Rise of Zombie VCs that stick around collecting fees as their startups run out of cash and die. The AI boom is the exception.

By Wolf Richter for WOLF STREET.

Outside of the boom in anything with AI or Machine Learning (ML) in its name or description, a lot of hot air has come out of the Venture Capital industry from the steamy levels during the free-money era of the pandemic.

Since the Fed started hiking rates and switched from QE to QT, marking the end of free money, VC funds experienced large-scale write-downs of their portfolio companies. They now cannot exit those startups by selling them because the market has tightened, after many hundreds of companies that VCs sold to the public during the free-money era via IPO or SPAC merger collapsed and entered into our pantheon of Imploded Stocks.

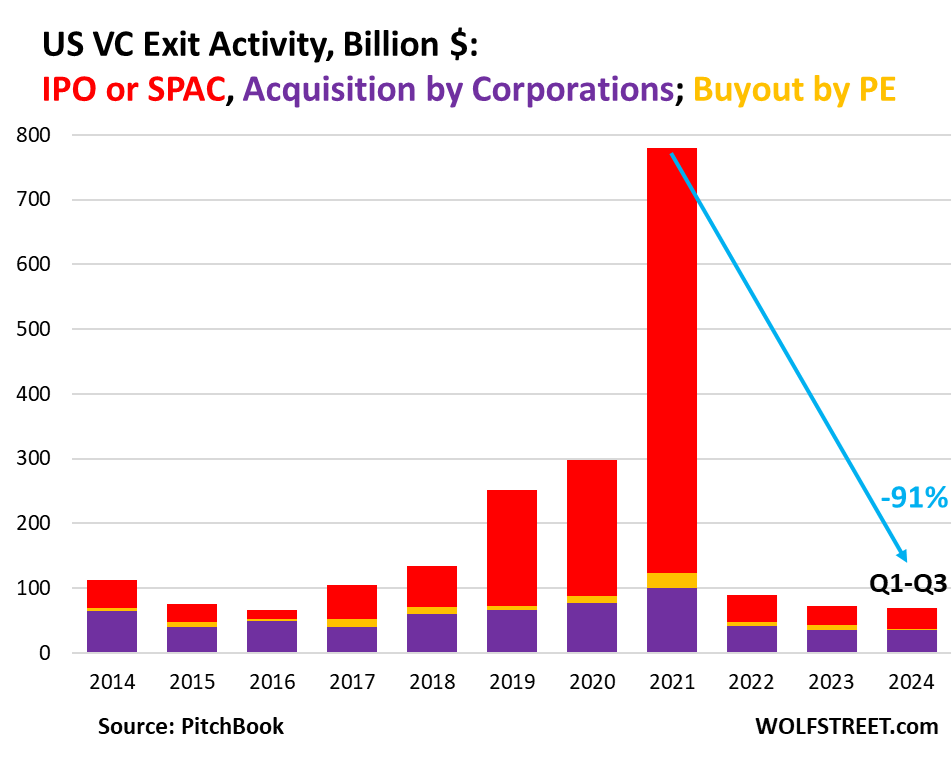

Exits in dollar terms amounted to only $10 billion in Q3, according to the Venture Capital Monitor for Q3 from PitchBook. VC funds sold only 14 portfolio companies via public listings. For the year through Q3, VCs booked only $69 billion in exits, down by 91% from the full-year 2021 of $780 billion in exits, which was the steamy and final year of free money. In 2024 so far, compared to 2021:

- Exits via IPOs or SPACs: -95% (red)

- Exits via buyouts by PE firms: -91% (yellow)

- Exits via acquisition by Corporations: -64.5% (purple)

Successful exits are what makes the VC industry work. VC funds have to be able to sell their portfolio companies, at least some of them, at a huge profit, and then distribute the proceeds from the sale to the limited partners (LPs) in their funds so that these investors can re-invest their VC allocations in new VC funds that invest in the next cycle of startups.

The exit is when everyone makes money – except, as we learned over the past three years when these newly public IPO and SPAC stocks collapsed, the buyers; they ended up holding the bag. But now the whole system of exits, fundraising, and dealmaking has gotten clogged up because the pipeline of exits is blocked.

“The market continues to be flush with headwinds despite the 50-basis-point rate cut from the Federal Reserve (the Fed) in September, which will continue to pressure the exit market for the near term,” PitchBook said in the report.

