If you look at auto sales, which are flirting with all-time highs, and at commercial real-estate prices, which are way beyond all-time highs, and if you look at the loans, including subprime, that make it all happen, you’d think the US economy is in a white-hot economic boom.

But the economy is barely limping along. What’s booming is cheap but iffy debt that for the moment still looks good on the surface. And that is rattling bank regulators.

“We are clearly reaching the point in the cycle where credit risk is moving to the forefront,” explained Thomas Curry, Comptroller of the Currency, in a speech today. The Office of the Comptroller of the Currency (OCC) – one in the triad of federal bank regulators alongside the Fed and the FDIC – is fretting about banks’ exposure to the increasing risks of ballooning auto loans, particularly subprime auto loans, and commercial real-estate loans.

As they did in the run-up to the Financial Crisis, banks are “repackaging” these loans, including subprime loans, into highly-rated asset-backed securities, in face of “strong demand by investors” that are reaching for yield, in an environment where banks “are reaching for loan growth,” Mr. Curry said. After having “already extended credit to their best customers,” they’re now lending to “less creditworthy borrowers, with all of the increased risk that entails.”

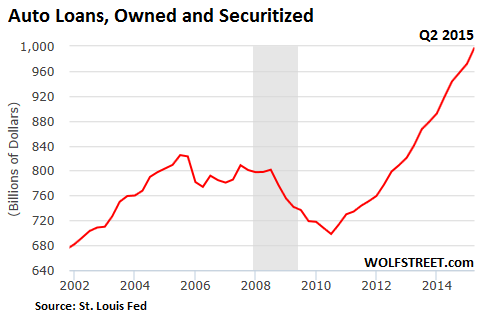

But the auto-loan binge is good for everyone. It’s good “for automakers and the economy,” he said. “It’s also good for banks,” whose financing made “this activity possible.” By the end of Q2, auto loans accounted for 10% of all retail credit in OCC-regulated banks, up from 7% in Q2 2011.

Total auto-loan balances outstanding shot up 10.5% in 12 months at the end of the second quarter and hit $1 trillion, according to Equifax. And 23.5% of new loans earlier this year were subprime, up from 22.7% a year ago.

This is what the auto-loan boom looks like. I mean, it’s not like a bubble or anything:

So Mr. Curry continues:

But what is happening in this space today reminds me of what happened in mortgage-backed securities in the run up to the crisis. At that time, lenders fed investor demand for more loans by relaxing underwriting standards and extending maturities.

Today, 30% of all new vehicle financing features maturities of more than six years, and it’s entirely possible to obtain a car loan even with very low credit scores. With these longer terms, borrowers remain in a negative equity position much longer, exposing lenders and investors to higher potential losses.

Although delinquency and losses are currently low, it doesn’t require great foresight to see that this may not last. How these auto loans, and especially the non-prime segment, will perform over their life is a matter of real concern to regulators.

Though auto loans – or most asset classes – aren’t “inherently unsafe,” he said, “what is inherently unsafe are excessive concentrations of any one kind of loan.”

You don’t need a very long memory to recall the central role that concentrations – whether in residential real estate, agricultural land, or oil and gas production – have played in individual bank failures and systemic breakdowns. It’s an old movie that’s been reprised on a regular basis.

And so he segued to the OCC’s next warning: commercial real-estate loans.

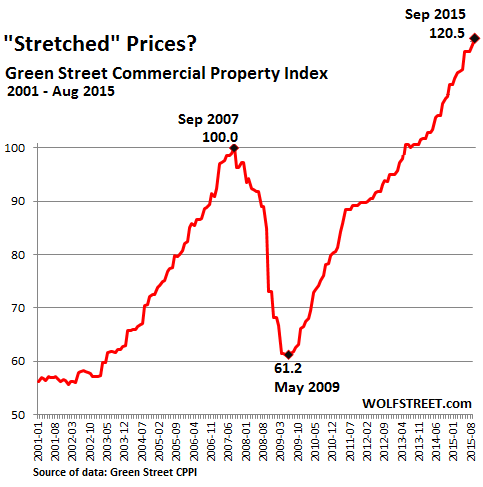

Commercial property prices in the US rose 1% in September from August, and 10% from a year ago, according to the Green Street Commercial Property Price Index (CPPI). They have soared 97% from May 2009 and are now 21% higher than they’d been during the crazy days of September 2007, the peak of the commercial property bubble that collapsed with such splendid results during the Financial Crisis.

