Six years of Fed & Wall Street hype come home to roost

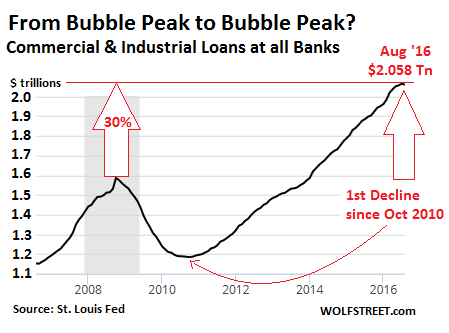

Something funny happened on the way to the bank: In August, commercial and industrial loans outstanding at all banks in the US fell for the first time month-to-month since October 2010, which had marked the end of the collapse of credit during the Financial Crisis.

In October 2008, the absolute peak of the prior credit bubble, there were $1.59 trillion commercial and industrial loans outstanding. As the Great Recession chewed into the economy, C&I loans plunged. Many of them were cleansed from bank balance sheets via charge-offs. But then the Fed decided what the US needed was more debt to fix the problem of too much debt, thus kicking off what would become the greatest credit bubble in US history. By July 2016, C&I loans had surged to $2.064 trillion, 30% above their prior bubble peak.

But in August, something stopped working: C&I loans actually fell 0.3% to $2.058 trillion, according to the Federal Reserve Board of Governors. That translates into an annualized decline of 3.8%, after an uninterrupted six-year spree of often double-digit annualized increases. Note that first month-to-month dip since October 2010:

It’s still too early to tell how significant this dip is. It’s just the first one. It could have occurred because companies borrow less because they need less money as there’s less demand, and expansion is no longer on the table. Or it could have occurred because banks are beginning to tighten their lending standards, with one hand on the money spigot. And all this is occurring while banks write off more nonperforming loans (and thus remove them from the C&I balances) that have resulted from mounting defaults and bankruptcies by their customers.

The ugliest credit stories in terms of bonds, according to Standard & Poor’s Distress Ratio, are the doom-and-gloom categories of “Energy” and “Metals, Mining, and Steel.” Next down the line are two consumer-facing industries: brick-and-mortar retailers and restaurants.

But these metrics by credit ratings agencies are based on companies that are big enough to be rated by the ratings agencies and that are able to borrow in the capital markets by issuing bonds. The 18.9 million small businesses in the US and many of the 182,000 medium size businesses don’t qualify for that special treatment. They can only borrow from banks and other sources. And they’re not included in those metrics.

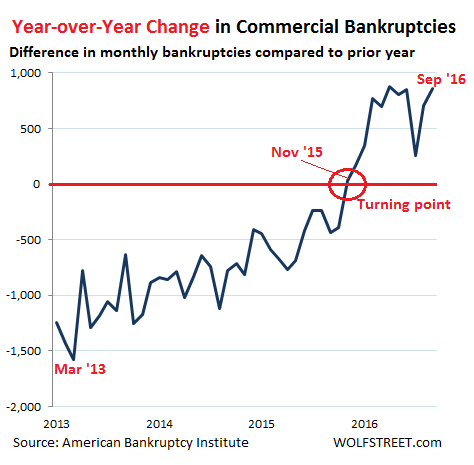

But when they go bankrupt, they are included in the overall commercial bankruptcy numbers, and those numbers are getting uglier by the month.

In September, US commercial bankruptcy filings soared 38% from a year ago to 3,072, the 11th month in a row of year-over-year increases, according to the American Bankruptcy Institute.

For the first nine months of 2016, commercial bankruptcy filings jumped 28% compared to the same period in 2015, to 28,789. Most of those are not the bankruptcies we hear about in the financial media. Most of them are small businesses that go that painful route – painful for their creditors too – in the shadows of the hoopla on Wall Street.

By comparison, just over 100 oil and gas companies in the US and Canada have gone bankrupt since the beginning of 2015. About a dozen retail chains have filed over the past year, along with about 12 restaurant companies, representing 14 chains.

