Jump in government spending also boosted GDP growth. But surging Imports, falling residential fixed investments, and inventories dragged.

By Wolf Richter for WOLF STREET.

Our drunken sailors, as we’ve come to call them lovingly and facetiously, were at it again, and they splurged on goods in particular, but also on services, and they accounted for 69% of GDP, and they moved the GDP needle, driven by big increases in income, and they saved the rest.

A much smaller group of drunken sailors – the really drunken sailors at the federal government – also dug deeply into their pockets to spend money, but they had to borrow a bunch of it, thereby further ballooning the national debt and driving the debt-to-GDP ratio higher.

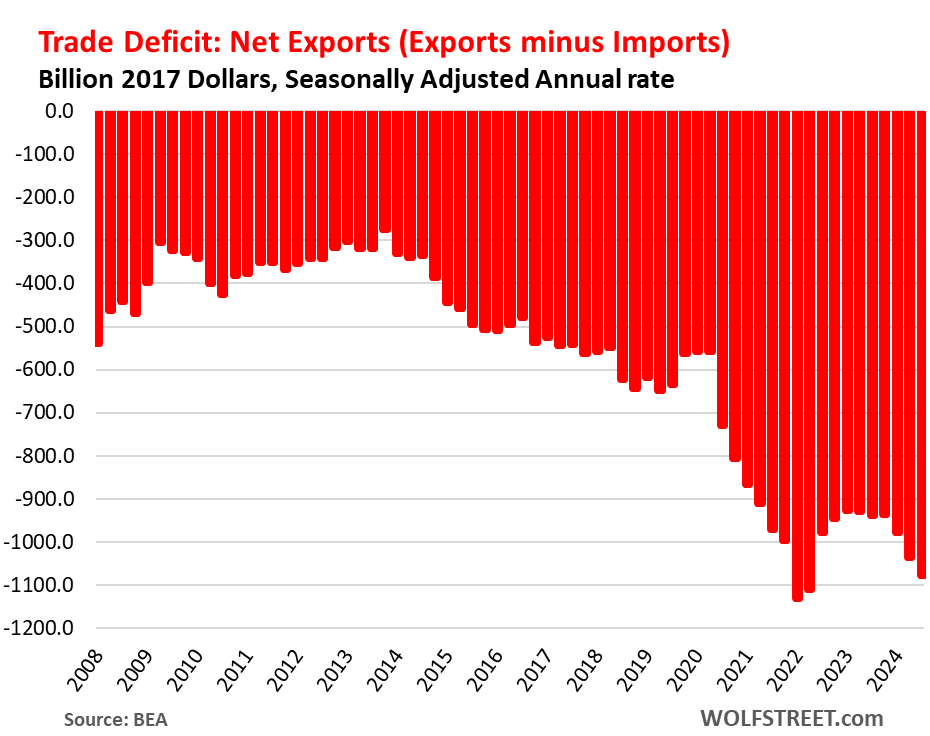

What dragged on GDP: The trade deficit worsened further, driven by rampant consumer spending and expected consumer spending on goods, a portion of which are imported. Companies were front-loading imports for the holiday season to not get caught up in a potentially long strike at East Coast ports. Slower growth in private inventory investment also dragged on GDP.

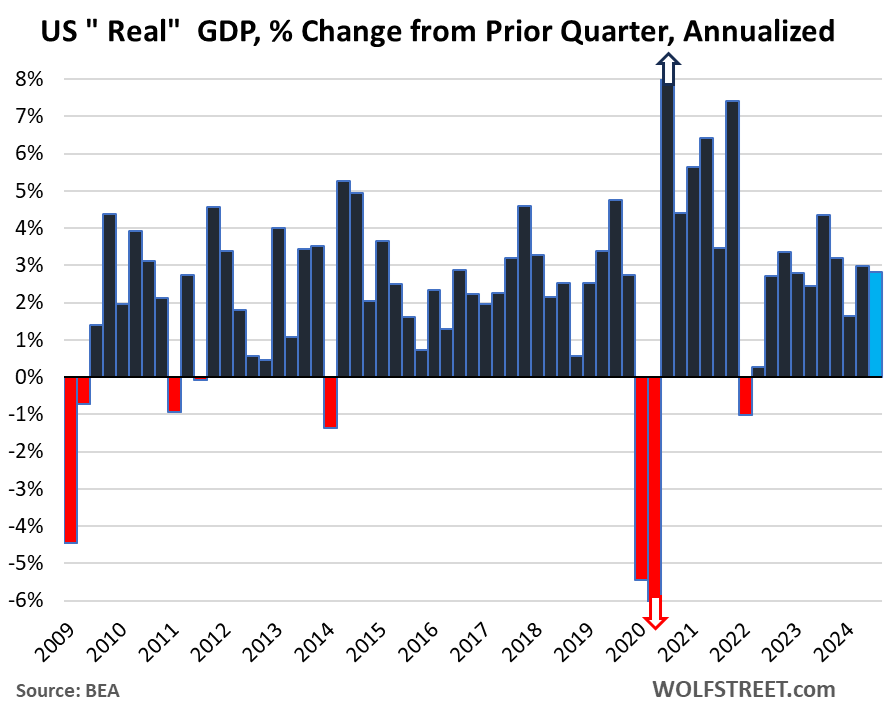

So, GDP, adjusted for inflation (“real GDP”), grew by an annualized rate of 2.8% in Q3 from Q2, well above the 15-year prepandemic average of 2.0%, according to the Bureau of Economic Analysis today. By comparison, in Q2, GDP grew by 3.0%, and in Q1 by 1.6%. Year-over-year, GDP grew by 2.7%.

By major category, adjusted for inflation, in annual rates:

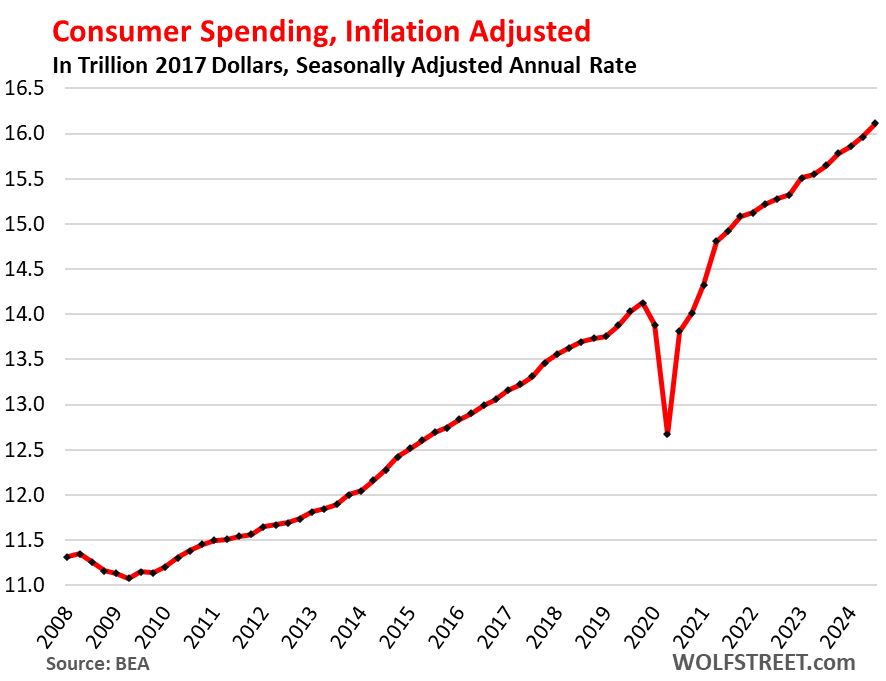

- Consumer spending (69% of GDP): +3.7%, an acceleration from Q2 (+2.8%), driven by a 8.1% surge in spending on durable goods.

