During the worst time of the year?

This is anecdotal evidence – a personal observation, numbers I counted myself. So it’s reliable, and you know the source. But it is not statistical data. It doesn’t cover the entire city, just a small part of it. Yet it’s so unusual, so striking, that I decided to share it.

I advise caution using this observation. It needs to be confirmed by data. But if it is confirmed, San Francisco’s crazy Housing Bubble 2, which is so much crazier than the prior housing bubble that blew up in 2007 with such spectacular results, is going to have a problem.

Today I walked to the Kaiser medical facility, 8 miles round-trip, from where we live near the bottom of Russian Hill facing Fisherman’s Wharf to Geary and Divisadero. I chose a loop to avoid walking the same way twice. On the way back, I crossed Pacific Heights near the highest point because it’s a gorgeous area, with splendid views, and some of the most expensive housing in the city.

Minus the two stretches of the route at the beginning and at the end that I walked out-and-back, I pounded 7 miles of different sidewalks. There were also some commercial strips with few or no residences, and two schools. So that’s the route: about 6 miles through different residential areas.

The first realtor sign was on our block. When I saw the second realtor sign a few minutes later, I started counting. I walk everywhere in San Francisco. I see realtor signs from time to time but I might go weeks without seeing any. Sometimes I see two or three on the same walk.

I walked this route many times, for years. I know it inside-out and notice things that are different. And today it was different.

By the time I got back, I’d seen 14 realtor signs, advertising 15 units. San Francisco is on sale.

Last time I’d seen that many units for sale in such a short time span was during the Great San Francisco Housing Bust in 2008-2011. And even then, it wasn’t often that I’d seen that many in such a short span.

At the top end today was a property at 2505 Divisadero, at the top of Pacific Heights, with an asking price of $11.85 million.

These were just the units with realtor signs in front. Not all units are sold via realtors. And not all units sold via realtors have signs in front of them. So these 15 units are just the visible part of what is for sale on that stretch of sidewalk.

Today’s route went through older neighborhoods. They’ve been untouched by the phenomenal construction boom that is currently snarling traffic in other areas of the city where condo and apartment high-rises and medium-rises pop out of the ground like mushrooms. Those units are new supply. They’ve been hitting the market this year. Many more will hit next year. And even more in 2017.

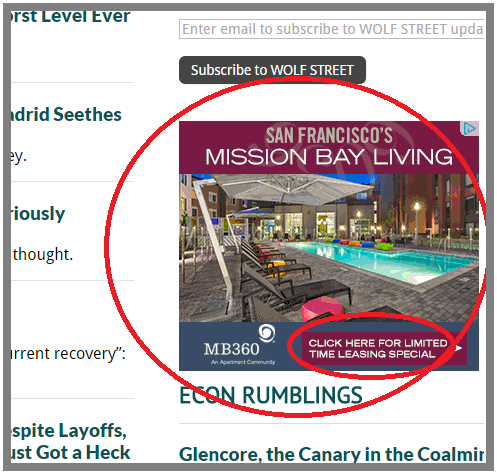

On the leasing side, we’re suddenly seeing – once again – promos with giveaways to entice people to grab one of these units. Here’s a screenshot I took of an ad that ran right here on WOLF STREET on October 25, offering a “limited time leasing special,” namely “up to 12 months free parking or $3,600 off your 2nd month’s rent”:

This is a sea change.

But November isn’t a great time to sell. The housing market usually peaks in late spring or early summer, and then declines, with prices coming down often sharply in the fall and winter. This year, the median sale price of all types of homes peaked in May at $1,255,000, based on San Francisco MLS. By September, the median price was down to $1,150,000, an 8% decline. January is often the low point.

So why are they suddenly trying to dump all these homes on the market, during the worst time of the year?

Perhaps they’re seeing the writing on the wall. Layoff announcements have started to burst into the headlines. San Francisco’s darling, Twitter, which even extorted a payroll tax exemption from the city by threatening to leave when it was looking for larger digs, has started to axe people. Others are moving to Oakland and elsewhere because office space and housing are getting too expensive in the city. And suddenly, all this new supply of housing is coming on the scene – and for years to come.

Clearly, from what I’ve seen today, some folks who’ve been through this before want to get out of their properties at peak bubble prices while they still can.

