So who the heck are the Really Great Ones?

Americans have been on a borrowing binge. To buy their favorite cars and trucks, they’ve loaded up on $1.14 trillion in auto loans. Young and not so young Americans are mortgaging their future with student loans that now amount to $1.28 trillion. Credit card and other debts are at $1.12 trillion. And mortgage debt stands at $8.82 trillion.

So, total household debt was $12.35 trillion, according to the New York Fed’s Household Debt and Credit Report for the third quarter 2016. That’s a massive amount of debt. Many consumers are struggling with it. Student loans are seeing enormous default rates, and repayment rates are far worse than previously disclosed. And “debt slaves” has become a term in the financial vernacular.

But it isn’t nearly enough debt…

Neither for the New York Fed whose President William Dudley, in a speech a few days ago, practically exhorted households to borrow more against the equity in their homes so that they blow this cash and drive up retail sales: “Whatever the timing, a return to a reasonable pattern of home equity extraction would be a positive development for retailers, and would provide a boost to aggregate growth,” he mused, with nostalgic thoughts of 2008.

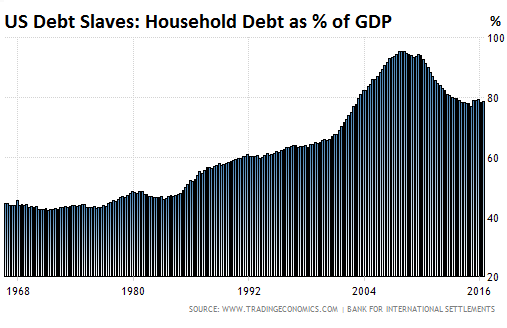

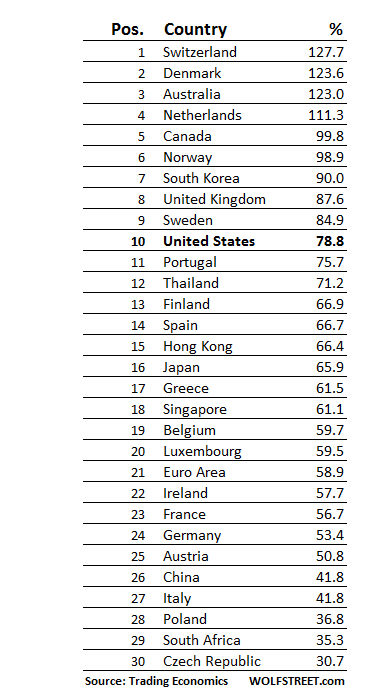

Nor for the global rankings of debt slaves, where US households squeaked into the ignominious 10th place, barely ahead of Portugal! I mean, come on! Portugal!!

There are many ways to measure household indebtedness and debt burdens. Comparing total household debt to the overall size of the economy as measured by GDP is one of the measures. And per this household-debt-to-GDP measure, the Americans are in 10th place with 78.8% and look practically prudent compared to the peak just before the Financial Crisis (via Trading Economics):

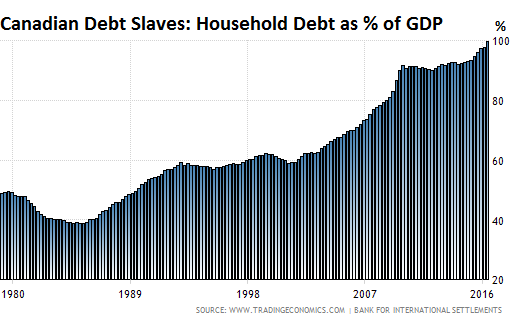

We have long written with great amazement about Canadian households that, tougher than nails, have funded a fantastic housing bubble with even more fantastic levels of debt, though this bubble is now coming apart at the seams in the once hottest market, Vancouver.

But their household debt-to-GDP ratio of 99.8%, as hair-raising as it may seem, only landed Canadian households in 5th place (via Trading Economics):

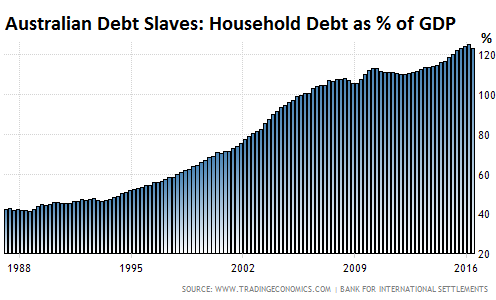

And we’ve have long written about the immensely over-indebted households of Australia, who’ve funded their extraordinary house price bubble with dizzying levels of debt. The bubble has started to unravel in Western Australia and is threatening to spread to other markets. But even with a mind-blowingly glorious household-debt-to-GDP ratio of 123%, Australians are only in 3rd place (via Trading Economics):

So who the heck are the Really Great Ones?

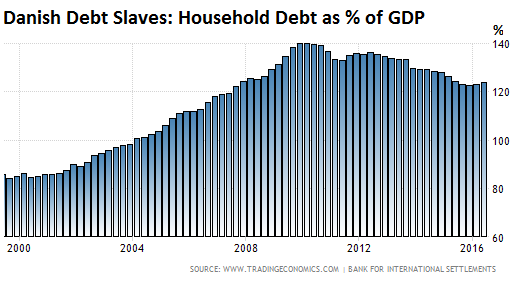

Danish households clocked in at 123.6% of household debt to GDP. These figures from the Bank for International Settlement, gathered up by Trading Economics, cover the period through Q2 2016. So Australians, who were essentially neck-to-neck at the time with the Danes, might have surpassed them by now. But that stunning level of 123.6% of GDP is good for 2nd place, though it’s down from 140% just before the Financial Crisis (via Trading Economics):

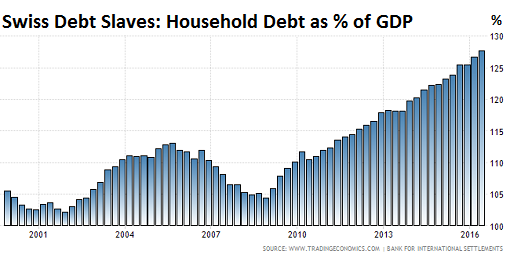

And here is Number 1, the most glorious debt slaves of all, the country whose central bank is trying to manipulate down its currency by imposing steeply negative interest rates: Switzerland. And what has thrived in this zero- and negative-interest-rate nirvana is debt, with the household-debt-to-GDP ratio soaring over the years to 127.7% (via Trading Economics):

That leaves the Also-Ran Debt Slaves:

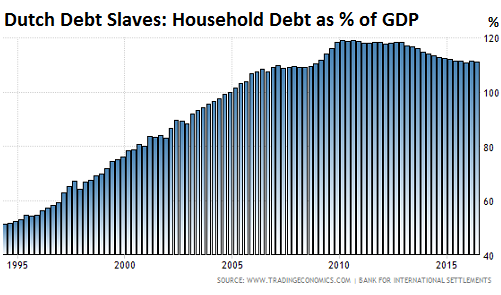

In 4th place, the Netherlands with a household-debt-to-GDP ratio of 111.3%. Now, I know that the fearless folks of the Netherlands believe that they’re on top of the heap of debt, that they in fact are the Number 1 debt slaves, and by some measures they may be, but not by this measure (via Trading Economics):

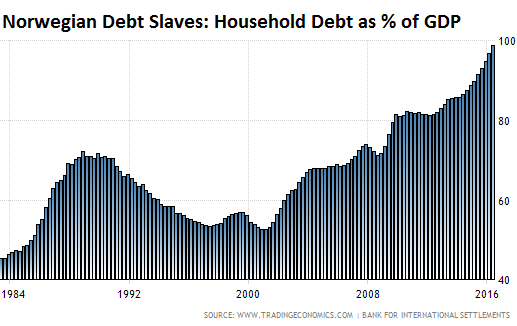

In 6th place, barely behind Canada, is a country whose people just recently discovered the pleasures of loading up on debt: Norway. These folks nearly doubled their debt-to-GDP ratio from 2002, when it was barely over 50%, to Q2 2016, when it was 98.9%. Note how the debt levels have skyrocketed over the past few years. Where did the Northern prudence go? No one knows, but good riddance (via Trading Economics):

