Vancouver in turmoil, Toronto spikes.

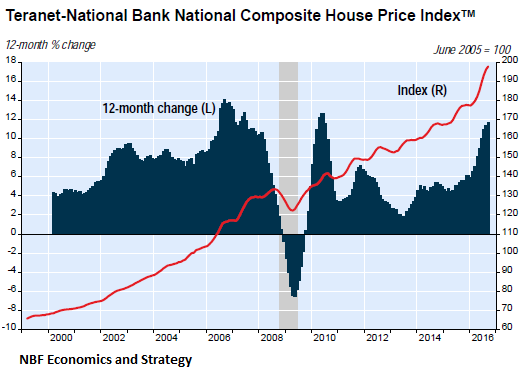

Canadian house prices jumped 11.7% in September from a year ago, according to The Teranet–National Bank National Composite House Price Index released today. But the index papers beautifully over the dynamics in each metro.

In six of the 11 metro markets of the index, prices have been languishing or even declining over the past couple of years, as they’ve hit the wall of reality after often stupendous price gains in the prior decade: Montreal, Calgary, Edmonton, Quebec City, Halifax, and Ottawa-Gatineau.

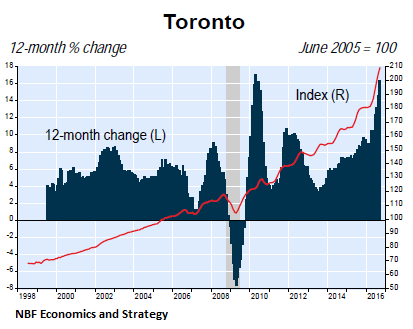

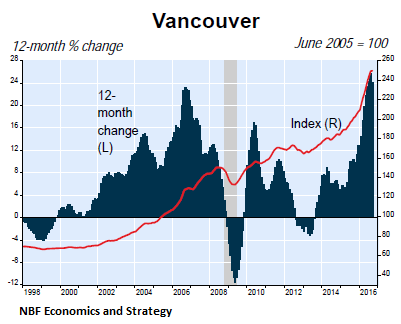

In the two largest markets – Toronto and Vancouver, which combined account for 54% of the index – prices have blown through the roof. Both markets are among the hottest, most over-priced housing bubbles in the world. UBS recently ranked Vancouver Number 1 globally on that honor roll.

But suddenly the dynamics have changed.

Vancouver’s housing market is in turmoil, to use a mild word, as sales have crashed, after the implementation of a real-estate transfer tax this summer by British Columbia, aimed squarely at non-resident investors. In Vancouver, those investors are mostly Chinese. And where do these folks now go to inflate prices? Toronto.

Still, the national house price index (red line, right scale), after the 11.7% jump over the past 12 months (blue columns, left scale), has doubled since 2005!

The index, similar to the Case-Shiller Home Price index in the US, is based on repeat sales. It looks at properties that sold at least twice over the years to establish “sales pairs.” It then uses a proprietary formula to deduct price changes from these transactions and extrapolate them into an index for each of the 11 markets and nationally. It’s not perfect, but it offers an alternative view to median prices or Canada’s “benchmark” prices.

Prices in Toronto have been spiking (red line, right scale), with double-digit year-over-year percentage gains (blue columns, left scale) so far this year, including a breath-taking 16% in September.

Vancouver makes Toronto look practically tame. Vancouver went completely crazy, with year-year-over price gains reaching 26% in the summer. Now a new reality went into effect. Market activity has collapsed, as no one knows what anything is worth, with buyers and sellers jockeying for position. And on a monthly basis, the index was essentially flat (+0.2%):

Most Canadians have not seen their incomes rise anywhere near the rate of the house price inflation of the past many years, if their incomes rose at all. Thus, many of them have been priced out of the housing market, or have access to it only via highly risky financing schemes that put both lenders and borrowers at risk, despite historically low interest rates.

Once enough people are priced out of the housing market, demand collapses. This would normally be where housing bubbles deflate in a very painful manner for lenders, homeowners, and everyone getting their cut, including governments and the real estate industry. But there has been a strong influx of mostly Chinese investors that need to get their money, however they obtained it, out of harm’s way at home, and they pile into the market, and they don’t care what a property costs as long as they think they can sell it for more later.

But British Columbia threw a monkey wrench in to the calculus this summer when it adopted a 15% real estate transfer tax and other measures aimed squarely at non-resident investors. It hit home, so to speak.

