“Fears of an impending liquidity crunch in that asset class.”

“What is happening in this space today reminds me of what happened in mortgage-backed securities in the run-up to the crisis,” U.S. Comptroller of the Currency Thomas Curry warned in October about the auto loan bubble.

And his warning is now becoming reality.

Subprime auto loans aren’t big enough to take down our megabanks, the way subprime mortgages had done. But they’re big enough to take down specialized auto lenders and cause a lot of tears among investors that bought the highly rated structured securities backed by subprime and deep-subprime auto loans that are now defaulting at a rate last seen during the days of the Financial Crisis.

And they’re big enough to knock the auto industry, one of the few booming sectors in the otherwise lackadaisical economy, off its record perch. An auto-loan implosion would start at subprime and work its way up, just like mortgages had done.

The business of “repackaging” these loans, including subprime and deep-subprime loans, into asset backed securities has also been booming. These ABS are structured with different tranches, so that the highest tranches – the last ones to absorb any losses – can be stamped with high credit ratings and offloaded to bond mutual funds designed for retail investors.

Deep-subprime borrowers are high-risk. Typically they have credit scores below 550. To make it worth everyone’s while, they get stuffed into loans often with interest rates above 20%. To make payments even remotely possible at these rates, terms are often stretched to 84 months. Borrowers are typically upside down in their vehicle: the negative equity of their trade-in, along with title, taxes, and license fees, and a hefty dealer profit are rolled into the loan. When the lender repossesses the vehicle, losses add up in a hurry.

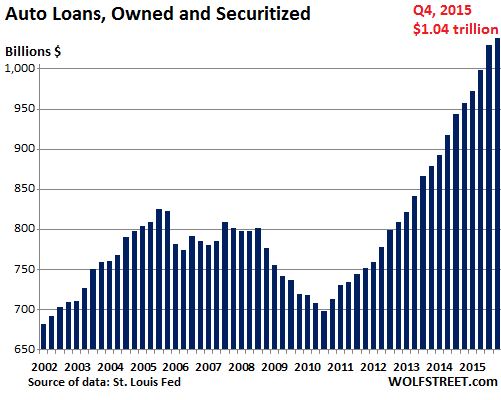

Auto loans in general have been in a huge boom that reached $1.04 trillion in the fourth quarter 2015:

Equifax reported last year that 23.5% of all new auto loans where to subprime borrowers. So unlike the mortgage crisis, subprime auto loans aren’t in the trillions, but in the neighborhood of $200 billion. Many of them have been repackaged into asset backed securities. And these securities are starting to implode.

Auto loan ABS delinquencies reached 4.7% in January, the highest since February 2010, according to data from Wells Fargo, cited by Bloomberg. During the Financial Crisis, delinquencies topped out at 5.4%. During normal times, they range from 2% to 3%.

John McElravey, head of Consumer ABS Research at Wells Fargo Securities, warned that these delinquencies would entail a wave of defaults. The default rate is already skyrocketing. It hit 12.3% in January, up from 11.3% in December, the highest since 2010.

He pointed a several factors, including initial jobless claims in oil states like Texas. The data are worth watching closely, he said, “especially against the backdrop of sub-par economic growth.”

Skopos Financial in Texas is a master at securitizing subprime auto loans. Private Equity firm Lee Equity Partners owns a 97% stake. When Skopos “opened its doors” in 2011, it had “one goal in mind,” as it says on its website, namely, “making tough, deep subprime auto loans easier to finance for dealers.”

In November, it securitized $154 million of subprime and deep-subprime auto loans. Citigroup was the lead underwriter. Over three-quarters of the loans are to borrowers with credit scores under 600. And another 14% have no credit score at all. The highest tranche was awarded lofty ratings of A from DBRS and AA from Kroll Bond Rating Agency.

In this manner, thinly capitalized lenders that came out of nowhere, like Skopos, are offloading the risks to institutional investors, such as your bond mutual fund.

But now, only three months later, Asset-Backed Alert reported that the securities have already “experienced enough collateral defaults to approach a ‘cumulative net loss ratio trigger event’ set by Kroll. Should losses reach that level, Skopos would have to stop collecting excess cash flows and redirect the money to bondholders.”

This would make it “difficult” for the company to keep “doing business as usual” and “virtually impossible” to raise more capital through securitization of its subprime loans.

Sources said other deep-subprime lenders including Go Financial and United Auto Credit face similar pressures due to rising losses among the loans underpinning their securitizations.

And this lightning-fast deterioration of the collateral for these securities is “feeding fears of an impending liquidity crunch in the asset class.”

“For these smaller firms, securitization is their only source of funding in this space,” one source said. “It only takes one deal of theirs to go sideways in terms of performance and they can impact the whole subprime-ABS market.”

