Lennar’s incentives jumped to $48,100 per house, prices -5.8% year-over-year. Builders take share from existing houses, where demand wilted because prices are too high.

By Wolf Richter for WOLF STREET.

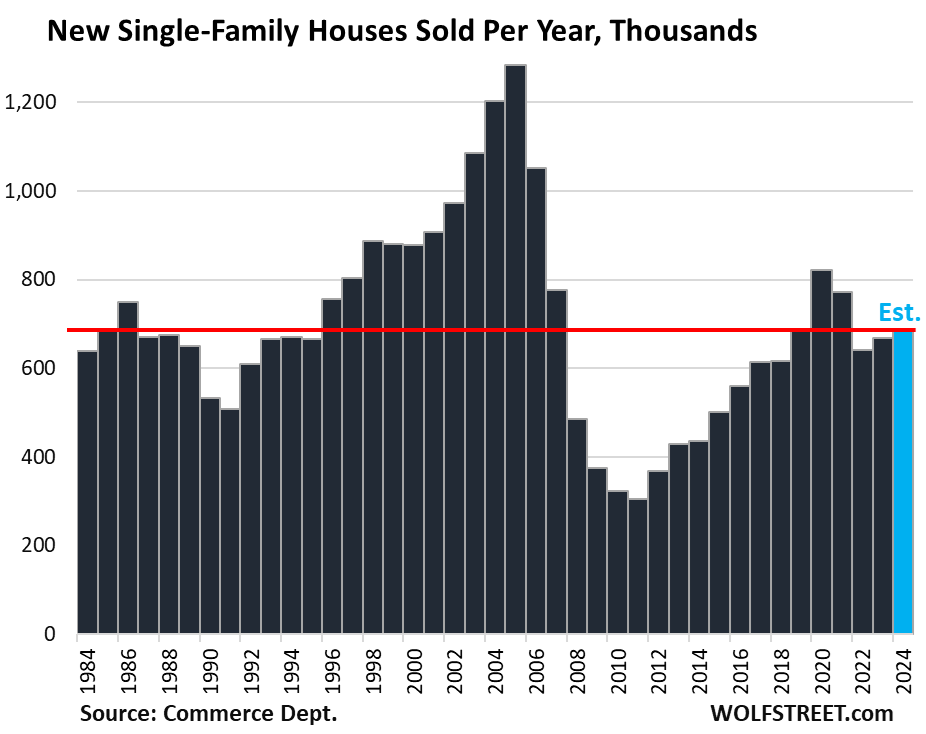

Sales of new single-family houses at all stages of construction rose by 7.3% year-over-year to about 59,000 houses in September, not seasonally adjusted. This was also up by 7.3% from September 2019, according to Census Bureau data today.

Homebuilders are building and selling houses at a brisk pace, motivating buyers with lower prices, big incentives, and mortgage-rate buydowns that are costly for builders, but that make new houses often less costly for buyers on a monthly basis than equivalent existing houses.

For the first nine months of 2024, sales of new houses at all stages of construction rose by 3.2% from the same period in 2023. Using this increase as a factor applied to the remaining three months of 2024, we estimate that sales for the whole year will grow by 2.9% from 2023, to 678,000 houses, just a hair above the level of 2019, far higher than any of the years between 2008 and 2018, but below the heady free-money years of 2020 and 2021.

But homeowners who are thinking of selling have been clinging to their aspirational prices, and so inventories of existing homes are piling up, supply is spiking as sales have wilted. The year 2024 is on track to produce the lowest sales of existing homes since 1995.

And demand has shifted from existing homes to new construction as homebuilders, the pros in this business, are taking advantage of homeowners’ refusal to adjust their pricing to reality.

Inventories balloon: a good thing, but not for builders.

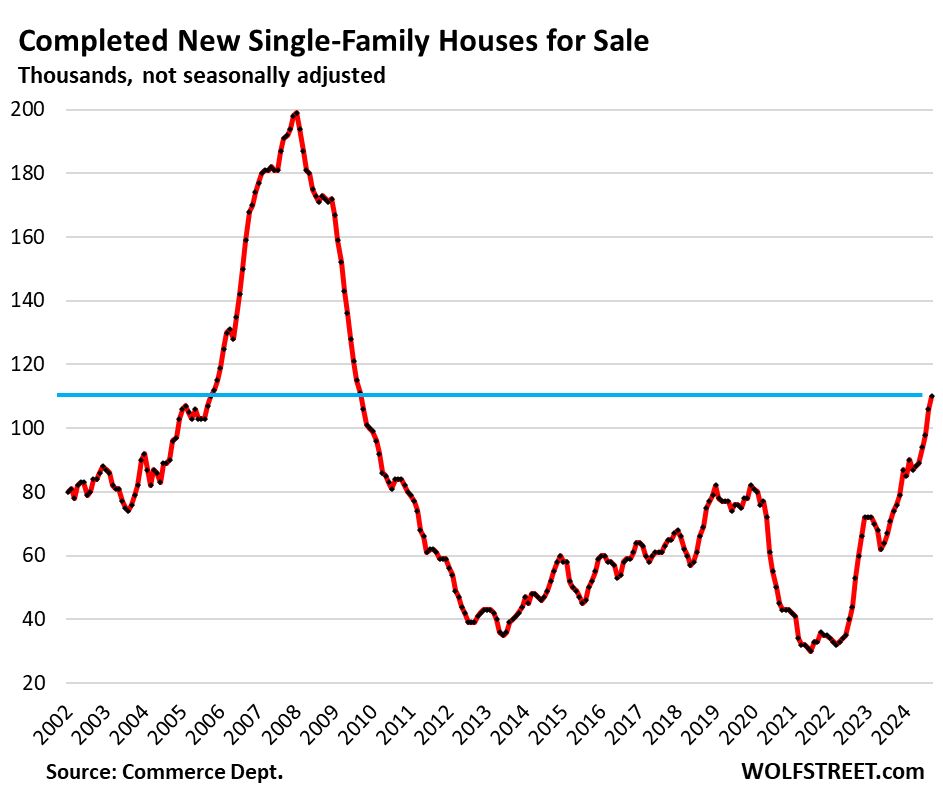

Inventory of new completed houses jumped by 49% year-over-year to 110,000 houses, the highest number of houses since August 2009 when homebuilders were trying to survive the Housing Bust.

Sales of these “spec houses” account for about half of total sales, the other half being houses in various stages of construction.

Spec houses are essentially move-in ready, and many buyers find that appealing, rather than having to wait for months before they can move in. But builders have tied up a lot of capital in spec houses, and they have to be sold quickly. Rising inventory of completed houses encourages builders to lower prices and offer deals.

This buildup of spec houses is a big positive for the overall housing market – the bigger the inventory of spec houses, the better – it will help resolve the massive dislocations in prices that have befallen the housing market. But it puts the squeeze on homebuilders’ margins, as we’ll see in a moment with Lennar.

Sales of completed new houses jumped by 29% year-over-year to 27,000 houses (not seasonally adjusted), as homebuilders motivated buyers with lower prices, bigger incentives, and mortgage-rate buydowns that are costly for homebuilders.

But they’re not selling them as fast as they’re building them, and supply of spec houses has risen to 4.1 months at the current rate of sales, which is still in the normal range, but more than double from where it was two years ago. During the Housing Bust, when sales collapsed, supply exploded to 11 months at the worst moments.