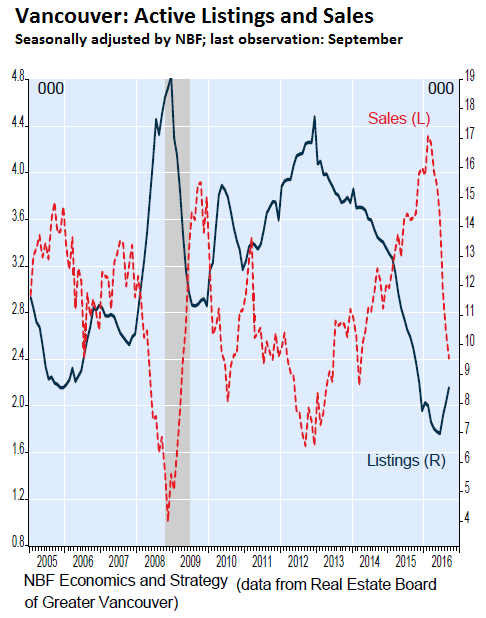

Total sales in Vancouver plunged 32.5% in September from a year ago, with sales of detached homes falling off a cliff – down 47% [read… Vancouver Housing Bubble Bursts, Hot Money Flees to Toronto].

Home sales have fallen every month since their all-time crazy peak in February on a seasonally adjusted basis, for a cumulative decline of 44%, according to Marc Pinsonneault, Senior Economist at Economics and Strategy at the National Bank of Canada.

But home prices have not yet fallen, he wrote in the note, “because market conditions have just started to loosen from the tightest conditions on records. We see home price deflation starting soon (10% expected over twelve months).”

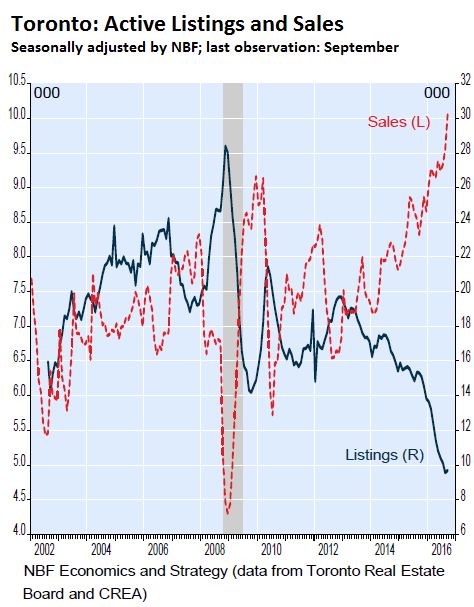

His chart shows the plunge in sales (red line, left scale, in thousands of units) even as active listings have started to rise (blue line, right scale):

In Toronto, the opposite is happening, with sales spiking on a seasonally adjusted basis way past prior record levels, even as new listings have plunged.

For now, “Toronto is now the red hot market,” explains Pinsonneault:

Home sales broke records in each of the last three months. But the historically low supply (in terms of the number of homes listed for sale) is also contributing to market conditions that are the tightest on records.

But the situation can turn on a dime, as Vancouver demonstrated. When a bubble pops, the first thing that stops is transactions. This happens suddenly. Sellers refuse to cut their prices, while buyers refuse to step up to the plate. Things grind to a halt. Once sellers are forced to relent on price, transactions start rolling again, at lower prices, and each lower price, due to the metrics of comparable sales, pressures down future prices of other transactions.

Once Chinese investors figure out that they’re likely to lose a ton of money in Canadian real estate, because their compatriots who’ve piled into the market before them have already lost a ton of money, they’re going to lose their appetite. This is the hot money. It evaporates suddenly and without a trace. As Vancouver shows, bubbles don’t end in a plateau.

Even the Bank for International Settlement and the OECD have warned about the Canadian housing bubble, and what it can do to the financial system when it deflates. Read… Canadian Housing Bubble, Debt Stir Financial Crisis Fears

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

You worry too much. When the bubbles burst the losses will simply be socialized in true capitalist fashion. Not a problem.

Now, timing the collapse profitably could be a problem, especially if you can’t socialize the losses, but you shouldn’t be doing that anyway.

How does one profit from a RE collapse in Canada?

Canadian banks dont keep the mortgages in their books, they sell them to CHMC (the canadian equivalent of our fannie mae).

Maybe short the canadian dollar? Even that might not work as historically CAD is correlated to price of oil so I dont see how you can make money there.

