Commodities had once again an ugly week. Copper hit the lowest level since June 2009. Gold dropped below $1,100 an ounce. Other metals dropped too. Agricultural commodities fell; corn plunged nearly 7% for the week. Crude oil swooned, with West Texas Intermediate dropping nearly 7% to $47.97 a barrel, a true debacle for energy junk-bond investors.

It was the kind of rout that bottom fishers a few months ago apparently didn’t think was possible.

For example, in March, coal miner Peabody Energy had issued 10% second-lien notes due 2022 at 97.5 cents on the dollar. Now, these junk bonds are trading at around 49 cents on the dollar, having lost half their value in four months, and 17% in July alone, according to S&P Capital IQ’s LCD HY Weekly. Yield-hungry fund managers that bought them at issuance and stuffed them into their bond funds that people hold in their retirement accounts should be sued for malpractice.

Other bonds too have gotten slaughtered in July.

Among the bonds: Cliffs Natural Resources down 27.6%, SandBridge down 30%, Murray Energy down 21.2%, and Linn Energy down 22.3%, according to Bloomberg.

For example, Linn Energy 6.25% notes due in 2019 were trading at 78 cents on the dollar at the beginning of July and at 58 on Friday, according to LCD. There was bloodshed beyond energy, such as AK Steel’s 7.625% notes due in 2021. They were trading at 62 cents on the dollar, down 22% from the beginning of July.

“The performance is a disappointment to investors who purchased about $40 billion of junk-rated bonds from energy companies this year, thinking that the worst of the slump was over,” Bloomberg noted.

But the worst of the slump is far from over.

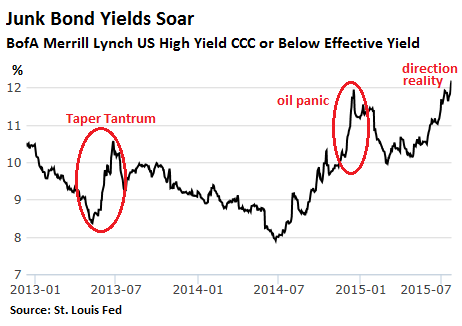

The riskiest junk bonds, tracked by the BofA Merrill Lynch US High Yield CCC or Below Effective Yield Index, have been hit hard, with yields jumping from the ludicrous levels below 8% of last summer to 12.19% as of Thursday, the highest since July 2012:

Note the spike in yield during the “Taper Tantrum” in the summer of 2013 when the Fed discussed ending “QE Infinity.” After which bonds soared once again and yields descended to record lows, until the oil panic set in, as investors in the permanently cash-flow negative shale oil revolution were coming to grips with the plunging price of oil.

But in the spring, bottom fishers stepped in and jostled for position as energy companies sold them $40 billion in new bonds, including coal producer Peabody. Now a lot of people who touched these misbegotten bonds are scrutinizing their burned fingers.

But how much worse can it get?

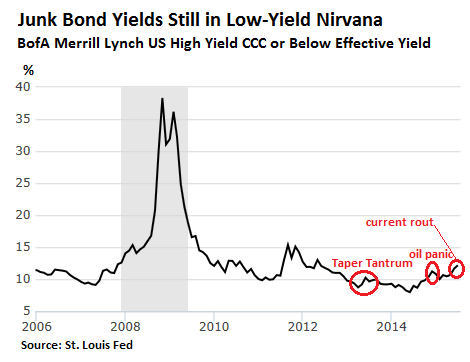

Take a look at the recent past. In the chart below, note how yields can spike when the real selling starts and when liquidity suddenly evaporates, while hedge funds are waiting on the sidelines, with the smartest among them knowing that the first waves of buyers will get burned.

In fact, the “bloodletting” that has transpired so far is a series of barely perceptible squiggles compared to real bond sell-offs:

“It’s been a tough environment for issuers lately,” S&P Capital IQ’s LCD HY News Today summarized the high-yield market on Friday when Exterran Energy Solutions threw in the towel and withdrew its $400 million offering, while Builders FirstSource “was forced to” offer a higher rate and downsize its junk-bond offering in order to bamboozle fund managers into buying it.

This week, only $4.46 billion in junk bonds were sold by six issuers, nudging up the volume for the year to $194.34 billion, almost 3% behind last year’s pace. Sentiment, as LCD said, has “definitely soured for lower-rated offerings, and those tied in any way to commodities.”