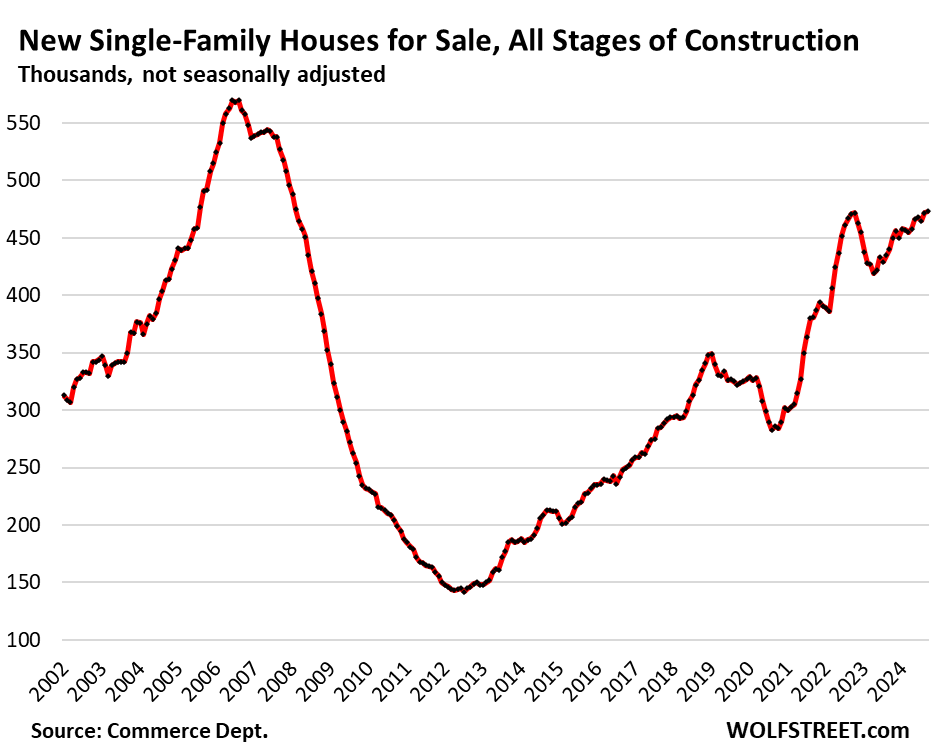

Inventories of houses at all stages of construction – from not yet started to completed – rose to 473,000 houses, the highest since February 2008, having eked past the highs in the fall of 2022. Supply rose to 7.9 months.

Prices, mortgage-rate buydowns, and incentives.