Commercial bankruptcy filings skyrocketed during the Financial Crisis and peaked in March 2010 at 9,004. Then they fell on a year-over-year basis. In March 2013, the year-over-year decline in filings reached 1,577. Filings continued to fall, but at a slower and slower pace, until November 2015, when for the first time since March 2010, bankruptcy filings rose year-over-year. That was the turning point. Note that there is no “plateauing”:

In September this year, bankruptcies exceed those from a year ago by 855 filings – the 38% jump. March and May saw similar year-over-year increases. So this looks like it’s the beginning of a new and long trend that is not going to fit into the rosy scenario.

Rising bankruptcies are an indicator that the “credit cycle” has ended. The Fed’s policy of easy credit has encouraged businesses to borrow – those that could. But by now, this six-year debt binge has created an ominous debt overhang that is suffocating these businesses as they find themselves, against all promises, mired in an economy that’s nothing like the escape-velocity hype that had emanated from Wall Street, the Fed, and the government.

Restaurants are experiencing a wage of bankruptcies that rivals that of 2009-2010, with “very challenging” sales trends. Read… Restaurant Industry, Leading Indicator of US Economy Sours, Bankruptcies Pile up

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf,

It would appear the fake economy has encountered a “Divine Wind.” Perhaps you could do another spot on all these mergers and acquisitions, it would appear this has hit a fever pitch.

IPOs too!

Cheap money is seductive. And it tempts those that can borrow it to swing for the fences..But even cheap money requires repayments. The real killer is if it’s USD and that’s not your currency. The strengthening $USD must be a concern. I wonder if this has effected the timing of the Fed rate hike?

“But even cheap money requires repayments.”

Exactly.

What good does it do to get cheap credit if the borrower can’t pay it back? That’s just buying time. It’s why a monetary stimulus policy can’t work at the lower bound. It can only make a bad situation worse.

The Financial Industrial Complex has increasingly offered cheap credit to compensate for lack of income. After all, why should they pay you when they can get you in debt instead? Ultimately the problem is income, and not credit. It’s their way of papering over the fact that they are in fact liquidating the U.S. and other economies.

What do you see when you remove the contribution of the FIRE sector from GDP statistics? You see that the real economy has been in recession since the bursting of the dot-com bubble.

Investment in the real U.S. economy tanked years ago and stayed that way. You don’t invest in operations you plan to discontinue. You extract the residual value and close it down. The only reason most of the U.S. hasn’t yet turned into Haiti is because it still has residual value left to extract. These things must be done delicately, or you hurt the spell.

I wanna know when a big sports league or public institution, part of the military/sports/industrial complex, goes tits up.

NFL TV ratings are down 20%, nobody actually goes to NBA games and baseball is talking about signing a guy for 500mil. Could that one guaranteed contract bankrupt the whole league?

Actually the real danger is with the public universities that have been captured by the professional football team/cabal, run by rich alums and their toady athletic directors. All have opened huge credit lines to build massive facilities that have become huge money losers.

Only five football programs across the D I spectrum actually generate revenues. There is a glut of football product on TV. Ticket prices to college games are now on par with some NFL venues. This will not end well.

Our local state school has lost between $13mil and $18 every year for the last five years just on its athletic department. The alums opened a $50 mil revolving line of credit to cover the gap. Wonder what bank is holding that note? Who will bail them out?

When we cannot afford our own debt-laden, high-priced bread and circuses, what will come next?

ooooh, that’s GOOOOD. very, very interesting. and fascinating….

A life of quiet contemplation and religious devotion?

I’m surprised the media isn’t one of the industries that shows up as being endangered. Here it is election season and I haven’t seen one ad that wasn’t shown by a news anchor, associating it with his commentary. No one is watching tv and nobody wants to. Sports have peaked, mostly because no one can afford to attend the games, so they have eliminated their fan base.

I bet they are kept alive by powerful business interest and the MIC.

In my country the people employed by the public TV corporations are the highest paid government workers in the country. Many of them make more money than our highest politicians like the minister-president, even though most of them are idiots. Only a few semi-government jobs (e.g. board positions at the banks, power companies, healthcare institutions) pay even higher.

It’s easy to understand why these media mobsters are paid so well: they spread (and sometimes maybe invent) the daily lies and fraud that are vital for keeping the sheeple in check and the zombie economy alive and kicking.