In high-grade bonds, there has been a peculiar flavor…

A mad frenzy by companies to sell as much debt as possible while they still can, even as yields and spreads are rising and as prices are falling, before the junk-bond debacle spills over into high-grade bonds. LCD:

The high-grade primary market continues to be swamped with issuance, but the broader sector groaned under the weight of trailing supply and the increasingly aggressive fiscal policies of active issuers, including another spate of big-ticket benchmark deals backing M&A and share buybacks.

This week, $33.5 billion in high-grade corporate bonds were issued, including Intel’s $7 billion offering for its acquisition of Altera and United Health’s $10.5 billion offering for its acquisition of Catamaran.

The United Health deal was the 11th this year over $10 billion, all of which were plowed into M&A and share buybacks, rather than productive investments. In 2014, there were only three such deals, same as in 2013; in 2012, there was only one. That’s how mad this frenzy has become.

Total high-grade bond sales this year have soared 29% from the same period in 2014, itself a “record-smashing” year, and are up 44% from the same period in 2013, according to LCD. These are big desperate increases.

But yield spreads between high-grade corporate bonds and equivalent Treasuries have been rising, and corporate bond prices in relationship to Treasuries have been falling. The BofA Merrill Lynch US Corporate Option-Adjusted Spread reached 1.53% (up from just above 1% a year ago), matching the peak of the oil panic in January, the widest spread since October 2013, “as technical dynamics deteriorated.”

Treasury yields are still extraordinarily low, and the Fed still hasn’t raised interest rates yet, so the average yield across the corporate high-grade index, at 3.4%, is still extraordinarily low as well, and prices are still extraordinarily high. Hence the mad frenzy to issue new bonds.

To fund share buybacks and M&A

Over 50% of the issuance so far in July was for M&A (up from 17% in all of 2014), including our latest hero, Anthem’s $54 billion deal to acquire Cigna, which added, as LCD said, “to the seemingly endless refill of the pipeline for blockbuster M&A-driven debt offerings.”

But buyers of high-grade bonds are very gradually coming out from under the Fed’s ether made of ZIRP and QE, and they’re smelling the acrid stench of burned fingers wafting through the junk-bond market down the street. They all know: the fire starts at the riskiest margin and works inward. And they’re seeing, despite whatever denials they might have, that this process has begun, just when US corporations carry a far greater load of debt than ever before – thanks to the greatest credit bubble in history – while revenue growth is stalling.

Bond fund investors get hit the hardest: UBS, despite the well-known problems Puerto Rico has had for years, wasn’t shy about loading up its clients with Puerto Rico bond funds. Now the whole scheme is blowing up. Unleash the lawyers! Read… UBS’s Puerto Rico Bond Funds Implode, “Collateral Value” Drops to Zero, Investors Screwed

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Can people recommend the best way to short junk bonds? I tried shorting the long ETFs, but they are always getting recalled by the brokers after only a short period of time. Makes me think I am in China :). Oh well at least the police hasn’t showed up yet.

You can research SJB and see if that meets your needs.

What could possibly go wrong. Commodities are collapsing and Junk investment yields soaring. Anyone near the beach better head for the hills.

I’m basically a bond investor and I haven’t bought any bonds for my taxable account in over a year and a half. I have no confidence whatsoever in the “economic recovery” meme. Mathematically speaking, this so-called “recovery” is a fraud from top to bottom. It’s a debt-fueled dead-cat bounce that has no sustainability of any kind.

As Wolf noted, plummeting junk bonds do have plenty of room to fall further. A lot of them are just getting started – a bond going from 98 to 78 to 58 means the bond still has a long way to go to reach zero. Near the end of that trip, vulture funds will typically pick up these dogs at 1 to 5 cents on the dollar and then see if there is any meat on the bones left for them to pick clean.

I’m beginning to suspect that the jig is finally up for this fake recovery. This time around, I don’t think a few trillion dollars of new counterfeit money-printing from the Fed will do the trick. That’s been tried and will ultimately be proven to have been a failure. I think additional money-printing would be taken by all as an absolute vote of “no-confidence” in the phony recovery and the Federal Reserve.