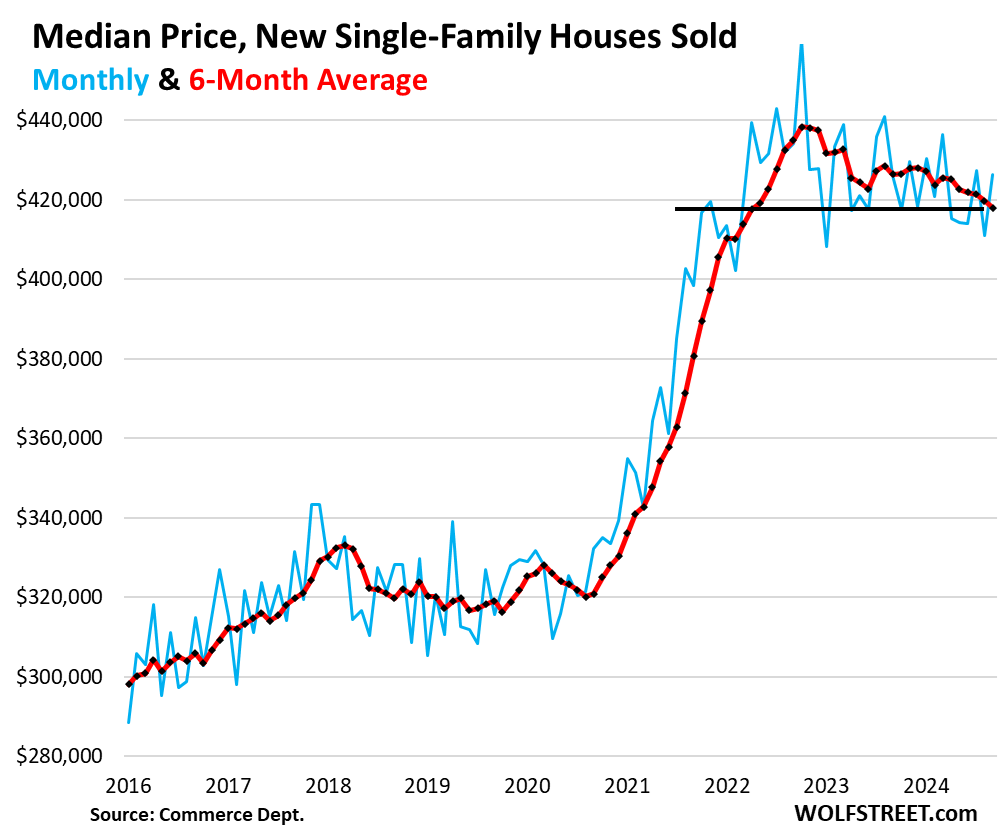

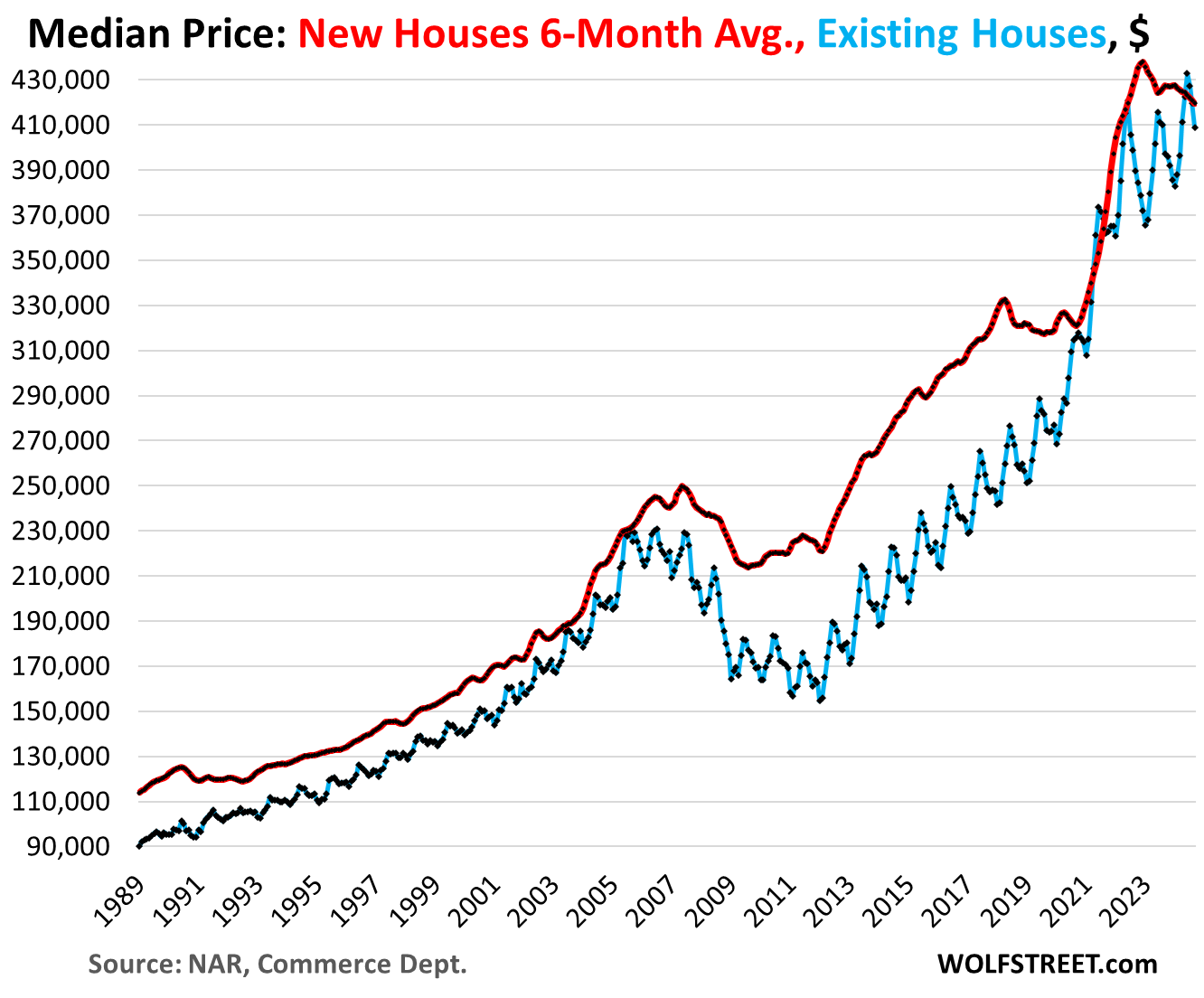

The median contract price of new single-family houses at all stages of construction is a volatile metric with big monthly revisions (blue in the chart below). For example, the August price was revised down by $10,530 today. So we look at the six month average, which irons out the month-to-month squiggles and revisions – to see the trends (red in the chart below).

In September, the median contract price was $426,300. The six-month average ticked down to $418,000, the lowest since May 2022 and down by 4.3% from the peak in October 2022.

However, these are contract prices, and they do not include the substantial costs to homebuilders of mortgage rate buydowns and other incentives – which are big values for buyers. We’ll look at homebuilder Lennar in a moment.

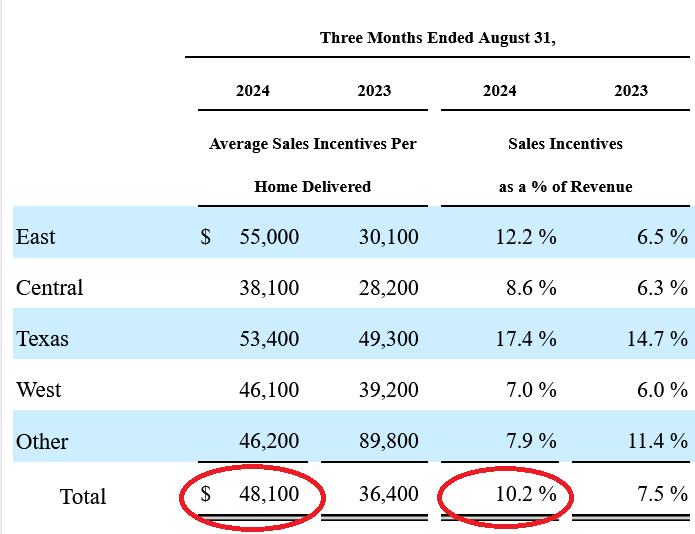

Lennar disclosed in its Q3 quarterly filings that sales incentives, including mortgage-rate buydowns and free upgrades, cost on average $48,100 per house it sold in Q3, or 10.2% of revenues, a 32% jump in incentive costs from a year ago ($36,400 on average per house, 7.5% of revenues).

In addition, Lennar’s average sales price dropped 5.8% year-over-year to $422,000 per home. Those prices are reflected in the contract prices by the Census Bureau.

But homebuyers got $48,100 in additional incentives as part of the deal, including the costs of the mortgage rate buydowns, a value that wasn’t reflected in the contract prices by the Census Bureau.

It was reflected on Lennar’s income statement though, and gross margin was squeezed by 2 percentage points compared to a year ago, to 22.5% in Q3 2024, from 24.4% in Q3 2023.

These are big benefits to buyers of new houses that end up producing a lower monthly payment and a nicer house.

In this way, homebuilders are keeping their sales up, even as sales of existing homes have wilted. They’re taking market share, and homeowners haven’t figured it out yet.

Prices of new houses versus existing houses.

Contract prices of new houses (which do not include the benefits to buyers of mortgage-rate buydowns and other incentives) have eased down from the peak (red in the chart below).

But the median price of existing single-family houses is still completely out of whack though it dropped along seasonal patterns (blue).

Given lower prices, mortgage-rate buydowns, and incentives from builders, new houses on a monthly payments basis can out-compete existing houses, and so a portion of demand has shifted from existing houses to new houses, which is a factor in the demand destruction taking place in the market for existing houses, where prices, after a 50% jump in two-and-a-half years are far too high.

The big homebuilders have figured out how to deal with this market. Unlike homeowners sitting on vacant houses waiting for lower mortgage rates or whatever, builders have to build and sell houses to keep their revenues flowing and to keep their businesses intact, and they’re doing that.

This long-term chart shows just how unusual this situation is. The median price of new houses was substantially higher than that of existing houses even during the Housing Bust.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Good post. I took a quick look at Lennar’s 8/31/2024 10Q quarterly financial statements filed with the SEC. It’s crazy, even with incentives increasing 32% from the prior year to $48,100, they have been able to raise their earnings per share from the prior year, $3.87, to $4.26, a 10% increase. They still have a lot of room to add additional incentives and drop prices more, when necessary.

yes, builders have lots of room left to get very aggressive with their pricing and incentives to keep volume high, adding supply and making deals.

Wolf, going to need some help here. I’ve read the article twice. There are numerous mention of the word house but no mention of what kind of house. Two br bungalows or 10 br mansions.

I ask this as during the 70s, after a difficult time not all dissimilar to now, the builders recovered by building smaller cheaper houses for a period. Has/is this occuring now?

Asking for a friend.

Here’s your help: Listen to the Rolling Stones song, “You can’t always get what you want.” My all-time favorite, especially recommended for people who grew up always getting what they wanted, and read the lyrics that display on the screen of the video.

https://www.youtube.com/watch?v=Ef9QnZVpVd8

(“but if you try sometimes you might just find that you get what you need.”)

Builders are building what is selling, meaning where the demand is. If there is demand for mansions with pools, that’s what they build. If there is demand for houses people can afford, that’s what they build.

“You can’t always get what you want. But if you try sometimes you might just find that you get what you need.”

I would be curious to see data on the $/sqft of the new homes plotted along with the average selling price.

San Diego Diego Broker and investor here. Yes! I travel all the time and interview new home builders in all the cities. What I learned is the higher priced builders sell their unbuilt land to builders like DR Horton, who can move first time home size easier. They also put sold signs on spec homes to make them appear busy/ more desirable, have 50% cancellations in some areas and I’ve seen new build here in SD county adjusted from 1.5M to 1.2M with more incentives available still. I’d hate to be the guy who bought the last 1.5M, bc that rate buydowm will adjust in a year or two and his new neighbor will be paying 20% less for the same home.

I quit working with buyers last year for the most part. I will not encourage people to buy in the This market. With few exceptions. I’m one of the good, truthful, successful, small realtors in SD who cares more about people than money. Thanks for reading. Jennifer

Which begs the question, why aren’t all the angry people that comment here (DC, The Bird, etc.) upset with the builders for taking too much profit. Seems as irrational as their other complaints.

They wouldn’t be doing this if it wasn’t for the massive inflation of the past five years. It’s not their fault that people FOMOed.

What this tells me that if a home builder can offer all these incentives and still make profit, then the current market is too high.

If the homebuilders are offering incentives and still make a profit than home prices are still too high?

Huh?

How many companies do you think will build houses if they don’t make a profit?

JimL,

You might want to ask yourself why very highly leveraged purchases (houses, autos, college tuitions…) seem to be the primary markets where the alleged “sticker price” is actually well in excess of actual “acceptable price” (price at which *some* transactions manage to get closed – which are also presumably profitable per your own observation).

