A subsidy that is now reversing.

After the brutal beating following Election Day, US Treasuries took a breather early this week. But today, the beating resumed and will continue until the mood improves.

Mid-day, the 10-year Treasury fell so hard that its yield, which moves in the opposite direction of price, spiked to 2.42%. By the end of the day, the 10-year yield was at 2.36%, up 4 basis points for the day, and up an entire percentage point from July this year (via StockCharts.com):

The market is 100% certain that the Fed will stop flip-flopping in mid-December and raise rates by moving the upper limit of the Fed funds target range to 0.75%. The markets see more rate hikes next year. A Fed funds rate with the first “1”-handle since 2008 would be a phenomenon a whole generation of Wall Street gurus has never seen in their professional lives.

Mortgage rates are chasing after Treasury rates. The Mortgage Bankers Association reported today that the 30-year fixed-rate conforming mortgage ($417,000 or less) reached 4.16%, its “highest weekly average since the beginning of 2016.”

This caused a flurry of activity. Last week, amid the post-election interest rate spike, mortgage applications plunged. But homebuyers may be trying to lock in whatever rate they can get, before they go even higher, and mortgage applications surged.

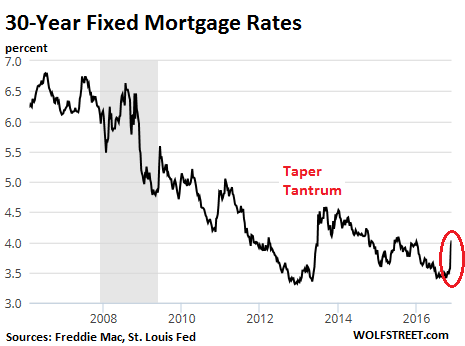

This chart, based on rates reported by Freddie Mac, shows the current spike:

Ironically, from a historical point of view, nothing major has happened so far. That spike is still small compared to what came before, including the spike during the Taper Tantrum in the summer of 2013, when the Fed started musing about ending QE Infinity. Compared to prior years, rates are still very, very low, but home prices have since soared, and for home buyers even a minor uptick makes a world of difference.

In San Francisco, as an extreme example, the median house price has skyrocketed from $695,000 in 2011 to $1.3 million in Q3 2016, according to Paragon Real Estate. This 87% surge in 5 years has been enabled by super-low interest rates. Other factors included the high-paying jobs created by the startup and “tech” boom, and the bubble of wealth it entailed.

But now interest rates are rising. Paragon looked at what that does to the costs of housing, and by how much household incomes would have to rise to buy the same home at even slightly higher interest rates.

For these estimates, the costs of housing include principal and interest of a 30-year fixed-rate mortgage, plus taxes and insurance. The base is the median house, at $1.3 million, with a 20% down payment ($260,000!).

- The recent increase in rates from 3.57% to 4.125% jacks up costs by $330 a month, or almost $4,000 a year.

- If rates drift up to 4.5%, costs jump by $560 a month, or $6,700 a year.

- If rates reach 5%, the additional costs jump by $10,600 a year.

What happens in some saner parts of the country is similar, but on a lower scale, depending on taxes and insurance costs. For example, for the national median home, priced at $232,200, with rates going from 3.57% to 4.5%, costs would rise by about $1,200 a year. If rates hit 5%, costs would jump by about $1,900 a year. For households on a tight budget, these additional costs would turn into an impossible squeeze.

And when mortgage rates rise beyond 5%? This used to be ridiculously low. Now it seems unimaginably high. For example, a mortgage rate of 6.3%, about the middle of the range during Housing Bubble 1 – the one Greenspan inflated when he cut rates way too low. That range lasted until mid-2008.

At 6.3%, the costs of a median house in San Francisco would jump by $1,730 a month, or nearly $21,000 a year. For the median home in the US, the cost would jump by $2,500 a year, which would move the house out of reach for many budgets.

Paragon points out how these low rates have “subsidized” the house price bubble: From the peak of Housing Bubble 1, which in San Francisco occurred in 2007, to Q3 2016, the median house price soared 45%. But due to plunging mortgage rates, the monthly housing costs increased only 14%.

Now with rates rising, that process is going to reverse.

The household income needed to qualify for a 30-year fixed rate mortgage with 20% down on that median $1.3 million house in San Francisco was $251,000 before Election Day. Paragon observes:

By Friday, November 18, the income requirement increased by $13,000. And if the interest rate goes up to 5% (and again, we are not saying it will), an additional $35,000 in annual income would be required.

Hence, at 5%, a minimum qualifying household income of $286,000 a year. In this scenario, even in less costly markets, there are two things that happen:

One, many people have to step down to a lower-priced home, or they don’t buy at all. A market-wide shift of this type puts downward pressure on prices and volume.

And two, as people stretch more to buy homes at higher interest rates and higher monthly costs, they have even less money to spend on other things. This creates a new drag on consumer spending. It’s how low mortgage rates not only subsidized the house price bubble but the entire economy by giving consumers more money to spend – not just the US economy but exporter nations around the world.