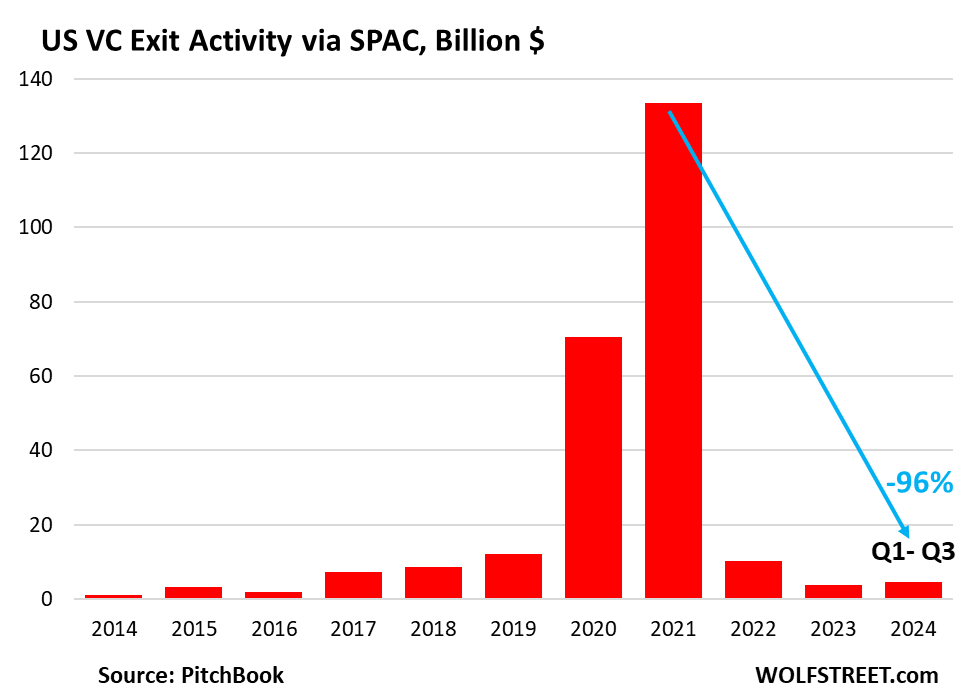

Exits via merger with a SPAC, which have proven to be particularly destructive to buyers of those shares, have collapsed by 96% in dollar terms from the peak of the whole year in 2021 to just $4.7 billion so far this year.

Blocked exit pipeline causes indigestion. Because VC funds cannot sell, or don’t want to at currently possible valuations, their portfolio companies have been staying private for longer as they wait for the miracles to be performed by some rate cuts from the Fed.

These still private companies have to raise funds in new rounds of funding, often down-rounds at lower valuations. And those that are not so lucky and cannot raise funds are left to fend for themselves by cutting expenses until they run out of money and shut down.

The backlog of companies in the blocked exit pipeline has ballooned the US private company inventory by about 26% over the past three years, to a record high of 57,674 startups, according to PitchBook.

“This upward trend of private company inventory means investors are struggling to translate numbers on their balance sheets into realized returns to reinvest into VC, so startups are having a harder time securing additional rounds of funding,” PitchBook said.

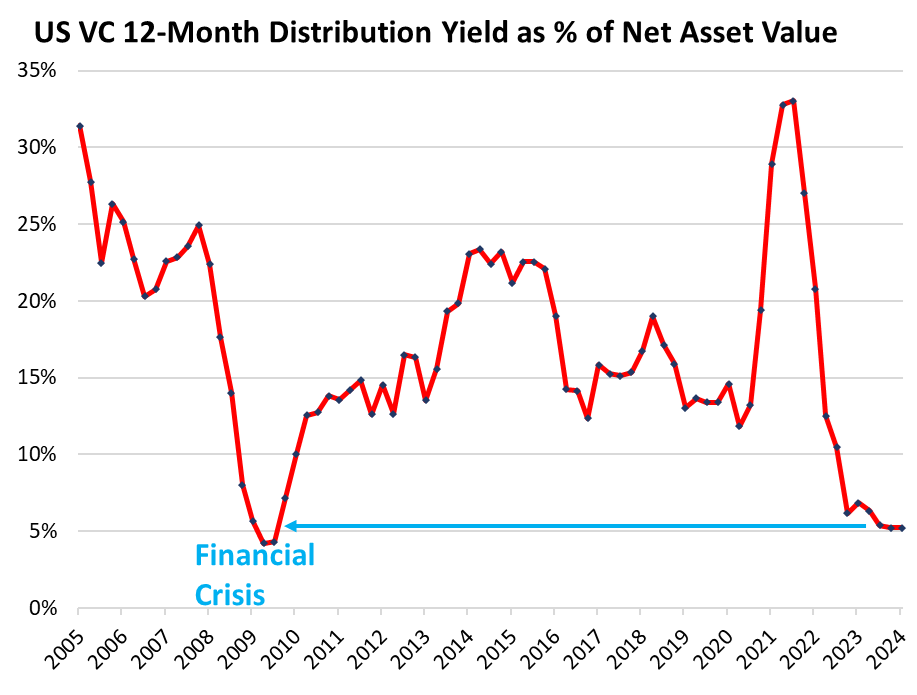

And cash distributions to their Limited Partners have plunged. PitchBook:

“As a share of net asset value (NAV), our most recent data shows that cash back to LPs is flowing at a rate nearly as low as during the global financial crisis (GFC) and has been in the single digits for eight consecutive quarters.

“The average quarterly rate of distributions over the past decade has been 16.8%, demonstrating just how dire the distribution scene has been.