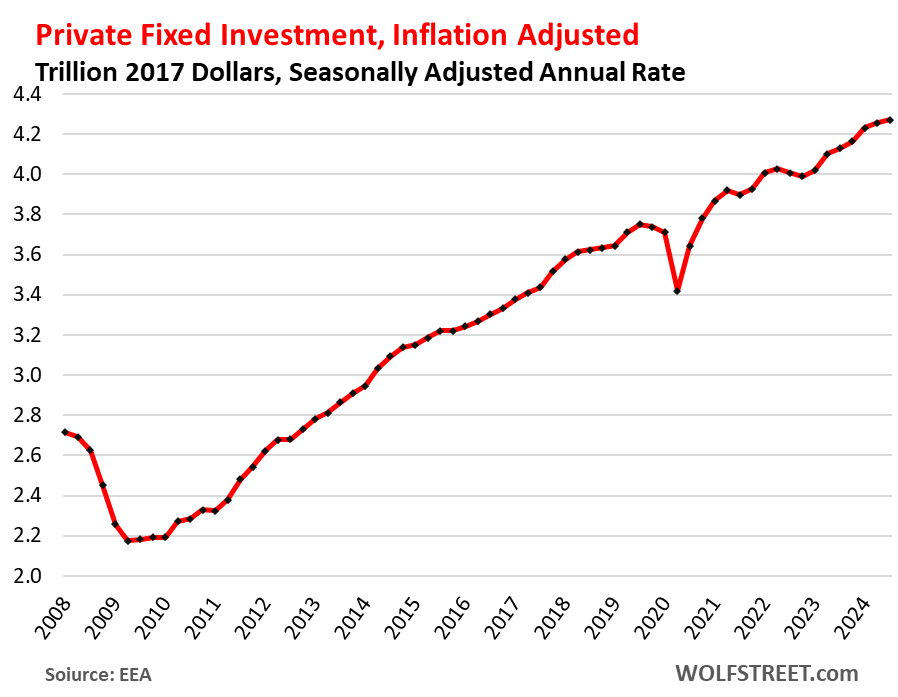

- Private fixed investment (18% of GDP): +1.3%, a deceleration from Q2 (+2.3%) and from Q1 (+6.5%), dragged down by a drop in residential fixed investment.

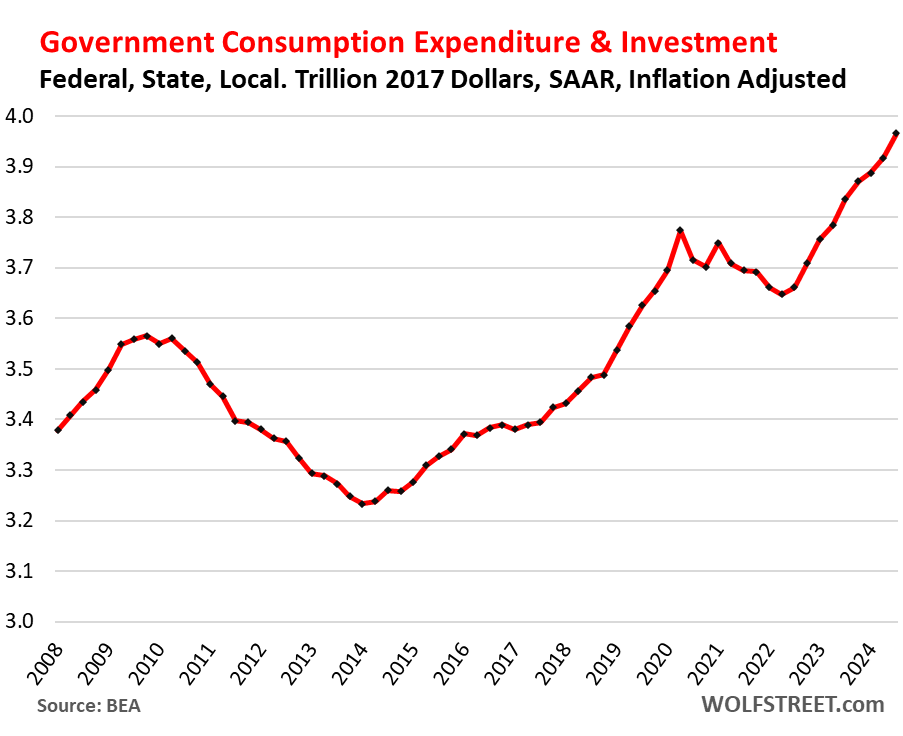

- Government consumption and investment (17% of GDP): +5.0%, an acceleration from Q2 (+3.1%). Federal government +9.7%, driven by a surge in defense spending. State and local government +2.3%.

- Change in private inventories investment dragged on GDP growth, after adding to it in Q2.

- Trade deficit worsened for the third consecutive quarter, on surging imports to meet strong US demand for durable goods. Imports drag on GDP. Exports add to GDP.

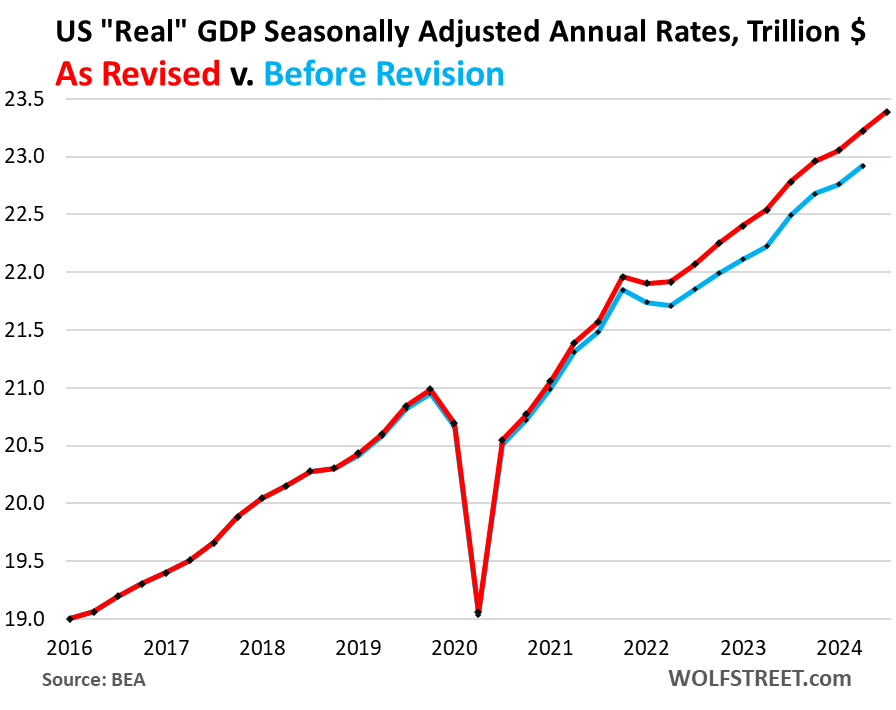

“Real” GDP in dollar terms, adjusted for inflation and expressed in 2017 dollars, rose to $23.4 trillion annualized in Q3. A month ago, the BEA heavily revised upward the prior years of GDP, consumer income, consumer spending, and the savings rate. The blue line shows GDP before that revision:

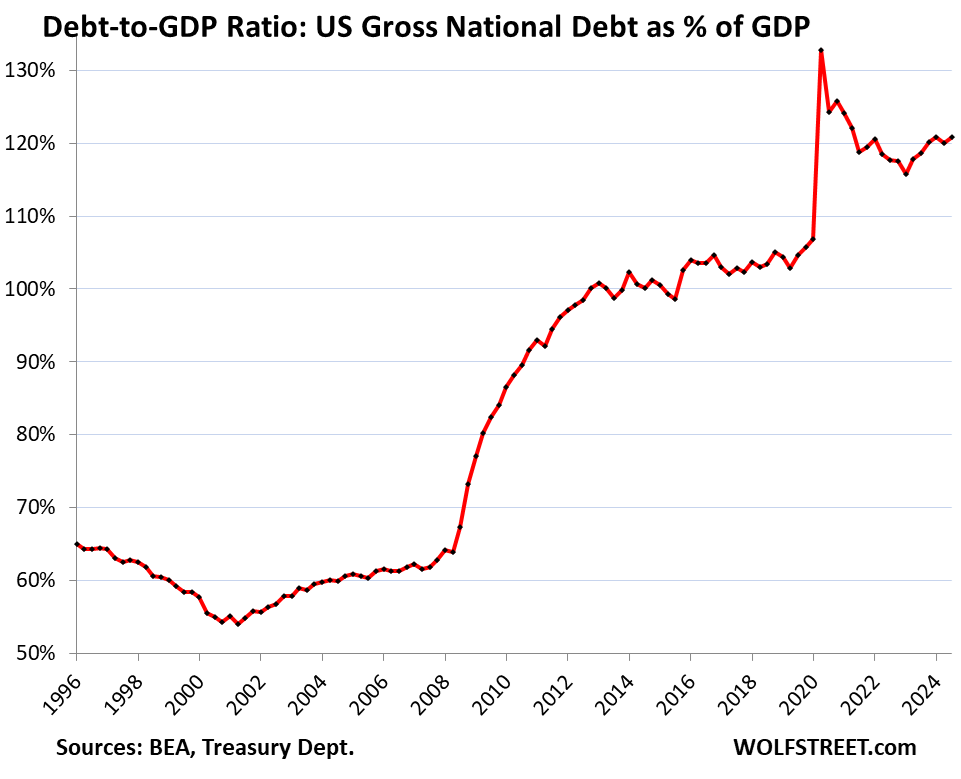

The actual size of the US economy: “Current-dollar” GDP (not adjusted for inflation and expressed in current dollars) rose by 4.9%, to $29.4 trillion annualized. This is the amount we use for the US debt-to-GDP ratio here further down.

Consumer spending on goods and services rose by 3.7% in Q3 from Q2 annualized and adjusted for inflation, the fastest rate of growth since Q1 2023, and the second fastest since Q4 2021, powered by phenomenal spending growth on durable goods.

- Services: +2.6%.

- Durable goods: +8.1%, driven by motor vehicles.

- Nondurable goods: +4.9%.

Retail sales data – sales of goods, not services – released earlier in October, including large up-revisions of prior months, pointed the way with a three-month annualized growth rate, not adjusted for inflation, of 7.0%.

Consumer spending – personal consumption expenditures, as they’re called officially – accounted for 69% of GDP.

Private Fixed investment rose by 1.3%, annualized and adjusted for inflation, decelerating from the prior two quarters (Q2 +2.3%, Q1 +6.5%). Of which:

- Residential fixed investment: -5.1%, second consecutive quarter of declines.

- Nonresidential fixed investments: +3.3%, a deceleration from prior quarters (+3.9% in Q2, +4.5% in Q1):

- Structures: -4.0%, first decline since 2021.

- Equipment: +11.1%

- Intellectual property products (software, movies, etc.): +0.6%.

Government consumption expenditures and gross investment jumped by 5.0% annualized and adjusted for inflation, a further acceleration from Q2 (+3.1%) and Q1 (+1.8%).

Federal, state, and local government consumption and investment accounts for 17% of GDP (with state and local governments accounting for 61% of total government spending, and the federal government accounting for 39%).

This does not include interest payments, and it does not include transfer payments (the biggest part of which are Social Security payments), which are counted in GDP if and when consumers and businesses spend these funds or invest them in fixed investments.

- State and local governments: +2.3%.

- Federal government: +9.7%, compared to Q2 (+4.3%) and Q1 (-0.4%.

- National Defense +14.9%.

- Nondefense +3.2%.

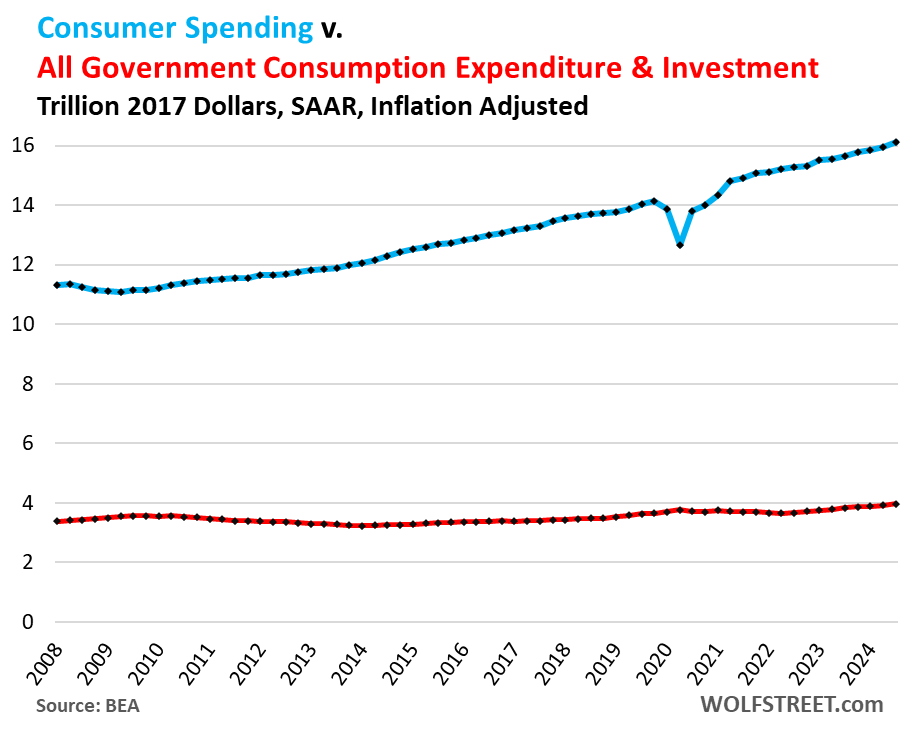

Consumers v. Governments. Consumer spending accounts for 69% of GDP, and the percentage increase moves the needle much more than the combined federal, state, and local government spending (which accounts for only 17% of GDP) because it comes off a much larger base.

Personal consumption expenditures (+3.0%) contributed 2.46 percentage points to the GDP growth of 2.8%.

Federal, state, and local, government consumption expenditures and investment (+5.0%) contributed only 0.85 percentage points to the GDP growth of 2.8%.

This chart shows both, consumer spending (blue) and government spending (red) in inflation-adjusted dollars at annual rates. Remember that big parts of government spending, including interest expense, do not enter into GDP and economic growth. They only enter indirectly if and when the recipients spend them or invest them in fixed investments:

The Trade Deficit (“net exports”) in goods & services worsened further for the third consecutive quarter:

- Exports: +8.9%, to $2.63 trillion. Added 0.94 percentage points to GDP growth.

- Imports: +11.2%, to $3.71 trillion. Subtracted 1.49 percentage points of GDP growth.

- Net exports (exports minus imports) worsened to -$1.08 trillion and subtracted 0.55 percentage points from GDP growth

The Debt-to-GDP ratio worsened a tad to 120.8% in Q3 because the gross national debt in current dollars (not adjusted for inflation) grew even faster than GDP in current dollars (not adjusted for inflation). By contrast, in Q2, GDP had grown a little faster than the debt, and the Debt-to-GDP ratio had dipped a little. For the past four quarters, the debt-to-GDP ratio hovered at just over 120%, despite the strong economy:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I saw a lot of these drunken sailors at the last CU boulder. Thankfully everything at that game was free for those of us in the box from the invite.

best of luck to all them sailors as this ships keeps sailing.

Maybe higher tariffs on manufactured goods is an idea who time has come.

That idea came a long time ago, but it’s really hard for anyone, including Trump — he only partially succeeded in 2016-2020 — to implement them because there is so much resistance to tariffs in corporate America and from stockholders because they got so rich off those imports (offshoring production to cheap labor countries to boost profit margins), Walmart and Apple at the very top of the list. And they have recruited armies of economists to constantly attack tariffs from all directions.

Tariffs are a direct tax on the profit margins of foreign producers and US importers. And maybe they can pass some of them on to end users, but that’s not guaranteed if local competition keeps prices down, in which case tariffs are just a tax on foreign producers and US importers. And this country needs to raise taxes, and tariffs is about the best way of raising tax receipts, much better than taxing incomes. With taxes you have to choose the lesser evil, and tariffs are the lesser evil.