Basically, my sense is that high leverage transactions (grossly facilitated by the G’s interest rate manipulations),

1) Allows vast inflation of sticker prices (wholly divorced from production costs) through the artificial creation of lower/stable monthly amortization costs – with the residual default risk sold off to 3rd parties (who are simultaneously being starved of yield in the savings markets)

2) Those leverage-inflated sticker prices leave a *huge* amount of room for sellers to discount to the hardest-negotiating buyers – and *still* make more-than-decent profits.

That why’s $50k worth of incentives are possible…because the home builders are marking up SFH prices $200k-$250k above their production costs.

3) But the whole inflation/price volatility w*orehouse is made possible due to the Fed’s stangulation of honest interest rates.

So who should regulate how much profit is “too much” for a private business? Why not go after the healthcare industry for pulling the same $hit?

Mr. Market is the decider. The problem is Mr. Market has been in bed with all sorts of folks and is no longer run by “We the People.”

It certainly varies by industry (look at tech and antitrust rulings globally). Regarding construction it’s local and regional regulations that can skew the market.

I used to be able to just build a house. Now certain builders favor different areas based on regulations and codes. In my community there’s all sorts of governing bodies that weigh in. Historical preservation and environmental regulations (“green” building codes) make it costly for many things.

Economies of scale have always existed but the Big Boys are incentivized to a great degree as they’re able to build neighborhoods, whereas the little guy can only build a few homes at a time.

The same is true for many industries that, the “more productive” companies (BIG) are given advantages and enabled to grow bigger and shut out competitors.

Builders don’t set prices the market does. They compete against existing homes so they need to stay in line with existing home prices or they’ll be priced out.

Prices are up across the board. They’d be much more if builders didn’t continue to add supply to the market.

Perhaps new builds are not available in their markets.

I dont know a lot about it but if I learned that any builders had lobbied or maybe still do lobby for the govt to buy mbs, which fortunately for the whole country isnt happening now, and hopefully never does again, then I wouldnt be too impressed with the builders. I dont care if the excuse would be, well its to increase profits, I think it damages the country in net, but thats just my feeling.

Our subdivision typically has two builders paired in each section. In our section it was Lennar and Ryland. Lennar worked hard to keep an inventory of spec homes. Ryland wouldn’t start building until they had a contract in place. As a result, Lennar sold out our section months after we moved in while Ryland took another two years.

There is a cost to holding inventory but there is also a cost to inaction.

So Lennar is throwing down 11.4% of their gross margin to buydown rates for buyers and they still have more than 22% gross margin. A third of their gross margin is going to buydown mortgage rates. And this has been going on now for probably 3 years?

And people wonder why new homes are still overpriced despite a decent drop taking the cream off the top.

It’s still insane, but this is the new normal with approaching $2T in deficit spending which is extraordinarily buoyant to the economy.

I really hope with see a continued acceleration of core inflation that spills over into headline by January, so we can start hiking rates again. It’s late 70s / early 80’s all over again.

Look at their SEC filings. Net Margin is at around 7-8%. I mean compared to many industries that pretty slim. They are for profit companies, I can’t imagine Wall Street investors would accept margins much lower than that.

That’s high. Retailers are around 1% to 3% net profit margins. Grocery stores are 1%-2% net profit margins. Albertsons was 0.8% in Q2. During the high-inflation period, it briefly went as high as 2.5%, but that was unusual.

10% increase earnings growth lmao. That’s it??? They were buying their own shares too. Look at their backlog n revenue growth.

Sell.

Very expensive price to book. Homebuilding is an asset based business.

In our subdivision, existing homes sell within days when properly priced, while new construction homes sit on the market for 3+ months. Also, 69% of all existing homes are cash sales, so mortgage buy downs are not a factor and they typically close in 2-3 weeks. Last month, a 20-year-old house across the street was listed for $1,795,000 and closed three weeks later for $1,845,000 cash sale. Similar sized new constructions are priced about $2,500,000 and sit on the market for 3-4 months before closing.

I’d hardly call a neighborhood with 1.5M+ houses a “subdivision?” What did it look like before the division?

But I digress..

I had occasion too visit such a sterile neighborhood and I was thankful I didn’t live there.

You obviously don’t live in coastal California.

69% cash sales doesn’t sound representative of the national single family home market. But hey yeah if I drive up to Vail or Aspen, the majority of those are cash sales and well above the $2.5M price point

This shows that builders cannot unilaterally increase prices, they compete against existing homes.

Wolf,

On your median price graph at the end, why didn’t you also do a 6mma for existing houses?

The median price of existing houses peaks in June and bottoms in January, like clockwork, 6 months apart, and all the 6-month average does is shift the peaks and valleys by three months. The chart looks the same, but shifted and with slightly rounded corners. So that’s not helpful at all. It’s just confusing.

To iron out the June-peak-January-valley, I would have to do a 12-month average.

The median price of new houses however is hugely volatile in a random manner, not seasonal. It just spikes and plunges month to month, made worse by huge random revisions, up and down.

I really appreciate the comment about existing home sales. Sellers got too used to the price increases during the pandemic. I unfortunately had to sell a property in California in 2023 for a loss. Unlike most people, I didn’t want to wait to find out prices wouldn’t increase and continue to pay high property taxes and insurance. Had I taken the advice of others, I would have just lost more money. It’s the sunk cost fallacy.

I wonder how much builders pay for land and for construction. Using Lennar’s data, the average sales price was $442,000 with $48,000 in incentives. This makes Lennar’s averages sales price $394,000. Subtract the price of the land, cost of construction, cost of doing business and you get their profit. Or am I reading this wrong? Any ideas?

As a potential cash buyer, laying out $400,000 would lose me about $20,000 in interest this year (and the same next year, and the next, and so on, if interest rates stay about the same). $20,000 is about what I pay in annual rent, and I don’t have to deal with maintenance, insurance, landscapers, garbage, water, sewer, appraisers. If the refrigerator breaks, the landlord replaces it. If the surrounding area goes to hell, which happens more often than you think, I could be out of here in 30 days.

It would not bother me much if the place burned down or is destroyed by a hurricane or earthquake. I would prefer that not happen, but it is no big tragedy if it does. If that sort of stuff happened to a house I owned, that would be a big deal.

Builders pay a lot less than what you’re thinking for the land. These are typically larger developments with 1,000s of homes. So typically they’re buying 100s of acres so their price per lot is extremely low. You then factor in concessions from towns for roads, parks, development incentives, future assessments, etc. and land cost is very cheap.

It’s the other factors that are hard to control especially after COVID. Labor and Materials wreaked havoc for a while.

In terms of your first paragraph, you’re reading this wrong. The “contract price” is written into the contract, which is what the Census Bureau uses for its price data. Lennar includes the cost of the mortgage rate buydowns and other incentives in its gross margin calculations. Its gross margin is 22.5%, after all the incentives and everything. While down from 24.5%, it’s still a very healthy gross margin.

But that’s not what the Census Bureau tracks. It tracks the selling price in the contract. And that’s what the data is based on.

Their net margin is 7-8% so they are not pocketing 22%.

That’s pretty high. Retailers are around 1% to 3% net profit margins. Grocery stores are 1%-2% net profit margins. Albertsons was 0.8% in Q2. During the high-inflation period, it briefly went as high as 2.5%, but that was unusual.

Man, covid really broke a lot of things and help set some weird new records…record low mortgage rates in history, record how price increase in short duration and if I read that chart correctly also another record when new home price is less than used home (if I read it wrong, then blame it on I need new glasses)

New home is nice and if it’s cheaper with more incentive, even better but a major downside is I think most new builds now come with HOA requirement…part of the appeal of owning a non-condo/townhouse is not to pay HOA or be subjugated to some insane HOA board members making up crazy rules. Second downside is, for people living in metro part of SoCal or NorCal, new build is much less of a factor so really can’t take advantage of this as much.