“Property pricing has shown no signs of weakening” the Green Street report said. “But one has to wonder how long that will continue. The repricing of risk in the corporate bond market should prove to be a strong headwind for commercial property, where valuations are now rather full.”

But not yet.

Even ratings agency Fitch, which rates Commercial Mortgage Backed Securities, is beginning to fret: “There is nothing inherently dangerous about a real estate cycle,” Fitch explained last month, echoing the OCC. “It only becomes dangerous when market participants forget there is one.” And it warned: “CMBS cannot afford a repeat of the 2008-2009 experience.”

The Financial Crisis was caused by just these sorts of bubbles that blew up in near-sync. The response has been seven years of loosey-goosey monetary policies that inundated the world with liquidity and ultra-cheap money in order to inflate valuations to even higher and crazier levels than they’d reached before the Financial Crisis. That’s the one thing monetary policies have accomplished. Forget the real economy. And the irony is that regulators are now publicly worried about the monster they’ve wrought.

And the real economy? Now even Moody’s is getting edgy. Read… Moody’s Warns “of Jarring Slowdown” in Jobs, Jumps on Recession Bandwagon

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The poster child for this is Conn’s, which had booming sales thanks to in-house loans to people with room temperature FICO scores, using the purchased appliance as collateral. Then Conn’s learned why that’s not a good model and the stock has lost 2/3 of its peak price.

With auto loans it’s insane. People come in upside down on their current car loan, wrap the difference into the new loan along with the sales tax, and voila! – an LTV of 120%. So the price is perhaps $50,000 and the value drops to $40,000 as they drive home. As a result someone now holds a piece of debt paper with a face value of $60,000 and collateral worth $40,000 and steadily falling.

It has been clear to me, at least since my eyes really opened up after the 07/08 debacle, that people fall into three camps; one doesn’t have a pot to piss in, the other two do but half see what is happening and the other half live in la-la land for whatever reason. And to be clear, each has their own problems and risks.

Nothing structurally has changed, so problems are just getting bigger, albeit out of the purview of most.

To get creative, suppose the US pisses of China, who is to say they don’t take their pile of Treasuries, cut deals with a bunch of EM markets/governments, and pay off their dollar denominated debts with them for whatever they can negotiate? To be clear, if Argentina is deep in the hole, China could throw a bunch of T-Bills at them, they invoke all the clauses they can and literally pay off *everything* at par overnight (or in a very short period of time). China could negotiate whatever terms they could get and that is what it is worth to them in exchange.

China could literally have a spread sheet of cleanest dirty shirts, use a sort function, and voila; they walk away from their dollar exposure! Without a single shot fired or a single soldier killed, they could rewrite trade and other geo-political relationships over a long weekend.

Think Venezuela wouldn’t sign up for that? Brazil?

After that, who would want dollars? This is happening already, as I understand it, on a smaller scale as various folks try to diversify out of this asset into the other and so on, but the decision calculus is different at this level.

Maybe I am just a dumb redneck and maybe there isn’t anyway this is possible. In some manner, I say this tounge-in-cheek, but the point is that one day folks are going to wake up and there is going to be a new set of rules and owing/owning (the remaining) dollar debt and it is not going to be fun. Now is the time to get the debt free chair because at some point the music is going to slow down/stop and all hell is going to break loose.

This may go on for a few years yet, but this can’t go on forever.

