It’s ugly, but slightly less ugly.

By Wolf Richter for WOLF STREET.

What portion of tax receipts gets eaten up by interest payments on the monstrous Treasury debt? That’s the question. And we got data on it today for Q4.

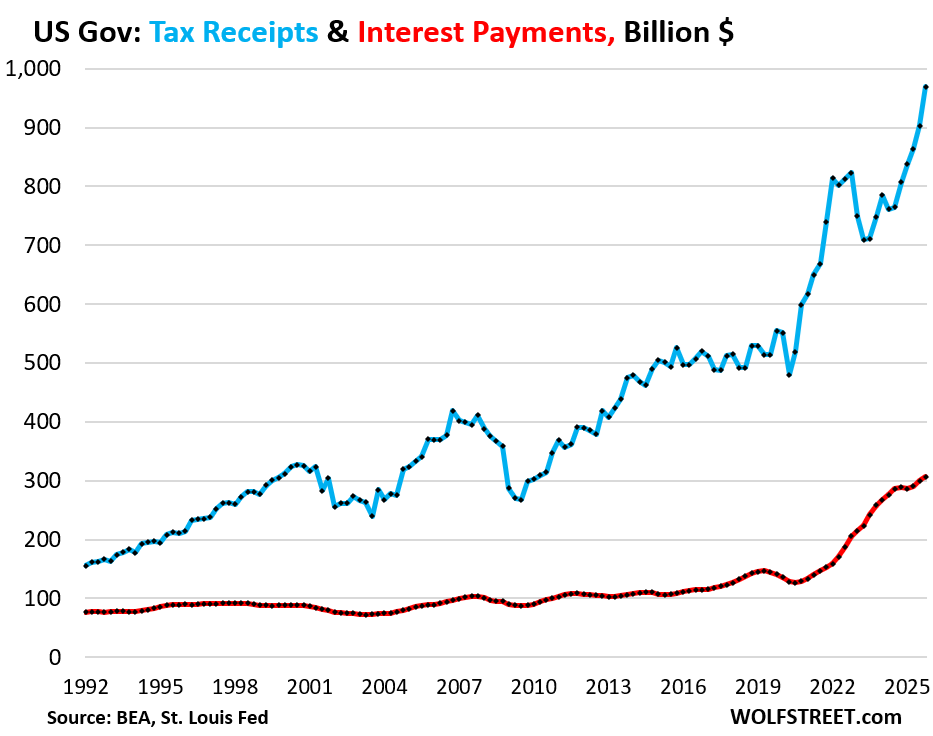

Tax receipts by the federal government jumped by $67 billion (+7.4%) in Q4 from Q3 to a record $902 billion. For the whole year, tax receipts jumped by $456 billion (+14.6%) to $3.57 trillion (blue line in the chart below).

Interest payments by the federal government on its monstrous Treasury debt rose by $7 billion (+2.4%) in Q4 from Q3, to $307 billion (red in the chart below). Interest payments don’t occur in a vacuum, but in the context of funds coming in to pay for them: tax receipts.

This measure of tax receipts, released by the Bureau of Economic Analysis today as part of its revised National Accounts data, tracks the receipts that are available to pay for general budget expenditures, such as interest payments, defense spending, government salaries, etc. Excluded are receipts that are not available to pay for general budget expenditures and are not included in the general budget, primarily Social Security and disability contributions that go into Trust Funds, out of which benefits are paid directly to the beneficiaries, and those payments are also not included in the general budget.

