Fed is seen as deprioritizing inflation fight, while a tsunami of supply heads for markets.

By Wolf Richter for WOLF STREET.

At the auction today, on the eve of the release of the CPI inflation data that may “surprise” markets with a further acceleration of inflation, the US Treasury Department sold $39 billion in 10-year Treasury notes, maturing on August 15, 2034, at a yield of 4.066%, substantially higher than the yield at the last 10-year Treasury auction on September 11 of 3.648%.

There was plenty of demand at the auction, given the juicy yield – yield solves demand problems, that’s what yield is for – including from foreign investors. The total amount bid was $97.3 billion.

Indirect bidders, which include foreign bidders, bid $34.6 billion, and were awarded $30.2 billion, or 77.6% of the total, the second-highest share ever, behind February 2023.

Primary dealers, bidding for their own house accounts, were awarded 13.9%, or $5.4 billion. Direct bidders were awarded $3.3 billion. And the New York Fed (SOMA) got $535 million to replace maturing securities that were in excess of the $25-billion a month cap of the Fed’s Treasury QT roll-off.

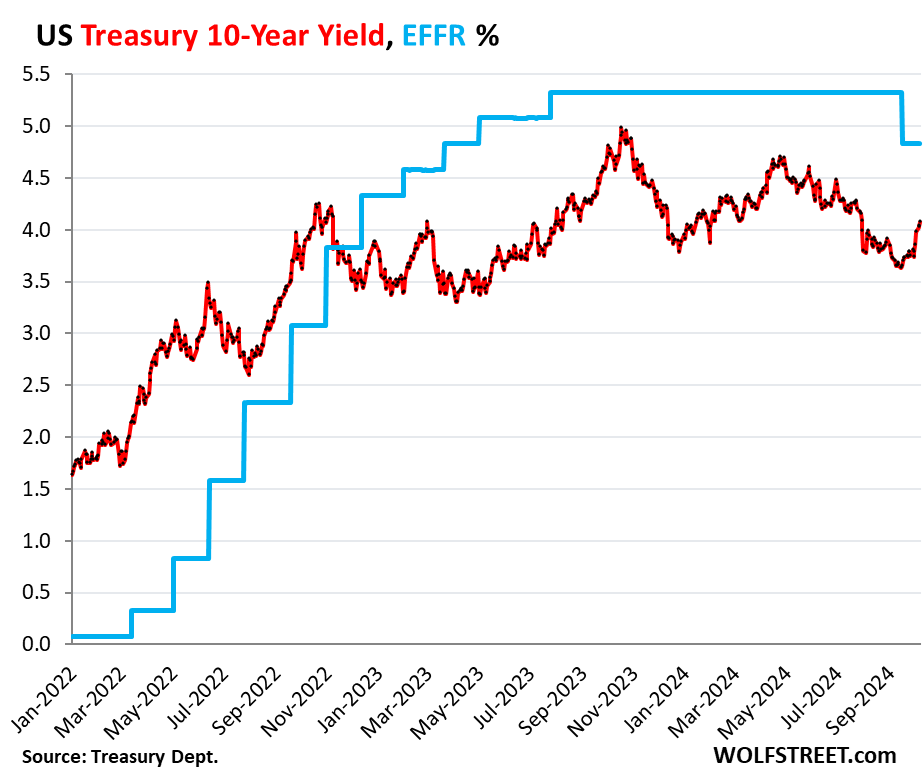

In the market, the 10-year yield jumped to 4.08% at the moment, the highest since July 31, up by 43 basis points from the day before the Fed’s monster rate cut (3.65%), and up by 10 basis points from Friday (blue = effective federal funds rate which the Fed targets with its headline policy rate):

Today and over the past few trading days, yields for maturities of 6 months and longer rose, while yields of short maturities are pricing in rate cuts in November and December.

And in another milestone of sorts, the two-year yield jumped back over 4% today, now at 4.03%, the highest since August 9.

Longer-term yields, especially 10-year and longer, are driven by inflation fears. No one wants to end up holding a 10-year Treasury security with a yield as purchased of 3.6% when the average inflation rate over the life of the security is 4%. That’s the demand-side of it.

Longer-term yields are also driven by supply, and there will be a tsunami of supply over the next few years as Congress and the White House – whoever will end up in it – are recklessly ballooning the deficit, and thereby the issuance of new debt to fund the ballooning deficit, including 10-year Treasury notes.

This surge of the longer-term yields continues the process whereby the yield curve un-inverts step by step, but in the opposite way of what was expected: with longer-term yields rising sharply – instead of falling slowly – thereby pushing up longer-term interest rates that matter for the economy, including mortgage rates.

At the same time, as rate-cut-mania got dialed back, shorter-term yields fall more slowly.