It’s time for people who can’t afford to live here to make room for those who can, says the “real estate rock star” who is prominently and hilariously featured in this haunting video about Housing Bubble 2, and what it does to the people caught up in it… “Million Dollar Shack” In Silicon Valley (Video)

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

All bubbles create the conditions for their own eventual collapse. After a market conks out mortgage companies will no longer lend on the shacks they lent on during the bubble. In a bubble anything with an address will sell. It’s like every buyer becomes drunk and can’t think straight. I’ve seen foreclosed houses that I couldn’t believe anyone ever lent a dime on, and in some cases the same house would be foreclosed on 3-4 times as the market moved down over a period of years and wiped out a succession of buyers.

This is exactly how it went the last time as well. Sellers, sensing nearing a market top, or just plain “can’t believe how much it’s worth”, put houses on the market. They sit. After a few price reductions and no offers, they withdraw them from the market.

Some period of time later, a desire to sell turns into a need to sell. So now it goes back on the market, at a still lower price, and chases the market down until it either sells for an eye-popping low number or becomes a foreclosure. These “potential” sellers have now become “forced” sellers.

The flip side is the speculator with a few properties, or people who don’t have to sell. They’ll just sit tight and wait for the market to recover.

What’s amazing is that the last nationwide bubble, the first declared in a few generations (i.e. since the great depression) has repeated itself in under 10 years. Last time the post-mortem showed lack of lending standards (instead of the real problem – govt issuers Freddie and Fannie), wonder what this post-mortem will show?

This time, the post mortm will show that low interest rates forced investment cash into fixed assets with a yield vs bonds that don’t. As bond yields rise again, there will be less venture funding, less FDI, and thus less new jobs, less need for housing, and less pressure on housing. Low interest rates artificially inflated housing prices, enabling people to pay crazy prices. The moment those rates go up, lenders will Reset the appraised value. What matters is the cash flow, not the purchase price.

When people making over 100K live in a truck in the company’s parking lot, you know it is pretty much over. Time to go.

When the job market starts to tank, the housing market will soon follow…

I am seeing lots more signs in my town as well. Much more inventory than last fall. Love the narrative Wolf and hoping we are seeing the inflection point because I will go a little further than Petunia and say this crap needs to end.

There is actually a peak in new listings for District 7 every Sept/Oct, it’s weird.

Overall volume is down this year though.

The weather in SF is actually often at its best in Sept/Oct due to the “Indian summer.” My guess is that is why. 15 listings in 6 miles does not sound like that many to me, anyway. I am in complete agreement that the market is too hot but this doesn’t convince me that it is popping yet.

So now we have some October data: the bottom falling out of luxury housing in SF. See my new article, posted in the nick of time :-)

http://wolfstreet.com/2015/11/08/san-franciscos-luxury-condo-bubble-turns-into-condo-glut/

This could be it, and 8% decline in SF house, meaning the rats that bought at the top are desperately trying exit a sinking ship. The problem is, with renters paying 4-5K a month in rent, there is not much left to put together a down payment.

Also, From the LA times, “Fannie Mae, Freddie Mac detail plans for 3% down-payment mortgages”

It’s not going to help much if people are loosing their jobs in a collapsing economy. The stock market will eventually catch up to the real economy sometime next year.

The Fannie Mae 3% down mortgages won’t affect the SF market because the highest amount they can lend is 417K. From what Wolf writes this wouldn’t buy you a card board box in SF.

“…this wouldn’t buy you a card box in SF.” not today but possibly tomorrow. Tomorrow may come sooner than SF’ers thought.

I thought the limit was doubled during the crash, so it must have been temporary. Meantime, in Canada, the limit is 1M. Yet, the popular meme is that there won’t be a housing crash like in the US – because of prudent regulation. :)

Multiple unit properties have higher limits.

True, it is happening. But on the brighter side, nothing wrong with the correction. There are tons of people eager to come and start businesses right here in San Francisco. Some correction will make the business expenses, leases affordable for those entrepreneurs, which will mean more jobs, demand for services.

The problem is there ain’t no corrections. To quote Morgan Kelly (no relation) who predicted the Irish real estate crash- there are no soft landings.

The same hysteria on the way up works on the way down, Everyone runs to the same side of the ship.

There are only hard landings in real estate, The only question is how hard. Given that the bubble has now surpassed 2006…

PS to last: this is partly because of the leverage. No where else but RE can Joe six pack borrow 6 figures with 5 % down ( soon to be 3 apparently)

This means that a 10 % correction, par for the course in the stock market, puts a whole bunch of people into negative equity.

