OECD frets about Canada’s House Price Bubble

In its economic outlook released today, the Organisation for Economic Cooperation and Development (OECD) is generally gung-ho about the Canadian economy, and practically bubbling over with new enthusiasm for the global economy. It now expects global growth to accelerate from 2.9% this year to 3.3% in 2017 and to 3.6% in 2018. Call it the “Trump effect” gone global.

But for Canada, despite its hunky-dory economy due to the “moderately expansionary policy stance in the 2016 federal budget,” the OECD has a stark warning: “House prices, housing investment and household debt are very high, posing financial stability risks.”

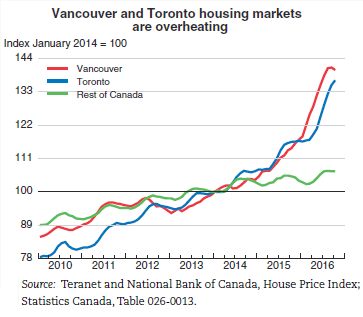

The OECD’s chart shows the house price indices for Vancouver and Toronto, which make up about one-third of the national housing market, versus the index for the rest of Canada. Note the hook at the top of the red line: a feeble sign that house prices in Vancouver might be heading south:

And there is a risk of “a disorderly housing market correction, particularly in the high-price Toronto and Vancouver markets,” the report warns. How far in the future could this be? Last month, I pointed out the divergence now appearing, with Vancouver in turmoil, and Toronto in a price spike [There’s No Plateau in a Housing Bubble, Not Even in Canada].

A “disorderly housing market correction,” as envisioned by the OECD, would reduce residential investment, which has become a key in the Canadian economy. Through the reverse “wealth effects,” private consumption would take a hit, and in the end the banks are on the line, and it “could threaten financial stability.”

[I]nterest rates have fallen to very low levels. This has added further fuel to already overheated housing markets in Vancouver and Toronto and encouraged Canadian households to take on even more debt, the repayment of which might be problematic. Both of these effects have increased financial stability vulnerabilities.

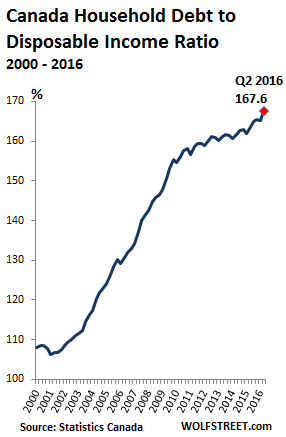

The indebtedness of Canadian households, when measured against disposable income, continues to “edge up from already high levels,” encouraged and enabled by low interest rates:

Of the OECD member states, only six have higher debt-to-disposable income ratios: Ireland, Sweden, Australia, Norway, the Netherlands, and Denmark (the last two with a ratio of over 250%). All of them have majestic government-aided and abetted housing bubbles. For American debt slaves, this measure is just over 100%, below where Canada’s was in 2000!

The “very low borrowing rates have encouraged household credit growth and underpinned rising asset prices, especially for housing,” the report says.

In terms of “financial stability,” the report takes into consideration the banks’ size as a percentage of GDP, nonbanks’ size as a percentage of GDP, housing loans as percentage of total chartered banks’ loans, and liquid assets as a proportion of short-term liabilities.

In a separate note, Peter Jarrett, Head of Division, Country Studies, OECD Economics Department, has a special word about Canada’s housing bubble, the indebtedness of households that it entails, and the risks to the system:

Local housing markets are presently highly disparate in Canada. While in most smaller localities real estate prices are fairly stable and not out of line with the fundamentals (incomes and rents), 10 of the 15 large Census Metropolitan Areas monitored by the Canada Mortgage and Housing Corporation (CMHC) show signs of overvaluation, and seven show moderate or strong evidence of overbuilding.

Emphasis added. Overbuilding leads to a glut. And gluts entail the very “disorderly” housing market correction the OECD is warning about.