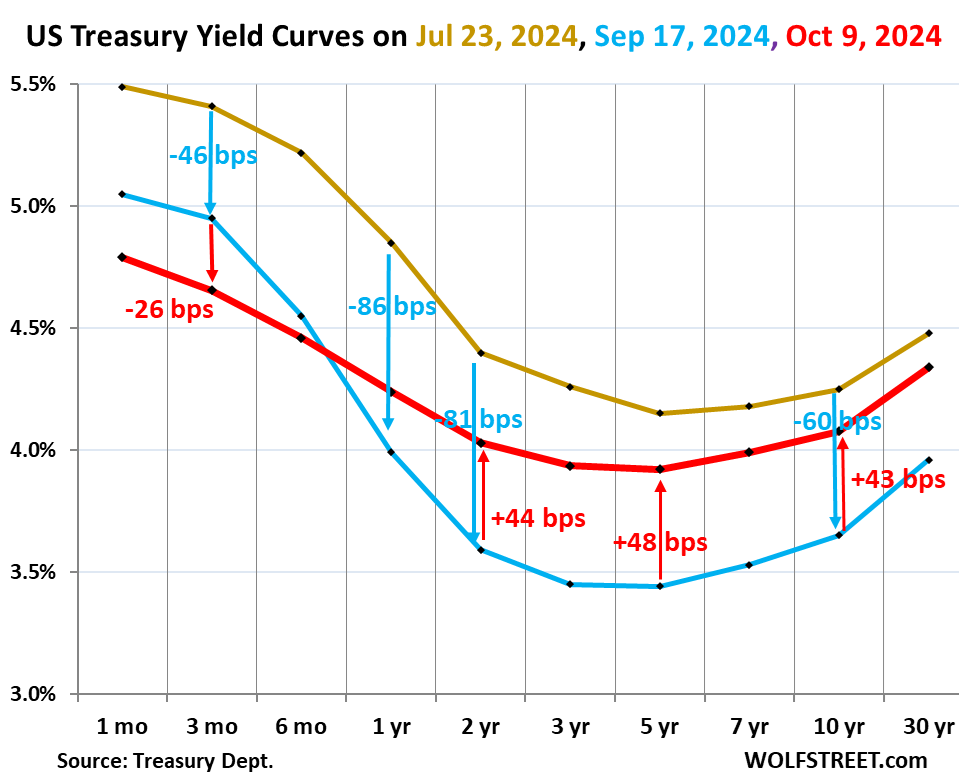

The chart below shows the “yield curve,” with Treasury yields across the maturity spectrum, from 1 month to 30 years, on three key dates:

- Gold: July 23, before the labor market data went into a tailspin.

- Blue: September 17, the day before the mega-rate cut.

- Red: today, October 9.

The 10-year yield is now just 17 bases points below where it had been on July 23, before the most recent rate-cut mania started, and the 30-year yield is just 14 basis points below July 23, a massive disappointment for those who had been counting on a flow of monster rate cuts to drive longer-term interest rates down further. So the opposite happened.

Mortgage rates had spiked on Friday and Monday by 36 basis points combined, to 6.62%, a huge move, but yesterday and today, they rested a little, and today ended at 6.61%, per the daily measure of Mortgage News Daily for the 30-year fixed rate mortgage.

The bond market is now smelling the inflation rat again. Suddenly, the perceived labor market weakness vanished, wages increased sharply, nonfarm job creation was revised up sharply, CPI inflation already accelerated, and tomorrow – that’s the worry – the next shoe might drop. And then there’s this tsunami of supply to worry about.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“The bond market is now smelling the inflation rat again”

And his initials are JP.

“Dishonest” , Lolll, you got that one right

Judas Priest?

I can still watch econ and do Soc here.

30yrs fixed mortgage rates to the rescue of the housing market…lol…poor RE agents will have a hard time now selling that narrative

30YRFM going above 8% in the not-too-distant future methinks…

They have kept records of interest rates for past 2000 years and a few averaged it all out. It’s always around 7%. I don’t know where everybody believes these interest rates need to be lower than they are. They’re not even close to what’s normal throughout history

I had seasoned realtor friend who sells 50 homes a year

jokingly asked if he could work for me

I’m booked pasted 1st year and then some

I do it the OLE FASHION WAY

C A S H F L O W

Cjmac – if you think of ‘everybody’s’ opinion of interest ‘prices’ in terms of ‘everybody’s’ opinion of gasoline prices, does that help? (…finding the cheapest money vendor, like finding the cheapest gas station is an endless quest. Crypto a misbegotten ‘EV’ attempt to avoid some of the cost of money?)…

may we all find a better day.

Will the FED have egg on their face if they pause in November with all of their recent forward guidance of cuts. Are the bond vigilantes taking control of the longer end of the curve? If so any further easing on the short end will only make the economic pain worse as longer rates continue to increase. Do the FOMC members even want to admit this…in private at least?

UK yields also up on the USA effect, although others not so sure since we recently joined the 100% + of GDP debt group.

While I think the US is over-heating economically, not the worst disaster in the world after all, unfortunately the UK is perhaps entering stagflation due to idiocy of the new chancellor who has scared everybody with money away.

As ever though, watch Japan, as soon as Japan folds on funding US debt the others won’t be far behind.

