Whiff of turmoil in the bond market as inflation fears moved to the front and center.

By Wolf Richter for WOLF STREET.

The bond market, which has become very edgy about inflation and future supply – given the ballooning debt – is now seeing the previously unthinkable: a rate hike possibly late this year or next year. That is what the 1-year Treasury yield, the 2-year Treasury yield, and the 3-year Treasury yield are telling us. Those yields have spiked since the war in Iran started.

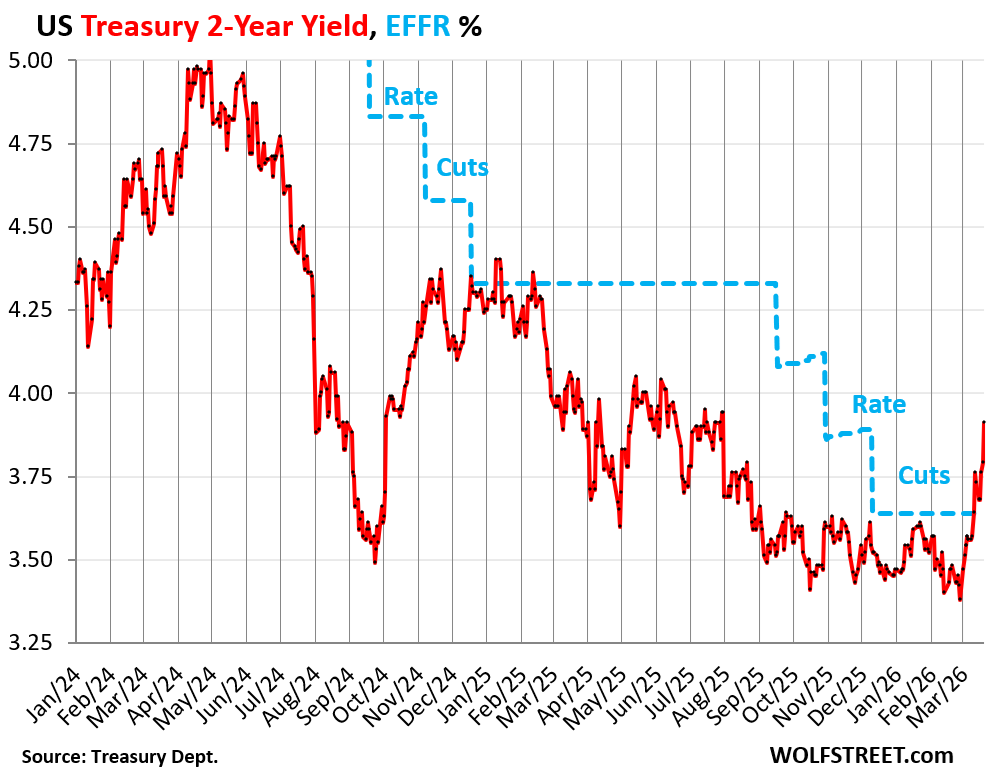

The 2-year Treasury yield spiked by 53 basis points since the beginning of March, to 3.91%. In other words, it flipped from fully pricing in 1 rate cut to fully pricing in 1 rate hike in the span of three weeks.

The 2-year Treasury yield punched through the Federal Funds Rate (EFFR, blue in the chart) for the first time since November 2023, which had been nearly a year before the Fed even cut its policy rates, and is now at the highest point since before the Fed’s last three rate cuts that started in September 2025. The EFFR is the overnight rate the Fed targets with its policy rates; and with the 2-year yield now 27 basis points above the EFFR, the bond market has scuttled rate-cut expectations and replaced them with rate-hike expectations.

Back in October 2024, the 2-year Treasury yield shot higher as the Fed began backpedaling on its rate cut projections, after a lot of the bad data in the prior months was suddenly revised away, and the economy was doing fine after all, the labor market wasn’t deteriorating, and inflation turned out to be alive and well.

The 2-year Treasury yield has a good record of anticipating somewhat distant rate hikes and rate cuts.

