Foreign investors had a big appetite all year for Treasury securities. But China lost interest, Japan struggled with the yen.

By Wolf Richter for WOLF STREET:

The question on our worry-list is how long foreign investors will continue to support the recklessly ballooning US Treasury debt, that has soared to $35.8 trillion, from $35.0 trillion on July 27. If demand slacks off, yields will have to rise to create more demand, and that could get expensive.

Foreign investors play a big part in this demand, but proportionately not as big as years ago. The importance of China and Japan has dwindled, while the Euro Area, big financial centers, and other countries, including Canada, Taiwan, and India, have piled up Treasury securities and have become large holders.

So far, knock on wood, there has been solid demand from foreigners: They piled up Treasury securities at an accelerated pace since late 2022 as the Fed’s rate hikes and higher long-term yields made US Treasury debt more attractive than a lot of sovereign debt that yields less than US debt.

For example, Italy’s 10-year yield is at 3.36% currently, versus 4.08% for the US 10-year yield, which has risen since the rate cuts. France’s 10-year yield is at 2.90%, Germany’s is at 2.19%, Japan’s is at 0.97%, which is far below Japan’s inflation rate (core CPI increased by 2.4%). And they all have their ballooning-debt problems, none more than Japan.

So for investors, these foreign yields are crummy deals compared to the US 10-year yield of 4.08%, and so there is demand. Cleanest dirty shirt.

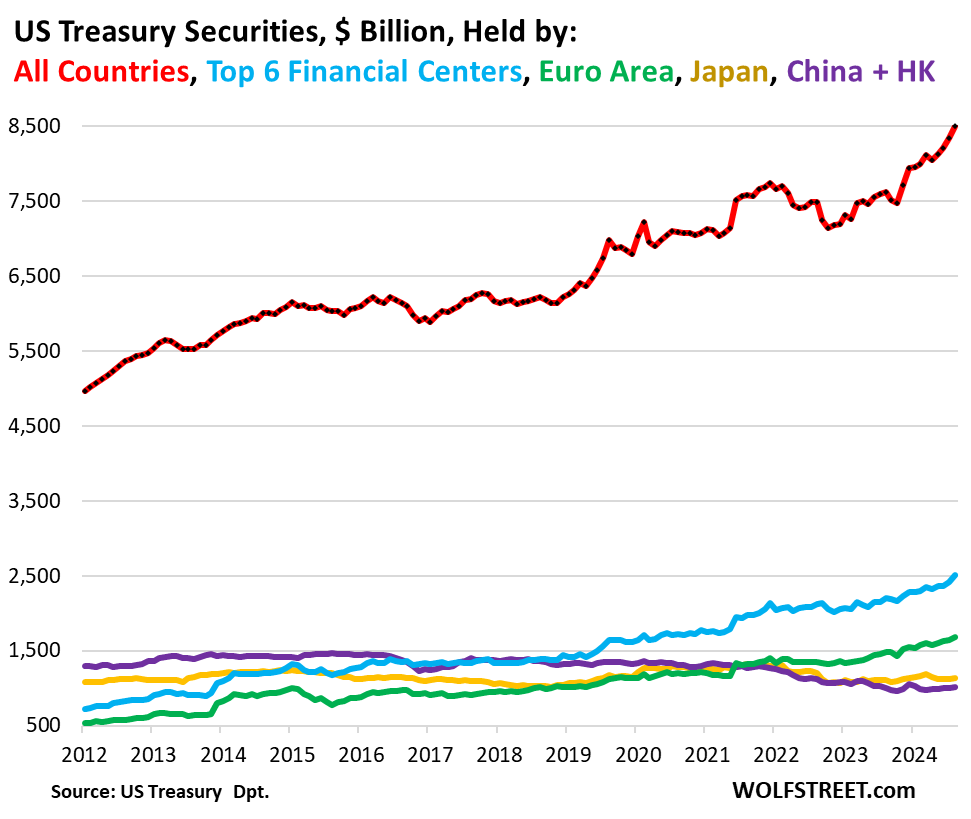

Treasury debt held by all foreign entities jumped by 2.0% in August from July, and by 11.5% year-over-year (+$880 billion), to an all-time high of $8.50 trillion, according to Treasury Department data Thursday afternoon (red line in the chart below).

In summary, the biggest holders:

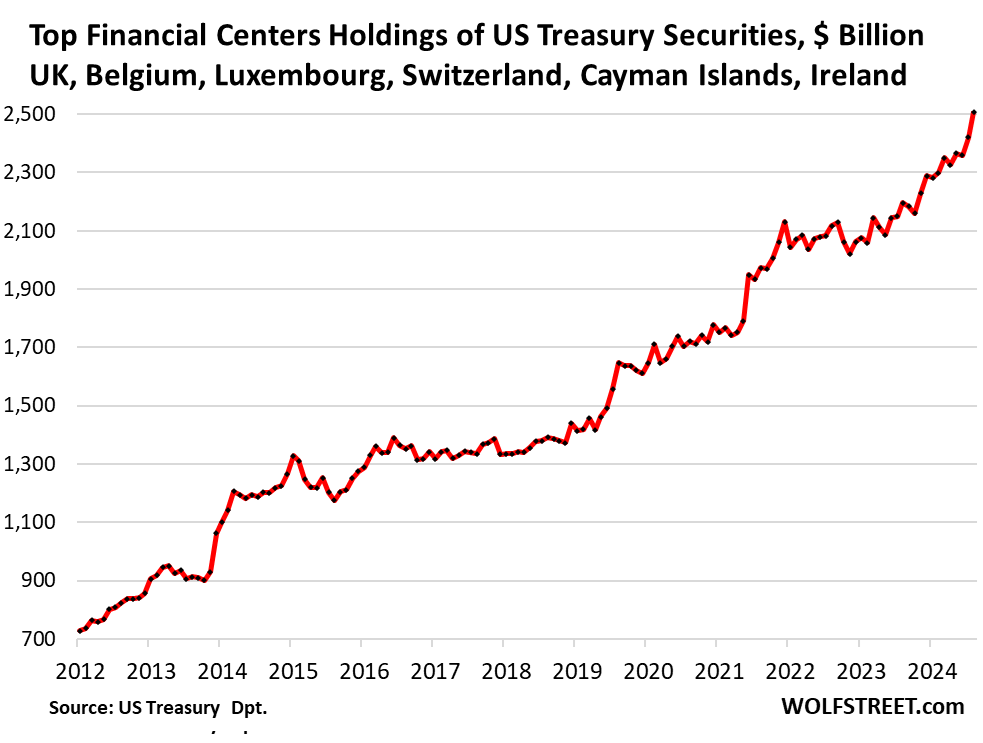

- Top six financial centers: $2.51 trillion, +3.6% month-over-month, +14.2% YoY (blue). They are: London, Belgium, Luxembourg, Switzerland, Cayman Islands, and Ireland.

- Euro Area: $1.69 trillion, +2.3% MoM, +13.5% YoY (green). This includes three of the financial centers above (Belgium, Luxembourg, and Ireland).

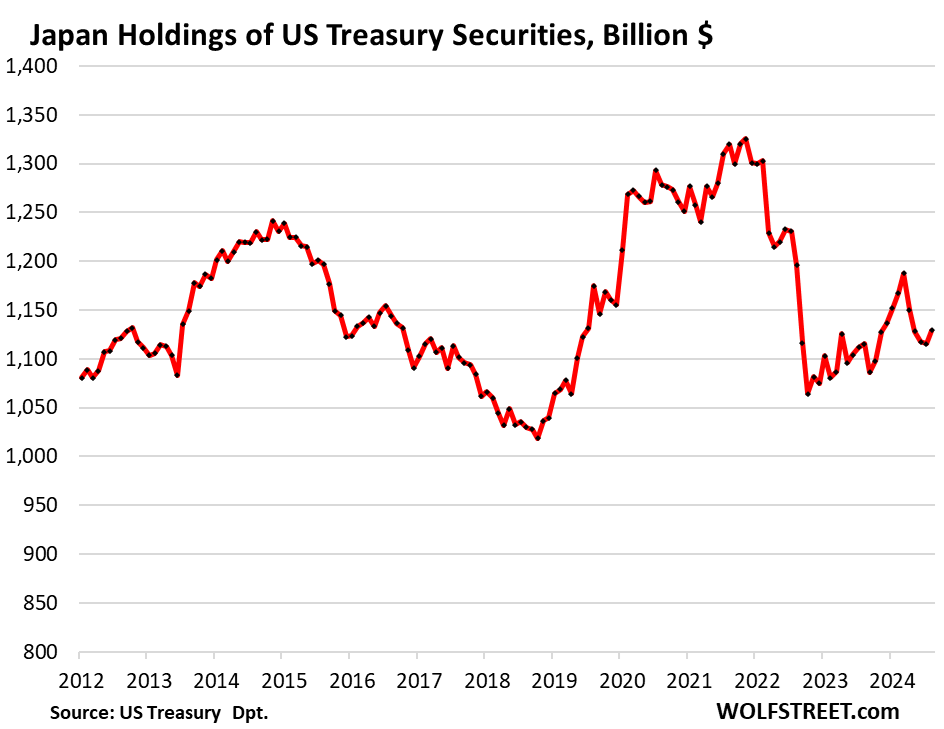

- Japan: $1.13 trillion, +1.2% MoM, +1.2% YoY (gold).

