Bond market frets about inflation, leveraged Treasury bets unwind, housing market frets about spring selling season.

By Wolf Richter for WOLF STREET.

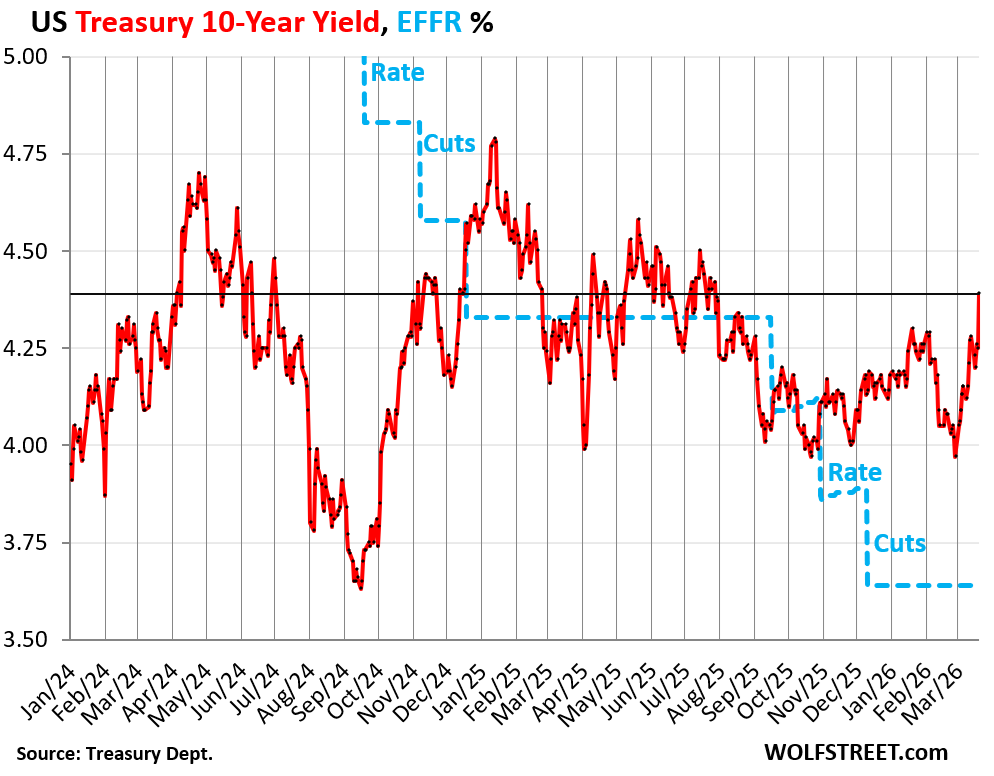

The 10-year Treasury yield spiked by 14 basis points to 4.39% today, the highest since July 2025. It has now spiked by 46 basis points since the low during the brutal flipflop over the weekend at the beginning of March, when the invasion of Iran kicked off, and the 10-year yield first plunged to 3.93% on the haven trade and then flipflopped into the inflation trade and spiked back to 4.07%, and the highly volatile dance then continued, and the yield has been zigzagging higher ever since.

Rising yields means bond prices are falling, and hedge funds are taking big losses on complex highly leveraged trades, such as the 2-year-10-year yield spread and swap spreads, according to Bloomberg, and their efforts to unwind those positions are now aggravating the bond sell-off and the spike in yields.

The Effective Federal Funds Rate (EFFR, blue line), which the Fed targets with its policy rates, shows the rate cuts that the 10-year yield has been blowing off.