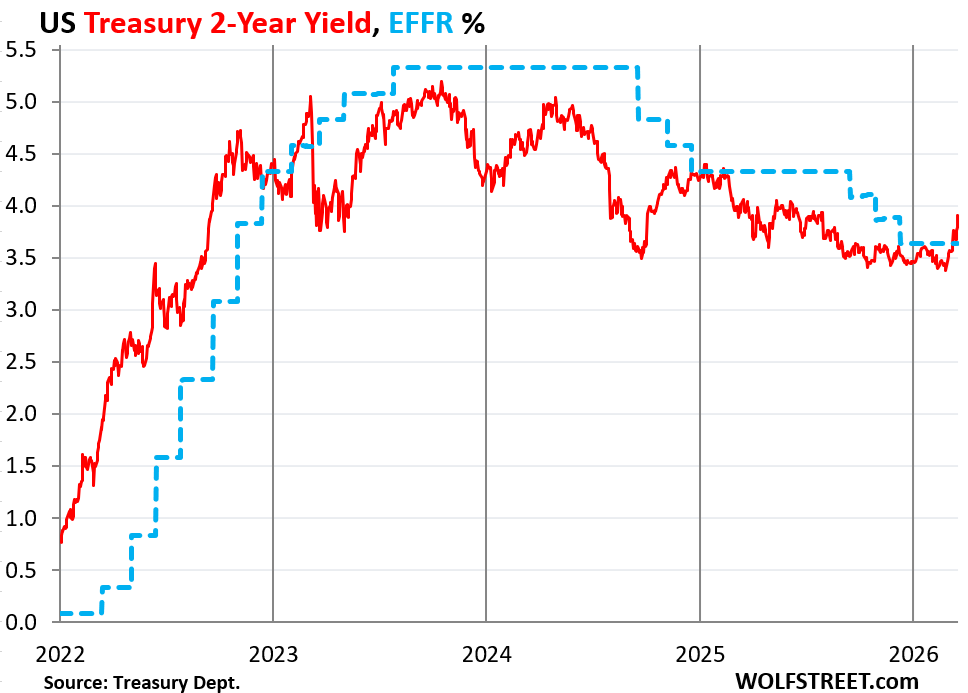

Here is a view going back to the beginning of the rate hikes in this cycle. The 2-year yield stayed ahead of the rate hikes until the end of 2023, when it started pricing in the pause. It anticipated the 100 basis points in rate cuts in 2024 several months ahead of time.