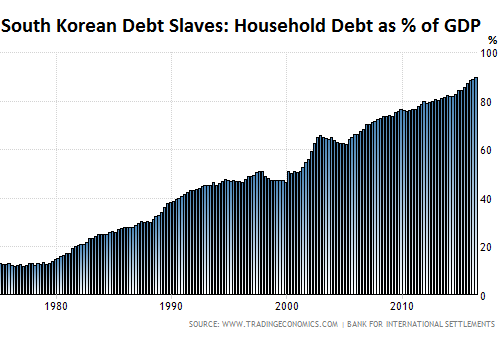

In 7th place, with 90% household debt to GDP: South Korea. Nothing is going to stop them. They have been relentless in piling on debt, except for minor dips during the Asian Financial Crisis and the Global Financial Crisis, and even those crises slowed these brave folks down for only a little while (via Trading Economics):

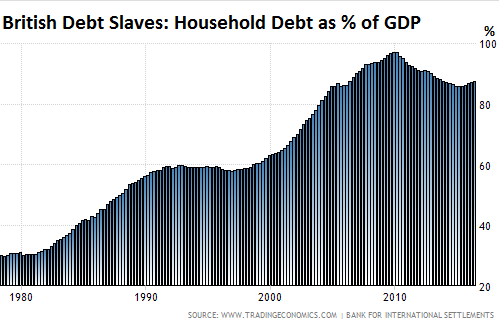

In 8th place with a household-debt-to-GDP ratio of 87.6%, the Brits. Like the Americans and a few others, they had ambitions of prudence after the Financial Crisis but have recently tossed these nettlesome ambitions into the wind and are now once again finally increasing their debt levels (via Trading Economics):

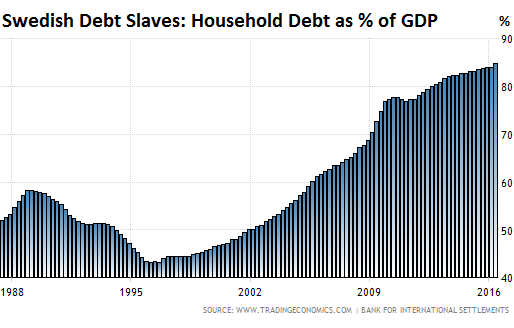

In 9th place, a country whose consumers have discovered the power of debt in the late 1990s and haven’t looked back since: Sweden, with a household-debt-to-GDP ratio of 84.9%, up from about 43% in 1996 (via Trading Economics):

This – 10th place – is where American debt slaves fit in. So we barely measure up. Note that household debt in some of the European debt-crisis countries, such as Italy, Spain, and Greece, is by comparison with their Northern brethren, fairly low, though their public debts and banks got them into trouble.

Here is the list of the 30 countries with the most indebted households in relationship to the size of the economy. Find China:

And here’s some inevitable food for a terrifying thought: The countries with highly indebted households, so the top of the list, are mostly countries were central-bank policy rates are very low or even negative, and where mortgage rates are super low. What happens to those housing markets, the households, the banks, and the overall economies when interest rates rise even a little and that whole equation of perennially ballooning debt falls apart? We already know what happens.

The other options is a big bout of inflation to help wipe out the purchasing power and burden of that debt. But that debt is a huge asset class with very low returns as it is, and if a big bout of inflation sets in, the holders of these assets – banks, pension funds, insurance companies, and other institutional investors – are going to take a licking, as are the hapless people (which is nearly everyone) that counted on the purchasing power of those cash flows. Those are the two options out of this debt nirvana.

So what would Yellen do? Read… Treasuries Got a Break. Now Beatings Resume until the Mood Improves

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

United States in eighth and tenth place. Presumably United Kingdom, not otherwise listed, is number eight.

Ooops. Yes. Thanks.

U.S. unlike other countries have been conditioned for someone to take care of them and this is with being the reserve country of the world. For this reason they should be #1 for indebtedness.

Oh really? Perhaps you have forgotten that every developed country besides the USA has universal healthcare. The fact is that the US actually does a terrible job of taking care of people.

– In e.g. Netherlands, Denmark & the US interest payments on a mortgage are tax deductable. I.e. part of that interest payment is financed by the taxpayer. It allows the home buyer to spend more money for a house.

– In Australia a person can become “an investor” and buy a house to be rented out. Then the costs for that house are tax deductable (again shifting part of the costs onto the taxpayer).

– But in some countries (Netherlands, Denmark, Australia) there’re restrictions on where to build a house. (Zone regulation)

All separate things combined have pushed up home prices & total Household debt.

– The australian “tax saving” program for that “investor” (see above) is in that land well known under the keywords “Negative Gearing”. (Google it)

add to that:

– endless subsidies for homebuyers that often amount to free money, e.g. in Netherlands on top of the standard 103% mortgage (= no money down needed) one can often get a starter subsidy (buyers under forty who didn’t own a house in the last 5 years) of 25-50K euro, while these people are already loading up to the max on debt. The starter subsidy is usually interest free for a few years and after than one only has to pay interest on the loan if the home appreciates. If the home doesn’t appreciate at all even the whole loan amount doesn’t have to be paid back (= the local taxpayers get stuck with the bill).

– the Netherlands has a ‘National Mortgage Guarantee’ which is a free put option for homeowners. For less than 1% of the total mortgage amount the homeowner is guaranteed never to lose a penny when he has to sell the home. Think 1% is not free? It is, because thanks to this semi-government guarantee people get even lower rates for the banks, because there is ‘zero risk’ for the bank (= even more risk for the taxpayers, but who cares). This mortgage guarantee protects a whopping 200 billion in basically subprime Dutch mortgages with just 0.8 billion in funds (probably invested in ‘zero risk’ real estate and government debt). After over 1000% price rise for the average Dutch home in 25 years, this seems subprime insurance to me …

– of course nobody wants to know if you have other debt like huge student loans. Don’t be stupid enough to mention it when applying for the mortgage and all will be fine.

– The Dutch government also has been doing everything they can to jack up rents outside the social housing sector, especially after 2008. Owning a home is now often 2-4x cheaper than renting on a monthly basis. Of course there is a reason why buying is so much cheaper, but nobody wants to know … if the market crashes taxpayers will have to pony up and home debtors will be fine, homeowner evictions are extremely rare in Netherlands.

The Dutch are a bit worse than most other countries when it comes to juicing the housing market (basically the whole economy revolves around it) but similar tricks exist in many other economies in the West.

– OMG. Didn’t know it was that bad in the Netherlands.

– Subsidies are NEVER free. They will have to come out of someone’s hide. Think: Taxation.

Wow, this is worst then Canada. Basically this is money printing scheme money done through housing subsides. I thought Canada was the only country in the world relying on housing to prop up a dying economical activities.

– Yes, I have heard of the “Mortgage Guarantee” system (have family that lives in the Netherlands). Sounds too good to be true and it is. Because then the taxpayer is subsidizing the lenders (again). As a result, it is/was not uncommon to see dutch houses that are financeded for the full 100% (or more).

– Without that guarantee I assume banks are only willing to provide financing for say 80% (like here in Germany). And the people have to come up with the remaining 20% of the money.

“In e.g. Netherlands, Denmark & the US interest payments on a mortgage are tax deductable. I.e. part of that interest payment is financed by the taxpayer. ”

A tax deduction is not the same as something being financed by the taxpayer. This way of thinking assumes all of your income is owned by the government and it’s only by their benevolence that you get to keep some of it. A very medieval peasant way of thinking…

>A tax deduction is not the same as something being financed by the taxpayer.

Actually yes, it is. It is a subsidy.

If all sources of income are taxed at a certain level, except for one which is taxed less or not at all, then the government is “picking a winner” at the expense of everybody else.