We’ve already seen the Credit Bubble Peak. It was marked by “Totally Crazy Lending.” Now the next phase has set in. Read… Now it Begins to Unravel

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Fk the Fed. Should have raised rates in 2012-3 when the housing bubble started up again. Now they want to raise rates, because they hate Trump and fear wage growth for the middle class? They can suck it. Hope they get thrown into a wood chipper feet first, and their bone meal used to feed the white house rose garden.

The Feds hate Trump??? Trump helping workers instead of screwing them out of their wages? Reality will be hard and fast!

Yaeh, things are about to get crazy. All that fake recovery crap is about to boil over into a melt down, and everything that has been hooked up to the free money from QE is going to be on a 220 volt live wire. Depression may not be a strong enough concept to describe where this is headed.

I agree things sure look like they are going to start unraveling and soon

Should boost housing Wolf as first timers & step-uppers scramble to lock in these historically low rates now, as conditions & rates begin normalizing to the mean.

Happy Thanksgiving!!!.. PJS

Yes, we’ve seen some of that last week. This will go on for a little while … and then it gets too costly.

Happy Thanksgiving to you too! And to everyone else out there!

Wolf:

I read a bunch of different analysts and your writing is beautiful in it’s simplicity. I only found you recently. You are now my go to guy!

When I began my financial odyssey I worked for Union Bank in California. That bank is no more but at the time it’s management training program was second to none. In my pen, where I spent 6 months analyzing financial statements, there was a banner that said “Brevity is the soul of wit”. That was 36 years ago. I have never forgotten it.

HAPPY THANKSGIVING

Wolf – would you please comment in the future on the general effect of rate increases on the categories of debt that have increased so much in the past 10 or so years? Auto debt and financing of auto purchases? (I think you covered some of that.) Student debt – especially new debt that will be incurred? Corporate debt and government debt – will either or both of those have to refinance at higher interest levels? There may be others that I haven’t thought of.

Debt in general? :-]

The big problem is debt that has to be refinanced at substantially higher interest rates (if and when they occur), such as bonds of all kinds, corporate, government, munis…. Substantially higher interest rates may make it impossible for strapped companies or municipal entities to roll over these bonds. This is when bankruptcies and debt restructurings occur.

This is not a problem for current borrowers with rates that are fixed once you get the loan, such as fixed-rate mortgages or auto loans. They’ll be paid off at the rate they had all along. I think student loans are also convert to fixed rate loans once you start making payments on them (not sure about this … knowledgeable readers please chime in).

But it’s a problem for new borrowers who have to borrow at higher rates, and thus will end up paying a lot more for their house, car, or education.

Even if the mortgage rate is fixed, increasing rates can still be a problem especially if people shoehorned themselves into the home with very little or no down-payment. Higher rates means the home is probably going to be under water which means the bank could ask higher payments or there could be a loss when selling the home (but who bothers about what will happens 10 or 30 years down the line…).

Probably different for US states with ‘jingle mail’ because the banks or taxpayers have to eat the loss? It’s also different in my country due to government mortgage insurance, but this only applies if you stay in the home. With millions staying put to avoid capital loss, the housing market will lock up and I don’t think that would be good for prices (although in the short term it would drive up rents, and maybe prices for more affordable homes too?)

As to the new borrowers: they may have to pay a higher rate, but if they have patience the principal will get lower to compensate for the higher rate. Depending on their financial position (e.g. possibility of down-payment) some new borrowers may be better off when rates start rising seriously.

In the US many borrow even for the down-payment, but not through mortgage. Last time the mortgage crisis was caused by LIBOR-linked mortgages. I wonder how many of those are still around. People should be crazy underwriting fixed-rate mortgages now or even some time ago. They may have to fund at higher rates two years down the line.

“http://www.nytimes.com/2016/11/24/science/global-warming-coastal-real-estate.html”

A little problem that is also finally starting to kick in.

Pretty soon a whole bunch of people in Florida, The Carolina’s, and California, are going to have some very expensive, unsalable Investments.

I believe both Wolf & I live in the Bay Area so know that, that 1.3 mil barely gets you a 60 yr old run down starter. It’s more like 2.2 mil for a small 15 yr old 4 bdrm; so more like an extra $500+ mo on a 30 yr fixed. It’s gonna quickly price out most folks – especially 1st time millennial buyers who are seeing rents tick down due to the unprecedented apt glut forming here & elsewhere.

Been saying for a while and still sticking to my guns. Not only won’t the Fed be raising in Dec but Yellen (via one of her cronies) will take the rate hike off the table before FOMC. Everyone keeps saying they ‘want’ to raise but I’ve yet to ever hear them back it up with the ‘why’. Here’s 7 reasons why they won’t be hiking and on Dec there will be an 8th.

January 27th – No Fed Rate Increase in January, as expected, but its statement suggested that future rate increases are likely.