There are some readers here who live in other countries, and for them, US tariffs are always a terrible idea because these people in other countries have gotten rich off the US trade deficits. So let them hate tariffs all they want.

“(offshoring production to cheap labor countries to boost profit margins)”

Wolf – this is nothing new – in the 60’s pharmaceuticals went to the Carribean; electronics did it in the 70’s and 80’s before they went to asia.

The lower cost of labor offset the cost of shipping – and frankly having managed a factory in Mexico, the labor force was reliable and the quality was on par with US factory.

Question for the labor unions: what did you think was going to happen when you negotiated higher wages – might be good in short term to appease workers but lost jobs in the long term?

We’re now paying the price for three decades of the failed free-trade dogma.

China and other countries were the ones that benefited, along with US corporations.

Imo, that wasn’t free trade.

Sold as such, but it doesn’t account for the significant differences in safety and environmental regulation between the US and many “cheap” labor countries.

It may be billed as “free trade” but it is not a level playing field at many many levels. Safety may be local but environmental issues often aren’t

Those savings went to corporations and their shareholders. The taxpayers

and workers paid the price with

a declining standard of living

and government deficits to pay for the knock on effects.

“Question for the labor unions: what did you think was going to happen when you negotiated higher wages – might be good in short term to appease workers but lost jobs in the long term?”

Get what you are saying, but…the landlord/RE speculator class has also been pretty damn brutal over decades (but especially last 5 years) about using *their* leverage to squeeze the hell out of workers (unionized or not) – *also* forcing the price of US labor to levels that are uncompetitive with many alternative manufacturing nations.

Result – 55 years of relentless US merchandise trade deficits.

Multiple special interest groups/pleaders have really done a horrific number on US international trade competitiveness.

Back in 1975 i worked for Kawasaki Motors in Lincoln Ne. — we started making snowmobiles in 1975 and needed 6061T6 aluminum in 5×10 sheets – tons of it.

We were able to buy EXACTLY that aluminum from Japan cheaper than we could from any USA source – including transportation costs of ship and trucking from California

– labor cost was just too high here

Labor costs typically are 20-35% of gross sales – so we bought from Japan for years

Imagine that tariffs are up, income taxes removed. I’m certain that most of the tariffs will be paid by end users. Acting something similar to what we have in Canada: sales taxes (GST/PST), on only foreign goods. But the new prices feeds inflation directly (unlike in Canada). In Canada the tax is paid only once at the post of sale. Not on every step in the production/business pipe (like tariffs).

Now, from the government point of view, the more imports the better. This could be quite a strong force to encourage imports.

And there is so much more to it.

You got this backwards.

Sales taxes are different from tariffs in that you cannot escape sales taxes, but you can and do escape tariffs by producing in the US.

That’s the either-or purpose of tariffs: either pay taxes or produce locally. So tariffs ENCOURAGE local production and DISCOURAGE imports, and if you want to import anyway, you pay the tax. It’s not rocket science.

Example. Production of widget A. By local production, the taxman gets total $X. But the A has a huge tariff Y. If Y >> X then the money talks. All I’m saying is that there is a double sword incentive. Just noting it, that’s all.

Biker

You’re talking about a MONOPOLY. read what I said about a monopoly and price increases: regulation or prosecution.

But normally, there is competition included based on price. And then your theory is toast.

And forget that “eliminate income taxes” bullshit. That’s just idiotic. No one is going to do that, ever, it doesn’t matter what they say or want. It cannot happen and won’t happen. No one can stop the sun from rising either, and it doesn’t matter what they say or want.

All income taxes combined account for over 96% of total federal tax receipts. Tariffs account for 1.8%. You can triple the tariffs, which would be a LOT, and they’ll account for only about 5% of total tax receipts. No one is going to eliminate the remaining 95% of tax receipts. That stuff is just idiotic bullshit.

I guess we are talking about tariffs in the context of Trump. And he is promising to reduces a lot of taxes, and cover *any* public expense with tariffs (see childcare). Which part we should believe, which not? Many are picking parts what he says what they like, thinking that the rest is just too crazy or so.

My speculation is that there is a danger in over-reliance on tariffs for budget spending. This produces a government’s temptation to maximize the tariffs. Increase them over time even more, and eventually even support increasing imports (in some ways), when the increases stop working. Normally tariffs are reducing imports. But this over-reliance could create a counter force. Monopoly or not. This is my small theory.

Judging by the inflation in the last few years, there is a lot of monopolies in US economy. Not sure how would that differ for tariffs. Just any price increase to product’s input, has been used as excuse to rise prices a lot.

Maybe his followers expect Trump to feed the multitudes with a few loaves of bread and some fish? Their other savior did it.

Man! Are THEY ever in for a shock when he just takes care of who he has ALWAYS been taking care of, for a profit….he is a businessman…not a politician….or so they say.

But then what do I know?…I hate bean counting…..don’t even like doing my own bills, much less “investing”. (aka gambling)

If you aren’t downsizing you are very stupid.

Hi Wolf,

Don’t tariffs allow US manufacturers to raise their prices to match the costs of imported products? In theory, US producers should benefit from selling cheaper goods. But I recently read an article about US companies raising their prices to maximize their profits against the newly set tariff prices—akin to raising plywood prices when a hurricane is about to hit.

As a result, US consumers don’t directly benefit from the tariffs.

Is my logic correct?

@Kentucky:

I agree with your logic. Domestic producers can and will raise their prices to just below prices of imported products, so consumers will really not benefit from tariffs. They will not leave money on the table.

The other argument that economists have against tariffs is that the domestic manufacturers will not have much compulsion to innovate and produce better products.

So consumers will suffer both from higher-prices as well as lesser quality.

This is exactly where we are heading in the EV space where tariffs are being levied to very high levels on imports.

“tariffs allow US manufacturers to raise their prices to match the costs of imported products?”

No. Tariffs don’t allow anything. The lack of competition does.

If there is only one producer in the US, or an oligopoly, yes. Which is why monopolies and oligopolies are so bad and in theory are targeted either for regulation or prosecution by trust busters.

If there is vibrant local competition, they will compete on price to gain or maintain market share, and profit margins are then limited. If someone tries to raise prices to match tariffed imports, they will lose sales, and eventually they’ll have to cut prices or vanish.

@Wolf: You said:

“If there is only one producer in the US, or an oligopoly, yes. Which is why monopolies and oligopolies are so bad and in theory are targeted either for regulation or prosecution by trust busters.”

The key words are “in theory”. Companies and right-wing politicians have pushed back at regulation and trust busting so much that consolidation has been the norm since the 1990s. With Republican administrations, they are with the corporations and there is virtually no trust busting. And with a Democrat administration, any trust busting is met with huge push back by

corporations and Republicans. So they tiptoe and try to do something here and there.

We all know that FTC Commissioner Lina Khan is in huge trouble for her recent anti-trust efforts. Even Mark Cuban who is supporting Harris is against Khan continuing in her position if Harris wins. This is the state of our anti-trust efforts.

Further, you said:

“If there is vibrant local competition, they will compete on price to gain or maintain market share, and profit margins are then limited. If someone tries to raise prices to match tariffed imports, they will lose sales, and eventually they’ll have to cut prices or vanish.”

The key words are “If there is vibrant local competition…”. There is no real competition, let alone vibrant competition in most industries. Most industries have 3 to 5 giant companies and consumers have very little choice or leverage.

Two cases to prove my point:

(1) The auto industry where our domestic manufacturers have raised prices of their pickup trucks to stratospheric heights. Foreign producers are careful not to get too aggressive with their market share since the so-called “Voluntary Restraint Agreement” was rolled out by our then “free-market” President Reagan in the 1980s.

(2) Apple and Google Pixel phones are selling upwards of $1,000-1,500. A few years back they were selling for a few hundred dollars. Agreed that the more recent phones have more technology, but in this space, we all know that prices have come down drastically over the last 2-3 decades even with huge technological advances. I would submit that Apple and Google have monopoly power in the smartphone market. Huawei started to make some inroads with their phones about 5 years back, and we all know what happened to them.