- China and Hong Kong combined: $1.01 trillion, +0.3% MoM, +0.2% YoY (purple).

The chart also shows how the importance of Japan and China has dwindled over the past 12 years, from being by far the top two foreign creditors in 2012, to being far below the financial centers and the Euro Area in 2024

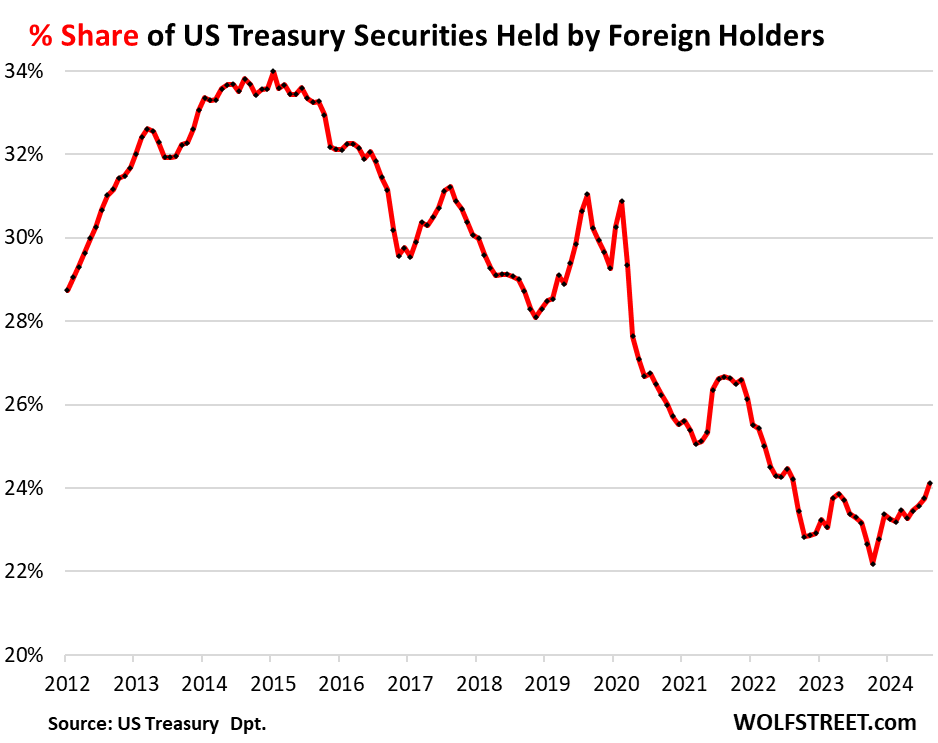

The share of foreign holdings had dropped from the peak of 34% in 2015 to a low of 22.2% by October 2023, as the US debt ballooned faster proportionately than foreigners increased their pile of it – they increased their pile but more slowly than the debt grew.

But since October 2023, foreigners increased their holdings at a faster pace than the debt ballooned, and the share of the debt that foreign investors are holding has risen, and in August reached 24.1%, the highest in two years.

The six largest financial centers: +3.6% MoM, +14.2% YoY, to a record $2.51 trillion. Their holdings more than tripled since 2012!

These countries specialize in handling the financial holdings of global companies, individuals, and governments. Ireland is a favorite for US mega-corporations to store their profits. So some of the holdings at these financial centers are actually held for US entities, and not foreign investors.

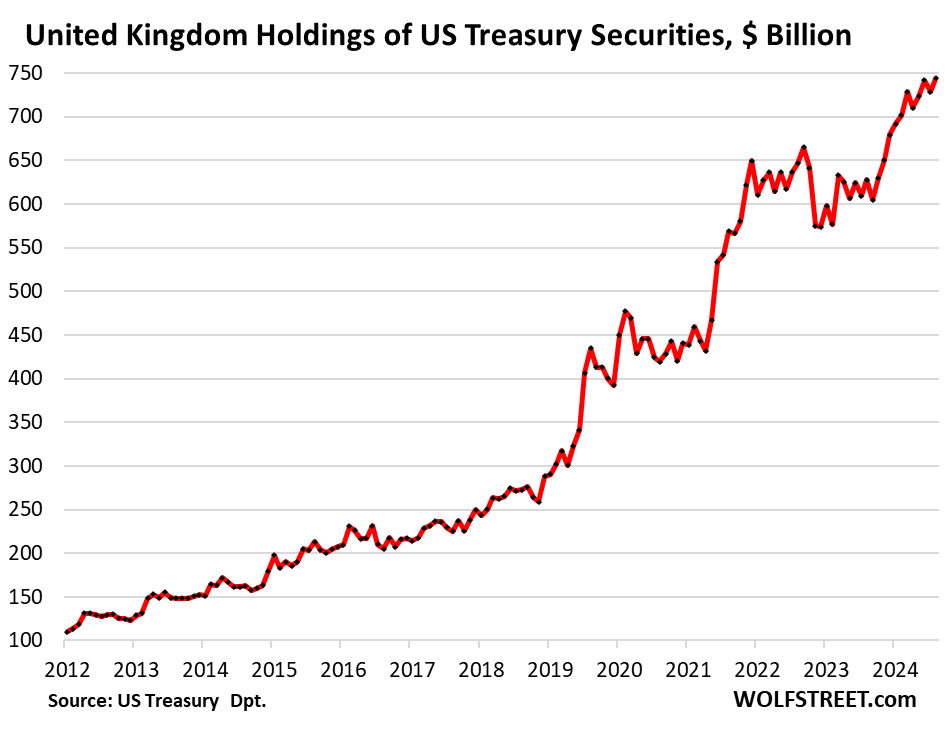

- UK (“City of London” financial center): +2.1% MoM, +18.5% YoY, to $744 billion

- Luxembourg: +0.5% MoM, + 9.9% YoY, to $402 billion

- Cayman Islands: +11.0% MoM, +35.5% YoY to $420 billion

- Ireland: +2.9% MoM, +9.5% YoY, to $322 billion

- Belgium (home of Euroclear): +2.9% MoM, +2.6% YoY, to $325 billion

- Switzerland: +3.8% MoM, +4.5% YoY to $296 billion.

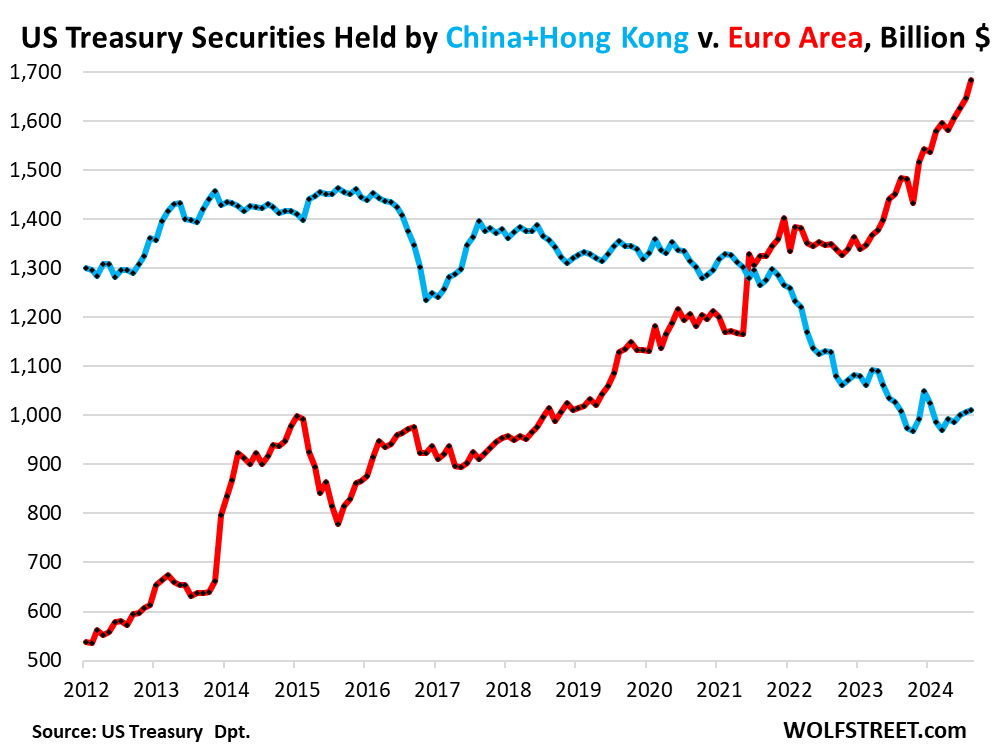

Euro Area v. China + Hong Kong. China and Hong Kong combined have reduced their holdings from $1.45 trillion in 2015 to $1.01 trillion in August (blue). Over the past five months, their holdings have inched up. Year-over-year, their holdings were essentially unchanged.