Japan is just a marionette.

Excellent article.

Wolf’s articulate.

“The bond market is now smelling the inflation rat again.”

So is the options market.

I was just looking at TLT put prices today as I’m about ready to re-enter my namesake position. Puts at a $90 strike get more and more expensive as you go out in 2025 and 2026.

Seems like options traders are also betting on higher inflation and rates on duration.

Lol, why would you re-enter now? The time to do it was a few weeks ago…

I was waiting for CPI and the bond market reaction, although you’re right the buy-in would have been better at that point.

I also made some money shorting TLT earlier in the year, but exited that position with a decent profit in May.

One of the determinants of option pricing is time to expiration. Options with more time have higher time premiums.

True, although a $90 strike is pretty far OTM.

I hadn’t actually looked at calls, but you’re right they’re fairly expensive too around $97/98 strike in the same July 2025 expiration.

Now you’re telling me this? Is one in December better than two in June?

While Schrödinger the fed cat hovers in suspended animation, dazed and confused— the inflation rat and labor rat are alive and well eating copious amounts of cheese pizza.

Unfortunately, as the deficit grows, rates stay higher for longer and the Fed cat will be perpetually frozen — and imho, whoever crawls into the white house will end up being humiliated by the deficit plumbing dynamics.

4% is a juicy yield? Maybe in clown world where every politician is trying to act like Santa Claus but in the real world that’s well below inflation.

Gold is saying the same thing. Oil is noting that a huge part of the economy has already cratered, despite assurances from government statisticians that all is well.

It’s juicy for many foreign investors. 10-year yields:

Japan: 0.95%

Germany: 2.26%

Spain: 3.01%

France:3.03%

Italy: 3.56%

But if USD weakens vs those currencies even fairly mildly then the extra yield is not going to be seen.

And there is no reason why the USA isn’t now just the last least dirty shirt to get a wash.

“Oil is noting that a huge part of the economy has already cratered”

Oil is “noting” nothing of the sort. Low natural gas prices are putting a ceiling on the price of oil, which is currently a lot more expensive on an energy-equivelent basis.

Correct. The US is the largest producer of crude oil, petroleum products, and natural gas in the world. And production has been soaring from record to record. There is a glut of these products in the US, and the US has turned into a big exporter of them. It’s the glut (supply) that pushes down the price, not demand.

Plus those exports bring in money into the US and helps make the US dollar stronger. Also it lowers manufacturing costs in the US. Specially for refining chemicals.

This is part of the reason why the economy is in a soft landing IMHO.

What is also interesting is Germany has installed so much solar and wind the past few years on sunny and windy days, spot electricity has turned negative. Crazy.

Just like NIRP for loans a few years ago, we are seeing where you can get paid to use electricity. LOL

Oil is noting Middle East concerns ( possible Straits of Hormuz being impacted by a potential growing conflict ).imho

WTI dropped to $75 today. Back in mid-2022, it was $120. Between 2010 and 2014, it was mostly between $100 and $120. Back in 2008, it was $150 briefly.

Today at $75, oil is a pretty good deal, I’d say. There are not that many things that dropped that much in price over such a long period.

oil is down because the US is producing records amount of oil. Global demand has not dropped to indicate an economic slowdown. Even as adoption of EV cars hit the road that are not using gasoline.

Same thing goes for Nat Gas. Consumption is at record highs but supply is growing even faster than consumption. Nat Gas and Coal use for electricity is at ATH peak consumption.

We could produce even MORE gas if it was allowed to be flared off during oil extraction. Most of our natty gas isn’t specifically drilled for – it’s actually a byproduct of oil extraction.

Currently, this excess gas has to be captured and transported out of the oil fields per regulation – if we increase the capacity to remove this gas, we’ll be able to extract more oil too.

We have virtually unlimited hydrocarbons in the USA for use in our lifetimes. The limitations on extraction are political, not technological or geological.

“in our lifetimes”.

Our great grandchildren will one day have great grandchildren. On some date there is no more fossil fuel. Will we be remembered as the A**hole generation then?

Louie

We will run out of clean air to breathe before we’ll run out of fossil fuels to burn. That’s what I always like to say, tongue-in-cheek, but only sorta, unfortunately. We’re contaminating everything, the air, the water, farm soils, food, you name it, we did it. But so far, so good?

Louie,

100 years from now, we will be producing and consuming more hydrocarbons than we are today.

Energy production on a graph is an upwards-sloping sine wave. It’s a cyclical market with a consistent uptrend.

A bet against future energy production is a bet against human ingenuity and progress.

I have seen estimates of “proven” hydrocarbon reserves that could last 100s of years at increasing consumption. Hundreds of billions if not a trillion plus bbls globally.

There’s a lot of “unproven” theoretical reserves in the good ol’ USA. For said political reasons it is not worthwhile to spend money to “prove,” when the known pumps and sells today.

> A bet against future energy production is a bet against human ingenuity and progress.