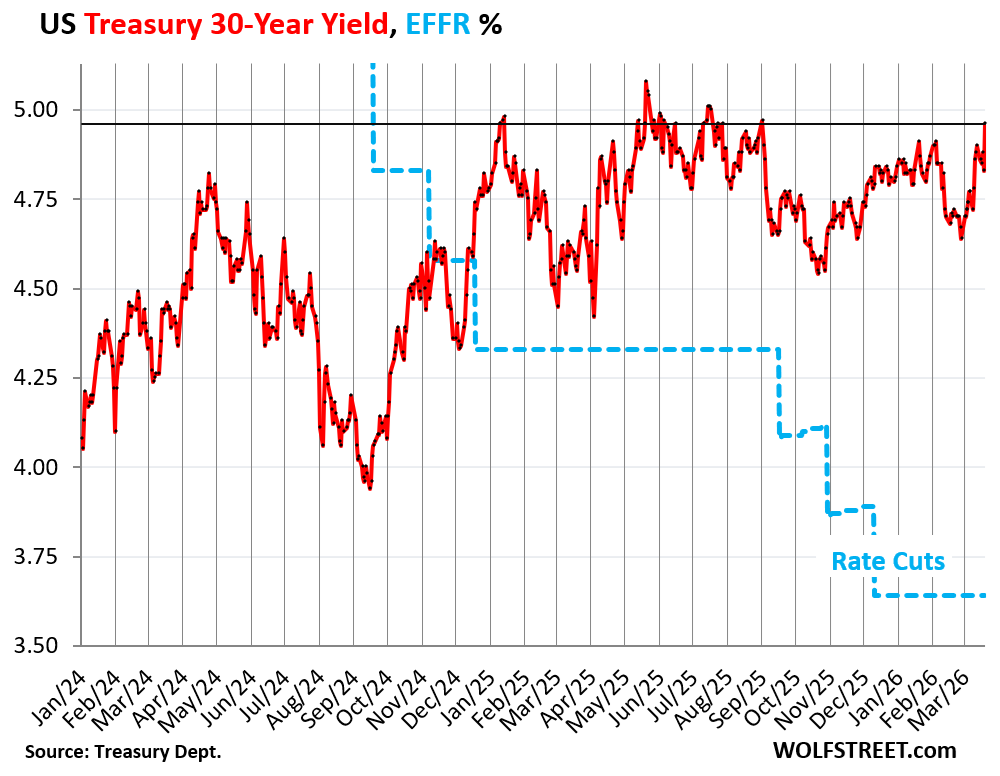

The 30-year Treasury yield spiked by 13 basis points to 4.96%, back where it had been in September, and just a hair from the 5%-line.

The 30-year yield has already been over 5% and near 5% several times in this cycle, initially in October 2023, when it rose as high as 5.1%. But at the time, the EFFR was 5.33%, the yield curve was massively inverted with all short-term yields substantially higher than longer-term yields.

What’s different now is that the Fed has cut its policy rates by 175 basis points starting in September 2024, and short-term yields have dropped by about that much, while the 30-year yield has largely remained within reach of the 5% line.

Why? Because the 30-year yield reacts to bond-market issues, such as expectations of future inflation – and those inflation fears are now getting rekindled – and expectations of supply of new bonds that investors have to absorb – and those expectations are getting boosted by the expected onslaught of borrowing by the government to fund the war in Iran. The US Treasury debt already went over $39 trillion, up by $2 trillion in 7.5 months.

30 years is a long time for inflation to go off the rails and for the onslaught of new supply to go haywire. Investors have to be enticed with higher yields to take those risks.

Inflation is spooking the bond market. The current inflation data (delayed by the government shutdown) predates the war in Iran and doesn’t yet reflect the spike in energy prices. Inflation accelerated last year and so far this year.

Consumer price inflation, as measured by the Fed-favored core PCE price index, accelerated to 3.1% in January driven by a spike in services inflation.

Inflation that producers face, as tracked by the Producer Price Index, jumped in February, after accelerating over the past six months and zigzagging higher since the low-point in 2023.

And the Price Index for Gross Domestic Purchases, which is part of the GDP data and reflects inflation adjustments in GDP except for imports, accelerated to 3.8% in Q4, the worst in three years. Now the energy price spike will come on top of that.

A lax Fed that keeps rates too low, or cuts rates, in face of accelerating inflation, spooks the bond market, and yields can surge in that environment. The bond market wants the Fed to crack down on inflation. And the bond market wants to believe that the Fed will crack down on inflation in the future any time inflation rears its ugly head.

Bonds lose purchasing power to inflation. And inflation is key to the bond market. The yield is supposed to compensate investors for inflation and for the risk of future inflation, and for other risks investors are taking. And that yield needs to be high enough in the eyes of those investors to compensate them for those risks as they see them.