Just go 50 Miles away from coast in socal and you have plethora of new builds..

I want to move away from coast in next few years .

The concern with moving away from the coasts in SoCal is wildfire risk seems to increase significantly with each mile as you travel eastward.

Fire risk in CA has more to do with local topography, is it hilly and wooded, highest risk places are like that, and as long time Bay Area people remember, you can have a horrendous fire in places like the Oakland hills, whereas a place like Modesto isn’t really at any fire risk.

Are builders using this to pad profits? Are they running the HOAs?

The uk has an ongoing issue with house builders making their properties leasehold – which basically means very long term rental with automatic renewal rights – and flogging their customers by boosting the “ground rents” unreasonable amounts every year. It’s the first thing I think of when I see these hoa fees.

The other problem with HOAs is the people in charge overpaying their brother in law to mow your lawn. Or just overpaying someone else because they’re stupid.

HOA would have me up at night seething. My worst nightmare.

Can anyone tell me if some HOAs don’t let you plant trees because it increases yard maintenance costs? Trying to answer my own theory…

MussSkye – HOAs are a mixed bag. Ours specifically states you have to have three trees in your front yard and even has a list of which ones are acceptable.

My biggest problem is their micromanagement. I got a compliance letter after replacing my fence in kind. They said I didn’t ask for permission. I told them permission wasn’t required because I was maintaining an existing asset and that they should be sending a letter to the neighbor down the street whose fence was falling down.

(me seething at night)

At least you guys have trees!

Try golf course in Homes county Florida. No Hoa and low taxes. Great.

And no hurricanes, no stinky red tides, cheap flood insurance and your neighbors are MAGA lunatics…

NO THANKS!

Data support this narrative of economics in telling the story. That’s why I visit Wolfstreetgood data and narrative. The comments section is quite entertaining as well.

Re: “homebuilders, the pros in this business”

It’s my understanding, that the big home builders are basically unregulated banks, or essentially the equivalent of financial conduits, that manage money foremost and then subcontract labor to efficient crews.

That’s a very simplified concept— but what stands out is the financial leverage and flexibility these players have in this housing war.

As we watch existing homes pile up in an epic train wreck, these monster builders are going to morph the housing downturn, into a bloodbath.

As existing homes engage in mass denial and wage a long term strike, these building vampires are going to suck potential buyers into their graveyards.

The existing home Frankensteins will be left in the wind like ghosts,in forgotten ghost towns.

As mortgage rates levitate higher, the new builders, wearing their banker costumes, will be shooting fish in barrels.

Happy Halloween!

What you say isn’t wrong, but one advantage existing homeowners have over new home builders is location.

Existing lines are generally in more sought after areas. Homes were originally built there for a reason. In many cities new homebuilders are building far away from city centers.

Granted the power of this advantage may vary, but it is a factor.

Builders are cutting prices, bc building new houses is a mistake. They

rush it, bc completed new single family houses are piling up on the cusp of systemic change in the RE market. The boomers need only one floor,

no carpet, to prevent falling. The zoomers need Land/apt to cut cost.

Interesting subject, existing vs. new construction and the business dynamics. I have to agree with a previous comment made on the subject:

Existing homes are selling one hearse at a time. Thanks, Wolf!

Production homes (aka tract homes) do not hold their value. You get what you pay for is a statement of fact. They may be new, but they are not built well. Many bedroom community neighborhoods fall victim to suburban poverty. Always buy location first, and then house. And make it a well-built home.

And don’t get sucked into the “Keep up with the Jones” square footage game. Build a reasonably sized house that you will utilize the majority of spaces most of the time.

I wonder about this too. In my northern California town new build prices are plunging and incentives growing, as Wolf notes. But I look at these houses, cookie cutter, large square footage on teeny lots, and they are just…depressing. In addition the locations are outlying and thus closer to the fire zones.

I’m feeling better and better about not being seduced by the newness and buying my 1955 bungalow in early 2020. New HVAC, solid plaster walls, inground pool, and walking distance to grocery stores, downtown, and the park.

New homes are built so close together you can spit from your bedroom window into your neighbor’s bedroom.

I’ve noticed this too. Much of the benefit of not sharing a wall (condos) goes away when there’s only a few feet between your wall and your neighbors.

I live in a newly built home of 1,459 sq.ft., one level. There are about 20 homes on my street (a cul-de-sac). We have very wide streets, actual concrete sidewalks, and small yards. I am in a quiet area (low traffic) and two miles from anything I need, including a major hospital system. Everything here is NEW and under warranty for 5 – 10 years (A/C, appliances, house structural, etc). The house is very energy efficient, may I add.

Who lives here? Well, mostly young families starting out, young couples with no kids and good jobs, retirees (like me @ 81 years old). There are NO rentals on my street and in the entire subdivision, maybe two out of 300 homes.

Our HOA fees are $500 annually and their “job” is to maintain the common areas and write “tickets” for folks that are keeping their lawn cut and landscaping visually acceptable.

What does it cost to live here? It’s actually pretty inexpensive, and is around $900 – $1,000 /month for me (house is paid off) and that cost includes all utilities, fiber internet (1 Gig), homeowners insurance, and PROPERTY TAXES. This are house cost expenses only, not food, car insurance, health insurance, etc.

I still cut my own grass which takes 30 minutes if I am taking my time. The outside of the house is brick and Hardiplank which is low maintenance.

These new places can be a good deal if you want inexpensive living. What will the future hold for this piece of real estate I own? Don’t know , but there are thousands of these starter homes being built and they seem to get sold and people are happy at the cost to buy and own one. There’s more to living than worrying about whether or not the “value” of your house is going up or down.

As an alternative, I can move into a 55+ age apartment complex near me with other old , sick people for about $2,000/ month (one 750 sq. ft. bedroom – rent about $1,800, utilities about $200). Oh, if I want a garage for my car, add $150/month, otherwise, the car sits in the hot Texas sun all day.

And no, I am not going to move in with my daughter and her husband!

Correction:

“Our HOA fees are $500 annually and their “job” is to maintain the common areas and write “tickets” for folks that are NOT keeping their lawn cut and landscaping visually acceptable.”

Kentucky et al.

Good lordy. People all over these comments are whining about how expensive and unaffordable houses are, and then you come along and tell people to not buy a new house that they could actually afford because it might have cheap windows and be in a neighborhood where prices might not soar in the future.

What kind of bullshit advice are you people giving to struggling homebuyers looking for affordability? Whining about houses being too expensive, and then warning about the houses people could afford being too cheap? The bullshit gets knee-deep around here from time to time.

Listen to the Rolling Stones song, “You can’t always get what you want.” My all-time favorite, especially recommended for people who grew up always getting what they wanted, and read the lyrics that display on the screen of the video.

https://www.youtube.com/watch?v=Ef9QnZVpVd8

(“but if you try sometimes you might just find that you get what you need.”)

Thurd2,

I live in a very sleepy midwest/Appalachian metro. New homes are built on top of each other here too. It is very cost efficient for the builders and buyers line up for them.

Kentucky

Agreed, I had a top window contractor out to my home and he demonstrated builders of these tract homes put the cheapest pile of s$it, energy inefficient windows in these homes to maximize profits. Showed the energy loss right in my living room. The cost to replace all these crap windows can run 10 to $20K right out of the box. Then you’ve got all the other cheap crap they put into these homes. Be careful when you compare home value based on square footage.

Swamp Creature – for entertainment, read some reviews of DR Horton homes.