If the Dutch government where to tax interest as income (which I was never able to convince myself it is not), everybody else would need to pay less taxes.

Indeed interest deduction in the Netherlands was conceived as a tax rebate for the rich, and a politically viable way of ending it is a re-design of the tax code.

– Your reply reveals YOUR way of thinking, not mine.

– It’s Always financed by the taxpayer. A deduction means that the government receives less taxrevenues and that has to be compensated by increasing taxes somewhere else.

– What A LOT OF people fail to notice is that a deduction for interest payments on mortgages is actually a subsidy. But NOT for the borrower, but for the LENDER !!!!!!!!

“What A LOT OF people fail to notice is that a deduction for interest payments on mortgages is actually a subsidy. But NOT for the borrower, but for the LENDER !!!!!!!!”

Be fair its a subsidy for both.

Just like US defense spending it is economic stimulus.

Only the dutch method is much more dangerous as it must one day implode, and unlike US defense spending. You cant turn it of without causing global financial issues.

“Be fair its a subsidy for both.

Just like US defense spending it is economic stimulus.”

– Agree. A tax deduction for a mortgage means that a borrower can make a higher offer for a house and spend more money. In that regard this subsidy/tax deduction is indeed an economic stimulus.

– But the borrower hands that subsdiy over to the lender. I.e. the lender receives more interest. So, there’s no benefit for the borrower. The situation even gets worse for the borrower because the government is then forced to increase some other tax (e.g. sales tax, income tax, etc) to pay for that tax deduction.

“Only the dutch method is much more dangerous as it must one day implode, and unlike US defense spending. You cant turn it of without causing global financial issues.”

Please elaborate. Why are you comparing US defense spending with “the dutch method” ??

“Please elaborate. Why are you comparing US defense spending with “the dutch method” ??”

Bottom line, both are variant’s of Economic stimulus.

If I turn off US defense spending.

A small sector of the Economy is effected. Quiet seriously. It will send ripples through the predominantly US Economy.

If I turn off the dutch housing bubble, The whole country and the global financial system will be seriously negatively effected. There will not be ripples, there will be Tsunami’s.

Willy, you tend to sound like a nut case. I recommend that youdo not quote somebody else at full length then add one or two sentences of your own. You waste everybody’s time. Do not use ALL CAPS frequently in your messages or multiple exclamation marks at the end of your sentences. This does not make you sound more convincing, quite the opposite. It makes you sound as if you are screaming.

– Agree. I should have been using less large caps. But sometimes people are so entrenched in their (outdated) views.

“When the facts change, I change my mind. What do you do, Sir ?”

Johmn Maynard Keynes

Yeah for Australia – we didn’t come in at number one.

I guess we’ll have to work harder at that.

Unlike in the good ole US of A our mortgage debt are recourse loans – the banks will hound you for every penny.

Unfortunately the Australian ‘debt slave’ also is unlike other countries: we do not have low mortgage rates.

Standard variable rates are higher here than fixed rates in other countries.

A VRM will now run around 4.9% so we aren’t in that basket.

The A$ has also gone up this year (for some strange reason) as well which will lead to the Reserve Bank cutting rates.

That probably won’t flow through to VRM payers though as the banks will keep some for themselves as usual to increase profits.

The spread between the discount rate and VRM rates is now much higher than during the GFC and hence the huge profits of the commercial banks.

90% of the appreciation in real estate in Australia is compliments of our 100% cash Asian friends. Australia welcomes anyone who wants to load up on Aussie real estate with cash purchases, our Government is not too fussy about where the money comes from.

We support International crime should be on large signs at all Australian International airports.

Most states (probably 70%) in the US have recourse loans.

Yes. People don’t realize that about 38 states are full recourse, including Florida, which was one of the epicenters of jingle mail.

Don’t people declaring bankruptcy in Florida get to keep their homes? ( I thought this was one reason many big-time financial miscreants bought mega-mansions there)

No. The mortgage is secured by the home. So if the borrower defaults, the bank takes the home and sells it during foreclosure. Then it can try to go after the former homeowner for the remaining debt (outstanding mortgage + costs – proceeds from the sale). Bankruptcy simply prevents that bank from going after the former homeowner, garnish their wages, etc. A judge supervises the proceedings and decides what the bank can do with the remaining debt. But the home is that bank’s.

Bankruptcy law in the US is federal, so it’s the same for all states.

However, foreclosure can take a long time. And often, homeowners continue to live in these homes without making any kind of payment, until evicted.

Florida’s property laws may have some quirks (whether creditors other than the home lender, like the IRS, can take the home, etc.). But I’m not the right person to comment on that. Maybe some other readers can.

Have you ever wondered why there have been so many foreclosures in states such as California, Arizona, and Nevada?

If you live in one of the 12 “non-recourse” states of Alaska, Arizona, California, Connecticut, Idaho, Minnesota, North Carolina, North Dakota, Oregon, Texas, Utah, and Washington you are potentially in luck! If you so happen to own property in one of these states, and have substantial assets elsewhere, you can legally hand over the keys to the bank and exonerate yourself from the mortgage with no penalty against your other assets!

See more at: http://www.financialsamurai.com/non-recourse-states-walk-away-from-mortgage/#sthash.qb86xmLc.dpuf

P.S. In Texas these rules apply for 1st liens, but not 2nd liens and Home Equity loans.

P.P.S. Furthermore, Texas has an *UNLIMITED* homestead exemption in bankruptcy as long as you didn’t defraud your creditors by paying off your house within 1 year of declaring bankruptcy. So if you have a $10,000,000 home (or even a $100m home) as long as you do not have a mortgage it essentially does not count toward your assets.

The wrinkle in Florida law Wolf was referring to is the homestead exemption which allows a Florida homeowner to shield his primary residence from claims of creditors. This only works if you live there most of the year.

These statistics don’t tell the whole story (it’s not necessarily better or worse in reality, just incomplete). The main pitfall is that debt as a percentage of GDP for the households (or any entities) by itself, does not say a lot about the balance sheet situation and thus the real position these people (or entities) are in.

I don’t have the whole story for all countries involved, but for the Netherlands one important thing to note is that the Netherlands has 1) one of the highest retirement savings amounts per capita which is not factored into net wealth in these stats and 2) mortgages are financed at 101% LTV (and outside of Amsterdam and the big cities I don’t see Dutch RE as being significantly overvalued in terms of affordability). I would say that the balance sheets of Dutch households overall are fine at this moment, although in a (asset price) deflationary environment you will have obvious problems. These pension assets are also partially invested in RE. However, there is no strong indication this is going to happen any time soon or at all.

Dutch mortgages are also full recourse loans, by the way and our bankruptcy laws are nothing short of draconic (heh heh, squeeze those disgusting unprotestant undisciplined spendthrifts!) .

What these statistics point to, is the rapid balance sheet expansion that has been going on since, oh I don’t know, probably since the gold standard was abandoned? Whether this is unsustainable and what might be the consequence of this unsustainability, is something only time will tell.

What is valid though, is that expanded balance sheets may lead to a precarious middle class (aka the precariat, or aptly named debt slaves). With these balance sheets, if (but ONLY if) there is ever even a moderate asset deflation, society will (without any reform) turn into a massive debtor’s prison with extreme inequality. I hope I live long enough to see the outcome of all this funny business.

I forgot to mention the Netherlands also has student loans but you only have to pay back 4% of your income above the minimum wage, and after 35 years the remainder is forfeit. The other thing about these loans is that the rate is linked to Dutch treasuries so the rate is now 0% (as it cannot become negative by law).

So in terms of “debt slaves”, when it comes to student loans in the Netherlands it’s more like a government handout. The cost of education (tuition and books) can also be carried as a loss years into the future (although few people use this). Another advantage of the student loan is that it is deductible from your net wealth, over which you pay a 1.2% annual tax.