[H]ouse prices in Toronto and especially Vancouver, which together make up one third of the national housing market, are such that, in tandem with high household debt (which nationally reached 167.6% of disposable income at end-2015, near the top of the OECD country range), they represent a significant financial vulnerability.A sharp fall in house prices triggered by a shock that results in a large increase in unemployment could weaken households’ ability to service their debts, resulting in a rise in mortgage defaults that could endanger financial stability.

One factor driving market strength in Vancouver and Toronto is foreign buying [emphasis added]. Unfortunately, limited data are available on such purchases, but the federal government has allocated some funding for Statistics Canada to begin to gather such data.

British Columbia has begun to address the price distortions caused by foreign buying. It imposed a transfer tax applicable to non-resident investors and other policies. And they’re hitting Vancouver’s housing market hard.

And then there’s the classic risk associated with house price bubbles: construction booms and what they do to the economy and banks when they crater:

[T]he share of residential investment in Canada’s GDP is currently the OECD’s highest…. Strong residential investment may in principle reflect robust demographic growth, but Canada’s outcome appears stronger than what can be justified by underlying population increases. And the larger the share, the further it could fall if the boom ends with a bang.

And there’s one more thing. Soaring house prices are not only a risk to the economy when they come down, and to the banks when mortgages curdle and construction loans implode, but they’re already “squeezing middle-class families in these high-priced markets.”

“Squeezing middle-class families” can’t be all that great for the economy.

One of the ironic aspects of the OECD’s handwringing about the Canadian housing market, household debt, and the banks? The report names the culprit repeatedly – low interest rates – but all the solutions it proposes for the “authorities” are focused on macro-prudential measures, of the type Canada has already implemented. But it fails to point out the solution that has been obvious for years in the face of rampant asset bubbles: higher interest rates.

Higher interest rates are now happening in the US. Read… How (Slightly) Higher Mortgage Rates Maul Housing Bubble 2, Affordability, and the Rest of the Universe

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The theory the Central Bankers don’t know:

Minsky Moments:

1929 – US (margin lending into US stocks)

1989 – Japan (real estate)

2008 – US (real estate bubble leveraged up with derivatives for global contagion)

2010 – Ireland (real estate)

2012 – Spain (real estate)

2015 – China (margin lending into Chinese stocks)

Irving Fisher looked at the debt inflated asset bubble after the 1929 crash when ideas that markets reached stable equilibriums were beyond a joke.

Fisher developed a theory of economic crises called debt-deflation, which attributed the crises to the bursting of a credit bubble.

Hyman Minsky came up with “financial instability hypothesis” in 1974 and Steve Keen carries on with this work today.

Steve Keen saw the private debt bubble inflating in 2005. He had the right theory and it wasn’t a “black swan” to him.

In 2007 Ben Bernanke could see no problems ahead and his models didn’t include money and debt. He had the wrong theory, neoclassical economics.

Canada you are going to find out, its the debt deflation sting in the tail that is the killer.

OECD: overblown economic cognitive disorder.

Canadians have convinced themselves that their housing market is unique and can never falter nor fail. We have substituted speculation for genuine economic activity/productivity but it is a game that can’t be kept up indefinitely. The government won’t act to burst the bubble until the middle class is totally priced out of the market. It’s hard to see a happy ending to our excess.

“Government won’t act”???

Are you aware of what’s going on in Vancouver? It’s a full on collapse due to government actions. Not Toronto(yet)but Vancouver house sales are down about 60% YoY and the entire industry is in a state of shock which is quickly turning to panic.

Mick, “It’s a full on collapse” you mean the sales are collapsing but not the house prices yet.

Jack, because the boards put out “Average prices” which don’t differentiate between a condo in east Van from a mansion in Shaughnessy, we have only general info, but the average price has dropped from about 1.6m in the summer to around 1.1m right now.

Anecdotal stories from realtors say that prices of houses are down around 15%, but falling. If you mean, “Has it collapsed?” That is happening in real time right now.