+1

when public sector jobs pay more than private, the fix is in and the decline is sure. However, it will be a long and painful descent (a few sheeple at a time) not a fall off the cliff.

Dutch?

I’ve often thought that the alums could turn around the corruption and decay of the academy within a year by simply organizing and making it a public campaign to stop donating and write them out of their wills. And they should. But football stands in the way. What kind of a utter moron thinks that a public university is worthy of charity, anyway?

Where’s my foam hand? We’re number one! We’re number one.

if 1 bank in europe can still function with hundreds of billions of non performing loans, let alone multiple banks. if half the companies in china cant even make interest payments on their debts and they are still in business what a few trillion dollars in the US? here in canada private debt to gdp is something like 250% plus, how long will it take for this to happen here? if its not here already. let face reality does it really matter? if everyone just goes out and gets a massive loan borrow way beyond our means and never look back, the world would seem a lot brighter. solve most of our issues. money is free. well if you know the right person for the rest of us its next to free.

wolf what your opinion a steve keens idea about debt jubilee?

Of all the economic ideas I hate, I hate “debt jubilee” the most. It’s vicious noxious propaganda, issued by those who owe the most, at everyone’s expense.

There is an established process that will solve this debt problem without the toxic debt jubilee nonsense: bankruptcy. It will destroy the wealth of creditors who’ve already been paid to take that risk (via interest income). That’s how it should be. And that’s the way to do it.

Have you actually read Steve Keen on the subject?

It’s not what upsets you. It’s at nobody’s expense. Because Monetary Sovereign governments are not restricted in their ability to buy debt they will buy the debts. Those who have been sensible and avoided debt would get an injection of money as well to compensate;

This is precisely what KILLS me. You think it’s at no one’s expense when the central bank (“monetary sovereign”) effing PRINTS the money to pay off select creditors in a debt jubilee. That’s what makes this so repugnant and such an ASININE idea. But that’s the only way you can pull off a debt jubilee. Otherwise it would just be a default.

But when you print the money to pay off creditors, EVERYONE PAYS, including those who neither owe nor own the debt. Why should I bail out Warren Buffett? or anyone else who borrowed too much or owns too many defaulting bonds?

Quit harassing me with this propaganda. This idea needs to die.

In other words, a debt jubilee will make the next debt jubilee which will surely follow even bigger.

It’s a stupid idea like fighting a debt problem with more debt, but I digress.

Our whole civilization will have collapsed before any of that. Remember we have ordained it by our consumption. We cannot grow indefinitely in our finite world. The economy cannot go into reverse. It just collapses. Every post Wolfstreet has demonstrates it’s happening. Slowly now but then [when?] fast.

As Jan Baudrillard says;

“Prophesying catastrophe is incredibly banal. The more original move is to assume it has already happened”

It started in 1971, Gail Tverberg “Our Finite World”agrees with that date.

“a debt jubilee will make the next debt jubilee which will surely follow even bigger.”

Except that bigger BS Jubilee, will be Hyperinflation like never seen before, followed by total financial collapse. Think Zimbabwe to the power of 10,000,000 +.

As a BS jubilee, would involve the printing, of 100’s of trillions of $.

The printing presses, and Data entry clerks, would not be able to keep up.

@d:

don’t worry, thanks to the coming ‘cashless society’ the BS jubilee will happen in an instant, the recent ‘Pounding’ of the British currency will be a slow-motion event compared to it.

All you ever worked for magically erased in one moment. No need for printing presses, clerks or politicians to keep up. Everyone will be poor except those who make the rules (and the people behind the scenes who tell them what to do).

1 second after you enforce a cashless society.

The rest of us will be using, shark’s teeth, or greenstone, or oz’s of Kauri Gum (Amber), or some such.

The fools in the city’s will have a problem, the rest of us, will still have ways of getting food, outside the cashless society, so wont.

You can force the city’s to pay tax with electronics, just as you force them to pay tax with money, you can not stop an alternative/parallel system.

There will never be a completely cashless society, as it completely takes away, all peoples self determination, when you do that.

