it, with $3000 down, would have been about $400/month. Even though I have a good job I could not afford such a purchase. There is a disconnect coming somewhere, someway. There seems to be lots of money floating around the system (“the plenty of money to loan” commercial that NY Geezer speaks of) but is seems to act a lot like smoke in that if you try to grab onto some of it you come away with an empty fist. When this thing does finally jump the tracks I guess the best course of action is to be an observer and not a rider.

That’s one of your easer questions to answer, Wolf. Socialism will get the bad paper, the big and little sub-prime houses will get the vehicles to re-sale at the auto auctions, and the high risk people will be traveling on public transportation again. It hasn’t been that long, I really don’t know why you’re asking.

Wow “Car loans with record long loan maturities: 44% with maturities of 61-72 months, 28% of 73+ months.”

Well lot more work for repomans I guess… Thanks to modern technology the banks can immobilize the car on a whim by 1 click – it can happen while the car is being driven. Then the repoman goes out to re-posses the car that deadbeat cannot drive away.

Alas – what to do if many people lose their cars and unable to go to work? Talk about trickle down economy…

That 1 click bank tech, takes two clicks, and a few seconds to revert, if you are ready for it.

Then you have an untraceable car on the repo list, like the old days.

Unlike the old days not many repo men need to chase the list the old way as the banks keep them busy with pick up A at X.

However the number of empty X’s is growing.

What scares me the most are ‘cash back’ new car loans.

I can see this attracting real criminals maybe preying on Granny- then what happens?

BTW: The Gerber ‘Protection’ Plan etc. AKA life insurance on infants as new as 2 weeks old also has red flags.

When an adult is smothered there are signs, clues. Not so much with a new born.

They’ve got a nerve calling a hazard ‘protection’

But that’s life insurance.

Let me tell you about my car park – that is assuming that you’re remotely interested in what a middle aged debt free Belgian has to tell you about cars:

First off, I’m a petrolhead, and I call the shots in my family when it comes to cars. My wife is in charge of everything else, including all the finances (which is why we are debt free).

Up until may 2015, we drove a 15 year old 250.000 km Citroën Evasion family car, but then far too many check lights started flashing and I told my wife two things: 1) we need another but decent second hand car and 2) you will choose the make and model since you’re driving it 90 % of the time, that is, provided I give my blessing, since this is the only field in which I am more knowledgeable than you are. To my surprise, she went for a (in Europe rather unpopular) Fiat Freemont 2 litre diesel, aka Dodge Journey, before Sergio marchionne forced itself upon Chrysler. We bought a 2012 Freemont with 47.000 km on the odometer for 18.000 euros, 4 extra winter tires and Tomtom GPS-system included. Retail price for this car when new: about 33.000 euros plus the extras mentioned. The car is in mint condition and drives like new, simply because the former owner took exceptionally good care of it. I plan to drive it for at least another 15 years.

Our second car, you ask? That is a 1994 Lada Samara 1,1 litre (1100 cc) petrol convertible/pick up car – a rather bizarre conversion of a conventional 1,1 Lada samara by the German company Bohse. It sat in a show room for 18 years before I bought it from the second owner for 3.500 euros, while it had only 600 km (six hundred) on the odometer. The interior is everything you’d expect from a Russian car: all the cheap plastic trimmings tend to break merely by looking at them, but the engine and gearbox are solid and you can repair virtually anything with a screwdriver. In other words, I bought a second hand new car for virtually next to nothing, that gets you from point A to point B without comfort, and without breakdowns.

So what’s the secret? Never buy new and always buy the less popular, but decent models. That’s why you’ll never see me driving an Audi or a BMW: extremely decent cars, but ridiculously expensive. Do not, I repeat, do not try to keep up with the neighbours when it comes to cars.

Great advice. Thanks

This could be important to anyone buying of a lot.

My sister recently bought a new car. Because she had to decide whether to pay cash, using a HLOC, or use the manufacturer financing she knew exactly what the price would be.

Come the closing- there’s a blizzard of paper- and the ‘fog of war’ but she knew it exactly…

And it was 500 over.

The culprit – Buyer Protection

What’s that? It was assurance (insurance?) mainly of two things- that the car was clear title and that it hadn’t been in any accidents.

That’s right: an authorized factory dealer wanted to charge her in case they didn’t own the car and they wanted to charge her for making sure it hadn’t been in an accident.

But they had slipped up- the salesman had never mentioned this charge.

It may have been intentional, I’m sure many dealers will try and slip it in.

So she balked and after some grumbling they waived it.