Thanks Mick, that’s what I was wondering :-)

I have read in several analyses (probably also on this site) that the Vancouver correction had already started before the government announced it 15% tax. Of course, one could blame insider trading for that ;-)

Wake up, it’s a bubble. All bubbles that get to big are just waiting for a pin to prick it and there is nothing one can do about that. My guess is that the Canadian politicians did this to save face ‘see, we are doing something’ at an opportune time. Probably has nothing to do with upcoming elections etc. ;-(

And BTW, -60% sales means nothing except if you are a realtor. When there was some housing bubble trouble in Netherlands in 2008, sales volume in some areas declined by 80-90% for years. Still prices hardly budged thanks to ultra-low rates and all kinds of government puts for homeowners. Sales volume is now finally up to its former record highs and prices in some areas are even higher than before the 2008 hiccup.

My understanding is that the downturn in Vancouver real estate started in June 2016. Coincidentally, a Canadian court of law issued the first ever North American Mareva Injunction (asset freeze) on behalf of a Chinese bank in June 2016.

http://vancouversun.com/news/local-news/more-and-more-chinese-cases-target-property-in-b-c-say-lawyers

Bubble up! Bubble down! It’s all about timing.

RickRod, you got that right, just like nobody believed that Trump could be elected president.

The middle class is not priced out of the market! Households who earn 250 percent the median household income of the city are priced out and they are not in any way middle class earning 180k per year, yet they are completely priced out? 2 million for a tear down that was 900 2 year ago is not a bubble at all!!!!! The politicians including that ugly rat wynn think need to be shot in the face for treason. If the prices come down by 50 percent to 1.3 that would still be a 50 percent increase from 2 years ago….this is disgusting…Id rather take my money and burn it than enrich ppl and had them over a million in a year for doing nothing….bubble will burst….guaranteed. It is sure as hell not local ppl in Canada causing this, its, ppl from overseas who pay no tax and employee 4000 kids for the same money that we have to pay one employee and then they come here and rape us on housing in our own city, obviously we cant compete with them…politicians in Canada need to be lined up and all shot in the face for treason…and data my ….if you are in the game you know what I just stated is exactly what its about plus 0 interest rates, what a micky mouse country …

The chineee money launderer owns Canada. And Canadians are too dumb to see it.

Shawn, so what else is new?

I suggest you moderate your language…you’d be less likely to stroke out that way.

Premier Wynn has nothing to do with the price of housing in Vancouver…and as for insisting on her looks: so very discreditable and embarrassing for you.

I do not understand the claim that”the solution (to low interest rates) is higher interest rates”.

Worldwide debt is staggering and the value of the assets that stand as security for that debt (mostly taxpayers net worth) are shrinking like a leaky balloon. The entire world is in a period of secularly lower interest rates, and the decline in interest rates has been occurring over a long-term time frame.

I believe that the secular time frame of the interest rate decline and the volume of debt are related, i.e., interest rates will not be able to sustain an increase until the debt overhang is addressed. The current rate rise will not be sustained until the underlying issues of debt are addressed.

But the debt overhang is constantly increasing. Therefore, the solution of simply raising interest rates does not seem to be a feasible solution.

The report blamed low interest rates for the housing bubble (including construction) and the risks it produces. So the solution to preventing or resolving a housing bubble is higher interest rates. This should have been done years ago before the bubbles got so huge.

Now there’s no easy way out. So any solution, especially a “disorderly” one, is going to be painful. The longer the bubble is allowed to inflate, the more painful the solution will be. In the end, housing bubbles are always resolved. It’s just a matter of whether it happens earlier (better) or later (worse), and in some kind of orderly manner, or “disorderly.”

… and the more painful the solution, the more politicians will fight it and kick the can down the road.

The Dutch bubble is 35 years old now when we start counting after the last crash, and 25 years old when we start counting from the first year with double-digit price increases. Politics isn’t even thinking about preventing the bubble from expanding further, they love it and every year brings new incentives to pamper homeowners (especially those with big mortgages) and punish renters in the free market even though you would think the near-zero mortgage rates and conditions in Netherlands do not require any other ‘help’.

Our last bubble had a price runup of 100% from 1975 to 1980, with strong speculation by a small group of citizens. From 1981, without any clear cause, priced crashed by -50% within 1.5 years. For many years after that home prices went nowhere while inflation was 5-10%, so the crash erased more than all the earlier bubble gains. Many speculators went bankrupt, a good lesson if you ask me.