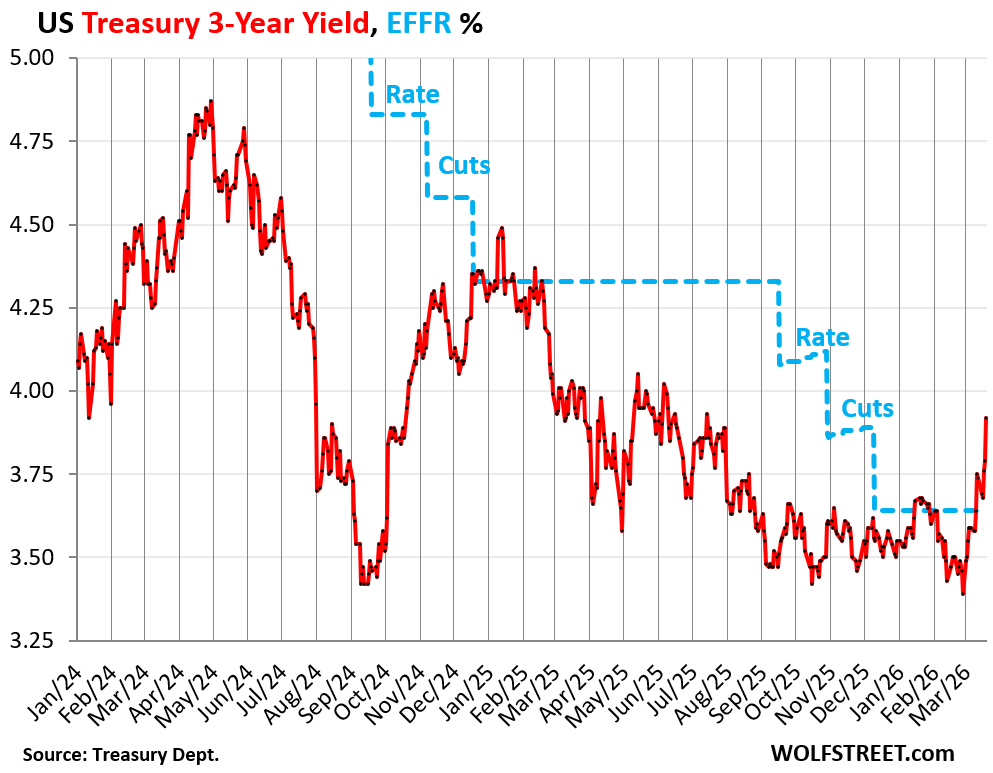

The 3-year Treasury yield spiked by 53 basis points since the beginning of March, to 3.92%, the highest since before the last three rate cuts in 2025.

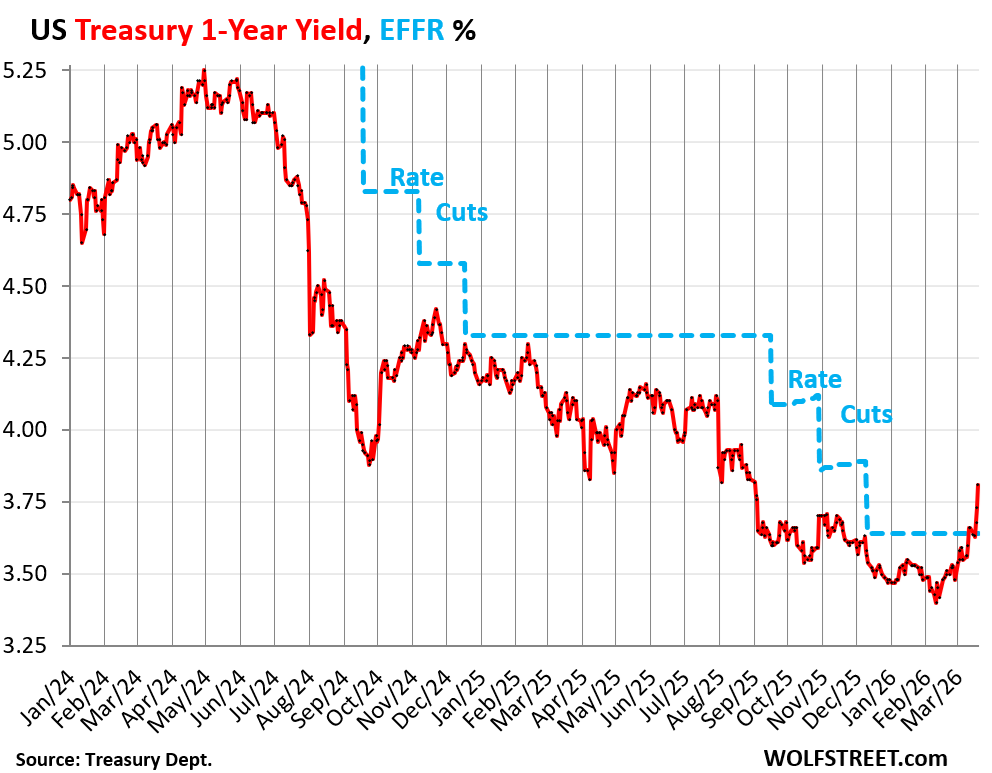

The 1-year Treasury yield shot up by 33 basis points since the beginning of March, removing the rate cut from its less-than-one-year window, and pricing in the potential for a rate hike by late 2026.

Inflation fears are now front and center in the bond market.

This spike in yields started at the beginning of March after the war in Iran kicked off, which caused energy prices to spike, and they spiked even in the US, which has purchased only minuscule amounts of crude oil and petroleum products, and no LNG at all, that were shipped through the Strait of Hormuz.

The US is the largest producer of crude oil and petroleum products in the world, and the largest natural gas producer, and is a big exporter of gasoline, diesel, jet fuel and other petroleum products, and the largest exporter in the world of LNG. This is not a shortage problem for the US, but an inflation problem tied to global commodity prices.

Fertilizer prices in the US also spiked, though the US is a huge producer of fertilizers. The oil and gas industry, and the petrochemical industry in the US are minting money right now because their selling prices have shot up.

