Government crackdown and legal entanglements take all the fun out of the Medicare Advantage plan bonanza.

By Wolf Richter for WOLF STREET.

Humana is one of the big health insures with Medicare Advantage Plans that have come under intense scrutiny from this Administration, from the prior administration, from Congress, from legal actions, and from investigative reports in the media, amid allegations of dramatically overbilling Medicare. These insurers are facing a full-blown government crackdown.

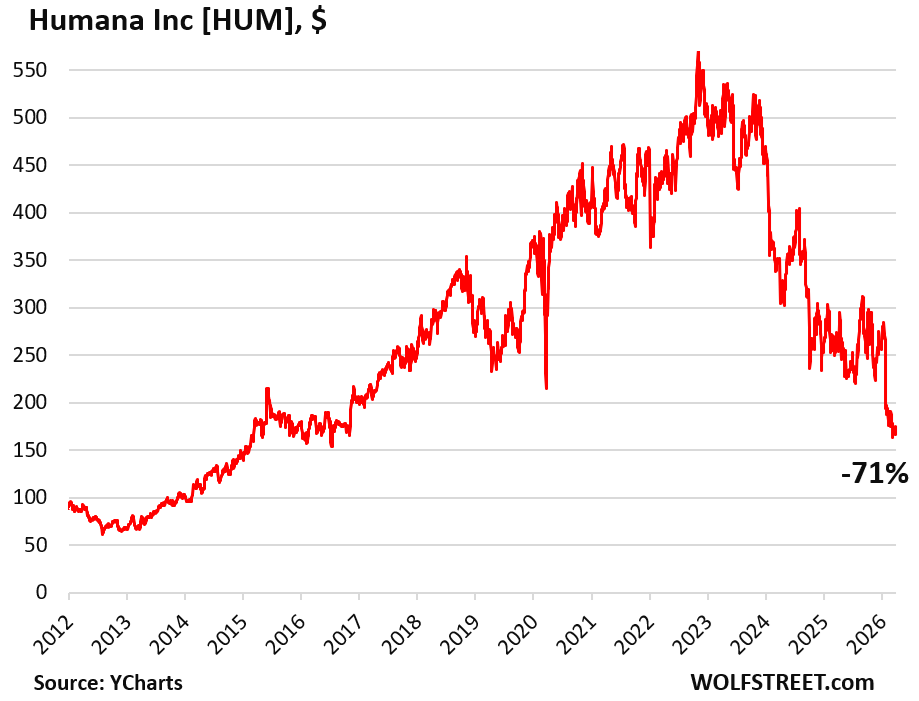

But it was so sweet while it lasted, generating huge profits, big revenue gains, and a massive run-up of the price of the stock: Humana’s shares – along with others in that arena – shot higher and higher from 2017 through 2022. But amid that crackdown, revenue growth has stalled over the past few quarters, and Humana posted a big loss in February.

Humana’s shares [HUM], which started cratering in November 2022, have now entered our pantheon of Imploded Stocks, for which the minimum requirement is a plunge of 70% from the more or less recent all-time high. Its shares today fell 1.8% to $166.01, down by 71% from the all-time high on November 3, 2022, and down by 37% from a year ago, and pretty exactly back where they’d first been 11 years ago, in March 2015 (data via YCharts).

This is what happens when corporate revenue growth, profits, bonuses, and lucrative stock-based compensation plans depend on overbilling the government, and the government finally belatedly gets tired of it, and cracks down.

Medicare Advantage plans are a semi-privatization of Medicare under which the government pays the health insurer a monthly amount for each of their enrollees, and the insurer then pays for the treatment of the enrollee (the enrollee pays for Medicare Part B and some also pay a premium for the Advantage Plan). Advantage Plans include prescription drug benefits and assorted other benefits, caps, and reductions.

The monthly amount that the government pays to the insurer for each enrollee rises with the health problems the enrollee has. So, inevitably… if the insurer “finds” more and bigger health problems, or exaggerates existing health problems, they can claim substantially higher monthly fees, even if those health problems don’t exist, or never get treated. And the government pays them for it.

This type of overbilling led to higher costs for Medicare, and part of those were passed on and led to higher Medicare Part B premiums that seniors pay. According to a report by the US Congress Joint Economic Committee earlier in March, “in 2025 the federal government paid Medicare Advantage insurers an estimated $76 billion to $84 billion more than it would have cost to cover the same beneficiaries in Traditional Medicare.”

The committee found that “overpayments increased Part B premiums by $212 per enrollee in 2025, totaling $13.4 billion in higher premiums.”

And it found that since 2016, these overpayments “have added an estimated $82 billion to Part B premiums.”

But every dollar that was overpaid by the government added to the revenues and profits of the insurers. And the incredible trajectory of their stocks from 2017 through 2022 shows that.

And there are other aspects, as the Medicare overbilling scandal has metastasized. For example, a federal court ruled last week that Humana, CVS Health subsidiary Aetna, and Elevance Health, must face a civil lawsuit that alleges, based on a whistleblower that came forward in 2021, that the insurers paid “hundreds of millions” in kickbacks between 2016 and 2021 to online brokerages to steer people to their Medicare Advantage plans – because those Advantage Plans were so immensely lucrative to the insurers.