This is the ground reality.

Sean,

Get what you are saying, but the US has been *so* slow to re-organize in the face of international competition and the macro numbers (employment-to-population, trade deficits, etc. etc.) since 2000 have been so lastingly terrible…and other macro numbers so god-awful (debt-to-GDP, inflation, looming entitlements crisis) that at least a partial, hopefully pretty temporary tariff regime has to be attempted (*something* new has to be attempted) – since the promises of “free market adaptation” have pretty much failed for 20-25 years.

I definitely can see US producers abusing the crap out of a tariff regime – but the alleged “free market” contingent hasn’t come up with an effective empirical insight/solution for over 20 years (other than using the Fed to print money to paper over the worst of the macroeconomic decay – which ain’t exactly a free market solution).

Wolf, that’s a very good analysis of the idea of raising tariffs., hadn’t seen that thought process before.

Thank you.

Now the classic rebuttal by economists against this idea is the Smoot Hawley tariffs which purportedly sent the world into the Great Depression.

I’d like your thoughts on this

Exactly.

Tariffs are stupid. Be careful what you ask for. Free trade has made this country very rich.

It made the poor richer than …

Rico,

“Free trade has made this country very rich.”

Country who??? Free trade has made the rich immensely rich. That’s what free trade is all about. It has gutted the American workforce and lots of companies that were manufacturing things in the US. You’re talking like a Wall Street goon that would sell his own kids to make his stock portfolio go up.

I just think the idea may work, and it is a unique idea to a revenue problem we have.

So curious about how you would rebuff their Smoot Hawley tit-for-tat tariff hikes by other countries, often called “Beggar Thy Neighbor” by the economists

Pete,

ALL countries should impose tariffs to encourage local production. It would also lower fuel consumption and pollution from shipping every little thing across the world to fatten up profit margins a little. Taxes have to be raised, better on imports than on income, lesser evil. And most countries already do.

China has tariffs, including on auto imports. That’s why nearly every vehicle that is sold in China is made in China: tariffs!!! Try to sell an imported cellphone in China, LOL. Other countries do too. Then there are administrative blocks and red tape (Japan is good at that). The EU knows how to protect its markets too — see the current tariffs on Chinese EVs.

Only the US has been made the laughing stock of the export powerhouses of the world.

Some tariffs are good when foreign companies are subsidized by their governments to sell below market price to remove competition by taking market share. Once the completion is gone, they can increase the price.

It happens all the time.

Does the U S government subsidies any business or like this chip program or are they Laissez-faire?

Tariff on Chinese products have increased the cost of construction materials by equal proportion. It doesn’t seem the tariff was absorbed by producers and importers. End consumers paid for the cost — at least that is true for construction.

China had tariff for imported cars decades ago and it only made the cars prohibitively expensive and local car makers lazy and profitable. It never worked for China and I doubt it would work for US.

Typecheck

Then the tariffs weren’t high enough to stop the Chinese construction materials from being imported, LOL. Why do US homebuilders have to import this shit? They should have bought from and nurtured the US producers. It’s just always the same BS.

China imports raw materials. But it doesn’t import drywall and other manufactured construction materials. It exports those. Only the US imports them. You people are the reason why the US economy’s manufacturing sector has plunged into the abyss. This is now a national security issue for the US.

Chinese producers kill US companies with their subsidized underpriced products, and after they kill them, they hike prices, and you get shitty China-made drywall that then has to be torn out.

When the discussion comes to tariffs, it’s just all propaganda being spread all the time. This BS has infested everything.

Short-term thinking to eke out higher gross margins and higher stock prices sacrifices long-term wellbeing of the workers, US producers, the economy overall, and the security of this country.

Theorycraft against real world examples… Seems highly irresponsible to me. I admit to being conflicted about the idea of tariffs against nations that don’t treat their workers well. But I’m suspicious of anyone who argues how great a solution it is. It’s not, it’s a bludgeon with unforeseeable fallout.

“There are some readers here who live in other countries, and for them, US tariffs are always a terrible idea because these people in other countries have gotten rich off the US trade deficits. So let them hate tariffs all they want.”

I never “got rich” off of free trade but the USA-Japan trade agreement and the ignorance of Canadian customs agents has helped me save a few bucks on car parts 😆. So I hope any potential new tariffs are implemented selectively lol

Agree totally.

The US worker has been screwed in this flawed “no barriers” policy and doctrine. US corporations lobbied and allowed offshoring while no other country lived up to their side of the bargain and protected their industry.

History too suggests that US has done well when the blue collar has done well. People how make fun of Trump’s tariffs have been indoctrinated by paid economists.

Whether Trump can pull this off or not remains to be seen….or whether he will even win. But his thinking is correct and the best for the country

I’m not a supporter of globalization at all, but I just wish he had a little bit more coherent of a plan for the tariffs. He only seems to have a vague impression of what they actually are. There’s also his whole thing about tax cuts which would offset the revenue, and I’d be surprised if the Republicans enact some robust antitrust enforcement to prevent the now-tax-advantaged US companies from monopolizing the market once the foreign imports are gone.

Germany has and had a hughe trade surplus.

But that just means we export our labour for green paper. So much of our productivity just gets exportet without having a net benefit at home.

And that green paper helps corporations. BASF buys monsanto, build huhge industrial complexes in USA and China. Same with DHL or VW.

But not much of that money gets spend at home. Otherwise the trade would be balanced. To turn green paper into goods it needs to be spend and importet but thats not whats happening. The trade imbalance stays. The productivity gets imported and the money is turned into foreign investment outside of Germany.

China turns its trade surplus into foreign investment, too. But they try to buy with it influence rather than shareholder profits. And wastes a lot of money along the way, too lol.

I wonder how much of the belt & road project is a valve for forex, a channel for industrial overcapacity and strategic investment in practice.

I think Michael Porter may beg to differ.

Tom V.

Michael Porter was one of the idiots that are responsible for this mess. As part of getting my MBA in the mid-1980s, I had to buy and read his then new “Competitive Advantage” — boiled down to cheap labor and differentiation, cheap labor wherever you can find it. That triggered the whole offshoring frenzy over the past 30 years.

Which is precisely why the US should have changed that calculation by imposing tariffs. The damage is now huge. Entire industries have wandered off to other countries, and today there is no longer the infrastructure, the people, or the knowhow in the US to manufacture that stuff in the US. An example is the landmark tower of the new Bay Bridge between San Francisco and Oakland. So that was over a decade ago. At the time, it was no longer possible manufacture such a big steel structure in the US because all the expertise and infrastructure had wandered off to China over the decades, and they had to have it made in China, and ship it over here in pieces. That’s the long-term strategic result of encouraging offshoring – and China knew how to play short-termism in Corporate America. Porter is a card-carrying idiot.

Cheap labor is much less of an incentive today due to automation. Industrial robots cost roughly the same, no matter where the plant is, which is why auto manufacturing is such a big industry in the US, and most vehicles from foreign brands that you can buy in the US are made in the US, and some brands, such as Honda, have more US content in their vehicles than the legacy US brands. Teslas have the most US content. That is one industry that has survived. But there are many others that haven’t.

Increasing tariffs during a period of low unemployment and elevated inflation doesn’t seem like it would be very politically palatable, yet here we are. Tariffs amount to an immediate tax on consumers. Newer tariffs have been in place for some time now and I’m not aware of any impact on localization and reduction of imports. Maybe long run there could be some domestic investment to fight it, but I haven’t seen it.

Tom S.

“Tariffs amount to an immediate tax on consumers.”

This is ridiculous braindead bullshit propaganda that foreign companies and US importers and Wall Street goons have planted all over the place for 3 decades to stop tariffs. It’s just plain old BS.

Tariffs are an IMMEDIATE TAX ON PROFIT MARGINS OF FOREIGN PRODUCERS AND US IMPORTERS.

Whether or not and to what extent they can pass them on to end users is determined by local competitions, and if it happens only happens partially and with a lag.

Tariffs are tax. So you propose to tax consumers’ income more instead of foreign producers’ and US importers’ gross margin? Hell yes, you are!