The problem seems to be growing as of now. I can see all sorts of atrocious consequences. These are so obvious, the flaw seems to be the ability of humans (like AI) to hallucinate when facts are right here. A bet on human-mediated solutions is a bet, too. “Human ingenuity and progress” didn’t put the known working regulatory mechanisms of nature here. To the contrary.

Had my suspicions, but now am CERTAIN, especially if really a thought out comment.

No way well informed.

Yeah. There is plenty fossil fuel, alright……enough to do whatever damage we choose…..in whatever order we choose.

Single cell critters are on the top of podium right NOW, anyway…… followed by maybe insects (on land only!…is Land a separate event? and as yet undiscovered stuff)…likely sea or deep sea. Probably ought to give virus a separate category (event) and prions are a really tough call.

Hope everybody enjoys watching a good game!!!

Water rules this ball.

Maybe should go long afterlife…..or already are?

Tell that to Alan Blinder who says that “food shocks and OPEC ii (supply shocks) deserve much more blame for the alarming rise in inflation in 1979-1980.”

Oil has fallen bringing gasoline prices down. At this juncture, there are countervailing forces working on the economy.

Good last name, I will agree there.

Don’t know the material, but seems unlikely he justified “cause”.

so….Just a guess on my part….or drunk still.

OK, enough moderation problems for Wolf. Will do my best to just read, do Soc, and shut up.

You are all welcome.

Everyone claims to know that “real” inflation is nothing close to what CPI shows.

Their ‘evidence’ is always some variation of “well geico raised my car insurance last year” or “soda pop used to be a nickel now it’s $2.50!”

Neutral real interest rates cannot stay negative or even zero forever under “normal” economic conditions. 4% 10Y Treasury or roughly 2% real long term rates don’t seem unreasonable to me in a growing but stable economy. The days of ultra low rates (nominal or real) are over. That is the real rat that the bond market smells (no pun intended)

Real Rat-

“Neutral real interest rates cannot stay negative…”

What are you expecting for inflation prints over next 5-10 years, please? Real rate estimate only as good as inflation prediction accuracy. (My crystal ball is admittedly hazy….)

What real rates are reasonable in a flat, or shrinking, economy? I would want a higher real yield in that case, not lower (yield is proportional to money at risk). Demographics is destiny, and it’s not looking too good right now.

JeffD:

Humans are antiquated accessories to productive economy. Humans are only required for menial tasks. AI is for thinking.

Once robotics catches up (by some estimates later today) we can all relax, peacefully!

/s (but not for many who believe in, anticipate and desire this reality!)

“4% 10Y Treasury or roughly 2% real long term rates don’t seem unreasonable to me”

But the 2-year is 4% right now. The 10-year should have some term premium.

Tick tock tick tock… for a long time we’ve been waiting for the other other other other shoe to drop. It’s probably time. Ironically, I was excited in my 30s… in my 40s, I’m scared.

That being said, the data in the article reflects that the markets are losing faith in the government ever reigning in spending. Which is so hilarious.

That’s normal. Mid 50s you relax again. 40s are still super productive growth. BUT, in creeps the realization you’re not immortal.

By mid 50s you’re comfortable being 2/3 dead and things don’t seem so important. At least that’s my experience.

60s, no idea yet.

Tomorrow will be interesting. I’m expecting a low CPI reading. That said, I expect a pretty big jump in the report after this one.

Or perhaps and upward revision will happen to the Aug and Sept numbers after the election.

Not a conspiracy theorist, but also would not be surprised

In my opinion, the bond market didn’t smell a rat – it smelled both a rotten corpse (the US dollar) and donkey dung (negative real rates of return due to inflation). The bond buyers are saying “if you want us to loan you money, you’re going to have to pay more. We’re done being suckers. The free meals are no more. Think you’re driving the bus, Jerome? Think again!”

No sure I agree, as the average Joe/Jane isn’t really a large player. I mean come on, does anyone really believe the last 15 years of interest rates has accurately reflected/priced risk and inflation?

Nobody believes that. As soon as it was clear that the Fed was going to use monetary policy to enforce financial repression, everyone with half a brain went long equities.

Question: With China trying to stimulate their own economy now and increase their domestic consumption, is it possible this will end up reversing the deflation in goods? I know Wolf doesn’t cover China but I don’t really have any good sources to read up on it so maybe my question is dumb

Go listen to Apple podcast MicDropsMarkets hosted by Tracy Shuchart. Listen to podcat #38. She pulls in an expert on China and discusses China Macro and latest Stimulus. Worth the listen.

Thanks! I’ll look for this

I have a good source. Girlfriend just went to China to visit and friends were asking her to buy/bring miscellaneous items (purses from Macy’s, shoes from Zappos). Get this, all this stuff made in China costs more in China. Apparently people routinely buy things from Costco to bring to China when traveling. I always just assumed it was only us who needed all this cr*p. So yeah, reversing.

…price-gouging in the PRC? Dumping here? Both? Neither?…

may we all find a better day.