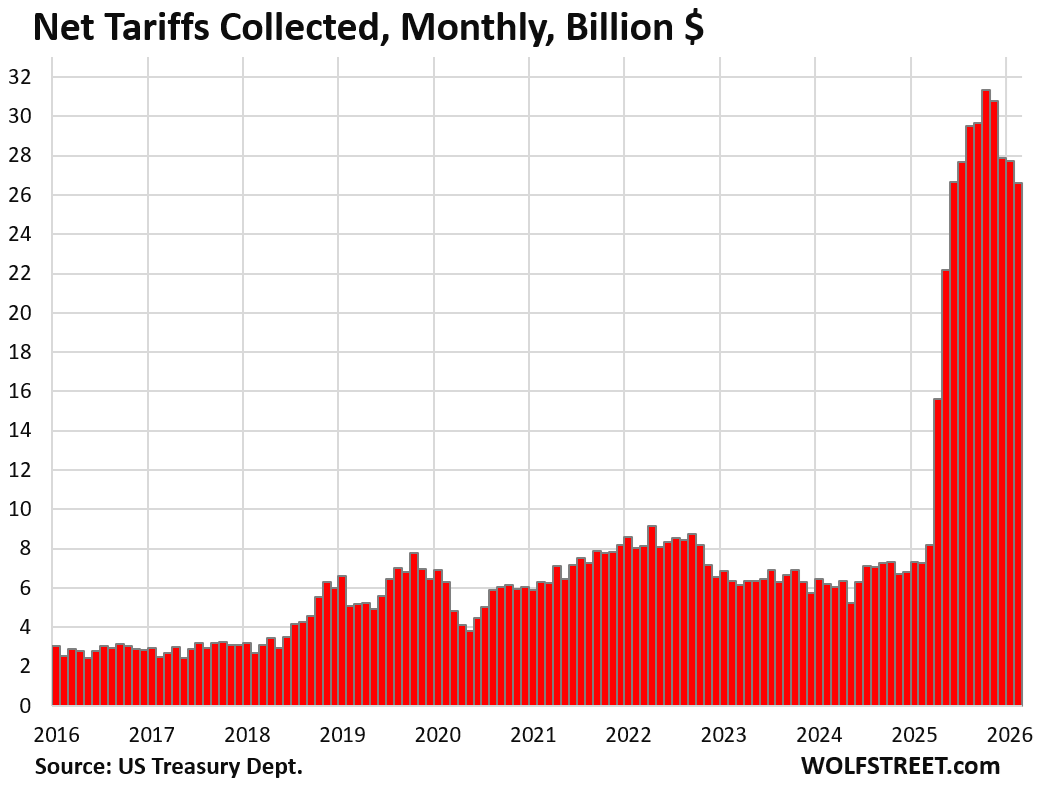

A growing economy generates more taxable income and higher tax receipts – both from corporate and individual taxpayers. Growing asset prices generate capital-gains taxes. But those capital gains tax receipts can drop precipitously when asset prices drop, such as in 2022. In addition, in 2025 there were the revenues from the new tariffs.

Tariffs amounted to $90 billion in Q4. For the past 12 months through February, they amounted to $304 billion, per the most recent Monthly Treasury Statement.

But the Supreme Court struck down part of those new tariffs, and the government will be paying out refunds of some of those tariffs. At the same time, the government already announced replacement tariffs under different laws. So in 2026, net receipts from tariffs, including refunds, will likely be smaller. But that was the situation for Q4.

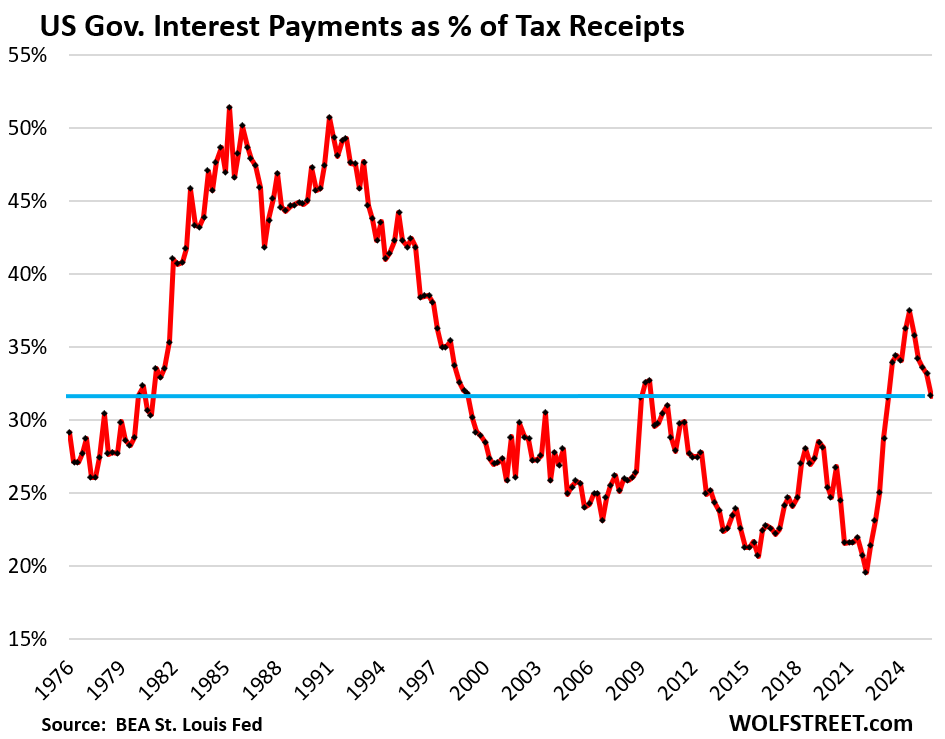

Interest payments as a percent of tax receipts: Interest payments in Q4 ate up 31.6% of the tax receipts available to pay for them.