Long story short, if you play the game right your student loan pays itself back and if you play the game excellently the student loan can be a real profit machine (the maximum you can borrow is roughly €100k if you stay in school for 7 years and borrow the max amount. This is a €100k investment fund which you can borrow at 0% and invest/trade with for a return exceeding 0%, all the while not paying any taxes over the excess returns. Really it’s a finance student’s wet dream).

In my case, my student loans are mostly bad for banks taxpayers since I lend them their own money back at higher rates (note that deposits are at about 0.6% and are insured by the gov up to 100k in case the bank goes belly up, so that’s about as risk-free as it gets in this world, which is strange in a way because the gov 1-yr is negative while you can invest in a deposit for 0.6% which is guaranteed by that same government. It really all doesn’t make a lot of sense, but as a small fish these are better risk-adjusted returns than at any time in history).

So tl;dr not all (student) debt is bad (for the lender).

are you a Dutch realtor, banker or economy student?

extremely unrealistic description of the real Dutch situation …

” if you play the game right” yeah right, every ‘clever’ Dutchmen thinks they will play the game right and stiff the neighbours with the bill, and homes and pensions will keep appreciating forever. In your dreams.

Moreover, most of those pensions are illiquid, as they are heavily invested in government bonds and, besides, CANNOT be withdrawn on demand. The next debt crisis or euro crisis will wipe out a hell of a lot of these. And the euro bond market is already on life support from Draghi and fellows, only until they finally find themselves cornered: there would be NO BID should they ever try to sell their artificially overvalued papers. So pension “savings” should hardly count as a cushion for the Dutch mortgage bubble.

Economy student.

Nothing unrealistic about my description. If I borrow at 0% and invest risk-free at 0.6% in a deposit then I am earning a 0.6% risk-free return. That’s literally free money that the system is just giving me (the icing on the cake is this money doesn’t affect my eligibility for any other welfare benefits like rent subsidies and so forth).

Either way, in the statistics I might show as an individual with about 300%+ debt-to-income but this debt is generating cash for me, since I didn’t spend it. Not all debt is equal, and not all of it is bad. Considering the public debt-to-gdp of NL is quite modest, I don’t see any problems could arise with this setup.

Also, nobody said homes would keep appreciating forever. You don’t need to be invested in real estate to stick your neighbour with the bill. Real estate is (obviously) significantly overvalued in many locations right now.

How come you’re always so salty nhz?

My question would be where all those returement savings came from? My guess would be that they came from those good days of the Dutch Decease, when gas was abundant and was enough to sustain all those government hand-outs. Now gas is mostly gone and again the question arises what productive activities will support the real estate market going forward? There is some wind potential, but what else?

Dutch pensions are not government handouts.

Our pension savings are delayed salaries: every month Dutch workers set aside a non-trivial part of their salary, with or without help from the employer.

The money goes into private pension funds, who put it in whatever passes for solid investment opportunities (mostly abroad) at the time.

The funds are strictly regulated and must keep a certain level of liquidity. If they do not, pension payments are cut until liquidity is restored.

No bail-outs, no redistribution, no government intervention, except for regulation.

(There is also a pay-as-you-go system called AOW: a basic pension for all residents. However, the AOW has no savings.)

>what productive activities will support the real estate market going forward?

Productive activities? That is so much 20th century.

NL has a huge current account – largely as a result of the pension system explained above – and is a tax heaven.

Import and export to and from Europe largely goes through the Rotterdam harbor and will continue doing so in the foreseeable future.

We have a few advanced industrial companies, too.

Other than that: yes, the middle-class is shrinking here too. Wages are stagnant. The banking sector is way too large. Pension funds are suffering from low interest rates. The gas field is running out. Our trading partners are not doing that well.

Housing prices will have to, eventually, go down.

– Ah. Pensions yes. But here we are talking “Household debt”.

Debt is a liability, pension is an asset. These statistics only show something about the liability side of the balance sheet, hence say nothing at all about the solvency of the households. Debt-to-income is a terrible metric except maybe to get an idea of balance sheet sensitivity.

@Wolf I think having some statistics about interest service-to-income ratios would be much more enlightening, if you can find them. I think US would go to the top 3 at least and the Netherlands would be near the bottom. China would be much higher (it’s hard to maintain high debt-to-income when interest rates are upward of 10%).

tl;dr these statistics don’t really say anything worth knowing and it’s definitely nothing to be alarmist about (not to say there aren’t problems, there are).

what info does debt service-to-income provide with current ridiculously low rates, that are the lowest in 400 years (or according to some the lowest in 5000 years). Of course it is relatively easy to service debt when the debt is free (or even cheaper than free)!

It only tells you that the system is completely f***. ? Yes, all will be fine if rates keep declining forever, if banks keep assuming that there is zero risk in mortgages because of NHG etc. and if the government invents some additional homeowner / debtor subsidy every few years ;-)

You said above: “borrow at 0% and invest risk-free at 0.6% in a deposit”. Do risk-free investments exist? Borrowing means credit creation hence currency creation. Prices rise as a result of this. So that measly 0.6% deposit rate might at some point become net negative. When it does, bond investors start to rebel, rates rise and the whole “free money” scheme unravels.

@NHZ: you are exactly right. However people have been saying rates will rise for 6+ years because they are the “lowest in modern history”. To some extent the rates are supply and demand based, and the demand is also based on the ability to service the debt. Hence without structural improvements in people’s balance sheets (which won’t just magically appear) or a substantial rise in default risks or some other paradigm shift, I don’t see rates rising. Central banks putting a relentless bid under bonds also doesn’t help the rising rates case.

Time will tell. Even modest rates rises could feed into a higher rates > increased default risks > higher rates feedback loop. It should be obvious this is what’s happening quite far from the top (in yields) so plenty of opportunity there, and no reason to jump the gun.

@No Debt: Well, it’s risk-free as long as the government/economy doesn’t completely collapse. However, in the case where this happens all bets are off and there is no purpose in planning for such an extreme event.

Surprised Ireland’s not up there: according to the source*, the figure dropped from 94% in 3 years. Why? Sensible mortgage lending restrictions imposed by the government on banks. However, this has done little to slow the growth in house prices or (especially) rents, since there is a chronic lack of supply. Builders are only interested in building for rich “investment” cash buyers, not for average people who are just looking for somewhere to live at a sensible price.

* http://www.tradingeconomics.com/ireland/households-debt-to-gdp

Ireland is included on the list, but way down in 22nd place, with a ratio of 57.7%

Could that be because many debts were erased or written down in the books when their bubble popped? I have heard some examples of that (especially for speculators with multi-million euro property loans), but have no idea how common that is.

I cannot imagine the debt went from 94% to 58% in three years just by making new loans difficult (and maybe forcing people to pay down existing loans), such policies usually mean only that the bubble grows slower or shrinks a bit.

Yes. Same thing in the US. Part of the decline in household debt after 2008 was the wave of foreclosures where homeowners lost the house but also got rid of the debt. Nearly 40 states in the US are full-recourse, but if the borrower doesn’t have anything, it’s not worth going after them in the US system (unlike Spain). When push comes to shove, they can always seek protection from creditors with a bankruptcy filing. Lenders know this is useless and just sell the house and charge off the remaining debt.

Good point. Most of the so-called “debt deleveraging” (-debt reduction) that show up on FRED plots and the like really are losses taken by the banks, and paid for by depositors through ZIRP. The debts never got paid down, they were simply written off.

@ Wolf:

OK, that explains the difference with Netherlands.

Over here the government stepped in, mostly through taking over the banks and forcing them to be extremely friendly towards delinquent homeowners. Very few people were evicted and because of the strong decline in rates, most of the mortgages that went under water after 2008 (a total of 1.1 million if I remember correctly, about 20% of Dutch mortgages) are still being paid, because paying the mortgage is now often cheaper than renting (and there is a severe shortage of affordable rentals).

Some people got their whole mortgage forgiven while they could stay in their home, but the banks won’t tell what numbers we are talking about here (most of the cost of this was effectively paid by the taxpayers who funded the banks after 2008).