March 16th – The Federal Reserves stands pat at its March meeting but stress it is prepared to raise interest rates in April.

April 27th – The Federal Reserve did not raise its key interest rate on Wednesday but its leaders signaled that they may raise rates at their upcoming meeting in June.

June 15th – The Federal Reserve left interest rates unchanged on Wednesday even as it said that the labor market has “strengthened” and growth of economic activity has picked up, implying a rate hike as soon as July. Still think they give a damn about credibility?

July 27th – The Federal Reserve’s monetary policy committee said Wednesday that it left its interest rate target unchanged as expected, but is likely hike rates at their next meeting in September.

September 21st – The Federal Reserve holds interest rates steady and indicates that moderate US economic growth would allow it to tighten its policy this year as early as next months meeting.

November 2nd -The Federal Reserve kept interest rates unchanged on Wednesday in its last policy decision before the U.S. election, but signaled it could hike in December as the economy gathers momentum and inflation picks up

You may be on to something there Patrick,the only reason i can see them raise is to salvage what little is left of their credibility. scenario # 2: inflation picks up substantially witch would leave them way behind the moving train,either way we’re screwed! lol

We are one good stock market crash away from plunging rates, and the Fed knows that, The Fed may raise rates a little, but then it will lower them again.

In 2011, the USG gave first time home buyers tax credits in order to goose the market. If the Government chooses to do so, it can buy rates down to 2% for a three year period, and push mortgages out to 40 year ams. Payments on a $300,000 loan would be around $700 a month. That could spur another round of home buying, as long as there was inventory out there to buy.

Anyway, the fact that higher rates would make it even more difficult for the Treasury to finance the debt, means that the Fed will have to keep rates down.

What if the stock market spends the next 20 years not plunging but just drifting up and down with a downward bias, and no one can make any money? The Fed won’t even notice it.

They could even use Dutch tricks like sub-1% mortgage rates, full mortgage tax deduction from income tax (in Netherlands that means the government pays about 50% of the mortgage), full government mortgage insurance (no risk of losing money when selling the home!) and countless other homeowner subsidies and guarantees.

Our ‘first home buyer subsidy’ applies to everyone below 40 who hasn’t owned a home in the last 5 years. In addition to a normal mortgage (always the maximum you can get), which doesn’t require any downpayment here, you can borrow 25-75K from the local government at ZERO rate, and even more if you use the money to improve energy performance of the home.

Wait, it gets even better: you only have to start paying interest on that 25-75K loan after four years if the home has appreciated, so if the home doesn’t appreciate the loan remains totally free and you even don’t have to pay the money back when you finally sell the home at a loss! Please note that the normal mortgage is also insured against loss by the government so the buyer has all the upside and none of the downside. Of course, this also means that ‘starter homes’ immediately appreciate by 25-75K in areas where the government offers this option, so for starters the gain is totally fake but it’s nice for politicians and landlords who are in on the game.

All this has worked wonders over the last 30 years in producing one of the biggest housing bubbles on the planet. If you think it cannot get any more crazy, look at the Netherlands and all the idiot ideas that may be coming to your country too if politics gets desperate ;-(

Of course, miracles don’t exist and sooner or later reality will set in with a vengeance – but it obviously can take a long time …

There’s a different reason why I believe the Fed will hike rates from nothing to next to nothing: to have something to cut if the need be.

Today the US stock market is doing great, but it’s doing so only at the expense of everything else, including US securities, and owes a lot to foreign buyers betting on short term US dollar inflation or simply abandoning their ships (for example EM bonds) for safer shores.

But as my high school Latin textbook said “Fortuna ut antiqui dicunt caeca est”. Foreigners may discover that short term US dollar inflation is taking much more time than they expected to materialize and pull out. A million other things can happen: the carnage on bond markets, which isn’t limited to the US, wasn’t supposed to happen, as central banks “have that covered”.

Investors these days are not merely prone to panic, they tend to believe all the craziest rumors: see how the Iranians and the Saudi have been playing commodity markets for months now without cutting a single barrel and laughing all the way to the bank.

Having rates over 1% is something the US economy, even with its present leverage, can afford, especially given the rest of the world is so desperate for yield and ready to pour on US security markets, and would give a lot of maneuver room, at least relative to other central banks, in case of a true crisis (which, contrary to what traders believe, is not a 10% drop in stock values).

The Fed has watched Europe’s crazy experiments with NIRP’s from a safe distance and rightly concluded those things are like flying cars: great idea on paper, embarrassing in reality.

why loan 10years out when it’s not a good return?

that’s why.

where are you, convexity?

Inflation is already at 1.6%. There are, of course, reasons to disbelieve this. For example, the falling rents (making close to 50% of the CPI) were cited as a key driver of falling inflation. Those, I hear, are up more than 10% year-on-year. How then CPI is under 2%. Another one is healthcare costs.

