Subprime, which means “bad credit” and not “low income,” is always in trouble. But it’s only 14% of auto loans. Prime is in pristine condition.

By Wolf Richter for WOLF STREET.

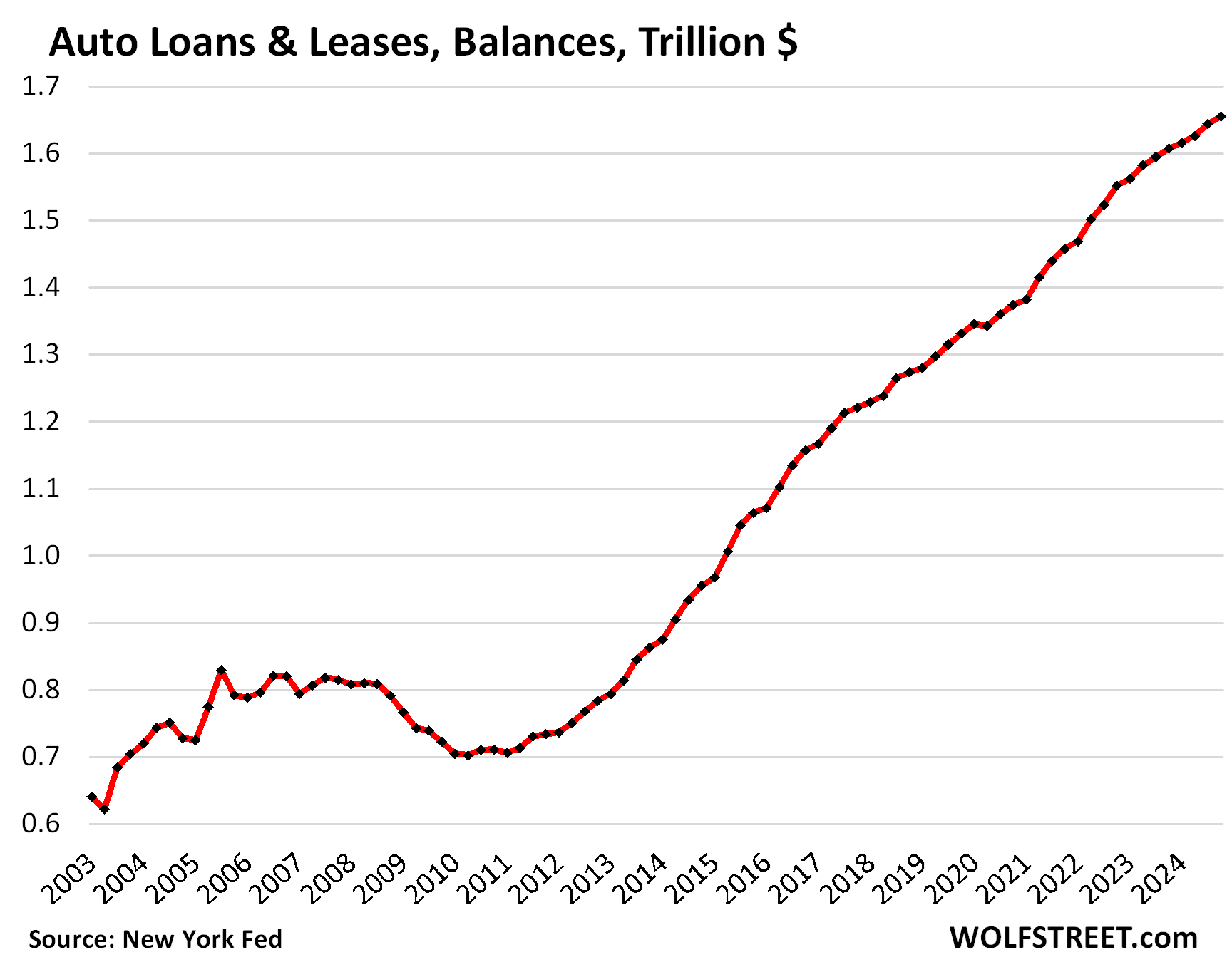

Total balances of auto loans and leases for new and used vehicles inched up by 0.7%, or by $11 billion, in Q4 from Q3, and by 3.0% or by $48 billion, to $1.66 trillion, according to data from the New York Fed, which is based on Equifax credit report data. This relatively modest increase occurred even as the population, employment, and incomes grew, causing disposable household income to grow by 1.3% in Q4, and by 5.1% year-over-year, far faster than auto loans and leases, and so the auto-loan-to-income ratio dipped further.

