Mega-startups go parabolic. Flame-out already happening.

It’s anecdotal evidence, but it’s everywhere in San Francisco and Silicon Valley. A neighbor was cooling her heels by the curb, suitcase next to her. She’s going to Europe on a “vacation-thing,” organized and paid for by her company, she told me. A team-building perk. She’s a coder at a startup, her first job out of college. When she moved in less than two years ago, trucks kept pulling up to deliver her latest acquisitions. One day, she gingerly parked a new BMW in the garage. As we were chatting about her trip to Europe, a limo pulled up for her ride to the airport. That too was part of the perk. No expenses will be spared.

This startup occupies super-expensive San Francisco office space that’s way too big for the number of employees. It’s embellished with designer furniture. Free lunches are de rigueur. All paid for with the boundless money it is getting from investors.

But who cares, except for a few wayward souls in the VC community who lament those sizzling burn rates. Bill Gurley, partner at Benchmark, had stepped to the forefront a few weeks ago to warn that “the average burn rate at the average venture-backed company” is at an “all-time high since ‘99 and maybe in many industries higher than in ‘99” [“Excessive Amounts of Risk” Doom Startup Bubble].

Marc Andreessen, founder of long-forgotten Netscape, then warned in a series of tweets: “When the market turns, and it will turn, we will find out who has been swimming without trunks on. Many high burn rate companies will VAPORIZE.” His final and most eloquent tweet: “Worry.”

Some other VCs chimed in when they had a minute, in between throwing even more cash at these companies to drive their valuations ever deeper into the stratosphere: in the first half, they’d thrown $15.6 billion at them in later-stage financing rounds, the Wall Street Journal reported, on track to break the record of $28.4 billion set in 2000, the year of peak craziness as the whole scheme was already collapsing.

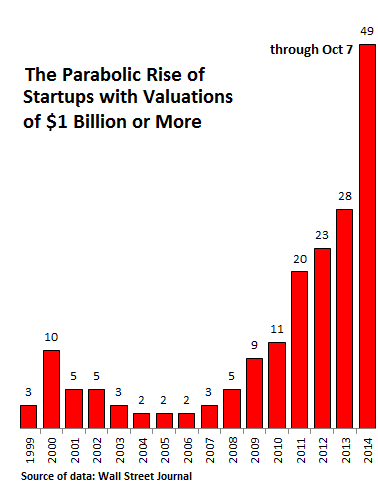

So now, 49 US startups that have not yet gone public and have not yet been acquired have valuations of over $1 billion, with five of them in, or nearly in, the $10 billion club. Uber tops the list with a valuation of $18 billion. And Snapchat, one of these $10-billion outfits, doesn’t even have revenues yet though it might eventually by selling ads via its disappearing messages.

Never before have there been that many startups with $1 billion valuations. The prior record was set last year when 28 companies achieved that milestone. In 2000, before it all collapsed, 10 startups had valuations over one billion. A parabolic rise of mega-valuation startups:

The overall IPO market has been whipped into a frenzy this year, with the most startups going public in the first half since 2000. But not the $1-billion-and-over kind; only 7 of them have gone public, including Alibaba that decided to sell its shares to US investors rather than to investors in China where it belongs. By contrast, in 2000, 38 companies with valuations of $1 billion or more were pushed out the IPO window.

They have their reasons for not going public. Some of them, like Snapchat, don’t have revenues, so convincing even exuberant investors to pay top dollars would be a slog. While that may not be a problem for zero-revenue Biotech startups that proffer the hope for a blockbuster drug, it’s a big problem for social media companies.

Other startups have revenues but are spilling prodigious amounts of red ink. That hasn’t kept them from going public, as the Twitter IPO has shown. Hope is a powerful motivator. There have to be other reasons why so many of them remain in private hands.

Turns out, it’s easier for VCs to multiply their paper profits if these startups do not go public. It’s easier because they control the valuations to a large extent. They don’t have to rely on the finicky stock market that has a nasty tendency to close the IPO window and crush these stocks just as the party is really hopping.

Pre-IPO “valuations” are an artifice decided behind closed doors within a tight community where everyone benefits if the valuations are ratcheted up relentlessly. In the current climate of boundless liquidity and near-zero returns on conservative investments, there is plenty of liquidity sloshing around, waiting for the next opportunity to book a paper profit. That paper profit is nearly guaranteed as long as everyone believes that everyone believes that valuations will be higher in the near future.

Look at Snapchat. It was driven from an already dizzying valuation of $2 billion last November to $10 billion earlier this year, with investors putting in an amazingly tiny amount of actual money. That kind of return would be hard to accomplish even in a frothing-at-the-mouth IPO market [read…. How to Rig the Entire IPO Market with just $20 Million].

This game of multiplying valuations and paper profits in the shortest time is so appealing that the startup scene is drowning in liquidity from all over the world. But how will they get their money out? Who will bail VCs out of these sky-high valuations and give them real money?

Two options: A corporate buyout, such as Facebook’s decision to print $19 billion of its own shares to buy a tiny messaging app maker. These miracles of corporate finance are always cool. Or an IPO. But in these mega-valuation startups, potential gains will have been harvested by private investors. And when time comes to go public, retail investors are likely to end up holding a deflating bag.