The countries of the Euro Area have more than tripled their holdings in 12 years, from $534 billion in 2012 to a record $1.69 trillion August (red).

The Euro Area’s holdings surged by 2.3% MoM and by 13.5% YoY (or by $200 billion YoY)!

There have been reports that China has shifted some of its USD holdings from Treasury securities to US Agency securities due to their slightly higher yields. US Agency debt is not included here.

Japan’s holdings: +1.2% MoM, +1.2% YoY, to $1.13 trillion.

Authorities have been struggling to contain the plunge of the yen. It currently trades at around 150 yen to the USD. Since early 2022, the yen has lost roughly 30% of its value against the USD because the Bank of Japan has decided that it would do the absolute minimum as late as possible to tighten monetary policy.

The BoJ has hiked policy rates twice, two tiny baby steps, from -0.1% to 0.25% currently. And over the past few months, it started slow-motion QT. To prevent the yen from collapsing further, the Ministry of Finance intervened in the foreign exchange markets multiple times, selling large amounts of USD holdings to buy yen with it.

Despite big gyrations in its Treasury holdings, in August, they were where they’d been in mid-2013.

United Kingdom: +2.1% MoM, +18.5% YoY, to $744 billion. The City of London is one of the top financial centers in the world, and so a portion of those securities could be held for US clients. The UK is also included in the Top Six Financial Centers above.

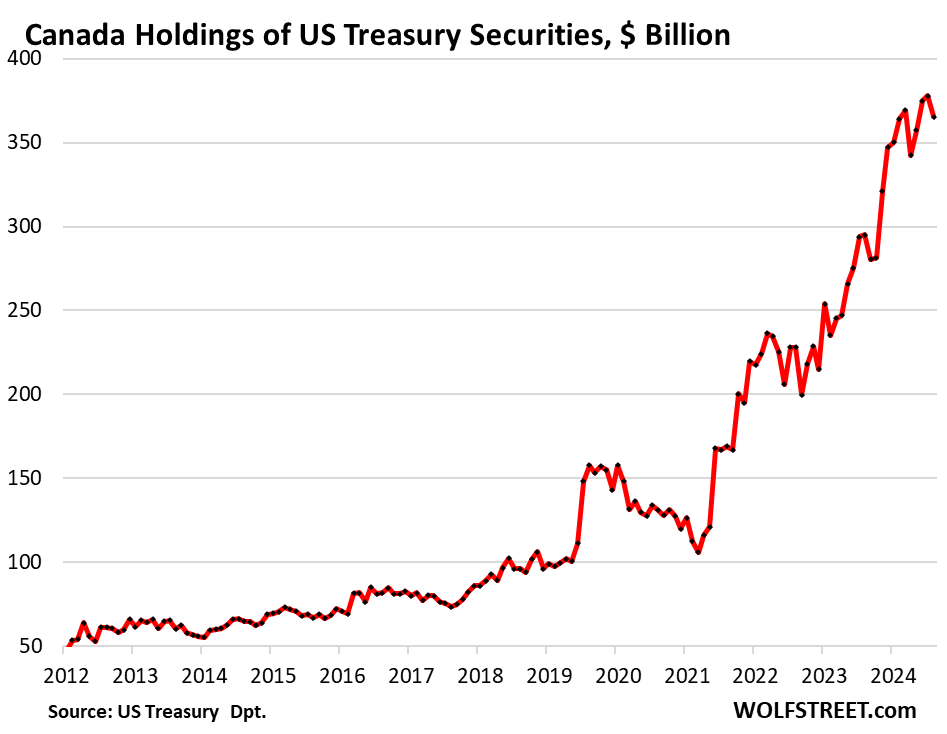

Canada: -3.3% MoM, +23.8% YoY to $365 billion. Since March 2021, holdings have more than tripled. Over the past 12 years, holdings have multiplied by a factor of 7!

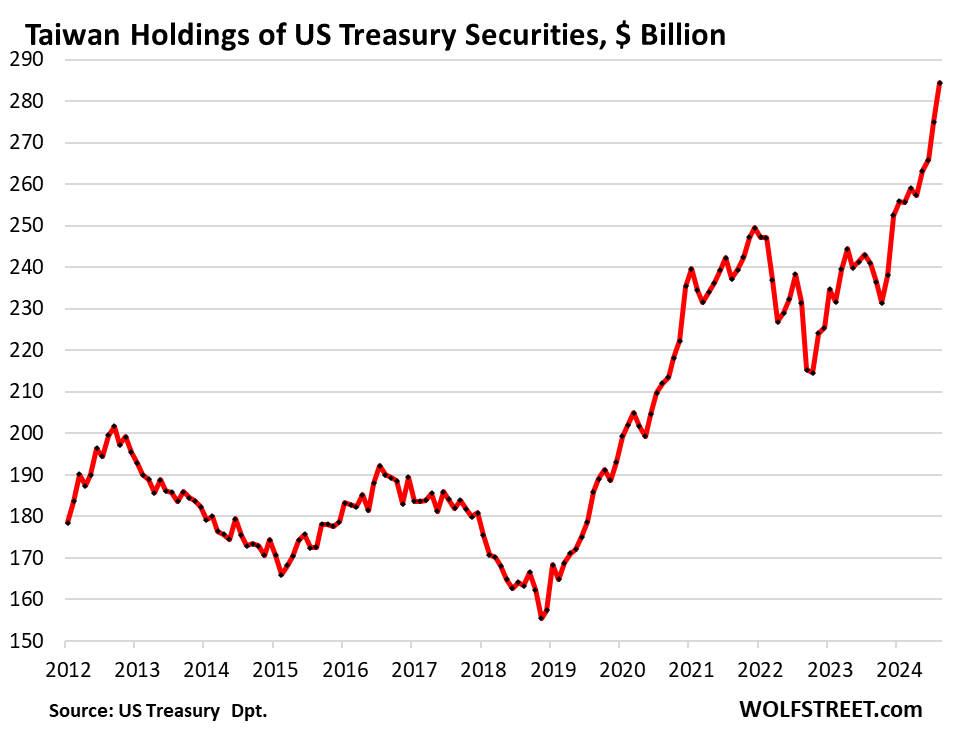

Taiwan: +3.4% MoM, +18.0% YoY, to $284 billion:

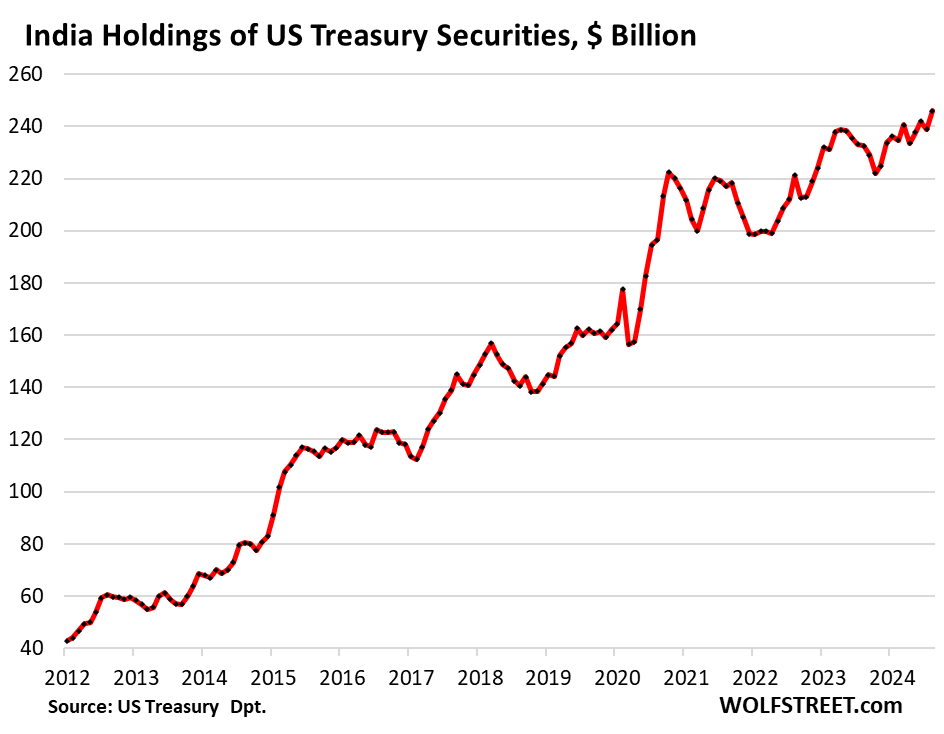

India: +3.0% MoM, +5.8% YoY, to $246 billion. Its holdings have multiplied by a factor of 6 since 2012:

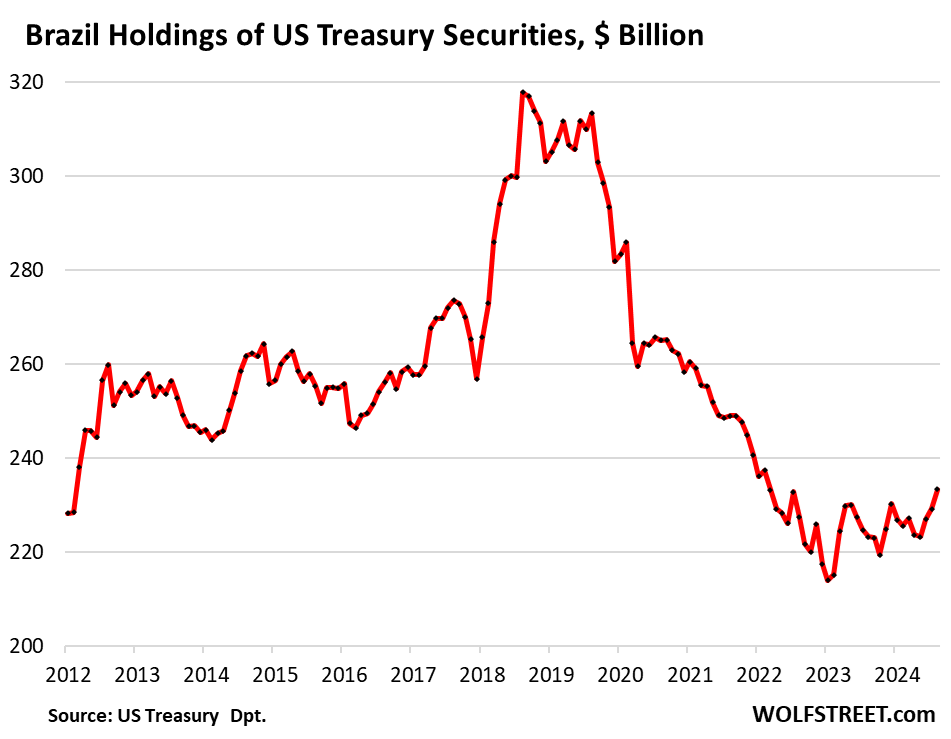

Brazil: +1.8% MoM, +4.5% YoY, to $233 billion. Between 2018 and 2021, Brazil cut its holdings by about one-third, undoing the entire spike of its holdings in 2018. Since January 2023, its holdings have zigzagged higher.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

A few questions Wolf:

1. Is the buying you portray all done by central banks, or is it more individual entity oriented.

2. How does duration purchased vary from country (zone) to country?

3. Is it safe to assume nearly all purchases are held to maturity? (Or is there shorter term trading of US Treasury securities within some countries?)

4. Can you generalize about who picked up the slack as % share of US Treasuries held by foreigners declined from over 28% to about 24% over the last dozen years?

Clearly, and contrary to surmise to the contrary, the US dollar is “not dead yet” (apologies to Monty Python).

Thanks.

1. No. Look where the buying now takes place: financial centers, Eurozone, Canada, etc. These central banks are not buying ANY Treasury securities.

2. You can look that up yourself. There are only about 150 countries that buy Treasuries. You can look up holdings of T-bills and holdings of notes and bonds, by country.

3. No, risky to assume. If you assume that, you may vanish in a pitfall.

4. US investors, obviously. You will see, if your read this, data through Q2:

https://wolfstreet.com/2024/09/24/who-holds-all-these-us-treasury-securities-update-on-the-investors-in-the-recklessly-ballooning-us-national-debt-in-q2/

This excellent article touches upon what is arguably the most important financial issue of our generation. How is this madness of nonstop fiscal deficits, artificial suppression of interest rates, huge asset bubbles, continuing flood of Treasury issuances,

and massive QE interventions going to end? Don’t be lulled by recent QT. We may find out sooner than we think. And I fear the answer may be very ugly: “Emergency” pivot to QE, resurgent inflation, reduced demand for Treasury debt, capital controls, and outlawing of private ownership of gold and bitcoin. I fear for my children and grandchildren.

I agree it is a major issue which is not getting any serious attention from the main media….

How can this money printing just go on and on?

The printers will continue printing as long as GDP keeps roaring and buyers continue showing up for treasuries. We are in a growth phase, Harry, get with it! (sarcasm)

MrFooFoo,

“The printers will continue printing as long as…”

The US printers stopped printing in 2022 and started shredding. By now, they destroyed about $2 trillion of the stuff they’d printed.

https://wolfstreet.com/2024/10/03/fed-balance-sheet-qt-66-billion-in-sept-1-92-trillion-from-peak-to-7-05-trillion-back-to-may-2020-below-7-trillion-in-1-2-months/

TLV:

Everything you have articulated here has already happened*. some several times. Many of these events in just the last hundred years. you and your children and grandchildren will just have to navigate through it just as our parents and grandparents did. Be sure everyone is well educated which will be very helpful.

* bitcoin not yet but it surely will be unless it dies of its own accord.

QT the inverse of QE removes money from the financial system. Similarly, so do bankruptcies.

Does it? What is the over debt level then, must be lower huh?

Kinda interesting blurb at S&P a few months ago, which gives background as to what motivates foreign buyers to look at Uncle Sam’s dirty shirt:

“But a report in April (commissioned by the French Finance Minister Bruno Le Maire and overseen by Christian Noyer, the French economist who served as Governor of the Bank of France) suggested these savings are “poorly allocated” and that the continent exports its savings by buying foreign debt securities. Additionally, the report argued that lack of depth in European capital markets is becoming “increasingly untenable” and warned that the monetary union can “no longer defer [this] deepening … if it wants to close the widening economic gap” with the U.S.

The Noyer report estimates that 20% of European savings are invested in non-European debt–representing the doubling of such holdings since 2012.

. In fact, Europe has become the biggest foreign holder of U.S. Treasuries securities–having surpassed China and collectively holding roughly 19% of outstanding U.S. government debt securities. Admittedly, China using custodian services located in the euro area to recycle parts of its foreign-exchange reserves in U.S. assets somewhat blurs the line of real treasury holdings.“

From:

CreditWeek: What Does The U.S.-Eurozone Interest Rate Differential Mean For Currencies And Capital Flows?

It’s also interesting that a lot of foreigner buyer entities are also very engaged in FX trading, so maybe they need to have more chips for their casinos Luxembourg is a huge FX mkt for china….

US treasuries yield the most and GDP is killing it right now. Investors see little to no risk. This isnt rocket science. Until a better option comes along, US treasuries are the best dirtiest shirt.

i think you have cause and effect backwards. gdp is killing it precisely because the united states is borrowing and spending $2 trillion a year beyond what it raises in taxes.

without that war level deficit spending, gdp would not be where it is.

investors see little to no risk at the short run, but what happens if the u.s. has to drop short term rates, pushing investors to invest in longer term treasuries for yield instead. the 10 year at 4.1 might go to 6-7% and then the u.s. has a problem.

basically, the developed world has crap interest rates, as they want to be able to maintain unsustainable spending, so the u.s. is able to raise a ton of money by offering slightly less crappy interest rates.

i don’t think this whole game is sustainable.

Franz G,

I hate to disappoint you: Federal government “consumption and investment,” as it’s called for GDP calculations, was $1.49 trillion in Q2, or only 6.4% of total GDP of $23.22 trillion (all annual rates). It contributed only 27 basis points to 3.0% GDP growth. So if federal government consumption and investment had been flat, GDP growth would have been 2.73%, still far above the 10-year average of 2.0%

People constantly exaggerate the impact of federal government on GDP because it suits their political narrative. There is an impact, but it’s not that big.

Here is all the GDP data, including the government portions of it:

https://www.bea.gov/sites/default/files/2024-09/gdp2q24-3rd.pdf

wolf r, i wasn’t talking about the increase in the deficit, just deficit spending at all. one of the hallmarks of keynes theory is that government spending has a multiplier, so $1 trillion spent by the government leads to more than $1 trillion worth of output, although it’s not clear how much exactly.

also, unless i’m misreading that bureau of economic analysis sheet, the money you noted doesn’t include transfer payments to individuals that than get spent in the economy.

if federal spending were to drop to no deficit, that is, $2 trillion less, i’m quite confident gdp would drop more than $2 trillion.