FED said labor Market is cooling and proactive approach for further deterioration as reason for 50BP. They said both risks are balanced now and shown bias towards labor market deterioration.

Off-course they wont accept any haste or mistake on their part. Labor Sept data and revisions for earlier months have clearly shown they are wrong again. Even after new labor report, Collins, Kugler Goosbee and few others are signalling more cuts are coming.

In name of credibility, will FED will go ahead with 25BP rate cut in Nov?

I think they will.

What they SHOULD do is different than What they will do. ITs only few weeks away.

Now that they were shown to be wrong on labor, and that CPI is coming in hot, they should be coming on saying “We made a mistake, and we are going to reverse our 50 bps cut on an emergency basis.” But of course, they won’t. Their main priority is keeping asset prices high.

The Fed doesn’t operate in a vacuum.

They are under political pressure to

cut rates . Once the election is over

they will take corrective steps but

undoing the damage will take time.

The Fed’s job isn’t to give politicians what they want.

“The Fed’s job isn’t to give politicians what they want.”

only in theory. They did it before they can do it again.

“The Fed’s job isn’t to give politicians what they want.”

Correct, it is to give corporations what they want, which is also what the politicians want.

If the US long term bond rate exceeds the US GDP growth rate,

which it does,

there is no way way the US government can grow its way out of the debt problem.

Higher US inflation, here we come.

The logic is not correct because the base is different. 4% of the debt (a level) is a different amount than 4% of the entire US economy (GDP = a flow = roughly GNI = Gross National Income, which is generated all the time).

So what you have to figure is how much more tax receipts 4% GDP growth will generated to pay the additional interest. We cover that actually here:

https://wolfstreet.com/2024/08/29/spiking-interest-payments-on-the-ballooning-us-government-debt-v-tax-receipts-gdp-and-inflation-q2-update/

Next stop 60 trillion debt. Let’s do it!

Well, as long as you have demography on your side and the population is growing and immigrants are getting in US, there is nothing to worry about. The US can go a long way …

as long as lower and middle-class folks are losing new job openings to illegals who will work for scraps and no benefits, americans are doing better off! yeah!

Did I miss the sarc symbol on this? Debt payments just surpassed both social security and national defense in size and Yellen foolishly has been funding the deficit with T bills during a time when long duration treasury bonds could have been utilized at the lowest rates in human history (2020 to 2022 that is). The chickens are coming home to roost on this unprecedented peacetime deficit spending, rates are going to be higher permanently.

Yes, tax receipts will rise and fall with the rise and fall of economic activity. Property taxes are another matter. Local municipalities cannot afford to have home prices correct.

With regard to the Yellen comment below, it still amazes me that the interest rate on the short end (4 and 8 week T-bills) is coming down at all with the treasury increasing supply as much as they are.

“With regard to the Yellen comment below, it still amazes me that the interest rate on the short end (4 and 8 week T-bills) is coming down at all with the treasury increasing supply as much as they are.”

4 week has started to rise again.

Local municipalities can afford to have home prices correct, but they won’t like it. Rapidly rising home prices let them raise more money with constant, or even lower, rates. Property owners squawk, but their ire is directed at the appraisal district, not the city or county officials.

When house prices drop, this process reverses. Local governments are forced to raise the rates, which are immediately attacked as “tax increases” followed by “throw the bums out” at the next election.

The total dollars involved might even stay the same, but the political dynamics change a lot.

@David in Texas,

That’s not how it works in California. Property tax increases are capped at 2% annually, period.

That tax receipts chart is interesting.

Pretty flat/range-bound 2015 through 2019.

Then $200 – $250 billion surge (say 40% up) during pandemic era (with volatility, but still $200 billion up thru today).

I think a closer examination of timeline and breakdown of inputs into this reported surge would be interesting.

The first instinct call is to say that money printing-for-three-stimulus-pandemic-packages is behind it.

But as with pandemic spending in general, wasn’t the primary point income *replacement* (during pandemic lockdown) rather than (somehow) income growth?

If people weren’t being paid by their employer (due to lockdown) and instead being (partially) paid by the government, how did GDP/tax revenue/etc *surge*?

Perhaps it is a timing matter (chart resolution is a little too low for that) but it does seem odd.

Tax receipts rose because:

1. rising incomes from work (more people working, each making more money, including through wage inflation)

2. massive capital gains tax receipts on the HUGE spike in asset prices. The latter is a result of money printing.

During the pandemic, the actual unemployment spike was very short — you can see that in Q2 2020 when tax receipts plunged — and then turned into a labor shortage with spiking wages that lasted years.

Wolf,

1) Well, as I mentioned, a zoom-in to that 2020-current time period would be useful vis a vis the timing of the printing/stimulus packages. Again, if much/most of the G stimulus was *replacing* income halted by the pandemic (no work salaries due to lockdown) then it is hard to see where a 2020-2021 *surge* in tax revenue would be coming from. Maybe a surge in 2022/3-current but that’s what a zoom-in might reveal. You mention this.