There were already inflationary pressures for months before energy prices began to spike: The Fed-favored core PCE Price Index, which excludes food and energy, accelerated to 3.1% for January, the worst in nearly two years. The Fed’s target for it is 2%.

Gasoline and diesel prices have already shot higher. Consumers pay these prices directly by filling up their gasoline or diesel vehicles.

But fuel prices worm their way into prices of goods (as transportation and material costs rise) and into services such as airfares where a major component is fuel. Sometimes, energy price spikes are one-time events that fade as soon as energy prices plunge again; other times they trigger larger and broader inflationary pulses that can get way out of hand, such as in the 1970s.

Powell was clear about it in the FOMC meeting press conference: The Dot Plot median projection was still for one rate cut in 2026, but “if we don’t see that progress [on inflation], then you won’t see that rate cut,” he said.

At the moment of the FOMC meeting on March 18, the bar for a rate hike was still high. But it’s only March.

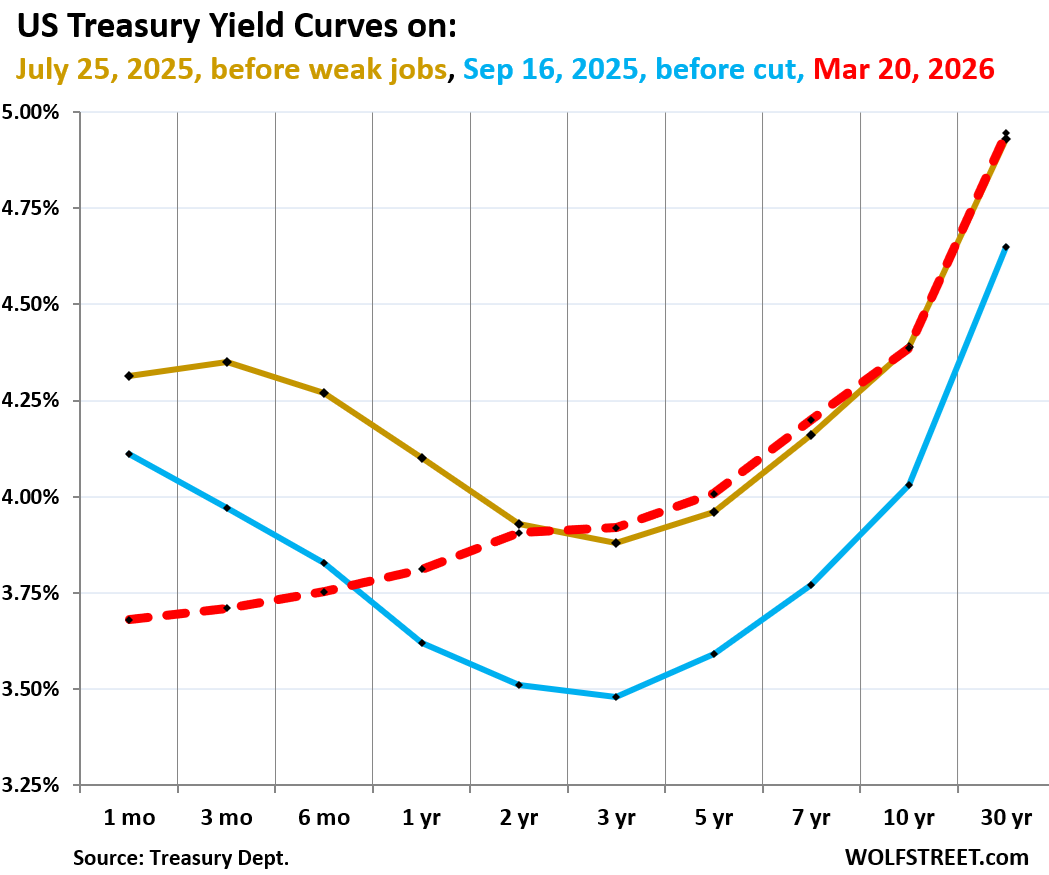

The yield curve solidly uninverted this week. What happened is that yields at the very short end up to the 3-month yield didn’t move much, sticking with the status quo of no rate change in their window. But the longer yields rose, and the yields in the middle – 1 year through 5 years – rose the most, which eliminated entirely the sag in the middle, that had been formed when for the past three years, those middle yields were lower than both, short-term yields and long-term yields.