The current bubble had a price runup of 1000-1500% from about 1990 to now despite very little income growth. Basically everyone is a speculator now and with the amount of government guarantees etc. nobody knows what will happen with this bubble bursts. It might be an even bigger mess than when the 1631 tulip bubble burst – which caused over two years of total economic chaos and the lynching of at least two high level politicians, because it proved impossible to settle the debts.

Always hard to take that punch bowl away when everyone is having such a great time!

@Wolf,

Raising interest rates in my mind puts a bullet in a whole lot of undeserving backsides. Raising interest rates will increase the value of the Canadian dollar, depress exports, and throw a lot of good, hard workers out of a job. All because of the lending habits of bankers.

In bubble markets, simply apply old-fashioned rules that say a bank must require a 20% down payment (cannot be borrowed) and monthly payments cannot be more than 25% of household take home pay.

If everyone is meeting this standard and housing prices are high, by definition you cannot have a bubble. I’m certain you have more expertise in these areas than I, so feel free to educate me where I’m wrong.

And central banks can only attempt to raise the rates banks charge each other. But in our current depression, that may be much more difficult than it appears.

Applying such rules to the Dutch housing market would probably do even more harm than raising mortgage rates from the current +/- 1% to a still ridiculously low 3% ;-)

Which doesn’t mean I’m against down payments, but what you suggest doesn’t work in practice. The Netherlands required something like 20% down when rates were 12% around 1990, as rates declined to around just a few % the required down payment went down to less than zero (we now have 103% mortgages as standard, for some time even 120% was considered normal). It works like that in most countries, apparently it makes sense to politicians and bankers ;-(

It’s very simple: artificially low rates are distorting the whole economy and causing huge bubbles. This isn’t just the bankers fault, the public was mostly complicit. Nobody forces you to take the maximum (huge) mortgage you can afford when rates are e.g. 1%, but most buyers do it anyway. Everybody is a speculator now with dollar signs in their eyes, it’s not just the evil bankers causing this bubble trouble.

If people lose their jobs because of rising rates, they probably were doing a job that can only exist in a market that is supported by artificially low rates, a job that would not have existed in a free market.

Btw, what is a bubble market? The high priests at the FED are convinced there is no housing bubble in the US (nor anywhere else, probably) and anyway, according to them you can only spot a bubble in hindsight so it is never the right time to raise requirements for homeowners (or other speculators).

To me it seems the real problem is homeless and transient people can’t vote/ don’t count.

Oh, I see what you mean…the homeless and transient people are

The movers and shakers who will get our economy moving again.

Glad you cleared that one up, dave…..your moniker is appropriate.

Cheers,

Fred

“Oh, I see what you mean…the homeless and transient people are

The movers and shakers who will get our economy moving again.”

This attitude you have is a big part of the problem.

It says, that you believe, only the big spender’s, are entitle to a voice or a vote. That is what is wrong with America. Among other places.

This is not your average housing bubble: when this goes, the economy goes with it, just like the last one in the US. So the resistance will be strong, including roadside robbery of stubborn, remaining savers.

In a true democratic fashion, it will be blamed on the previous government. In fact, it is the peak bubble of government incompetence of all stripes.

Even Milton Friedman agreed that Foreign Policy has precedence over Domestic Affairs. This bubble will burst when China is ready. When their credit binge reaches the peak needed to bend them to their knees. Is this a fair assessment Mr. Richter?

The Canadian government/Bank of Canada will not willingly raise rates. With oil prices so low Canadian exporters benefit from a weak dollar. A rate increase before any meaningful US rate rise.

“What Happens “If the Boom Ends with a Bang?” ”

That depends on whether the “Bang” moves outside the condo/Apartment/boxes of air in the sky, market.

I have experience of these staying in the singular market, and spreading from it.

If it stays in the boxes market, smaller speculators, and some of their financiers, get fried, along with some of the constructors. Whilst the regular market stabilizes for a while.