It’s easy – just change bankruptcy laws such that debtors can officially opt to become serfs. Or better yet, make it “non-optional”, like they did with student loans. That’s the easy way out for the banks, and they’re the ones calling the shots now. Imagine the irony of Trump arguing that U.S. bankruptcy law is too lenient. “We must do it to save the working peoples’ pensions… They do want your great pensions, don’t they? The pensions are going to be sooooo great!”

Please note that due to the Swiss Tax System, it is in most cases financially attractive to keep the mortgage debt. But this does not necessarily mean that the owners of an appartment/house are too high on mortgage debt.

Remember that still around 65% of the people living in Switzerland rent the appartment/house they are living in.

Presently, you will obtain a mortgage with 20% down payment and being able to prove that you could still foot the bill with the mortgage rate going from around 1.5% to 5%.

Consequently, the majority of the people living in Switzerland cannot afford to buy an appartment or a house.

I’m very surprised about the Swiss at number one and have never seen that in other debt statistics from e.g. IMF and OECD (probably more reliable than Trading Economics?).

Netherlands too encourages people to keep the mortgage debt as high as possible, you don’t need any down payment (103% mortgage is standard, and some years ago even 120% was perfectly normal) and there are more owners than renters. Also, the increase in home prices in Netherlands dwarfs the increase in Switzerland – so it’s totally impossible for the Swiss so have far higher personal debt, this simply cannot be right.

I think the high position of Switzerland is due to some anomaly in the statistics, maybe due to all the foreigners banking there and creating fake fiscal positions?

Trading Economics gets the data from the Bank for International Settlement (BIS). These institutions (including BIS, IMF, World Bank, etc) all get the same data from the countries themselves.

Also this measure is debt-to-GDP, not debt-to-disposable-income which is another common measure. The Swiss are near or at the top in terms of income, so the debt-to-income ratios would be lower than some other countries.

Good that they are not using disposable income, because if you believe our statistics office, the disposable income of the Dutch (including those on social security etc.) varies with a factor of less than 2x for 99% of the population.

garbage in, garbage out.

And as we can see GDP is correlated to debt levels, i.e. some “prudent” countries manage to squeeze out every last penny of GDP through financialization. Debt-adjusted-GDP is nowhere in any statistics. You might develop such measure, and it can earn you a Nobel prize one day.

Trying to wrap my head around this…

We’re indebted to the future, right?

Now, who owns these debts?

Central banks are buying debts, right? And they will probably continue doing so.

Who owns the ECB, who are we/our descendants indebted to?

At a rough guess, the central banks will eventually have a fire sale and flog their debt portfolios to the wealthy for pennies on the dollar. The taxpayers in each country will pick up the difference between book and market and the central banks will be off the hook. That’s how the system is supposed to work isn’t it ?

Every time I read the financial press I am reminded of Lily Tomlin’s wisecrack, “I try to be cynical, but it’s so hard to keep up”.

in practice (not officially of course) the debts are owned by savers and taxpayers; they are on the hook if the debtors do not pay up.

Taxpayers are not the same as debtors, many of these people who owe huge debts pay very little of no taxes, especially in countries like Netherlands that are a tax paradise for everyone who buys a (severely overpriced …) home.

The same disparity exists within Europe, just look at the Target2 balances. Most politicians do as if these are irrelevant (just ask clueless politicians like Angela Merkel) but some day this will matter, e.g. when one of the bigger eurozone countries drops out, or when there is an even bigger financial crisis. The Germans think they are ‘wealthy’ but they only are on the assumption that ClubMed is going to pay their debts – this is not going to happen and Northern Europe is in for a very rude awakening.

Most of the mortgage debt is owned by institutional investors, such as pension funds, insurance companies, mutual funds (including those for mom-and-pop investors), and the like. The ECB, the Fed, etc. own only a smallish-part of it.

it is reassuring that much of the mortgage debt is owned by the institutions that guarantee those fat pensions ;-)

BTW, ECB has been in discussion with the Dutch government for several years now about buying a huge chunk of the Dutch mortgage debt. The problem seems to be the Dutch National Mortgage Guarantee (NHG) and how this would be applied if the mortgages are moved from institutional investors to the ECB.

My impression is that the ECB knows that it is a Ponzi system and maybe they even suspect that Dutch politicians are trying to offload the downside risk of the bubble …

You got a source for this? Seems far-fetched to me, the ECB is not a hedge fund (tho close) and doesn’t buy mortgage debt except maybe indirectly.

Actually, the Fed is the largest holder of mortgage debt in the US. They’ve been buying it up from the banks for years now. They now own about $1.8 trillion worth of mortgage backed securities.

Yes, the Fed may be the single largest US holder of mortgage debt, but it only holds about 8.1% of it – as many other (smaller) institutions hold the vast majority.

– In the US, total outstanding mortgage debt = $14.1 trillion.

– Fed holds $1.74 trillion in mortgage-backed securities. Which, according to my math is just 8.1% of total mortgage debt. Hence, a “small-sh part of it.”

The central banks are not doing you any favors. For all their talk about inflation being merely 1-2%, the cost of living closely tracks the rise in national debt, and for those whose incomes do not keep pace, it means a steadily declining standard of living (sometimes described as “the hollowing out of the middle class.” The poor suffer as well, but well, they were always poor.

You only have to look at a few old movies or newsreels to see it. Compared to the crowd at a baseball game 40 years ago, or that attending the inaugural, the man on the street today practically looks like a hobo.

State funded Student loan’s along with many other State debt’s.Can not be absolved in bankruptcy, in many nation’s.

How long before Citizens start changing Nationality’s to avoid Student loan debt. For qualification’s that can not get them into a high paying Job.

There are many “Qualification’s” particularly from P45 style US private university’s. That are State debt funded, and not worth the paper, they are printed on.

The picture is not complete without including savings. A man who makes $28,000 a year and who has $0 savings and $6000 in debt is in bad shape.

A man who makes $120,000 a year and who has $300,000 in savings and $6000 in debt is in very good shape.

This article presents just a piece of the picture.

Yes … you’re referring to household “wealth” which is a different measure: assets minus debt. We have written about that too over the years. And there always are some interesting and surprising findings too.

Why would someone have $300,000 in savings on which you receive almost no interest, and $6,000 debt on which you pay higher interest?

In a vicious cycle that job could disappear in a blink of an eye, and you are left only with debt. We are currently in a artificial virtuous cycle, and many have never experienced the opposite cycle.

It could just be a temporary debt from using credit cards for convenience while shopping or travel. A few big splurges a year can get you a $6000 average balance.

I agree that that is theoretically possible, however, I am talking in Canadian context where every living creature with 26 chromosomes has an average non-mortgage debt of over $20,000.

I guess that I am not “normal”. My wife and I have not had any debt since 2003. We use credit cards to fly several times a year and for car rentals, but I pay them off as soon as it is posted.

Roy Cohn, a notorious NYC lawyer and eventual close friend of our current president, had a financial philosophy that was based on the premise that owning anything in America was too risky. He considered the legal framework of the country to be hostile to owners. This is interesting because he was a prominent figure in the anti-communist movement and witch hunts. In his personal life he found it safer to lease everything and own nothing outright. His premise was that you didn’t have to own it, to enjoy it, and if you don’t own it, they can’t take it. People around the world seem to be coming to the same conclusion.

There’s an old business axiom that you lease anything that goes down in value and buy anything that goes up. You lease cars, trucks, machinery. You buy buildings and land.

There is no need to invest in a depreciating asset. That cash can be better used elsewhere.

Individuals deviate from this rule because of emotional attachment, with unfortunate results.

that Mr. Cohn may have other objectives with leasing than the strictly financial side.

I once won a lawsuit about commercial fraud against a very rich Dutch businessmen (net worth around 160 million, 20 years ago) only to find out that there was nothing to collect from him. All his assets were in financial vehicles, the trophy homes and cars that he had were all leased and ‘not his own’. Just to be sure, right after the verdict he sold his main company (the one involved in the fraud) to his secretary for one guilder. That is illegal, but the secretary was stupid so she could not know that she got the ownership illegally, and the businessman had no money anyway officially so I got nothing …

People who want to protect themselves in this way are usually big crooks. It’s a sure way to get rich of course, but you need some help from lawyers and other crooks in the justice system.