Of all loans and leases outstanding, only 14.0% were subprime rated, according to Experian data. Of the newly originated loans, 16% were subprime rated, which is historically low, and down from 22.8% in 2019.

One of the reasons the growth of auto loans was relatively modest in 2024, despite rising new and used vehicle unit sales, was that more people paid cash for their vehicles, given the higher interest rates.

For new vehicles, the share of cash purchases rose to 20% in recent quarters, from 18% in Q1 2022. It’s in new vehicles that subsidized leases and rate-buydowns entice buyers to finance though they might otherwise pay cash for the vehicle. For used vehicles, the share of cash purchases rose to 65%, from 59% in Q1 2022, per Experian data.

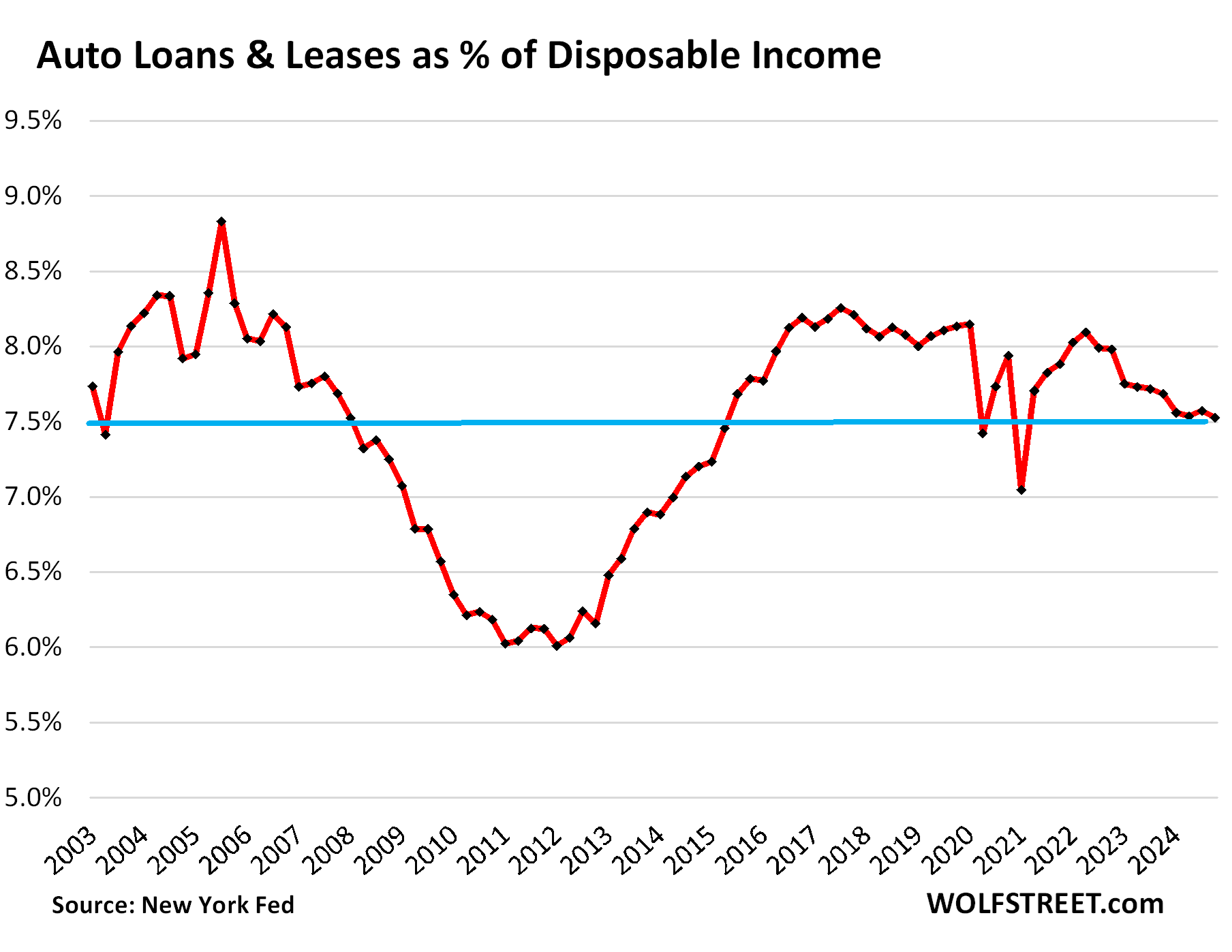

The burden of auto loans and leases: Debt-to-income ratio.