Enough of them will revolt, to be a big problem. Every time.

I couldn’t agree more!! A debt jubilee is total nonsense, as there will most certainly be someone left holding the bag, for example a pension fund or even a charity and/or the debt forgiveness would creep into and be reflected by the currency or economy. It already is reflecting the ridiculous and disastrous consequences of ZIRP and NIRP.

The debt (including its time or lending value) must be resolved. A first year accounting class teaches this basic principle: For every credit there must be a debit and vice versa.

I’m glad you commented on this because I noticed this was brought up in a comment on one of your previous articles and I couldn’t quite articulate my opinion but yep, nonsense is a great way to define it.

We try hard to keep this place an Adolf free and Racist/Discriminator free, zone.

Should it not also be a “BS Jubilee” free zone.

BS jubilee, is simply Taker “Anti Rich” Propaganda, of the worst order.

It can not work without economically destroying everything around it.

Simpler to Bankrupt all the Debtors, liquidate the remnants of their holdings, then ban them from obtaining more credit, until their death’s.

Whist at the process. Outlaw the ability, of Creditors, to enforce Debt, Against Descendants.

Get over Ayn Rand’s farcical philosophy and grow up, please!

The people who need to grow up.

Are those promoting.

A completely financially untenable, and unworkable, taker debt jubilee.

I dont have any debts. Why should I have to subsidise you, through taxes, and having my financial reserves devalued, as you dont want to pay your debt’s.

The problem is not Capitalist, or the 1%.

The problem is the Socialist, Communists. and those who live on credit (they can not afford). Whilst demanding somebody else pay their way for them.

The point of the post was.

Take your BS Jubilee C#$P Propaganda, elsewhere, along with Adolf, and all Racist, Bigots, and Discriminators, we as a community dont want it here. neither does wolf.

Besprechen

Hitler, Racist, Debt Jubilaum,

Heir ist. VERBOTEN.

was just curious. i like to read and listen to a lot of different opinions. especially how things seem to be shaping up i like to hear a lot of predictions of outcomes. things might get really bad and sadly not many people actually know what may be in store.

wolf who do you like to read? follow?

agree.

A debt jubilee would reward bad/stupid behavior and make sure we are stuck with a dysfunctional economy for at least one more generation.

However, I’m afraid that bankruptcy of all the speculators would also bankrupt all the savers, something they didn’t sign up for when they parked their money at the bank and a risk they definitely were not paid for either. Here in Northern Europe, rates on savings accounts have been at or below inflation from the moment the euro currency started) while the risk has been steadily increasing and there are no good alternatives (I should have parked all my money in gold in 2001, but that’s in hindsignt …).

The time to buy Physical Gold, was when it was under 300 Oz.

Now is a time, not to have your cash reserves in a bank , even in the US. One should never be close to the FDIC limit, if one wishes to hold in a bank, and keep Blind faith in FDIC.

Everybody relies on FDIC, this is fine, until the big one hits, and then the only way they can fund FDIC, is to print it.

Result, Hyperinflation.

Unless they dont pay out, the full sum in FDIC.

I always though. I would be dead and gone before the big financial implosion occurred.

The way the: Eu, ECB, china and the PBOC, are playing, I may be wrong on that.

“if half the companies in china cant even make interest payments on their debts and they are still in business what a few trillion dollars in the US?”

You can’t compare how the Chinese or Japanese deal with debt to how US companies deal with debt. In the case of China, most debt is money borrowed from the government, given to state owned companies.

In Japan, most Japanese debt is owned by the Japanese.

I think it unlikely that Chinese state owned companies will ever be forced to pay back their debts or default for lack of payment. China is more stable than the USA in that regard.

Much what I read about these Chinese business loans sounds similar to the free ‘starter loans’ that our government doles out to countless well-connected entrepreneurs and the huge and totally useless subsidies for big companies (e.g. the billions of carbon credits for power companies) . It is all just free money, at worst you may have to pay some of it back if you make loads of money thanks to the loans.