This is the rosy scenario. It assumes that the stock market, perched on top of its own ludicrous valuation, doesn’t get spooked beforehand. But there are signs that it is already getting spooked. Then all bets are off. Corporations get stingy, the IPO window closes, and what does get pushed out, experiences a hard landing, or simply shatters on impact. And suddenly the new money dries up. Startups with high burn rates can’t replace their cash and simply flame out. That’s the scenario Andreessen had warned about. It will be the sort of financial bloodletting people will remember for years.

The Dow was down over 300 points today. IPOs may experience hard landings. It’s suddenly tough out there. Even gold, it has been through heck. But wait – unlike the still prevailing exuberance for stocks, gold sentiment is at a historic low. Read….. The Calm Before the Storm in the Gold Market

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

How many companies can you build that rely on advertising when the consumer is dead broke? What revenue potential do they have? None! The valuations are insane.

Can anyone point out where to get some information on how best to short the market in the 2000 bubble?

This is a Potemkin economy, complete with Potemkin companies (e.g., Snapchat) with Potemkin valuations. It is as phony as the dotcom bubble of 1998-2000. There is no substance behind the facade. It is all Wall Street hype and wishful thinking.

It appears to me that these manias are occurring with increasing amplitude. That means that on the parabolic upswing, valuations are rising even faster than during the previous bubble. The flip side of that coin is that when this bubble finally meets a pinprick, valuations will probably collapse even faster than they did during the prior bubble. That goes for both the current stock market bubble and housing bubble 2.0.

Wolf is right to ask how the promoters get their money out and has hit a home run with the suggestion that retail investors (and pension funds, in my opinion) will be left holding a deflating bag. That is how it always works with flimflams and con jobs – those who are clever fleece those who are gullible.

My only hope is that the Fed will not be able to goose up “asset” prices the third time around.

Gee these past few days feels like Feb 2000 when internet related stock was the rage including even the hardware stocks like Cisco, Lucent and Sun not to mention lest we forget the IPO frenzy with small and big investors fighting for few IPO scraps..

The recent IPO frenzy and the biggest sucker bait IPO of the year Alibaba is sure sign of lot of liquidity looking for something “better” than minus yield (if inflation is taken into account). BTW – even the liberal mouthpiece 60-min exposed the Alibaba’s dim prospect and certain doom if they were stupid enough to branch outside China (that is IF one is stupid enough to trust the “audited” financials). Heck this was 2nd time they did the IPO after rather tepid IPO back in 2008 in HK and by the end of 2008, it slumped 55 percent and the company lost more than $20 billion in market value. Ma the man ended up delisting in HK, and did some accounting trick to reel in suckers again this time thru NYSE.

Yep it is not gonna end well and yeah we learn history so as to repeat it.

This does remind me so much of the tech bubble burst of 1000-01. At that time a friend of mine was a coder, and accepted a job for a tech start-up consulting firm in Minneapolis. He spent 80% or more of his first few months in different classes taking courses. About 10% of his time was with clients. The other 10% or so was sitting around doing nothing. His boss told him repeatedly not to worry, that the time he and other employees were spending in training was increasing their value as employees, and “since we’re a human capital company, it increases the value of the company as well.” Get it? Keep spending money on training employees and the company (and presumably it’s stock) will just keep getting more valuable. You don’t actually need to produce anything!

One day he showed up for work, and all the locks had been removed from all the doors. Two men from the parent venture capital company were there, along with members of a security firm. The employees were let go, escorted out of the building, and the company shut down. They went from rolling in venture capital dough and spending money hand over fist on all the training and perks they could get their hands on, to non-existent. All within a week.

That girl is going to pull up in her BMW one morning to a similar scenario.

I personally think it will be one more QE and then kaboom. The current sell off will escalate and combine with a be few more cases of Ebola. It’s a perfect storm for QE5.

I have made a huge bet by switching from my inflated shares investment into physical precious metals. The way I look at this is not an investment but an insurance policy. I just hope I will come out alive from this mother of all bubbles.

As for the VC backed IT companies, I will make sure I have popcorns ready for this horror show. Human never learnt history and expect different result every time.

If it happens, I think it will be a little different to the 2000 dot com bust – back then everything was tarred with the same brush – anything remotely related to the internet was punished severely. Now, there are a number of firms that are doing well – google, amazon, ebay, salesforce. Others who haven’t been able to show a good business case will probably crash.

The problem is that the stock market can’t go like this forever so we have to be prepared for a crash.

Even if the crash will be knocking at our doors in a few years that’s not a bad thing, because right now is the time to prosper and to get into the startup culture.

I’ll just mention the last three IPOs I witnessed closely:

Rocket Internet / Zalando / Alibaba.

All three massively overvalued pre-IPO, all substantially down post-IPO.

So,

around millenium, it crashed;

in 2007, it crashed,

now its 2014 – if you think about every 7 – 8 years is a crash to come, we are now in time :-)

Regards

Thanks for this article! Didn’t realize just how frothy is the VC and IPO “markets”!

This looks like Dot CON 2.0 on steroids!

Overall, these two charts just about show where things are headed: bit.ly/1lEfOq2

But remember what Mark Twain once said: “History does not repeat, but it does rhythm”!