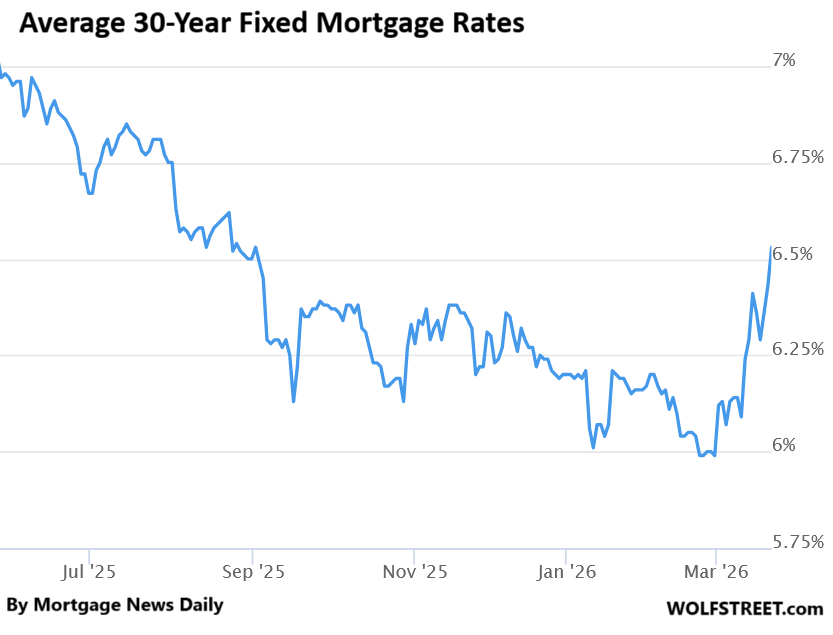

Travails in the bond market hit the mortgage market. The 30-year fixed mortgage rate tracks the 10-year Treasury yield, but is higher, and the spread between them varies. It is not particularly influenced by the Fed’s short-term policy rates.

The average 30-year fixed mortgage rate spiked to 6.53% today, according to Mortgage News Daily. Spring selling season is going to be tough. The disappointment is huge. Everyone had been counting on an average 30-year fixed mortgage rate that starts with a 5, and they’d already tasted it briefly at the end of February.

Over those two weeks since then, the average fixed mortgage rate spiked by over 50 basis points.

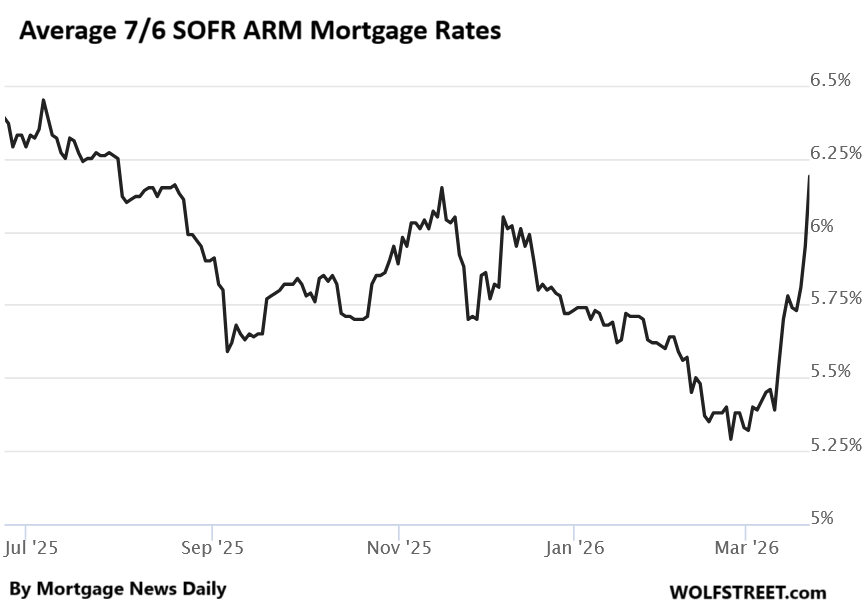

Adjustable mortgage rates have also spiked. The average ARM that is fixed for the first 7 years and then adjusts every 6 months based on SOFR (an average repo market rate) spiked to 6.19% today, the highest since August.

Over the past two weeks, it has spiked by 80 basis points.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

This is about to get interesting. What are the chances we see Fed funds hike in the next 6 months?

50/50 IMHO but it will all depend on a high inflation number so it will be pretty awful before they raise it if we are losing lots of jobs at the same time

Zero! If bond yield rises and stays above 5%, there will be immense pressure on FOMC from the most powerful POTUS in history to lower the rates and to buy more t-bonds when they roll over MBS runoff. Also, it is a myth that US has an independent central bank. Also, the job market is bleak for the graduating class this year. Dollar remains strong during the war and that helps the FOMC to brush off the oil price increase as “one time” event. One or two more rate cuts are highly likely before the elections. Someday, the bond vigilantes will wake up, but not anytime soon! Also, many long-term liability managers find 5% very attractive!

