Bond market frets about inflation, leveraged Treasury bets unwind, housing market frets about spring selling season.

By Wolf Richter for WOLF STREET.

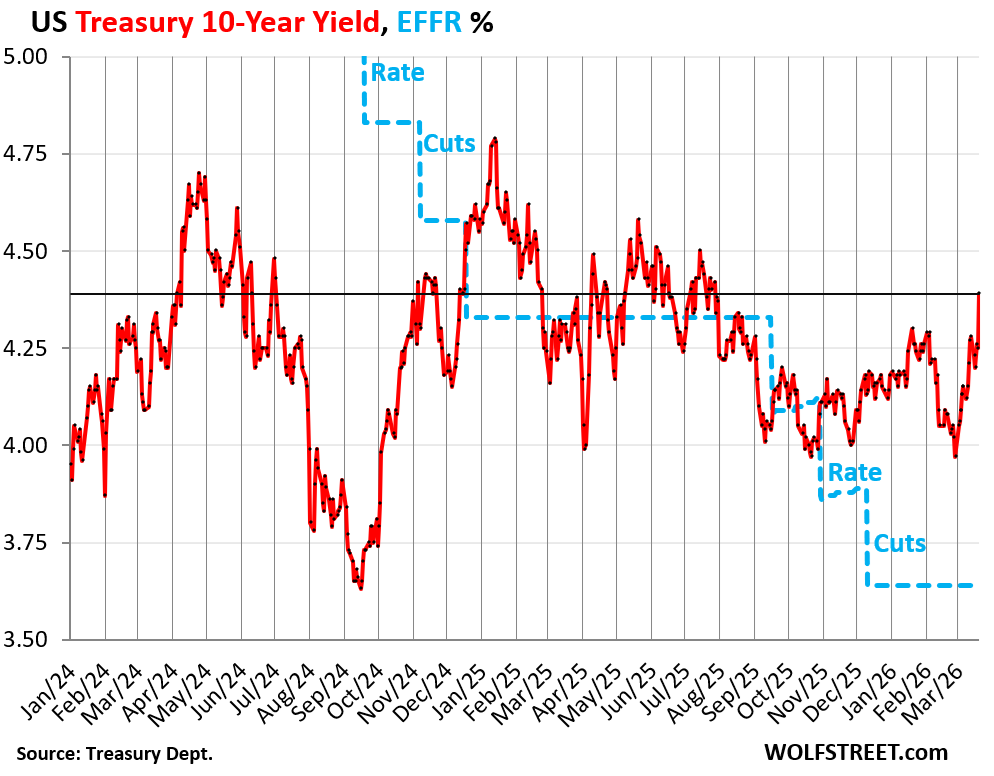

The 10-year Treasury yield spiked by 14 basis points to 4.39% today, the highest since July 2025. It has now spiked by 46 basis points since the low during the brutal flipflop over the weekend at the beginning of March, when the invasion of Iran kicked off, and the 10-year yield first plunged to 3.93% on the haven trade and then flipflopped into the inflation trade and spiked back to 4.07%, and the highly volatile dance then continued, and the yield has been zigzagging higher ever since.

Rising yields means bond prices are falling, and hedge funds are taking big losses on complex highly leveraged trades, such as the 2-year-10-year yield spread and swap spreads, according to Bloomberg, and their efforts to unwind those positions are now aggravating the bond sell-off and the spike in yields.

The Effective Federal Funds Rate (EFFR, blue line), which the Fed targets with its policy rates, shows the rate cuts that the 10-year yield has been blowing off.