But even if we ignore consumer inflation, the asset price inflation has been much much higher.

did you see the fed bleak or even file into a room to explain the rout

I am thankful for being a renter,landlord hasn’t raised the rent in 5 years and in return i change the light bulbs and fix the plumbing. his monthly HOA fee has got be around 700.00 by itself,i assume he payed in cash when he bought it. here’s to stress free living and happy Thanksgiving to all Wolf readers!

I’m just guessing but you are probably keeping your landlord out of foreclosure. He may be underwater and grateful to have a steady tenant. I was in that situation myself, and was glad it was only costing me $100 a month to keep from going under. BTW, that was a house I bought with a 20% down payment, which I lost when I sold.

I’m in a bit similar situation in the Netherlands and paying about the same rent as 6 years ago when I started renting here.

There probably is a difference with the US situation though: in Netherland it is almost impossible to evict a renter when they have a normal contract. Renter protection is extreme (as long as they pay the rent). Many landlords have started to use ‘temporary’ 1-year rental contracts, invented for homeowners who want to rent out their old home when they move to a new one and haven’t yet sold the old one. But these temporary contracts have many strings attached for the owner.

In my case, the rental contract automatically became ‘indefinite’ because the landlord didn’t cancel it after renting ‘temporary’ for a year. My apartment just went on the market (forced by the bank I assume, because the mortgage is under water) but I don’t think anyone is interested in buying an apartment including a renter. If I take the HOA fees into account – which the owner still pays – the yield is something between 1 and 2%. And not much chance of appreciation either, with rates in Europe at 5000-year lows (according to some, but for sure they are lower than at any time after the Middle Ages).

The only risk is that the RE agent and the bank arrange a short sale under the table, assuming that the current owner has plenty of money in the future to pay them back. Not likely I guess …

You are describing a pretty common situation.

My sorely missed ex inherited from her grandfather an apartment in what at the time was a very prime location on the Spanish coast. Said apartment came with a renter included who had a bad habit of falling back on his rent payments and never catching up and, as he learned the new landlady wasn’t local, stopped paying rent altogether.

As the rent contract was very old, it became a struggle to evict the b***ard. Luckily the legal fees were cut short when the guy had a stroke and died while at a football game. Even more so, death by witchcraft is not included in most penal codes.

@ MC:

Yes, bad renters are a common problem in Netherlands and probably much of Europe. It is one reason why many speculator homes stay empty instead of renting them out (this is in addition to the currently very low rental yield).

Until recently renters could get away with not paying rent and it was almost impossible to get evicted. Housing corporations have recently started to evict renters who are 3 months behind (while people with a mortgage aren’t even officially in default if they haven’t paid the mortgage for over a year …).

But for private landlords this is a huge problem because no one will help you deal with such a bad renter, you have to go to court and even a conviction will often not help. One can try shutting off water, electricity etc. or sent a few guys from the local gym for a visit, but that is officially a crime and some bad renters may not even care ;-)

I’m sure my landlord is happy that I’m helping with the mortgage payments, he knows that I have the money to pay rent forever, so no risk for him as long as I stay. Some renter protection is good, but in much of Europe it has gone way too far and in the end that is bad for all honest renters (and only good for the crooks and those without money).

I wonder how this is going to affect the large and somewhat troubled commercial real estate market. I believe a lot of that debt has been tied up in bundles and resold. Malls are dying and brick and mortar businesses are hanging on by the skin of their teeth and a downturn (which I do expect) will start a cascading effect. I also agree that interest rate rises will have a significant impact on rolling over corporate debt which will have a sobering effect on the artificially shown profits. One reason I was for Trump as I’d rather have a realist businessman in to handle the crisis that I feel sure is coming

A realist businessman? He is the king of corporate bankruptcies. He doesn’t handle problems he walks away from them.

Two things that can’t be done. You can’t run the government like a business and you can’t run a business like it’s government. When a Hurricane Sandy hits, the government steps in to backstop businesses and private citizens. Businesses don’t function that way, nor should they.

We can argue whether Trump is a good businessman or not (put me down for not). The better question is, does a businessman really bring anything to the government table?

Good points. Unfortunately, as of now he appears to be primed to use the Presidency to further his own businesss interests more than anything. Michael Bloomberg is a businessman, Trump is a carnival barker. Four years of America as soap opera.

IMHO a businessman will often be the better choice when you need a ‘manager’ to turn things around, instead of the politicians of today who only kick the can down the road, make the problems even worse and try to fill their pockets on the side.

Of course, some big business executives are similar to current politicians. But it seems to me Trump is mostly a self-made man and if he choses the right people to help and advise him there is a chance he can turn around the USA for the better.

Also, Trump no longer has to prove himself, build a legacy or make lots of money (like e.g. the Clintons) as he already did that. I don’t know if he is up to the challenge, if too many insiders from the ‘Deep State’ take part in the new administration he will probably not get very far with making changes because the elite really likes how things are going …

nhz,

Self made? Donald Trump went from rich to even richer, which is much different. He went to the best private schools, had amazing connections, took over as president of his father’s organization, and had a huge inheritance. Now, he did grow the business even further, which is to be commended, but, at the same time, he grew it in a way that required multiple bankruptcies.