The chart below shows the yield curve of Treasury yields across the maturity spectrum, from 1 month to 30 years, on three key dates in 2025 and 2026:

- Red: Friday, March 20, 2026.

- Blue: September 16, 2025, just before the Fed’s first rate cut in 2025.

- Gold: July 25, 2025, before the labor market data turned sour again.

The 1-month yield (3.68% on Friday) is bracketed by the Fed’s policy rates (3.50%-3.75%) and closely tracks the EFFR (3.64%).

Despite the turmoil, the borrowing must go on.

The US government sold $606 billion of Treasury securities this week, spread over nine auctions, including 10-year Treasury Inflation Protected Securities (TIPS) and 20-year Treasury bonds.

Of these auction sales, $571 billion were Treasury bills, with maturities from 4 weeks to 52 weeks, most of them to replace maturing T-bills.

| Type | Auction date | Billion $ | Auction yield |

| Bills 4-week | Mar-19 | 91 | 3.615% |

| Bills 6-week | Mar-17 | 92 | 3.635% |

| Bills 8-week | Mar-19 | 86 | 3.635% |

| Bills 13-week | Mar-16 | 96 | 3.610% |

| Bills 17-week | Mar-18 | 69 | 3.610% |

| Bills 26-week | Mar-16 | 83 | 3.570% |

| Bills 52-week | Mar-17 | 54 | 3.485% |

| Bills | 571 |

And $35 billion of the auction sales this week were Treasury notes and bonds.

| Notes & Bonds | Auction date | Billion $ | Auction yield |

| TIPS 10-year | Mar-19 | 21 | *1.896% |

| Bonds 20-year | Mar-17 | 14 | 4.817% |

| Notes & bonds | 35 |

The issuance of 20-year bonds was halted in 1986 and was restarted in 2020. So the entire issue of 20-year Treasury bonds this week adds to the overall debt as it replaces no maturing 20-year bonds because there are none out there in the wild that were issued before 2020.

*TIPS yield: With TIPS, the “yield” is established at the auction, and interest payments are made every six months. But TIPS holders also receive inflation protection, based on CPI, and this inflation protection is added to the principal, and the interest rate (which is fixed for the term of the TIPS) is applied to the entire principal, including the inflation protection. As the principal grows over time with CPI, the interest payments increase, though the interest rate remains fixed. So the yield figure, which is low, is on top of the CPI rate that changes with CPI.

And in case you missed the first half of the bond market analysis yesterday: Treasury Yields Spike, 10-Year to 4.39%, 30-Year to 4.96%, Mortgage Rates to 6.5%, as the Bond Market Gets Antsy

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

There is this ominous text in the Fed Implenatation notes from March 18:

>>Increase the System Open Market Account holdings of securities through purchases of Treasury bills and, if needed, other Treasury securities with remaining maturities of 3 years or less to maintain an ample level of reserves.

I sure hope that will not happen. It constitutes QE/printing against USG bonds.

Did you just wake up? That has been in every statement starting with the December meeting. Several articles about this here. All you have to do is read them.

Thanks for the timely response and (as always) maintainnng a cool head in what appears to be a major monkey wrench turning point.

I think mr Powell is happy to vacate his

office soon.

Who knew bonds could be so exciting?

Wolf man – one simple, honest question for you –

Why does an ‘entity’ that takes money continuously from every worker through income tax, receives corporate tax, tax on fuel (gasoline) and dozens or hundreds of other taxes, need to keep borrowing money? You’d think they’d be sitting on a Mount Everest size pile of cash!

If you or I acted like this, we might get admitted to the mental hospital, or at least to debtor’s prison. Any thoughts?

The government is borrowing because no one wants to pay the extra taxes it would take to cover the deficit. Borrowing is pain-free, taxes are not (until borrowing isn’t pain-free anymore).

Wolf, not asking for political analysis, but how long do you see oil prices remaining elevated and affecting overall inflation? Is this indicating the market thinks we will see increased inflation for 2-3 years?

The March 20 table on treasury.gov already shows the 10-year TIPS real yield picked up a 2 handle overnight. 2.01% is the highest I see in the table going back to July 2025.

Boy, that escalated quickly.