Humana has also gotten caught up in allegations that it had been overbilling the government for Medicare Part D (prescription drugs) plans, and settled a number of those cases, including for $90 million in 2024, a whistleblower case brought by one of its former actuaries.

But as far as investors and Wall Street analysts are concerned, the bigger the Medicare overbilling, the better because it made everyone a lot of money. Just don’t get caught.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

THANKS for helping put the spotlight on these egregious MedicareAdvantage Plan practices. It really is scandalous and sad.

Just like the fraud in MN, CA and elsewhere in various gov’t connected programs…this graft has been going on for a long time.

Gov’t is and has been part of the problem: both from management and oversight povs.

Thanks wolf

Are there any good providers of this stuff?

Everyone I know who is on any kind of Medicare plan loves it, compared to what they had before — and the costs involved.

This isn’t about enrollees being unhappy, it’s about the government getting screwed. Enrollees got some of the benefits because plans were able to fund them by screwing the government.

Medicare is complicated and confusing, and everyone has to make their own careful decisions. Advantage plans differ, as do providers. There are also difference by state. These are very complex decisions.

You might want to ask people in your area what plans they’re happy with.

I’ve been on medicare a couple of years, and the supplemental medicare coverage insurance, “Plan G” costs a little more than the advantage plans, but is far superior IMHO. It basically covers everything covered by medicare but pays the 20% not paid by medicare for parts A & B. There is no underwriting whatsoever with Plan G supplemental plans. Very simple.

Get BC/BS so you can pick your out of service area provider if need arises. Extremely important if you’re not close to a regional medical Center like TMC in Houston, Stanford in Wolf’s neighborhood, Cleveland Clinic. Medical tourism is alive and booming within the US. It’s your life and you must be proactive and find the best provider for your situation and hound your local provider for a referral. My own provider is the largest in Hawaii and denied my referral. I went to MD Anderson direct and they had me approved for out of service area in one day.

Biggest recent bummer was the significant yearly cap increase for Advantage customers. Mine is now over 7K, They also take nearly $500/mo from SS extra because I still work and make North of the cut off line. And SS is taxed both ways. 15.4% off my income for SS/MC and then taxed on it when I get it.

But it comes in handy if you have a medical incident over $10k per year which happens once you get over 50 or so.

In the end you have some choices:

Spend it

Leave it to your spouse

Leave it to your kids

Leave it to your dog

Spend some of that hard earned coin on your own health because life above ground is waaaaay better than ashes in an urn for most people. And grandkids in the yard is still a great way to enjoy the sunset years.

Guess who made his name in the Medicare fraud game? Florida senator Rick Scott! But no one cares.

Time for a slap on the wrist.

Fraud of this magnitude will probably force the board of directors to cut CEO’s bonus by 20%.

Forget that, if they know how to look out for #1 then investors reward you!

Haha

You know just don’t go full Nahhhzeee, never go full Nahhhzeeee 😂

…plus a pardon and lobbying gig.

Once again, no one will go to prison and might even run for elected office afterwards.

Those of us who have been to places with national healthcare like Taiwan know the benefits. These plans work because of caps on medical procedures, doctor’s visits, imaging/diagnostics, and medicine all of which are nonstarters in the US because of profiteering.

Lastly, tover 40% of the US population is obese. Diabetes, obesity, and blood pressure are lifestyle diseases that waste resources on people who choose to be unhealthy. Why should we subsidize their behavior?

But look at where all the innovation in new medicines happen. It’s like 98% in the us because our system rewards innovation.

Medicine has to overcome the fact that Americans don’t do what they are supposed to.

Don’t check your blood pressure

Don’t eat right

Don’t exercise

Smoke

Drink

And American medicine still keeps you lousy lots alive most of the time.

Howdy Youngins. Always pay attention to every credit card charge. Humana also charges credit cards yearly renewal fees for policies that did not exist. BOA card services makes it extremely difficult for the card holder that notifies them about fraudulent charges. They protect the merchant first…Long wait times for customer service centers …. Certain claims must be called in and you will wait and wait and wait…..

That’s why use an Amex

But Medicare for all. Ugh.

Talk about a golden goose for fraudsters.

The government just as much to blame.

No legitimate oversight and out dated tech. Employees dont care.

Just waiting for that pension.

Taiwanese health care?

Caps on procedures?

Go for it.

Hope u like dying waiting for that procedure past your cap.

As a former Humana actuary (unfortunately, I am not the aforementioned whistleblower), this is not at all surprising. I’d love to see a study that shows what portion of healthcare spending goes where – @Wolf let me know if I can help! I would bet the amount that goes to doctors and actual providers of care (not admin/IT/coding staff at the hospital conglomerates) has got to be a laughably small percentage, if not a rounding error.

The whole system is broken way beyond repair and this is just one tiny example of how the industry is set up to scrape every last extra dollar possible out of the system for as long as possible.