The burden of these auto loans and leases on households – accounting for more people, higher employment, and higher incomes – can be tracked with the auto-loan-to-disposable-income ratio.

Debt-to-income ratios are a classic measure of the borrowers’ creditworthiness, their ability to deal with the burden of debt.

We use disposable income (by the Bureau of Economic Analysis) because it represents an after-payroll-tax cashflow from all income sources but excludes capital gains: Household income from after-tax wages, plus income from interest, dividends, rentals, farm income, small business income, transfer payments from the government, etc. This is the cash consumers have available every month to spend on housing, food, debt payments, etc.

- In Q4 from Q3: auto-loan balances +0.7%, disposable income +1.3%.

- Year-over-year: auto-loan balances +3.0%, disposable income +5.1%.

As disposable income grew faster than balances of auto loans and leases, the burden of the auto debt on households, in terms of the debt-to-income ratio, dipped to 7.53%, and has been in the same relatively low range all year.

Our Drunken Sailors, as we have come to call them lovingly and facetiously, have switched to just an occasional drink?

Serious delinquency rates: total, subprime, and prime.

The 60-plus day delinquency rate for all auto loans and leases inched up to 1.58% in December 2024, not seasonally adjusted, up just a hair from December 2023, per Equifax data. The highs in 2024 had been in January (1.59%) and February (1.61%). During the Free-Money era of the pandemic, delinquency rates had dropped below 1% (red in the chart below).

Subprime is always in trouble. Fitch, which rates asset-backed securities (ABS) backed by auto loans, splits out the delinquency rates for prime-rated auto loans (blue in the chart below) and subprime-rated auto loans (gold in the chart).

Subprime means “bad credit” at the time of origination – a history of delinquencies and unpaid bills – and not “low income.” Low-income people have trouble borrowing, and if they can get credit at all, the amounts are small. It’s people with high-enough incomes that get seriously into it over their head, often as part of a learning experience early on in their careers.

Fitch’s subprime 60-day-plus delinquency rate ticked up to 6.15% in December 2024, up from 5.94% in December 2023. These delinquency rates peak in January or February. They hit an all-time high of 6.4% in February 2024 and may end up in the same neighborhood in February 2025.

Only 16% of all auto loans originated in Q4 were subprime, most of them to finance the purchases of used vehicles, particularly older used vehicles, sold by specialized subprime dealer-lender chains, or financed by specialized subprime lenders. Lenders package these loans into ABS and sell these bonds to pension funds and other institutional investors that buy them for their higher yield. Only 14% of all outstanding loans and leases were subprime. It’s a small specialized high-risk-high-profit part of auto lending.

Prime-rated auto loans are in pristine condition, with delinquency rates hovering at 0.37% over the past few months, including December. Even during the Great Recession, the prime delinquency rate rose to only 0.9% in the worst months (blue):

In case you missed the earlier parts of the debts of our Drunken Sailors:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The delinquencies will continue to increase with the government cuts in payroll.

But they are in a very healthy range right now so unless a deep sudden recession where unemployment spikes, this is a non issue.

You think gov’t employees are typically subprime borrowers? I would guess the opposite.

Perhaps Gov’t employees will be subprime borrowers in the near future…eh?

My 50+ year old stepson is a “Subprime” guy. Has an old felony on his record, only works part time, won’t take any responsibility for his son’s future (previous wife), has no credit to speak of and is basically a loser. He bought a used VW Jetta, paid too much, and got a loan with an interest rate of ~12%.

He has had a couple of cars repo’ed over the years. I think his girlfriend, who has a real job, co signs for this jerk. Now that my wife has passed away, he is no longer on my radar (or hers).

He’s called a POS in these parts.

Glad he’s not on your radar any longer.

Being a stepson myself and a reformed loser who was once basically the guy you describe minus the kids and now has a nearly 800 credit score is if you raised this kid you have a duty to him like any other father, if you married the mom after he was 18 your right to wash your hands of him. 50 is depressing to be such a loser I figured it out by my mid 30’s but I would encourage you to open your heart and see if it’s possible to lead him to a better path if not for his own sake do it for the grandkids.

Chris, I married his Mom when I was 49 (she was 47) years old and he was 28 and in prison. We did all we could for him over the years including having him live with us for two years. We paid the down on his cars, and he couldn’t hold a job long enough for them to get to be his instead of the finance companies. He got married and within a year, divorced and left her with a newborn.