They don’t sell them to CHMC- the latter insures them for a fee that is paid by the buyer. I once flipped a house in four months and I had paid a 2 % insurance fee- CMHC did ok on that one!

The prob with Vancouver- or TO Chinese buying is it’s all cash or enough cash that CMHC is not required ( Bank Act only allows bank to make 75 % loan without insurance)

Americans have been getting their heads handed to them shorting the C banks for years. Understand–it’s a cartel. There are only five of any size: Scotia, Royal, CIBC, Montreal, Toronto Dominion.

Sorry Western Bank but it is what it is.

They are immensely profitable.

Up until 2008, the Royal, with dividends re-invested had returned 17

percent per year for ten years!

A typical C bank ATM will charge you 1.50 to print a ‘mini- statement’ the action in an account for a week or so.

The profit % here exceeds that of a drug deal- the f&cking machine isn’t spitting out anything but a .01 cent worth of paper!

Re: shorting C$ – I like this more. If the kid is a chip off the block we are looking at big probs with govt spending,

Plus only only 3 of ten provinces are in reasonable shape.

If the Feds were to announce that they’re not responsible for provincial debt ( they’re not) the SHTF for Ontario, to name one.

The biggest myth is that all the Chinese Buyers who buy to flip are rich and buy cash. I have been in the Vancouver industry and was in it since 2006 and know many Chinese mortgage brokers. All told me their clients have specifically asked them to not tell anyone in the Chinese community that they take out high ltv mortgages to “KEEP FACE.” Only a small handful are rich the rest have some money and are trying to get rich in by flipping and inflation prices. THANK GOD the tax was implemented. THANK YOU LORD. AND CONTRARY TO THE PURE IES AND HORSE MANURE YOU ARE FED. The price inflation and bubble has been 100% and purley caused by Chinese Foreign Money. PERIOD. END OF STORY. The same thing will happen in Toronto. These two cities have median incomes that are some of the lowest in the country. In Halifax the median income is higher than both and you can buy a beautiful large home in a AAA neighbourhood for under 1 million. The only reason is because there is no Chinese there. This is not racist. THIS IS A FACT! The Chinese do not buy to hold they buy to flip and double their down payment in 3 to 6 months or less and inflate prices for families wanting to work and live in the city. IT IS DISGUSTING. It would be ok if it was a few trying to do it but that is not the case, they all do it and they inflate the entire market to where a 200k house hold income earner or top 5% can’t afford to buy a home and raise a family. THIS IS CRIMINAL.

“How does one profit from a RE collapse in Canada?”

By getting out at the top of the market, and before the collapse. Easier said than done, judging from the numerous smart people who get stuck with the collapse because they can’t get out.

“I dont see how you can make money there.”

Swaps and hedges and options and derivatives and fine print, a crafty game not for the uninitiated, dedication demanded. Honestly, have a drink and talk yourself out of it.

The mortgages are bundled into Mortgage Backed Securities and sold to investors. The MBS are what are insured by CMHC.

I think Vancouver real estate hasnt had the last word yet. I wont be surprised to see the prices still going up this spring. Vancouver is seen as a safe heaven by rich chinese and it is a very small place considering the amount of chinese millionaires willing to go there. If chinese economy collapses , more rich people would want to escape and go there, if it prospers , still more people will have money, it is hard to see how the prices will come down. Also, there is a huge underground marijuana economy in vancouver that recycles all the cash into real estate.

Nevertheless, those charts are absolutely telling, at some point reversion to the mean is bound to happen.

I don’t think pot can levitate the market no matter how big it may be. The rich Chinese are probably going to get poorer not richer. T

he 15% tax makes it almost impossible to preserve capital due to the rest of the transaction costs. I will surely remember your comment if you are right however.

Agree with most of yr stuff except for marijuana.

There are tractors driving through pot fields in Washington State.

The US market for BC bud is long gone.

The challenge now is to hang on to the domestic market.

Unless the Can Govt stops fretting- the US is going to get even for all the money we made in Prohibition 1.0

BTW: I speak from Nanaimo, a well- known hub of production, brokering, etc.

Not sure what your local market is like. Down south, the green stuff has been off its highs (no pun intended) by about 30% since 2008.

Screw ’em, displaced Canadians can live in the woods and eat berries like bears do.