2) a) I’ll buy a surge in capital gains taxes due to stimulus asset bubble – although taxes only occur when *sales* occur and sales create *downward* price pressure, even during a bubble. Sure, theoretically things could *still* net out to a bubble asset price hike.

2) b) At least in SFH asset mkt, actual sales (AKA capital gains realization events) have fallen off a cliff since March 2022 (35% down). Again the asset bubble *price hikes* might have offset (and then some) the *volume cratering* but…

In any event, the dynamics illustrate why “It is Good to be The King” (hat tip History of the World, Part I).

On the one hand,

1) The G prints money, allocating the incrementally unbacked fiat to its designated spending agenda (good, bad, or otherwise),

2) This printing spikes asset prices and salaries…which then also get taxed by the G, spiking tax revenues.

By having near-complete control of the printing and taxing policy levers/flywheels, the G appears to always come out ahead (although I don’t discount the fact that multi-decade abuse of this position can, in the end, cause the G’s wheels to fly off).

In any event, the result is a much more centrally managed economy than is almost always portrayed.

3) This “heads-I-win, tails-you-lose” dynamic also illustrates why the G has a very significant bias towards inflation (consumer and saver interests be damned) – the Fed’s inflation/taxation flywheel only works with significant inflation occurring.

Cas127,

The stimulus didn’t replace income. That’s what should have happened. Instead, folks working from home, with no commute to pay for, received checks. Businesses without pandemic impacts to their operations, received PPP money.

What items could surprise leading to a hot print? Vehicles &? How will stocks react if there’s a hot print? My guess would be unfavorably.

“Vehicles &? ”

Yes, durable goods jumped, a reversal from a series of drops.

Yes. “higher for longer”! Like Milton, the second wave of inflation is coming ashore!

The composition of N-gDp will probably end up with inflation increasing faster than the real output of goods and services. It’s called stagflation.

The government has finally figured out how to live with increasing interest rates while borrowing more money. As described in the FY2025 budget, just tax the interest paid at a capital gains rate of 46%+. whether gains are realized or not.

Since the US government is only one of the 2 countries that taxes citizens income regardless of where earned, it is not much of a stretch given the current sanctions mania for the government to tax US treasuries regardless of who owns them.

Doesn’t matter what the interest rate is if the Fed has to give it all back and the “investors” have to give half back – cuts the effective rate down by more than 50%.

Super easy, barely an inconvenience.

Perhaps why gold is being bid. “Super easy” why to destroy confidence for sure.

Hedge accordingly.

Yeah. My point was that interest rates in a vacuum are meaningless. You have to evaluate WRT inflation, taxes, and alternate use of capital. And the real clincher – actual probability of the return of principle and the utility of said returned principle .

All these roll up into expectation value.

BTW, the proposed 2025 tax code seems to want to elevate labor over capital. Where have I heard that before – we pretend to work and they pretend to pay us. Reality is always a novel eye opener to the theoretical cadre. At Sloan School one of my finals was graded as Street Fighter.

Regarding inflation, while the recent/current (not to mention long ZIRP era) interest rate changes by the Fed are important/key, now may be a good time to recap the extremely large pandemic era incremental spending bills…

1) CARES Act ($2.2 trillion in March 2020)

2) American Rescue Plan ($1.9 trillion in March 2021)

3) Inflation Reduction Act ($900 billion in August 2022)

For 1 and 2, a decent case can be made that a lot of panic, opportunism, and carelessness played a role. A lot of evidence of rather massive fraud has emerged, at least partially due to an eagerness simply to shovel money out the DC door with few to no safeguards. As with the CDC, DC proper had decades and decades to pre-plan for national emergencies and yet seemed to lack much of a well-thought out economic stabilization plan at all.

For 3, the case for simple political opportunism becomes stronger due to the 29 month lag since the start of the pandemic and the project specific nature of the spending.

Another crucial point is that while spending *authorization* can occur in an instant, actual allocations and disbursements occur over time. That means that there is always *some* time for safeguards/tripwires for spending pauses/reversals to be built in.

If DC had any desire whatsoever to do so.

There is little evidence to that effect.

I agree on 1), and disagree strongly on 2). By March of 2021, it was clear that vaccines were being rolled out and the economy was bouncing back. There was zero reason to pass that outside of political vote buying.

Yeah, the rate-of-change in money flows, the volume and velocity of money, hit all-time highs in November 2020.

Fair amount of LTCG harvesting being done in long bonds given were basically 365 days from the 23 peak in the 10-year. 125bps from peak to trough in the yields over that time.

Core CPI hotter than expected at 3.3%, bond and mortgage rates should continue to rise.

With respect to CPI, my back-of-the-envelope calculations have us repeating 1977-1985…

…of course the CPI was calculated a bit different back then, but that were I see us. Nothing new under the sun people, hedge accordingly.

No, we won’t repeat 77-85. But that doesn’t mean rates won’t stay high.

Velocity increased during the Great Inflation because of the “monetization of time deposits”, the decline in “gated” deposits.