Some of these monster homes going up around me are a real joke. One was completed over a year ago, and I see more contractors in front of the homes making repairs to all the defects, than were there to build the home in the first place.

My niece in N.C. (Raleigh) works for Lennar as a Purchasing Agent buying building materials. Let me say that she says for ALL Lennar homes (low end, or otherwise) they get the same low quality materials. They most certainly don’t install Anderson (or other brand) top quality windows in their builds.

That’s homebuilding in the U.S. with probably all the very large home builders. If you want a “good” home, built with the BEST materials, you have to build it yourself (Indy builder, you pick the stuff out). I’ve done this before and it’s a gigantic hassle and costs roughly 25% more than you thought it would. And that’s money you will not get back in a sale.

I’ll just repeat it here: Listen to the Rolling Stones song, “You can’t always get what you want.” My all-time favorite, especially recommended for people who grew up always getting what they wanted, and read the lyrics that display on the screen of the video.

https://www.youtube.com/watch?v=Ef9QnZVpVd8

(“but if you try sometimes you might just find that you get what you need.”)

Builders are building what is selling, meaning where the demand is. If there is demand for mansions with pools, that’s what they build. If there is demand for houses people can afford, that’s what they build.

Wait!!!!

You regularly complain about house prices, then when there is news of houses selling at reasonable prices you complain about the cheap construction?

I detect a pattern: you complaining no matter what the circumstances.

It sounds like a you problem.

The argument can be made there will be issues with every new or existing home. New homes – okay cheap windows. Home built before the 80s lots of asbestos risks to consider if you want to remodel. Really old home lead pipes. More recent but not new homes the roof is probably coming up on the end of its useful life. Old homes – electric issues and probably don’t have energy efficient heating and cooling systems or appliances.

I have owned several homes. Each one of them increased in value, subsidizing the purchase of the next home. My current 26 year old production home has been selling for 3X what I paid for it.

I think you may be full of the stuff that makes the grass grow green.

Presumably the mortgage and down payment amounts are based on the contract price, n’est pas? But since that includes the cost of the buydown, the true value of the home as a now “existing” home is less. So if changed economic circumstances force the new owners to sell any time soon, they’ll be unable to sell it as an existing home in competition with the builder they just bought form unless they, too, spiff the buyer with a buydown. There goes a substantial piece of their equity, perhaps all of it if they used some incentive program to get in with a small down payment.

Prop taxes are also based on the pre-incentive selling price.

Yes, you are ABSOLUTELY correct in everything you said!

It’s good that new homes are coming on-line in competition with a stubbornly high-priced alternative. Already lived-in homes remain at near record highs and they seem to think they live in their own pricing universe. It is the new home that is the way to go. The only problem is that many new homes come with miniature-sized backyards, if you have kids and want them to play around.

New houses are so sad.

Get used to it, they are not going away.

With inflation rising and the wealth gap increasing in this country, people need a place to live and raise their families. Not everyone wants a huge, expensive, inefficient house with a 1/2 acre backyard.

We (family of four at the time) had a big house on three acres when we lived in Connecticut. That was too much to take care of as I was working long hours and going to school at night to get my advanced degree.

Depending on where you are in your life cycle, there are plenty of housing choices and not one size fits all.

I regretted that as soon as I posted it. A happy home is a happy home. Certain new communities make me sad, and those are the ones I always picture in my head.

Kids shouldn’t be outside they should be inside learning how to use AI

🤣❤️

To our horror, our university system is promoting AI, and has bought Pilot and made it available to all professors and students, thus rendering it futile to grade any papers submitted that were typed rather than hand-written in class.

Green – …what’s your take on the big Morlock U./Eloi State game this year?

may we all find a better day.

I live in a old house and would happily trade for new ones.

Old homes with backyard looks good on paper for sure.

These new sub divisions have got pretty good well maintained parks.

Kids no longer go outside. They play video games inside and meet their friends over discord.

The housing market is an example of the paradox of the Capitalist epistemology.

What happens when selling and buying are at an impasse.

The greedy rich trap the proletariat on the renting treadmill.

I think that Capitalism’s flaw is that through its use of blind competition as the driver for everything, it ends up valuing everything only in the negative sense (“what did it cost to make this?”) as opposed to the positive sense (“what benefit does this have to society?”).

In my opinion, the source of that negative value isn’t labor time like Marx said. It’s one layer of abstraction below that: the power to demand something in return. That can come from any finite resource, including labor time and effort, where value is added to something and which also incidentally tends to benefit society. But that power can also come from scarcity, where there is a stock of finite natural resources, or in this case finite land to build on, and that gives you the same power without the same societal benefit. That’s what gives people the ability to be greedy, but greed is only the proximate cause of the increasing prices. Those prices represent a tremendous amount of “wealth” that’s been created – wealth of a highly peculiar variety when viewed from the perspective of anyone who doesn’t have a stake in it.

Of course that’s not the whole story; that are also speculative feedback effects adding to the problem, as well as a lot of moral hazard coming from the government once the prices become so high that the market is “too big to fail”, and so on.

Slightly off topic but I saw an interview with David Marsh (former FED governor? hope I got his name right) on CNBC – it was quite interesting. Wondering what the braintrust here thinks of him as the CNBC hosts were mentioning him as a distant future FED chair candidate.

With housing being one of the main asset classes that has benefited from 25 years of favorable FED policy via ZIRP, MBS, QE etc this guest did not sound as if he thought any of it was a good idea. He even sounded as though he thought the FED had become political during that time frame and was risking its credibility with all of the errors and inflation.

OK you have my attention with your claim that a potential governor of the Fed, repudiated the Fed policy going back to the beginning of the monetarist experiment, QE.

Well, like the country club Supreme Court, you say whatever it takes.

However, contrary, to what one actually believes.

Kevin Warsh stated the Fed’s theory of inflation has not been clear. I did not hear him say they had become political. However, an unanchored Fed is a risk in a few ways is what he implied …to paraphrase. The serious nature of the problem with the Fed’s actions, messaging ,pivoting is the general theme of his interview. ,

He didn’t say FED is political but he hinted something like this.

His take was: FED always say they are data dependent. Now with stock market all time high, home prices ATH, ultra loose financial condition, low un employment rate. then what was the data FED rely on to cut rates by 50bps instead of 25 bps.

Housing prices and stock market prices play absolutely zero role in FED rate setting decisions. No should they.

The election will change the nature of the stimulus. Markets will move, reflecting the current bookie’s line.

IMO, the most important segment of society is the 90 pct of citizens that are not being well represented.

It’s not just housing. Buyers are becoming more attractive, enticed by the sellers ante.

Bubbles are in the eye of the beholder until they burst.

I travel a lot and notice that neighborhoods with older homes seem to have more old cars, appliances, and trash that accumulates over time out front. Less so with new construction.

Yeah, consumer trash in the yard, especially the front reduces the curb appeal. On the other hand, it really presents an opportunity for young people to buy with sweat equity as part of the deal.

Or, maybe old people living in old houses will tug at the heart strings of the young lambs who overpay because their not tough enough. My favorite people.

Did you ever notice that people are hoarders? Even seen the insides of a garage that has the cars parked outside of it? I have, and it’s because the garage becomes and “junk storage” room.

This is pretty typical everywhere.

Throwing, and then leaving all the trash, appliances, dead vehicles, etc., etc., in the front yard is how some folx keep their taxes down for decades…

Works pretty well almost everywhere from what I have heard… LOL

One of these junkyard dog Realtors sent a flyer in the mail advertising one of these newly completed monster homes to out of state buyers from California. The house was built with the minimum 7 feet between the neighboring monster home. The flyer was photo shopped using AI Next-gen Adobe Photoshop software, showing dense forest on both sides of the house. When the buyers got here, they were shocked to find the houses were right on top of each other, not in the woods like the flyer showed. These Realtors will do anything to make a buck and mislead out of state buyers, who buy properties unseen. I don;t know how they can sleep at night.