“People who want to protect themselves in this way are usually big crooks. It’s a sure way to get rich of course, but you need some help from lawyers and other crooks in the justice system.”

Or in the past they or their parent’s or grand parents have had something stolen or unfairly from them by the State or court’s.

If you don’t protect it, the Socialist takers, will take it from you.

That’s just the way the world has become.

Consumer protection law’s, have become consumer and taker, extortion tool’s.

Wealthy and working people, are simply soft targets, for do nothing takers.

yes, I can imagine that although it’s probably more a risk in the US and similar countries than in Europe due to the ease of claiming huge damages in court or e.g. heavy penalties for supposed tax evasion.

“His premise was that you didn’t have to own it, to enjoy it, and if you don’t own it, they can’t take it. People around the world seem to be coming to the same conclusion.”

Now hes a smart guy. So as this has been my philosophy for over 25 years and i didn’t get it from him or a book.

I developed it through dealing with the state illegally taking thing’s from people.

So I suppose I am at least not stupid,

that was just BEAUTIFUL, Miss Petunia. i love how/when you write.

“…His premise was that you didn’t have to own it, to enjoy it, and if you don’t own it, they can’t take it. People around the world seem to be coming to the same conclusion.”

Wolf: A little perspective on your debt concerns:

To begin with lets look at Merriam-Webster’s definition of the term: “The state of owing money in amounts greater than one can repay.” ( NB – from the 1989 edition)

But the world has changed since then and debt is an entirely different animal today. It is now accepted world wide as a contract which will provide the debtor with a reliable and substantial risk free, tax free long term return in terms of real wealth. How so? Simple. one borrows a 100 cent dollar and repays, eventually, maybe, with 10 cent dollars.

This is how governments everywhere, even in the frozen North, “balance ” their books. This is why your concerns about stock buybacks are misplaced. The stocks may not be that attractive in themselves, but being short the dollar or any other fiat currency certainly has been a bonanza for borrowers and looks to stay that way indefinitely. “Indefinitely” because there is no politically viable way out from under in a world addicted to living above its means. Consumption is in; thrift, saving and the like are out.

The Swiss, historically the world’s leading moneymen, understand this. They realize that the rules of the game have changed. With NIRP they don’t even have to worry about investing the borrowed funds. They can spend them on real assets or just sit on them, confident that every day the real value of their indebtedness is shrinking.

So there’s no need to fret about the future of the millennials et al coming out of school up to their eyeballs in debt. They may not know it yet, but they’ve got it made. Unless ……..

From the Globe and Mail: (last paragraph)

“And so we hear endlessly about a dream of home ownership that is ultimately about maintaining wealth and status for certain groups. Included here are the long-time owners in Vancouver, Toronto and some other cities, the politicians who depend on their votes and the big chunks of the economy that live off home sales.

A house is a nice place to live, especially if you’re raising kids. Partake if you can afford it, but don’t be persuaded by the voices of the housing sector’s dream syndicate. They’re mainly looking after themselves.”

Vancouver and Toronto skews the stats. As such, they are misleading. I live on the BC West Coast that, it seems, retired people who have assets seem to flock to by the thousands. My first home was on the Sunshine Coast and I paid it off by age 30, (and believe me, I did not make a very good wage). My second house, (which was an improvement over the ‘shack’), was purchased in Campbell River because I had to relocate for employment. I paid that one off in about 6 years and was mortgage free again by age 40.

Over the years the value of the house ebbed and flowed, nevertheless, I paid it off by age 50. In my mid-fifties I sold it and moved away. It had appreciated 5X purchase price in less than 10 years. By selling the home it allowed us to downsize and buy a ‘fixer-upper’ on a river, plus an additional 16 acres raw land zoned residential. I am now 61, and have been retired for 4 years. That….is what home ownership can do. That…is what modest debt can do for families.

Having said that, we have always had junker cars. We did not borrow money for vacations. We do not ever have a credit card balance. We used to eat suppers out for only rare treats or special events. We cooked our own meals and our very good meals were planned around the weekly grocery store sales. There were no impulse buys. Along the way my daughter completed university and my son now has an electrical company. They were well looked after. The problem isn’t housing, it is common sense. People need to appreciate their station in life and adjust their purchases, accordingly. If a person lives and works in a place where housing, be it renting or ownership, is unaffordable, then they need to make plans to move to where they can afford to live and prosper. The problem is, people think they can and should have it all.

I have an older brother who chose to live in Paris for the last 40+ years. Recently, my entire family had to tell him to stop asking us for money as we had our own problems to solve and bills to pay.

It always comes down to the ant and the grasshopper.

http://www.bartleby.com/17/1/36.html

The problem isn’t housing! The problem is everything else. The problem isn’t a house purchase per se, it is trying to buy a home where you do not belong; like Vancouver, Toronto, New York, SF, Seattle….you folks know the list.

Even the ‘Tiny House’ movement is trendy and boutique….overpriced. It is unbelieveable.

regards

Paulo – Totally agree.

Work with what you have. Bought our old abandoned farm (128 acres) on the Island in the early eighties. Family thought I had gone coo-coo! Over many years of weekends, vacations and working holidays, the place is now home to most of the family that thought I had lost my marbles!

The really good part is ownership without debt and being a responsible, charitable and engaged manager of the land. We lease out small garden plots for the price of a part of the harvest. Working with what we have.

“The problem isn’t housing! The problem is everything else. The problem isn’t a house purchase per se, it is trying to buy a home where you do not belong; like Vancouver, Toronto, New York, SF, Seattle….”

Amen!

“Even the ‘Tiny House’ movement is trendy and boutique….overpriced. It is unbelievable.”

Another manifestation of the squeeze on the middle class: Pushed into tiny houses.

I chuckle whenever I see comments like this. It perhaps escapes your mind that where you are is a function of two things:

1. You’ve made “good” choices in life.

2. Other people makes bad choices in theirs but it lifts the country’s GDP in the period when you cash out.

You might not be able to cash out with 5x if Canada hadn’t gone on a borrowing binge. Remember the tide that lifts all boats?

I dislike Warren Buffet but even he has to be right sometimes. Let’s see how naked future generation is when the tide goes out in Canada.

So you were able to be mobile and relocate for work. Perhaps you were lucky that you could find work in places where houses were still affordable. But not everyone lives under the same circumstances, nor with the same luck.

“The problem isn’t a house purchase per se, it is trying to buy a home where you do not belong”

Are you saying people who grew up in Vancouver, Toronto, etc., do not belong there, but some foreign “investors” do?

yup.

I have lived in Vancouver. And Calgary. Unaffordable. When enough people leave there will be a shortage of workers and wages will rise. When enough people leave, housing prices will fall allowing affordable purchases. I worked construction in Calgary and hated every second of it. I transferred to lethbridge and finally moved back to the Island. I was a kid in Vancouver and my parents left for the Island in ’69. It was unaffordable then.

There are many professions that allow relocation. It takes planning and action to take control of your circumstances…that is all Ii am respectfully suggesting.

Growing debt along with inflating assets (mainly real estate) are a direct result of government’s Central Banks choking market interest rates. People are very “can I make that monthly payment” oriented, so a 3% mortgage rate translates directly into 300% more mortgage debt than a 9% rate.

And when you consider that GDP still includes “government” as part of the output of an economy, as governments tax away the income generated in the private sector, it begs the question as to whether the last private sector employee can pay for everyone else’s debt too.

Add to that the composition of GDP like housing sales and all kinds of other stuff associated with home sales, and it gets even more funny. The Dutch economy grew at a whopping 1.5% last year, thanks to … people selling more homes to each other at much higher prices!! I doubt that outside home prices and government wages anything else improved …

Just make sure there are enough RE transactions and the debt to GDP will remain ‘managable’ :-)

Existing home sales are not counted in GDP.