The process of monetizing time (savings) deposits began in the early 1960’s. The sharp increase in DFI DD velocity since 1964 was the consequence of a variety of factors which include:

1) the daily compounding of interest on savings accounts in commercial banks and “thrift” institutions (S&Ls, CUs, and MSBs),

2) the increasing use of electronics to transfer funds

3) the introduction of “negotiable” commercial bank certificates of deposits, and

4) the rapid growth of ATS (automatic transfers of savings to DDs) and NOW (negotiable orders of withdrawal) accounts, and MMDA (money market deposit accounts)

…all which enabled people to economize on demand deposits (exploit opportunity costs), and resulted in the sharp increase in DD Vt.

LOL! Rates are not “high”. My first auto loan was 15%, my first home loan was 8%.

I’ve never had a mortgage under 6%.

Tick Tock….didn’t dive too deep into it but looks like CPI data is reading hotter than expected, if that’s truly the case beyond the headline, then add that shoe to another that dropped and if Pow Pow still decide to cut by next meeting, then we know where his head is at…..

So far the market is just barely down, still a long day to go but the reaction right now is more of a meh…

That’s always how it is. The media says that the market “rallied based on fill in the blank factor,” and when that factor comes away, it never reverses the rally.

This is an everything bubble, plain and simple.

For sure, wait until the Robotaxi event today….I am sure TSLA will get a nice 10% by tomorrow.

Bubblicious only needs rumors and hopium to feed…

To be honest. I did not think the FED could get CPI down to 2.4% even though this is a hotter than expected. If you would have asked me that 2 years ago I would have said no way.

Markets are being continually reassured: Don’t worry about inflation.

The headlines tell us this is the “lowest inflation reading since 2021,” because they only look at the headline number and there’s no 3, 4 or 5 in front of it!

It looks like Powell pays more attention to the employment numbers as opposed to the inflation rate.

JPow overplayed his hand last month with a 50 basis point cut. Two consecutive 25 point cuts would have been a smarter strategy—or at least one with less risk. Now he might have to come empty handed to the next meeting. I don’t think he’s necessarily a very quick-witted guy—certainly no Larry Summers, baggage notwithstanding.

Wolf, not sure if you know the answer, but I am curious as to how many times the Fed has begun a rate-cutting cycle with the markets and gold at an all time high? Is this unprecedented?

But in the past, the Fed didn’t succeed in bringing this much inflation down so far without pushing the economy into a recession. Inflation came down a whole lot despite a strong economy and lots of demand. So the Fed cut its policy rate to narrow the spread between its policy rate to inflation rates. These are both unique factors.

If inflation rises again, it can hike rates again. Rate cuts are not permanent.

Sure, of course the Fed has also never printed so much (balance sheet still over 7 trillion) nor have they had so many “emergency measures” REPOS and bank lending etc.

Future rate hikes with 36 trillion in debt? LOL, okay.

Did you happen to catch that Dimon interview? they cut to commercial right after Jamie said that rates should be 7-8% for 1-2 years.

What I’m getting a slight whiff of, is owners’ equivalent rent rising as a reaction to higher mortgage rates, pushed far higher by long treasuries — so the embers of contained, cooling inflation, are re-igniting by the Fed loosening conditions — and the deficit increasing which spills into more treasury issuance that ends up requiring higher yields.

Plus of course a wide assortment of revised data coming in early 2025, including CPI and unemployment — not exactly the right environment for soft landing.

OER probably is more affected by spiking insurance costs and maintenance costs, than interest. All homeowners have to deal with insurance and maintenance, and it spreads across the survey population very quickly. Interest only affects those that recently bought.

I have a PhD in economics. Actually, I don’t, but I DO a know this – the ‘agency’ isn’t supposed to have diddly squat to do/say with the interest rate. The interest rate is supposed to be set by the bond market (the free market). When the ‘agency’ sets the interest rate, that is price fixing. ‘Foul, player offside!’ The interest rate is the price of money. So, the clowns are artificially fixing the price of money. If they (the clowns) would stop price fixing, the interest rate would likely be 8% or more. Soon, the clowns may be unemployed, or in the insane asylum. Buckle up!

“‘Foul, player offside!’”

LOL, no, they’re following the rules of the game that have been set forth by Congress since 1913.

You just don’t like the rules of the game. And you don’t like the game itself. And you want a different game. But that’s the game we have.

Another reason for the rise in gold. People/central banks forgoing long term treasuries in favor of gold (not playing the game).

A shift to return OF capital over any return ON capital…

Interesting times.

“People/central banks forgoing long term treasuries in favor of gold.”

The increadibly strong demand at today’s 30Y auction begs to differ.

One auction does not a market make…

There is a new trend and the past performance is not a guarantee of future returns…

LOL. Great line Wolf.

Farek – There are many countries who wish they had the same game as the FED. LOL

Look at China. Stock market has been flat for 12 to 14 years. Mexico is the same price as 10 years ago. Brazil stock market is down 30% over the past 10 years. German DAX is only up 15%. The list goes on an on. You can say the same for many other global economies. I have a feeling they are all envious of the FED? The SP500 is almost up 300% over 10 years.