I really like the waterfront properties that have the water photoshopped blue, when in reality it’s brown.

Anybody who would buy a house ‘sight-unseen’ is out of their phucking minds!

No sympathy here!

When you are interested in a house, the first thing to do is type the address into Google Earth. There you can see the surroundings, how close houses are packed, if it is near a garbage dump or train tracks or an airport. I have eliminated many houses by doing this.

Simply check out the property using Google maps.

Google Earth has more features that I like to use than Google Maps. You can actually go back in time and see how the area has changed. See if the newly built house is sitting on what once was a gas station, or a dump, or who knows what.

Reminds me of a house I onced looked at that was photographed with a ultra-wide angle lens. It made the interior look much bigger than it actually was.

I love the house my parents bought when they retired and moved to Country Manor in Delray Beach Florida. The house was advertised in flyers with a canal in the back of the property where you could dock a boat. What they got instead of a canal was a DITCH full of weeds. Other owners got scammed as well. One of them called the marketers of the development and the realtors that sold them the property “cocksuckers” . A few years later they widened Military road right into peoples backyards. The whole place went to shit. My old man held it for 20 years and sold it for a loss when he moved.

“Can’t you understand what’s happening here? Don’t you see what’s happening? Potter isn’t selling. Potter’s buying! And why? Because we’re panicky and he’s not. That’s why. He’s pickin’ up some bargain. Now, we can get through this thing all right. We’ve, we’ve got to stick together, though. We’ve got to have faith in each other”.

The home buyers in this post-pandemic housing war, are a herd of people flowing away from the stark reality of stupid-high home valuations.

Conversely, the sellers are a proud tribe, locked into the belief that there’s a pent-up tsunami of buyers bidding up prices. Whatever the price is now, it’ll be higher next week…

That game of chicken and the collision play into the hands of home builders that can take advantage of this slow-witted battle. Even though home builders are seeing margins drop, this existing home transaction strike, buys more time for home builders to exploit this anomaly.

Eventually, this anomaly probably causes a downdraft for everyone involved in the pandemic bubble — which is why the reluctant buyers, who remain patient — will be the winners in this war.

It’s likely these slow witted buyers are patiently watching their cash grow in safe places like money market funds:

From the NYT about a week ago:

“It’s not until rates fall below 3 percent that people start to pull money out of money market funds,” Peter G. Crane, a founder of Crane Data, said in an interview. “I don’t see that happening soon. And I don’t see any big movement from money market funds into the stock market.”

The Federal Reserve tracks money fund flows from institutions — corporations that use the funds for paying short-term expenses or as a holding facility in between stock and bond market trades. Using these records, Mr. Crane found that since 1990, whenever the Fed has lowered interest rates, cash has rapidly flowed into money funds — far more rapidly than when the Fed has either raised rates or left them unchanged. That may be because banks tend to lower their already paltry savings rates more rapidly than money market funds do — making the funds more attractive on a relative basis.

The key take away there is, banks are already lowering rates, because they’re a lot like the home builders, who can’t afford to play this waiting game— the margins and profits declining will eventually show up in earnings declining. The banks are obviously a barometer for liquidity, and it’s obvious they want to lower yields back to zero — this is very definitely a time to remain patient and watch all these greedy players flounder.

I wonder if the NEW vs Existing home “price crossover” is a sort of “death cross”?

As you mentioned the home builder will capitalize whatever it takes. Does this begin to create gravity for the rest of the housing purchase market?

If so, what does it take to create a “race to the bottom?” Some form of liquidity call, possibly from increasing costs elsewhere?

I’m thinking about taxes, insurance, medical costs (with the assumption that the “existing” homes that are vacant are owned by an older demographic on average?).

Only if existing home owners need to seller. If they can pull the house off the market and wait there’s not a big immediate effect

A vacant home is a money suck, just the carrying costs. And when prices go down, it’s a painful money suck. Only really wealthy people don’t care about that. Most people get tired of it after a while and want to stop the bleeding.

We were lucky enough to sell our single family existing home back in August 2023.

Then, again, we didn’t think it was “worth” some huge astronomical amount so we didn’t hold out for a higher offer.

In Canada new homes are about 50 percent higher in price than existing homes. Some of that is because of the harmonized sales tax.

I like how the housing prices basically track the money supply expansion perfectly. Of course I still have to listen to this idiot Powell get on TV and say things like “it’s because people moving to the suburbs” and “um actually technically the fed doesn’t target home prices”. What a joke.

Going into the Fed cut election week will be entertaining for mortgage rate confusion, and a universal, global period of exasperation in wondering what makes sense and how to prepare for uncertainty — perhaps shocks and new risk.

I suspect the buyer strike for existing Hines is spilling into new home sales as everyone and their grandmother examine the roulette wheel, unsure how the odds change, as the wheel spins dramatically faster.

It’s almost laughable that the Fed can’t win with a soft landing narrative at the next meeting — the day after election, when any move either way will be misinterpreted — and the more likely move to do nothing, also makes them look like pikers — selling the neutral rate and R* is a perfect way to acknowledge they have no clue as to what’s going on — let alone how the post inauguration timeline plays out.

Their tea leaves are as good as those of home builders or buyers out in strike. The odds look great that mortgage rates will stay higher for longer. As for the global bet on nividia surging higher and higher as everything else goes lower — good luck on that outcome!

Tea leaf reading guru speaks:

“ Swaps traders are pricing 20 basis points of easing for the Fed’s meeting in November, below a full quarter-point. Traders now price 39 basis points for this year’s final two Fed meetings, raising the prospect of the central bank skipping one meeting, a view that has gained ground in the wake of a strong employment report for September”

Demand low, supply high, prices still high, because of rich idiots bidding against each other. I hope this will end at some point the way it should, but it takes too long..

Currently, the sellers have mind set that come what may home prices won’t go down and Govt would do whatever do prop up the home prices.

So far, real estate holders have been right for last few decades if you look at long term price.

This is the reason many sellers holding out for prices they aspire.

On top of this, economy is on fire fat least for upper middle class and above. They have homes, locked in mortgage rates, stocks, 401k etc etc.

I have many friends on the lower income strata which has none of the above other than paltry increase in wages but other things have increased so much their increase in wages have not kept up. A point in case, in last 4.5 years, home prices have almost double in my region. All other costs have increased a lot.

If your story is true, your low income friends are an outlier. For the past couple of years wages have greatly outpaced inflation. It hasn’t been close. Furthermore these wage increases have been among the lower levels of the economy. Tech workers are doing worse than McDonald’s workers in terms of wage increases.

Mick is agonizing over the ever-increasing prices. So, he revised the lyrics.

“You can’t always get what you want, but if you try sometimes, you get what you can AFFORD!

He also mentioned that this big govt deficit spending is because of FED. If FED has not made money so cheap for the last decade or more even though economy was good, then politicians would not have encouraged to borrow and spend this much adding trillions to US Govt deficit.

In essence, he hinted that FED works for the politician.

Hi Wolf:

The tract home builders are marketing quality—which is total fake value BS. They, like realtors, sell the sizzle and not the steak. Yes, these new homes provide shelter and maybe are next to great schools. I do not, however, expect these types of homes to build equity if developers build 1,000 new ones behind them in the next few years.

Living in single-family homes in central city neighborhoods has become an unattainable privilege for young and old alike.

Most people are likely to use 20 percent of their living space 80 percent of the time. The solution? More density, less square footage, and better-built homes. The location (e.g., the convenience factor) and better construction ultimately drive real value.