Eventually, he went to live with a girlfriend and he is where he is. My wife’s other two kids turned out fine as did my two. This kid (man) was just a bad deal and very opportunistic. His real dad had nothing to do with him from the time he went to prison.

cc: Wolf Street

Dear Chairman Powell,

Please keep interest rates at this level or raise them as you try to combat the persistent inflation you caused by ZIRP. The more interest I make, the more I can spend to stimulate the economy and pay off any debt.

Thanks,

Drunken Sailor

Except inflation is also increasing

Jon, the increase in interest I get far surpasses any increase in my costs due to inflation. Inflation affects people differently depending on their spending habits and debts. I spend more, but I don’t buy crap like jewelry or suits or expensive shoes. I have no debt except credit cards which I pay off every month. I eat well, because I do not go to restaurants. I prefer not to have a stranger cook for me, using food which I do not know where it came from, eating amongst a crowd of strangers, and paying five times more for a restaurant meal than if I bought and cooked the same food myself. But, as I said, everybody is different, and inflation affects everyone differently.

thurd2, you nailed it. Last night my wife and I had prime rib, grilled potatoes, and green salad with bleu cheese — all in, about $8 before drinks. Better food, better chairs, better music, and no one trying to get us to leave.

Clete, that sounds great. I do not really understand the restaurant business nowadays. I think in the old days, it was just as cheap, or even cheaper, to go to a restaurant to buy a meal as buying and cooking your own food. But that has changed of course. I guess restaurants are still useful for travelers, the lunch crowd and dating, but it is hard to believe that is enough to keep them profitable.

I’m with you on all that. I tell my son if he stops eating out he will save at least 10k a year. Visiting him in Omaha where the unemployment rate is 3% I broke out the recipes I inherited from my wife. They were her Aunt Dora’s who cooked and baked every day. I made the family pizza, sweet and sour cabbage soup, fettuccine alfredo, chicken cacciatore, Jonboht( olive oil garlic zucchini green pepper onion potatoes in tomato sauce with crusty homemade bread. They loved it.

We rarely dine out, but when we do, it’s a real treat. I expect to pay as much as I expect to get great food for the price. Establishment gets one chance, and only one chance, to ever have us visit a second time. We love walking to our downtown establishments, but every price on the menu smells more like the cost of rents than food.

“The more interest I make, the more I can spend”

More proof that higher rates benefit asset holders via interest income.

I have a different perspective. Higher rates encourage savings, which is important for the many retirees who need income and don’t have pensions. Higher rates also encourage the prudent use of capital. Besides, asset holders, on the whole, were enormous beneficiaries of low interest rates and ZIRP. If asset holders win regardless of the policy, then I prefer the policy which encourages savings and provides a modest and safe income on those savings.

Short TLT-

Not necessary to villainize savers. Or quite possibly I’m mistaking your point….

See Rocky comment below.

Respectfully.

John H – definitely not a dig against savers; with my bond portfolio I’m arguably in this category myself.

Just pointing out that higher rates aren’t restrictive for everyone.

I agree with you, we need to keep the interest rates at this level and maybe a tad higher. I was discussing this with a coworker just yesterday and we both agreed that this would be best despite one of us being a Reb. and the other a Dem.

Looking at Wolf’s “Auto Loans & Leases, Balances, Trillion $” chart I was thinking that looks a lot like the “Total Student Loan Balances Due, Trillion $” chart I saw a while back. Going to Google it is crazy how the total of both kinds of loans increased by “about a Trillion” from 2009-2023. We all know the old saying “A Trillion here a Trillion there and pretty soon you owe a lot of money”…

LOOK AT THE SECOND CHART

I originally posted since I tought it was interesting that that both “car” debt and “student” debt went up by a similar amount of “about a Trillion”. In trying to make a joke I was not missing that “car” debt to income is about the same as 20 years ago it may have seeled like I missed the second chart. I’m often telling people waiting for the $400K homes to come back that prices in the Bay Area may be lower than they are now years from now but I would not wait for $400K homes to come back with so many people making so much money. Things are going pretty well for us but my wife says she often feels like we are the “poorest” people in town (I responded that we are not the “poorest” but we may “spend the least”)…

I may be the poorest person in my neighborhood. (Definitely spend the least, starting a few weeks ago).