No other country is close and people are always complaining?

It is good if you owned real estate and stocks. If one does not, they missed out on a lot of wealth creation.

Well that’s just great, but 10 years ago I was in high school. When was I supposed to “get in” on this “wealth creation?” Was wealth actually created, or was it just currency debasement?

Most assets in America are held by the rich. So what you’re saying is that it is good if you’re rich, and if not, well, sucks to be you. Do you think that’s a recipe for future societal success?

As witnessed the Chinese housing ponzi in China finally came to an end. As for the U.S. stock market take a good guess where all the money will flow to when the stock market ponzi finally implodes. Well after all the margin calls.

Steve B:

Yes, only you misspelled “feudal” societal success.

You’re welcome.

I think it shows that at least currently, China doesnt see real value in bubble stock prices but instead in producing a wide variety goods that sell. Stock gains “wealth” arent realized until you sell. One shouldnt envy another even if they do good, but envying bad money printing is crazy.

Steve B/TS – all that, and then you’re asked (ordered) to soldier to protect it…

may we all find a better day.

I am reminded of a time where the Fed called upon Congress to pick up the stimulative ball, because they were tired after all their running with it. Classic case of be careful what you wish for.

1970s stagflation is my base case,. I have been saying this for years.

Rising rents will support house values in job rich locations … if you can’t buy, you rent. Even if sales remain slow, in job rich locatiions, prices will slowly grind higher, because of rising rents.

In areas void of jobs, house prices will sag. Those people will lose money.

Why? Renters will only rent in locations close to work.

This is old school thinking. Remote work has flipped the script.

LOL!!!

Well, then so much for any “manufacturing renaissance”!!! Hilarious. If I don’t see an employee often enough, they don’t last long. The true minimum wage is still zero. That hasn’t changed.

Manufacturing is only 11% or so of total employment. New highly automated plants have relatively few employees, and most of them are highly trained workers, tech workers, and people with advanced degrees. But the service jobs it takes to build manufacturing plants, design the equipment and software that make them work, design the products to be manufactured, sell the products to be manufactured, etc. those are big important jobs that are NOT in manufacturing, and many of those jobs can be on a hybrid basis.

Manufacturing is hugely important, not because of the relatively few direct employees a plant has, but because of all the work related to manufacturing.

What’s the ratio of remote workers to those of us who have to bring our physical selves to a physical location to get something done? That would be the number which determines if the “script” actually has been “flipped” 😆. While I do know some people who work from home it’s not a large number in my circle, but my circle is very limited relative to the whole of the economy so I can’t judge it on that.

and the 30yr — today went for +39 bps yielding about 4.39%.

Chance to buy more before inflation gets to 2% in another few years.

The 30y was trading around 4.404 right before the auction, which stopped thru by 1.5bps to 4.389.

Very strong demand at these yields.

The Bank of Canada was buying up treasury bonds today especially the 5 year treasury bond to drive down 5 year mortgage rates.

No, it’s not “buying up treasury bonds” or anything else. It’s engaging in repo operations, and has been for a long time.

Looking forward to Wolf’s coverage on latest CPI readings….but according to MSM, we got greenlight to party and next round of rate cuts…party on Garth!

”

MONEYWATCH

U.S. inflation continued to cool in September, latest CPI data shows “

Core CPI accelerated for the 3rd month in a row and hit 3.3%. But gasoline costs plunged.

https://wolfstreet.com/2024/10/10/beneath-the-skin-of-cpi-inflation-core-cpi-accelerates-for-3rd-month-on-sharp-flip-of-used-vehicle-prices-amid-sticky-services-inflation-gasoline-plunged/

Core CPI is the one they care about the most, no? So let’s wait and see if they still insist on cutting the next meeting, then perhaps they have some explaining or spinning to do…or maybe they miss the title of most wreckless FED ever and want it back?

Bostic said today he’s open to a pause in November, suddenly.

The FED should drop policy rates further and at the same time increase QT.

Hi Wolf, We were due the September Treasury monthly budget statement on Thursday – the day of the 30 year bond auction. None published. Is this coincidence or has Janet gone AWOL with the credit card again this month and they are holding the figures back whilst the market digests the auction?

– Mr. Market tells me right now that the FED will cut rates by – at least – 25 basispoints and perhaps even 50 basispoints in the next meeting.

– That same Mr. Market also tells me that it’s likely that the FED will cut rates even more after that, to 4%. When ? Mr. Market will tell me in advance.

– There is absolutely no need to listen to what the FED is jawboning. Mr. Market still reigns supreme.

The Fed tells Mr. Market publicly what it will do, and we discuss this here because it’s all public, and then Mr. Market prices all this in, but gradually over time, usually incorrectly until it gets closer to the meeting, and then it nails it, and then Mr. Market gets on the phone and tells you. If you wait for your phone call from Mr. Market, you’re the last to know.