Leverage in reverse is, in a nut shell, why what would be a ‘correction’ in a stock is a crash in RE.

Interesting article Wolf. I’ve seen the same thing out in my formerly less-desirable neighborhood of SF outer richmond. There are more For Sale signs out here than I’ve ever remembered.

Numerous friends from the neighborhood and random neighbors have been pushed out to points afield as out here many of us rent single family homes which don’t have rent control protections. Its a very sad time out here for many of us; especially when those homes sell, then sit vacant or turn into obvious Air BnB places.

I was telling this to a friend about a month ago who lives near the Geary/Divis Kaiser buildings and she remarked that there were at least dozen places for sale w/in a couple blocks of her place.

Incidentally, her building went “Sale Pending” recently. She and her husband are hoping to hang in…

I hate to hear that. In Houston around the Montrose section I lived in, housing sales roll around routinely. But we don’t have a Prop 13 like you do in CA, which seems to slow the rolling sales.

You’ll know when it is really bad. When I first moved to Houston in 1988 I was STUNNED at the number of houses that were up for sale. Some streets it was almost everyother house. The crazy part of this anecdote? This was during the RECOVERY phase and within a couple of years, things were finally back to normal. I would have hated to see what it was like at the bottom of the market.

Wolf, keep walking and report back!!

Something is definitely happening. I lived 12 years in SF, about half in Cole Valley and half in Inner Richmond/Lake, and since I nearly bought in 2011, and chose to move instead, Ive been tracking the market for both rental and SFR sale. The prime Inner Richmond rentals have come close to doubling in the time I’ve been gone, but it appears that it might have inflated too far.

With any bubble, there is a lot of momentum, and as soon as something changes (reduced ease of vc money, minor layoffs) it can be all you need to change the momentum. The first thing you will hear is the attitude change; the can’t lose, it always goes up, gotta buy now idea goes from obvious to idiotic, and then the fear creeps in. Then people rethink the house they are overpaying, and the people that bought recently realize they are idiots. Then the inventory comes a rising, as for sale sits, and some people with sense realize it is time to cash out.

This time it has to be even scarier in a way, because some folks may know that it was something of a miracle that they got bailed out of the last bubble. Like my friends in the Fruitvale that paid 400k for a 1000 sq ft box in a bad area. Went down to 125k, now back at 400k. What do you think they are doing? I can assure it isnt likely they are banking on 500k next.

But back to the rental market…oddly enough, my old apartment from 2001-2004 is back on the market. In 2000, I rented it at 2200, and each of the subsequent years, wrote to the landlord that Id like a rent decrease, or would move out. She reluctantly gave in, but that was the power of the post internet 1.0 bubble bust. 2br condos in Cole valley at the time were 500-600k (they are 1.2m now most likely) but I had no money and knew that 0% down interest only loans were potentially a disaster (they were for 98% of the market, just not SF, and a couple of other places, but I digress)

Anyway, a couple of weeks ago, my old rental hit the market for $3200. And sat. Now it is $2999. Catchy, huh? And it’s not just that. It’s also the inner richmond places offering a free month’s rent, and other places with price cuts. I’m not close enough to the market to know what is happening, but I’ve been through two of these cycles there before, and Im sensing the same dynamic.

Wolf, I know what you are talking about, but I think it is still early. But if there is any more bad news on the VC front, or the unicorn dreams have their horns sheered off, the carnage in the market will be significant.

Thanks for the observations Wolf. It’s the roll-up of this that hits the numbers hard in 3, 6, 12 months. For what it is worth, a similar thing is happening in the Hamptons. Properties just aren’t moving (selling). Also, I’ve heard the summer rental market was very difficult this year. What’s important here is these are the wealthier neighborhoods housing the prime beneficiaries of the Fed’s ZIRP. Certainly it appears we have crossed the tipping point.

Here in Winnemucca Nevada, on I80, there’s lots of property for sale too, but, when I moved here 20 years ago, not a place cost over $100K, now half the properties are between 100K and 400K ! What a change ! Anyway, there is a housing boom in the 100K – 200K range for all those folks escaping the crime ridden big cities, SF, LA etc. Clean air, clean water, low crime, no traffic, 3 traffic lights total in town !!! When you are ready, we are here !