The good news is that health insurance is so convoluted that not even AI can take away those jobs :D

If the current broken system gets just a little more expensive, people will find it cheaper to just go see a doctor and pay cash, old-school style. Cut out the insurers and all the middlemen. At least for anything routine, non-catastrophic.

The only real reason we have a system that requires a gazillion middlemen just to get stitches, antibiotics or even a basic chest Xray… is to pretend someone else is paying, and to do it in such a complicated way that the real profiteering parasites can hide themselves, while spooning out a few bribes to their pet politicians to make the system even more lucrative for themselves.

As an unfortunate Humana customer, this year’s premium increase was 32.7%! I will be moving on next year

ouch!

Howdy Andy. Some plans have no open enrollment period. You can change anytime of the year. They hide and confuse US on purpose.

A court appointed receiver is needed to untangle the mess created by Humana and it’s BOD’s. Disgorge those high falutin’ salaries and bonuses.

BK Courts are notoriously corrupt and rigged.

Any system needs a certain amount of operational types to make sure there are facilities, equipment, etc and that the highly skilled are properly compensated. Like oil in an engine. Unfortunately, too many of these people think they are the engine when they really are just mucking it up.

If Medicare advantage costs more than Medicare B, why even offer it? The concept was to bring in private industry to lower costs. But if they are not in competition with B or other providers, then the incentive is to just bill, bill, bill.

They do offer lower costs to enrollees. It’s just that the government made itself very vulnerable to getting ripped off, and it did.

One can only wonder how much fraud could be found if you had a real DOGE department with a way for whistle blowers to easy pass information along to be investigated. In fact, you could possibly offer reward money that’s based on the amount of fraud uncovered. Start paying people to narc.

This is what happens wen lobbyists put on the full court press and the public goes MAGA on a President who in the end was nothing better than a slimy used car salesman that would sell a total lemon to a single Mom with 3 kids on a 15% car loan.

Sure, just sell the US healthcare system to for profit Wall St. grifters. I am amazed at all the college educated idiots that still think Obama walks on water.

Be brave. If you fell for the Health Insurance = Health Care” big lie you can admit it here. Heck, most Americans still don’t know the difference. Personally, my list of friends with Obummercare insurance that were denied treatment and died grows ever longer.

“I am amazed at all the college educated idiots that still think Obama walks on water.”

🤣 Obama did it 🤣

You got the wrong President. Medicare Advantage is a Republican thingy. They used to be called Medicare+Choice in the 1990s. Then under Baby Bush Republican, in 2003, the plans were revised to be roughly what they’re today and re-named Medicare Advantage. Privatizing is a Republican thingy. They wanted to privatize Social Security too at the time, but then the stock market crashed 50% and that put an end to it.

Baby Bush Republican also presided over the creation of the high-deductible health insurance plans, for which Obama-did-it gets blamed, which my wife and I have had since 2006. High-deductible health insurance plans were later incorporated into the ACA (Obama). They come with a Health Savings Account (HSA), to which the contributions are tax deductible, like an IRA account. For 2026, the tax-deductible HSA contributions are capped at $4,400 for self-only coverage and $8,750 for family coverage. And you can invest this money tax free until you need it.

But unlike IRAs, the money in an HSA is NEVER taxed if you take it out to pay for your healthcare.

This system provides cheap healthcare for people with high incomes that can benefit from the big fat tax deduction because they can afford to max out the HSA contributions, and that can invest this money in their HSA accounts in their younger healthier years. Our HSAs are now chockful, and they pay for all our out-of-pocket healthcare expenses. My wife still contributes to hers as she still has a high-deductible health insurance plan. When she broke her hip a couple of years ago, she hit her $4,500 max out of pocket, which she paid for with her HSA card. And when you look at her HSA balance now, you can barely see the dip. I can no longer contribute because I’m on Medicare. What a bummer! Thank you Baby Bush Republican!

Never underestimate how Republicans tilt everything in favor of people with high incomes. And that’s not fair. And Obama-did-it still gets blamed for the wonderful Baby Bush Republican high-deductible health insurance plans with HSAs. The guy can’t catch a break 🤣

Retired in 2000 with pension and Healthcare. 8 years later went on Medicare. The wife followed some years later. The Healthcare company offered an advantage plan and I signed up. Since that time I noticed everything began to get cheaper. During my younger days I always paid a larger portion. Today many of our drugs are free. I can also say even including Medicare costs overall are less.

Not complaining but think something has gone wrong. Waiting for the other shoe to drop, this just maybe the start.

I respect Mr. Wolf’s reporting; however, I cannot see anything wrong here. Just regular Capitalism on the billing end and probably downsized medical claim processing with draconian worker metrics, maybe AI as well.

I don’t think there is any other place in the United States where Medicare and Medicaid fraud is more rampant than in Miami, Florida. Here, clinics fight tooth and nail for every available senior, luring them with parties, cash debit cards, over treatments and meds. They provide elders with nice places to spend the day, dance and socialize. Medical care always comes last and nobody seem to care about.