1. There’s a lot of nonsense about transfer payments being spread around.

The biggest parts of transfer payments (Social Security, Medicare, unemployment benefits, etc.) are self-funded, meaning the government doesn’t borrow money to pay for them, but collects money from payrolls to pay out this money to beneficiaries or healthcare providers (like any pension fund or insurance), and the net effect on consumption over the long term is zero. In fact, Social Security has collected $2.7 trillion MORE than it has spent over the past 25 years, and that $2.7 trillion is now in the Trust Fund to be paid to beneficiaries to supplement the outgo when the current receipts are not enough to pay for the current outgo (which has been the case over the past few years).

2. Your conclusion is BS. When a company with $2 billion in revenues and $200 million in net income borrows $400 million by issuing bonds, thereby adding $400 million in new debt, it doesn’t suddenly have revenues of $1.6 billion ($2 billion minus $400 million of new debt) or a loss of $200 million ($200 million net income minus $400 million in new debt). That’s not how that works. Same with GDP. You can subtract anything from GDP, including the number of ants in your garden, but the outcome is going to be nonsense.

There are only two kinds of capital: equity capital and debt capital. Companies issue both; governments issues only debt capital. But it’s still CAPITAL (a stock of money), and it’s treated as capital, and you cannot subtract capital (a stock of money) from revenues (a flow of money) or spending (flow of money) or income (flow of money).

A lot of government expenditures do NOT count in GDP and don’t contribute to GDP neither directly nor indirectly, nor with a multiplied effect or whatever. For example, interest payments do not go into GDP and do not add to measures of economic growth. A lot of government spending doesn’t show up in GDP, so you cannot subtract it from GDP, which is why you cannot subtract government spending from GDP. If you do that, you get bullshit, which is of course what a lot of ignorant moron bloggers and youtubers out there pollute your brains with.

Very good article. Like all the “ratholed money” countries.

And no, I’m not worried at all……..about what?

Small time bean counter’s silly mental artifacts? Har-Har!

Just invest more and smarter, idiots!……get an extra trading screen and software….if you haven’t got at least 3 at your “trading” desk you’re obviously a loser!

India’s 10 year govt securities rate is 6.7% . They have not cut a single time in the last 18 months. Reason India is buying us$ treasury securities is India’s (140 billion breathing souls consuming ) Imports (crude oil +gold + advanced macheniries+ defence equipment)is always more than Exports (soft exports is the crowning glory. all other material exports are not so much) by a faxtor of 30-40 billion $ monthly defecit. RBI’s $ and other convertible currency stockpile is only 600 billion $ . If exports falter India has only less than a year’s worth of foreign exchange at any time. Rupee is weak at 84 to $. You can compare $:₹ from 2012-2024.

If you compare with china ,reminbi is stronger now than 1997 (Hongkong takeover). China ,Japan run monthly export trade surplus . Indian ₹ was 40 to $ in year 2000.Now 84. Japan due to zero interest rate policy got whacked from 105 to 150 by speculators. Reserve bank of india mentioned even yesterday we wont follow other central banks in reducing rates. Food inflation can topple elected Indian govts. India is not a ponzi economy like AU,NZ, Canada (housing bubble+ brown people import>education scam + dirt ) India is buying physical gold always but buying us$ securities is like hoarding IV fluids for emergency operation due to neccessity to feed the 1.4 billion souls and keep the economy running.Indian diaspora remitting $ to home is the 2nd largest $ earner next to software exports.

Well said!

… (140 billion breathing souls consuming ) …

I’m sure you meant 1.4 billion.

:-)

Spent a nice 2 years buying India 3 month CD’s at 5.25 % sheltered in a Roth. the 3 month return is down to 5% now.

Robert (QSLV)

IBEF :: In FY24, Indians residing abroad sent an unprecedented US$ 107 billion in remittances to their families in India, surpassing the US$ 100 billion threshold for the second consecutive year. This net remittance amount nearly doubles the combined total of US$ 54 billion from foreign direct investments (FDI) and portfolio investments during the same period. T

Indians are like Mexicans: loyal to their families, and prone to remember where they came from. Their remittances represent an act of love that has great economic effect on the homelands. This cannot be overestimated.

On some level I suppose I should be be concerned with US debt levels but I honestly feel so disconnected to it being relevant in that whatever it grows to is fine as long as I get better yields, and if I don’t, it is what It is. Obviously could be a lot of explanations to this but simply notice how little concern or reaction I have to any of it. I know as percent of revenue applied to interest payments on debt clear is a problem but at the same time feel so distant.

Debt to GDP from several countries I looked at:

Worst offenders: China and Japan +

Lowest: Luxembourg, Mexico, New Zealand, Australia, Germany, Ireland +

Middle (over 100%): U S, Canada, France, Italy, Greece +

What puzzles me is why the yields on 10-yr. U S treasuries (the whole T curve) are higher than many other EU yields.

Treasury interest rates have consistently been higher than that of other sovereign debt since the Fed stared hiking.

Bingo – you get it. This is the phenomenon at the core of division/confusion surrounding the state of the US economy. The word “Debt” to most brings with it a negative connotation and means ‘bad.’ But if taking on debt means increasing output, isnt that good? This is a classical econ debate and a fun/important discussion to have.

taking on some levels of debt for increasing productivity/output is good. but most of what the united states borrows for is not that.

Exhibit A: piles of more debt to pay interest on existing debt.

publius, exactly.

Interest payments do not go into GDP and do not add to measures of economic growth. A lot of government spending doesn’t show up in GDP. That’s why you cannot subtract government spending from GDP. If you do that, you get bullshit, which is of course what a lot of ignorant moron bloggers and youtubers out there pollute your brains with.

Come on Glen tune in.

I mean it must be high or low, but it’s alright, that is I think it’s not to bad – Ed S

Sullivan, “ladies and gentlemen..the Beatles”

I am in Canada, all our savings and investments are in USD denominated ETFs and USD money market account. I expect US Dollar to soar about 15 – 20% within the next 18 months time frame. Everybody is so negative about prospects for USD, it is still the cleanest dirty shirt. Moreover, the USD Index has a low open interest in the futures market – a perfect setup to go higher, nobody pays any attention to it. FLOT is yielding 5.94% – it is a low risk ETF. UUP yields 6.19% and has a potential for decent cap gains.

That will be interesting to watch. I would not feel overly confident arguing with you one way or another. If it turns out you are right, what does that say about the state of the global economy?

US fiscal deficits of 1.9 trillion per year with no sign anywhere that they will decline or can decline. At least measured by military capability, each new trillion buys less and less bang.

Beneath the covers it seems like GOLD is flowing east and US paper is flowing west. Who will turn out to be right. It’s not even an argument because the US absolutely, never, ever can acknowledge a role for gold as money. We are all in on the current path.

Is Europe even a viable economic zone cut off from the rest of Eurasia ? Is the rest of the G7 simply exporting prosperity to the US ? Who knows, all very interesting

The CAD is position to appreciate against the USD in the coming months.

The aggregate demand in US and major global economies is accelerating, and we are in the last quarter of the year which is characterized by increase spending due to the coming year end holidays. As result major commodities will appreciate, which will be a significant tailwind for the Canadian Trade Balance (Canada is a commodity based economy) and as consequence for the CAD, while due to increase spending the US Trade Balance will deepen further, which will further increase the devaluation pressure for the USD. I personally think that the Canadian Economy is positioned better that the US one, considering the above and the Canadian fiscal deficit which contrary to the US is fully under controll. One of the major weaknesses of the Canadian economy is the huge investment of the households in US assets, and the huge dependency of the Canadian economy on the US one. However, in the next coming months the CAD will appreciate.

Cayman Islands jumps out at me. +11.0% MoM, +35.5% YoY to $420 billion: big numbers, in the big leagues! What’s the story there? Offshore economy/finance?

1 Foreign investors prefer to have their investments beyond the reach of the US government, mainly IRS. Investing through Cayman entitles helps, although FATCA has made them more transparent.

2 US tax exempt investors (foundations, 401k, IRA, etc.) have certain types of investments taxed. These restrictions can be mitigated by investing through Cayman or other offshore corporations.

Thanks! I guess the US public benefits indirectly, if these folks are willing to hold US debt.

The real problem on the horizon, I think, is something like Tether, which trades “completely” offshore to the US-centric financial system.

I took a sizeable position in gold in 2005 and I did not sell much of it all the years. Sometimes it was hard to hold. Last week I started to sell some because I am planning to spend a lot the next 5 to 6 years and it’s up a lot this year.