Stay liquid and stay mobile!

Regards,

Cooter

Except that China doesn’t have the cleanest dirty shirt, it’s real estate bubble is even bigger.

I believe that in the “dollar repudiation” scenario you imagine the effect domestically would inevitably be devaluation/ hyperinflation. In that case, the debtor wins huge while the liquid/ solvent person gets fucked.

The best place to be in that scenario would be leveraged to the hilt on multifamily rentals. Your leverage would simply evaporate, leaving you with title to assets of inherent value. It’s a strong dollar/rate hike scenario that will crush the levered crowd i’d say.

Brutal work schedule lately – late to reply.

In the beginning, I worried a lot about inflation/hyper-inflation. I am firmly in the deflationary camp these days. The money has to flow to the peons for hyper-inflation. Since only a very small subset have access to the gross excess of liquidity in the system, folks like walmart will borrow at 0% and fail to expand/profit selling low margin cheap products to poor people with no money.

Until I see a mechanism for the transfer of significant wage growth to the working/poor class, hyper-inflation isn’t going to happen. So, if one leverages, and doesn’t have access to the mana from heaven, they are going tits up … and that may very well be the plan. The Buffets of the world can run around and scoop things up for pennies on the dollar.

I don’t know what China is going to do with that huge pile of treasuries, but if they are smart they will try to get as much value or minimize losses as much as they can. And I get that they are in over their heads with domestic credit expansion – but they don’t have a common law based system like the US and I can’t logically run those scenarios.

Regards,

Cooter

Cooter +10000000

Your analysis is based on the rules of the old economy, pre 2008. You have not been affected by the financial collapse, so for you, nothing has changed.

For the the rest of us, who have been wiped out by the crisis, the economic realities are different. When we make deals, like the car deal you describe, we know it is a bad deal, but we have no choice. If we can make the payment and get to work, it is a necessary choice. We are fulfilling all our needs like this. If we can get the credit, and still eat, we do it. You can complain all you want about how stupid we are, but we know something you don’t, we are the average case, and they can’t afford not to keep the game going. Your future rests on our survival.

While most Americans do need a reliable vehicle to take them to their job(s), there is a drastic difference between leveraging yourself to the hilt by buying a brand new Benz and climbing in the hole $50K+ Vs. a 2-year old Maxima for maybe $18K. And then paying it off and driving it until the wheels fall off (which would be a hell of a lot longer on the Nissan).

I get it. You are what you drive. Luxury automobiles are the crack cocaine of the aspirational wealthy. And EZ credit terms make even the most unaffordable vehicles affordable. A couple of mixed paychecks though and it’s back to riding the bus.

Regardless of the state of the economy, this is purely a personal choice — one which is all too often decided poorly.

You don’t get it either. For people who have nothing to lose, it doesn’t matter if the car cost 50k or 10k. They are not looking to build assets or are even being aspirational, it is what can I get for the payment I can afford. When you can’t make the payment it doesn’t matter if you lose a 50K car or a 10K car. If a car payment is going to be in your future anyway it doesn’t matter how many times you roll over the loan either.

I refer you to the corporate finance sector for further examples. Every time the interest rate drops they refinance, increase the debt, maintain the same payment. This is how the economy is working in high finance and low finance.

https://research.stlouisfed.org/fred2/graph/fredgraph.png?g=2cDq

https://research.stlouisfed.org/fred2/graph/fredgraph.png?g=2cHL

It’s late in the cycle (or early in a recession and bear market).

Here in the UK, investors have for years been buying yield. Commercial property prices have soared because of yield compression rather than rising fundamental value. The banks are lending on cash flow and momentum. The smart money has been getting out for months now.