Vancouver is Done! Mark my words. The Chinese game is over. And Canadians can go back to forming families and buying homes and living their lives in peace. The Chinese completely used Vancouver Housing like penny stocks and Casino slots. Sorry But you and I in Canada can not afford to do it, because we have to actually pay tax on our income and also if we own businesses we have to pay our employees 10 dollars minimum an hour instead of 2 dollars a day. In China the same employee that we pay $80 per day for an 8 hour shift, buys a business owner, 40 employees! They then take their profits, to Vancouver buy real estate and flip it and inflate the prices. RAPING CANADIANS….The politicians who stood by this long and let it happen need to be hung for TREASON!

Don’t worry. Government has a couple of plans to keep Canada’s housing bubble inflated and plenty of slave labor available to keep taxi companies, restaurateurs, roofing companies, etc. very happy.

First we have the immigrant program:

http://news.nationalpost.com/news/canada/chris-alexander-announces-tory-leadership-bid-wants-canada-to-boost-immigration-to-400000-a-year

Then we have the so called “temporary” foreign worker program:

http://www.nationalobserver.com/2016/03/10/news/migrant-workers-call-trudeau-reform-temporary-foreign-worker-program

Why does “capitalism” need such things?

‘Why does “capitalism” need such things?’

Heavens, man, where’s your sense of ruthless exploitation?

There are literally millions of people out there who are desperately seeking ways to enrich the wealthy in return for mere subsistence. so Just get yourself some lobes and have at it, and ignore their pathetic pleas for bathroom breaks and on-time pay checks.

You’ll be glad you did.

Yes Walter, there are millions desperately seeking ways to enrich the wealthy. The problem is THIS wave of dreamers are illiterate even in their own language and they are truly unskilled. Unless the wealthy need moats dug around their estates, they aren’t good for much except taking the government dole and buying subsistence commodities. They can’t run a paint sprayer, a pressure washer, a nail gun and they have no idea what building codes are. I have currently employed two females as house cleaners. They do that quite well.

It has nothing to do with Capitalism. Far more hideous.

Things will be interesting, that’s for sure. As a renter and one day first time buyer I’m definitely watching closely.

Vancouver rent is still high, the Chinese were buying Canadian re as the loonie was falling and the won rising.

Even if re sales drop, the mortgage rates are still low and easy enough to get for first time buyers to jump in.

I also completely disagree that it will be a rush to the exits if Chinese buyers start to see 40% price drops in value.

That’s cause most of these guys paid with cash, have a higher net worth and hedged with other investments.

Though I would love to see interest rates skyrocket in Canada and see housing prices collapse 50-80% – I won’t hold my breath!

If the market crashed you still wouldn’t buy. Who wants to buy in a crashing market? That’s why the prices stay low, people won’t take advantage of the fabulous deals out there for a whole BUNCH of reasons.

THAT IS THE BIGGEST LIE. Most Chinese did not pay CASH. Pure bull..I have been in the industry in Vancouver since 2007 and worked with tons of Chinese mortgage brokers. They all told me all Chinese buy with mortgages and they all tell them to not tell other Chinese to save face! Pure bull. There is a huge myth that all the Chinese are rich, only a small percent of the buyers are rich the rest where following other Chinese and buying and flipping and inflating prices to get rich. PERIOD

I think for Wolfstreet to present a clearer picture, would be to have data on property loans versus outright purchase with cash, for the transactions in each city.

Now, property crashes in any country is always predicated on the fact of over-leveraging, leading to unsustainable price increases which eventually leads to a correction as the borrowers default.

Go travel to many booming Asian economies, such as in Hong Kong, Singapore, South Korea, Sydney etc.) and you will notice that many wealthy Chinese are buying up properties globally with ALL cash down (as opposed to No-cash down in the US during the years before her sub-prime crisis).

I’m not questioning where the wealthy Chinese get their money or if they are actually laundering money. The fact is, if they purchase with all cash down and no loans, then that IS the actual market price of said property since there is no leverage involved.

These wealthy Chinese (or Indians or Russians, or globalist for that matter), who buy with ALL cash down has very long-term holding power, regardless of how the prices fluctuate. They are actually the backstop in the event of a crash because they are not pressured to take any loss at any point in time. (maintenance notwithstanding, and property taxes and other maintenance costs are low relative to purchase price).

It is leverage that is the killer, NOT high prices by itself.

Even if the local incomes cannot rise fast enough to support buyer demand for further property price rises, an All Cash buyer is not affected. They just collect rental and wait for future inflation to set in. In a market where buyers are priced out, rentals inevitably escalate, as evidenced in San Fran and many other “gentrified” cities.