My view from the Mission District is that the bubble can’t pop soon enough. No fault evicted twice in rapid succession 10 and 11 years ago, we landed on our feet (barely) in a rent-controlled apartment in a larger building. What we paid for market rent then is probably no more than 30% of the going rate. Our current rent could get us a bunk bed spot in a room with two or other bunk beds.

The neighborhood is changing so fast that one has to check in on his or her favorite spots weekly to make sure they are still there. And the tents…..everywhere. The area under the 101/Cesar Chavez interchange is one of the fastest growing neighborhoods in the city, if not the entire state.

Let me mention the looks from the new people (what social value do they add with their new business ventures, like doyourlaundry.com or selfiemyass.biz?) at us poor oldtimers. Well, if looks could kill, I’d be dead many times over. And all they talk about is money because that is all they care about.

Pop goes the bubble and take you sneers back to mommy and daddy. Thank you very much.

I hope this bubble pops right in every snobby broker, Real Estate, startup and greedy landlords faces. So tired of hear the motto “If you cant afford it, you shouldn’t live here” crap. Everyone deserves a decent place to live that is affordable. If not, then what country are we really living in? It is despicable in my eyes to see how things have gone. This will be the third bubble I have seen as an adult and one in the 90’s that I didn’t really pay attention to since I was too busy going to college and getting drunk. The last one took my feet from under me. But, that was all my fault for listening to my ex who got real greedy and wanted to keep moving up in housing. And her real estate agent who kept saying prices will always be going up. What a joke. Greed crashed the last bubble and it will do the same to this new one. I just hope the damage is minimal for the middle class and below who stuck it out.

Be careful Lars. They’ll screw up Winnemucca just like they did Omaha!

I visited Omaha last year to visit friends and really loved it. I can see why people want to live there. Don’t worry; I will try not to let your best kept secret out!

This time it’s different…

That’s what I’ve been hearing and I live near Seattle. No bubbles here and that’s a quote…from the “this time it’s different crowd”. And you can take that to the bank though IF they were the ones that loaned the money to buy the bubble I’m thinking some of the banks could be in a bit of trouble again themselves.

But again, this time it’s different…

Well well well, I wake up this AM check on CNBC and what do I see?

‘San Francisco real estate in correction’

At this rate M. Richter will soon charge us for stock tips!

Not bad for a anecdotal stroll though.

Here in Denver, it’s the same story. LOTS of inventory popping up in the higher priced/yuppified neighborhoods. Seems the city dwellers are chasing the market down. Likewise, in suburban areas, I see a lot of for rent signs and some for sale signs. Apartment inventory is piling up everywhere, too, with tens of thousands (literally) of new units coming online or slated to be built in 2016 – 2017. We currently rent in a popular Denver suburb and got a decent deal after we told the landlord that other buildings were offering significant concessions: 8 weeks free rent, etc. Yet the media keeps on with the INVENTORY IS SO LOW! speech.

At the same time, and this is somewhat anecdotal, I hear stories from folks who are either moving back to the Midwest or the South (where they’re from) to escape the insanity that Denver and the Front Range have become. Either that or families are banding together and living in multi-generational situations or buying houses with people they barely know in order to cut housing costs:

http://www.9news.com/story/money/personal-finance/real-estate/2015/11/02/co-habitating-friends-roommates/75006674/

From CO Springs to Ft. Collins, you can cut the desperation with a knife as you drive around to see PRICE REDUCED! signs all over the place.

But I’m sure it’ll turn out just fine in the end.

I live in Bernal (rent) and there is tons for sale in Bernal/Noe area. Realtors say that the winter swings no longer apply… but I believe something might be changing. I heard from a lender than everyone with tech money bought 1-3 years ago, and there are fewer and fewer potential buyers with 10-20% cash down or more. The market is slowing down, at the least. I’m also hoping for a bubble. I’ve been here since the last one and the signs are certainly there.

Can someone please tell me why anybody would WANT to live in a Big Shitty? Been there, done that. Marina district of SF a couple of years after the Summer of Love. Portland, Seattle— even Vancouver BC— the only one I would consider living in again if somebody gave me a penthouse rent free.

Right now I pay $1100 in rent for a three bedroom timber frame house on five acres with a stream running past, 360 degree mountain view, and two of the best ski areas in North America within 45 minutes drive. Where? Send me $1,000 in cash and I’ll tell you!