And wait until the student loan defaults really start to kick in, that party is just now underway…

It does not take a genius to figure out the endgame. The question is still: When? All signs pointed to 2015 as the maximum possible stretch, when more debt actually subtracts from the “GDP” whatever that means, yet, here we are, almost in November, and everything is still limping along. Some wary voices are starting to whisper again about systemic this and that, but no major credit event yet. Never underestimate the capability of humans to believe the impossible :)

This is going to go on for a very long time. They haven’t even fixed the banking system, or the mortgage markets. They haven’t fixed anything because no one in Washington knows what to do. This is how things got this bad in the first place. It is not a coincidence that Trump is doing well running for the presidency, like him or not, he is a rational competent businessman.

Yes … my 3 rules:

People are

1. stupid

2. fragile

3. but most of all, wanna believe.

Dark energy is most pervasive in the Universe but I think the strongest is human denial. It creates what is not.

I have suspected that there might never be a real systemic breakdown (aside from all the mini breakdowns that are a constant flow now), because I think the upper echelons have found ways to suspend financial accounting rules forever. They may have free money indefinitely to keep their sand castles patched together.

For example, people often point to a derivatives explosion as a possible cause of systemic risk. I’m not an expert, but from the amount of insider collusion we’ve seen in many aspects of this industry, it wouldn’t surprise me if a -$50 billion derivatives ‘tranch’ (or whatever) can be essentially written off as a matter of course, via bookkeeping, given a phonecall from one powerful banking guy to another. This is what Martin Armstrong suggests: when the derivative bombs go off, they will simply make phone calls and rewrite the legalese that governs the contracts. People have speculated that this actually already happened several times in the last two years, and massive derivatives losses are escaped through creative accounting and agreements between parties behind closed doors.

Agreed. Or the CBs will force these people to sort it out.

Another variant of this theme is that, for Credit Default Swaps (CDS), ISDA has to declare the event a default to trigger the CDS.

While it sounds dumb, the contracts are written thusly and if they don’t declare the freaking obvious the CDS don’t pay.

I don’t do full life insurance for this reason – I do term only and keep it short-ish. I don’t want to dump money into a bucket that will be empty when I need it – and that is exactly what a lot of derivatives are going to be because the money just isn’t there if things really hit the fan.

Regards,

Cooter

Used car prices are set for the greatest collapse in history, because repo is so easy today. Remotely disable the vehicle, pick it up, and park it in a field somewhere with the MILLIONS of other underwater vehicles. It’s coming.

That’s when our brilliant gov’t will introduce cash for clunkers 2 to insure another worthless asset gets artificially propped up.

C Smith said, “Used car prices are set for the greatest collapse in history, “.

Wouldn’t bother me one bit. I drive an ’86 Toyota 4X4 pu, my wife a 2009 Yaris. We think of them as, “Transportation”, not a penis substitute, an image maker, or an ‘experience’ that car adds seem to think we all need. I am 60, my wife is 56. In the next few years we will buy our last vehicle, for cash, like the others. Transportation, folks.

But, don’t forget, debt that can be rolled over is really an asset.

Someone’s debt is ALWAYS an asset on the creditor’s books. Every debt always has two sides: the entity that owns it, and the entity that owes it. There is no way around this. That’s why debt, when it blows up, can be so dangerous in the financial world.

I am a UK renter-saver who is frustrated, but relaxed that there is set to be a real estate correction.

Yes, there are two sides, but I believe the UK and US banking sector overall is in much better health. So much risk has been palmed off by the major banks and snapped up by other market participants yield chasers in the market. The major banks have ever more incentives to allow it to crash, to issue fresh debt on crashed prime asset prices. That’s where the treasure is, for the major banks. Fresh lending in volume. Dangerous is those smugly sat on massively overinflated assets. They should look to sell prime property. I’m not going to weep for them into a hard correction, given that I’ve never owned a property and they’ve been living in wonderland.

———————

Three Truths for Finance – speech by Mark Carney (Governor of The Bank of England)

Remarks given at the Harvard Club UK Southwark Cathedral dinner, London.