One of their mistakes was making it a round 500, crazy. But a month later shopping with someone else another lot tried the same thing: 470 for ‘protection’.

I suggest negotiating your best price and then you also discover this ‘protection’ right at the end- then ask them what is being sold- proof they own the car?

Then balk.

t you negotiate

Read the fine print for negotiable and ridiculous document prep and advertisement fees. LOL dealers passing their own ads often subsidized ads and few keystrokes to print out the sales contract.

Last time I bought a brand new car was in 2005, and 4 cars bought since 2005 were all 3-yr old fully loaded with built-in nav pkg used Audis and Volvos bought at wholesale used car prices from my employer (ex-sales rep cars with no accident and pre-paid manufacturer maintenance pkg) all paid cash.

I sold 1 Audi earlier this year after 1 year of driving 25k miles for $300 less than what I paid (plus sales tax).

Cars will hit the used market in droves. In a coule of years. Student loans are already insulated from doing harm. Accept that the barrowers will be on the hook forever.

Debt based economies must keep the ability to barrow alive. And thy will.

Well I kept my 1990 jeep pickup since buying it new. I had the motor professionally rebuilt and am still driving it. There’s no reason in the world to buy a new car, most of them are electronic nightmares anyways. Even if you do nothing yourself, 6 to 10 thousand dollars should virtually rebuild a car to factory new.

The author lists “not gaining equity in the car” as one of the faults of a lease. Why would somebody want to have more equity in a dwindling asset? Either buy it cash and keep it until it falls apart, or lease it. With leasing, you only pay for the part of the car you use up. You don’t have extra cash tied up in it. That’s why businesses lease.

I agree with your cash payment philosophy, unless interest rates are as ludicrously low as they are now.

But leasing is the most expensive way of automobile ownership. It’s great for dealers and the industry. Dealers can make a lot of profit and customers never know about it (there is no “selling price”). And the industry loves it because the customer has to get a new car every two or three years. That’s why we used to push leases. Every lease was a home run for us.

If you get a new car every 3 years, it is foolish to buy. You lose half the vehicle’s value in the first 2 years. You have your cash tied up in a depreciating asset. Many businesses and a lot of individuals need a newer car.

I personally always bought used cars and drove them for many years. It always worked for me. Now I live in China in a huge city that has excellent public transportation, and I don’t even own a car. Last week I took a taxi all the way across town, 35 minutes, for $5.65 USD. The buses run every few minutes and cost 13 cents. The subway will come on line in a few months and will cost about a quarter.

Getting a new car every three years is foolish, financially, no matter how you finance it.

And if you put so many miles on a car that you NEED a new car after three years, then a lease is outrageously expensive (lease-end value and miles driven are big factors, and if you put a lot of miles on a car, you’re going to get punished).

The main reason businesses lease is because they can write off part or all of the cost against taxes. That’s how and why car leasing began, then it spread to the consumer, as he became maxed out.

Also over the 20 plus years of evolution since leasing took off, a new younger generation of financial illiterates entered the market. They usually could write off nothing. They also wanted instant gratification, and the test drive was just too much to resist.

And when there a closer actually called Wolf on duty, you’re fecked.

Joke!

Then in Canada our rev guys tightened up a lot on realtors for example who used their car for bus and personal, limiting their deduction.

It is a cliche that the average Joe or Jill leases only to reduce their monthly payment for the same car, i.e., they rent the car for the wrong reason. That is how the ads are pitched, the monthly payment.

This should make a good selection for cash buyers like myself when the SHTF. My last new truck was a 2008 loaded that I bought for 28,000. The same truck is now 55,000. No way am I going to pay that for any vehicle. Let the repo,s roll.

I waited a long time for a good deal on a used car. i checked out all the usual sources, even that pit of villainy and vileness called Craig’s List. Through private connections i was informed of a vehicle somebody who wanted to leave in a hurry wanted to sell. I got a 1999 Nissan Sentra loaded with working goodies and well cared for according to the CarFax. I am very happy with my vehicle and it should be good for quite a while. ^,..,^

New cars are a total waste of money unless you plan to drive for 10 + years or more. I bought a 2008 Lexus 460 with less than 30k miles for 30% less than new list in 2010. We will drive that car for at least 12 years. My F250 Was purchased new in 2002 and I’m still driving and will drive another 10 years most likely. New it was about $45k and a new one today is $75.

Am I normal?

You’re very smart. Maintain those vehicles well and they’ll last way beyond expectations.

ie. Mobil 1 EP oil & filters, xmission, coolant, differential fluid changes regularly, etc

Best of luck…