Those yields look too low for what’s coming at the bond market: The next wave of Inflation and a Fed that’s comfortable with 3%+ core PCE inflation.

By Wolf Richter for WOLF STREET.

The US government sold $620 billion of Treasury securities this week, in nine auctions. Of these auction sales, $480 billion were Treasury bills, with maturities from 4 weeks to 52 weeks, most of them to replace maturing T-bills. And $140 billion were 3-year, 10-year, and 30-year Treasury securities.

The Treasury Department reduced the size of three T-bill auctions (4-week, 6-week, 8-week) this week by a total of $55 billion compared to the same week in March and by $65 billion compared to the same week in February, as large amounts of tax receipts are flowing into the government’s checking account in April around Tax Day, including from quarterly estimated taxes for Q1 and from capital gains taxes for 2025.

| Type | Auction date | Billion $ | Auction yield |

| Bills 4-week | Apr-09 | 81 | 3.560% |

| Bills 6-week | Apr-07 | 75 | 3.615% |

| Bills 8-week | Apr-09 | 76 | 3.575% |

| Bills 13-week | Apr-06 | 96 | 3.635% |

| Bills 17-week | Apr-08 | 70 | 3.600% |

| Bills 26-week | Apr-06 | 83 | 3.615% |

| Bills | 480 |

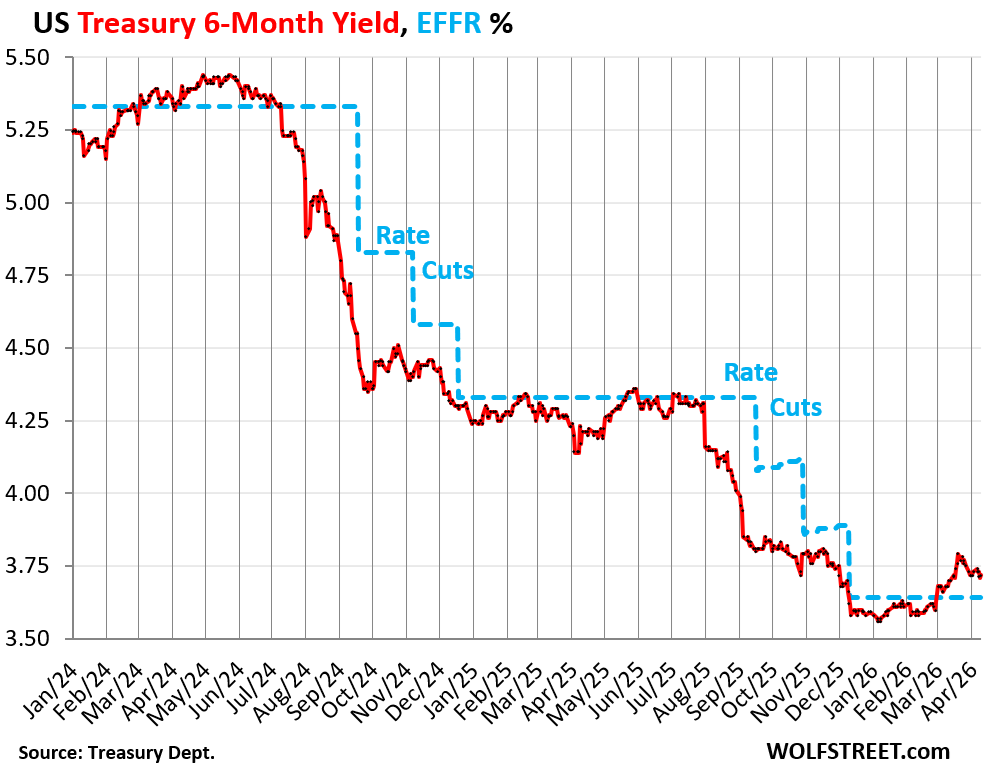

At the 26-week Treasury auction this week, the yield rose to 3.615%, 8 basis points higher than last week, and also 8 basis points higher than the same week in March. This is the “high rate.” When calculated like note or bond yields, it corresponds to an “investment rate” of 3.73%.

In the secondary market on April 6, the day of the auction, the 6-month Treasury yield traded between 3.72% and 3.75%.

On Friday, the 3-month Treasury yield closed at 3.71%, roughly unchanged from a week ago, and solidly above the Effective Federal Funds Rate (EFFR) which the Fed targets with its policy rates (blue line).

The 6-month yield had risen above the EFFR at the beginning of March when the war in Iran began, indicating that the market began to see a chance of a rate hike in its 6-month window.