I am also holding € and $, it’s just a need. I am living in Germany.

Longer term all currency holders will be punished, I think.

All this is way beyond my pay grade. But it’s starting to feel like the credit card is maxing out, and the minimum monthly payment is getting tough to make.

The problem is that the credit card doesn’t have a credit limit, and is therefor never maxed out, and that the government can make the payments that are due by charging those payments to the credit card, no problem, and lenders are fine with it.

Just kidding, sorta. Credit card mechanisms don’t apply to sovereign debt. And the interest rates, below 5%, are a lot lower than credit card interest rates too.

of course, but the fact that every nation in the world can’t borrow seemingly unlimited amounts of money in their own currency at reasonable rates shows that there is a limit to the game.

it’s just that the united states hasn’t found it yet.

Super easy answer here: the hegemony of the U.S. Dollar. We call the shots.

But growth I slower than 5%. Interest and debt are growing faster than GDP.

Historically, GB, Spain, Portugal, Netherlands, Argentina, etc., may disagree with the concept of no credit limit.

No, no, no. you cannot compare the growth of the debt “not adjusted to inflation” to GDP “adjusted for inflation.”

You MUST compare the debt (always in current-dollar) to current-dollar GDP. The debt might still grow faster than current-dollar GDP in some quarters, but they’re much closer.

In Q2, current-dollar GDP grew at an annual rate of 5.6%, faster than the debt. So with current-dollar GDP growing faster than the debt in Q2, the debt-to-GDP ratio dipped a bit to a still huge 121.7%.

Wolf, I just want to exclaim a sincere thanks on behalf of your readers of the level of attention you give your comments and attention to detail when replying. This is a prime example. You’ve read this reader’s mind for what the comparison between debt to GDP looks like.

You leave no stone unturned. Caught me in a good mood wanting to give some praise. No brown-nosing here. Just very appreciative.

Big thanks. Much love.

From the viewpoint of large organizations (40 billion cash flow a year and larger) U.S.Treasury securities are a low cost insured banking account. Inflation works as a banking fee. Yield curve inversion is velocity of money slowing down. These beliefs calm my anxiety about U.S. debt but don’t really help that much with investing.

Reckless, Madness, Untenable . . . the smart people realize the dire situation we’re creating , but the “smart” money keeps piling in. What happens when it all implodes and topples like a jenga tower?

What can an average Joe or his children do to insulate themselves?

Not gonna “implode.” But gonna have more inflation (maybe in the range of 3%-6%) than we had before.

So, default is never in the cards? I can handle 3%-6% inflation – I remember the 70’s-80’s.

Correct, actual default is not going to happen, a government doesn’t default on debt in its own currency.

They can and do default on debt they issued in foreign currency, though. For example, Argentina didn’t default on its peso debt. It defaulted on its dollar and euro debt. And it blew up the peso and the peso debt with double- and triple-digit inflation.

Inflation can be a form of default if it’s big enough. But as we have seen, the Fed can stop it from getting that big. It will likely allow it to run in the 3%-6% range.

If inflation is likely going to run in the 3-6% range, it doesn’t imply nice things about the Fed’s communications (e.g., the 2% inflation target), transparency, and governance.

If it’s really going to take 3-6% inflation to avoid crisis, the Fed isn’t doing anybody any favors by communicating a 2% rate target.

Bobber,

1. So the Fed’s target is 2%, but their measure for that target is “core PCE” inflation, currently 2.7%. Most of the time, core PCE runs lower than “core CPI,” but the CPI is the main consumer price index we have (the PCE price index is kind of weird, and it’s not used to index anything, everything is index to different versions of CPI, such as SS COLAs, TIPS, I bonds, etc.). So the 3-6% refers to core CPI, which is currently 3.3% and rising.

2. letting core PCE inflation run somewhat over target by keeping interest rates higher, but not so high as to trigger an economic slowdown or a recession, is likely the new game. So they’re not going to panic if core PCE gets to 3.5% and core CPI to 4.0%, and their policy rate at that time is 4.25%, something like that. But they’re going to crack down when core PCE is maybe 4-5% (core CPI over 5%), with policy rates at 4.25%. So they’ll pivot and hike at that point. That’s my guess, and that’s what I meant.

3. Their communications are geared to inspire confidence that inflation will go back to 2%. The hope is that this will reduce inflation expectations to 2%, which the Fed hopes will keep inflation lower. But that whole theory about “well anchored” inflation expectations keeping inflation down is just a theory — and if you ask me, a flimsy one.

if 3-6% is the real target of what will be allowed, the 2% is an illusion, and the 10 year should really be 6-9%. i agree with bobber. they’re misleading the bond market as to what the real target is to prevent yields from blowing out.

Franz G,

read my reply to to Bobber, right above your comment.

So be an owner of assets to keep pace with inflation.

Over the decades I’ve personally come to understand US treasuries as the last “paper wealth” that will still be standing before the lights go out. Stocks, corporate bonds, even bank deposits can drop or disappear through market forces or Sunday evening rule changes but Treasuries seem to always be there, the number is the number and the terms are set. Aside from real estate or I suppose physical gold they should be at the base of most people’s financial pyramid. Short and long term cash sleeps comfortably in Notes and Bills and the individual saver/investor sleeps relatively well too.

The day there is a wobble or doubt about US treasuries being paid in full and on time is the day you crack open that special bottle of wine and enjoy a meal with your loved ones because the following morning the whole system comes crashing down.

I agree.

Lots of comments about how the Fed props up the stock market, but the bond market is what they really care about. They’ll let stocks crash and burn if it’s needed to prevent a sovereign debt crisis.

there’s never a possibility that the u.s treasuries or euro based debt won’t be repaid in full. the possibility is that inflation takes hold to the point that investors demand much higher yields, and the yield curves blow out.

Foreign governments own 9.2 trillion dollars out of the 35 trillion of Treasuries issued (26 percent).

The problem is with short-term debt, an excessive volume of suddenly prone shiftable liquidity. A run on the dollar, a loss of confidence in the dollar, will stem from foreign accounts ending their rolling over of T-bills.

The BEA says we spent 1.1 trillion dollars on interest alone. Discretionary spending has fallen significantly. There’s no such thing as a shortage of safe assets. There’s a surfeit of safe assets. That’s why we have an O/N RRP facility to support short-term interest rates.

Without the O/N RRP we’d have negative interest rates and higher asset prices. The FED has a long way to go to ensure price stability.

“The BEA says we spent 1.1 trillion dollars on interest alone. Discretionary spending has fallen significantly.”

Just to make sure: that’s an “annual rate,” what interest expenditures would be for the entire year at the current quarterly pace.

The foreign treasury buying topic is incredibly fascinating and a rabbit hole that’s like a black hole.

This foreign buying is linked to tax treaties and IRS reporting which in many cases is related to foreign baby boomers looking for income streams.

Several weeks ago I was getting curious about Mexican bonds, because yields were like 12% — but, all these nagging issues of residency and taxes and currency exchange rates and differentials, make the foreign investment game challenging.

Obviously the Yen carry trade comes to mind — and that type of sophisticated strategy rolls over to foreign buyers that leverage bets into equity markets as well.

The narrative of a weak dollar really doesn’t fit well with the deficit narrative — it’s confusing to think about the cleanest dirty shirt — because in reality the other shirts belong in the trash can.

In that perspective, even the upcoming global election chaos is probably not going to amount to much of anything, because the entire world depends on dollar stability — and even though there are various ideological disagreements, the dollar and US treasuries are the only game — period — it doesn’t matter if you’re speculating in bitcoin, gold, Yen or candy — you need dollars to make a deal.

US treasuries, and the dollar, are ultimately backed by the full faith and credit of our nuclear arsenal, and our willingness to use it (note Japan 1945). Those looking for or hoping for a collapse of the US dollar or financial system do not seem to grasp this simple fact.

True, but imperialism expenses are not often popular with the populace if there is any direct impact. Given we have harmless countries North and South and lots of fish on the other sides not much concern

Probably more a matter of time scale as I am sure other Empires(Khmer, Roman, etc) thought the same thing, albeit no nukes. There is no near term danger of anything other than perhaps inflation and inconveniences. Fortunately the US doesn’t engage in expensive and unnecessary ground wars that are impossible to win with undefined objectives.

What nimrod bought the recklessly ballooning US debt?

Ok…I bought a few treasury bills.

With all the good economic news about, my cleanest dirty shirt won’t be noticed.

No laughing too loudly. Boiling the Frog slowly (aka moderated inflation) applies to us domestic froggies buying debt as well as international concubines like Canada, Japan, UK, Australia and the terminally foolish Euroweanie colony.

Smart of China to aggressively buy gold for the past few years and diversify away from $US-T. Gold is going to hit $3000 by year end.