“Whether or not and to what extent they can pass them on to end users is determined by local competitions”

Where there’s no local competition, or the price to source locally is higher than tariffs, companies simply mark up the selling price to include any tariff they have to pay, and it gets passed right through to the consumer. Take imported aluminum castings as an example. You cannot find a domestic source that is even close to the same price as China, it’s up to 10x to source domestically. Noone is opening up a casting shop due to tariffs, or changing their supply chain, they’re marking it right up and it gets into the price of a vehicle.

Probably an even better example is with imported pharmaceutical products, the consumer has no choice whether or not to take the lifesaving drug. Whoever imports the drug passes the price increase right along to the consumer. I’ve seen tariffs as one of the forces driving inflation. It’s not all bad, it keeps certain nationally important domestic industries from collapsing due to international competition, but consumers do pay higher prices for it.

And yes, income tax is transparent and obvious and passed through legislation from congress, so it is preferred to tariffs, in my opinion.

Tom S.

Companies ALWAYS charge the highest price they can that will allow them to still succeed in their sales efforts. It doesn’t matter whether imported or not.

Prices are set by the market place, not by costs.

Profit margins are determined by costs and prices. Tariffs hit profit margins, not prices.

For-profit companies are NOT charities. Chinese companies are not charities either. Big pharma is not a charity. They ALWAYS charge the highest price they can, and if they can produce it more cheaply overseas TO FATTEN UP THEIR PROFIT MARGINS, not to lower prices, LOL, they will. Tariffs will see to it that they cannot produce it more cheaply overseas, that their profit margins will be lower than if they produce it locally (after transportation costs, loss of IP, etc.), and so a company decides where to produce it, which HAS ZERO IMPACT ON PRICE. PRICE IS SET BY THE MARKET because companies are already charging the highest price they can get away with. This is a decision about profit margins.

Lower prices create more sales. So that’s the mechanic here. If there is no competition, an importer will charge the highest price that will still allow them to get to their sales targets.

A true monopoly for essentials, like the wires to your house, must either be owned by the users/rate payers, the municipality, or must be heavily regulated.

Correct!

However, my questions are; after we have brought all the manufacturing that we offshored in the interest of “free trade”, will our products be competitive on the global market? Who will be buying our products? Will they have enough dollars to purchase our products?

Let alone trying to build all this out and supply the commodities and energy with our current debt:GDP. Seems like everyone is “turning Japanese”…

Interesting times.

Why don’t you let the manufacturers that make those decisions worry about that, rather than use this hypothetical BS as an argument against tariffs.

Look I agree with you about companies maximizing prices to maximize profits, however we have seen elasticity to price with the consumer before a dip in sales sets in. And you know the supply chains we are talking about unwinding are complex. I’m unconvinced we can tariff our way back to being a manufacturing powerhouse without a jump in the price of goods in the interim. The economics of opening say, a steel mill, just doesn’t attract investors. Even a new chip fab operation had to be hugely subsidized. Also, look at labor costs and constraints here in the US, you’d be talking about huge, even YUGE, tariffs. I think the timeline is long before the capacity expands domestically to really compete and save the consumer from paying. Tariffs are immediate, country specific, and very hard for businesses to plan for and adapt to. Or maybe I’m spewing braindead wall street zombie BS, at least it’s fitting for Halloween!

Wolf –

I think your critique of Tom S is mostly right-on-target and agree intelligent tariffs could do a lot to reduce tax burden and improve domestic production. But I do think you’re glossing over an important aspect.

A very common scenario is when, not a specific company, but an entire industry is located in, e.g. China.

Competition between multiple Chinese producers are what hold prices and profit-margins down. If we enact a tariff on all of them simultaneously, then it’s unlikely to change their profit-maximizing strategy much. They likely will pass on [almost] all of the tariff to end users immediately, while their profit-margins stay basically the same and still in balanced competition with each other.

Obviously each product is going to be a little different.

How essential is it? Will buyers simply not purchase the product at all? Or are they forced to pay whatever? Is the cost increase enough to bring in domestic or other (lower-tariff) foreign producers into the market? etc.

But there will be a lot of products which have no domestic competition and the tariffs still aren’t high enough to make it practical. On these, we’ll see [most of] the cost of tariffs go directly to consumers in the form of increased prices.

Bottom line is: in reality the cost of tariffs will be absorbed by both inflation for the end consumer and reduced foreign company profit margins. At least some of the burden will go to foreign companies which is good.

It just seems like everyone wants to argue about this issue in absolute black-and-white while the reality is much more nuanced shades-of-grey.

I general idea of tariffs is to encourage domestic production. Which is to say that domestic workers earn wages from things that they consume. I guess this desire is not that controversial.

However you do have a point. In the short term, the affects of tariffs will be based on

1. What are the profit margins of the products that are affected by tariffs. If they are low (e.g. toys) we should expect increase in prices

2. How is the domestic competition in that particular market (if it is high then it should have no affect on price)

3. Do we want domestic production of some of these things (e.g. toxic chemicals)

Like everything else this is nuanced. But a policy can be made that will do the best for US. The whole idea that US will produce high end technology and everyone else will send us everything else leaves high end tech workers at an advantage compared to other Americans. This is a flawed policy with seeds of social dissatisfaction….which we see all around us.

Hired economist like Mr. Krugman will write articles about it but common sense thinking will immediately debunk Krugman’s ideas. These guys get nobel prizes because their writings and their thoughts can be bought. The nobel prize adds legitimacy.

Bingo! In Krugman’s case, call it what it really is, a Nobel in eCONomic propaganda.

Yeah, but he’s not a graduate of the Chicago School, where most Nobel winners came from up to about 1990…maybe still?

But then you don’t know very much about that program, if anything, do you?

Apologies and general disagreement if I’m wrong.

I think that reality is successfully introduced as a hurricane or tornado.

Love is painful. A lesson that I have carried into my seventy something years,

The SE people have been dealt an apparent blow in the asking price of they’re condos. which just fell by half.

I love how they echo the nonsense.

“Boy black holes should be implemented”

Derrrrrrrrrr!!

Lets keep this party going!

Raging Everything Mania, fueled by “the most reckless FED ever.”

No. The Federal Reserve is very conservative and has been shrinking the money supply in the US for years with QT. Blame crazed manic speculators for prices, not the Federal Reserve.

I am not a manic speculator I am an INVESTOR

Anon,

Really? I never considered that.

@SoCalBeachDude: After doing QE and Zirp for close to 3 decades and printing trillions of dollars during Covid, the Fed has just mopped up a small portion of it with its QT the last couple of years.

Why do you think that the economy is doing so well in spite of the tightening for the last couple of years? It is like someone pouring 100,000 barrels of oil in the fire and trying to put it out with water from a fire truck.

You can say that they have done something to redeem themselves a tad bit but saying that they are “very conservative” is laughable.

Further, several Fed governors have spoken about the wealth effect on the economy. By holding down interest rates and paving the way for stock and housing market speculation, the Fed fully intended to keep the bubbles going. Sure, “crazed manic speculators” are present, but by and large there have not been any sensible investment alternatives available for prudent investors.

You have been repeating this view for quite some time, I don’t know why. But it clearly doesn’t pass the small test.

Solid straightforward accounting and analysis always passes the smell test and is based on solid facts as opposed to hopium and manic speculation and perceptions that apparently hold sway for an endless array of manic speculators who are the core problem stopping price discovery in the markets.

Oil prices to support economic growth.

Your comments never cease to assume me.

It’s like your blatant echo chamber thought process is so different from Wolfs logic centric approach.

It makes it seem as though southern California and northern California are from different planets.

Or maybe just Wolf lives in California and has managed to not BECOME FROM California

“The most reckless FED ever.” I think that title has now been officially retired around here. Plus from all that benefitted from seeing their home value rocket beyond their wildest wet dreams or seeing they can do no wrong on Mag 7 stock with every downturn becoming another buy the dip before resuming rocket course to Mars, is the FED truly reckless in their eyes or are they the greatest in wealth generation?