And even if there is no one who can afford to rent the property, the All cash down owner is not under any pressure to sell out. They can simply wait or lower it just enough to attract renters. For property as a tangible asset, there is always a threshold above zero dollars where a low enough rental will attract a long queue.

In comparison, if you own shares in a major listed company and say you want to “rent” or “loan” out these shares to a counterparty, very often, they do not even want to accept the risk no matter how low you offer. Not so, in property rentals.

Just as in equities, if you purchase shares of ABC company without any leverage, even in an unfortunate crash, you can afford to hold it without any further loss or losing more than what you already put in. The real danger is when you borrow stock to speculate and the margin calls comes knocking on your doors.

In addition, unlike shares, property prices rarely drop to zero (even in a catastrophic loss scenario such a natural disaster, you still may have insurance recovery; again unlike equities where no insurance will be willing to cover your investments). The Chinese (and many others) knows this and thus have formed a historical love affair with real estate.

Thus, if the percentage of borrowings per property transaction is low, then the chances for a property crash will be low, but if the data shows a high percentage of borrowings, then its almost certain the correction will be soon.

When a property market crashes, it can stay depressed for years. Some may not mind taking the hit, but many will be forced to sell to free up the cash for other uses.

I think there is a wrong assumption that many Chinese buy their properties by all cash. Base on the recent report on the recent luxury home sales in Vancouver, it is not true at all. While the house price rise up more than 30% within the last 10 month in Vancouver, don’t you think people with money are that stupid not to leverage their investment as much as possible in order to get the biggest gain? You think Chinese will not take the low interest rate advantage to leverage as much for quick money?

The full cash myth is created by those real estate agents. Or for those Chinese who has no choice but only can pay cash to buy a house. But it is properly a old story, these days they can easily to borrow money in Canada (even easier than locals). No one will full pay a house anymore. It is human nature, everyone is greedy and want to earn more.

I think he was asking for clarification as to sales volume – all cash vs leveraged purchases – and laid out his/her thesis as to how both will behave in a crash.

I like the comment a lot actually.

I would also note, on the all cash side of the argument, having been to SE Asia, Vancouver has to look like freaking heaven compared to urban cities there. I live in SE Alaska – not far from Vancouver – and if you have ever been in urban areas close to or in China – the clean air, drinkable tap water, lack of trash piled everywhere, wild life, trees, mountains, and just natural beauty of the Pacific Northwest has to grab one by the shirt collar.

To be clear, if you grew up in a gritty, industrial Chinese town/city, your family made its money (however), and you had a chance to write a check for a property in what appears like a utopian garden – wouldn’t you? Stuff some cash in a safe deposit box or make other arrangements in CA – and if s**t ever hit the fan, just walk away.

If the CN buyers are leveraging, its a dream – if the CN buyers are all cash, it’s a back up/escape plan.

Which brings us back to all cash vs leveraged purchases, which could make this side debate much more entertaining.

Regards,

Cooter

IT might be more interesting than that.

Back in the late 1920-1930’s Germany realized it was land short for a booming population. They started wars for “Lebensraum”, which is “Living-Room” or “Living-Space”.

They used warfare since they were good at it, and to their East were weak nations like Poland.

The Chinese need Lebensraum. They know it. We don’t. Rather than take out Canada in one week of war, and upset the UN, it is better to take paper currency and BUY up Canada. Then, to lower the population stress of China, start sending their 40 million un-married single men to Canada and populate, control, and take over Canada.

It is a very simple plan and there is much data to back this up.

Things actually get more interesting than this. I do believe some of Chinese may enjoy the life in Vancouver, but most of them properly can only enjoy that kind of life in a short amount of time.

The opportunities and the separation with the family is there key. While those Chinese can earn a lot of money from Chinese will probably it will not be the case in Vancouver. Even with the better living quality, those Chinese properly cannot enjoy their life such a small city very much. The same situation happen when HK and Taiwan immigrants move to Vancouver around 20 years ago, and many of them back to Asia after their kids finished the university in Canada. Whether the mainlan Chinese wil sold their properties and back to Asia after they realize it is not their lifestyle in Canada is still unknown, but at least we know that it is what HK and Taiwanese did in the past. However, no one would like to leave their money in a place of there is no or little growth, and Chinese especially concern about that. But one thing is true is that if you go to those Chinese online forum in Canada , it is not difficult to find out that many Chinese complaint about hoe boring their life in Canada or how much less money they can earn compare they did in China. At last, living in Canada is not for everyone

looks like home prices and mortgage debt have been growing in tandem according to this chart, it is a debt fueled bubble after all..