“This lagged data point is as of March 31, 2024, and knowing that Q2 and Q3 were also incredibly slow in terms of exits, we expect this rate to remain as low as data is added.”

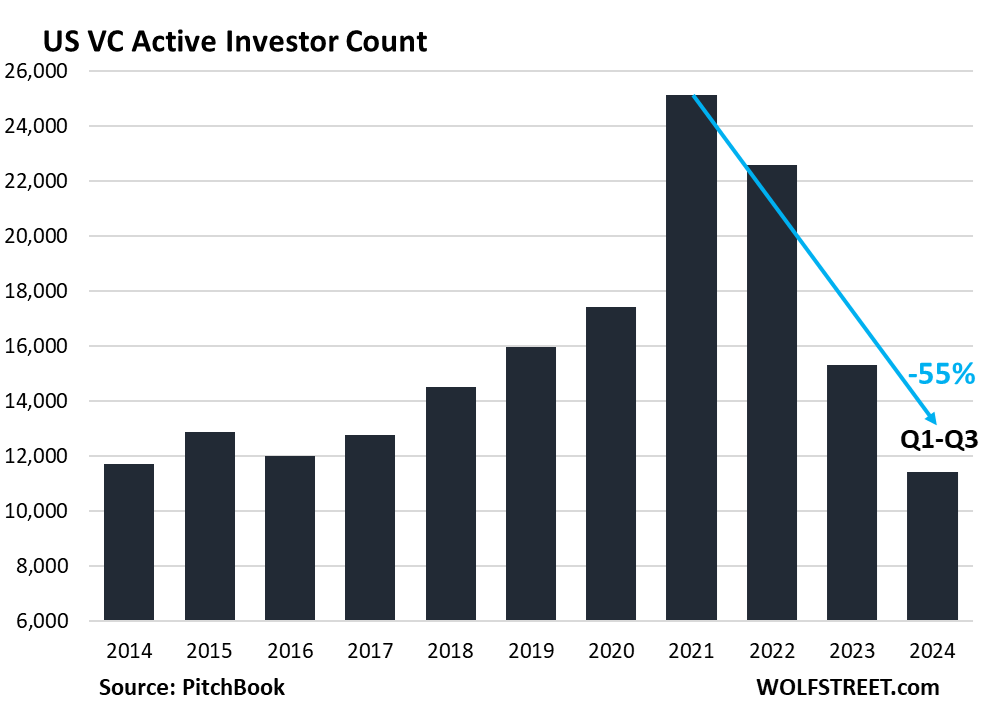

The rise of the zombie VCs. The number of active venture investors – those that made a deal in 2024 so far – has collapsed by 55% from 2022, to just 11,425 unique investors, according to PitchBook.

The other 45%, around 14,000 venture investors, have not made an investment so far in 2024. They represent the ballooning ranks of the zombie funds. PitchBook said in a note:

“So-called zombie funds can’t raise money from LPs or write checks to new startups. Unlike the companies they back, which go bankrupt when they run out of money, GPs tend to disappear quietly. By overseeing their existing portfolio and collecting management fees, these firms can operate for years as zombies.

“When the venture market took a turn over two years ago, industry watchers began to warn of an impending rise in these funds.

“One prominent voice, then-CEO of Techstars Maelle Gavet, predicted in a 2023 CNBC interview that: “[it] could be as high as up to 50% of VCs in the next few years that are just not going to be able to raise their next fund.”

Clamoring for lower rates to unclog the pipeline. Free money is the best money obviously, including for the VC industry whose free-money boom was spectacular, allowing them to exit a huge number of portfolio companies at huge valuations via IPOs and SPAC mergers that then collapsed within the portfolios of retail investors. But this may have been as good as it was going to get.

Now the Fed has cut by 50 basis points and everyone is clamoring for more cuts to make sure that T-bill yields of 5% are wiped off the face of the earth, so that this competition for VC funds vanishes, thereby making VC funds more appealing to LPs as an alternative.

But those rate cuts may be a mixed blessing. Since the Fed has started its rate-cut cycle, longer-term Treasury yields have shot higher, with the 10-year yield up by 45 basis points to 4.10% as of Friday, as the yield curve begins to un-invert and inflation fears resurface in the bond market.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Perhaps a company rename can help, as in, from anything “dot com” to anything “blockchain” to anything “AI.” But I guess the public company stockholders are the ones to fall for that.

Maybe put “NFT” in the name. Oh, wait…

What about the vr-verses?

You forgot all about those :-)

“57,674 startups in the pipeline” makes me scratch my balding head. what needs “disruption” so badly? bacon? cat litter? nail polish? eggs? carpets? cough syrup consulting?

I would struggle to come up with 1/10, no 1/100 of possible viable business ideas in a decade, and somebody managed to “create” 57,674 startups out of .. their .. place where sun does not shine

This startup culture and the infrastructure to fund it and guide it is actually one of the reasons why the US economy is so dynamic. New blood and challenging ingrained ways are always good, even if much of it eventually goes bust. It leads to the kind of dynamism that keeps companies on their toes.