Ugly, but slightly less ugly than in the prior quarters. The high in Q3 2024, at 37.5%, was the worst ratio since 1996, when the ratio was receding from the crisis times in the 1980s.

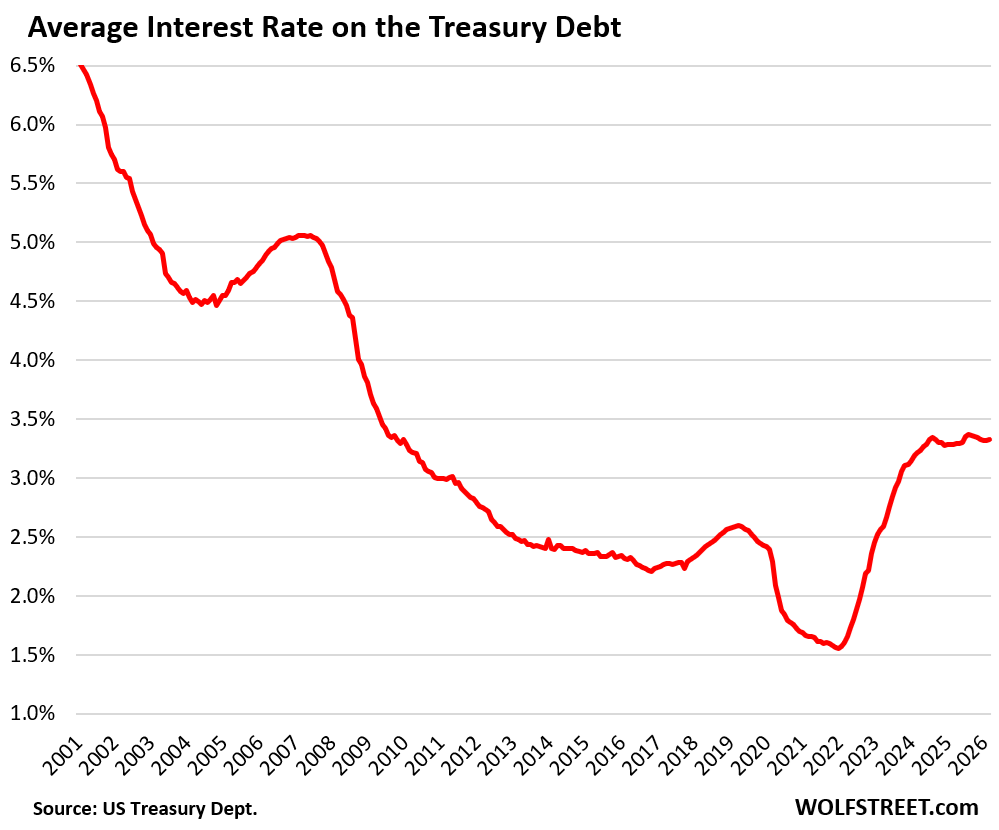

The average interest rate on the Treasury debt was 3.33% in March, according to data from the Treasury Department, having stabilized since Q3 2024 between 3.30% and 3.37%, after more than doubling since the Fed first hiked its policy rates in early 2022:

New interest rates enter the interest expense when old Treasury securities mature and are replaced with new Treasury securities at the new interest rate, and when additional Treasury securities are issued at the new interest rates to fund the deficits.

There are currently $6.8 trillion in Treasury bills outstanding (terms between 1 month and 12 months), and they constantly mature and get refinanced in huge auctions every week, and issuance is also slowly being increased.

As the Fed cut its policy rates, the interest rate that the government paid to sell new T-bills fell from over 5% in mid-2023 to about 3.6% currently, which pushed down on the interest expense.

But when longer-term debt is issued at auction, their interest rates are often higher than the rates of the securities that matured and that they replaced.

Recent 10-year note yields at auction were over double the yield at which the maturing notes had been issued 10 years ago. And the size of the 10-year note auctions has roughly doubled from 10 years ago. So the government paid over double the interest rate on over double the amount, which quadruples the dollar-interest expense on that issue from the issue it replaced.