If it spreads everybody gets it. Then you loose Constructors, finance entity’s (Possibly including Bank’s) and a whole lot of little people get stung, if it coincides with a general down turn little people loose their homes.

Such an event can start a general down turn EG 08 but only if the rest of the economy is ripe for it.

Objectively the whole developed world economy, topped by china, is VERY ripe for it.

“secularly lower interest rates,”

So the Fed and other Central Banks’ monopoly on setting the price of money (interest) is “secular” Whodathunkit.

The charade postures itself as a mistake or random set of events. CB’s, the OECD, governments, financial institutions, and the like all act in a highly coordinated, highly sophisticated tandem to achieve their objectives.

What objectives you ask? The objectives laid out at meetings like Bilderberg, where even lowly canadian premiers get invited, so they can receive their marching orders.

Everything is connected, banks, governments, media, ratings agencies, watchdogs like the OECD, all part of the worldwide system.

Right down to your mayor, if you live in a reasonably sized city. He knows the plan well and is acting out his role.

Globally, the Bilderberg meetings and the World Economic Forum Annual Meeting in Davos-Klosters Switzerland are where The Powers That Be meet as you so correctly point out Mick, but don’t forget the Fed’s Jackson Hole retreat and the Aspen Institute’s Ideas Festival. These places and events are where the deals and policies are made. Bloomberg Business News covers them somewhat, and at Davos there will be a ‘question and answer’ dog and pony show to make viewers feel like they are tuned in, but that is far from the truth.

I have friends in Thunder Bay and Winnipeg, and they do not trust/respect Canadian politics/politicians, but their biggest frustration is with the decline of the Canadian Dollar. I don’t think either of these two cities has had a big housing bubble, but it is my understanding that the average citizen’s quality of life in these towns is declining.

I have to say once again, that Canada is a bit more than Vancouver and Toronto + their housing markets. Furthermore, (call it flyover Canada), those of us who do not live in Vancouver or Toronto, and don’t even wish to visit those cities, aren’t exactly staying awake worrying about their citizen’s debt levels. Those of us who bank at local credit unions and carry no debt understand that that the major Canadian banks, protected by monopoly status, really just represent their major shareholder (elites). We really don’t give a fig if they walk into problems of their own greed.

There are many Canadas. There are the areas of foundation; rich in resources such as food, water, energy, space, cleanliness, and local opportunities. Then, there are the cities of noise, long commutes, over-priced housing, and over-priced activities (Hockey tickets). City jobs and city prices. This article puts the cart before the horse in assuming the major cities support the rest of Canada’s economy. In fact, it is the other way around. The rural people have always been exploited, first by England and the HBC charter elites, then by Totonto-based corporations and those elites, and recently to the movers/shakers living in western cities. And don’t forget their pension plan holdings.

As a country we have lived beyond our means for decades. Along the way our families and values have suffered with our supposed new-found wealth (really debt in disguise). It will be good to get back to the basics. For many of us, we have always been there.

A corny verse from Waylon, but maybe it fits:

“So baby let’s sell your diamond ring

Buy some boots and faded jeans and go away

This coat and tie is choking me

In your high society you cry all day

We’ve been so busy keepin’ up with the Jones

Four car garage and we’re still building on

Maybe it’s time we got back to the basics of love”

regards

“disorderly correction of house price bubble threatens stability”

This was an announcement by the same clueless e-con-omists who always cheer on disorderly corrections on the way up, especially if it is a stampede into RE investment or financial assets like stocks.

And yes, it’s all about way too low rates and countless other incentives from the government that shift the cost and risk of buying to those who do NOT participate in the madness (often strongly encouraged by OECD, IMF etc. etc. in the initial phases). Please note that in most of the countries mentioned above that have an even bigger housing bubble than Canada, foreign investment is irrelevant; possibly it’s a factor in Ireland and Oz, but certainly not in Scandinavia and Netherlands.

What many of these extreme bubble countries have in common is a ‘socialized’ housing market and financial system where reckless speculation is rewarded and prudent financial behavior is strongly punished. The Netherlands is a tax paradise for the little people – but only on the condition that you buy a way overpriced home to start with, so you end up an eternal debt slave. If you don’t like that housing tax paradise you can rent and be taxed through the nose by outrageous rents in the free market.