While I agree the startup culture is a major driver of the economy, I fear in the last 30 years the goals have shifted from the pursuit of products and customers to the almost single-minded pursuit of VC money. Of those 57K startups, I would bet more than half don’t have a single paying customer or even a finished product, just some wild idea showered with $$$ by some VC. VC money has become the crystal meth for entrepreneurs. It’s tremendously wasteful and inefficient.

I would bet that the vast majority of these new startups have to do with creating apps for your use. You know, an app to keep track of the length of your finger and toenails and let you know when it’s time to cut them. Plus, be able to send a message to your manicurist, if you have one. Or find you one….

I’ll bet there is not a new shovel being invented anytime soon.

But there is surely one in the works: the iShovel, a virtual shovel to dig virtual dirt, by subscription only for $49.99 per month.

/sarc

The cartoons this stuff produces are getting especially good.

I’d call it art…sorta…..

On a more serious note, I agree with your comment about many of these apps. I see these “fintechs” with apps that alert you when you’re about to run out of money so you don’t incur bank fees.

We had those too, back in the day. They were called checkbook ledgers, where we recorded income and expenses as they occurred, and knew to a penny how much money we had.

There is no need for a new shovel. Railroads usually bought the best and it is still possible to find some of them floating around out there in excellent condition to handle most of your labor intensive needs. But it may be necessary for someone to invent people who can figure out how to use hand-operated air-cooled tools without first needing to consult their Smarmy Phone or holding an endless round of verbal battle with that femme fatale “Dislexia”. (No doubt, there’s a biolab in China working on that one right now.) A decade before Wolf started weed whacking his own head strands, I went down to Biggest Box and picked up a Vidal Sasson POS electro hair clipper for around 13 buckaroos. Another corporate branding case of “good idea, poorly executed”. It took two washers inserted as spacers behind screws and I was off and buzzing. It still works, so if need be I could mow the neighbors’ lawns for them. But I have no control over any failures by the utilities folks to deliver voltage continuously any more than I can keep Apple from constantly screwing up their Ipads everying time they dump more sh*te into the darn things. That all may require some much larger washers!

@BuySome: “Smarmy phones” I love it. LOL!

Damn. You keep all the good hard researched info to yourself and leave strange little comments. My credibility here is getting shot to shit!

NBay,

To publish this stuff, you need to start your own blog. That’s not what this site is for. You can start a blog very easily and free on Substack.com It’s a breeze, no technical knowledge required. Kitten Lopez switched over to Substack. It could be your new passion. I think nbay.substack.com is still available. Go for it!

I’m too lazy to write all the time….or even some of the time. I’d rather chase info down, than write about/explain very much of it…..Also there are too WAY many subjects that are part of this world……So….overloaded desktop…….anyway,

You got me there.

Your site, your subject, your rules…..your discipline.

Wondered what happened to Kitten, though, thanks. I know you really helped her a lot. Good man.

You can look up Kitten on Substack. She posted some of her tragic laments there. Her partner James died of brain cancer. She got in trouble with a neighbor and the landlord, and lawyers and judges got involved and all kinds of complications ensued. She was forced to take some of her posts on Substack down with which she’d attacked certain people personally. Some of it is hard to read – so much anguish.

This is her Substack:

https://recordscratchradio.substack.com/

Tip: if you don’t want to subscribe, click on “that’s enough” instead of submitting your email.

Thanks

Venture capitalists? Couldn’t have happened to a bunch of nicer people…too bad most of them will still be filthy rich despite all these mishaps..

These types’ first instinct, I think, is to structure the fees so they aren’t the bag-holders.

Is there an app that would tell me how to do that?

Curiouscat,

You just reminded me of the ‘There’s an App for that’ Apple TV ads that ran along with the launch of the very first iPhone. What a blast from the past.

During 2021 SPAC boom you got 20-50x multiples on revenue, basically zero due diligence and didn’t need to be profitable.

If you needed to “wait a few years” in 2021 your company either no longer exists or will no longer exist soon.

All that’s left in terms of legitimate companies are seed and series A/B who were too small in 2021 and will take several more years (at least) until they’re ready for going public. They’ll have down rounds but be fine in the end as revenue grows over a handful of years.

Until then I think things will be very quiet.

2020 and 2021 were such a spike/anomaly in terms of aggregate numbers (# of deals/amounts of money), you really have to ask if some kind of semi-organized fraud was going on (“pandemic” funds-to-vapor “SPACs” pipeline for instance…although apparently/allegedly SPACs have some built in safeguards against utter fraud).

I have to ask my old question again – How exactly did “pandemic replacement” trillions somehow translate into many hundreds of billions available for things like SPACs? I mean in the forensic sense, players and timelines.

Which investors exactly – controlling tens/hundreds of millions each – thought the middle of a shutdown pandemic was a peak time to roll the dice on hundreds of vaporware SPACs?

My guess is that a granular investigation of the hundreds of SPACs (which made up a big chunk of the IPO count too) would turn up some very, very bizarre circumstances.