Now, I’m a small business owner who certainly isn’t as “successful” as Donald Trump, and I give him credit for that, but calling him self made is a huge stretch. He had everything lined up for him from the beginning.

” He had everything lined up for him from the beginning.”

Including all those very important “CONNECTION’S” in the NY construction system, you need to get anything done, at anything close to the pace, his family does.

Solves the problem, doesn’t it…………

Absolutely false. Of Donald Trump’s more than 520 companies in the Trump Organization only 4 have ever filed for corporate bankruptcy which is far less than 1% and the other 99% have never filed for bankruptcy. Donald Trump has never once filed for personal bankruptcy, and most of those 4 that did file for corporate bankruptcy were affected by the massive downturn in the casino industry. The Trump Organization has continued to grow in size and is an extremely well run and profitable organization.

>>> “The Trump Organization has continued to grow in size and is an extremely well run and profitable organization.”

How do you know that? Are you the organization’s CFO and leaking this info?

There is no public data on the organization’s financials. We don’t know anything about growth, size, sales, or profits. Nada. Zilch. You’re just making up stuff as you go.

“You’re just making up stuff as you go.”

Like all the followers, who do exactly what their hero POTUS ELECT 45 does.

Follow the fakestinians, who have proved, beyond any doubt, the truth can never catch up, with a professionally propagated, muslim lie (AKA Islamofascist propaganda)

It Will be interesting to ser how Black Friday turns out and how the X-mas commerce will turn out this year. Will the uptick in rates now experienced affect people’s behavior or will people use their cards until those cards are glowing hot ?

Speaking of Black Friday, I am sure that the Walmart commercials featuring a James Brown soundtrack pumping up consumers to be excited to shop at 6:00 pm today will have some success, but what a reflection this is on our culture in America.

rich’s comment regarding the Fed’s rates and the Treasury’s financing of our $20T debt is quite a valid point/concern. We have a national debt that’s five times the size of our 2017 federal budget, and closing in on six times the revenue. How the hell is this scheme going to continue to play out ad infinitum if not for ZIRP? Answer: not too good.

Another question for Wolf and readers is, are citizens scaling back expectations and desires for how much home they want to live in and pay for? In retrospect, when my family sold our business six years ago, I could have easily stepped up to bigger and more luxurious home, but staying in my modest, comfortable and paid off home was one of the smartest decisions I’ve made.

Today I give thanks for my health, my family and friends, and a damn good quality of life! All the best to everyone out there too.

I don’t believe interest rates have any impact on government. The government essentially always kites its checks, meaning it always runs a negative bank balance. And its debt will always be bought by the primary dealer banks, or the Fed if needed. So if rates go up, it just writes bigger checks and issues more bonds. Same as Japan.

Totally the opposite of the private sector. But I believe designed to be that way as an economic stabilization mechanism.

as to scaling back expectations:

I downscaled over a decade ago from a +/- 8000 sqft home (17th century mansion on top location) to +/- 1000 sqft apartment a few streets from the former property. Although I miss the special vibe of that age-old building, in most ways the downsizing was a pleasant experience and not just because of the finances. Repairs, heating bills, too many rooms that weren’t really used and were collecting garbage and dust, government officials wanting to be involved in every change you make etc. etc.

I have started to look at the housing market in a very different way and no longer think about ‘upgrading’ for the sake of it. Maybe one day I will move to a slightly bigger home again (with a garden, which I would like but don’t have at the moment; and with a bit more office space) but definitely not at the current price levels because it just isn’t worth it.

I’m in Netherlands but it looks to me like we are importing all the ‘Black Friday’ craze and other culture from the US, especially the negative side as the BF discounts here are much smaller ;-(

It’ll be record sales and record spending for Black Friday & Christmas sales.

Why wouldn’t it be? Times are good and Confidence has jumped after Trump’s election.

It’s next year that’ll be interesting – with plenty of carnage. Chaos in Europe and emerging markets.

2017 is going to be brutal.

And it’s all going to be Trump’s fault.

You watch it – whether it is or it isn’t. Trump will get the blame. Like it or not. Stiffing Saudi Arabia of all their Treasuries will help a bit though.

LOL Sauds.

Thanksgiving, Black Friday store sales fall, online rises

Sales and traffic at U.S. brick-and-mortar stores on Thanksgiving Day and Black Friday declined from last year, as stores offered discounts well beyond the weekend and more customers shopped online.

Internet sales rose in the double digits on both days, surpassing $3 billion for the first time on Black Friday, according to data released on Saturday.

Data from analytics firm RetailNext showed net sales at brick-and-mortar stores fell 5.0 percent over the two days, while the number of transactions fell 7.9 percent.

http://www.reuters.com/article/us-usa-holidayshopping-idUSKBN13L0ZH?il=0

“What if the stock market spends the next 20 years not plunging but just drifting up and down with a downward bias, and no one can make any money? The Fed won’t even notice it.”