https://www.google.com/search?q=vancouver+mortgage+debt+vs+home+prices&espv=2&biw=1093&bih=504&source=lnms&tbm=isch&sa=X&ved=0ahUKEwj74bSoztrPAhUIjVQKHXvXDIMQ_AUIBygC&dpr=1.25#imgrc=SKyzfZ9CBNdhRM%3A

Let me get this straight. From this website

http://vancouver.ca/home-property-development/residential.aspx

The property tax rate for residential on every 1000 dollars is 3.16567 for 2016. That is only $3165 for the entire year on a million dollar house? Correct me if I’m wrong. If correct, that is nothing by CA standards, no wonder there is a property bubble in Vancouver.

So for foreigners anothrr is 15% tagged on or 150k in a million dollar house? Is that a one time payment or is that every year? Please clarify. That seems like a huge amount, which would explain why the Chinese are all running to TO

Yes, that 15% transfer tax is on the sales price of the house. So C$150,000 on a C$1 million house.

There’s another vacant apartment tax coming. For non-resident investors, this can get punitive.

THANK EFFIN GOD!

i so live in the wrong canadian city.

Residential, new home construction, is Canada’s TBTF. If the building stops, then everything stops.

Hell, make it a 100% tax. Or just ban foreign purchases outright! It’s not like it’s particularly difficult to get Canadian citizenship- we literally used to sell citizenship to Chinese “investors”! The foreign owners are so shiftless they can’t be bothered to establish residency?

It would be really nice if our policy on this wasn’t built on propping up a bunch of upper middle class professionals who took out multi-million dollar mortgages on worthless glass-faced concrete cubbies, stick frame homes, and dubious renos of 80s garbage. Sure, I get that RE and construction are a huge part of the economy- but at some point it’ll have to retreat to viable proportions if we’re not to suffer from a total dislocation in the market.

The problem is everyone is in this chin-deep, and everyone is in it for themselves.

There is no meaning to tribal loyalties in a global economy with open borders and fluid capital movements.

If you had been owning a West Vancouver apartment and a wealthy foreigner came by to offer you an extra loonie million over your last offer, would you sell out?

I’ll bet you’ll take the money, kiss the foreigner and boast about your gains here, instead of railing against “foreigners”, whoever they may be.

This game has been ongoing for centuries, and blaming the “foreigners” is the convenient thing to do, except we forget Canada itself used to belong to the Native Indians, and the early colonizers (aka foreigners) basically swindled, robbed or did a land grab from those who were here first.

I’ll be honest with you, I’ll take the money once its big enough. That’s the smart thing to do, if the buyers are taking up huge loans to purchase. When the prices tanks, you can always come back around to it, there is plenty of land in Canada. If the ice melts from Greenland, we can do another land grab from the Dutch foreigners who lives in EU and is not really part of this land.

But I think we definitely should take more advantage from the foregin investment. The key is we want to tax then enough but still make their investment attractive while the locals can get more benefit. At the same time, we should minimize the downside of how these kinds of investment affect the locals. The problem right now is that only small group of people get benefit from such investment while most people suffered the unaffordable house price. Then the foreigners use our policy loophole to take the most benefit. Please understand that the last 12 months price increase is not the same of what happen in the last 10 years of you look at the graph, it is a exponential graph and properly mainly drive by speculation.

In fact, we should find some lands in BC which just allow the foreigners to invest and build anything they want, while we heavily tax them. We can even build a new city for them if they have money, and we guarantee their investment will be safe and they can feel free to flipped to another foreginer. As local, we provide services for this foreginer city and charge tax on them. By doing that, we can make sure locals can take the most benefit from the foreginers while didn’t affect the locals living as well as providing the safe heaven what the foreigners want. We have a lot of land to build these kind of city in BC anyways, what not.

To you and the fellow below- I am not ignorant of our history nor of my own status as grand-grand-grand-grand child of immigrants. I have no problem with immigration per se. This is NOT immigration. Foreign purchasing of residential property for speculative purposes is NOT immigration!! That’s why they’re called “foreign buyers” folks.

And no, I won’t take laundered money from mainlanders. I’ve spent enough time in China to know where it comes from. It doesn’t matter how much- some people still believe that they’re going to be held to account for what they do in this life.

Bravo. Someone with integrity.