I feel quite lucky and privileged. So much better than the other way around…

Problem with a big personal balance sheet chock full of recently purchased assets is, things go up and then they go down. I think the money- and credit- overindulgence era psychology is still with us. My big assets can take drastic drawdowns and leave me with a positive net worth. Current events are so weird, I’m not signing up for a bunch of new frivolities. I see a sea of red flags, unless one is a major financier with access to the top. My doom scenario is a rug pull on the American people comparable to what happened to the masses in the former USSR. I see plenty of data points that arguably are precursors.

Not THE poorest, but among the “poor/ workers” in my *extremely wealthy* neighborhood.

It’s great, because I can live like a king off their scraps (during the tourist season/ now).

It’s a bummer because if I splurge, a night out is costly (and rare).

Also, the grocery bill is certainly higher than 5 years ago (I am talking WalMart), but then again so is my paycheck (though due to my struggling nature I earn below my “peak”).

We had considered a new (to us) vehicle, but between prices and a less than expected driving burden, we decided against it.

Struggling but Blessed!

I fricking despise these new Ford-F monsters driving around in my poor-ass county when it’s clear from their pristine condition that they are never used for anything other than signaling “I can crush you”.

I don’t doubt Wolf’s statistics that everything, other than subprime, is ok with these morons since they would prioritize a luxury car payment over stiffing their landlord or buying healthy food for their kids.

Crazy how people make that choice, isnt it?

I too judge pickup trucks that are a bit too clean. And road salt doesn’t count – it just means you want your truck to rust out.

Gotta make up for the small wang somehow…

This is timeless biology. I’m thinking of male beasts of a bygone age with huge antlers. But some of those got into tar pits. They are making a show for themselves as much as anyone else. Hopefully these are somehow socially useful, though the nepo trend will be fed by very low estate taxes. Me, I want to see the balance sheet.

This comment says more about you than it does them

Yes, this stuff is just funny. People love trucks because they love trucks, including women. Big equipment has been very popular with Americans since forever. A whole part of the country has been called “Truck Country” long before everyone else was driving trucks to Starbucks. It just spread from there. Hi-end pickups are a status symbol as well.

OK, so for today’s laugh, saw one of these ginormous, lifted monstrosities with a bumper sticker that says “I identify as a Prius”. 2025!

Just the correlation between new pickup trucks and luxury cars is disgusting. Must be enraging for small business owners trying to purchase utilitarian workhorses. One town’s vehicle may be the $60k+ pickup truck, seems the vehicle to own in my town is the $60k+ German sedan or SUV.

Wolf – question – would it be possible to add a search function to your website so those of us with average memories can search previous articles?

Gracias…

It has one but it isn’t nearly as good as Google.

Just google your question with wolfstreet in front. So for example: wolfstreet drunken sailors

I use google with site:wolfstreet.com, which specifically instructs it to search within your domain.

I got a heart like a truck

It’s been drug through the mud

Runs on dreams and gasoline

And that ole highway holds the key

BOOM!!!

The Spirit of Christmases Yet To Come:

“Haul!”, the revenue agents will sing,

“A tax source found to-day ay ay.”,

And a big ass truck won’t buy you food,

Unless it’s filled with hay.

Etdeficit, etdeficit, etdeficit.

As with all ratio charts, breaking out the historical trends in both the numerator and denominator can be enlightening.

Wolf, can you link to or repost the historical disposable income chart that I’m pretty sure you’ve compiled lately?

Thanks in advance.

@Wolf, thanks for the Disposable Income chart. I just noticed that the rent of an average (east of El Camino) SF Peninsula 1 Bedroom apartment has followed disposable income up going from ~$700 in 2000 to ~$2,200 in 2024

Yes, rents tend to parallel disposable income growth… landlords exacting their point of flesh 🤣

By contrast, rents don’t parallel home prices, which created this situation today where renting is a lot cheaper on a monthly cashflow basis than buying an equivalent home due to the explosion of home prices.

Lol rent seeking is a dirty word in many circles for a reason. In their circles, I imagine they feel similar to the “Poors”.

I agree with Wolf that apt landlords appear to be (or at least *trying* to be) pricing so as to parallel increases in disposable income – it is quite possible that this stat (and other macro stats) get fed into programmatic yield optimizers.

(Macro stats are unlikely to be the primary optimizer variables – occupancy and local competitor pricing will always dominate – but it is definitely possible that local macro stats get thrown into the mix).

That said, optimizers are only going to puke out *attempted*/asking prices – if tenants don’t go along (ie, find alternative housing options) then occupancies will fall and the optimizers will recalibrate at a lower asking price point.