The point of building a net-loss-ratio trigger into a deal is to protect bondholders, so investors holding Skopos’ paper aren’t likely to be affected by weakening collateral. But increasing delinquencies and losses among deep subprime borrowers across the board are adding to concerns that the industry is vulnerable to a “perfect storm” of market forces including deteriorating credit quality, declining vehicle-resale values, and rising interest rates.

Hedge funds are already smelling the next “Big Short.” And they’re trying to figure out – though it won’t be easy – how to bet against these securities and against those bond mutual funds that hold them, and that may eventually be forced to dump them into an illiquid market.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

‘Wolf of Wall Street’ Jordan Belfort’s 1991 Ferrari Testarossa for sale

A barely driven Ferrari once owned by the real Wolf of Wall Street is now up for grabs.

Jordan Belfort’s white 1991 Ferrari Testarossa has just 8,000 miles on its odometer, and comes with the name and address of the former penny stock scammer.

Belfort — bought the Italian beauty from Kessler Motors in New York.

Monaco-based dealership Monegasque Classics Sarl is only offering a price on request — and may just put it up for auction at a later date.

Wolf this one is for you ;)

I’ll make them a deal: the Testarossa for 1 month worth of WOLF STREET ad revenues.

Wolf,

First off, thanks for the informative site you have. I’ve been a reader for several years now including commentary but have never posted. I traded commodities for 6+ years in the mid 90’s into the early 2000’s & have studied the technical & fundamental aspects of the ‘markets’ for well over 2 decades. Way back in the day I was looking for the big plunge (economically speaking) but eventually realized it would be a slow grind into the abyss along with occasional ‘explosion’.

This article exemplifies the slow grind to me. I’ve been checking these auto finance stats out for awhile now & it has been clear all along where it’s headed. Chitigrope- lead underwriter re Skopos Financial – figures. At a little over a $trillion, I wonder what the real numbers have been cranked to when you add up the ‘securitization’ factors in?

Thanks again for the site!

Bigfoot

“Slow grind” is a good term. I’ve been writing about these things, including auto subprime, for a couple of years, and what was just a hint back then is now glaring, but it’s still moving forward, with some things falling off the cliff, and others hanging in there. I try to sort it out the best I can and as early as possible. I don’t always get it right, though.

:-]

It’s a colossal brake stand. Tires screaming, but the car isn’t moving anywhere. ‘Cept a little sideways maybe.

Huge government deficits keep the hammer down, while the consumer is loaded to the gills with debt keep the brakes on permanently.

When problems show up, people like Jack Lew come out and say ‘don’t expect any help…’ But when Wall street screams loud enough, there will be congressional action, and a massive deficit increase, to keep the fuel coming.

Yeah it’s not going to end well and no it’s not different this time.

Low income and those with poor credit get whacked again with exorbitant interest rates and 6 to 7 yr loans.

At least it’s easier to repossess the cars as the cars with loan balances often have remote wireless kill switches – call it modern day repo man – which kills the engine even when it is moving.

I was saving up for a late 70 model Ford Ranger (HighBoy) when a deal fell into my lap I couldn’t pass up. All these new cars have so much electronics on them that they are (1) too complicated to work on, and (2) can be very quickly legislated off the market. And they will be driverless before too long (I heard one of the Euro companies is getting rid of car keys – have to use your cell phone – am not shitting).

http://www.technobuffalo.com/videos/audi-mobile-key-hands-on-this-android-app-turns-your-phone-into-car-keys/

They are talking (depends on adoption I am sure) about permanently removing keys from some models – cell phone app/key only – in maybe three or five years.

That said, my old man has been considering buying a used car for a while and I keep telling him to wait a year or two – when this bust hits there will be SO MUCH secondary inventory, much of it new, low mileage, and probably way under book value.

Also, one last piece of advice, I ask USAA (loan officer) what book value is when I buy used, based on the VIN – and act based on their perceived loan value – not what the dealer (or KBB, or Edmunds, or whoever) says the vehicle is worth.

I pretty much loathe car ownership at this point. I hate the whole system.

Regards,

Cooter

I remember a simple headlight change years ago….. brought on by helping a guy change a headlight on a new Malibu….had to pull the whole front cap off just to get to the light. No kidding.

Here in the UK bmw have a X model that costs a £1000 to change a sidelight. The front of the car has to be taken to bits to do the job.

Looked at a nice C class Mercedes wagon from the mid-2000’s at a price almost to cheap to resist. It featured a complete absence of a dip stick to tell if the engine was running dry of oil. Electronic read-out on the dash only, and a reputation for a fault prone electrical system. Electronically controlled seats locked in the forward position. $500 wasn’t cheap enough!

Planned self destruction isn’t a new concept!

Right there with ya regarding car ownership. I live in the sticks & have to commute so it’s an expensive necessary evil until I can get my own gig going again (might just be subsistence farming on a couple acres the way things are going.)