Of course, many of the new ‘entrepreneurs’ spend the starter loan on a nice office, big salary, wealthy lifestyle, Porsche company car etc . They continue this until the money runs out, and then come back with another ‘innovative’ idea. At least many of the Chinese companies are trying to produce something that is a bit useful for society.

I would like to point out that the big dip ending in Oct 2010 was not due to business/corprate borrowers dutifully paying off their loans, but rather that said businesses/corporations defaulted on their obligations and the loans were written off, hence no longer appeared as a loan balance.

I’m writing this to counter the common but false narrative that there was a lot of “deleveraging” after the crisis hit in 2008, which falsely implies that borrowers (private and corporations) were paying down their debt. They did not. The dip was because write-offs exceeded new loans, and by a significant amount.

Note also, as Wolf mentioned indirectly above, that the current dip in debt again is because writeoffs (for bankruptcies is a proxy) are exceeding new debt added.

My understanding is financial institution equities are more liable to rally once writeoffs are processed. That is, the stock tends to fall as writeoffs accumulate.

That is probably be true, and I think we are not disagreeing/ However, the point I am making is about something else, and I will iterate it here just in case it was not clear: Various propagandists have been pointing at the drop in debt balances as a sign that debtors are doing better and debts are being paid off, and that happy days are here again. My point is that debt balances dropped because they were written off as losses. The debtors did not pay off anything. And then new debt was taken on, making the curve rise again. Also not good news, since more debt is what caused the 2001-2008 bubble and debt crisis in the first place.

The interesting questions now is what is the end game of the corporate debt bubble. Clearly the banks have something in mind. They are not stupid, just evil. My guess is banks will take over the indebted corporations for pennies on the dollar once the inevitable stock market crash happens. And, as chicken says, that will happen when corporate debt writeoffs reach critical mass.

“My guess is banks will take over the indebted corporations for pennies on the dollar once the inevitable stock market crash happens. ”

Yes this is also my suspicion. Not publicly traded banks necessarily, private interests are driving this bus.

Energy companies emerging from BK are owned by the banks, debt for equity.

Unwind implies control, at least it’s not Unraveling or exploding? Maybe it already exploded?

I’m unsure of the correct order of nomenclature that would justify immediate concern.

Because of the all their tricks, they are making money into something arbitrary and meaningless. What’s going to happen when nobody believes in it anymore?

First, lets have a public audit of Steve Keens personal finances. If ANY of the banks/financial institutions he owes money will forgive his debt, then we go for it. Deal?

I have a better idea. Lets have a Regulatory and Taxes Jubilee!

Nobody pays taxes for the next five years. NOBODY. That includes corporate taxes. They don’t pay them anyway; they just pass them on to their customers. Only PEOPLE pay taxes.

No new regulations for the next five years.

“That includes corporate taxes. They don’t pay them anyway; they just pass them on to their customers.”

Not true. Income taxes are paid on income, not revenue. And corporations are liable for other taxes regardless of income or revenue.

It’s a weaselly way of trying to persuade people to support the repeal of taxes on corporations, disinformation long favored by terminally venal corporatists. And you fell for it.

Huh?

Do you honestly believe a for-profit enterprise will pay even one penny OUT unless that amount is coming IN to them from whatever product or service they sell? Yes, this does assume they’d like to stay in business. Or do you think they don’t care if their payment obligations exceed their income?

“Taxes are not the price we pay for civilization. They are the price we pay for politicians to play Santa Claus so they get re-elected.” – Thomas Sowell.

“Do you honestly believe a for-profit enterprise will pay even one penny OUT unless that amount is coming IN to them from whatever product or service they sell?”

They do it all the time. Hence the title of this article.

Do you really suppose corporations will reduce their prices, or invest more in the U.S., if their taxes are reduced? The experience of the last 30 years, at least, is that this is not at all the case.

Property tax comes to mind. Youve got to pay it no matter what your income or revenue or anything else for that matter. Taxes on automobiles in the form of registration is similar. I guess any tax that is imposed for just owning something would fall into this category. I’m sure there’s others.

“Do you really suppose corporations will reduce their prices, or invest more in the U.S., if their taxes are reduced? The experience of the last 30 years, at least, is that this is not at all the case.”

Static analysis. The rest of the world has not stood still.