Judging by the way most sailors are still on a never-ending drinking binge, if they care to know who Pow Pow is, they probably will say he is doing a decent or great job. With another cut, most normies will probably think he is excellent at his job.

no one disputes that powell has been great for the top 1% who own a disproportionate share of assets. not so much for the middle and working classes, however.

Isn’t it incredible how money printing and absurd government deficits benefit everyone?

(except the young, middle class, and working class – but those people don’t count)

“normies”

another word for lemmings or sheep?

again….thecon dot tv

It’s a word the dummies can rally behind

Wreckless fed is one thing, “most wreckless fed” can’t be shaken of after just a couple years.

What just happened? His first move a few months ago was a blunder, 50 point cut…tricked by a jobs report and the revisers….the judgment of…

“Most wreckless fed ever”.

When the O/N RRP facility finally drains, interest rate pressures will be on the upside.

I am no Fed lover but I think Powell has done a good job overall. QE during the pandemic was the right thing to do. They just overstayed their welcome. I guess the fiscal response undid them. They relied on models that were looking at liquidity injection into the capital markets but this time the money went directly to the people.

I doubt if their policies have much affect on the actual economy anymore. Keynes wrote about debt saturation where monetary policy fails to have affect. But they have outsized affect on the psychology of investors.

The problem with the Fed is that there has been mission creep. They were supposed to be the lender of last resort…to restore stability of the financial systems but over time their job has become to fine tune the economy at which they are terrible (everyone will be). This is not a Powell problem but an institutional problem. Powell was responding to once in a century problem as was Bernanke during 2008. Bernanke if he had stopped QE in 2011 would have been remembered as a great Fed chief. Powell had he stopped when vaccines were announced would have been a great Fed chief. Much less can be said about Greenspan’s prodigy Ms Yellen. She has been a disaster for US in every role she has served.

Lawmakers should decide what the role of the Fed is. If it is maximum employment without high inflation then the current trend will continue…risks will build…they will blow up….and QE will be the only option. The stakes are getting larger and larger. Unchecked they will lead to the demise of the financial system eventually from so much debt that all of it will have to be monetized. No one knows when but we are on the path.

reckless FED should be replaced with “Reckelss Gov”.

The Gov is spending like crazy. I have read so many stories of projects that are funded by the IRA. I just read that a $21 million dollar homeless shelter is going to be built with IRA funds. I am not saying it is bad to build a homeless shelter but that is just an example of how the Inflation Reduction Act is reducing inflation.

Also, a local $300 million dollar college football stadium is being renovated partly with $150 million COVID money.

This list goes on and on.

So your logic is:

“IF you own a house, then you shouldn’t be mad at the fed”?

Is that seriously what we’re going with here?

The worst solution is too reduce SS and Medicare benefits. They should increase the benefit pool. The worst idea dreamed up by the oldest bunch who made every wrong decision over the past 50 years let alone that they are likely senile;

Firstly, Social Security is not part of the general budget because it has been has been paid for by the working people and is not an entitlement as much as a right.

And I am one of the few that is slowing down on adding to the partying because I am past my personal expiration date by a few years and don’t need more stuff.

Maybe I should dump my current ride and buy a new C8 Z06 while I still can get in and out of it without too much help?

Do it, C8 Z06 is a hell of a car. That engine sound is intoxicating, plus if you look around, especially out of state, you can find MY24 for $5k – $10K below MSRP. Quite a different dynamic than just a year or two ago when people are paying $10K and over MSRP to buy one…yeah people are just smart and rational or perhaps just too drunk and rich to care paying over sticker

OMG, I was always beyond disgusted with those “manufactured” sounds. It just seems so lame to fake a car sound. Now I know that it is a marketing tool that works.

I would offer counter-advice that money is much more lovely than overpriced cars, especially if we get a blast of QE, and your dollars quintuple.

It is sobering to reflect that in a $23.5-trillion dollar economy, a single company like Apple or Microsoft can be worth one trillion buckeroos in their own right.

It just goes to show that if you have a garage and some ingenuity stewing around in your back pocket, convince your folks to let you tinker. If you’re anything like Jeff Bezos’ parents (now fabulously wealthy) they’ll thank you.

Which, for me, points up the obverse — the zillions of people conditioned to NOT do that. The crowd is an odd phenomenon of its own, and I find their shared norms and reward systems quite weird.

Exactly

American ingenuity is well rewarded

Invent the next useful sprocket, fix that doo dad or engineer whatever. You’ll be rich. Maybe not happy, but at least rich. 🎉 💰

DX 1M might test Sept 2022 high (recession), before plunging to the 80’s (inflation, higher CL).

The highest deficits are associated with the largest declines in currencies.

If a state government pays a contractor $10 million for road repair, facility construction, etc., that’s government spending, but when the contractor hires a subcontractor for $1 million, that’s private sector spending, right?

If the whole project is $10 million and got counted in GDP as $10 million, how it then gets split up is irrelevant, including labor and materials. The $1 million the subcontractor got doesn’t get counted again. It’s already part of the $10 million.

Should we be concerned about that debt to GDP ratio…?

No. Not yet. There are other countries that are worse. They will be the canary in the coal mine. When they start having problems…..it might even be good for the USD. Sort of hard to believe.

Believe me, it’s not good, try finding a house to buy

We should be concerned with low savings to high deficits.

That consumer spending chart is crazy. Up 5 trillion since 2010. When 70% of the economy is consumer spending….wow. No wonder the stock markets are rocking.

I think the economy could use some tax increases to slow deficit spending but you do not get elected or reelected raising taxes.

…and you don’t get re/elected by slashing spending, either.

Seems like problem of incentives.

The key is to convince the public that some are unworthy and therefore it is good to raise their taxes and slash spending that effects them.

Hi Wolf. You have covered the industry in the past. I am just curious.

I saw Carvana stock popped after earnings today. I have not looked at this earnings yet but in May, they said GPU was $6500. In comparison, Carmax was $2500. How does Carvana do so much better than Carmax or maybe I am missing something?

May, 2024

Carvana = Record Q1 Total Gross Profit per Unit (“GPU”) of $6,432 (+$2,129 YoY) and Non-GAAP Total GPU of $6,802 (+$2,006 YoY)

Today, 2024

Total gross profit per unit (“GPU”) was $7,427, an increase of $1,475

Sept, 2024

Carmax = Gross profit per retail used unit of $2,269 and gross profit per wholesale unit of $975, both in line with last year. Extended Protection Plan (EPP) margin growth of $69 per retail unit to $575 and service margin growth of $84 per retail unit from the prior year’s second quarter.

I was looking at an older investor presentation from Carvana this year and they are projecting over $7000 GPU going forward.

There was a handful of these online-only publicly traded used vehicle dealers. And most of them vanished last year. Carvana extorted $1 billion of debt forgiveness last year from bondholders, and survived, and now stock jockeys are going nuts over it.

MO popped as well, but I suspect that they will do well moving forward as more and more people lean on their addictions to cope. As far as I can remember, this was the only stock Alan Greenspan ever admitted to owning. The dividend has been excellent for as long as I can remember.

If Hollywood is any indication, which it is not, seems like the anti China rhetoric and policies will continue. Had to completely stop watching a show where it had China forcing the American invasion of Mexico so China could be justified in invading Taiwan. Oh, and the main character is ensuring Americans are protected from learning Russian and Chinese. Given the use of military assets comes with having input to narrative it is pretty interesting. China and the world, including the US are tightly connected. Nobody should want to see a breakdown in relations play out.

I was lucky for having worked for the CCP that transformed my POV, This giant facility would only provide a necessary resource for 1,5 million Chinese people. Being grounded in experience rather than emotion, they bought it they own it.

“The authoritarianism, in politics and government, the blind submission to authority and the repression of individual freedom of thought and action. ” as defined by a credible source.

What scared me the most was that I experienced the desperation of most of the good people that make life worth living.