Staring at 60, I miss the days when a well stocked 20″ tool box could almost always fix whatever mechanical malady you encountered. Rebuild kit for your carb with a kit or change a fuel pump by removing 2 bolts on the side of your engine block and a good ole analog multi-meter & timing light could cure your electrical/ignition ills. (pissed me off when they started putting electrical fuel pumps inside the damn gas tanks!) The new vehicles are great- when they work.

Cash for clunkers removed a lot of good iron from the market. One of my all time favorite rides I owned was a 1967 Mercedes 200D. Slowest car I ever had (topped out at 80mph going downhill) with a 4 banger diesel putting out less than 60 hp. Built like a tank, it weighed around 3500 lbs, got about 40mpg (when diesel was cheaper than gas). Had about 300K original miles when I sold it & still ran like an old Singer sewing machine.

“I pretty much loathe car ownership at this point. I hate the whole system.”

Amen.

I just passed my 10 year mark of not owning a car. (By choice..)

I rent occasionally and do Zipcar rarely. Fortunate personal circumstance… I know many can’t swing this.

As a car outsider I see the whole thing as such a racket these days… they get you with so many tickets, regulations, insurance… increasing engine complexity means drivers are ever more dependent. A whole apparatus is set up to extract your earnings.

http://www.brickhousesecurity.com/category/counter+surveillance/gps+detectors.do

and all the other toys they have.

Every neighborhood has a cash removal service for these Shut down units.

And everybody knows when the repo man may be due.

The devices locate vehicle thru GPS and disable the starter. They do not shut off car while in operation.

Car buying in the teeth of a recession/depression…?

We desperately, desperately need to see major job losses. That is about the only thing that will knock sense into into deliriously perma-optimistic North American consumers…

Kred… You are a wide eyed optimist. :) I’m not sure those addicted to endless debt and the latest greatest will learn even if they are required to donate an organ as part of the car deal. It does look like we are in the middle of a job loss increase as the O&G sector unwind picks up speed. Many high paying jobs are being lost and may not return for a decade, a generation, or ever.

Keep calm and carry on!

“Major job losses” with the labor participation rate at its lowest for nearly 40 years? You must be a economics professor, or worse, someone who believes the headline unemployment numbers.

Your article triggered the ad mechanisms to show me ads for local dealerships. Camelback Subaru even says ‘ Zero due at signing!’ right below your bit about this being similar to no money down mortgages. Perfect!

I was presented an ad for an Infinity. I could buy one but then never make another mortgage payment. :)

Great site. Daily reader.

“Hedge funds are already smelling the next “Big Short.” And they’re trying to figure out – though it won’t be easy – how to bet against these securities and against those bond mutual funds that hold them, and that may eventually be forced to dump them into an illiquid market.”

They should just short General Motors.

At least many of those financing their homes with subprime mortgages and liar loans were borrowing at low teaser interest rates, and they did so under the illusion that they were buying an appreciating asset. Subprime auto buyers know that they are buying a depreciating assets at a high credit card-like rates. The walk away factor was baked into the cake before the cars were driven off the lot.

The bridge is out! Another slow motion train wreck. Slow motion until it goes over the cliff.

These ABS are structured with different tranches, so that the highest tranches – the last ones to absorb any losses – can be stamped with high credit ratings and offloaded to bond mutual funds designed for retail investors.

Kinda like wrapping up dry horse manure and selling it as truffle! Nice!

in the oil bidness, we call it polishing up the turd…..

You could, if you wanted, look at money as a societal illusion/delusion… as one guy said: economics is the world’s last and biggest religion.

We basically have a set of agreements, that if a number in a spreadsheet column gets too high or low, a series of contractual consequences result from this happening. Bail-outs are interesting, because the laws of economics are temporarily suspended and companies or individuals are granted a kind of divine grace, from the economic center of the universe, that is the currency monopoly by a fiscally sovereign entity.

Which begs the question: if they can be suspended at any time, in what sense are they laws? Austrian economics is largely posited on a “day of reckoning” scenario that borrows quite obviously from biblical prophecy to portend a future final doomsday… which, we are told, cannot be postponed… But what if it can? What if it can be postponed forever, because there is no second coming, just like most of know that there is no literal enforcement of Biblical old testament law.

Each austrian-inspired blog I read writes in a vein of ….”Wait to see what happens when Daddy Market gets back… You’re all going to be in a lot of trouble then…” (WOLFSTREET not included, of course ;) )

Isn’t the fact that we got this far evidence that it really is a delusion or an illusion? Solvency is a number in a spreadsheet, isn’t it? And the new laws of physics — oops I mean the new laws of economics — point to the fact that a central celestial body does in fact have God-like powers: it has the ability to create currency. That is the single most important driving force within this system: the point at which new monetary units enter the system.