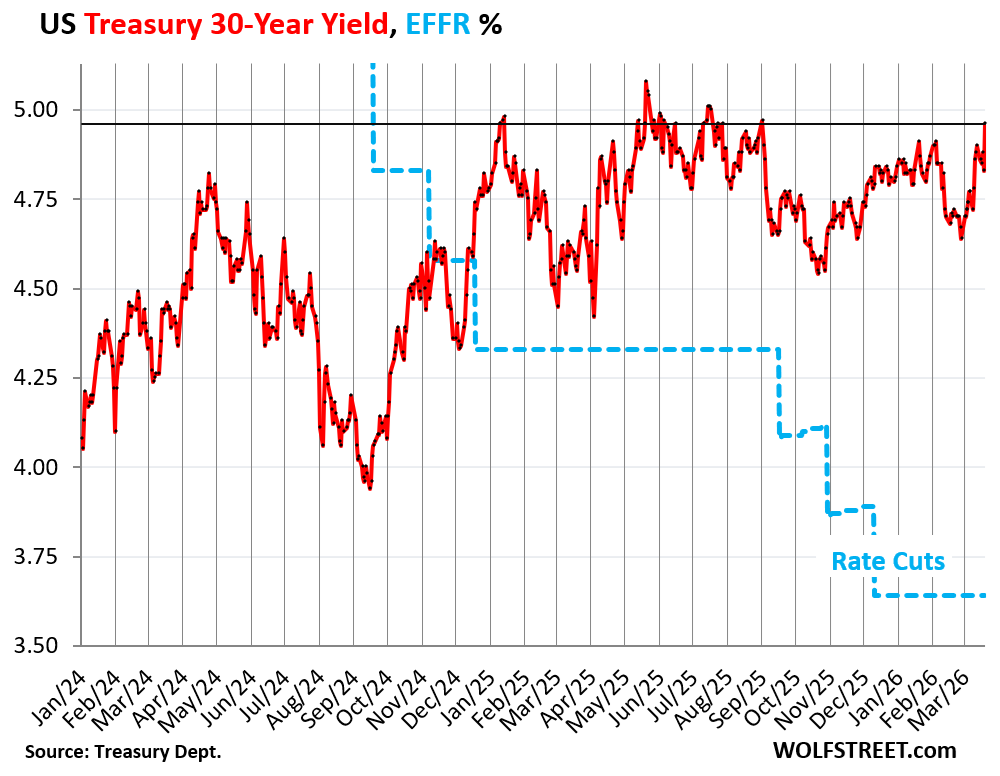

The 30-year Treasury yield spiked by 13 basis points to 4.96%, back where it had been in September, and just a hair from the 5%-line.

The 30-year yield has already been over 5% and near 5% several times in this cycle, initially in October 2023, when it rose as high as 5.1%. But at the time, the EFFR was 5.33%, the yield curve was massively inverted with all short-term yields substantially higher than longer-term yields.

What’s different now is that the Fed has cut its policy rates by 175 basis points starting in September 2024, and short-term yields have dropped by about that much, while the 30-year yield has largely remained within reach of the 5% line.

Why? Because the 30-year yield reacts to bond-market issues, such as expectations of future inflation – and those inflation fears are now getting rekindled – and expectations of supply of new bonds that investors have to absorb – and those expectations are getting boosted by the expected onslaught of borrowing by the government to fund the war in Iran. The US Treasury debt already went over $39 trillion, up by $2 trillion in 7.5 months.

30 years is a long time for inflation to go off the rails and for the onslaught of new supply to go haywire. Investors have to be enticed with higher yields to take those risks.

Inflation is spooking the bond market. The current inflation data (delayed by the government shutdown) predates the war in Iran and doesn’t yet reflect the spike in energy prices. Inflation accelerated last year and so far this year.

Consumer price inflation, as measured by the Fed-favored core PCE price index, accelerated to 3.1% in January driven by a spike in services inflation.

Inflation that producers face, as tracked by the Producer Price Index, jumped in February, after accelerating over the past six months and zigzagging higher since the low-point in 2023.

And the Price Index for Gross Domestic Purchases, which is part of the GDP data and reflects inflation adjustments in GDP except for imports, accelerated to 3.8% in Q4, the worst in three years. Now the energy price spike will come on top of that.

A lax Fed that keeps rates too low, or cuts rates, in face of accelerating inflation, spooks the bond market, and yields can surge in that environment. The bond market wants the Fed to crack down on inflation. And the bond market wants to believe that the Fed will crack down on inflation in the future any time inflation rears its ugly head.

Bonds lose purchasing power to inflation. And inflation is key to the bond market. The yield is supposed to compensate investors for inflation and for the risk of future inflation, and for other risks investors are taking. And that yield needs to be high enough in the eyes of those investors to compensate them for those risks as they see them.