Correct. Only the transactions fees and cost are counted, such as realtor fees and closing costs. This can represent 6% or 7% of the transaction price. Then there are the moving costs, the remodeling, buying new furniture and fixtures, etc., all of which are counted in GDP. So housing transactions do have some impact on GDP.

according to the Dutch statistics office, the improvement in 2016 for the Dutch GDP (1.5% instead of a little below 1% as expected) was mostly due to increased housing sales.

But maybe they are lying about that too ;-(

Degrees of debt, or the form of the debt measured by using differing metrics, does not alter the economic foundation of debt.

First rule of economics:

All debt will be paid.

Either with dollars worth pennies, or with pennies worth dollars.

It will be paid.

There is no ‘getting around’ this basic economic tenant. The debt will be disposed of, one way or the other.

– In Germany & Belgium interest payments on a mortgage are NOT tax deductable and the “owner” of a mortgage Always has to pay interest & principle. Hence the (comparatively) low level of Household debt.

– Whereas A LOT OF australians have “interest only” mortgages. They’re assuming that home values will continue to go higher. Bailing them out of their mortgage debt. Sheer lunacy.

yes, Germany is also about the only country in Western Europe that doesn’t have a housing bubble. Of course it helped that they had a financial black hole to the east in the nineties …

Belgium is a special case IMHO because of all the black money etc. going on in the RE sector, at least until the introduction of the euro. I have read interesting stories about how after 2000 or so they allowed Belgian citizens to use black money to buy homes in Belgium without paying any taxes or fines on that black money, effectively ‘whitewashing’ (officially there were minor fines, but recent government statistics show that most home buyers never paid them, probably due to some clever tricks from the banks).

– There’s another reason why we (Germany) don’t have a housing boom right now. Since say the year 2001 wage earners have been put on (what I would call) a “Wage diet”. There has been simply too little income/wage growth to support a housing boom.

Yes I know … I get a bit irritated when people from ClubMed start complaining about the ‘wealthy Germans’ who are extorting those poor South EU countries, as if the average German is very wealthy. It’s just a small elite that got fabulously wealthy thanks to the euro, and average wealth of German households is several times lower than e.g. those in Italy.

And it will get even worse for the average German when the Target2 balance becomes real, maybe this year already …

On the other side, I have been reading about Dutch pension funds ‘investing’ in German rental RE over the last few years, which probably means that German rents will be going up ;-(

@NHZ:

– It’s actually the german worker who has susidized the PIIGS countries from say the year 2001 up say 2010. German wage growth has been anemic but german exports became very large. (think: Current Account Surplusses & Deficits). Complicated story.

– And then the ClubMed countries started to complain about “extortion” in 2010, 2011 & say 2012 when in fact it was that the subsidies that were withdrawn.

“– Whereas A LOT OF australians have “interest only” mortgages. They’re assuming that home values will continue to go higher. Bailing them out of their mortgage debt. Sheer lunacy.”

Many do that as it is the only way they can afford to get into a property.

If price rises, they are keeping pace with the market.

Whereas those still trying to save a deposit, then take an I and P loan, are falling further behind the market.

Overhead a nice lady who worked at one of the large banks say they approved a 99 year old man for a mortgage. I cringed when she said it.

Small houses on the outskirts of Toronto are going for 500k. With a 50k down payment, mortgage is almost 2k a month plus all taxes and upkeep.

Houses selling for 850k can be rented for $1600. Yet renting is just throwing money away. It’s a licence to print money as everyone here says. Bubble mania is still going strong and on track for a strong spring. New houses still going up. Line ups for pre construction houses sold to flippers hoping to sell upon completion.

– Countries with a Current Account Surplus have – on average – lower interest rates than countries with a Current Account Deficit.

– The Eurozone (as a whole) is still running a Current Account Surplus, hence the lower rates (see also the surprisingly low rates in Southern Europe).

– If you want to see some “Housing Fireworks” then watch Hong Kong. Homebuyers borrow money with short term rates. The central bank of Hong Kong follows what’s going on in the US with short term rates. Remember what happened in the last say 14 months in the US with those short term rates ?

When interest rates rose (or threatened to rise) after Trump’s election, many people in The Netherlands rushed to lock in their low rate or to load up even MORE mortgage debt in fear of rising rates. Seriously. The next Dutch housing bubble-in-the-making (after the one ending in 2008) is worth tracking, in particular of capital Amsterdam. This is all thanks to Uncle Draghi and his scorched earth ZIRP. Mind that Holland has some of the biggest pension funds in the world. It was only due to the slightly rising rates at the end of 2016 and a rising stock market that some of these funds escaped payment cuts, which would have caused huge political and social upheaval. That’s the other side of the debt binge mirror that apparently no one likes to see.

I don’t think the Dutch bubble ended in 2008, that was just a small hiccup in an epic bubble that is still expanding.

The Dutch have learned over the last 25 years that you are stupid if you don’t take on maximum debt; savers are heavily punished (almost zero rate on savings accounts but severe wealth taxes) and debtors are rewarded in every possible way, including shifting the downside risk of their gambles to the taxpayers.

The last Dutch housing bubble popped in 1981, with average prices down 40-50% within 1.5 years, after a prior 100% price runup. The price runup in the current bubble is at least 10x bigger, if this bubble crashes it will take the whole Dutch economy with it. But don’t worry, almost every Dutch buyer of the last 20 years has mortgage insurance so nobody will be hurt ;-)

I agree. Mortgage insurance is more or less a farce. It has only a fraction of total outstanding mortgages in cash, so in times of a housing crisis it would essentially be worthless. And recently, conditions for paying out have been sobered. If government steps in, it would be dragged down as well.

Much of this says more about consumers than anything else.

You are not entitled to your own living space or a new car every five years. When I was on the low end of the totem pole I lived with housemates and drove a car that was already paid off.

Now that I have a better job, I have a mortgage that I am furiously paying off with that same car. Its 12 years old, but I am not buying a new one until after the house is paid off, and I have saved for the next one.

Credit cards are for making money, not losing more of your own. Don’t live above your means. I can’t remember the last time I paid interest. Now I just cash in rewards points on purchases I have vetted.

If you think like a dumb consumer, you will live like a dumb consumer.

“the debts that can’t be repaid won’t be repaid. And … all you have to work at is how you’re not going to repay them.” Steve Keen (partly paraphrasing Michael Hudson)

Wolf – I am sorry to see that you have no response to my comment on how one should now view debt. I suppose this could mean that you agree with me….. but I doubt it.

I can’t respond to everything that I agree or disagree with :-)

But I thank you for your thoughts.

Hi!

This article does not provide enough information to make any conclusion.

It will be interest to see GDP growth forecast for countries, labour size (how many employed and unemployed) and median/average age of contry. So basically if the people are old and near pension and high unemployment with high debt rate and low GDP growth forecast it means very bad. But if there are a lot of young families that need to live somewhere and it’s expected they will take huge loans. And if GDP growth is huge it’s no doubt they will pay all debt.

Cheers,

Znaiko

Debt levels can be broken down further by regions. It is likely that some regions are leading the country everywhere. In British Columbia, just as the party was about to run out of steam, the government du jour, in a pre-election frenzy, found yet another arrow in the quiver: they will lend a 5% down-payment to first time home buyers.

Isn’t democracy great or what?

I guess the question isn’t if, but when does the FED pop this bubble they’ve blown on behalf of their employers?

Nice work if you can get it….

Wolf, if you were given the task by a Central Bank to measure the health of an economy, what data would you prefer to use. Cheers.

How much money I am making would be my number one data point.

I put more “value” into this statistic :

https://www.gfmag.com/global-data/economic-data/916lqg-household-saving-rates?page=2

Household debt is one thing, I prefer to look at total debt load. Total debt in the US is about $65T and rising steadily at about $2.5T a year. The minimum load that could place on society is the total yearly interest owed on that debt, which according the government sources is about $2.4T a year. So this is about 15% of total GDP. If you plot interest owed over total GDP over time you will see the last two times this ratio exceeded 20%, a recession followed soon after. This IMO is about the maximum burden that can be placed without causing collapse. In fact due to economic factors since 2009, this level may be even lower.