Wolf, it’s Thanksgiving, not April Fool’s Day.

Happy Thanksgiving everybody!

As for the subject, it doesn’t matter to me what the mortgage interest rate is because I am not interested in buying. The treasury rates have no bearing on the lives of people in financial distress because they are already paying usurious rates, like 24% for a car loan or credit card, and 30% on a store department store card. These are not made up rates, they are rates that I have paid. The former middle class doesn’t have the savings or job security to go back into the housing market.

Since I do not contribute to the demand for credit in the housing market or retail, and I am hardly an exception in the economy. Regardless of how upbeat I feel, I will not be goosing up the numbers for housing. But I do take advantage of the holiday sales to replace items I need.

Petunia, 25% of American children are on food stamps, 69% have less than $1,000 in the bank (can’t afford to pay cash for new SUV tires), and 76% of Americans are living from paycheck to paycheck, but much of that is because Americans have been conditioned to buy stuff they don’t need, with money they don’t have to impress people they don’t like.

The flip side of these American debt-serfs is a finite group of financial engineers that have built the wealth-extracting machines that have hollowed out the U.S. economy. Robert Rubin is the consummate financial engineer. He left his Goldman Sachs CEO position to become the Treasury Secretary under Clinton. He engineered the repeal of three acts that had protected the American citizen from the big banks. He got the Riegle-Neal Act passed in 1994, making interstate banking the law of the land. Then, in 1999, he did Citigroup CEO, Sandy Weill, a solid, by repealing the Glass-Steagall Act by passing the Gramm-Leach-Bliley Act. Weill had already violated Glass-Steagall by acquiring Traveler’s Insurance. Then Rubin got Summers to pass the Commodities Futures Modernization Act of 2000, which deregulated derivatives trading. These three Acts ultimately destroyed the US economy and took many of the world’s other economies along with it.

Meanwhile, shortly after leaving the Treasury Dept., Rubin went to work for Sandy Weill at Citigroup, where he was rewarded for what he had done of Weill. Under Rubin’s rule, Citigroup imploded, but the well-connected former Treasury Secretary was able to garner $2.5 TRILLION for Citigroup’s bailout. Today, Robert Rubin has a net worth of over $100 million dollars.

Rich, point of information, Sandy Weill headed Traveler’s Insurance before the merger. John Reed as the C.E.O. Of Citi.

Petunia, don’t say such terrible things. TPTB have been counting on you to dedicate yourself single-mindedly to cranking up consumer spending, the housing market, consumer debt, and corporate profits. TPTB are disappointed in you….

:-)

Well,

There is that Xmas ornament in the shape of Trump’s Make America Great hat and it’s only $149… I’m so tempted.

My son just bought his first house for $181,000. This is a small city in Central Florida, not SF, so the price is ok. Brand new house, 4 bedroom, 2000 sq ft. He has a steady job.

My fear is if interest rates steadily march up over the years, he’ll never see any appreciation on the property. So I told him to make payments as if it were a 15 year loan. At least he may get a chance to pay it off.

if interest rates keep marching up it’s probably because inflation is marching up as well. The FED seems determined to stay behind the curve forever. Although that doesn’t bode well for appreciation, it probably means that paying the mortgage (I assume he has one) will get easier every year assuming he keeps his job.

I’m in a very different situation and would get interested in buying only when mortgage rates go sky-high. With the current housing market (in my country highest valuation to income in over 400 years, lowest rates ever, idiotic price level in general etc.) I see very little room for real appreciation of homes. Buying now may be prudent but only if you don’t have any money (so there is nothing to collect when the mortgage goes under water), if you have a fixed job that makes a mortgage attractive (in my country it’s all about the mortgage tax deduction) and if buying is cheaper on a monthly basis than renting (in my country buying is currently 2-4x cheaper than renting …).

I’m planning to pay cash and high rates (plus a down-payment requirement which we don’t have now) would eliminate over 90% of the current buyers. Prices would have to drop by 75% or so to get the market moving again. Even then, home prices would still be far above their inflation-adjusted values from the early nineties, when the economy was in pretty good shape. Of course almost everyone in my country is hoping and expecting that this will never happen; unfortunately for them, history is against them as my country has had several housing bubbles before and they always pop.

Very wise game plan nhz. My one and only home purchase took place during falling 30 year T-Note rates way back in 1995. On 7 November ’94 they were at 8.15%, and in barely a over a year, on 22 January ’96 they’d dropped to 6.04%. This spurred the housing market quite a bit, but when I saw my home I now own in summer ’95 I made a cash offer just over asking price, and that did the trick. It helped that my folks could write the check and provide me the mortgage, and it wasn’t a bad deal for them to be paid at a 6% rate back when capital had value and appreciated!

My next door neighbor just moved back to the USA from 35 years in Netherlands to her family’s home of 60 years (where she grew up), and man, she has stories that can add to what you have so eloquently commented on here. Best of luck to you!