You’re trying once again to make up conspiracy theories, which seems to be your hobby.

There was one guilty party in the SPACs: retail investors. They bought this shit, driven by their own greed and ignorance. And they made it all possible. If they had refused to buy these stocks, there wouldn’t have been any SPACs, and no boom.

That’s what is happening right now, burned retail investors are not buying them, and so the boom is dead, no one can sell SPACs because there are no buyers.

SPACs have been around since the 1990s. This was the second boom and bust. It takes about 15 years or so for a new generation of retail investors to come along that don’t know about the prior bust, and that are then jumping all over these SPACs driven by their greed and ignorance.

We, remembering SPAC bust #1, warned retail investors about the SPACs, but we were poohpoohed because these retail investors were driven by greed and ignorance. And those that got out early made lots of money. Like all scams, people can make lots of money, which is why scams exist. And people don’t care if it’s a scam or not, as long as they can make money. You can’t help them.

The question you should ask: “why did retail investors, driven by greed and ignorance, go so crazy?”

My answer is: “Free money is like a virus that turns brains to mush.” And we’re still not quite over this phenomenon of the mushed brains.

@Wolf: You said:

“The question you should ask: “why did retail investors, driven by greed and ignorance, go so crazy?”

SPACs, possibly Crypto and AI…Not sure if it was due to ignorance but certainly due to greed (Greater Fool theory).

How about the stock market and real estate? People buying at exotic multiples on the stock market and retaining 2nd and 3rd homes to cash in on ever-rising prices? Is this due to greed and ignorance too?

If yes, where is one to put their money in during zirp when the banks were paying close to nothing?

Are there any vehicles where prudent investors (who are not greedy) can put their money to get a decent rate of return?

I would contend there have been none over the last 30 years except the last two where inflation dragged a kicking and screaming Fed to raise rates.

So this is all by design to thwart the business cycle and to, by hook or crook, make sure that the markets do not come back to reality.

The government (by virtue of bad housing policies and taxation of interest but not dividends) and the Fed are both culpable.

>There was one guilty party in the SPACs: retail investors. They bought this shit, driven by their own greed and ignorance.

Thank you. I will never understand the tendency to infantilize these people. “You can’t cheat an honest man” comes to mind.

I am one of those who lost money on a SPAC. It was a stupid purchase at the time which I can now see in hindsight. It’s not like I can blame anyone else for my decision.

I didn’t lose a lot of money, but that money I did lose was the cost of tuition.

When the term “retail investor” is used, the public thinks of a middle-class stock buyer. However, I suspect many SPAC investors are ultra high net-worth investors who employ an RIA that buys stock on the retail investor’s behalf. Think rock stars, Hollywood stars and sports figures, etc.

No, you got the 3-step system of SPACs wrong. See below.

And retail investors are exactly what you said, “a middle-class stock buyer.” But “ultra high net-worth investors” are not “retail investors” – many have their own “family offices” which operate as hedge funds and are professionally managed but don’t have to jump through the regulatory hoops that a normal hedge fund has to jump through.

How SPACs work and who makes money (the SPONSORS):

Step #1: The ultra-high net-worth investors (including hedge funds., PE firms, and venture capital funds) were the “sponsors” of SPACs (they created the SPAC and IPOed it). Once the SPAC trades on the stock market as an empty shell company with some cash, it is looking for a target to buy. It trades typically at around $10 a share. And the sponsors make money already. So that is step #1.

A SPAC has two years to find a merger target. If it doesn’t find one in two years, the period can be extended or the SPAC has to be unwound, and Sponsors get much of their money back, and the IPO investors get nearly all their money back.

Step #2: When the SPAC announces a merger with a target company, the SPAC shares spike, because small retail investors buy them through trading apps, and so the sponsors make more money. And they take it and run.

Step #3: By the time the stock collapses, the sponsors are mostly out of it and made a ton of money. Sponsors make money no matter what happens, unless there is no merger. No merger is the only scenario when sponsors don’t make money. Which is why they will rather merge the SPAC with a dead body and blow up small retail investors than unwind the SPAC without merger after two years.

Small retail investors bought the SPAC shares after the IPO through trading apps, such as Robinhood. If the shares spike, the early ones make money if they get out early. The rest lost money. The sponsors – the ultra-high net-worth investors and hedge funds – the made money no matter what. That’s how that worked.

An article in a comment!

Damned good show…..I have been enlightened! Merging with a dead body was especially good!

Retention is another matter…..but this one is so well done it may just stick.

It would be interesting to see a list of companies launched by VC over the last 10 to 20 years and how those companies are viewed today. I would guess we would hear wonder stories if the outcomes were solidly positive. The only VC stories I have read before today were used to attack Mitt Romney.

It appears you might be confusing Private Equity (Bain Capital, Romney) with Venture Capital.

Private Equity is notorious for running solid businesses into the ground while enriching insiders.

Venture Capital is notorious for enriching insiders of startups, regardless of whether they take off or run into the ground.