Of those $620 billion in auction sales this week, $140 billion were Treasury notes and bonds.

| Notes & Bonds | Auction date | Billion $ | Auction yield |

| Notes 3-year | Apr-07 | 68 | 3.897% |

| Notes 10-year | Apr-08 | 46 | 4.282% |

| Bonds 30-year | Apr-09 | 26 | 4.876% |

| Notes & bonds | 140 |

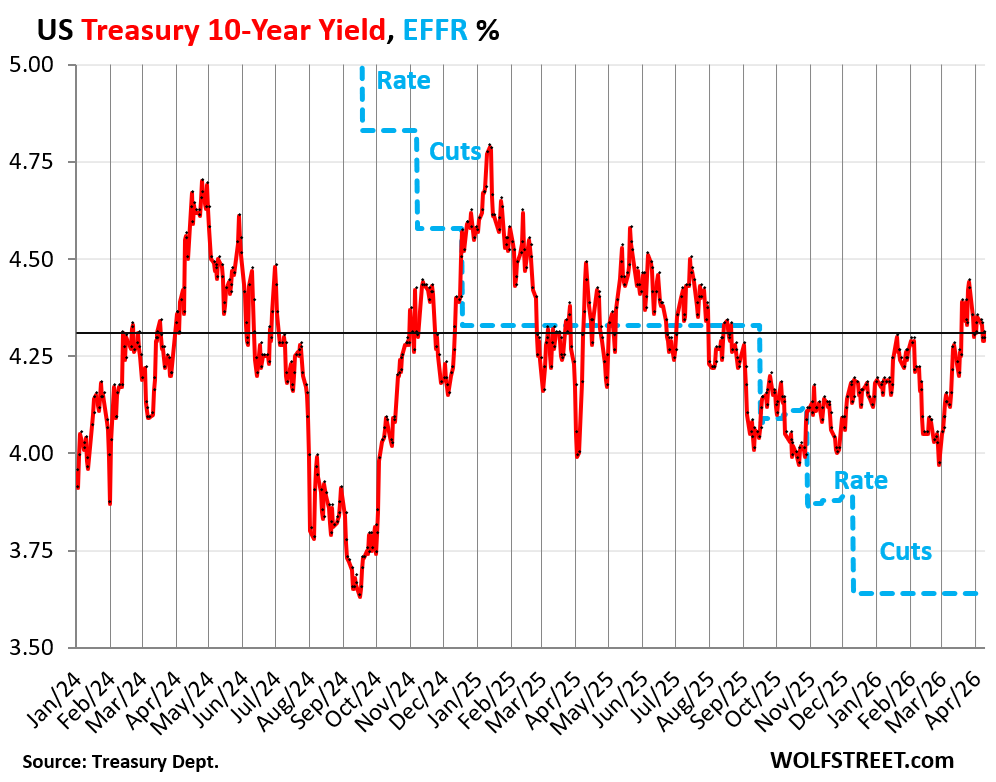

The 10-year Treasury note sold at the auction on Wednesday at a yield of 4.282%, up by 6 basis points from the auction last month.

In the secondary market on Friday, the 10-year Treasury yield closed at 4.32%. Higher bond yields in the market mean lower bond prices for existing holders.

Longer-term yields are determined by the yo-yo of the bond market and reflect the bond market’s views of the future – especially the path of inflation and the tsunami of supply of Treasuries to fund the ballooning deficits.

10-year notes outstanding increased by $26 billion this week: The $46 billion of 10-year notes sold at the auction this week at 4.282% and maturing in February 2036, replaced $20 billion in 10-year notes sold at auction in April 2016 at 1.765%, that had matured in February 2026. So with this week’s auction, the total amount of 10-year notes outstanding rose by $26 billion.