Interesting but not all debt is equal. Combining everything conceals the real issues. It would be more interesting to see a breakdown of the debt by category by country.

Credit card debt should be weighted at many times normal debt given its higher interest rates (often 18-30%).

Auto loans should be weighted higher too given they are on a declining value asset.

Mortgage loans, even on crazily overvalued properties are still better than credit card debt. 10 years from now the house is unlikely to be worth almost nothing (unlike like a car) no matter what happens to the bubble.

a couple point increase to each gdp and we are back in business. i guess this is like the currency war that you really dont want to win. you dont want to be number 1

I wonder why Trading Economics omits New Zealand? I believe we would be 7th on the list otherwise.

Yes, curious. Maybe it’s too small (4.4 million people – quite a bit smaller than, for example, a city like Greater Houston which has about 6.5 million). Or maybe the BIS wasn’t able to get the data?

Why no South American countries?

You have to have a stable currency and very low interest rates in order for household debt to balloon. That’s not really the case in South American countries. Mexico is by that measure the most indebted, in 35th position ahead of India, with a ratio of 16.3%. One of the reasons for this low rate is that a large number of Mexicans are relatively poor and do not have access to credit at all. That pushes the averages down.

Other countries like Venezuela and Argentina have consistently crushed their own currencies, which kills credit in that currency.

I will wear the chains of time. I will wear the chains of art. I will wear the chains of love. But I would never wear the chains of a banker.

Interesting article. I am disappointed that my country, Canada, is doing so poorly in this area. However, I have noticed our government trying to put water on this fire. They have been doing so with public declarations that there is a problem, and with bringing in regulations to calm Canadians’ borrowing.

That said, when our personal debt is added to our share of the national debt, we are doing much better than Americans who hold much greater (about 3 times) national debt, don’t you think?

In my opinion, debt is debt. Debt that doesn’t have a clear pay down path, and clear asset to show for it is bad.

I practice what I preach. My personal situation is very nearly debt-free. (We just upgraded our house to one which brings in about $4000 per month in rental income, and we have $150,000 debt to show for it.)

When you include Ontario and Quebec debt, the Canadian “national” debt is more than double.

Eew, you are somewhat right. I didn’t realize just how much provincial debt there is.

Seems that Canadian Federal + provincial debt is about 1.3T (https://www.fraserinstitute.org/sites/default/files/cost-of-government-debt-in-canada-2016.pdf)

At 35 million, our per capita is about $37,000.

The equivalent number for US is: $21.2T (Federal + state debt).

At 320 million, US per capita is about : $66,000

So y’all are just under 2 times as indebted when counting federal + state/provincial debt.

“brings in about $4000 per month in rental income”

What kind of rental is this? rents in Toronto which arguably has at least the second highest rent in Canada, are far blow hot areas in US. So to earn $4000 rental income, you’d have to rent 3 one bedroom apartments.

Now, a rental property with at least 3 one bedroom apartments, in Toronto, in an average neighborhood would cost you probably upwards of 1.5 to 2 million in this real estate bubble. And given you said you have $150,000 debt, then you must have paid the 1.35 to 1.85 million in cash.

I live in Yukon. We owned a paid off house which we sold for $375K. We purchased a new house with two suites (legally it is a triplex) for $550,000. We put about $50K into the new place. We’ve been whittling away at the 225K difference.

Our rental income: two rental suites at about $1.2K each, plus one mildly handicapped person living with us (we also have a “near suite” for her) that returns about 1.6K because of government support.

Well, your situation is then unique since in Yukon 3 bedroom houses can be rented for $1500.

Very interesting article. The relation of household debt to GDP however should be viewed with caution. A country with a lot of debt-fueled spending (USA) shows comparatively a higher GDP than a country with little or no debt-fueled spending (such as Russia or Switzerland). The higher the relative GDP the more comfortable looks the household indebtedness. A second aspect to be considered is net-assets. Households in the US have almost no savings which offset debt. In Switzerland for instance it is customary for tax reasons to have mortgage debt and to keep the balance on cash accounts.

I do not wish to defend the Dutch, whose mania for mortgages I often find disheartening.

However, almost all the private debt is, indeed, mortgages. And while the value of a car goes to zero after 10 years or so, and while you cannot sell your Bachelor’s degree, you are able to sell your house to pay down your mortgage.

So I am not particularly concerned about the 4th place of the Netherlands. Also, house prices fell by some 20% in 2009, with limited consequences.

If you look at Italy (my home country) instead, mortgages are a relatively small fraction of the paltry 41% of private debt. A large part are car loans and loans for things like holidays in Bali or Sharm-el-Sheik.

Given the ever-shrinking wages in Italy, I am more worried about the low Italian debts than the high Dutch ones.

canada is well positioned for an economic boom we finally got rid of harper the conservative who destroyed our economy.

trudeau is doing great the lower the real estate goes the better for our economy.

i predict 2008 prices which is still 50 percent lower than now.

we need to build our resource economy more and start taxing the elitist bankers

I thought Trudeau opposed an resources economy? IP is easy for elites to export.

I was just looking at rentals in Vancouver, and I searched for rentals which cost between $600 and $1000, and I found 1600 of them; here’s the Craigslist result:

https://vancouver.craigslist.ca/search/apa?min_price=600&max_price=1000&availabilityMode=0

It seems to me that in such a low cost rental situation, you’d have to be really stupid to buy a shack in Vancouver for a million dollar or more. People are real dumb; if you buy a house as an investment, it should be able to generate some income, and from what I see no property in Vancouver can generate any meaningful income.

We do not build houses anymore, we build jumbo homes. Then renting out a room is built into the calculus, and everybody has the same idea. That might explain low rentals, but I suspect those are still pigeon holes. What could possibly go wrong? Let the good times roll on, there is no tomorrow.

And we sell dreams, not reality anymore :).

Australia doesn’t seem to be big on Craigslist, but from the limited information I find on Craigslist Australia, it doesn’t seem properties in Australia can provide that much income from rentals either.

It would be great if someone could provide some insight on rental averages in hottest Australia regions?

Although America has a large influence on the world teh world does not revolve around it and its institution’s.

Try Ebay Australia and Trade me NZ for some quick Insight in to those markets.

I wasn’t implying anything; I just could find a lot of rental postings on Craigslist Australia. So, I was trying to find a good source where rentals are posted for cities like Sidney.

On Craigslist Australia, the rents that I saw for Sidney were fairly low in comparison to for example San Francisco Bay Area.

I pay $430 a week in rent for a 3 bedroom house in Melbourne. The house would cost $1,100,000 to buy.

This list does not include New Zealand. We are top contenders with about 7th place at 91.3% in 2015 according to this article based on BIS numbers;

http://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=11651662

We let bankers maximise profit with their debt products.

What was supposed to happen?

July 26, 2011 The Federal Reserve ADMITS that Its 12 Banks Are PRIVATE – Not Government – Entities

Much of the tens of trillions in bailout money and “easy” money from quantitative easing went to foreign banks (and see this, this and this). Indeed, Ron Paul noted recently that one-third of all fed bailout loans – and essentially 100% of loans from the New York Fed – went to foreign banks.

http://www.washingtonsblog.com/2011/07/the-federal-reserve-admits-that-its-12-banks-are-private-not-government-entities.html

May 21, 2013 Why the whole banking system is a scam – Godfrey Bloom MEP

• European Parliament, Strasbourg, 21 May 2013

• Speaker: Godfrey Bloom MEP, UKIP (Yorkshire & Lincolnshire)

https://youtu.be/hYzX3YZoMrs

The high dept of Swiss people is due to the tax laws. Its favorable to NOT repay your mortgage. Not surprising, most of the dept are mortgage dept and only a tiny fraction is consumer credit.