Allegedly Private Equity accelerates corporate evolution by kicking tail and getting lazy corporations and corporate managers whipped into shape. But oops, sometimes the patient doesn’t make it, or is a husk of its former self. Then allegedly Venture Capital bears risks to get the occasional super-winners of the future off he ground, and to the public’s benefit and embrace. Either way, the fees always show up in guess-whose pockets, from he git-go. Their funds bear the risk, along with (some will say) other stakeholders affected by their doings. I find the risk transfer game fascinating (as I haven’t been directly affected enough, I guess).

I understand this article puts VC in a bad light, but I made an investment into a VC fund about two years ago. It’s a very small fund($100 million). The fund has looked at 300 ideas and invested in 12 or 14 portfolio cos. I’m amazed at the great ideas. We are ready to cash in on our 1st investment at a 40x ROE. It’s not for everyone, but I like my chances in VC vs. the S&P at these levels.

“I understand this article puts VC in a bad light,”

Maybe you didn’t read the article? This article discussed:

– how exits are becoming very difficult to pull off now. You said: “We are ready to cash in on our 1st investment at a 40x ROE.” OK great, but who’s buying? Have you found anyone yet? Corporate? PE? Public? Done deal or just hope? Why did it take so long for the first exit?

– how VC exits via IPO and SPAC through 2022 blew up retail investors, NOT LPs. You’re an LP, not the retail investor. You’re the seller not the buyer here.

– how distributions to LPs (you) have slowed to a crawl. According to your statement, you have gotten zero distributions from the fund so far (no exits). So you haven’t made any money yet. You’re still waiting to make money. How long has your money been tied up in the fund? That’s the kind of stuff the article discussed.

— you as LP need two huge exits to come out ahead even if the other 12 portfolio companies fizzle or die.

Thanks for your feedback Wolf. To your comments:

1) Yes the money is in the bank. Buyers were the largest CPA firms in the world.

2) Agreed, yes I am an LP. I have been in banking for 36 years, I understand the difference. When my brother and I invested, we expected a 7 to 10 year tie up. Not a big deal for less than 5% of my portfolio.

3) You asked how long our funds have been tied up. As I noted in my comments, our funds have been tied up for 2 years.

4) Agreed that we need a few huge exits. One is in the bank. Our VC mgt team is great. So, I sleep well.

“Buyers were the largest CPA firms in the world.”

This doesn’t sound like an IPO exit – maybe an acquisition? Although a bit of a strange one at that (CPA firm acquirers? Multiple, different CPA firms?).

Could you provide more specifics, because this sounds like a pretty unique deal.

Which brings up the second point – one instance is an anecdote…it takes hundreds to make up empirical data.

I’m glad that you were unaffected by the systemic dynamics that Wolf pointed out…but I think you may have been pretty unique in this.

The aggregate stats are the aggregate stats both historical and current.

Data has been accumulating that both VC and PE fund track records, in aggregate, may have been fairly badly oversold (this does vary across time, although the 2020-2021 madness will likely leave an unprecedented impact crater to crawl out of).

And the standard depressing fact is that since public pension funds are the primary VC/PE LPs…taxpayers/fiat dollar savers are likely to be screwed.

Again.

As usual.

An exit after two years at 40ROE implies 40-80x revenue growth in those two years at that company.

It’s been done…by maybe 10 or 20 companies ever.

And…the exit was an AI utility that automates a core client-facing process.

Clever and lucky GPs.

Perhaps similarity to with Private Equity problems in general?

That is again a bad smell for small caps. Less likely that their most explosive growth period be as a public company. Exit problem.

Before there was too many PE grabbing small companies rather than allow them go IPO earlier. Private Equity was a king back then. Again less likely that their most explosive growth period be as a public company. Entry related.

“Less likely that their most explosive growth period be as a public company.”

This.

Sellers offload the revenue surge sizzle.

Buyers get the negative income shoe-leather steak.

I’m still amazed at the percentage of Russell 2000 firms that have negative incomes. It is an ugly number and it tends to be horrible year in and year out.

Kinda explains how there are fewer and fewer public companies at all (they’ve gone under) especially if you subtract out the SPAC vaporware.

This is the Destructive part, without much of the Creative part.

I think if Oxford ever needs a picture for reference next to the word Venture capitalist and kind of SPACs or king of dumping onto bagholders, they need a picture of Chamath Palihapitiya right next to it. Talk about talking his lemming followers to the cleaner..

Another ripple down of this is how should I say this; job creation destruction. Mr Greenspan can feel free to take me to lunch for that one.

To me VC is a mixed bag. They allow experimentation, however rarely does a great company seem to be built via this route. And def some very, very, lousy ones have. Very. There’s a certain reflexiveness to technology; which allows VC’s to optimize value quickly, but the actual value of what is built is often fleeting and very opaque. A country in Asia, north Asia said not to worry too much about America trying to build things, because we were too busy looking at our insta feeds. That type of value is what seems to be created by VCs.

“Rarely does a great company get built this route”. Really???