Seem like a boom for all risky assets for the incoming years.

Gold will be heading sharply down to well below $1000 per ounce and then headed much lower as huge amounts get dumped. There are few assets more absurdly overpriced than that useless stuff.

When the stock market crashed in 1987, total treasury debt was less than 2.5 Trillion, total US stock market capitalization was interestingly about the same, now the stock bubble dwarfs the debt bubble (!) US equities now over $57 Trillion– thanks in large part to AI insanity. Also, at the peak of the 1999/2000 tech bubble, the US market cap to GDP ratio was 132%, it has just blown through 200% (way, way, way past the Buffett indicator,) so even though the TV stock pumpers continue their relentless cheerleading and total ignorance of valuations, using the dot com bubble as a reference point, this is by far the biggest bubble in history.

Gold up 30% in one year? HUH? 30%??? S&P 500 & Nasdaq one down month in a year? HUH?? It’s the EVERYTHING bubble. It’s like a horror movie just in time for Halloween. There was no subprime housing bubble, and mortgage backed securities were rock solid, until suddenly there was a subprime housing crisis and mortgage backed securities fell through the floor. We saw what happened to stocks on August 5th, and that was supposedly due to just the unwinding of a carry trade. JUST THE UNWINDING OF A TRADE! So that tells you that the true fair value of stocks is MUCH MUCH LOWER. What if something genuinely bad were to occur? A recession/slowdown/hard landing. Disappointment from mega cap tech companies. Continued high inflation. Adverse geopolitical event. Valuation reset. Take your pick. Add a few of your own perhaps.

My LOCK S&P target is still 4500, 4100-4200 is a coin toss.

A big part of this issue relates to international trade. Most of these US dollar-denominated bonds were *not* purchased as investments, but as instruments for international trade, which is mostly conducted in US dollars.

There are many benefits for the US with the current system. One them is illustrated in this post by Wolf: foreign countries continue to buy US bonds despite these clearly being risky assets. But one huge disadvantage that this current US dollar-denominated system represents for Americans is that it creates an overvalued US dollar compared to other currencies, which hurts US-based industries sensitive to internal trade, such as manufacturing.

A long-term solution might involve conducting internal trade with a basket of currencies, SDRs from the IMF, or some other similar scheme (maybe assets backed by gold, cryptocurrencies, etc?).

With all due respect, U.S. treasuries are among the safest assets in the world. There is nearly zero risk.

Secondly, your logic regarding ‘currency-mixing domestic trade = increased efficiency,’ is bewildering, to say the least. I am having trouble circling your thought process there.

Wolf, you even work on Saturdays?! Good gracious. You are really dedicated to your craft. I’m shocked that your site hasn’t blown up. In a way, I’m kind of relieved it hasn’t because these comment sections would just become a cesspool. At the moment they are the best on the internet. I know your moderation has a lot to do with that so thank you.

I work on Sundays too 🤣 (though I might not write an article on Sundays.. time to catch up with other stuff).

But I ❤️ my work (most aspects of it), so it’s not really work, it’s something I ❤️ doing even on weekends. Life is short, you gotta do what you ❤️ doing. I got back from my swim in the San Francisco Bay a couple of hours ago, and the cold water and being immersed in nature and totally cut off from everything except seals, sea lions, and waterfowl put me in a superb mood, as you can tell. That superb mood was only slightly worn down by the 120 spam comments I got while I was swimming, and they clogged up all my filters, and I had to manually clean that out and block a bunch of IP addresses. But other than that, great day so far.

Hell yeah cold water swims are amazing for your health and this site is the best financial blog out there! Thanks for the in depth and balanced perspectives and keeping it all real in a not-so-real world.

If you have a genuine passion for something it is almost impossible not to be successful at it.

A treadmill I use at my gym has several recorded walks of San Fran. Neat place!

There are two storm clouds, no longer small and no longer on the horizon, that have the potential at some indeterminate future date to “wash” the U.S. $, and the foreign-E-$, “down the drain”. They go by the name of “foreign trade deficit” and “domestic federal deficit” (Twin Deficits Hypothesis).

These deficits have an insidious, if not an incestuous, relationship. Positive interest rate differentials are significantly responsible for the dollar’s exchange rate support (DXY Pivot ↑).

And an “overvalued” dollar in turn is the principal contributor to our burgeoning trade deficits (on-shore CNY Pivot ↓ and off-shore CNH Pivot ↓).

And as Professor Pettis puts it, “Excessive use of the U.S. dollar internationally actually forces up either American debt or American unemployment”. As: “many of the new cross-border investors were governments”…”foreign governments recycling the inflow of both foreign direct investment and current account surpluses.”

The U.S. can be more creative than selling its birthright for a mess of pottage (becoming a financial hostage to the Pacific Rim), indeed, its Western plantation (“the capital account reflects net change in ownership of national assets”).

To be effectively competitive in foreign markets, requires that we sell lower unit costs and higher quality products. This means concentrating on production, innovation, and product quality. It means giving workers a financial stake in increased productivity (share in profits, etc.).

Trade Balance: Goods and Services, Balance of Payments Basis (BOPGSTB)

https://fred.stlouisfed.org/series/BOPGSTB/

The query whither the Dollar? can only be answered by correctly estimating the future level of foreign investment demand for dollars. The foreign exchange value of the dollar will not fall significantly until foreigners become sated with dollar investments.

No one, of course, knows the future trend of the trade-weighted exchange value of the dollar (basket of foreign currencies). If it is assumed that the U.S. Government will persist in multibillion dollar unilateral transfers to foreigners and that the trade deficits, even though reduced from present levels, will continue; the future course of the dollar will be down, unless the payments gap is filled by foreign investment.

So is the plan no landing at all?

I don’t see how the fed can ever get inflation under control and return it to 2%. My opinion is we will just see continuing rising of prices at a higher rate than the fed wants.

Well Jobs now are the larger worry.

If Jobs go, we’re in for it. The R word

And I’ve heard once jobs start to slip, it’s not pretty. And you cannot stop the momentum.

Or so I’ve heard!

Real treasury yields need to go negative again. Specially the 10 year. This will solve the problem. A weaker dollar is the only solution. Real positive yields are unsustainable in the long run. If you adjust the debt to inflation it will start to reduce. It’s just maths.

More over, a weaker dollar will have the same effect as tariffs, without generate a full scale tariff war with allies and China.

That’s the same reason Bitcoin will never be a currency, cause it is deflationary. If everyone thinks Bitcoin is going up, then everyone expects the prices of everything to go down when measured in Bitcoin terms and therefore there is no incentive to expend. It’s a spiral of death to the economy, a japanification.

You’re talking like a troll from a foreign land wishing economic destruction onto the US with these prescriptions?

1. clue: a weaker dollar that you love so much would instantly boost inflation since the US has a huge trade deficit, DUH!

I’ve never heard of Agency debt, didn’t realize parts of the government had their own bonds. This is worth a Wolf article to explain it!

You’ve heard of them, including here, a lot. Agency debt includes the debt issued by the GSEs such as Fannie Mae, Freddie Mac, Federal Farm Credit Banks Funding Corporation and the Federal Home Loan Bank (FHLB).

In addition, it includes debt issued by government agencies, such as the Federal Housing Administration (FHA), Small Business Administration (SBA), Tennessee Valley Authority (TVA), the Government National Mortgage Association (Ginnie Mae), and maybe some others.

Some of this agency debt is issued as agency MBS (pass-through securities), but not all.

The two types of agency bonds – GSE bonds and government agency bonds – have largely de-facto fused into one category since the government conservatorship of Fannie Mae and Freddie Mac.

There are some differences to Treasury securities:

1. All these entities borrow to lend — they issue these bonds at a low rate, slightly higher than Treasury yields, and then lend these funds to third parties. So they don’t borrow funds that the US government then spends on its budget items.

2. Some agency debt is callable – can be redeemed before the maturity date at face value – which is a risk when rates go down and the bond gets called, and you lose your high-yield bond and have to replace it with something new with lower-yields. Treasury debt is currently non-callable (but decades ago, some of it was callable, which caused a stink when they called the callable 30-year bonds with 15% coupons issued in early 1980s.)

3. the yields are a little higher than Treasury debt because of the call feature and because of liquidity issues in the market for this debt, meaning harder to sell without a (small) haircut.

4. The interest income from ONLY SOME agency bonds is exempt from state and local income taxes (like Treasury securities). But others, such as Fannie and Freddie bonds, are not exempt.

What else should foreign holders do with the sea of dollars created by the US current account deficit instead of buying US assets and which US assets are safer than the risk-free US Treasuries?

This is a portfolio decision — given the n-many factors which influence individual portfolio construction there can never be a single answer to your question.