“If bond yield rises and stays above 5%, there will be immense pressure on FOMC…to buy more t-bonds when they roll over MBS runoff.”

What pressure? They’ve already said this is exactly what they’re doing. Sooo…they’re going to be pressured to do what they are going to do anyway? Seems like wasted effort.

And I doubt there’s anything magic about 5%. If PCE keeps climbing and threatens to pull a 4-handle then I don’t think there are going to be a lot of takers for 5% paper with fixed coupons for 30 years. “Yield Solves All Demand Problems.” I think I read that somewhere.

Bala wake up and sniff some coffee.

You need to re awaken your senses.

☕️

6 months may be too short of a time horizon.

Howse about the odds of a hike as between zero and none. The restraint of the Fed should not be interpreted as an abandonment of monetary stimulus whose status the Treasury department claims is not inflationary but necessary

Well, the 1yr T-bills went from 3.4% to 3.8% so maybe someone thinks it’s starting to be possible

Futures market says 6% chance. And an equally small chance of a rate hike.

In a year and a half the futures market sees a small chance of a modest rate cut.

The federal funds futures market is nearly always wrong except shortly before the Fed meeting. This is my favorite chart:

So the market expected the fed to raise constantly between 2009 and 2016? Seems like that flat red line between those dates was when the FED stopped doing their job and started their MMT experiment. It would be nice if some ivy league educated reporter would ask Powell about this. Instead he just stands there and blames one time events or shocks for his problems, and takes almost zero institutional responsibility for the current mess the FED enabled and created. The hubris is disgusting, even in his soft grandpa speak.

Yellen was in charge between 2014 and 2018, not Powell, and before her, Bernanke was in charge. They presided over the flat line. Yellen started raising rates in Dec 2015 through 2017 and started QT in late 2017. Powell took over in Feb 2018, hiked rates further and continued QT, and attracted the ire of Trump.

Yeah, it is a conventional wisdom machine: it can only tell you what the people buying futures think, which is often just an extension of the status quo. There’s no secret knowledge there.

I’ve never seen that graph before.

Not surprised in the least.

I agree. long-term rate projections outside of obvious upside / downside economic conditions is near impossible.

Great graph-

And while yes- you can’t blame Powell for Yellen and Bernanke – he is the face of the institution that screwed up big time. That institution that won’t accept any responsibility or accountability. Just a bunch of finger pointing at the other guy and the “one time shocks”

So while you point out that the market was wrong in guessing what the FED would do during that period from 2010 thru 2016- I could also argue that the MARKET was RIGHT in what should have been done, and the FED was wrong.

Appreciate the site and the graph. I’m done ranting, but gosh this one really “triggered” me. LOL. Maybe I’m reading it all wrong. Whatever but thanks.

Then you’ll really be astonished at Powell receiving the Volcker award, and especially his comments about Paul doing the right thing.

I would not want to be Warsh.

Me go Shoppy for Bondy

Nice to see that some aspect of the market is paying attention to inflation. Hopefully the Fed will wake up soon!

A 5% discount rate applied to long duration assets like technology stocks doesn’t seem to be an issue so far.

Unsure whether that lasts

Mortgage rates aren’t gonna get any better, and even if they do to some extent, the housing market is toast. Higher mortgage rates would be everyone’s greatest friend! An equalizer.

A neutralizer; a cleansing mechanism!

I’m not so convinced. Maybe we’ll see an equalizer for some markets, but I see elevated mortgage rates as more generally accelerating the accumulation of assets by the highest wealth brackets. Anyone buying with cash is unaffected by mortgage rates, and will benefit the most from a soft market of sellers lowering prices to battle rising mortgage costs.

Housing market is long due for price correction and is driven by affordability.

Home prices have already come down by 25 percent from peak from some of the hottest market

More to come I guess unless mortgage go down to 3 to 4 percent

When you buy RE using Cash, you are comparing what you can earn from the property to what you can earn in an essentially entirely liquid MMF – 3.25-3.5%.

Most rental properties, at current prices and no debt can yield 3-4% net and much of that can be sheltered from immediate taxation although depreciation recapture at sale can bite you.

Unless prices drop, investment real estate look less attractive vs TBills even for all cash buyers.

You’re ignoring the long term appreciation that many buyers expect (and historically, has happened with enough holding time).