This time around I tend to agree with you. The commodity slump is here to stay (there will be dead cat bounces but they won’t last) and speaks volumes about the reality of the “robust recovery” the world is supposedly experiencing. If things are going so well, why aren’t Chinese factories buying more commodities to manufacture more export goods?

But fear not: the bond bubble will be propped up, no matter the cost. On Friday the ECB approved Italy’s request to have their central bank directly purchase corporate bonds from three utility companies. One of these is S&P BBB rated, only two steps removed from junk. And this is only the beginning. Many large local European banks are junk rated and their bond prices have started sliding down from the insane valuations they had in March-April, when BB- rated bonds issued by shaky Austrian and Italian banks yielded less than 130bps.

I am starting to believe we are about to see a “Fed disconnect”. What I am about to say may sound naively stupid (and it probably is) but it’s a conclusion I have come to after watching the behavior of the four largest central banks in the world (Fed, ECB, PBOC and BOJ).

The Fed will never admit it, but they understood ZIRP and QE have completely failed. That’s why the now infamous “taper” and why instead of embarking on NIRP they have started making vague mentions of an interest rate hike which will probably materialize later this year. They also know when there’s another Lehman moment, they will have no rates to cut to rescue too big to fail corporations. In short they are reaching for the exit, albeit at a snail pace. In this they are helped by the fact the US economy, despite being a shadow of its former self, is far more reactive and free market oriented than its chief competitors.

The other central banks, instead, have failed to understand this because they are really nothing more than policy-enablers. The ECB exists for two only reasons: keep the euro depressed to help Germany export more than it should and Italy, France and Spain spend more than they could. The PBOC exists to help the Communist Party to stay in power by purchasing social peace through prosperity, no matter how phony it is. And the BOJ has morphed into the only way the Japanese government can stay solvent without bankrupting the country through taxation.

The financiers have extracted the wealth out of the middle class and then they moved on to corporate America, where all the equity has been replaced with debt. Americans no longer have the income or credit to bail out this bubble. All the debt is junk. Most of it will never be paid back. The investors/pensioners will be lucky if it is just rolled over, at a higher rate, of course.

It’s not just America. Every country on the planet is in the same boat. There is no escaping it. In the end we will all be like Greece.

One of my good friends I’ve known for over 40 years had a stock portfolio worth about $6 million on January 1.

He invests in traditional blue-chip dividend stocks – oil, railroads, utilities, and consumer “sin” stocks (tobacco/booze).

He’s in his mid-70s, 90% of his wealth is in stocks, and he doesn’t quite understand why he’s down nearly $1 million so far this year, while the “averages” are still near their all-time highs.

He focuses on dividends, and seems incapable of believing that companies ultimately will reduce their dividends to zero if necessary when the going gets rough.

He also believes all the idiotic recovery propaganda, and just can’t see how it is all beginning to melt down.

My wealthy uncle in his mid 80s is the same way, with 2 exceptions. He’s only 70% in stocks, and holds enough “new economy” stocks (AAPL, FB, TWTR) to come close to holding his own on the total value of his portfolio.

I told him last Monday to sell AAPL before they reported earnings. I’m sure he didn’t sell, and is probably regretting it, since AAPL’s swoon down from 132 to this morning’s 123 has cost him at least half a million bucks.

Another friend who isn’t wealthy has most of his money in healthcare mutual funds. He thinks Federal Government spending will prop up the medical care industry forever.

Not one of these people can see that the entire financial system is a fraud that is beginning to roll over, simply because it is utterly unsustainable.

Even Communist China cannot keep its fraudulent stock market valuations pumped up, even with all their decrees. The 8.5% drop in China today is just further evidence that those who sell early will keep some of their capital, while those who continue to hold will ultimately get wiped out.

This is not to say that I like bonds – I think corporate bonds, junk bonds, and most government bonds are even worse deals than stocks right now, which is why I haven’t bought a bond for over 1-1/2 years.

so for a guy over 60, is it time to get out of all my previously thought “safe” Vanguard bond funds???

The end of company pensions and the forcing of employees to use a 401-k (we’re gonna let you mange your own retirement – ain’t that wonderful?) were great for employers, financial planners and brokers but a debacle for the naive masses…..