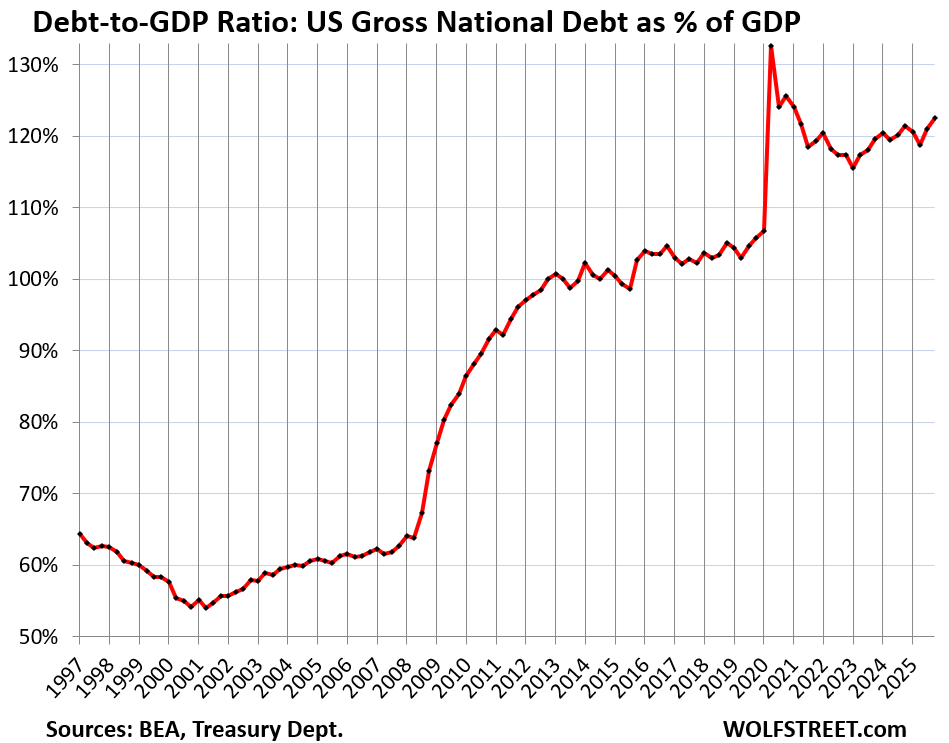

The ugly Debt-to-GDP ratio rose to 122.5% in Q4 and is now back on trend.

The ratio for Q1 and Q2 had dropped because of the effects of the debt ceiling, which prevented the debt from ballooning but drained the government’s checking account. At the beginning of Q3, the debt ceiling was raised, and debt issuance spiked in Q3 and Q4 to refill the government’s checking account.

The pandemic was unique in that GDP collapsed in Q2 2020, while the debt exploded, and the ratio spiked in a breathtaking manner. As GDP bounced off, while the growth of the debt slowed somewhat to still very high growth rates, the ratio backed off through 2022.

But in 2023, it started rising again even as the economy was growing at a rapid rate. The problem has been the $2.2-plus trillion in new debt that was added every year for the past three years by the Drunken Sailors in Washington:

But there won’t be a default on this debt because the US issued this debt in its own currency and can always create more currency to service the debt (the Fed buys some of the debt). So default is not the issue.

The issue is inflation. In an already inflationary environment, creating money to service an out-of-control debt would cause inflation to spiral out of control, crush the economy, and lead to years of wealth destruction and lower standards of living. Everyone knows this – even the people in Washington.

So the go-to hope seems to be to trim the annual deficits a little, including through tariffs, to where economic growth (as per nominal GDP) and modest inflation (3%-5%) outrun the growth of the debt, which would gradually over the years whittle away at the problem and lower the burden of the debt. This scenario assumes that there won’t ever be another recession, good luck with that.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

A very efficient mix of graphs and text, as usual.

Yes! Wolf your communication style is unmatched on the internet. Never change!

Wolf, what happens if there’s a recession? It seems like assets can crash like the Dotcom bubble, but then quick intervention restores everything to even a higher baseline. For the Dotcom era and even the Great Recession, asset prices took a while to sort out and then build the momentum from ZIRP / QE. It feels like we are heading towards an economy that can be in recession in definition, but certain assets could be protected regardless.

I mean, is that practically possible? Thoughts?

If there is lots of inflation, there won’t be any intervention. The Fed might let the recession solve the inflation problem on its own.