@Dan:

my only home (+ office) purchase was in 1992 when mortgage rates were near 12%.

I paid off the mortgage a few years later, everybody thought I was crazy because I should have kept the maximum mortgage (because of our mortgage tax deduction) and invest everything in the stock market as most people with money did in the nineties. When I sold in 2001 because of a crazy new tax rule, the price of the property had increased by over 400%. Unfortunately, that gain was mostly paper profit because most homes went up just the same or even more, and have kept increasing ever since including rents – and you have to live somewhere.

In hindsight I should have purchased in cash a modest home then, but I thought prices would collapse soon and the more modest homes were often even more overpriced. Plus I was planning to emigrate and didn’t want to get stuck with a property.

The market can remain irrational for longer than most people can stay solvent ;-(

Speaking of 15 year mortgages, I remember my Mom ranting and raving about the criminal use of 30 year mortgages to goose the real estate market, when the banks started moving that way back in the 70’s. A way to give people more debt and keep the prices up.

A daughter of the Great Depression, she knew the price of money and the danger of carrying that much debt. It was the whole amount of the loan that should be the number on the price tag, she argued, not the published listing.

So even now, in SF, if you buy a house for 2.2 mil, you are really paying over 5 mil on the life of the loan.

5 million – for a 2+1 that probably cost just 5000 to build in the post WWII era.

Is that not HYPERINFLATION – ????

The banks that are giving out these JUMBO loans are the ones that will blow up first……

Oh wait, they won’t call them in. Pretend they are still good, until they can get their buddies down at the FED-fronted hedge fund to take them off their hands…. at face value.

Rinse and repeat

yeah—Happy THANKSGIVING to you all, and a big clenched fist out to the Standing Rock water protectors on this day!

i’m also ever so thankful that this site exists. it is a touchstone of sanity as i quietly try to feel what’s changed, what’s going on right now in this cartoonishly over-the-top world. the older i get the less i know and understand. pigs are flying everywhere and i’m still trying to wrap my head around it all.

and PETUNIA… i cannot thank you enough for being an unusual woman. whew…i need that. and i raise my own rhinestone flip flops to you out of gratitude…

x

BTW, what’s happening to savings rates in the US?

In Netherlands the last 30 or so mortgage rate changes after the Trump election were all positive (higher rates, although usually just 0.1-0.2% more).

Of the last 30 or so changes to savings rates, almost all after Trump election were negative (even lower rates) and only two were positive (0.05% increase on rates for 10/30 year term deposits; yes, you can still lock in about the lowest rate in 5000 years for the next 30 years!!).

The bankers must love this turmoil :-(

nhz,

You always write about the distortions in the housing market due to all the intrusive tax policies. I hesitate to call them bad tax policies but that is the impression I get from your comments. I think that if the govt wants people to be better off, they should let them keep their own money or give them some. Do you think that direct payments to citizens would have been a better policy? If the govt wants to give people housing, they could build free or low cost housing and not interfere in the private markets. What is public opinion on the housing situation?

Petunia,

One of the comments my neighbor who just moved back from Netherlands has made to me a few times, is that when she arrived in her ancestral home 37 years ago, she was seen as an immigrant and given help in finding and subsidizing her home.

This practice is now under scrutiny, to say the least, with the influx of immigration into Europe from refugees displaced by the USA’s and NATO’s (amongst others’) intervention in North Africa and the Middle East.

As a person who is basically Libertarian, I don’t believe tax policies should intrude into the housing market. Nor do I believe the government should give people money-which they do via housing in Holland. I do believe governments should let people keep more of their money.

Although I can not speak for nzh, I would bet that most of Wolf’s readers would agree. How about you? What is the balance for governments to intervene or not intervene into residential real estate ownership and transactions? We have property taxes, zoning and eminent domain issues, but please remember what James Madison so perfectly stated, “The rights of persons, and the rights of property, are the objects, for which Government was instituted.”

Here in south Minneapolis, I say, “My house. My rules.”

I’m all for letting people keep as much of their productivity as possible. However, this country was founded on principles that are bigger than the pursuit of profits. “in order to form a more perfect union…life, liberty, and the pursuit of happiness”. There is a moral obligation in these words that remind us that we are our brother’s keeper. It guarantees us our lives collectively.

@Dan:

fully agree.

@Petunia:

I have no problem with the government building or otherwise offering very basic affordable homes for those who don’t have the money and would otherwise ‘have to live on the streets’. But the Dutch situation is far removed from that.

To give you an idea: a Dutch Labour politician recently suggested that the government in her area should build 400-500K villa’s for the new refugees, instead of housing them in a rebuild former government building (with perfectly fine but relatively small apartments, according to her this was not a way to treat refugees). 90% of the Dutch population could never afford such homes if they wanted; and I’m sure the villas would be completely trashed in a few years.