All the govt defined pension plans, 401K, IRA, Roth, were designed to be pools of money the govt could easily identify for taxation or confiscation. I learned this in the early nineties when I worked on Wall St. There is no reason people need these vehicles to save money, except that the govt wants to know where the money is, and restricts your use of it to favor their donor base, Wall St.

When I hit 56 I put all my money in GICs and term deposits. I turn 60 next week and am pleased I have not risked my nest egg chasing the big score. I have now been retired for 3 years and am doing just fine on a reduced income. In fact, things are great. Reason? No debt, ever, beyond a small mortgage paid off years ago.

I have a buddy now 56. He is freaking about the future. He bought scads of paper gold a few years ago, convinced it will go to to the stratosphere. He is losing his shirt and plans to continue on and double down. Meanwhile, he is carrying a $100,000 mortgage. Nuts. Last year he asked me about energy stocks? I told him to stay the hell away from them as they were looking for new suckers and junk investors.

Unless you are born in the robber baron bankster class, or are totally consumed with getting more and more, Aesops fables make for pretty good investment advice. I am thinking of “The Ant and the Grasshopper”, and the “Tortoise and the Hare”. Add in some hard work, reasonable expectations, and an aversion to debt the Bob’s your Uncle.

Cheers!!

As far as Gold goes. My prediction is this. Gold is going to get sunk back down too 200 bucks like it used to be and all of that Gold that the Russians and Chinese have been buying up is going to be worthless.

He who laughs last, laughs the loudest.

Sometimes he who laughs last is a raving lunatic:

https://www.youtube.com/watch?v=8IelTUWgMvU#t=3m14s

https://www.youtube.com/watch?v=A_u2PMzFIYM

My own take at an extreme prediction is the BRICS nations will demand gold bullion for their exports. China’s products, Russia’s energy and the BRICS’ resources can’t all be substituted, so the other countries will have to go along. Neighbouring countries may end up adopting this procedure as well.

Gold will be revalued as a means for international payments and will trade at multiples of today’s price.

VegasBob,

I watched the launch of Jeb Bush’s campaign, while most people listened to it, I watched the audience. I wanted to see why Jeb thought he had a chance. His supporters, look like the folks you describe, untouched by the financial crisis. While they may be down, they are far from out. Like the Madoff victims, everything always looked ok to them, until it wasn’t.

Mark, WHERE are you buying your Kool-aid? From “People are liars, friend” Jim Jones? I guess you’ve bought the whole barbarous relic, expensive doorstop propaganda hook, line and sinker just in time for a TOTAL GLOBAL COLLAPSE. Good luck with that. Enjoy your laugh.

Vegas Bob, send your two friends each a copy of Taleb’s ‘The Black Swan’ soonest. Worried, Hell Yes – run, do not walk to the nearest 401k exit or you will not pass GO or collect $200. Keep in mind if you pull more than $3000 out of whatever bank account you deposit the 401k funds into, a.) they will tell you it will take at least a week to get the cash for your withdrawal and b.) will probably generate a Suspicious Activities Report. Because, sir, YOU are an unsecured creditor. I’m glad you’re here but you are very late to the party.

Very sobering information and opinions here. In fact, I think I am about to alleviate that sober thing in a few minutes. I live in west central Alabama, Southeast USA. We have the flagship state university here. There is a belief around here that we are bulletproof economically. Adding retail space and apartment complexes like they are going out of style. Around 100,000 in metro area, if you can really call that a metro area. We did have a major rebuild to do following a direct hit from an F4-5 tornado in 2010. But the most of the damage was to single family dwellings. Those retailers damaged or destroyed have long since rebuilt. And, many of those destroyed neighborhoods are being replaced with retail space. Most of the jobs created since 2010 have been in retail. People lease vehicles around here like they are about to stop making them. The debt load per capita in this berg must be unsustainable, as in miss one pay check and the dominos tip. Housing costs to income ratios are definitely at the high end of the range. Never mind the interest rate, simple division of the home prices by loan term and addition of insurance and taxes should scare people half to death. But apparently don’t.

The point is, I fear for my sanity when I see so many inexplicable trends locally, while watching the bigger picture and what I consider to be the almost guaranteed downside reality that others have pointed out on this post. If anyone lives in or has knowledge of similar areas, I would appreciate your observations. I fear that I may be the one whose tether has slipped.

Regards.