Cheers!

“Most people are likely to use 20 percent of their living space 80 percent of the time. The solution? More density, less square footage, and better-built homes.”

Multifamily. Condos and apartments, plus work from home, both earners, and commute to the office once a week by walking 15 minutes, then you’ve got good use of the home.

You don’t get it. People are not all stupid and you do not understand their motivation. If you understand retail, you have to understand the customer aka the buyer and what they are looking for. If used home sellers understood their partners across the aisle, then perhaps, they could sell their homes. But instead, companies like Lennar are eating their lunch, asking for seconds, and getting pie for dessert.

Here is a little example in my tech area. If you drive out about 30 mins out from my area, you can a buy a brand new house with new streets, little parks, walking paths, etc and get TWICE the house for the same price in my area. In other words, $1.3MM new house will get you 2400 sqft, but in my area 1200 sqft pos built in the 60’s will cost you $1.3MM.

A 2400 sqft house will cost at least $2.4MM in my area, slightly updated.

Yes, smaller yard and closer together, but brand new.

Of course, my house is better location, but not everyone can afford $2.4MM+ for a updated house in my area. So like intelligent adults, they compromise to make it work for them. I talked to the sales person at this development and they are targeting tech workers. The whole neighborhood is almost all tech workers with their Telsa or two. This what they can afford and still be near work etc.

Big yard? Quality build? Seriously, understand the customer. They want 10 years of basically maintenance free house. The decision marker is usually the wife and she wants brand new house that nobody lived in. No stinky dogs, no crayon marks, etc. This subdivision is 85% sold out and they are fire selling the rest to close up shop and move on. This is how you make money in retail.

These poor used home owners with delusions of high value are just sad. In the same area as the new subdivision, they are trying to comp it as the new homes. Yeah, I really want a 2400 sqft built in the 80’s with crappy updates versus a brand new home. 89 days later and time to renew the listing or pull it off the market and raise the price for the spring?

Density? Jesus. Do you understand what that means? Here is a real life example. A 5000 sqft SFR is allowed to have 4 units to built on it.

With FAR, coverage, setbacks, you can build two duplex on the lot, front and back units. Each unit is 1500 sqft, three stories, maybe four if garage is allowed. Maybe $1.1 MM per unit. Depending on the lot, zoning, overlays, maybe 1 parking per unit or 2 units have 1 parking. Off-street parking.

Yes, in the city and maybe better transit and “location”, but stairs and hearing the next door neighbors fucking. Great. Better construction? Yeah right. So, brand new, no parking, no yard, great location, and tight quarters. Seriously, talk to some real estate folks. Good luck.

Points taken. However, in 10 years, those production homes will not deliver significant value via increased equity. Don’t expect an investment windfall when it sells. To your point, Lennar knows it will compete with the 1000 homes it built 10 years earlier. It’s almost akin to planned obsolescence.

If central city neighborhood real estate prices are stagnant, then for damn sure, the outskirts communities aren’t increasing in value either.

MW: 10-year US Treasury yield ends with biggest six-week climb in a year as consumer sentiment rises

My back goes out far too often and I’m laying around spending too much time scanning financial stuff.

Nonetheless, one of my favorite chart gurus says the 10YUST yield has recently broken out of a downward trend line that goes back to the 80s and this is happening as the term premium is expanding, apparently that’s based on old voodoo from The Adrian, Crump, and Moench (ACM) model, found at NY Fed,

What I find interesting, related to the FGDA, is how rising home inventory for new and used homes will fit with higher mortgage rates and weaker demand — especially going into winter.

An old friend of mine, said the best time to make an offer on a house or land, is after the first snow storm.

In regard to Perfect Storms, the epic election amplifies the concept of crazy — crazy overbought mkts, with yields unexpectedly rising fast — VIX at 20 today, probably headed towards 30.

I think 2025 is the year everyone has egg on their faces — everyone that doesn’t believe in inflation.

Hmmm, time for ice.

You should be looking at MOVE not VIX.

I’ve been playing with stock charts and their $move only goes back a few years — but, the index is at 128 which isn’t screaming too loud and Vix anemic around 20. I don’t think either index will be predictive here.

My main curiosity is relationships to gold and Spx — most assets absolutely hate when the 10yr heads towards 5% — and that’s looking like it’ll be part of the election trade.

Even though everybody dismisses treasuries as pointless, they pack a knockout punch near 5%.

The 10yr fast acceleration after the Fed cut is actually epic, and if that trend maintains pace, we’ll be looking at Shiva the great destroyer by mid November— especially with another rate cut (or in December).

Interestingly, bitcoin hasn’t been tested by a 10y at 5%, but it seemed somewhat immune around October 2022. Bitcoin thrived in the zirp era, and the dollar was weaker then too, so I don’t think bitcoin had been through much realistic stress yet. Right now the election trade is pushing everything higher on overbought exuberance — but the main feature of a 5+ 10y is its ability to bring valuation into focus. It’s very binary and clear — and exposes stupid risk.

“their $move only goes back a few years”

The Move Index data/charts that I can see go back to 2003. And it’s historically fairly high right now.

“gross margin was squeezed by 2 percentage points compared to a year ago, to 22.5% in Q3 2024, from 24.4% in Q3 2023.” Oh…. I feel so sorry for them, Wolf. NOT! They cut every corner they can and provide near useless warranties to get these profit margins.

What is happening with condominiums? Wolf reports on Canadian real estate and I see on the internet that there have been some spectacular bankruptcies in Toronto of megaunit developments. I live in a mature Detroit suburb where development space similar to adjoining cities is limited to repurposed sites such as no longer needed schools, churches or even gas stations. There has been a spate of small-time would-be condominium developers, who are owners of unrelated businesses, trying their hands as developers of small single sites with projects shoehorned into single family neighborhoods. The units are touted as luxury with tiny pools and gyms with insufficient parking. There are the inevitable zoning fights with tax hungry city governments siding with inexperienced developers against their citizens. City governments love the beautiful computer-generated images and refuse to evaluate the experience and financial strength of the developer. Some approved projects never get started and some projects once started, stall leaving piles of fenced off dirt. It seems unlikely that small time developers will be able to cut prices or offer mortgage buy downs. The concern of nearby residents is that conversion to low-income housing will be a remedy for unsellable developments. We celebrate entrepreneurial risk taking, but failure of city governments to do financial due diligence of would-be developers puts communities at risk.

Footnote tidbits: can these housing monsters keep earnings higher for longer, while cutting prices?

Lennar’s earnings are expected to grow from $14.18 per share to $16.04 per share in the next year, which is a 13.12% increase.

S&P 500:

“What’s different about this quarter is how high valuations are. At a forward price-to-earnings ratio (P/E) of 22, currently, stock valuations are near 25-year highs. So, $275 is the number to watch. That’s the consensus estimate for S&P 500 EPS in 2025. We would consider a 2% cut in estimates to around $270 to be the base case — remember, estimates almost always come down as companies report results“

“A large chunk of S&P 500 EPS growth in the third quarter, although growth rates are slowing. Based on current consensus estimates, 3.3 points of S&P 500 EPS growth contribution — essentially all of it — is coming from the Mag 7.”

“Of the S&P 500’s anticipated EPS of $60.26 in the third quarter, more than half is seen coming from the info tech sector”

Earnings Revisions: On September 30, the estimated (year-over-year) earnings growth rate for the S&P 500 for

Q3 2024 was 4.3%. Five sectors are reporting lower earnings today (compared to September 30) due to downward

revisions to EPS estimates and negative EPS surprises.

If home prices were 48k sales might pick up. That might take federal and or State legislation though.