And the idea that the money supply should not expand, while population expands, technology expands, everything else expands – where did we get *that* crazy notion? From the scarcity theory of value…

Perhaps we ought to have an increasing money supply.. and perhaps we ought to do that democratically and universally, in the form of a universal basic income. That’s my view, anyway. It means everybody gets 1000 dollars a month just for being a citizen. End rant, I guess..

And if it doesn’t matter anyway, could I just get $10,000 a month? The thing is, I live in San Francisco, and you can’t even rent a tent for $1,000 a month.

What you mention is an ongoing point of discussion in the UBI community ( https://www.reddit.com/r/BasicIncome ).

Its definitely a tricky thing, but the consensus seems to be that the importance of having a UBI *at all* is more important than having it achieve immediately its goal of livability for people in high-priced environments.

The US congress and senate were on the verge of passing a UBI bill in the 70s under Nixon, and it fell through because people thought it *wouldn’t be enough*. So now we have no UBI. The community seems to be of the opinion that not repeating that mistake is very important. Its more important that we get that first 500, or 1000 dollars, or whatever we can, than that it be a truly universally liveable income for people in all areas of the country.

You aren’t actually taking all this seriously, are you?

so what if people all got a basic income and most all decided to stop working? Where does the money come from?

I believe this is actually called “helicopter money” and its arrival heralds the imminent and unstoppable demise of your economy.

ucde- I think you hit it. A delusion, fueled by an illusion, caused by a contusion. Reflecting on my beliefs from the 90’s, if you had told me we would see a time when ZIRP, NIRP, & a $20 trillion debt would be possible, I would have deemed you insane & assured you we would have imploded long before such ridiculousness could happen.—– But alas, here we are.

I just keep searching for the most plausible monetary re-set scenario. Seems like we will have some sort of worldwide debt jubilee. Best I can figure, ‘they’ will keep things limping along until it’s to ‘their’ benefit not to & accompanied by lots more war. Unfortunately, we aint in the club

. You’ll get your $1,000 about the time it buys you a loaf a bread, chunk a cheese, & a jug of milk.

Ucde you kind of knocked me off track. We all know Economics is more art than science. But even art deteriorates. Jack the Dripper comes to mind. Doomsday, Ragnarok, or Armageddon is hardwired into our DNA, and those scenarios are merely reflections of that. Hi tech IS a religion, but I remind everyone of The Book of Bokonon 1:1 – “This religion, like all religions, is a pack of lies.” LLAP?

If the sub-sub prime car loans are paying 25% interest, the lender will get half the value of the car back in a couple of years, come hell or high water. If the borrower defaults and is repoed, the lender gets back the total value of the car (minus depreciation) along with whatever flesh was taken off the top in the form of usury.

I dont see how this is a risk to anyone other than the poor schmuck who could not get a decent interest rate and a 48 month loan. Auto loans are well secured. Auto pricing is in a reasonable range. And if there is a local surplus of repo vehicles, cars and trucks easily move to markets where demand is more robust.

It is certainly not a risk to the banking system.

otoh, during the mortgage bubble, liar-loans were going out at 120% of an inflated property value. After the market collapsed, the foreclosed properties may have been worth half of what the peak loans were written at. There are still a huge number of upside-down mortgages remaining from 2008. But the total is down from 30% to 15%, so even there the systemic risk is easing.

The biggest risk to the financial system today is the price of oil. If it can stabilize at 30, we squeek through. But if it drops into the teens, there will be hell to pay in the banking sector. Given the ongoing oversupply in global oil, the oil price can crack at any time, and the markets go south.

Be careful out there!

So here’s a simplified calculation:

If a deep-subprime customer buys a new car at retail for 25,000, rolls $3,000 in negative equity of the trade-in and $2,000 in title, taxes, and licence fees into the loan, the total loan will be $30,000. If the lender repossesses the car a week later and then sells the car at auction (typical), it might only bring $19,000 (wholesale value of a used car). But the loans is for $30,000. So the loss = $11,000 plus all the expenses of repossessing the car, prepping it, and selling it at auction.

In your scenario, two years later, the car might be worth $14,000 at wholesale. If the lender “collected” 20% interest per year for two years on $30,000, that’s about $6,000. So they’re about $10,00 in the hole. Plus the expenses.

On a beaten-up cheap used car, the loss might be much smaller, if they get the car back in one piece.

Also note all these profits (and losses if a default) are spit up between the dealer, the lender, the underwriter of the asset backed security, and the ABS holders.

Saved me the job and did it neater.

You forgot another big cost, depending on the jurisdiction, they have to hold it for somewhere between 30 and 90 days before they can cash it up. Near new car must be in undercover secured storage.

Cars are a Liability. Any way you look at them.