We also have single moms on social security, paying 280 euros a month to the housing corporation for very nice family homes with garden that cost over 1000 euros for someone who is working and doesn’t quality for all the subsidies. The result: over 3/4 of the homes in this area – formerly for well-off citizens – are now occupied by people on social security, former refugees and other ‘difficult’ cases. The homes still look very nice but the social situation in the area has become a disaster. Of course the current inhabitants will never leave because and I’m sure they will vote to keep the current system in place.

You may think it is nice that people who have never worked or are recently arrived ‘refugees’ (which IMHO are 90% economic refugees, and not political or war refugees) get a great home, but I think it makes for a very bad incentive.

I guess most Dutchies who shoehorned themselves in a home they could otherwise never afford – either in heavily subsidized rental housing or in a home far above their means with maximum mortgage – love the system and hope for the best.

The others curse the system because they have to pay through the nose – if you don’t qualify for the countless subsidies, tax deductions etc. etc. our housing market is one of the most expensive in the world, both for buying and renting. And if the housing market crashes, those who did NOT profit will get to pay most of the bill too.

I just think the Dutch system is extremely unfair and will cause tremendous damage in the long run, because this bubble will blow and take most of the Dutch economy with it (which – a bit like the US – has changed from real production to mostly shuffling financial paper over the last 25 years).

I have no doubt that our politicians do NOT want people better off, they want to protect the elites that profit hugely from the RE market. Most multimillionaires/billionaires here made their fortune through real estate and the rest of the population pays for it. And of course, for politicians the housing market is the prime target for re-election promises. I have no doubt that with the next election, another stupid housing subsidy will be invented for a specific voter group, probably minorities or former ‘refugees’ while other will vow to fight for keeping all the current goodies intact whatever happens.

Our rental market with housing corporations for ‘social housing’ is a bit unique in the world and probably originated from the best intentions long ago; but is has metastasized and is now mainly a system that rewards parasites and crooks and makes housing UN-affordable for everyone who does NOT depend on the government. Many people on social security live in nicer homes than people who are working day and night; not good.

I would rather see cash payments to the poor than housing subsidies, when possible, because it is more efficient.

I recall a widowed neighbor who received welfare, when I was young. Instead of cash they made her go pick up flour, cheese, and other foodstuffs. She used to sell all the items to my mother because none of the items were ethnically appropriate for her. The entire exercise was ridiculous because they were basically subsidizing my family.

The control they try to exercise over people is what introduces all the inefficiencies in welfare systems. I can tell you that nobody handles money better than poor people, they have to.

After the trump effect Wears off…back to snafu

Hope your Turkey is moist and your stuffing is fluffy, then when you’re done eating you’ll be nice and puffy.

Finding 3.5 million in gold in your new house wouldn’t be bad either, like the bloke in Normandy.

This is real, up here in Canada, not only are they hiking rates, they’re passing all kinds of laws which are crushing the housing market. When you understand that these events are orchestrated, and done in unison, all the fog lifts and you see the picture clearly.

Yes, there was collusion with the BC government tightening the screws on chinese money, then the US government looking at all cash deals in certain cities in the US. The fix was clearly in and this b!t<h is going down. Only remaining question is if we get a real washout in RE prices at the bottom – hopefully no blackrock and others getting sweet deals from their govt connections to screw the middle class.

Rates are going up in Australia…………..again.

SEE:

http://www.theage.com.au/money/eyes-on-other-majors-as-westpac-increases-mortgage-rates-20161125-gsxj5m.html

“Westpac is the first major bank to increase interest rates on its fixed rate home loans and investment loans, but market watchers expect others to follow.

Property investors who take a Westpac five-year fixed rate mortgage from next week will see an increase of 0.6 percentage points to 4.59 per cent in the interest rate – the biggest of the increases.”

We don’t fool around here in Oz. No small jumps in anything. Big increases all the time and little or no decreases. (Gasoline, electricity, NG, fines, fees, etc)

No doubt the big banks will use this increase to offset losses in their commercial and corporate areas.

And jut the other day there was an article about how well Australian banks had met their capital requirements.

Did the Bank of Japan prevent the US bond market from imploding?

The turmoil in the financial market was far from good news to President-Elect Donald Trump.

The 10-year Treasury yield was on pace for the largest 2-week rise since 2009. The crash in the bond market happened alongside a 10% devaluation of the Japanese yen.

The mainstream media presented the dumping of Treasury bonds as good news. Investors miraculously expected the US economy to boom and inflation to rise now that Donald Trump will be their president. The same media analysts that predicted two weeks ago that the financial world would collapse if Trump were elected are now convinced that Trump’s plan to increase spending and lower taxes will finance itself.

This can be the case for the 1 trillion infrastructure spending Trump promised, but the tax cut for the more wealthy Americans will do nothing more than explode the public debt1).

Now that interest rates are rising, consumers, companies and the governments have to pay more to service their debt. They will spend more money on interest without increasing productivity, hiring more employees or consuming more. The sell-off in Treasuries was bad signal for the US economy at large.

https://gefira.org/en/2016/11/23/did-the-bank-of-japan-prevent-the-us-bond-market-from-imploding-again/