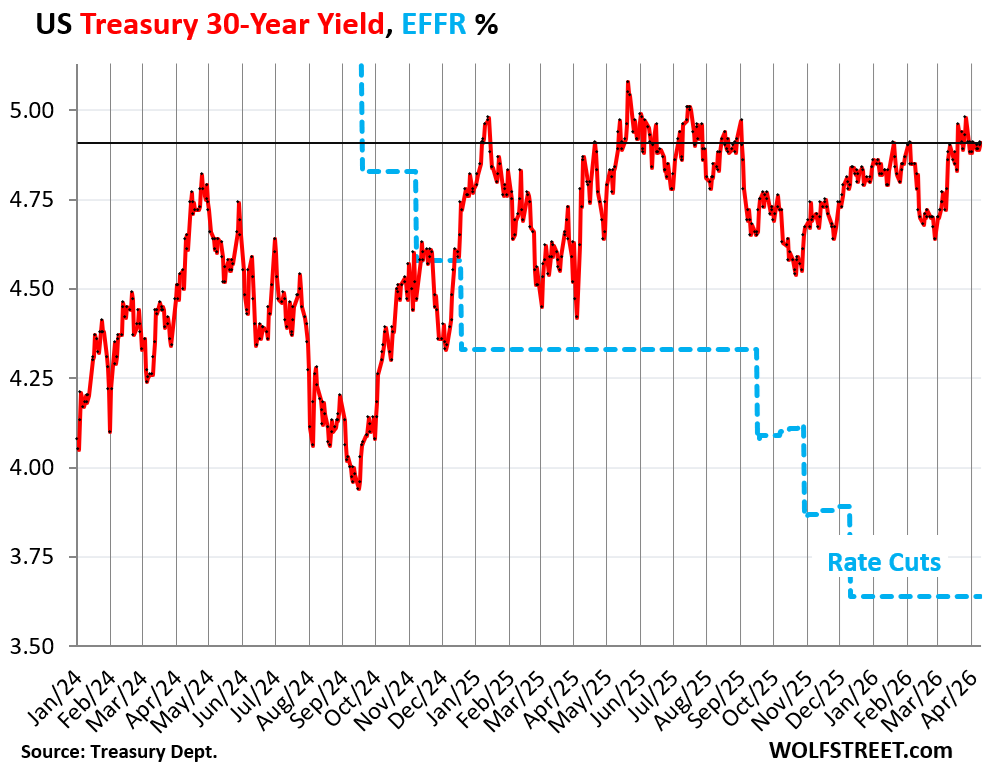

The 30-year Treasury bond sold at the auction on Thursday at a yield of 4.876%, a hair higher than a month ago.

In the secondary market, the 30-year yield closed on Friday at 4.91%. It has been on the verge of 5%, and sometimes over 5%, for over a year.

This end of the Treasury market completely blew off the Fed’s rate cuts:

Not with a 10-foot pole at current yields.

At this yield, with this potential path of inflation, with this Fed, and this path of the debt, 10-year paper looks very unappetizing to this observer, and 30-year paper looks even worse.

Inflation, as measured by the Fed-favored core PCE price index has been rising for months and in January and February was at around 3.0%, and that was before the energy price spike.

The Fed appears to be comfortable with 3% inflation, and seems not overly frazzled about inflation going over 3%, and that was before the energy price shock hit, and now it’s going to “look through” the energy price shock for a while and let inflation do its thing.

And maybe that’s the only way the debt – which is on an “unsustainable path,” as Powell likes to say – can be dealt with given the hopelessly Drunken Sailors in Washington: Let it run hot.

Higher inflation, such as in the 3% to 5% range, and higher nominal economic growth beget higher tax receipts, which make the interest payments easier to deal with, and we’re already seeing some of those effects, and years of higher inflation reduce the burden of the existing securities when they mature because they get paid off with devalued dollars.

But it’s a horror show for bondholders if they buy those securities when the yields are too low and don’t sufficiently compensate them for the devaluation and the other risks they’re taking.

That 2% is still the Fed’s official inflation target, but inflation has been above 2% for over five years. The low point was in April 2025, when the core PCE price index was up 2.6%. Even as the core PCE price index was accelerating in the fall toward 3%, the Fed cut its policy rates three times – an indication that it feels comfortable with 3%-plus.

That leaves no wriggle room for buyers of 10-year Treasures at a yield just 1.3% higher than pre-energy-price-spike core inflation rates. The energy price spike could drive inflation substantially higher, and the Fed will bravely “look through it” for a while, which is a bad omen for the next 10 years for investors that bought 10-year paper at a 4.3% yield.

In 2020, investors bought 10-year Treasury notes at auctions at yields below 1%: At the March 2020 auction at 0.85%; at the April 2020 auction at 0.78%, at the May 2020 auction at 0.70%, at the June 2020 auction at 0.83%; at the July 2020 auction at 0.65%; at the August 2020 auction at 0.67%… They were hoping that yields would fall into the negative after their purchase. There was talk of that.

They got their faces ripped off when inflation began to soar starting in mid-2020. The core PCE price index went from the low point of 1.0% in June 2020 to 1.5% in December 2020, to 3.9% in June 2021, and blew past 5% in December 2021 when the Fed was still near-0% and was still doing QE. The Fed didn’t end QE until early 2022, and the first timid rate hike came in March 2022.

Some of those investors that had bought those misbegotten 10-year notes in 2020 were the banks that had believed the Fed’s “forward guidance” of no rate hikes for a long time, and that then collapsed in the spring of 2023 because the market values for their securities had plunged as yields had soared amid inflation and the Fed’s steep rate hikes and QE.

Inflation never came back down to 2%, and the next wave of inflation has started, and the Fed will let it run hot. And maybe that’s the only way to manage the path of the debt, given the Drunken Sailors in Washington.

But for potential buyers of long-term securities, these are treacherous times. Inflation destroys the purchasing power of bonds; a higher yield is supposed to compensate investors for the loss of purchasing power, plus for the other risks and costs they’re taking on. And to this observer, the current 10-year yield is too low for this environment; it’s not compensating investors nearly enough to take those risks over the next 10 years.

In case you missed it: US Government Interest Payments, Tax Receipts, Average Interest Rate on the Debt, and Debt-to-GDP Ratio in Q4 2025

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()