On the way down all hell will break lose as the sheeple think they only signed up for the good part of the housing bubble, years of living way beyond your means. And with homeowners a majority in most of these countries, politicians will do everything to pamper them until it is way too late.

BTW regarding raising rates: the Netherlands has been talking about ending its ridiculous mortgage tax deduction since the last housing crash in 1981 (this tax incentive was considered one of the main drivers of RE speculation). Only some cosmetic changes have happened since then, because it was never a good time for politicians to take away the goodies for homeowners – just like it is never a good time to raise rates and always a good time to buy a new/extra home. Politicians and bankers will run the ship into the ground, changing course is no longer an option.

In Toronto they are building lots of condos, however, there is no available land to build “houses”.

Toronto and Hongcouver are being flooded with Chinese. I live in a million$ plus neighbourhood, and I have now have over 60% Chinese neighbours! 4 years ago there was only 1 Chinese couple who were Canadian born!

In the last 5 years, Condo prices in Toronto have really gone nowhere while housing has soared.

Of course, if interest rates spike like the whack job Greenspan pulled you can look for a deep reset, however, I think Central Bankers are aware of the new mountains of debt tied to low rates!

Just saying!

@Greg. Consider what happens to Toronto’s financial industry when banks, insurance companies, and large private lenders start taking multi-billion dollar losses due to this bubble collapsing.

And of course, banks are already taking hits on Alberta, which is in a depression.

big hits to finance companies is good; most of these produce absolutely nothing of value, on the contrary it;s only paper shuffling to benefit the elites. In many countries in the West (US, UK, Netherlands come to mind) the financial industry has grown to several times the percentage of GDP it represented 25 years ago, which is ridiculous.

The financial sector needs to shrink down, just like government itself. Too bad for all the people who are now doing this useless work …

Damn straight! Bankers really do not produce anything that is tangible. Farmers grow food. Assembly line technicians make make autos, combines, tractors etc.

The transformation of the US’s economy starting from around 1980, think Ronnie Reagan, to where it is today is not sustainable in the long run. The UK is under this also. The City of London is the engine of the UK’s economy with London accounting for almost one fourth the nation’s GDP.

Homes are shelter and should not be employed for speculation. If government wished to end shelter inflation tomorrow they would put into place regulation no one could own a property they do not live in full time.

That would put a big dent in the bubble.

that’s a big “If” …

Most governments LOVE inflation in necessities, especially if the elites can make good money from it. In most Western countries until recently a huge chunk of the multi-millionaires and billionaires made their fortune through RE speculation; lately other types of financial speculation are becoming more important but the huge debt buildup in the housing markets is always a major factor.

Once you own your house and are out of debt completely, you find that you don’t require a big income and hanging on to your current job isn’t the be all end all of life. You can tell your boss to go f himself and take that fun little job by the beach that doesn’t pay that well.

No, it is in the government’s interest to keep you deeply in debt. It is the basis of social relations.

Kent

One of the secrets to happiness…get out of the system. We’re all controlled by debt and taught Keynesian economics at school. We’re programmed to get a job, take on debt, to finance the “dream”.

When these asset bubbles burst around the world, I fear we might not see the population so well controlled!

Better still if you have your own source of clean food and water. To be honest, those are the two that concerns me the most.

The only positive is in the footnote: our reports have a track record of a one year weather forecast.

I’ll be really surprised if it ends with a bang. Without any irony intended, this time around, I think the Canadians will engage in Chinese style intervention i.e.:

1. Tighten.

2. Loosen when a crash looks imminent.

Repeat as necessary. It sure as hell has worked in China, why can’t it work in Canada?

Those looking for a crash anywhere will be disappointed.

it worked in China, do you mean the housing (speculation) bubble in China is done? IMHO they only postponed the inevitable while the problem keeps growing. Netherlands same story, the measures to prop up the bubble get more desperate every year and at some time they run out of options and/or money.