Apple, Cisco, Nvidia, Google, Airbnb, YouTube (before being acquired from Google), Instacart, Stripe, and Facebook were all products of VC.

Sure, only small fraction of VC companies that make it. But it’s certainly not rare. And when VC is successful, it can be great for America, not just investors.

“more cuts to make sure that T-bill yields of 5% are wiped off the face of the earth, so that this competition for VC funds vanishes”

And so they’re not literally underperforming the risk-free rate of return…

I hold some equity in a once-successful startup. I was on the ground floor and exercised options for pretty cheap (but not nothing). In 2021 I turned down an offer for almost a million bucks for it because the paper value was higher.

Today it is worth considerably less and basically unmarketable, although at least the company is still there. “Waiting for miracles” is exactly the right phrase to describe the present business plan.

The unmarketability of minority positions in private companies is too little discussed and if ever better resolved, might really result in an investment Renaissance.

And marketability is better than it has ever been (online exchanges) but still pretty awful.

That said, the truth is that the ultimate problem is likely the ultimate low-to-no profitability of said private companies. Profitable ones tend to find ways for minority investors to exit.

Yup. In their last fundraising round they offered liquidity to current employees, but not to former employees holding shares. Cute.

People (investors/startup employees) tend to underestimate just how abusively/discriminatorily they can be treated by privately held companies (almost everything is contractually defined in the enormously long investment documents – which few read – and each situation is unique…although usually to the marked advantage of core insiders).

I’m no fan of the G, but at least they provide a standardized set of legal treatment for public company shareholders, which in and of itself promotes marketability of shares.

What went wrong with the company?

B2B service provider; their business was highly dependent on the continued rapid expansion of the tech industry. Now that the tech industry is in no-growth mode, it’s a hard time for companies like that.

On the plus side they do have SOME recurring revenue, and they are sitting on a pretty decent cash hoard, having raised money at peak valuation and then laid a lot of folks off. Since I have no other options, I will keep waiting and hope the horse learns to talk…

The SPAC mania was an epic regulatory and market failure.

Next crop of startups will need to show some minor improvements over the last crop / things such as revenue, profitability, careful financial management, and organic growth not fueled by incineration of investors’ cash…

Hi Wolf. Any thoughts on PE? Seeing a lot of headlines on how it is bloated and will lead to a crash or financial crisis.

Thanks.

Similar dynamics at work. But PE is highly leveraged at multiple levels, so the issue there is broader and more complicated, and there is risk of contagion to the banks. The Fed has been exhorting banks to be careful.

PE has been funding distributions by borrowing against its portfolio companies when it can’t sell them, which puts another layer of risk on top of it.

But the vast majority of the exposure isn’t to banks, but to investors, so if it blows up, the biggest losses will be absorbed by institutional investors, not the banks. In terms of banks’ exposure, it doesn’t have the magnitude to trigger a financial crisis. Banks may have some losses, but they’re equipped to take some losses.

Why are SPACs legal? It’s clear they scammed retail investors? How is it different than MBS fraud of 2006-08 where poor securities were rated AAA?

Why do the people and Govt still don’t regulate SPAC?

I probably lost some amount of money here through Index Funds.

I want to invest in something more meaningful than large/mega cap but I’m also not an active investor.

It’s not even about returns, I want to support the small/mid cap American companies.

But the whole SPAC fiasco has turned me sour on most stock investing, minus a couple of companies I see their products in the open.

I hate how unequal the stock market itself has become.

I’m surprised it’s not a cultural meme where the bottom half of the market has only X% of total cap.

Wolf, I am putting several of your articles together. It would seem that with inflation still as high as it is and the jobs report as strong as it is, the Fed would be advised to delay any additional rate cuts. In addition to this putting pressure on VCs it would seem that this isn’t going to be great for the Florida real estate market either. But both of those have done very well in the recent past and should have planned on this as a possibility.

While I am enjoying the dramatic increases in the stock market, I would be stupid to believe that there will never be another bear market and assume that 35% of my portfolio would be temporarily, hopefully, wiped out. The way to prevent or correct a bubble is to have these shocks from time to time. The fittest will survive. When I was searching for VC money decades ago I kept hearing that their clients assumed that they would lose all their money. We’ll see how they react it that comes to pass.

But I am having trouble feeling for these people when they are trying to get one candidate for President to make their earnings tax-free. And I’m sure all the portfolio managers will cut their fees because they will no longer have to pay taxes. LOL

“No taxes on ‘overtime’!” So, the VC and PE managers will have one hour work weeks and the rest will be overtime.

Yet another hand off to the ultra-wealthy, while the knuckleheads get a pittance tax cut.

“The way to prevent or correct a bubble is to have these shocks from time to time.”

The Fed has gone from “taking the equities punchbowl away” to spiking it with LSD.

(Paid for by spiking housing rents 40%).

The old saying is nobody sells a great successful business, earning good coin. Hence I believe investors don’t want to pay full price + for these VC offerings. Caution must prevail with markets at al time highs.