“And no, I won’t take laundered money from mainlanders. I’ve spent enough time in China to know where it comes from. It doesn’t matter how much- some people still believe that they’re going to be held to account for what they do in this life.”

i know, Colorado Kid, i got choked up when i first read this earlier, too. i’ve read it half a dozen times already.

No the game has not been going on for centuries. Get real. All cashing buying by the Chinese is a very recent thing

Canada only works with healthy immigration rates. We let in over 250,000 per year. Those new citizens need houses infrastructure, and jobs. Without that, Canada would be a barren wasteland /wilderness like Siberia.

Isn’t Siberia considered an systemically important wildlife habitat?

Too bad the foreign purchasers aren’t actually immigrating and establishing residency, much less becoming citizens, as explicitly stated. These non-sequiturs can be avoided by reading the post you’re responding to.

There’s no plateau in any human narrative based on exponential promises of more, when you zoom out far enough. Examples abound, since the first detectable housing bubbles, in Egypt (pyramids, large cities) Some (David Graeber) argue that money evolved from the early concept of credit (promises) and then acquired other functions. I argue based on reality, that money (tokenization of promises) was never more than that, it always remained a promise of more, and all talk of store of value and medium of exchange is the narrative (bubble) talking.

Housing in Canada only requires relatively recent data to be spotted as a bubble, which makes this kind of scary, seeing the decline is always faster than the rise.

I’m going to quibble …

Money was almost exclusively “asset” money for the longest time, be it sea shells or gold. It wasn’t a “promise” and it served the function of solving “coincidence of wants” in trade.

A group of productive humans with a working money system will always outproduce a group of humans who barter – just how it is – so we need a working money system.

Credit, which you dub “promises” was actually innovated by the Chinese around 1000 AD give or take (would have to check my bookshelf) where they used paper claims on strings of metal coins. While loans had existed forever, they were always made and paid (plus interest) in the currency of borrow – which as I pointed out was typically an asset, such as gold.

Paper credit is different because the issuer has the ability to expand the money supply at will – and naturally this went on for some time and then collapsed due to over issue of paper vs metal stock.

I would also note credit is extremely important in a functioning economy and we would all be vastly poorer without it – but humans are humans so we can’t help but screw it up every now and again.

Regards,

Cooter

“Credit, which you dub “promises” was actually innovated by the Chinese around 1000 AD give or take (would have to check my bookshelf)”

Check in the section on mesopotamian grain transactions- you’re off by a few millenia.

I meant paper credit (aka fiat money) – and went on to provide how paper credit was not the same as asset backed credit. I should have been more clear in my wording.

Read it as “Paper credit (aka fiat money), which you dub …” which is what I meant.

Regards,

Cooter

Hi Cooter,

Read your comments on ZH, they stand out from the noise. And boy, do we have a lot of noise these days :) . The narrative is crumbling.

I don’t regard this as right or wrong (I’m well past beyond that :) ), but I argue that the premise is that no one will lift a finger unless they get more out of it (even animals need positive ROE). Capitalism, as it is called now, but it was ever the same, a promise of more. Humans simply need a narrative, that’s all I’m arguing. Of course it is an advantage, evolutionary. However, the price of being at the top of the food chain is extinction, that’s the gold medal of champions, always. No exceptions. it’s the law.

Cheers,

Some guy on the net.

I follow the Royal Bank stock price closely because someone near and dear to me owns several thousand shares and simply refuses to see what I see – a very large top that has been forming since the weekly price peaked at $83.16 in late November 2014. No one seems to remember the stock was practically cut in half from its ’07 high in early ’09. I wouldn’t be surprised at a break-out in this lunatic algo driven environment but if it fails on high volume I think a few shrewd, patient short sellers will finally have their way and the downside will be epic. There has to be some pretty interesting skeletons in these Canadian bank closets that will eventually see the light of day.

Whereby the Best Banking System in the World was bailed out, even by the Fed …

https://www.policyalternatives.ca/sites/default/files/uploads/publications/National%20Office/2012/04/Big%20Banks%20Big%20Secret.pdf

Uh oh:

‘Where Will All the Money Go When All Three Market Bubbles Pop?’

http://charleshughsmith.blogspot.com/2016/10/where-will-all-money-go-when-all-three.html

Smith refers here specifically to U.S. stocks, bonds, and real estate, but there are huge bubbles everywhere in the world and they are all connected. So I ask the question again: where does money go when it dies?