Re: recapture, a bitch for sure, irrelevant if never sold, or 1031 lets you roll into the next property, deferring recapture.

Just a comment that the ‘official’ rates listed here are not available to retail investors. I looked real-time at government bonds at both fidelity and vanguard today and it did not hit these rates for the retail secondary market. Sure the dealers get their spread and I’m moving modest amounts compared to banks and hedge funds, so I wonder what the typical difference is for individual bond investor in the secondary market versus the headline rates? Does Treasury Direct provide the same rate to the small guy?

Buying bonds in the secondary market is very different from buying them at auction:

1. You cannot buy in the secondary market through your broker a “10-year yield.” What you can buy are securities with roughly 10 years left to run before they mature. That could include a 10-year note issued six months ago with 9.5 years left to run, or a 30-year bond issued 19 years ago with 11 years left to run, or something similar. So if you’re interested in a 30-year yield, you will have to look for a 30-year bond that was recently issued, and there might be some available, such as a 30-year bond that was issued six months ago with 29.5 years left to run.

2. I just checked at my broker. The top offering (lowest price): $245 million of 10-year notes of the same CUSIP, with a coupon of 4.125%, issued Feb 17, 2026. It sold at auction in mid-February at a yield of 4.177% (at a discounted price of $99.57 per $100). At my broker, the highest ask yield (lowest price) for this CUSIP is 4.379%. So if you accept that yield, you can buy it at that price. So that’s 1 basis point off the average market yield at the moment of the close on Friday (4.387%). But on Friday, there was huge fluctuation in the yield, and for most of Friday, the yield was lower than 4.387%.

3. The highest bid for this CUSIP at my broker is 4.382%. So bid and ask are 0.3 basis points apart, which is almost nothing, and both are just a hair below the closing average on Friday.

But this is a Saturday, and there is no bond trading. So when you look on Monday, it will all have changed, based on market yields on Monday, which will be different than Friday, and probably lower.

So I don’t know what you’re looking at, but at my broker, I can buy a recently issued 10-year note within a hair of the market yield.

The vanguard long term Treasury ETF (like all ETFs) reports a 30 day average yield, which was 4.83 on Friday. This is pretty darn close to the 30 day average for the 30 year Treasury.

Ishares has a 7-10 year Treasury ETF that has a 30 day average of 3.95%, a little below the average of the 7 and 10 year yields over the last 30 days.

As Wolf notes, there are important differences between buying individual bonds and holding them to maturity (you know exactly how much money you get over the entire maturity period) vs a bond fund (where they are constantly buying and selling bonds to match the current market/yields), so this might not be what you want, but you can get it.

Whats the average duration in the ETF ?

Vanguard has two low expense ratio long duration ETFs.

VGLT is regular treasuries. It’s typical duration is 14 years.

EDV has a typical duration of 24 and is only treasury STRIPS.

Classical long duration ETF is is iShares TLT with very rich options. Duration is 15, but expense ratio high at 0.15.

Some points. STRIPS and TIPS should really only be in retirement accounts because of tax laws.

Also, as low coupon bonds from the ZIRP era are replaced by more recent bonds with higher coupons in these ETFs, their duration will naturally drop.

Fun fact, duration on a par bond can NEVER exceed 100 divided by coupon rate, no matter the term of the bond. Thus, a 5% bond with a 30 year, 50 year or a 1000 year term can never have duration more that 20. Thus, century bonds are not as dangerous as they seem if coupons are high enough.

The unsustainable US debt and the foreign loss of confidence in the $ will inevitably lead to higher cost US debt. Why would China or any nation in its right mind purchase US debt at interest rates below 5%? Trump may try to lower interest rates but the market will decide

Great points, but there is no alternative to the current US-dollar-backed financial system.

Someone, please tell me if I am wrong.

… I guess we’ll find out

Bitcoin.

*ducks shoe*

I will see myself out

You are 100% correct right now. Unfortunately this is one of those things where you are tight until you are not.

Right now there is not a viable alternative to a dollar backed financial system. However, the things that would allow an alternative to come into existence will also allow it to grow rapidly and negate a dollar backed financial system.

There is a huge network effect involved here. Momentum keeps things going until it doesn’t.

The current GDP growth rate for St. Louis is 2.05% as of March 2026

If Wash gets his way and the Fed further reduces its balance sheet, should we expect yields on bonds with maturities over a year to rise more?