Canada is NOT different. My own country has had many housing bubbles over the centuries and I assure you they always pop; in some cases the downturn took 10-50 years, so maybe it will be only possible to spot in hindsight. The only difference is that this time the global housing bubble is so epic that when it pops it could take the whole economy with it.

I should point out one of the reasons my home town of Vancouver is called a “no fun city” is because everyone stays home, afraid of spending money on a dinner or entertainment. The pub and retail industries in turn have to pay enormously inflated rents and leases to their landlords. Our governments have favoured the exclusive West Side of the city with public works and parks. All classes of people are struggling in this desirable but expensive environment.

I guess the elite class isn’t struggling, otherwise why would these people with unlimited funds keep flocking to VA?

Market has already turned down in the US, over a year ago in some areas. Once even the dumbest of the dumb realize appreciation is not just dead, but depreciation is probable that will kill demand that was responsible for probably 30% of the transactions that were primary driver of the insanity of the last 3-4 years (aside from Chinese money printing).

If the govt wanted to really put a stake in the heart of this without raising rates which could affect marginal businesses, they could eliminate the mortgage interest deduction for properties other than your primary residence. Restricting foreign ownership of housing – turn out the lights, the partys over. RE would go down 50% +/- in the US. Best way to make this country more competitive. Pull the trigger Mr. Trump, you magnificent bastard.

I don’t believe the debt/real estate king is your guy for doing away with the mortgage interest deduction in any way, shape or form.

maybe, but for the RE kings themselves the mortgage interest deduction is probably irrelevant.

I don’t know the details of the US system, but in my country mortgage interest deduction only works well for incomes of maybe 2x – 5x median wage (typically the upper 10% or so of society, but not the 0.1%) and doesn’t apply for investment properties.

In fact, one of the reasons of the dysfunctional rental market in the Netherlands is that officially there is no mortgage tax deduction for investment properties, which means landlords have at least 2x higher costs than homeowners = sky-high rents.

You know things aren’t well when even the hard core bulls are calling for a correction in Vancouver…and even more unsettling is that for the last few years all anyone ever talked about was real estate and how much their houses have gone up…. lately not a peep at the office water cooler or Xmas party last weekend. Me thinks everyone on fence lookn to sell will be doing so after XMAS… early spring exodus is 6 weeks away get the popcorn ready.

Homer, I’ve got my double-buttered Orville’s ready for the feature presentation–everybody selling at the same time, LoL.

Looks Locke Canada is about to experience the disjuncture that we in the South went thru 8 years ago. Somehow they avoided the world recession because their housing market was sane, and not fed with criminal securitization.

What’s the state of securitization and it’s evil twin, credit default swaps in Canada, Wolf?

Bill, we “avoided the world recession ” because the Chinese money launderers have kept a low profile until recently. Apparently, that’s changing finally.

“In the end, housing bubbles are always resolved.”

Looking at that shocking household debt to disposable income chart for Canada I wondered exactly where and when prior to the year 2000 there existed housing bubbles that grew with such ferocity and were then later popped.

Looks like according to the below link (Its Business Insider so I’d be skeptical of anything on that site), it was every 18 years for the first 144 yrs of the USA’s history.

Correlation with past bubbles seems dicey. This seems to be a unique time in history. The last US bubble was resolved by blowing a new one. And outside this site, and a few others, no one dares mention it. Just as Trump was ignored by the main stream media, so is the current bubble, which is described as an ‘affordabiliy problem’ or the result of ‘Inequality’, rather than insane lending practices (and yes Virgina, you can get a loan for your 20% mortgage down-payment!)

http://www.businessinsider.com/the-economic-crash-repeated-every-generation-1800-2012-1

people have no idea …

the Dutch housing bubble is MUCH bigger, is has been growing since around 1990 and current prices are 1000-1500% higher than 25 years ago although the statistics of the realtors will claim an average increase of only 600-700% (because the type of homes on the market has changed hugely over the last 25 years). The measures to prop up the bubble are also far more desperate then they are in Canada, they probably were already more desperate in 2000 …

The Netherlands has had many housing bubbles and busts over the years. To get an idea about what is ‘normal’ look at the chart on this image, which is the ratio of house price to income for the Herengracht in Amsterdam:

http://www.huizenmarkt-zeepbel.nl/images/huizenprijzen_300jaar.jpg

This is a location where the homes are ‘constant’: they were always the same, well kept merchant homes for the higher middle and upper class. Not always representative of lower class homes, but it gives I good impression of what is going on. The current prices are easily the highest relative to income in 400 years; incidentally Dutch rates are also the lowest in 400 years.