Am not sure I understand you. At the end of the day, surplus dollars held by overseas entities must end up in an American bank account. And those dollars in American bank accounts will be invested in something – either in risk-carrying assets (e. g. real estate) or risk-free assets (e. g. Treasuries). There is no other way. So foreign entities owning dollars must invest those dollars in the USofA as long as they want to stay in dollars. Otherwise, they would have to sell those dollars to someone else against another currency and then that someone else will have to invest the dollars in the USofA.

Hey, non-US folks commenting here. BRICS+ fantasies of de-dollarization and replacing the US dollar as the global currency are getting really old.

I understand there is the big BRICS+ meeting in Russia with all of the fanboys of this. Those heads of state are old and this plan will not live beyond them. Heck, Lula (supposedly) fell down and went boom on his head, like a old man losing his balance.

I realize my country can be a bunch of assholes and often, I am at odds with our policies. But, I like my prime cut steaks and fresh strawberries.

I like my big ICE SUV and my house and my beach house. I like my kids going to the best private schools and getting the best careers and jobs and hopefully, getting married to similar level of people.

I feel bad at times, but I am not willing to give up my lifestyle. If US folks are truly honest to themselves, they are not willing to give up anything, either. No real outrage about Ukraine, Israel, or business as usual to keep up our hegemonic empire. What happened at Afghanistan? Don’t remember and forgotten like a fart in the wind. Smells bad at first, but dissipates quickly. So shall BRICS+.

@HA: I wouldn’t get too cocky. Past performance is not indicative of the future.

BRICS+ is not just an adhoc group. And it is not made up of old politicians making unilateral decisions. They have their own bureaucracies and institutions which will last well beyond the current group of politicians – and they have institutional knowledge and memory.

These are countries with billions of people and they are going to make decisions in their own interests. So I wouldn’t be arrogant enough to assume that the future is going to be the same as the past.

I am with you! I also like driving my boat in the summer while staying at my beach house! The Hobie 16′ is also a lot of fun!

Mr. Richter,

Speaking of inflation, the dollar, US Treasuty Securities, the Federal debt and foreign buyers of it, per your recommendation, I purchased a 3 pound can of Kirkland Columbian coffe at Costco the other day ($14.99).

My question for you is, since this is such a large size, how does one keep the coffee from going stale after opening?

Kudos on your inflation-fighting strategy.

It’s whole bean. That’s the key. After you grind it, coffee begins to oxidize (go bad) immediately. Within hours you can taste the difference.

Which is why ground coffee is sold either vacuum-packed or nitrogen-packed to prevent it from coming in contact with oxygen, which causes oxidation (oxygen causes iron to “rust” and coffee to go bad). Once you open a new bag of ground coffee, it goes bad very quickly.

Whole bean coffee doesn’t have that problem because only the surface of the bean (a tiny part of the total bean) is exposed to oxygen and goes bad. And it’s too small a portion to taste. So if you drink coffee every day, and the bag lasts a week or two or three, there won’t be any detectable deterioration. That’s my experience with any whole-bean coffee. Maybe if it’s open for a year, you might taste some deterioration. But I’ve never tried that.

What I do is I grind the coffee right before brewing it. Even if you wait an hour, the oxidation has already started. Once I brewed the coffee, I drink it right away, I don’t dilly-dally around, because it instantly begins to oxidize very rapidly and is bad within 10 minutes or so and goes from bad to terrible in 30 minutes (“old coffee” taste).

Just remember: That wonderful smell of coffee is the smell of coffee oxidizing and going bad.

Wolf – superb and artistic piece of ‘everyday’ inflation-adaptable technical writing, a real pleasure to read!

may we all find a better day.

Like oxidation heat loss is a function of surface area relative to volume. So if you use a double walled mug that is taller and narrower your coffee will remain hotter and taste better longer!

Until I discovered this by accident I always felt rushed drinking my coffee. Now it’s a relaxed cup of coffee. Try it I think you’ll agree!

Buy a coffee grinder, as Wolf says. Only costs about 15 bucks. Only buy whole bean. The difference in taste between grind-yourself whole bean coffee and already ground coffee from a can is very pronounced. You won’t go back to that already ground stuff. Whole bean and a grinder is the way to go.

I see ten-year Treasuries hit 4.18% today. In your face, Chairman Powell. It used to be said, “Don’t fight the Fed.” Looks like it is now “Ignore the Fed.” Bond market says we have a strong economy and increasing inflation. When ten-years get back up to 5%, I’m buying.

I concur. Additionally, put the freshly brewed coffee into a

carafe immediately. The heater in most coffee brewers is in fact a coffee burner. The coffee ought to have a reddish hue after brewing. If its brown its burnt.

Thanks for this tidbit. I love pure black coffee!

Baloney. Coffee is fine from the Costco DD container and is good for at least two hours after brewing in the morning. I think Wolf is a “coffee snob” – like one of those obnoxious oenophiles.

A small strong delicious cup of coffee — and making it — is one of the simplest big pleasures in life, and you’re not going to be able to take it away from me by calling me a coffee snob 🤣❤️

People in the SF Bay Area know about good coffee. Cafe Trieste in San Francisco started it all with the beatniks. Peets, opened in Berkeley, and continued the tradition of providing quality coffee (Major Dickason whole bean is my favorite). It is not being a snob. It is just not liking to drink the muck that often passes for coffee.

For the last several months I’ve tried turning the question on it’s head:

To what extent does the treasury market/federal debt expand/contract based on the needs of the global economy/markets?

Try as I might to come up with metrics to define this I’ve failed. Anyone got any ideas?

TLT showing no sign of slowing down on the way to 85.

inflation expectations and the expected volume of federal deficit financing now represent the principal factors determining long-term interest rates.

If current projections of federal deficits materialize in this and the next few years, interest rates (both long and short-term) will be driven up sharply by the increased demand for loan funds.

They are war economy budgets and require the controls dictated by a war economy if they are to be achieved.

The Nominal Broad U.S. Dollar Index peaked at the same time the 10yr constant maturity yield peaked 10/22. From this past performance, one can project that the currency markets / foreigners are now predicting higher US interest rates and therefore higher interest rate differentials between FX pairs. I.e., the $ has retraced most of the recent fall in the $’s value due to the FED’s policy rate reduction.

Japan was kind enough to give us a rather large hint as to what is transpiring when they unexpectedly raised front end rates by a mere 15 basis points a short time ago. The carry trade unwind that ensued was spectacular. Every country mentioned is either like Cayman just a PO Box domicile for US Hedge Funds or a money laundering center like London. Hard to short Euro government debt but you can issue there which is rather the same thing. All of this is one reason the derivatives market is such a gargantuan behemoth now. The most interesting twist, besides Japan, has been the very recent 50 basis point cut in the US that actually only helps folks that have access to the discount window. We should probably be really worried about what the Fed is seeing on the bank side because post cut we have had a 100 beep swing in overnight / 30 year and my bet is that this move in rates indicates the market is much more fragile than we think it is.

In terms of your last sentence, nah, it was a couple of days at the end of the quarter when liquidity flows are very big and temporary frictions can rise, that SOFR went up a few basis points for a couple of days, which (higher yields) is how liquidity gets redirected from where it’s in excess supply (low yields) to where it’s needed (higher yields). This is going to be the normal condition as excess liquidity gets removed from the market by the Fed’s QT. The Fed’s Logan addressed that today, no biggie. And she is big on the Fed going slow on rate cuts and keeping QT going. Article coming.

Logan;

Logan said longer run it’s likely money market rates should be close to or just above the interest on reserve balances rates

iORB @ 4.09 and money mkt paying 5.07 — additional rate cuts are ridiculous

Oh well, it’s ok being paid to wait for a correction

IORB = 4.90% currently. Money markets she talked about are not the MM funds you buy. The TGCR = 4.82%.

Of the foreign banks buying U.S. debt, how many of them have used the Fed’s other facilities, and to what extent?

Full FAITH and credit!

Same as it ever was!

1. Banks in foreign countries don’t have access to the Fed’s facilities.

2. Some CENTRAL BANKS have access to the Fed’s swap lines. When Credit Suisse was taken under, the central bank of Switzerland (SNB) engaged in dollar swaps with the Fed for a few weeks as backstop for the dollar-liabilities of Credit Suisse. Those matured and were gone within a few weeks. And nada since then.

3. Or did I just waste my time on another one of your homemade conspiracy theories?

MW: 10-year Treasury yield heads toward highest since July as deficit worries rise…

The market value on the huge outstanding $35 trillion in US Treasuries keeps falling as yields on these securities keep marching higher. As long as they are held to maturity this is not an issue, but it does significantly impact the market value of those US Treasuries now.

MW: Dow falls over 350 points as stocks extend losses amid rising bond yields

Drunken sailors typically have the cleanest dirty shirt.