Inflation likely to spike for all the expected reasons(war, energy costs, greedflation, supply chain interruptions, etc.) but guessing the Fed will keep interest rates where they are at and not raise them. The whole transitory rationale again and I suppose given enough of a time horizon everything is transitory. Don’t give a loaded gun to somebody that doesn’t know how to use it or may shoot themselves in the foot. Wouldn’t be so bad but when you shoot 300 million then much worse.

Wolf, to what degree will the FED look at energy induced inflation and attribute it to supply shock and discount it as requiring higher rates ?

Do they even make such distinctions ?

They will “look through” energy price spikes by focusing on core inflation measures that do not include the direct energy costs, such as the core PCE price index, but it already accelerated to 3.1% prior to the energy issues. With a lag, higher energy prices filter into non-energy products and services, and that’s about when the Fed gets very leery of looking through that. That’s a lesson it learned in the 1970s.

So keep your eyes on core PCE price index and core services PCE and also core services PCE without housing. The Fed will be talking about them.

“Your access to this site has been limited by the site owner”

What the fuck site owner?

quit using a gangster VPN that does business with hackers and spammers and then recycles those IP addresses to its regular users. The VPN you’re using (you know who it is, and I know who it is) is among the worst in terms of assigning IP addresses to hackers and spammers that attack my site. When my site gets attacked by a hacker or spammer, my firewall blocks that IP address from accessing my site, and when the VPN recycles the IP address to you, you get blocked. Seems you know exactly what is going on, which is why you switched IP addresses to post this comment.

Good job of digging.

Dear Host,

I am in the market for a VPN provider. Would you be kind enough to warn those like me directly or by “hint” whom to avoid?

Thank you, –Geezer

I’d rather not say. But never use a foreign-based VPN. Use a reputable US-based VPN. I’ve used Firefox VPN without problems. And I have never seen it crop up in my firewall. But there are no guarantees. There are other reputable US VPNs.

Having VPN is the most scary thing for me. For sure avoid 100% free VPNs. Their business model is just to steal from you. But still I don’t want to pay anyone to still anyway. Going with US provider seems safer.

I spent years working on internet security. I could be paranoid.

Probably there are safe providers, but will they be in the future?

VPNs are opaque, some are open source, most not. I don’t want to expand my circle of trust to some third-party companies.

VPNs have virtually all the access to your system.

Similarly, I only trust Apple, and to some extent google. I use Apple keychain, I would not trust e.g. 1Password. They might have good intentions but there are bugs and foreign attacks.

Just my 2 cents, again I could be too paranoid.

Another way of looking at this. If you are young and poor, you have nothing much to lose. You want to access some services for free (geolocation, free WiFi etc), browsing flexibility/opacity etc that e.g. VPNs provide.

But if you are at the stage where protection of your nuts is most important, you should rather say good bye to the flexibility.

I know that this is a contradiction to what the media are saying: if you want to be safe, use VPN. There are other means to keep you more secure, but the weakest link is a person and his internet behaviour.

Which VPN is that? I use VPNs for some browsing, but not sites I trust, like this one.

I’d rather not say. But never use a foreign-based VPN. Use a reputable US-based VPN.

I read an article the other day that exemplifies what’s wrong with the post 2009 mindset. It was titled “Could the stock market really have a down year in 2026?”

It’s incredible to me that people feel that 10-20% gains, year after year, are sustainable and expected. There’s going to be a lot of pain someday, I just don’t know when.

Yeah…

But until then people are racking in the coin… with a long time proven track record of profit….

People are playing the game hoping not to get burnt….or worse yet, not knowing that they can get burnt.

There are a lot of people that don’t study history, or don’t have the advantage of being old enough to remember that at some point in time there could or will be pain of some flavor.

Until then…Party on Garth, Party on Wayne.!!

Live on the edge !!

It is entirely possible that a lot of foreign investors look elsewhere this year to park their money. That would be a serious drag on stocks. Also, consumer spending dropping due to increases in almost all fixed costs would curtail retail investment. A lot of headwinds this year in addition to the own goal by this administration of kicking an Iranian hornets nest with no beekeeper suit on. Who knows, but common sense would indicate this year may not be as good as previous few. However, if you have a long time investing horizon you might as well keep DCA’ing.

Iran has cracked the Iron Dome. Nearly 100 injured in Israel’s nuclear city.

Irin IS controlling Hormuz.

Warflation is “transitory””

Stocks are getting ready to rumble.

Tbill and chill looks better than ever.

This is not your typical ME skirmish.

Transitory being sarcastic