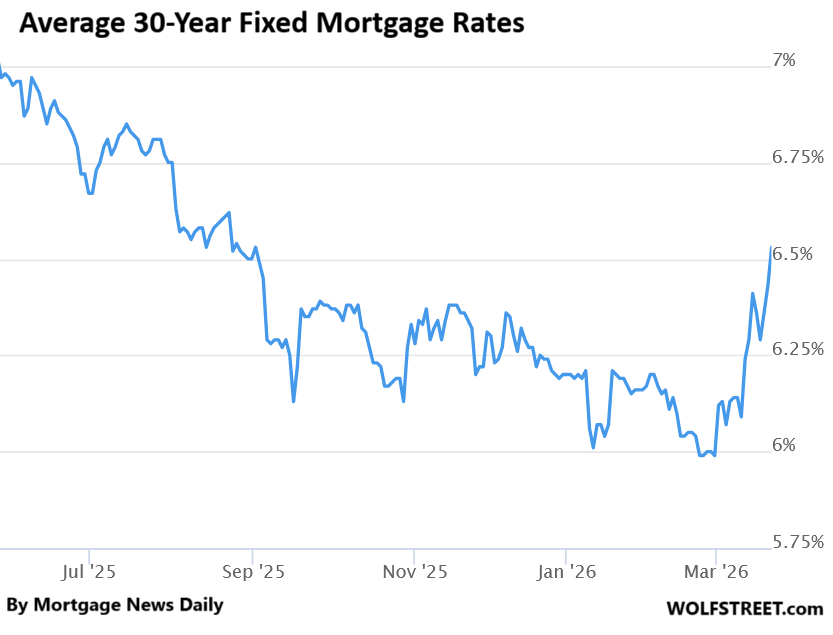

Travails in the bond market hit the mortgage market. The 30-year fixed mortgage rate tracks the 10-year Treasury yield, but is higher, and the spread between them varies. It is not particularly influenced by the Fed’s short-term policy rates.

The average 30-year fixed mortgage rate spiked to 6.53% today, according to Mortgage News Daily. Spring selling season is going to be tough. The disappointment is huge. Everyone had been counting on an average 30-year fixed mortgage rate that starts with a 5, and they’d already tasted it briefly at the end of February.

Over those two weeks since then, the average fixed mortgage rate spiked by over 50 basis points.

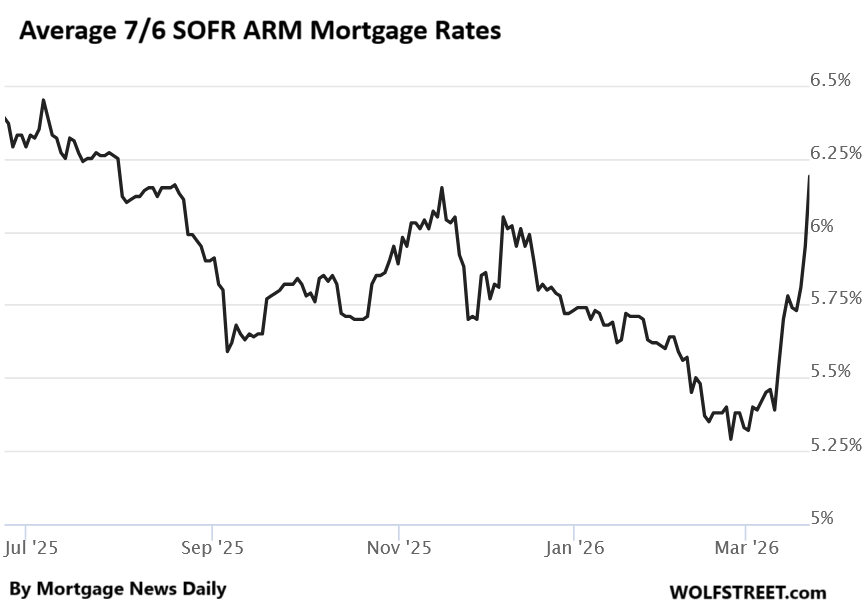

Adjustable mortgage rates have also spiked. The average ARM that is fixed for the first 7 years and then adjusts every 6 months based on SOFR (an average repo market rate) spiked to 6.19% today, the highest since August.

Over the past two weeks, it has spiked by 80 basis points.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

This is about to get interesting. What are the chances we see Fed funds hike in the next 6 months?

50/50 IMHO but it will all depend on a high inflation number so it will be pretty awful before they raise it if we are losing lots of jobs at the same time

Zero! If bond yield rises and stays above 5%, there will be immense pressure on FOMC from the most powerful POTUS in history to lower the rates and to buy more t-bonds when they roll over MBS runoff. Also, it is a myth that US has an independent central bank. Also, the job market is bleak for the graduating class this year. Dollar remains strong during the war and that helps the FOMC to brush off the oil price increase as “one time” event. One or two more rate cuts are highly likely before the elections. Someday, the bond vigilantes will wake up, but not anytime soon! Also, many long-term liability managers find 5% very attractive!

“If bond yield rises and stays above 5%, there will be immense pressure on FOMC…to buy more t-bonds when they roll over MBS runoff.”

What pressure? They’ve already said this is exactly what they’re doing. Sooo…they’re going to be pressured to do what they are going to do anyway? Seems like wasted effort.

And I doubt there’s anything magic about 5%. If PCE keeps climbing and threatens to pull a 4-handle then I don’t think there are going to be a lot of takers for 5% paper with fixed coupons for 30 years. “Yield Solves All Demand Problems.” I think I read that somewhere.

Bala wake up and sniff some coffee.

You need to re awaken your senses.

☕️

I would not want to be Warsh.

Me go Shoppy for Bondy

Nice to see that some aspect of the market is paying attention to inflation. Hopefully the Fed will wake up soon!

A 5% discount rate applied to long duration assets like technology stocks doesn’t seem to be an issue so far.

Unsure whether that lasts