This is one of the funniest lines Wolf has written…funny because it is unfortunately true:

“Now the Fed has cut by 50 basis points and everyone is clamoring for more cuts to make sure that T-bill yields of 5% are wiped off the face of the earth…”

That was my favorite sentence of the whole article.

IMO it’s pretty embarrassing that these fund managers couldn’t even outperform the risk-free rate of the last couple years.

SPACs need to die no cap they rizzling investors but are so ohio up to no good skibidi

Holy shit. I didn’t know my daughter reads wolfstreet. Hey, honey how was school today?

Excuse me while I consult the Urban Dictionary…

DM: Walgreens announces massive closures as retail apocalypse hammers business

Walgreens said on Tuesday it would shut 1,200 stores over the next three years as new CEO Tim Wentworth plots a turnaround at the struggling pharmacy chain.

It’s heartening to think that retail investors might be getting a clue about how this all works, even if just temporarily.

Wolf you are deleting my posts!!! I am trying to educate other investors!

Buy NVDA this is a DISCOUNT today!!!!!

You’ve trolling the comments every single day with your NVDA promo BS. For amusement’s sake, I have allowed some of them and have trashed the others. You’re just too cheap to pay for an ad. If you want to place an ad for NVDA on Wolf Street, contact me via email. I will make you a good deal, I will sell you a creampuff ad slot that was never driven up the hill or in the rain, for 70% off LOL

In terms of the discount, I think you can buy NVDA for an even bigger discount in the future. So why rush? When these things go on sale, 70% off is much more appealing than today’s 5% off, if you still want it then. I mean, can you imagine Walmart running a holiday sale with their big-screen TV 5% off? No one would show up. But 70% off would bring in some buyers.

Buy wholewheat and lots of veggies today!

My TLT puts have a much higher return potential than NVDA. You should sell your NVDA shares and start shorting bonds if you want to make some real money.

/sarc, and also NOT INVESTMENT ADVICE

Will be interesting how AI pans out. It literally is used in most every product now, not unlike probiotic this and probiotic that. Feels like the cycle will be quick this time around or somebody will put a catchy adjective in front of it and keep it rolling. I have almost filtered it out as completely meaningless which is unfortunate but too much work to separate the real use from the abuse of it.

“…NOW! As seen on TV! PROBIOTIC AI available to the public! (…and, get twice as much’, just pay an additional fee…)…”.

may we all find a better day (hopefully, without the ‘additional fee’…)

That is FN 4 B year abiogenesis you are talking there dustoff!!!!!!!…..

Out of a box of nothing but really speedy electronic on/off switches?

Maybe even of smartphone size?

Maybe should save that for AI to accomplish LATER ON? Gotta string these memes out, ya know?

Hey. Ya know that 10+ year no soap/shower experiment I’m running? (based on skin “acid mantle”?)

Anyway, if you have TV, there is this Doc lady hustling all these creams to stop you from stinking for 72hrs or whatever, and without showering!….and for several months now……and she FINALLY said it “lowers pH”!

Hope she loses her ass…Docs make plenty just being DOCS…think median or avg pay is twice as much here as in the next closest country.

Of course the managers are screwing them like every other biz….economy of scale and much more attention to how the beans move things around……time/motion studies and all that inhuman horseshit.

Hey. Have seen it and think I mebbe need to cut a deal with her before she goes broke so she can offer a packet of free probioAI(tm) with every purchase. Or not. (I frequently wonder at the myriad long-term effects of sleep-pattern changes on our species and the spacecraft in the wake of expanding world trade/colonization/Industrial Revolution over the centuries in rough analog…best).

may we all find a better day.

What challenges are venture capital firms facing when trying to exit investments in the current financial climate?

TU – …a human-caused changing financial climate? (…sorry, couldn’t resist…).

may we all find a better day.

I just want to make sure I have my definitions straight. It sounds like “Retail Investors” are any non-professional investors, such as individuals trading through brokerages.

Institutional investors would be everyone else? The mutual fund, hedge fund, pension fund managers and the folks investing the float at insurance companies.

Would it be correct to say institutional investors are anyone that gets paid to manage the portfolio?

“Would it be correct to say institutional investors are anyone that gets paid to manage the portfolio?”

That’s too broad. A financial advisor that manages your portfolio is not an institutional investor.

Institutional investors are pension funds, insurers, mutual funds, REITs, PE firms, VC firms, banks, etc.

My follow up comment is that I am surprised that there is enough retail money around to absorb $120B+ in SPACs in 2021. Maybe there are more big retail investors than I think?

LOL, who do you think holds directly or indirectly the $50+ trillion in stocks? Martians?

Households = retail investors, and they hold over $40 trillion in stocks and stock funds, plus they are sitting on about $7 trillion in CDs and money market funds, plus they’re sitting on trillions of dollars of bonds and Treasury securities, plus….

$120 billion is a flyspeck for households = retail investors.

Wouldn’t the “stock funds” fall under “mutual funds” or ETFs and be counted as institutional money?

I would guess that the mutual fund market is a noticeable chunk of the $40T since lots of folks make it the default 401k choice?