The chart clearly shows: housing bubbles are always resolved – however, it may take a long time.

Correct me if I am wrong, but I seem to recall Amsterdam suffered one of the first housing bursts in recorded history around 1660 which, among other things, forced Rembrandt to declare personal bankruptcy shortly before his death, albeit these days this event is considered to be partly caused by the housing burst itself and partly by Rembrandt’s legendary ill-advised investments. I think in your chart it’s the massive dip to the left just before the first highlighted crash, which I take was somehow linked with the Dutch War of Louis XIV (1672-8).

Don’t know the specifics about Rembrandt but 1672 is official ‘Disaster Year’ in Dutch history.

In the chart of the Herengracht Index you can see a bust around 1675. Keep in mind that the chart is a ratio, the real home prices fluctuated far more than the +/- 5x shown in the charts, because in bad times incomes often decline strongly. This is indeed tied to the war with the English in 1672-1674 (the Dutch were engaged in many wars around that time, similar to how the US Empire is now struggling to remain in power).

But this crash was soon forgotten, it was off to the races for an ‘all time high’ in 1736 that was only surpassed around 2000. My own city had a severe housing bubble around that time because it was one of the two headquarters of the Dutch VOC, the first multinational company (much bigger than even current Apple, if you correct for inflation). Many middle class citizens speculated in VOC shares to build mansions outside the city, with the value of their shares as a downpayment. Of course if the middle classes start participating the end is near, and this time was no different. The city has never fully recovered but that doesn’t mean the elites won’t try to pump up an even bigger housing bubble ;-)

Sweden is probably a basket case. The Swedes do not pay of their housing loans, only the interest. Housing, cars, boats, most Swedes buy these with borrowed money and they usually do not pay off these loans. Keep that in mind when regarding hoe Sweden works. TPB did enforce mandatory paying off of loans, but this applies only to new loans taken after this decision was enforced and this hasn’t cooled down the Swedish bubble economy. At the same time police, health care, care of the elderly, education, you name it are coming apart at the seams in Sweden. Their defence forces are according to their C-in-C able to defend a single location for at most a week, police is retreating from large parts of the country etc. Something for Wolf to look into !

same for Netherlands …

After the 2008 financial crisis there were some minor changes to the ridiculous system of homeowner subsidies, guarantees and incentives. Homeowners will be ‘gradually’ (glacially would be a better word) adapting to paying off the mortgage, 50 years from now the mortgage tax deduction will be slightly limited compared to now. Don’t rock the boat! This change in tax regime is costing the average homeowner about 1 euro per month and they are already crying foul … And just like in Sweden this only applies for new mortgages, the many existing ones keep profiting to the max.

With current ultralow rates (around 1%) one would think that the mortgage tax deduction is no longer relevant and people will hurry to pay off their mortgage, but mortgage debt keeps growing anyway. Of course, many have used all the price increases to keep living the good life and they have no way to pay off the mortgage – they fully depend on ever rising homeprices.

I think the social problems are very similar too. Netherlands is swamped by economic migrants from all over the world who come here for a free life-long vacation, and get priority treatment from the government while the elderly and many others have to live in dire conditions and are crushed by sky-high taxes. I think in many ways the living conditions in Netherlands have deteriorated compared to 1990 when the current bubble got started. But we have an epic housing bubble to show for it ;-)

Realist, just wondering, do you or have you lived there (Sweden)?

The answer is yes, I have lived there and still have relatives there.

Canada should invite Hilary to come straighten the mess out for them, along with a few GS guys they’ll kick this can clear into the next parallel universe.