But playing chess against HAL 9000 (and dueling with local government authorities who restrict incremental apt supply so as to shield phoney-baloney “wealth effects” among incumbent home owners) is exhausting, depressing, and a relatively new historical phenomenon.

Who knows what Trump will do, but the Feds did find enough RealPage optimizer-centered collusion-facilitating hanky-panky to launch an indictment in January.

Grandson always asks me ” Grandpa how come you always have a few bucks when I ask you for some”. Well I answer” cause I drive a 20 year old pickup and pay cash for what I need.” Old fashioned yep I guess so, but it works for me

…

What kind of truck, Rocky?

My car is currently 14 years old with 195k miles… goal is to get at least 20 years / 300k out of it which seems reasonable.

Boss at work was telling me about his friend, who literally drove a Civic with a half million miles to the junkyard. The motor was perfectly fine but the frame was completely rusted out.

I had 16 years and 180K on my car and just threw in the towel. Still ran well and was my daily but it was getting uncomfortable since it old and worn out. I drive 60 miles round trip in SOCAL traffic and I just couldn’t handle it anymore.

I figured I’d sell it for cheap to someone and bought a new commuter car. The tech and comfort in a modern econobox is a huge difference compared to a 16 year old econobox. Wireless andorid auto, 34 mpg hwy, lane keep asssit (which seems dumb until you try it on a road trip and you’ll never want to go without).

I think there’s a happy medium between living in perpetual debt and punishing yourself because you don’t want to spend a dime of what you make to be comfortable on your daily commute.

fully agree. i will never buy a car without birds’ eye camera and beeping sensors that beep if you get close to something on any side or if you’re pulling out of a spot and someone is coming, again. the risk is just not worth it.

“it was getting uncomfortable since it old and worn out”

Suspension can be rebuilt. Parts replaced. That’s what I’ve been doing to my ride – the front is now all brand new – control arms, ball joints, coilovers, bearings, CV axles – I even replaced the intermediate axle which was a PITA since you have to drop the subframe.

Personally I wouldn’t replace a vehicle with a good motor over this – but I also dislike the newer cars and can do some of my own work, so for me it makes sense to keep driving what I have.

“Wireless andorid auto, 34 mpg hwy, lane keep assist”

Also things I don’t care for. I have a flip phone, and I’ve moded my car well beyond stock so MPG isn’t on my mind (although I can manage 22 hwy with cruise control).

Don’t even get me started on the electric servos that are in modern steering systems and necessary for your lane-keep assist – I feel so disconnected from the road vs a traditional hydraulic rack & pinion system. I get that this is “the future” but again, not my cup of tea. I guess not needing power steering fluid flushes is a benefit.

“I think there’s a happy medium between living in perpetual debt and punishing yourself because you don’t want to spend a dime of what you make to be comfortable on your daily commute.”

Can’t argue with this. Replacing the entire front suspension cost me nearly $1000 but it was totally worth it.

Short:

I realized that a reason people replace their vehicles is not necessarily mechanical.

It’s the stereo knob, the sticky vent where I spilled the soda that one time and the uncomfortable seat etc.

I am in a 2013 Tacoma and love it though (but I generally commute on my ebike), rather my wife enjoys it as it serves her work needs.

Our other “vehicle” is an ‘06 Wrangler. I have wondered why I have 2 lifted vehicles with oversized tires… until I find the potholes on I-70.

Rust, bane of my existence. 2010 base utilitarian Colorado (really an Isuzu) with under 50k on it is going to rust out from underneath me, replacement cost at least twice as much as we paid. Dreading it.

More confirmation that the eCONomy is just fine for now. Thanks Wolf!

Reading your posts, and seeing the panic on the faces of some local realtors, who have been living high on the hog, have been of great comfort lately.

Loving the higher rates today. back in the 0% days my IRA cash earned me $50/yr. I have since doubled the amount in cash and now earning ten times that amount. 3 cheers for the savers.

MW: Another EV maker goes bust, as Nikola files for bankruptcy

NKLA -35.33%

Yep, from a 30+ billion dollar market cap to zero in five years! We crashed tech companies so much faster “back in the day”… (i.e. 2001)

One can only imagine if Harris was in office, how many $100 of millions would have been given to the company by the Feds to stay open and continue to lose money.

Why do you have to be so political?

I believe next quarters NY Fed Household Credit report will be the first where servicers should be reporting student debt delinquencies again.

Should be interesting to see how much that impacts total delinquencies.