Authoritarianism, as you provided the definition, comes in many forms. Sometimes from internal sources and often times from external sources. Pinochet in Chile being supported externally to overthrow a democratically elected President, and of course Pol Pot, where a significant portion of the population starved and many executed, brought about by the largest bombing campaign (and illegal) of Eastern Cambodia and Laos. Interestingly Pol Pot was supported by the UN until 1993, long after their crimes were well known. A very complex world we live in with many hands on the levers of change, often to the benefit of the few. You can choose almost any country at random and see that at work.

My point is however that creating a false and reductionist view of China in a tightly coupled world economy is not a good idea, especially in cases like extreme tariffs but also just propagating the red scare continuously. There is a balance that can be struck where all boats can be lifted with a rising tide.

…whilst even momentary relief from the endless stream of financial/cultural/environmental (the ultimate supply/demand factor) termites that constantly-chew on the legs of a ‘level-playing field’ table of planetary market competition appear remote as ever…

may we all find a better day.

Yeah Dustoff, I’m kinda down, too. It’s the election……once more we are facing the cancer or the train wreck….or maybe the can can be kicked further…..I just wrote in Bernie for the third time……..

Still very grateful I’m not in jail or under a bridge and headed there.

And……we will likely get to see what the wealthy will do with the poor….or if they can hide from them…..with more than our share of life finished…….that is selfish…I know.

Wretched species.

The gdp is 3 pct positive, according to the equation is equal to the sum of

C = personal consumption expenditures

G = government expenditures

E = exports of American goods and services

I = imports of goods and services

The E-I, net exports, the Trade Deficit, has been running at negative between 6 and 10 for the past two decades.

Which logically leads us to the question:

How the hell have we been paying for the obvious Fed sponsored financial keggar.

Wolf,

I do agree that the US has been the primary free trader in the world. By that I mean nearly the only country that allows imports with no pushback ie tariffs or regulation. It has helped the folks on welfare that don’t work (Walmart stuff is cheaper) and the very rich but has impacted the middle class and working poor with lower opportunities/ wages. I have read the cost of an Apple phone built in the US would only be $20 more!

It is silly to think tariffs will replace income taxes but tariffs either generate revenue from the tariff or higher income tax revenue from work moved back to the US. Hopefully that could be used to reduce the deficit.

It is important to apply tariffs from top to bottom otherwise games occur. I would also argue to apply them over a 3-4 year period to allow the market time to adjust.

Finally to argue with the folks that think there is little competition- cell phones are a great example. You can buy a cell phone for as little as $20 – yes it only does calls and text. A cheap smart phone is $50. But if you want the latest and greatest with a huge screen etc – you can pay $1000 to three or more different companies. That is a perfect example of a competitive marketplace. marketplace.

@Bob: You said:

“inally to argue with the folks that think there is little competition- cell phones are a great example. You can buy a cell phone for as little as $20 – yes it only does calls and text. A cheap smart phone is $50. But if you want the latest and greatest with a huge screen etc – you can pay $1000 to three or more different companies. That is a perfect example of a competitive marketplace. marketplace.”

Wrong. Competition can only occur between comparable products. A Toyota Corolla is not a competitive product to a BMW 3-series though it can be competitive to a Nissan Sentra.

You are talking about a product range that can go from low-end to high-end.

And you can stifle competition for any part of the range (or any product for that matter) by imposing targeted tariffs or using other retaliation tactics.

In the high-end smartphone space, Apple, Google, and Samsung have basically formed an oligopoly. Much like a lot of our other industries.

Wolf, this is an off the wall question:

I believe legit / sustainable GDP growth comes from invention, productivity improvement and growth in population.

Unsustainable GDP growth is driven by the government borrowing or creating money.

I realize this is a very simplified view.

How much of the current GDP growth in constant dollars are in category 1 vs category 2?

Thanks you have great information.

Yes of course. The problem is that productivity has increased without a consumurate increase in wages for the only people in the US that matter. The blessed working people.

Bob,

RTGDFA

What you said, “What dragged on GDP: The trade deficit worsened further, driven by rampant consumer spending and expected consumer spending on goods, a portion of which are imported.”

Which is technically correct ignoring the Trade Deficit which has a life beyond our lifetimes. 3 – 7 years were I too guess.

Bob

the GDP is the money value of everything produced. So it was produced using current inventiveness and labor and everything else you can think of.

Irrespective of anything else the economy has shown that with current resources it can produce all this.

Now the question of debt. Debt and government borrowing only influences what gets produced. For example if the government took on massive debt and started paying for portraits of Harris, it would add to GDP but no one wants that shit. So it is unsustainable.

Larger portion of government spending only distorts mix of production. You could argue that if government stopped portrait productions, a lot of painters would be unemployed and GDP would fall unless they can start painting something else.

It is complicated which is why everyone is confused. But in the end debt to gdp becomes a drag one way or the other.

DM: Ford CEO says he can’t live without his ‘Temu Tesla’ – a $30k EV that he flew in from China

While appearing last week on Robert Llewellyn’s ‘ The Fully Charged Podcast,’ Jim Farley revealed he drives a Xiaomi SU7 delivered from China.

Hi Wolf. Some people are expecting this increasing debt to GDP/ fiscal spending to become a headwind for the economy in the near future. Do you expect something similar? And a novice question why would that happen? Any thoughts on timeframe? Thanks

Not the “near future.” Debt-to-GDP issues play out over the years.

We could eventually get a revolt of the bond market at this pile of issuance, which would dive longer-term yields higher, and if the 10-year yield hits 6% or 7%, it could slow some business investments and bash the housing market, pull the rug out from under the stock market, etc., which would eventually lead to slower growth.

I’m more and more convinced that we won’t get a recession until the AI spending bubble blows up. And that’s going to happen some day.

Wolf, AI spending is one part of private investment. I think the aggregate has been well behaved but within this aggregate there is disproportionate AI spending..which implies something else is slowing. Do you any data on this? Is this even true?

But agree with your assessment that without AI investment slowing a recession is very unlikely.

Side note: Ever thought of writing a book on econometrics? A guide on where to find data and how to use the confusing Fred and related tools?

AI spending is much more than just investment. It’s huge salaries that then get spent as consumer spending; it’s office leases; money made by investors on their startups that then circulates, power plants getting built and taken out of retirement; data centers getting built (construction), power sold to data centers (industrial production). etc. etc. There are AI conferences that people travel to, consultants being hired, it’s now everywhere all the time. This a huge amount of money that is now circulating.

Overall PCE +2.1% yoy, core PCE +2.7% yoy

Services inflation continues to run hot and now durable goods are pushing up on inflation.

In the circular flow of income, unless savings are expeditiously activated, then a dampening economic impact is generated. It was called secular stagnation.

As the ratio of transaction accounts to savings investment type accounts in the banks has doubled, the velocity of circulation has increased.

Globalization has been bad for developed nations. Now we are paying the price, including the US divisions. But it kept the inflation low for decades. If some tariffs are introduced then that could be good for US. But it will be bad for inflation. This cannot be demonized, it needs a lot of careful planning. Saying that we can drop lot of taxes makes all the discussions evil.

” But it kept the inflation low for decades.”

What is you starting point? That was a pretty broad statement.

Starting 90-ties AFAIR.

With the baby boomers retiring (and dying), the vast majority of Americans in the “market” have never had to be frugal and have known nothing but the the “Fed put” as they are all post Greenspan. They do know how to spend however!

Interesting times.

Half of the USA has millions and the other half has nothing.

One group can spend as much as they want and the other group spends every penny they have.

Inflation is really low compared to where it’s headed.

I dunno,

I don’t spend much except on bills and necessities to keep this rock concert going. And well I’m doing ok. Still I have to watch the spending pretty darn closely.

You’d have to be making a million a year not to care at all. I think

I don’t care. I live big. My wife is a vegetarian, so my home not seeing meat often.

Today I have cooked Chicken Fricassée. I feel like I’m going overboard and not deserving the luxury but YOLO. I feel so RICH doing this. After an exercise the extra protein is welcomed.

I encourage others to go back to the base and enjoy simple things.

My brain is convinced that this is better than having a chopper or yacht. Train your brain. A hint: anything that is “enjoyed” in America is bad for you :)

Every country which runs significant trade deficits like the US does should impose material tariffs, no question about it.