Market distortions are supposed to be more or less self-correcting by compensatory market forces. Bubbles can be seen as symptomatic of the failure of market forces (and legal constraints) to operate normally, mitigating distortions and preventing corrections from becoming destructive on a large scale by allowing destruction to occur on smaller scales.

Unfortunately the policies of the Financial Industrial Complex, notably CBs, have been aimed at corrupting market forces and legal constraints to maximize their profits and to preserve their wealth by preventing corrections. These corruptions have shown up as gigantic bubbles as the distortions have become huge. Instead of preventing the inevitable corrections from becoming catastrophic through orderly and timely recognition of losses, their policies have long since guaranteed meltdowns that will raze the global economy.

When the going gets weird, the weird turn pro. And apparently become financiers who enjoy hallucinatory fantasies. It is only a matter of when, not if, and it’s not just going to be ugly. It’s going to be weird ugly.

Where does the “money” go?

Well, what is money? Then, realize, these prices of bubble assets are NOT real wealth, but rather prices at that time.

Assets have no real value. When the bubble collapses, the “monetary” value of these assets vanish since they were never real to begin with.

To sound like a 1885 Maxists, the real value is the amount of Labor put into the item. To value a house, calculate the price/costs of the labor and materials to put into it. All else is ego, fluff, demand, fear, status, etc. Why is this? You can take the costs of labor and materials and BUILD that exact house. There is the realistic real value.

And the value of the land?

In real estate, the house (building) is depreciated down to zero over time for accounting and tax purposes, on the assumption that the building will have to be torn down and replaced eventually. But the land has lasting value, subject to change, and is not being depreciated.

Marx was particularly wrong when it came to economics.

Well, he knew how to borrow money, spend it quickly, and not pay it back … what we now call the New Economics.

Walter, that was freaking great. Caught the reference to the Ferengi Rules of Acquisition “It never hurts to suck up to the boss”…the Rules are a liberal caricature of capitalism. Your double ironic satire made my whole day!

Such great discussions on this site.

My .02 cents is that Chinese have bought RE all over the place. I don’t think an event of falling prices will make them run. It is my belief that ‘they’ are concerned enough about what is going on in the homeland (economy, environment, socially) that if they put $1million into RE and it drops to $500,000, they could possibly still be ahead rather than leaving the money in China.

I am speaking ‘generally’ of course.

Here is one of the best articles I’ve seen on the Melbourne property markets.

It pretty much recaps almost everything I’ve been posting here about Melbourne’s RE:

http://www.domain.com.au/news/rich-and-poor-how-melbournes-property-divide-has-widened-in-past-20-years-20161003-gru7d6/

Yeah, we looked at Syndal/Mount Waverley/Glen Waverley areas when we moved to Melbourne, but those areas were dumpy, old, and transport was not very good.

Who knew that the Chinese would ‘invade’ those areas pushing up prices by ten times!!

Don’t worry everyone, when Trump becomes the Pres, he’ll straighten this all out ;-)

A similar situation occurred in the Miami real estate market. One group of wealthy foreign buyers replaced the previous group and so on … Colombians, then Venezuelans, then Europeans, then Russians, then Mexicans, then Brazilians. The incremental demand in a market with a limited supply pushed prices up to unsustainable levels. There were bidding wars for properties as prices soared and buyers panicked. But then the strengthening US dollar together with higher property prices choked off foreign demand and the incremental buyers disappeared. Local buyers could not afford the high prices and sales stalled, which is always the precursor to price drops.

When asked about the high prices of oil on 2015, the Saudi oil minister said “The cure for high prices is high prices.” We’re talking basic economics here – supply and demand. At the moment demand for Canadian real estate is higher than supply. At some point the cycle will turn, probably later than most predict, since that is the nature of markets, crowd psychology and bubbles. They overshoot both on the way up and on the way down. Easy credit and excess leverage exaggerate these moves, but are not the reason for them.

Any idea when the next housing bubble will pop? Just looking to get some insight. Some say US Housing prices will drop in 2017, some predict later.

When will be a good time to buy?

Thanks for your input

Markets are local. Some condo (!) markets are already popping, among them: Manhattan, Miami, San Francisco…

Others are still booming.

I understand. But at the same time, at what point does it all come together? By that I mean didn’t the 2008 recession affect the US Housing market in general?

Sure, it may start off local, but don’t all the prices eventually come down together? (a general decline). Almost all prices of US homes were significantly lower in say, 2012, now they’ve all risen together.

Thanks Wolf. I learning about the housing market.