21 September 2015

‘…Moreover, when next time proves no different, the financial intermediaries at the core of the system will be on a substantially stronger footing. Their capital requirements have already increased ten-fold and their liquid assets are up four-fold. Their trading assets are down by a third and intra-bank exposures by two-thirds.’

—————-

UK Banking stress tests show banks can handle a major crash. And there has recently been a political/revenue move, with hard pincer taxation against leveraged landlords.

Good timing of Ferrari’s old owner fiat :-)

I wish the bug would hit the windshield already………

the fed will continue to bail out all banks now by a few clicks of the keyboard without anyone’s knowledge. they’ll keep this charade up indefinitely. The real killer will be the rejection of the US dollar and tbills from the rest of the world when they figure out the EXTENT that their sovereign savings are being debased by hundreds of trillions and counting exponentially. a world reset will happen with or without the US input.

This is the single biggest risk to Americans I think and enough ink isn’t spilled on the subject to suss out all the angles. Most of what I have seen on the subject has been ZH pointing out that the dollar debt sponges of the world (e.g. Saudi Arabia) are not net sellers – which is a trend that needs to be fixed at the rate the US is spending over revenue.

My thought right now, and subject to change if I can find a better one, is that the large holders of treasuries will trade them to large holders of dollar debt so they can buddy up and walk away from the dollar system. And that can happen very fast relatively speaking.

Then people will finally get the higher rates they wanted!

Regards,

Cooter

Lots of companies had good earnings, stocks are up. Dow isn’t too far from being back at 18,000.

If things are so bad, why are the markets doing so well? McDonald’s, Google, Microsoft, Amazon, GE, Ebay, all beat earnings expectations.

“Earnings expectations” are the most manipulative things out there.

Yes, Google had good revenue growth. But the other companies you mentioned? McDonald’s revenues dropped 4.8%. EBay’s revenues dropped 2.4%. GE’s revenues dropped 1% and Microsoft’s revenues plunged 12%!

If you think that this sort of revenue recession is good, you’ve fallen prey to Wall Street nonsense.

The Euro was always a dangerous construct with no mechanisms for recycling surpluses.

Recycling surpluses is actually the mechanism for getting money back to your consumers so that they can keep consuming your products.

The economies were too different for it ever to work.

Monetary policy could have been geared to the Club-med nations helping them but leaving Germany with massive inflation.

Monetary policy was geared to Germany destroying the Club-Med nations.

The longer it stays on the road, in its current form, the more damage it will do, it was designed to fail at the outset.

https://professorwerner.wordpress.com/2015/07/10/hallo-welt/

Remember all this? How quaint it all seems now, for those who lived within our means, witnessing bailout and massive reflation.

————-

Pretcher: ‘When financial institutions lend for consumer purchases such as cars, boats or homes, or for speculations such as the purchase of stock certificates, no production effort is tied to the loan. Interest payments on such loans stress some other source of income. Contrary to nearly ubiquitous belief, such lending is almost always counter-productive; it adds costs to the economy, not value.

If someone needs a cheap car to get to work, then a loan to buy it adds value to the economy; if someone wants a new SUV to consume, then a loan to buy it does not add value to the economy. Advocates claim that such loans “stimulate production,” but they ignore the cost of the required debt service, which burdens production. They also ignore the subtle deterioration in the quality of spending choices due to the shift of buying power from people who have demonstrated a superior ability to invest or produce (creditors) to those who have demonstrated primarily a superior ability to consume (debtors).’

————-

Repost from ‘What!?’ – a poster at DrHousingBubble (summing up my feelings)

‘WTF is up with all the math? Have we not all learned by now that math has been proven scientifically false? Math, gravity, physics, etc. have gone the way of alchemy and we have replaced them with new sciences like unicorn fartology, rainbowology, this time is differentology, etc… Come on, you are sounding like my grandpa. “Math”, “percentage”, “economy”, what quaint concepts… Horse, buggy, buggy whip kinda makes me chuckle…’