“•The United States has the third highest general top marginal corporate income tax rate in the world at 39 percent, which is the same as Puerto Rico and is exceeded only by Chad and the United Arab Emirates.

•The worldwide average top corporate income tax rate (accounting for 173 countries and tax jurisdictions) is 22.9 percent, 29.8 percent weighted by GDP.

•By region, Europe has the lowest average corporate tax rate at 18.7 percent (26.1 percent weighted by GDP). Africa has the highest simple average at 28.77 percent.

•Larger, more industrialized countries tend to have higher corporate income tax rates than developing countries.

•The worldwide average corporate tax rate has declined since 2003 from 30 percent to 22.9 percent.

•Every region in the world has seen a decline in its average corporate tax rate in the past twelve years.

It is well known that the United States has the highest corporate income tax rate among the 34 industrialized nations…”

http://taxfoundation.org/article/corporate-income-tax-rates-around-world-2015

@ ERG:

“•By region, Europe has the lowest average corporate tax rate at 18.7 percent (26.1 percent weighted by GDP). Africa has the highest simple average at 28.77 percent.”

Yeah right … that’s why so many US companies officially register in the Netherlands and pay (almost) ZERO taxes while smaller Dutch companies are bled to death with a 30-40% tax they cannot avoid. These official tax rates tell you nothing, how many US multinationals are really paying that high US tax on all their US activites? I bet exactly ZERO.

For multinationals, official tax rates are irrelevant; paying taxes is for the little people, for those without lobbying and other political representation.

this comment section should have its own talk show like Dick Cavett’s.

I was going to reply to JUSTME but decided to make a more general comment. My husband lost his small business in 2008 when the bank pulled his credit line and left him unable to complete several projects. They did this to every business owner we knew that closed their business. He would have had to close the business anyway, because it was construction related, but they made it impossible to simply unwind it to a close.

In 2008 the banks forced viable businesses into bankruptcy. We know plenty of people like that, including a guy who employed 75 people in a family business inherited from his father. That guy was making $14 an hour, and lucky to be working, when we met him.

The banks may be doing it again. These people are not smart, just greedy, and cowardly to boot. If loans are declining it may be them pulling the plug, and possibly causing the crisis. If I were in the markets I would be unloading the big bank stocks by the boatload.

Your husband’s problem was that he didn’t owe the bank enough money. If he had owed the bank, say, $2 billion, they would have worked with him and helped him stay in business for as long as possible because they wouldn’t have wanted to take that big of a loss. But the small guy gets fried.

I always wondered how wage increases everyone’s calling for can be justified, this doesn’t explain.

Exactly. Another way is to not use banks, difficult in many biz sectors. I think I noticed that cash on the balance sheet went way up in US corps after the 2008 blow-up. With the collective memory of about a week in this country, i’ll bet the cash is mostly gone now, spent buying back shares, what a great idea…

… we’ll just ride along ’til the wheels fall off … then … use politically correct financial word substitution and replace fall off with unwind ‘n keep on truckin’ ….

What can be seen in the credit markets, does not surprise. Excess speculation in the energy and tech sectors by use of leverage, is now in the process of being written off. With bankruptcies and resultant direct job losses being significant, as are the ancillary job loss.

What cannot be seen in the above ground banking system, is what forms “surprise events” from the shadow banking system. In particular the global private equity sector. The amount of global revenue taken out of the system, when adding in the knock-on effect, is substantial at about 10 to 15 trillion dollars. The direct effect is the cliff drop in exports and imports, bringing global trade to a snails pace.

When there are falling profit margins, the Feds LMCI being negative, CAPEX growth negative, and the speculative default rate is above 5.5%, then without exception, here is a resultant recession.

And who is suffering from all this corporate debt that is going bad? That’s right, bank depositors who got only 0.1% interest since 2008 so that banks could use their resulting much improved interest rate spread to earn themselves out if their loan losses.

It is the old order that is in recession The old metrics are no longer relevant. Snag for policy makers whose only remedy is to cheap money is there are not enough new order ideas to profitably carry the old order.

And why should it? Not a lot if point in progress if it ends up getting stuck in the past.